Society of Grownups Circles—Curriculum

15

You’re a Grownup (Don’t Panic) The Basics of Financial Planning

-

Upload

society-of-grownups -

Category

Education

-

view

163 -

download

0

Transcript of Society of Grownups Circles—Curriculum

You’re a Grownup (Don’t Panic)

The Basics of Financial Planning

© SOCIETY OF GROWNUPS02 | YOU’RE A GROWNUP (DON’T PANIC)

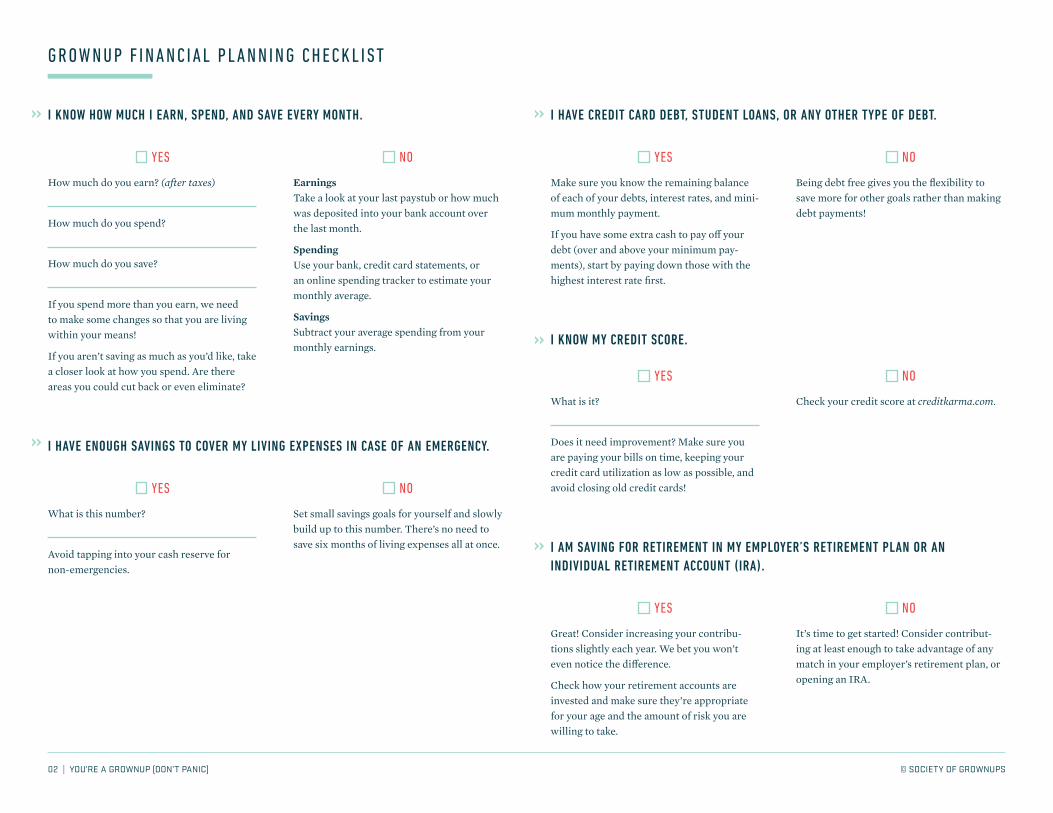

I KNOW HOW MUCH I EARN, SPEND, AND SAVE EVERY MONTH.

YES

How much do you earn? (after taxes)

How much do you spend?

How much do you save?

If you spend more than you earn, we need to make some changes so that you are living within your means!

If you aren’t saving as much as you’d like, take a closer look at how you spend. Are there areas you could cut back or even eliminate?

NO

Earnings Take a look at your last paystub or how much was deposited into your bank account over the last month.

Spending Use your bank, credit card statements, or an online spending tracker to estimate your monthly average.

Savings Subtract your average spending from your monthly earnings.

I HAVE ENOUGH SAVINGS TO COVER MY LIVING EXPENSES IN CASE OF AN EMERGENCY.

YES

What is this number?

Avoid tapping into your cash reserve for non-emergencies.

NO

Set small savings goals for yourself and slowly build up to this number. There’s no need to save six months of living expenses all at once.

››

››

››

I HAVE CREDIT CARD DEBT, STUDENT LOANS, OR ANY OTHER TYPE OF DEBT.

YES

Make sure you know the remaining balance of each of your debts, interest rates, and mini-mum monthly payment.

If you have some extra cash to pay off your debt (over and above your minimum pay-ments), start by paying down those with the highest interest rate first.

NO

Being debt free gives you the flexibility to save more for other goals rather than making debt payments!

