Slovenian Pension System in the Context of Upcoming Demographic Developments Boris Majcen and...

13

Slovenian Pension System in Slovenian Pension System in the Context of Upcoming the Context of Upcoming Demographic Developments Demographic Developments Boris Majcen and Miroslav Verbič Institute for Economic Research

-

Upload

melina-todd -

Category

Documents

-

view

218 -

download

0

Transcript of Slovenian Pension System in the Context of Upcoming Demographic Developments Boris Majcen and...

Slovenian Pension System in the Slovenian Pension System in the Context of UpcomingContext of Upcoming Demographic Demographic

DevelopmentsDevelopments

Boris Majcen and Miroslav Verbič

Institute for Economic Research

Contents of the Presentation

Relevant characteristics of the on going Slovenian pension reform

Estimated effects of the pension reform on fiscal sustainability and welfare

Supplementary pension savings

Concluding remarks

Pension Reform OptionsHigher contributions (or budget transfers)Lower benefitsLater retirement

Keeping status quo not possible!Who will loose? Only young and future generations or also pensioners?What about pension reform in Slovenia ?

Relevant characteristics of the pension reform

Improved horizontal equity in the pension systemThe gender divide regarding eligibility and benefits considerably narrowed (equalization of accrual rates, eligibility criteria for women closer to those for men)Greater emphasis on the principle of vertical equity or “solidarity” (minimum and maximum pension base, not capped social security contributions)Flexible retirement with bonuses and malusesEnabled development of supplementary pension savings within the second pillarGradual introduction of many stated changesThe pension system is highly intransparent

Lower benefitsPension base – from 10 to best 18-year average of net wagesAcrual rates – from 85% of pension base to 72,5% (till 2024); equilized acrual rates for men and womenCorrection of acrual rates also for the existing pensionersRevalorization of pension base (horizontal equalization of pensioners)Indexation of pensionsMaximum pension base – 4 times minimum pension base

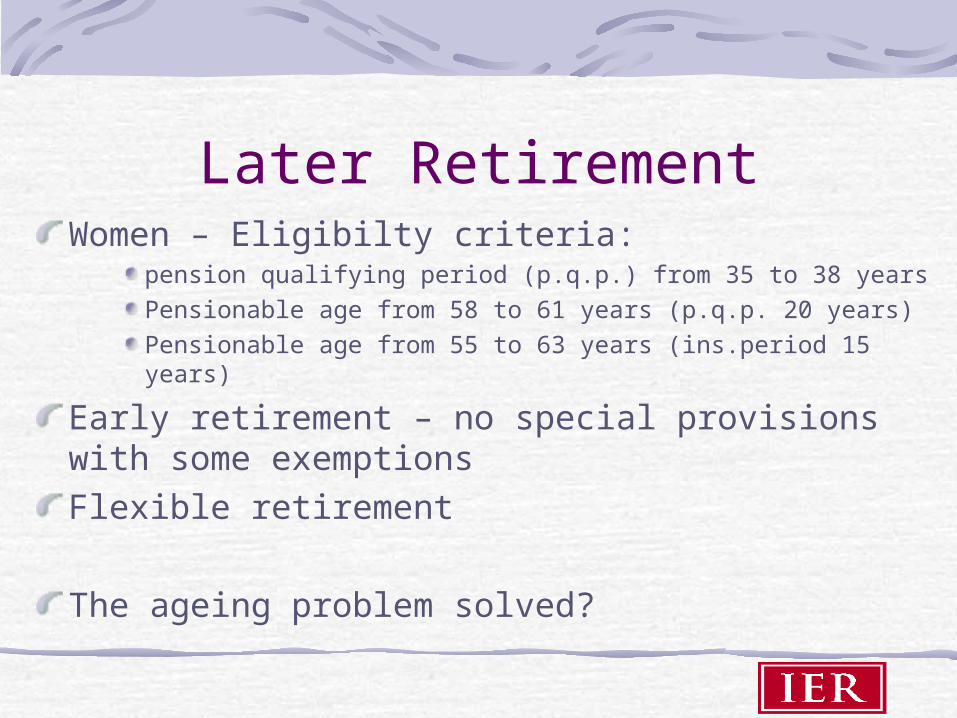

Later RetirementWomen – Eligibilty criteria:

pension qualifying period (p.q.p.) from 35 to 38 yearsPensionable age from 58 to 61 years (p.q.p. 20 years)Pensionable age from 55 to 63 years (ins.period 15 years)

Early retirement – no special provisions with some exemptionsFlexible retirement

The ageing problem solved?

