Social Safety Nets: The Role of Education, Remittances and...

26

Social Safety Nets: The Role of Education, Remittances and Migration 1 Yaw Nyarko Department of Economics New York University 19 W. 4th Street New York, NY 10012 email: [email protected] Tel: (212) 998 8928 and Kwabena Gyimah-Brempong Department of Economics University of South Florida 4202 E. Fowler Avenue Tampa, FL 33620 email: [email protected] June 25, 2010 1 Paper to be presented at the ERD Regional Conference in Dakar, SENEGAL, June 28-30, 2010. We thank David Klinowski, Ella Wind, Silvana Melitsko, and Moussa for outstanding research assistance. Any remaining errors, however are ours.

Transcript of Social Safety Nets: The Role of Education, Remittances and...

Social Safety Nets: The Role of Education,

Remittances and Migration1

Yaw NyarkoDepartment of Economics

New York University19 W. 4th Street

New York, NY 10012email: [email protected]

Tel: (212) 998 8928

and

Kwabena Gyimah-BrempongDepartment of EconomicsUniversity of South Florida

4202 E. Fowler AvenueTampa, FL 33620

email: [email protected]

June 25, 2010

1Paper to be presented at the ERD Regional Conference in Dakar, SENEGAL, June 28-30, 2010. Wethank David Klinowski, Ella Wind, Silvana Melitsko, and Moussa for outstanding research assistance. Anyremaining errors, however are ours.

Abstract

This paper uses

KEY WORDS: EDUCATION, MIGRATION, REMITTANCES, SAFETY NET, AFRICA

JEL: O, O55, F35, F43

1 Introduction

Increased international migration has been one of the major characteristics of the current wave

of globalization. As with any other activity, there are costs an benefits. Among the benefits are

improved global allocation of labor and reduced global unemployment, increased remittances from

high income high employment countries to low income high unemployment countries, increased

human capital formation, and diffusion of technical progress.1 Against these benefits are concerns

that migration robs sending countries of their best human capital, hence slows the development

of sending countries since migrants are usually the most educated, innovative, and risk takers in

society. Often, these emigrants have been trained at high social cost by the poor sending countries

while most of the social benefits of such migration accrues to the destination countries, usually the

rich developed countries. In spite of any possible disadvantage at the aggregate level, migration

allows household the opportunity to diversity its income source, hence hedge against risk.

In low income countries, Social Safety Nets (SSN) may be critical for the survival of some

households as well as possibly lifting households out of poverty in the long run. SSN are non-

contributory transfers to the poor or vulnerable groups and may include cash transfers, food aid,

health care, housing assistance, and other forms of welfare enhancing transfers.2 In developed coun-

tries, programs designed to provide social safety net programs are generally offered by governments

or through some organized institutional channels. In Less Developed Countries (LDCs), especially

in Africa, governments are not able to provide such social safety nets; they are generally provided

through informal mutual insurance among family members or community groups(transfer among

family or community members). In African countries where majority of citizens depend on low

productivity subsistence agriculture for their livelihoods, the need for SSN to mange risks posed by

crop failure or illness cannot be over-emphasized. Although there may be several sources of such

transfers, a major source of such intra-household (intra-community) SSN are migrant remittances.

With increasing emigration of Africans to the developed world as well as the oil-rich parts of

the developing world, remittances from migrants to African countries is increasingly becoming, not

only an important source of support for African household, but a source of investment resources as

well. For example in 2008, officially recored remittances to Sub-Saharan Africa reached 21.1 billion

US dollars but fell to 20.5 billion US dollars in 2009, amounts that far exceed the amounts of official

development assistance (ODA) in both years.3 Moreover, these remittances are are not as volatile

1

as other forms of flows to Africa; indeed they may be countercyclical, thus making them strong

candidates to cushion against income fluctuations. Remittances therefore functions as stable SSN

that positively affect household consumption and human capital formation.4 Indeed, several studies

have investigate the effect of remittances on consumption or poverty of households in LDCs.

The United Nations’ Development Program (UNDP) defines vulnerability as “any threat to

survival or livelihood”. This makes the definition and measurement of vulnerability a very broad

one; it may include threats emanating from dramatic changes in income, consumption, health,

education, and other measures of well being of individuals or households. This definition of vul-

nerability is comprehensive and very broad; however, it does not easily lend itself to empirical

implementation. In this paper, we define vulnerability as shocks to livelihood. Specifically, we

measure vulnerability as shocks to household income or source of consumption support. To the

extent that remittances are not considered loans to be repaid by recipient households, they may

be considered a form of social safety net that helps to cushion household against adverse income

shocks or provide a minimum standard of living and prevents then from selling off productive assets

in order to survive.

In spite of the important role that remittances play in complementing the incomes of recipients

in low income countries, it has not been analyzed as a social safety net in the literature. This paper

investigates how migrant remittances act as social safety net to reduce vulnerability in Africa after

controlling for education and the endogeneity of migration in remittances. Specifically, we try

to answer a couple of questions: (i) to what extent do migrant, especially international migrant,

remittances act as a form of social safety net? (ii) To what extend do migrant remittances substitute

for or complement non-remittance income in consumption? We do by specifying and estimating

a household consumption function which depends on permanent and transitory income, household

characteristics and well as shocks to income as well as a remittance function that depends on,

among other things, shocks to the income of recipient households. We assume that remittances are

a component of transitory income ...o the household through transitory income and the provision

of social. The empirical work is based on waves 3 to 5 of Ghana Living Standards Survey (GLSS)

and the four waves of the Cote d’Ivoire Living Standards Survey (CLSS) data sets.

There is a strong link between education (especially higher education), migration, remittances,

and welfare of households of sending households (Nyarko: 2009, Sasin and McKenzie: 2007). A

challenge facing studies of migration, remittances and welfare is the issue of endogeneity since

2

the decision to migration, household income, and remittances are not independent of each other

(McKenzie and Sasin: 2007). For example, migration may be influenced (and influences) educa-

tion attainment in sending households and migrant remittances (transfers) may be in response to

economic/social shocks in the “home country” due to such occurrences as poor harvest, death of

a bread winner, or illness of a member of her/his family in the “home country”. Indeed prelimi-

nary analysis of our data (Table 2) suggests that remittance receiving households and non-recipient

households are significantly different in several ways. This suggests that an analysis of remittances

and SSNs should be a joint determination of education, migration, remittances and household wel-

fare. Unfortunately, our data does not allow us to treat all four variables as jointly determined

in this study. We get around this “problem” by using an estimation method that can account for

endogeneity of some of the regressors.