I KNOW MY CREDIT SCORE.

YES

What is it?

Does it need improvement? Make sure you are paying your bills on time, keeping your credit card utilization as low as possible, and avoid closing old credit cards!

NO

Check your credit score at creditkarma.com.

I AM SAVING FOR RETIREMENT IN MY EMPLOYER’S RETIREMENT PLAN OR AN INDIVIDUAL RETIREMENT ACCOUNT (IRA).

YES

Great! Consider increasing your contribu-tions slightly each year. We bet you won’t even notice the difference.

Check how your retirement accounts are invested and make sure they’re appropriate for your age and the amount of risk you are willing to take.

NO

It’s time to get started! Consider contribut-ing at least enough to take advantage of any match in your employer’s retirement plan, or opening an IRA.

››

››

G R OW N U P F I N A N C I A L P L A N N I N G C H E C K L I ST

© SOCIETY OF GROWNUPS

TO P 3 F I N A N C I A L G OA L S

1

2

3

WHAT WAS THE LAST BIG FINANCIAL DECISION YOU MADE?

WHAT WAS THE LAST PURCHASE YOU MADE THAT MADE YOU FEEL GREAT?

WHAT WAS THE LAST PURCHASE YOU MADE THAT YOU REGRETTED?

YO U R VA LU E S

VALUE

VALUE

VALUE

VALUE

VALUE

03 | YOU’RE A GROWNUP (DON’T PANIC)

© SOCIETY OF GROWNUPS04 | YOU’RE A GROWNUP (DON’T PANIC)

PICK ONE VALUE TO THINK ABOUT FOR A WEEKChoose one value each week. Spend the week becoming familiar with that value. What does it mean to you? How does it affect your actions and financial decisions each day?

DO THE EXERCISE WITH YOUR PARTNERDo the values exercise with your partner. Have a conversation about the similarities and differences in your values, what they mean to you, and how you would both like to integrate them into your everyday lives.

DEFINE ONE SMALL ACTION FOR EACH VALUEPick something that’s simple and easy to do, but choose one bite-size action for each of your values and promise yourself to follow through on those actions within one week.

CHECK YOUR VALUES AGAINYour values may change over time as your life changes and your priorities become clearer. That’s OK! Revisit your values regularly, and don’t be afraid to change your financial plan based on your new values.

TA K E AC T I O N

Any third-party resources or websites referenced above are not under our control. We cannot guarantee and are not responsible for the accuracy of the resources, websites, or any products or services available through such resources or websites. While we hope the information in these materials are useful, it’s only intended to provide general education. It’s not legal, tax, or investment advice, and may not apply or be useful to your specific financial situation. If you need recommendations geared to your personal financial situation, schedule time with a financial planner.

Spending Plans: A Better Way To Budget

Spending on the Things You Care About

© SOCIETY OF GROWNUPS02 | SPENDING PLANS: A BETTER WAY TO BUDGET

W H AT A R E YO U R P R I O R I T I E S ? W H AT A R E YO U WO R K I N G W I T H ?

H OW D O YO U S P E N D ?

W H AT W I L L YO U S P E N D O N ?

SMALL STUFF

NEEDS

WANTS

PRIORITIES

TOTAL AVAILABLE CASH

WHAT DO YOU SPEND ON?

BIG STUFF HOW LONG IT NEEDS TO LAST

HOW MUCH? (ESTIMATE)

© SOCIETY OF GROWNUPS03 | SPENDING PLANS

Any third-party resources or websites referenced above are not under our control. We cannot guarantee and are not responsible for the accuracy of the resources, websites, or any products or services available through such resources or websites. While we hope the information in these materials are useful, it’s only intended to provide general education. It’s not legal, tax, or investment advice, and may not apply or be useful to your specific financial situation. If you need recommendations geared to your personal financial situation, schedule time with a financial planner.

THE GROWNUP BLOG - BUDGETINGsocietyofgrownups.com/blog/topic/budgeting Read more about how to put together Grownup spending and savings plans.

LEVEL MONEYlevelmoney.com This app will help you track your spending and show you how much fun money you have left for the day, week, and month.

MINTmint.com This tracker gives you lots of detail on your spending habits.

R E C O M M E N D E D R E S O U R C E ST I P S TO K E E P S P E N D I N G I N C H E C K

1. Be mindful, not mindless. If you feel the urge to make a purchase in the moment, distract yourself immediately and do something unrelated.

2. Be aware of decision points and external controls. Create an allowance for daily purchases, like coffee. It will allow you to consider, reflect, and make a decision about how important is this coffee today.

3. Get some help from your friends. Having a partner to help keep you accountable can be helpful. Someome to praise you, but also kick you in the ass when you need it, might just be enough to help you stay on the right track.

