SME Finance and Credit Rating of SMEs · Contents I. Introduction II. Asian Financial Markets III....

21

SME Finance and Credit Rating of SMEs Naoyuki Yoshino Dean, Asian Development Bank Institute (ADBI) Professor Emeritus, Keio University, Japan [email protected], [email protected]

Transcript of SME Finance and Credit Rating of SMEs · Contents I. Introduction II. Asian Financial Markets III....

SME Finance

and

Credit Rating of SMEs

Naoyuki Yoshino

Dean, Asian Development Bank Institute (ADBI)

Professor Emeritus, Keio University, Japan

Contents

I. Introduction

II. Asian Financial Markets

III. SME Credit Rating in Japan

IV. Financial Education

V. Alternative Sources of SME Financing

2

I. Introduction: SME Finance

Venture business:

Successful Japanese examples: Toyota, Honda, SONY, Seven-Eleven

HONDA had no support by the government

HONDA could not borrow money

M-bank made loans to HONDA

How to finance start-up business?

Human capital development in SME

3

II. Asian Financial Markets: Main Features

1. Bank-dominated financial system

2. Small share of bond markets Needs for long term

financing

3. Lack of long-term investors such as pension funds

and life insurance

4. Bench mark bond market (sovereign bond)

Infrastructure bond, corporate bond

5. High percentage of SMEs

6. Large share or Microcredit (finance companies);

lack of venture capital

4

5

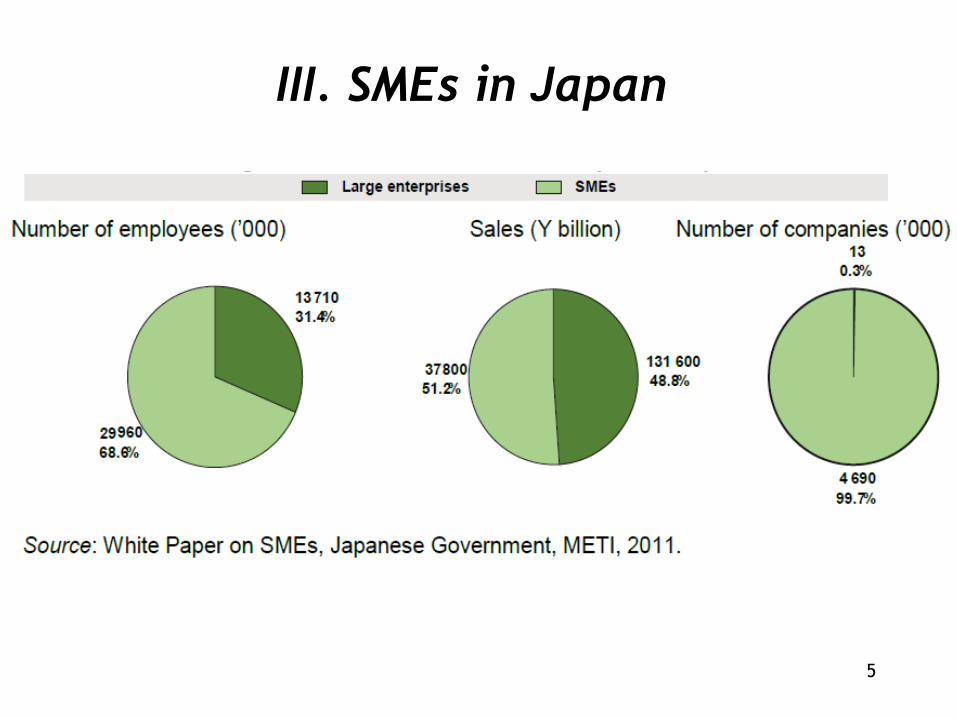

III. SMEs in Japan

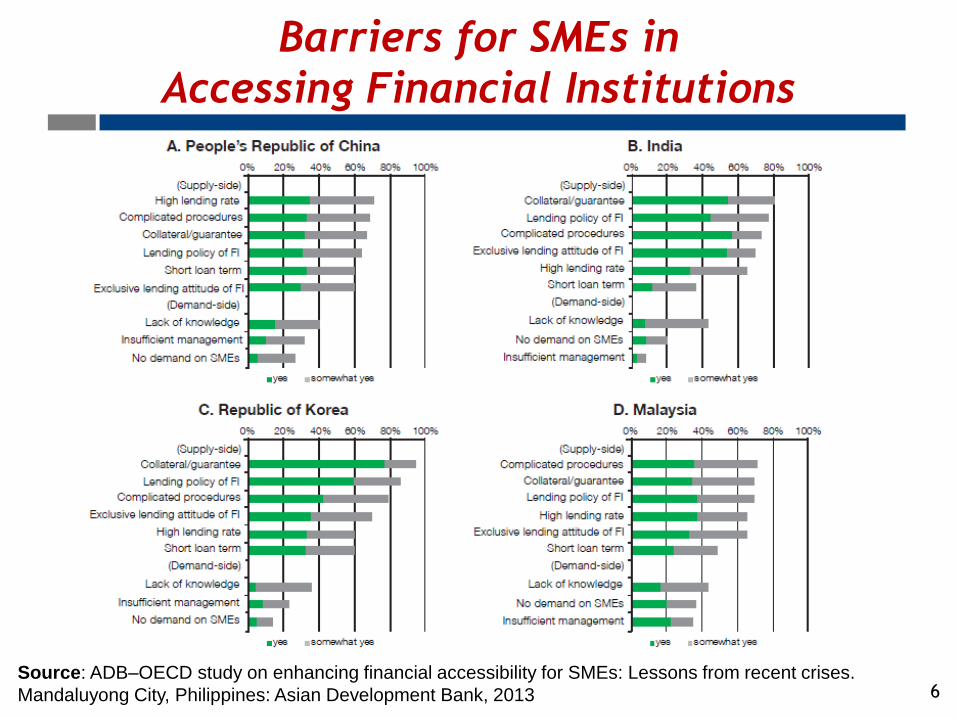

Barriers for SMEs in