International migration from Africa to the developed world and the remittances that flow from

such migrants to Africa has accelerated since the 1980s. Remittances are now not only a major

source of income for households in African countries, it is indeed the major source of household

income, especially as a way of insuring against shocks. It is therefore necessary to investigate the

role that remittances play as a social safety net. Yet, with the exception of Azam and Gubert

(2006) who treat remittances as contingent flows from a joint family decision on migration income

diversification, most of the work on remittances do not treat remittances as a form of social safety

net. We treat remittances as an informal social safety net in this paper. Second, this paper

sheds some light on how remittances affect household poverty in the short run and smoothen out

consumption.

Our results can be briefly summarized as follows: We find that

This paper makes several contributions to the literature on relationships among education,

migration, remittances and social safety nets in Africa in particular and LDCs generally. First,

The rest of the paper is organized as follows; Section 2, following this introductory section,

briefly reviews recent trends in emigration and remittances in African countries, section 3 reviews

the relevant literature on migration, remittances and the welfare of household members who remain,

while section 4 develops the household consumption function we estimate. This is followed by a

discussion of the data and estimation strategy in section 5 while section 6 presents the statistical

results. Section 7 discusses the policy implications and concludes.

3

2 Trends in Migration and Remittances in Africa

In the last thirty years, migration from African countries to the developed world and the resource

rich Gulf region has been growing rapidly. Indeed it is estimated that about 2% of Africa’s popu-

lation are emigrants and this stock is growing. Of particular interest to the development of Africa

has been the migration of skilled workers from africa, skills that Africa may lack and can ill afford

to lose. It is estimated that 48% of ...

Global remittances exceeded 338b in 2008 but fell to 317 in 2009. Global portfolio, private debt

and equity reached about 600b in 2007 but fell to -25 b in 2009, FDI fell from 580 b in 2008 to

375 in 2008 while ODA never reached 150 b in the period but fell to 95b in 2009. For SSA for

example official flows reached from 18.b in 2007 to 21.1 in 2008 to 20.5 in 2009. Shows the stability

of remittance and its possible impact on LDCs. In some countries, remittances constitute a large

proportion of GDP; for example it constitutes 27, .., and 4 percent of GDP for Lesotho, Cape Verde,

and Egypt. Must be emphasized that the figures refer to remittances that come through official

channels. It is estimates that a larger amount of remittances come through unofficial channels,

hence the data we have presented here are likely to be severe under-estimate of inward remittance

to Africa.

Estimated that about 2% of African population are international migrants; majority of them are

international migrants within Africa. The composition of emigrants from Africa and the controversy

it has generated. Nyarko however argues that the problem is not the proportion of skilled Africans

who have migrated, the problem is that Africa has trained very few highly skilled workers and

argues that policies should encourage training more skilled workers in Africa, partly through the

emigration policies of developed countries.

We focus on consumption and income vulnerability. We measure vulnerability by consumption

and income shocks caused by variation in rainfall as well as death of a bread winner in the family.

We make a distinction between international and domestic remittances in our study. Our data

comes from waves 3-5 of GLSS, waves 1-4 of CLSS, the national TLSS as well as the SALSS.

3 Previous Studies

The literature on migration and remittances in the development literature has been increasing at

an exponential rate with the increase in emigration of workers from LDCs to developed world and

4

the resultant increase in remittance flows to LDCs. Because of the rapidly expanding volume of

the literature, we only present a very limited review in this paper. The literature on migration

and remittances has generally focused on three broad areas: the determinants of migration, the

determinants of remittances, and the effects of remittances in the sending countries. There is a

subdivision of studies into those using household and individual level data (micro studies) and those

using aggregate data (macro studies). Although our approach uses both micro and macro data,

we will focus mainly on the micro approach since the paper uses household data in the empirical

analysis.

By far the largest number of studies on remittances focus on the effects of remittances on

some measure of household welfare in the sending countries. The results are mixed; while a large

number of researchers find significant positive effects of remittances on the welfare of recipient

households, others find no significant effects. For example Adams (2006a), Adams, Cuecuecha,

and Page (2008a), Esquivel and Huerta-Pineda (2007), Grootaert (1987), Guzman, Morrison, and

Sjoblom (2006), Litchfield and Waddington (2003), Giannetti, Federici, and Raitano (2009) and

Semyonov and Gorodzesky (2008) conclude that migrant remittances have significant effects on

household consumption in recipient countries. Besides increasing household consumption several

studies (Esquivel and Huerta-Pineda: 2007, Brown, and Jimenez: 2008, and Acosta et al : 2008)

conclude that remittances significantly reduce poverty in recipient countries. Mazzucate (2009)

find evidence of risk pooling between migrants and their counterparts in their home countries.

While several studies conclude that remittances decrease poverty, an overwhelming proportion

of studies that investigate the effects of remittances on inequality suggests that remittances tend to

increase some measure of inequality. For example, Barhman and Boucher (1998), and Brown and

Jimenez (2008) find that remittances increases income inequality in Nicaragua and and Tonga and

Fiji respectively, while McKenzie and Rapoport (2007) find that remittances increases education

inequality among Mexican households. Although there is a general agreement on how remittances

affect the level of household consumption, there is little agreement on the effects of remittances

on the pattern of consumption expenditures. Castaldo and Reilley (2007) and Misllitcaia and

Vakhitova (2009) find that remittances significantly affect the pattern of household expenditures,

Adams et al (2008b) find that remittances have no significant impact on the pattern of household

expenditure, all things equal.

Generally, studies suggest that migration and remittances, at worse, have no significant pos-

5

itive effect on household welfare; at best they have significantly positive impacts on the welfare

of households who receive remittances. A few studies, however, find significant negative effects.

Using Australian immigration lottery data, Gibson, McKenzie, and Stillman (2009) conclude that

emigration has short term significantly net negative effects on a wide range of outcomes of house-

holds, especially emigrant households, in source countries in the Pacific. The distinguishing feature

of this paper is the use of a natural experiment resulting from the introduction of the Australian

immigration lottery which allowed the authors to control for endogeneity of emigration. Similarly,

McKenzie and Rapoport (2007) conclude that migration has no significant effect on schooling for

12-15 year olds but has strong disincentive effects on 16 to 18 year olds to acquire education.