4. Make a wish list. This goes for everything from grocery shopping to new clothes. Have a game plan in place before you start buying to avoid impulse or emotional purchases.

5. Factor small indulgences into your spending plan. This can help you from splurg-ing and getting off track! Get that manicure once a month or spring for the nice six pack of craft beer.

6. Use credit cards wisely. Be honest with yourself. Will having access to a credit card just be unnecessary temptation for you to overspend? If so, skip it. But if you feel comfortable having one, charge a small amount and pay it off in full every month. This can help you build a great credit history.

Loans & Groans

A Student Debt Workshop

© SOCIETY OF GROWNUPS02 | LOANS & GROANS

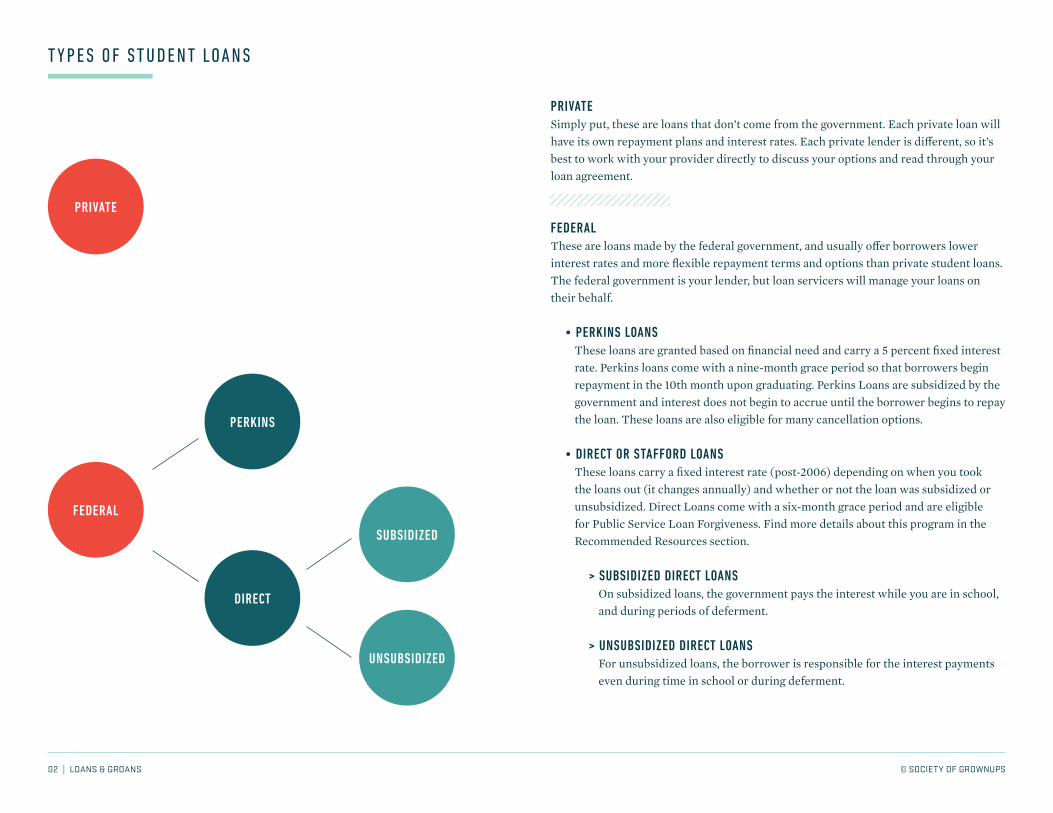

T Y P E S O F ST U D E N T LOA N S

PRIVATESimply put, these are loans that don’t come from the government. Each private loan will have its own repayment plans and interest rates. Each private lender is different, so it’s best to work with your provider directly to discuss your options and read through your loan agreement.

FEDERALThese are loans made by the federal government, and usually offer borrowers lower interest rates and more flexible repayment terms and options than private student loans. The federal government is your lender, but loan servicers will manage your loans on their behalf.

• PERKINS LOANSThese loans are granted based on financial need and carry a 5 percent fixed interest rate. Perkins loans come with a nine-month grace period so that borrowers begin repayment in the 10th month upon graduating. Perkins Loans are subsidized by the government and interest does not begin to accrue until the borrower begins to repay the loan. These loans are also eligible for many cancellation options.

• DIRECT OR STAFFORD LOANSThese loans carry a fixed interest rate (post-2006) depending on when you took the loans out (it changes annually) and whether or not the loan was subsidized or unsubsidized. Direct Loans come with a six-month grace period and are eligible for Public Service Loan Forgiveness. Find more details about this program in the Recommended Resources section.