Accessing Financial Institutions

6 Source: ADB–OECD study on enhancing financial accessibility for SMEs: Lessons from recent crises.

Mandaluyong City, Philippines: Asian Development Bank, 2013

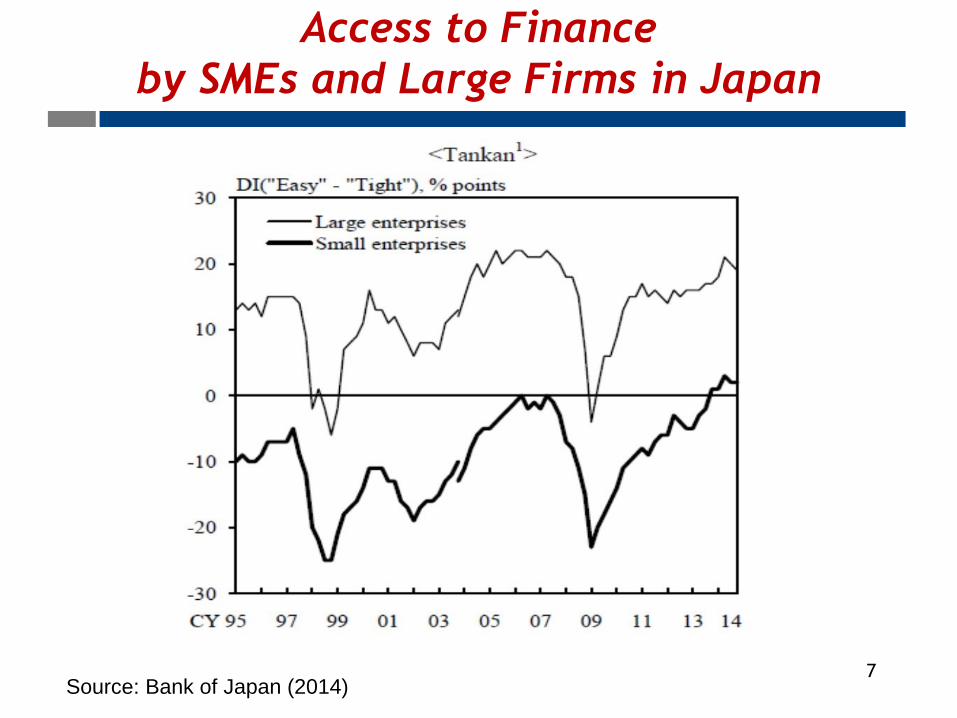

Access to Finance

by SMEs and Large Firms in Japan

7 Source: Bank of Japan (2014)

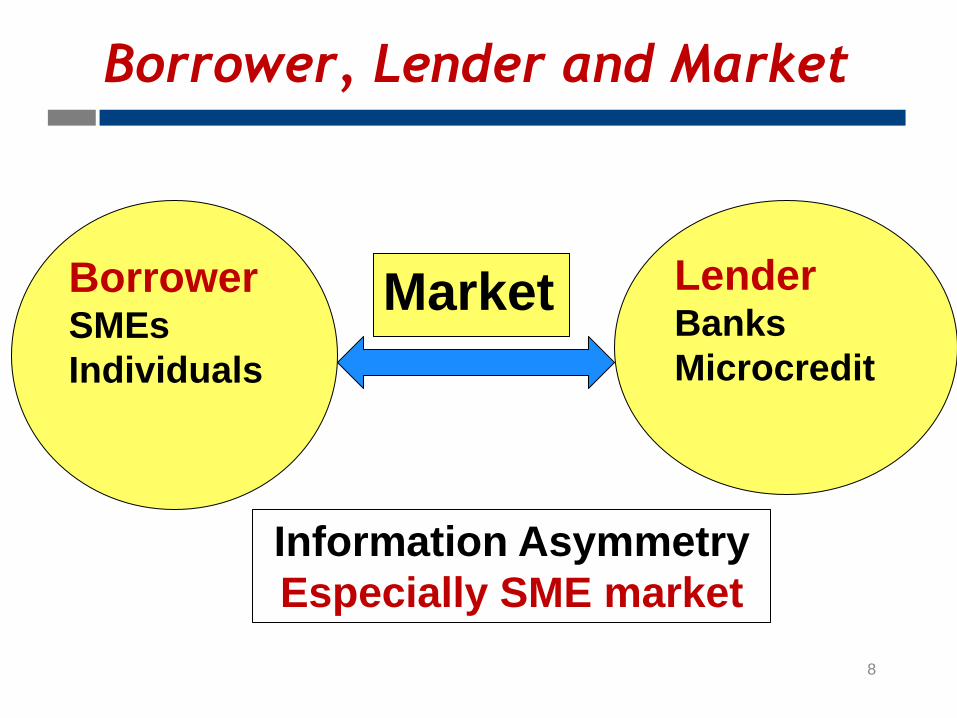

Borrower, Lender and Market

8

Borrower SMEs

Individuals

Lender Banks

Microcredit

Market

Information Asymmetry

Especially SME market

Four Accounts by SME

1. Account to show to bankers

2. Account to show to tax authority

3. His own account

4. Account to show to his wife

9

10

Credit Risk Database of Credit Guarantee

11

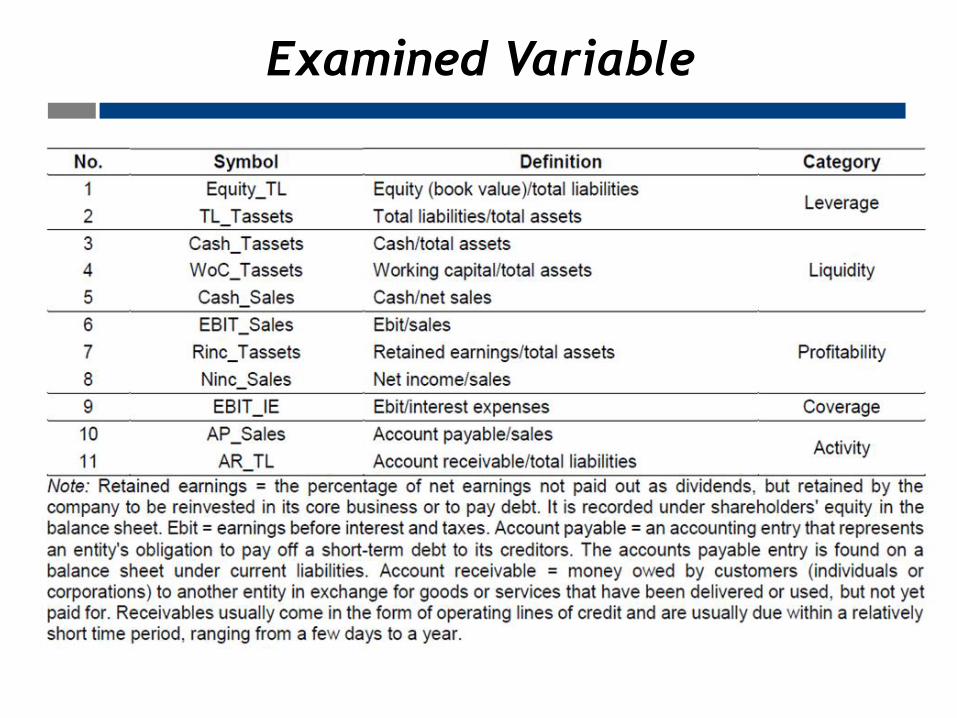

Examined Variable

12