Quisumbing and McNiven (2010) uses panel data from Filipino households to investigate the

effects migration and remittances on a host of outcomes. Treating the number of migrants and re-

mittances as endogenous, they find that a large number of migrant children decreases the value of

non land assets and total expenditure but remittances have a positive effect on housing, consumer

durables, educational expenditures, non land assets, and total expenditures per adult equivalent.

The focus of the paper is however on internal migration. Yang (2008) uses Filopino data to investi-

gate the effects of exchange rate shocks on remittances and finds that there is a positive response to

remittances when remitters’ exchange rate appreciate. He calculates an elasticity of 0.6. Yang and

Choi (2005) use Filipino data to investigate whether remittances act as insurance for recipients.

Using a panel data, the paper finds that remittances indeed function as insurance. Our paper

follows a similar pattern. Other researchers that find positive and significant effect of remittances

on poverty alleviation include Selim et al (2009), Ang, Sugiyarto and Jha (2009), and .. .

Besides consumption, researchers have investigated the effects of remittances on investment in

education, health or productive assets. Kugler and Lotti (2007) investigates the effects of remit-

tances on education and health investment in Latin America and finds positive and significant

effects on investment in these areas. Elbadawy and Roushdy (2009) finds that remittances increase

enrollment and completion rates of men and women at the university level while reducing child labor

(at least labor market participation). Osili (2007) investigates the effects of remittances on savings

and investment in the “home” country and finds that in addition to increasing the consumption

of household members at home, remittances increase savings and investment in business, housing,

other assets and human capital in their home countries. In addition to increasing consumption or

increasing household incomes in the current period, Selim et al (2009), and Ang, Suqiyaro and Jha

6

(2009) find that remittances increase investment in human capital as well as business formation.

These results suggest that the benefits of emigration and remittances exceed the short-run benefit

of increased consumption and may include reduction in inter-generational poverty reduction.

Emigrant remittance and its role as a social safety net is apparently not new and limited to

the current wave of globalization. Magee and Thompson (2006) report that Britain was a net

receiver of substantial amounts of remittances from its colonies and the US in the 18th to early

20th centuries that amounted about 1 to 2 percent of export earnings. The amount and intensity

of these remittances increases in real terms, over time and with increasing economic fortunes in the

remitting countries, suggesting that while the stock of emigrants in a country partly determines

the amount of remittances from that country, economic conditions in the host country is equally

important in determining the amount of remittances sent out. While a substantial proportion of

these remittances went to support consumption and business formation, the paper argues that a

substantial share of the remittances to Britain during the period went to finance further emigration

to the new world and the colonies in particular, a finding that is consistent with the idea that

remittances finance the development of human capital in sending countries besides its social safety

net role.

Kapur (2004) provides a comprehensive review of the literature on remittances—trends, sources,

destination, the determinants of its growth, and its development impact. The paper argues that

remittances have been the most stable and rapidly growing source of private resource transfer to the

developing world; that remittances to the developing have grown rapidly due increased emigration,

especially of skilled workers from the developed world, combined with increasingly frequent and

intensive financial crisis in the developing world has meant that these emigrants will have to send

money home to support their extended families at home. Although he argues that remittances may

have some positive effects in reducing transient poverty, the paper is generally not optimistic in

using remittances to finance development in recipient countries. The paper nevertheless provides

some policy guidelines for improving the transfers more efficient.

At the macro level, some studies find remittances to have significantly positive effect while

others find no significant effect. To the extent that increased GDP growth generate employment

for those at the bottom of the income distribution, one can argue that increased income growth

could be considered a social safety net. Vargas-Silva, Jha, and Suguyarto (2009) find that remit-

tances have positive and significant effect on in come growth in Asian countries; a 10% increase

7

in remittances/GDP ratio is associated with a 0.9 - 1.2% increase in GDP growth rate. Gupta

et al (2007) argue that remittances are an importance source of development finance that should

be properly harnessed for Sub-Saharan Africa’s development. Glytsor (2009) find growth effect of

remittances with a lag. Gapen et al (2009) conclude while workers remittances have no signifi-

cant growth impact in recipient countries, they nonetheless act as automatic stabilizers to cushion

macroeconomic shocks. In this regard, remittances act as social safety net at the aggregate level.

Sherman (2009) on the other hand cautions against drawing broad generalizations about the macro

impact of remittances since the effects depends upon several factors, including the characteristics

of migrants and the policies of both home and host countries.

Most of the studies mentioned above only look at remittances as any other income. However,

it is unlikely that all households treat remittances as a permanent income ..

A third group of studies concern itself with the determinants of remittances without regard

to its effect on the welfare of recipients or what induces emigration to begin with. Dustman and

Mestres (2010) uses panel data of German immigrants to investigate the effects of permanency of

migration on the probability and amount of remittance migrants send to their home countries. They

conclude that conditional on all other variables, permanency of migration reduces the probability,

and amount of remittances sent home. Niimi et al (2009) argue that remittances are negatively

correlated with the education attainment of the immigrants; on the other hand, Bollard et al (2009)

find that the amount remittances is positively correlated with the educational attainment of the

migrant, conditional on the probability of sending a remittance. Aredo (2005) uses panel data

from urban Ethiopian households to investigate the motivation for sending remittances. He finds

support for the hypothesis that remittances are in response to distress in recipient families (risk-

sharing hypothesis). Acosta et al (2009) finds evidence of Dutch disease effect of international

remittances.

4 A Model of Remittances, Income Shocks, and Consumption

Migration may be influenced (and influences) education attainment in sending countries as the

literature shows (it appears that the data we have available will not allow us to investigate the

determinants of migration).

8

5 Data and Estimation Method

5.1 Data

Estimation of the model require data on migrant remittances, household consumption, as well as

other household characteristics over some time period. These data requirements are exacting and

may not be easily available short of large surveys. We do not have information on individual

migrants and their history, education levels, or the characteristics of remitters to estimate the

determinants of migration (including education, migration networks, and family characteristics)

and education. We have information about the remittances received (households that received, the

amount of remittances, and number of remitters), household consumption, household income, as

well as socioeconomic characteristics.

The data used to estimate the equations above come from Waves 3 to 5 of Ghana Living

Standard Survey (GLSS) and Waves 1-4 of the Cote d’Ivoire Living Standards Survey (CLSS).