> SUBSIDIZED DIRECT LOANSOn subsidized loans, the government pays the interest while you are in school, and during periods of deferment.

> UNSUBSIDIZED DIRECT LOANSFor unsubsidized loans, the borrower is responsible for the interest payments even during time in school or during deferment.

PRIVATE

FEDERAL

PERKINS

DIRECT

SUBSIDIZED

UNSUBSIDIZED

© SOCIETY OF GROWNUPS03 | LOANS & GROANS

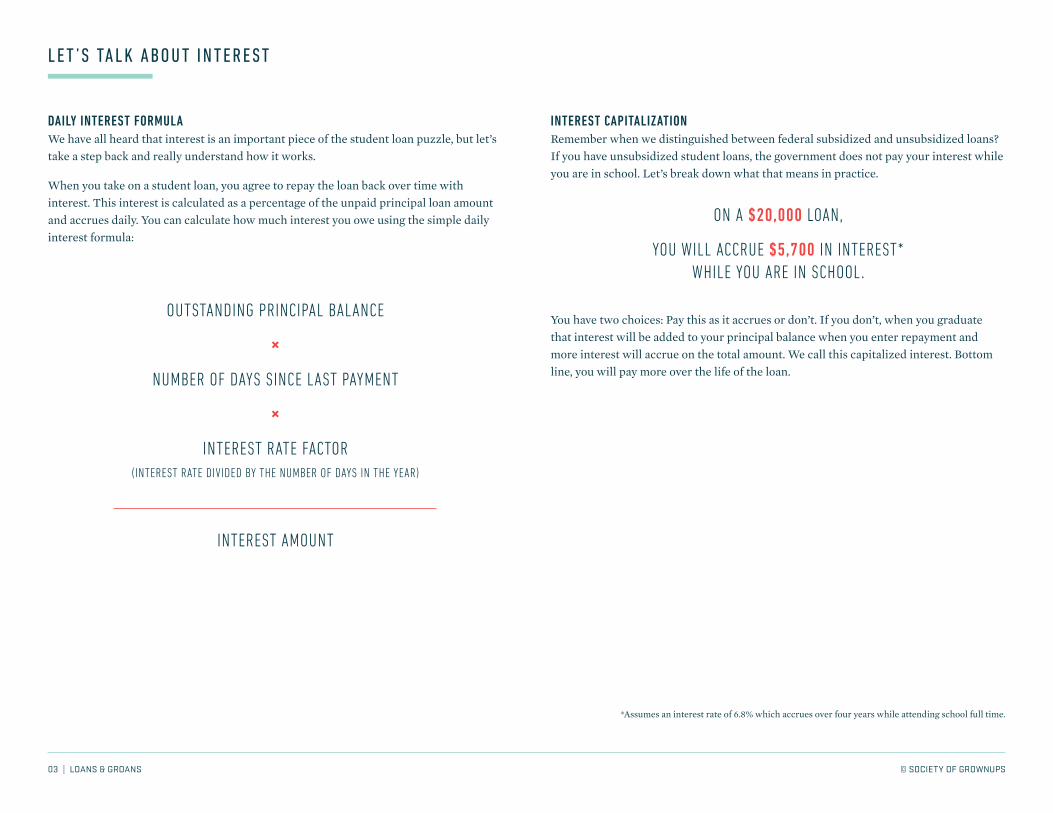

L E T ’ S TA L K A B O U T I N T E R E ST

DAILY INTEREST FORMULAWe have all heard that interest is an important piece of the student loan puzzle, but let’s take a step back and really understand how it works.

When you take on a student loan, you agree to repay the loan back over time with interest. This interest is calculated as a percentage of the unpaid principal loan amount and accrues daily. You can calculate how much interest you owe using the simple daily interest formula:

INTEREST CAPITALIZATION Remember when we distinguished between federal subsidized and unsubsidized loans? If you have unsubsidized student loans, the government does not pay your interest while you are in school. Let’s break down what that means in practice.

You have two choices: Pay this as it accrues or don’t. If you don’t, when you graduate that interest will be added to your principal balance when you enter repayment and more interest will accrue on the total amount. We call this capitalized interest. Bottom line, you will pay more over the life of the loan.

OUTSTANDING PRINCIPAL BALANCE

×

NUMBER OF DAYS SINCE LAST PAYMENT

×

INTEREST RATE FACTOR (INTEREST RATE DIVIDED BY THE NUMBER OF DAYS IN THE YEAR)

INTEREST AMOUNT

ON A $20,000 LOAN,

YOU WILL ACCRUE $5,700 IN INTEREST* WHILE YOU ARE IN SCHOOL.