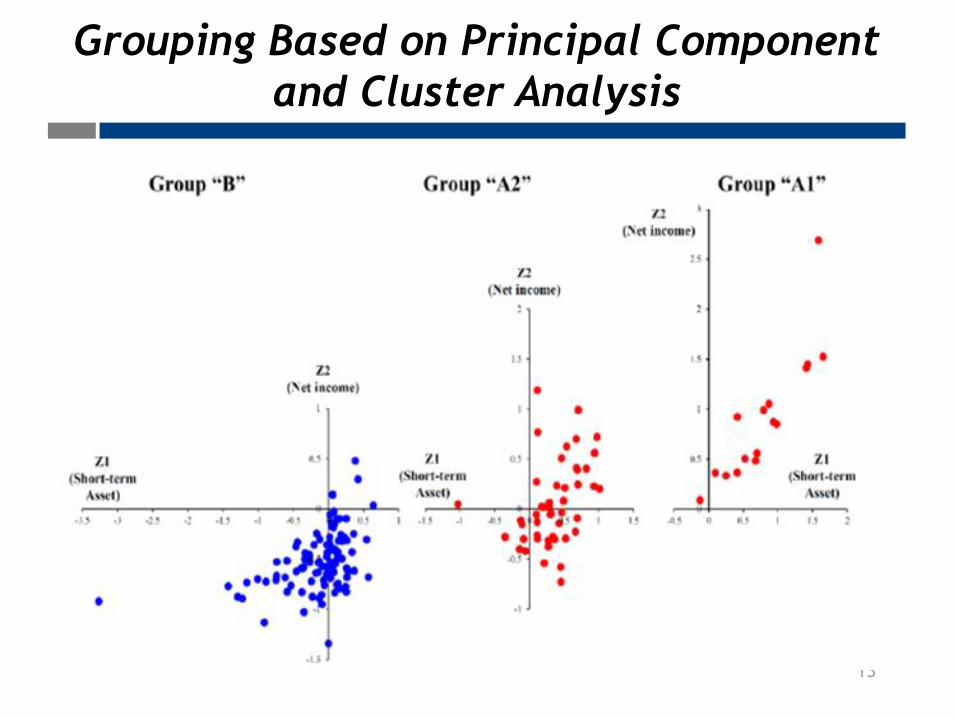

Cluster analysis:

The average linkage method

Dendogram Using Average Linkage

13

Grouping Based on Principal Component

and Cluster Analysis

Credit Rating of SMEs using Asian Data

(i) Sales

(ii) Assets

(iii) Liquidity (Cash)

(iv) Total Debt

14

IV. Financial Education for SMEs

Education Program and Textbooks

1. Financial Planners Association:

Individual Borrowing

2. Central Bank of Japan:

Text books, educate school teachers,

regional Education Program

3. Various Financial Associations:

Bankers Association, Stock Exchange

15

16

V. Alternative Solutions:

Start up businesses

Hometown Investment ---------------------------------------------

A Stable Way to Supply Risk Capital

Yoshino, Naoyuki; Kaji Sahoko (Eds.)