Both are large, nationally representative surveys of living standards in both countries. Beginning

in September 1987, Ghana with the help of the World Bank, has conducted surveys of living

standards of large nationally representative samples of households at regular intervals. GLSS1 was

conducted in 1987/1988, GLSS2 in 1988/89, GLSS3 in 1991/1992 and covered the entire country

with a sample of 4552 households in all 407 enumeration areas; GLSS4 was conducted in 1998/1999,

covered the entire country and had a sample of 6,000 households while GLSS5 was conducted in

2005/2006, covered the entire country with a sample size of 8,687 households. Each succeeding wave

of GLSS covered more households as well as provided more detailed and comprehensive information

about the living standards of Ghanaian households than previous ones.

The first wave of the CLSS was conducted in 1985 the second one was conducted in 1986, and

the next two waves following in 1987 and 1988. Since then, there has not been a follow up of the

CLSS. Wave 1 of the CLSS sampled 1588 households while the next three waves sampled 1600

households. The CLSS sample design followed a two stage sample design. In the initial stage, 100

primary sample units were selected from across the country; 16 communities were then randomly

selected in each of the 100 primary sample units. Unlike the GLSS, the CLSS is a rotating sample

with 50 percent of households in each wave re sampled in the next wave while the other 50 percent

are rotated out.

These surveys contain detail information on socio economic characteristics of households, eth-

9

nicity, gender, household size and composition, income, poverty status, employment, consumption,

and educational attainment, among other variables. The surveys also have information on whether

households receive remittance, source of remittance (internal or international), amount and form

of remittance, as well as the disposition of remittance, including consumption, private and public

investment, as well as human capital formation (health and education). The detailed nature of the

survey data allows us to investigate the effects remittances on poverty status and human capital

formation.

The dependent variables in the paper are household consumption and international remittances.

The GLSS and CLLS provide information on whether households receive remittance or not; whether

these remittances are cash remittances or remittances of goods, as well as the monetary value of

such non-cash remittances. We measure remittance as the monetary value of the sum of cash and

good remittances received by households in a year. We note that the questionnaire is administered

to the head of the household while remittance may be sent to and received by specific members of

the household. It is therefore possible that remittances may be measured with error on account of

recall problems.

Consumption is measured as real per capita adult equivalent consumption in a household. In

addition total consumption expenditure, we also estimated the equation for food consumption,

housing consumption and durable consumption. It is interesting to note that while non-remittance

income in both samples are significantly larger for non-remittance receiving households, house con-

sumption expenditures do not significantly differ between remittance receiving and non-remittance

families.

For the GLSS data, we measure education (education) as the highest level of education attained

by the head of the household where education is coded as follows: none = 0, primary = 1, technical,

vocational = 2, secondary, teacher training A & B = 3, SSCE, GCE A level, teacher training post sec

= 4, polytechnic = 5, bachelors = 6, masters = 7, doctorate = 8. Age (age) is the age of household

head (in years), workers (workers) is the number of adult workers in a household, household size

(hhsize) is the total number of people in a household, and all other variables are as defined in

the text above. In the CLSS data, we measured education as the number of years of education

attained.

Sample statistics of the cross-section data from GLSS5 are presented in table 1. About 35%

of households in the Ghanaian sample received some form of remittance. For the CLSS sample,

10

about 27% of households received remittances. The mean amount of rmittances were C 587,229.7

and CFA 56,883.00 for Ghana and Cote d’Ivoire respectively respectively. These represent 17 and

27 percent of recipient houshold incomes in the two countries respectively. These suggests that

remittances are very important in the lives of recipient households in Ghana nad Cote d’Ivoire.

Some comments on the characteristics of the sample data, summarized in table 2, are in order.

Surprisingly, a larger proportion of male-headed households were more likely to be poor than female

headed households.

To allow us to identify the effects of income shocks on remittances, we need a panel data set.

However, the GLSS and CLSS data sets are not are not true panels but repeated cross section

data sets. This means that traditional panel data approach will not work to identify the effects

of income shocks on remittances. We therefore follow Deaton (1985) and created a pseudo panel

from the GLSS and CLSS data sets to estimate the remittance equation. Deaton (1985) suggests

creating cohorts based on some pre-determined characteristics that are time invariant. Building

pseudo-panel data set involves a trade off between the size of a cohort and the number of cohorts.

Increasing the number of cohorts decreases the average size of a cohort thus increasing the chance

that the cohort means do not represent the population characteristics of that cohort. On the

other hand, increasing the size of each cohort decreases the number of cohorts leading to inefficient

estimates on account of possible lack of variation across cohort means and small sample size. For

the GLSS, we created cohorts based on 6 birth year bands, 10 regions and two locations giving

us 360 observations (120 x 3). For the CLSS data, we followed a similar approach and created a

pseudo panel with .. observations.

The distribution of cohort sizes are presented in table 3. The average sample size for a cohort

is 196.96 with a minimum of 88 and a maximum of 538. In general, the average cohort sizes are

largest for male-headed rural households while they are smallest for female-headed urban house-

holds regardless of the age bracket. This is partly due to the fact that there are more male-headed

households in the sample and the GLSS generally samples more rural households than urban house-

holds. In addition, younger cohorts are over-represented compared to older cohorts in the data.

Another characteristic of the data is that poverty rates are higher in older, male-headed, rural

cohorts than their female-headed, younger urban cohorts. The data also shows that conditional on

year of birth and gender, urban cohorts are more likely to receive external remittances compared

to rural cohorts.

11

5.2 Estimation Method

Our main concern in this section is whether remittances respond to shocks to household incomes

in the sending families and whether recipient households treat remittances as a form of insurance

in consumption. We therefore estimate a remittance equation (Rit that depends on the income

of receiving households (Yit), migrant incomes (Ymt), and other variables as well as a receiving

household’s expenditure functions (Cit).

Rit = γ(Yit, Ymt, Xit)

Cit = δ(Yit, Rit, Xit)

We envision that remittances will be influenced by shock to income. Assuming that Remittances

are related to household income in a linear way, changes in remittances will be related to changes

in household income. Formally,

∆Rit = γ0 + γ1∆Yit + γ2∆Ymt + X′µ + ε (1)

The coefficient of interest is the remittance equation is γ1. If remittances act as social insurance, it

must move in the opposite direction with shocks to non-remittance income of households. Therefore

we expect the coefficient on ∆Yit to be negative and significant; this is our test of remittance as a

safety net.