*Assumes an interest rate of 6.8% which accrues over four years while attending school full time.

© SOCIETY OF GROWNUPS04 | LOANS & GROANS

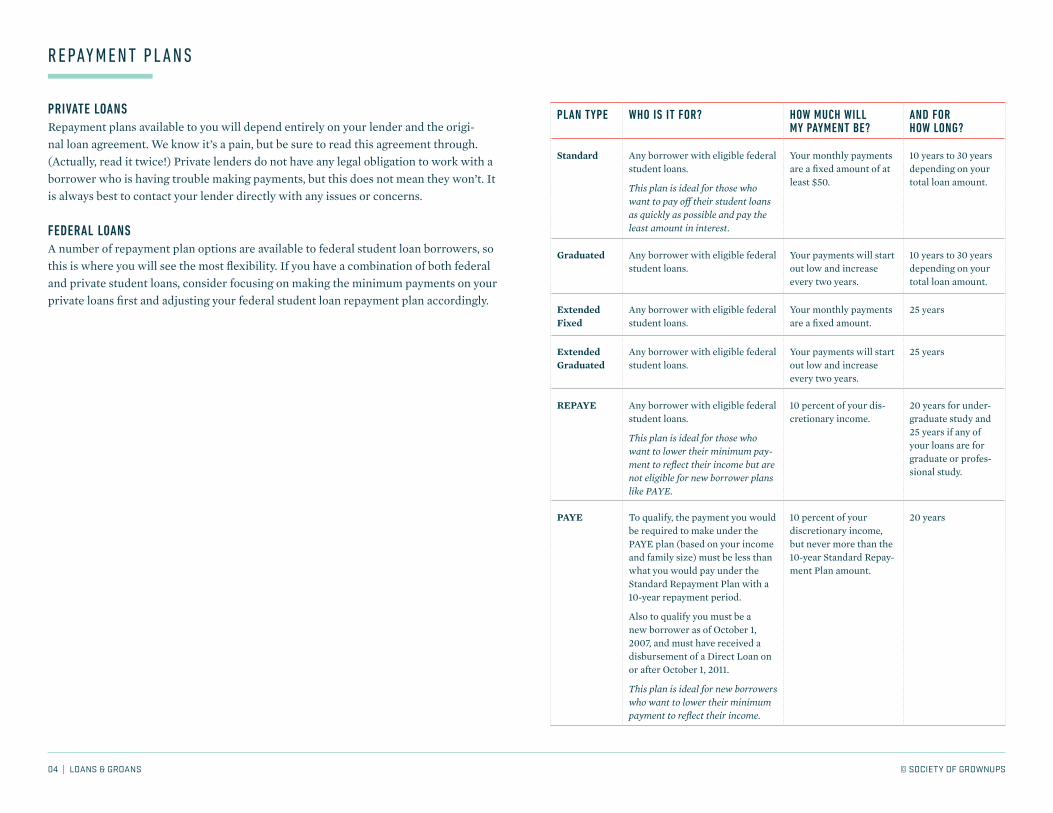

R E PAY M E N T P L A N S

PRIVATE LOANSRepayment plans available to you will depend entirely on your lender and the origi-nal loan agreement. We know it’s a pain, but be sure to read this agreement through. (Actually, read it twice!) Private lenders do not have any legal obligation to work with a borrower who is having trouble making payments, but this does not mean they won’t. It is always best to contact your lender directly with any issues or concerns.

FEDERAL LOANSA number of repayment plan options are available to federal student loan borrowers, so this is where you will see the most flexibility. If you have a combination of both federal and private student loans, consider focusing on making the minimum payments on your private loans first and adjusting your federal student loan repayment plan accordingly.

PLAN TYPE WHO IS IT FOR? HOW MUCH WILL MY PAYMENT BE?

AND FOR HOW LONG?

Standard Any borrower with eligible federal student loans.

This plan is ideal for those who want to pay off their student loans as quickly as possible and pay the least amount in interest.

Your monthly payments are a fixed amount of at least $50.

10 years to 30 years depending on your total loan amount.

Graduated Any borrower with eligible federal student loans.

Your payments will start out low and increase every two years.

10 years to 30 years depending on your total loan amount.

Extended Fixed

Any borrower with eligible federal student loans.

Your monthly payments are a fixed amount.

25 years

Extended Graduated

Any borrower with eligible federal student loans.

Your payments will start out low and increase every two years.

25 years

REPAYE Any borrower with eligible federal student loans.

This plan is ideal for those who want to lower their minimum pay-ment to reflect their income but are not eligible for new borrower plans like PAYE.

10 percent of your dis-cretionary income.