2013, IX, 98 p. 41 illus.,20 illus. in color

Available Formats:

•ebook

•Hardcover

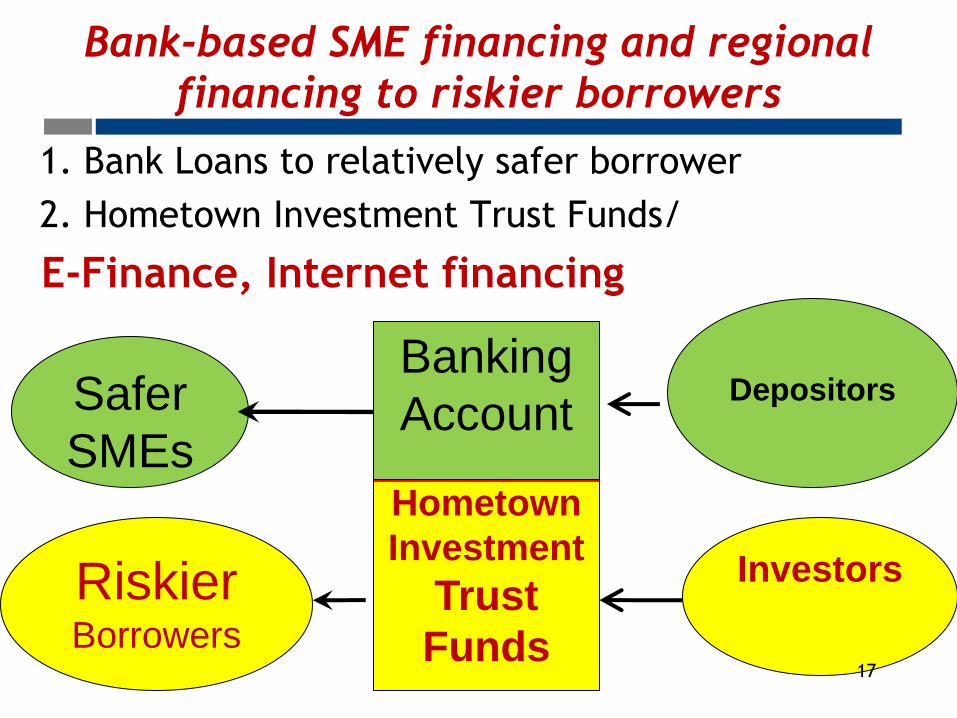

Bank-based SME financing and regional

financing to riskier borrowers

1. Bank Loans to relatively safer borrower

2. Hometown Investment Trust Funds/

E-Finance, Internet financing

Banking

Account

Hometown

Investment

Trust

Funds

Riskier Borrowers

Investors

Depositors Safer

SMEs

Banking

Account

17

Investment in SMEs and start up businesses

18

Two Types of Investors

1. Community Type Infrastructure • Hometown Investment Trust Funds

• Wind power Generator Funds

• Japanese Wine Fund

• Local Airport

• Agricultural Sector

2. Large Projects and Professional Investors • Pension Funds Brown fields

• Insurance companies Not green field

• Mutual Funds

Reference: Cargill and Yoshino: “Postal Savings and Fiscal Investment in Japan”. Oxford University Press

19

Credit Guarantee Mechanism

1. Credit Guarantee System

• 100% guarantee

• Partial guarantee (80%, 20%)

2. Differential guarantee ratio to each bank

based on their past performance

3. How to avoid moral hazard ?

4. To reduce information asymmetry

5. Temporary downturn of business

6. Structural downturn of business

7. Costs and Benefits of Credit Guarantee

20

Thank you very much

for your attention

21