The literature strongly suggests that household income is endogenous on account of the fact

that family income determines education migration and remittances. Ordinary Least Squares (OLS)

estimation will produce biased and inconsistent results. We therefore instrument for income in this

equation. We use exogenous shocks to rainfall as an appropriate instrument. Most Ghanaian

Ivorian households derive their incomes from rain-fed agriculture, a disproportionate large share of

services center around processing agricultural products while government derives a large share of

its revenues from taxes on agricultural exports. The bottom line is that rainfall shocks that impact

agriculture activities will have significant impacts on non-agricultural households in Ghana and

Cote d’Ivoire. Rainfall shocks is an appropriate instrument because it is correlated with income

but only affect migrant remittances only through the shocks it imparts to household income.

Household income (Yit) is written as:

Yit = α0 + α1Rain + X′β + ε (2)

12

This implies that shocks in household income can be written as a function of rainfall shocks and

and a vector of household and environmental factors. Formally, income shocks can be written as:

∆Yit = α0 + α1∆Rain + X′β + ε (3)

Equation (1) is the remittance equation we estimate with equation 93) serving as an instrument

to shocks to income. The variables contained in the X vector include the age of the household head

and its square, the educational attainment of the household head, the number of workers in the

household, the gender of the household, the number of adult workers in the household, the number

of household members with a high school or more of education, an indicator variable as to whether

a household has a member abroad, the number of remitters in a family, and whether a household is

located in an urban area. We used the shocks to growth rates in OECD countries to proxy shocks

to migrant incomes.∗∗∗

The dependent variable in the equation of interest is the shock to remittance while the variable

of interest is the shock to household non-remittance income (∆Yit). We measured this variable as

the deviation of current income from the “long term average” income, which in this case implied

the average income of the cohort over all waves. The shocks were divided by the average income

at the beginning of the period.

6 Results

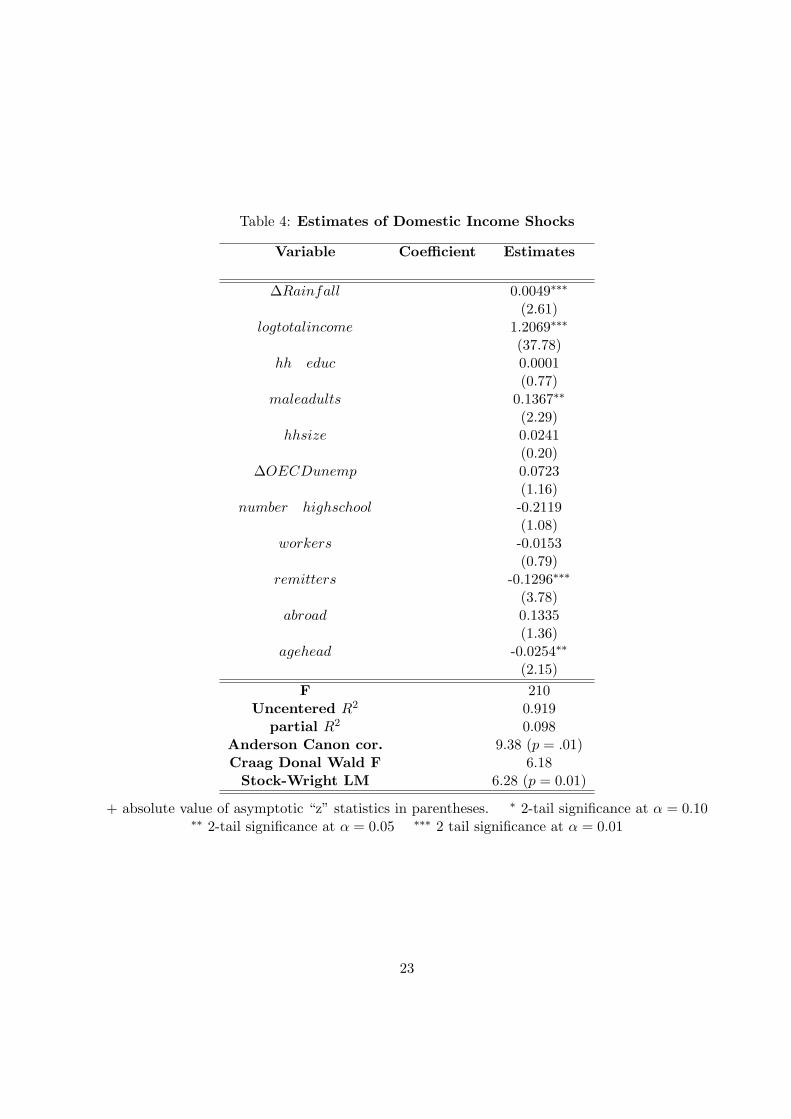

In this section, we discuss the results of the estimates of changes in remittances equation. Table 4

presents the first stage estimates in which rainfall shocks are used to predict shocks to household

non-remittance income while table 5 presents the estimates for the remittance equation using the

GLSS data. Column 3 of table 5 presents the IV results while we present a random effect estimates

in column 2 for the purposes of comparison. Regression statistics in table 4 suggest that rainfall

shocks and the other control variables predict shocks in non-remittance incomes of households

in the sample with a very high degree of accuracy. The coefficient of rainfall shocks is positive

and significantly different from zero indicating that shocks in rainfall are positively correlated with

shocks in non-remittance incomes of households. All diagnostics suggest rainfall shock is a “strong”

instrument for income shocks in our sample.

Our main results are presented in column 3 of table 5. The regression statistics suggests that

the model fits the data reasonably well. In particular, we reject the null hypothesis that all slope

13

coefficients are jointly equal to zero at any reasonable degree of confidence and the Sargan test

indicate that the instrument vector is appropriate. We do not reject the over-identifying restrictions

we impose in estimation. Most of the coefficients are of the expected signs and significantly different

from zero at α = .05 or better.

Our main interest in the coefficient of Income in this equation. The coefficient on this variable

is negative and significantly different from zero at α = .01. This suggests that migrant remittances

respond to non-remittance incomes of households counter cyclically; remittances increase when non-

remittance incomes of households decrease. Similarly, remittances decrease when non-remittance

incomes of households increases, all things equal. This suggests that remittance income sent by

migrants act as a form of insurance, hence an important social safety net for recipient households.

This results is consistent with the results of previous studies that find that remittances act as a

form of insurance for recipient households.