20 years for under-graduate study and 25 years if any of your loans are for graduate or profes-sional study.

PAYE To qualify, the payment you would be required to make under the PAYE plan (based on your income and family size) must be less than what you would pay under the Standard Repayment Plan with a 10-year repayment period.

Also to qualify you must be a new borrower as of October 1, 2007, and must have received a disbursement of a Direct Loan on or after October 1, 2011.

This plan is ideal for new borrowers who want to lower their minimum payment to reflect their income.

10 percent of your discretionary income, but never more than the 10-year Standard Repay-ment Plan amount.

20 years

© SOCIETY OF GROWNUPS05 | LOANS & GROANS

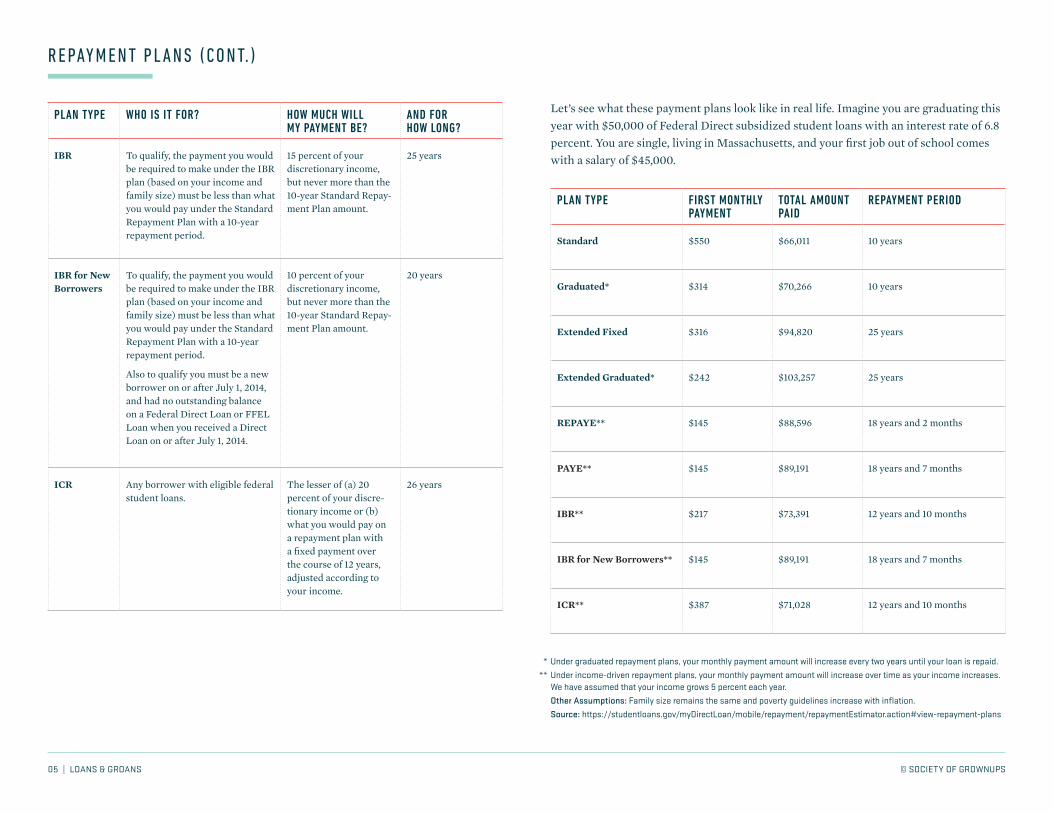

Let’s see what these payment plans look like in real life. Imagine you are graduating this year with $50,000 of Federal Direct subsidized student loans with an interest rate of 6.8 percent. You are single, living in Massachusetts, and your first job out of school comes with a salary of $45,000.

PLAN TYPE FIRST MONTHLY PAYMENT

TOTAL AMOUNT PAID

REPAYMENT PERIOD

Standard $550 $66,011 10 years

Graduated* $314 $70,266 10 years

Extended Fixed $316 $94,820 25 years

Extended Graduated* $242 $103,257 25 years

REPAYE** $145 $88,596 18 years and 2 months

PAYE** $145 $89,191 18 years and 7 months

IBR** $217 $73,391 12 years and 10 months

IBR for New Borrowers** $145 $89,191 18 years and 7 months

ICR** $387 $71,028 12 years and 10 months

Under graduated repayment plans, your monthly payment amount will increase every two years until your loan is repaid. Under income-driven repayment plans, your monthly payment amount will increase over time as your income increases. We have assumed that your income grows 5 percent each year. Other Assumptions: Family size remains the same and poverty guidelines increase with inflation.Source: https://studentloans.gov/myDirectLoan/mobile/repayment/repaymentEstimator.action#view-repayment-plans

***

PLAN TYPE WHO IS IT FOR? HOW MUCH WILL MY PAYMENT BE?

AND FOR HOW LONG?

IBR To qualify, the payment you would be required to make under the IBR plan (based on your income and family size) must be less than what you would pay under the Standard Repayment Plan with a 10-year repayment period.

15 percent of your discretionary income, but never more than the 10-year Standard Repay-ment Plan amount.

25 years

IBR for New Borrowers

To qualify, the payment you would be required to make under the IBR plan (based on your income and family size) must be less than what you would pay under the Standard Repayment Plan with a 10-year repayment period.

Also to qualify you must be a new borrower on or after July 1, 2014, and had no outstanding balance on a Federal Direct Loan or FFEL Loan when you received a Direct Loan on or after July 1, 2014.

10 percent of your discretionary income, but never more than the 10-year Standard Repay-ment Plan amount.

20 years

ICR Any borrower with eligible federal student loans.

The lesser of (a) 20 percent of your discre-tionary income or (b) what you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income.

26 years

R E PAY M E N T P L A N S ( C O N T. )

© SOCIETY OF GROWNUPS06 | LOANS & GROANS

Any third-party resources or websites referenced above are not under our control. We cannot guarantee and are not responsible for the accuracy of the resources, websites, or any products or services available through such resources or websites. While we hope the information in these materials are useful, it’s only intended to provide general education. It’s not legal, tax, or investment advice, and may not apply or be useful to your specific financial situation. If you need recommendations geared to your personal financial situation, schedule time with a financial planner.

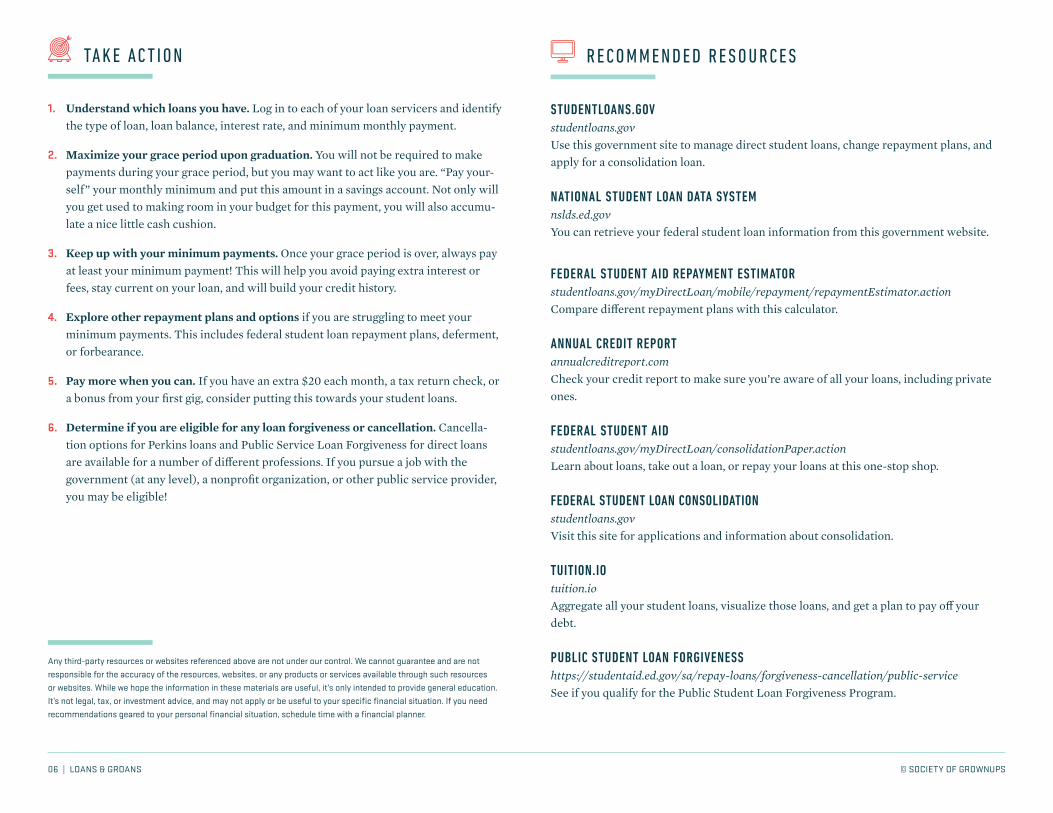

TA K E AC T I O N

1. Understand which loans you have. Log in to each of your loan servicers and identify the type of loan, loan balance, interest rate, and minimum monthly payment.