The coefficients of other variables in the remittance equation are generally of the expected

signs and most are significantly different from zero at conventional levels. Of particular interest is

the negative coefficient of ∆OECDuempl, our proxy variable for migrant incomes. The negative

coefficient on this variable suggests that decreased income opportunities (increased unemployment)

for migrants in the host countries results in decrease remittances to their families. This results is

expected and reasonable.

Other variables

OLS estimates in 2

7 Conclusion

14

8 Notes

1. For more on the effects of migration on diffusion of technology, see Andrew Burns and Sanket

Mohapatra: 2008, International Migration and Technological Progress, Migration and Development

Brief 4, Feb 2008.

2. For expanded discussion of SSNs, see Grosh et al : 2008.

3. This refers only to remittances that are sent through “official” channels. It is estimated that 2

out of every three dollars of remittances to Africa are sent through “unofficial” channels.

4. See the literature review section below.

*** We do not have information on the specific host countries of the migrants in the sample for us

to provide any finer proxy than this crude one. We assume that most of the external remittances

come from migrants to industrialized or natural resource rich countries whose economic fortunes

are linked to those of OECD countries.

15

9 References

1. Acosta, P., C. Calderon, P. Pajnzylber, and H. Lopez (2008), “What is the Impact of Inter-

national Remittances on Poverty and Inequality in Latin America?’, World Development, 30 (1),

89-114.

2. Acosta, P. A., E. K. Lartey, and F. S. Mandelman (2009), “Remittances and Dutch Disease”,

Journal of International Economics, 79 (1), 102-116.

3. Adams Jr, R. H., A. Cuecuecha, and J. Page (2008a), The Impact of Remittances on Poverty

and Inequality in Ghana, World Bank Policy Research Working Paper No. 4732, Washington DC,

World Bank.

4. ——————- (2008b), Remittances, Consumption and Investment in Ghana, World Bank

Policy Research Working Paper No. 4541, Washington DC, World Bank.

5. Amuedo-Dorantes, C. and S. Pozo (2006), “Remittances as Insurance: Evidence from Mexican

Immigrants”, Journal of Population Economics, 19, 227-254.

6. Ang, A. P., G. Sugiyarto, and S. Jha (2009), Remittances and Household Behavior in the

Philippines, Asian Development Bank Working Paper Series, No. 188.

7. Aredo, D (2005), Migrant Remittances, Shocks and Poverty in Ethiopia: An Analysis of Micro

Level Panel Data, Global Development Network Discussing Paper.

8. Azam, J-P. and F. Gubert (2006), “Migrant’s Remittances and the Household in Africa: A

Review of Evidence’, Journal of African Economies, 15 AERC Supplement 2, 426-462.

9. Barham, B. and S. Boucher (1998), “Migration, Remittances, and Inequality: Estimating the

Net Effects of Migration on Income Distribution”, Journal of Development Economics, 55, 307-331.

10. Bollard, A., D. McKenzie, M. Morten, and H. Rapoport (2009), Remittances and the Brain

Drain Revisited: The Microdata Show that More Educated Migrants Remit More, World Ban Policy

Research Paper No. 5113.

11. Brown, R. P. C. and E. Jimenez (2008), “Estimating the Net Effect Migration and remittances

on Poverty and Inequality: Comparison of Fiji and Tonga”, Journal of International Development,

20, 547-571.

12. Castaldo, A. and B. Reilly (2007), “Do Migrants Remittances Affect Consumption Patterns of

Albanian Households?”, South-Eastern Europe Journal of Economics, 1, 25-54.

13. Deaton, A. (1985), “Panel Data from Time-Series of Cross-Section”, Journal of econometrics,

16

30, 109-130.

14. Dustman, C. and J. Mestres (2010), “Remittances and Temporary Migration”, Journal of

Development Studies, 92, 62-70.

15. Elbadawy, A. and R. Roushdy (2009), Impact of International Migration and Remittances on

Child Schooling and Child Work: The Case of Egypt, Population Council Working Papers

16. Esquivel, G. and A. Huerta-Pineda (2007), “Remittances and Poverty in Mexico: A Propensity

Score Matching Approach”, Integration and Trade, 27, 45-71.

17. Gapen, M., A. Barajas, R. Chami, P. Montiel, and C. Fullenkamp (2009), Do Workers’

Remittances Promote Economic Growth?, IMF Working Papers No. 09/153.

18. Giannetti, M., D. Federica, and M. Raitano (2009), “Migrant Remittances and Inequality in

Central Europe”, International Review of Applied Economics, 23 (3), 289-307.

19. Glewe, P (1991), “Investigating the Determinants of Household Welfare in Cote d’Ivoire”,

journal of Development Economics, 35 307-337.

20. Glytsos, N. P. (2005), “The Contribution of Remittances to Growth: A Dynamic Approach

and Empirical Analysis”, Journal of Economic Studies, 32 (5-6), 468-496.

21. Gibson, J., D. McKenzie, and S. Stillman (2009), The Impacts of International Migration on

Remaining Household Members: Omnibus Results from a Migration Lottery, World Bank Policy

Research Paper, No. 4956, Washington DC, World Bank.

22. Grootaert, C. (1997), “The Determinants of Poverty in Cote d’Ivoire in the 1980s”, Journal of

African Economies, 6 (2), 169-196.

23. Grosh, M., C. del Ninno, E. Teslinc, and A. Ouerghi (2008), The Design and Implementation

of Effective Safety Nets, Washington DC, World Bank Publications.

24. Gupta, S., C. Pattillo, and S. Waugh (2007), Impact of Remittances on Poverty and Financial

Development in Sub-Saharan Africa, IMF Working Paper No. WP/07/38, Washington DC, IMF.

25. Kapur, D. (2004), Remittances: The New Development mantra?”, G-24 Discussion Paper Series

No. 29., Geneva, UNCTAD.

25. Kugler, M. and E. Lotti (2007), “Migrant Remittances, Human Capital Formation and Job

Creation Externalities in Central America”, Integration and Trade, 27, 105-134.

27. Litchfield, J. and Waddington (2003) Migration and Poverty in Ghana: Evidence from the

Ghana Living Standard Survey, Sussex Migration Working Papers No. 10, Sussex University, UK.

28. Lopez,C. and A. Olmeda (2006), International Remittances and Development: Existing Ev-

17

idence, Policies and Recommendation, Inter-American Development Bank Occasional Paper No.

41, Washington DC, Inter-American Development Bank.

29. Magee, G. H. and A. S. Thompson (2006), “‘Lines of Credit, Debt of Obligations’: Migrant

Remittances to Britain, 1875-1913”, Economic History Reviews, LIX (3), 539-577.

30. Mazzucato, V. (2009), “Informal Insurance Arrangements in Ghanaian Migrants’ Transnational

Networks: The Role of Reverse Remittances and Geographic proximity”, World Development, 37

(6), 1105-1115.

31. McKenzie, D. and H. Rapoport (2007), “Migration and Education Inequality in Rural Mexico”,

Integration and Trade, 27 135-158.

32. McKenzie D. and M. S. Sasin (2007), Migration, Remittances, Poverty, and Human Capital:

Conceptual and Empirical Challenges, World Bank Policy Working paper No. 4272, Washington

DC, World bank.

33. Niimi, Y., T. H. Pham, and B. Reily (2009), “Determinants of Remittances: Recent Evidence

Using Data on Internal Migrants in Vietnam”, Asian Economic Journal, 22 (1), 19-39.

34. Nyarko, Y. (2009), EU Policies and African Human Capital Development, EUI Working Paper

RSCAS 2010/30.

35. Page, J. and S. Plaza (2006), “Migration Remittances and Development: A Review of Global

Evidence”, Journal of African Economics, AERC Supplement 2, 245-336.

36. Osili, U. O. (2007), “Remittances and Savings from International Migration: Theory and

Evidence Using a Matched Sample”, Journal of Development Economics, 83,446-465.

37. Quartey, P. and T. Blankson (2004), Do Migrant Remittances Minimize the Impact on Macro-

volatility on the Poor in Ghana?, GDN Working Papers.

38. Quisumbing, A. and S. McNiven (2010), “Moving Forward, Looking Back: The Impact of

Migration and Remittances on Assets, Consumption, and Credit Constraints in the Rural Philip-

pines”, Journal of Development Studies, 46 (1), 91-113.

39. Raiham, S., B. H. Khondker, G. Sugiyarto, and S. Jha (2009), Remittances and Household

Welfare: A Case Study of Bangladesh, Asian Development Bank Working Papers, No. 189.

40. Sarris, A. and P. Karfakis (2010), Vulnerability to Covariate and Idiosyncratic Shcks and Safety

Net Targeting of Rural Households with an Application to Rural Tanzania, paper presented at the

ERD Conference on Social Safety Nets, the European Perspectives, Paris, June 17-18, 2010.

41. Sharma, K. (2009), The Impact of Remittances on Economic Insecurity, UN Department of

18

Economics and Social Affairs Working Papers.

42. Skoufias, E. and A. R. Quisumbing (2005), “Consumption Insurance and Vulnerability to

Poverty: A Synthesis of the Evidence from Bangladesh, Ethiopia, Mali, Mexico, and Russia”,

European Journal of Development Research, 17 (1), 24-58.

43. Townsend, R. (1995), “Consumption Insurance: An Evaluation of Risk-Bearing Systems in

Low-Income Countries”, Journal of Economic Perspectives, 9 (3), 83-102.

44. Vargas-Silva, C., S. Jha, and G. Sugiyarto (2009), Remittances in Asia: Implications for the

Fight Against Poverty and the Pursuit of Economic Growth, Asian Development Bank Working

Papers, No. 182.

45. Wiegand, C. and M. Grosh (2008), Levels and Patterns of Safety Net Spending in Developing

and Transition Countries, World Bank Social Protection and Labor Working Paper No. 0817.

46. Yang, D (2008), “International Migration, Remittances and Household Investments: Evidence

from the Philippine Migrants; Exchange rate Shocks”, The Economic Journal, 118, 591-630.

47. Yang, D. and H. Choi (2005), Are remittances Insurance? Evidence from Rainfall Shocks in

the Philippines, RSIE Discussion Paper No. 535, University of Michigan, Ann Arbor.

19

Table 1: Summary Statistics of Sample Data: Ghana

Variable Mean∗ Standard Deviation Minimum Maximum

income (Cedi) 2803230 1329305 0.00 8807433

non− remitinc(Yit) (Cedi) 2589893 1266434 0.00 8358552

remitinc (Rit) 2133466 272512.6 0.00 3054948

consumption (Cedis)

∆Remit -0.069 0.701 -0.616 0.3074

∆Rain (mm) 2.72 49.76 -116.53 117.62

∆Unemp -0.30 0.404 -0.861 0.38

remitters 1.01 0.491 0.0 3.0

agehead 15.306 7.036 3.47 48.70

education 3.299 6.08 0.0 16

hhsize 4.36 1.349 1.00 13

maleadult 1.106 0.33 0.00 8

N 352

∗ these are unweighted averages.