2. Maximize your grace period upon graduation. You will not be required to make payments during your grace period, but you may want to act like you are. “Pay your-self” your monthly minimum and put this amount in a savings account. Not only will you get used to making room in your budget for this payment, you will also accumu-late a nice little cash cushion.

3. Keep up with your minimum payments. Once your grace period is over, always pay at least your minimum payment! This will help you avoid paying extra interest or fees, stay current on your loan, and will build your credit history.

4. Explore other repayment plans and options if you are struggling to meet your minimum payments. This includes federal student loan repayment plans, deferment, or forbearance.

5. Pay more when you can. If you have an extra $20 each month, a tax return check, or a bonus from your first gig, consider putting this towards your student loans.

6. Determine if you are eligible for any loan forgiveness or cancellation. Cancella-tion options for Perkins loans and Public Service Loan Forgiveness for direct loans are available for a number of different professions. If you pursue a job with the government (at any level), a nonprofit organization, or other public service provider, you may be eligible!

STUDENTLOANS.GOVstudentloans.gov Use this government site to manage direct student loans, change repayment plans, and apply for a consolidation loan.

NATIONAL STUDENT LOAN DATA SYSTEMnslds.ed.gov You can retrieve your federal student loan information from this government website.

FEDERAL STUDENT AID REPAYMENT ESTIMATORstudentloans.gov/myDirectLoan/mobile/repayment/repaymentEstimator.action Compare different repayment plans with this calculator.

ANNUAL CREDIT REPORTannualcreditreport.com Check your credit report to make sure you’re aware of all your loans, including private ones.

FEDERAL STUDENT AIDstudentloans.gov/myDirectLoan/consolidationPaper.action Learn about loans, take out a loan, or repay your loans at this one-stop shop.

FEDERAL STUDENT LOAN CONSOLIDATIONstudentloans.gov Visit this site for applications and information about consolidation.

TUITION.IOtuition.io Aggregate all your student loans, visualize those loans, and get a plan to pay off your debt.

PUBLIC STUDENT LOAN FORGIVENESShttps://studentaid.ed.gov/sa/repay-loans/forgiveness-cancellation/public-service See if you qualify for the Public Student Loan Forgiveness Program.

R E C O M M E N D E D R E S O U R C E S

Can’t Get What You Don’t Ask For

Negotiating Salary

© SOCIETY OF GROWNUPS02 | CAN’T GET WHAT YOU DON’T ASK FOR

W H AT ’ S A B AT N A? ( A N D W H Y YO U N E E D O N E ! )C O M P E T I T I V E N E G OT I AT I O N : T H E 3 TO D O ’ S

1. BE PREPARED• Base your expectations on real information and figures.

• Research before you begin negotiations.

• How can value be added?

2. ENGAGE• Make a personal connection with the other party.

• If they see you as a person, or better, as a nice person or friend, it will be harder for them to be tough on you.

• Don’t view them as your opponent, but remember to assert your value.

3. FRAME• Negotiations aren’t personal.

• Don’t assume that there is no room for negotiation.

• Be flexible and creative.

Best Alternative To a Negotiated Agreement

• In some negotiations, the parties have two alternatives: make a deal or reach no settlement at all. This means they have no real BATNA.

• The stronger the BATNA(s) you have, the more power you have throughout negoti-ations.

• Stronger BATNA(s) also enhance our ability to walk away from negotiations when the deal won’t be in our favor.

T I P S F O R S U C C E S S F U L N E G OT I ATO R S

1. More often than not, let the other side give you a number first.

2. Never say “yes” to the first offer.

3. Make small moves (concessions) and be able to justify them — the other side should be able to justify their concessions as well.

4. Don’t offer a range of numbers, but do offer a range of options.

5. Know what’s possible — ask!

6. Practice, practice, practice!

7. Remember: Salary negotiations involve personalities, but they aren’t personal.

8. Be willing to walk away.

GLASSDOOR.COM & PAYSCALE.COMUse these websites to compare salaries by industry, company, and more.

GETTING TO YES: NEGOTIATING AGREEMENT WITHOUT GIVING INThis best-selling book by Roger Fisher and William Ury provides step-by-step strategies for negotiating.

R E C O M M E N D E D R E S O U R C E S

Any third party resources or websites referenced above are not under our control. We cannot guarantee and are not responsible for the accuracy of the resources, websites, or any products or services available through such resources or websites. While we hope the information in these materials are useful, it’s only intended to provide general education. It’s not legal, tax, or investment advice, and may not apply or be useful to your specific financial situation. If you need recommendations geared to your personal financial situation, schedule time with one of our financial planners.