20

Table 2: Characteristics of Recipients and Non Recipient Households

Variable Recipients Non-Recipients DifferencePanel A: Ghana

hhsize 3.8328 4.7488 0.9160

employmentinc 748,962 1,269,971 -521,005∗∗

agehead 45.875 44.918 0.9750

consumptionexp 2,203,562 2,067,719 135,843

nonremitinc 2796611 3,613,494 -816,883∗∗

remitinc 587,229.7∗∗ 0.0 587,229.9∗∗∗

education ∗∗∗ ∗∗∗ ∗∗∗

Panel B: Cote d’Ivoire

hhsize 11.23 11.97 -0.74

employmentinc. 1,495,162 1,612,618 -117,456

agehead 21.93 21.268 0.662

consumptionexp 2,028,326 2,158,300 -129,974

nonremitinc 1,495,162 1,612,618 -117,456

remitinc 556,883 0.0 556,883

education 6.7544 6.622 0.1324

∗∗ 2-tail significance at α = 0.05 ∗∗∗ 2 tail significance at α = 0.01

21

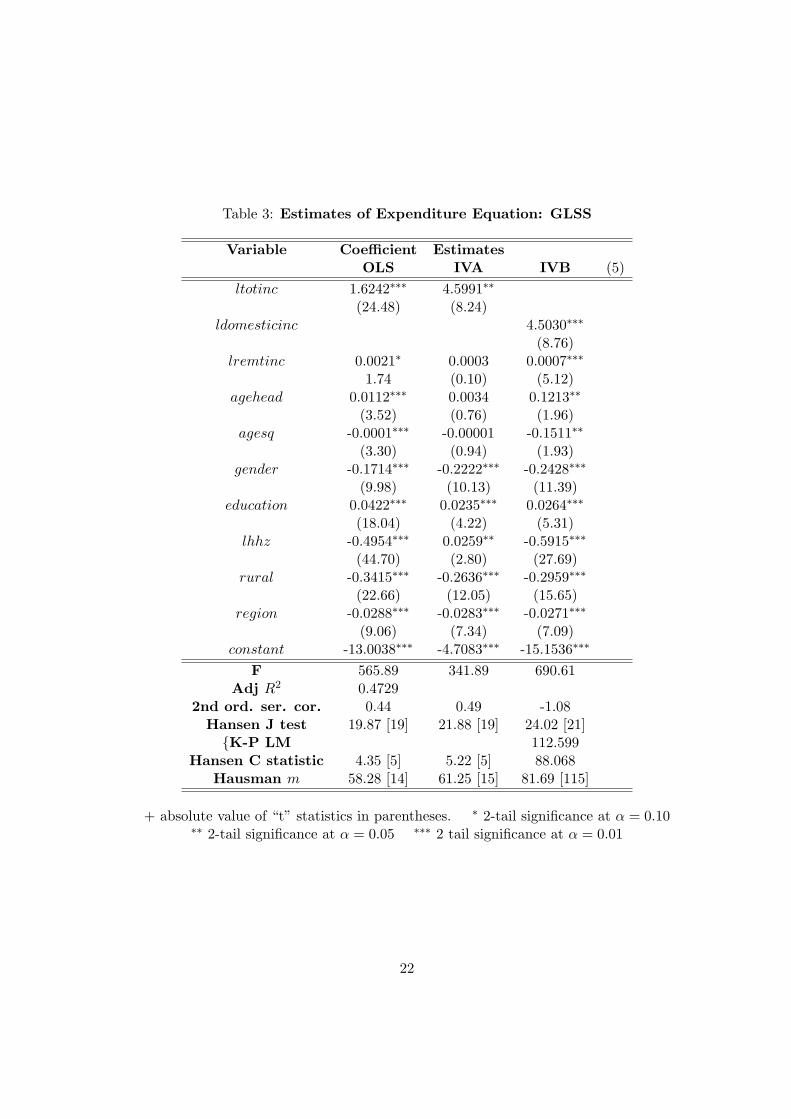

Table 3: Estimates of Expenditure Equation: GLSS

Variable Coefficient EstimatesOLS IVA IVB (5)

ltotinc 1.6242∗∗∗ 4.5991∗∗

(24.48) (8.24)ldomesticinc 4.5030∗∗∗

(8.76)lremtinc 0.0021∗ 0.0003 0.0007∗∗∗

1.74 (0.10) (5.12)agehead 0.0112∗∗∗ 0.0034 0.1213∗∗

(3.52) (0.76) (1.96)agesq -0.0001∗∗∗ -0.00001 -0.1511∗∗

(3.30) (0.94) (1.93)gender -0.1714∗∗∗ -0.2222∗∗∗ -0.2428∗∗∗

(9.98) (10.13) (11.39)education 0.0422∗∗∗ 0.0235∗∗∗ 0.0264∗∗∗

(18.04) (4.22) (5.31)lhhz -0.4954∗∗∗ 0.0259∗∗ -0.5915∗∗∗

(44.70) (2.80) (27.69)rural -0.3415∗∗∗ -0.2636∗∗∗ -0.2959∗∗∗

(22.66) (12.05) (15.65)region -0.0288∗∗∗ -0.0283∗∗∗ -0.0271∗∗∗

(9.06) (7.34) (7.09)constant -13.0038∗∗∗ -4.7083∗∗∗ -15.1536∗∗∗

F 565.89 341.89 690.61Adj R2 0.4729

2nd ord. ser. cor. 0.44 0.49 -1.08Hansen J test 19.87 [19] 21.88 [19] 24.02 [21]{K-P LM 112.599

Hansen C statistic 4.35 [5] 5.22 [5] 88.068Hausman m 58.28 [14] 61.25 [15] 81.69 [115]

+ absolute value of “t” statistics in parentheses. ∗ 2-tail significance at α = 0.10∗∗ 2-tail significance at α = 0.05 ∗∗∗ 2 tail significance at α = 0.01

22

Table 4: Estimates of Domestic Income Shocks

Variable Coefficient Estimates

∆Rainfall 0.0049∗∗∗

(2.61)logtotalincome 1.2069∗∗∗

(37.78)hh educ 0.0001

(0.77)maleadults 0.1367∗∗

(2.29)hhsize 0.0241

(0.20)∆OECDunemp 0.0723

(1.16)number highschool -0.2119

(1.08)workers -0.0153

(0.79)remitters -0.1296∗∗∗

(3.78)abroad 0.1335

(1.36)agehead -0.0254∗∗

(2.15)F 210

Uncentered R2 0.919partial R2 0.098

Anderson Canon cor. 9.38 (p = .01)Craag Donal Wald F 6.18

Stock-Wright LM 6.28 (p = 0.01)

+ absolute value of asymptotic “z” statistics in parentheses. ∗ 2-tail significance at α = 0.10∗∗ 2-tail significance at α = 0.05 ∗∗∗ 2 tail significance at α = 0.01

23

Table 5: Estimates of Remittance Equation

Variable Coefficient Estimates

OLS IV∆DomesticInc -0.0197∗∗ -0.2713∗∗∗

(1.98) (2.60)logtotalincome 0.0334∗∗∗ 0.3743∗∗∗

(3.17) (2.76)educ -0.0008∗ -0.0017∗∗∗

(1.70) (2.85)maleadults -0.0179 -0.0115

(1.35) (0.50)hhsize 0.0007 0.0008

(0.20) (0.13)∆OECDunemp -0.0231∗∗∗ -0.0882∗∗∗

(4.09) (3.51)number highschool 0.0216 0.0128

(1.52) (0.16)workers -0.0147∗∗∗ -0.0201∗∗∗

(3.30) (2.94)remitters 0.0237∗∗∗ 0.0578∗∗∗

2.60) (2.58)abroad -0.0712∗∗∗ -0.0348∗∗

(2.66) (2.11)constant -0.4947∗∗∗

(3.20)χ2 90.70 64.41R2 0.218

2nd ord. ser. cor. 0098Sargan 1.576 (p = .209)

Hansen C. statistic 6.22 [4]Anderson Can. Corr 9.62 (p = 0.01)

+ absolute value of asymptotic “z” statistics in parentheses. ∗ 2-tail significance at α = 0.10∗∗ 2-tail significance at α = 0.05 ∗∗∗ 2 tail significance at α = 0.01

24