Table 1:Estimates of total balance of the state pension fund (in % of GDP) using different assumptions about retirement age and indexation level of pensions

Source: Calculations using generational accounts model (March 2007); cf. Verbič (2007, p. 281).

2010 2020 2030 2040 2050 Retirement age of 60 years, 100% indexation of pensions –4,1 –6,0 –8,9 –12,0 –13,7 Retirement age of 60 years, 80% indexation of pensions –3,8 –4,7 –6,3 –8,5 –9,2 Retirement age of 61/63 years, 100% indexation of pensions –3,6 –4,6 –6,9 –9,9 –11,7 Retirement age of 61/63 years, 80% indexation of pensions –3,3 –3,5 –4,8 –6,6 –7,5 Retirement age of 65 years, 100% indexation of pensions –3,0 –1,9 –3,8 –6,2 –8,1 Retirement age of 65 years, 80% indexation of pensions –2,8 –0,9 –1,9 –3,5 –4,5

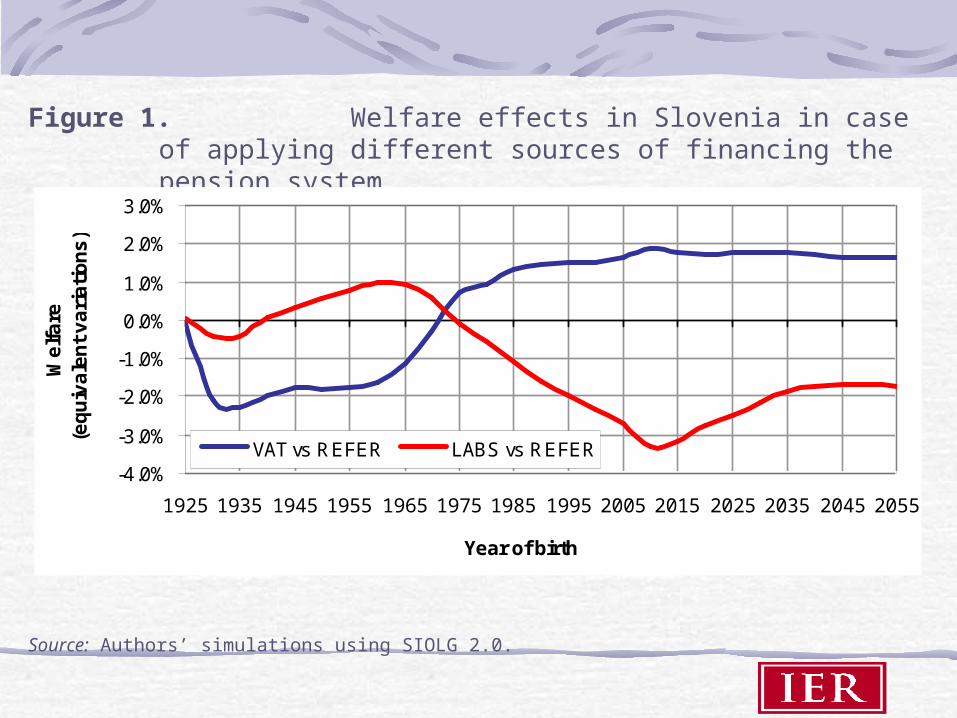

Figure 1. Welfare effects in Slovenia in case of applying different sources of financing the pension system

Source: Authors’ simulations using SIOLG 2.0.

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

1925 1935 1945 1955 1965 1975 1985 1995 2005 2015 2025 2035 2045 2055

Year of birth

We

lfa

re(e

qu

iva

len

t v

ari

ati

on

s)

VAT vs REFER LABS vs REFER

The Second Pension Pillar

Includes approximately 400.000 insured persons.

Low participation of employees from medium-sized and small enterprises.

Relatively underdeveloped system: low collected premia and low »profitability«.

Pension schemes can be individual or collective.

Tax reliefs are substantially more favourable with collective schemes: however, they are conditional on at least 51% participation of employees in an enterprise.

High administration costs.

Highly regulated system: required minimal rate of return amounts to 60% of yield on long-term government bonds.

Figure 2. Supplementary pension savings required in order to keep the total pension at the given level

Source: Authors’ simulations using SIOLG 2.0.

0%

5%

10%

15%

20%

25%

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Year of birth

Sup

plem

enta

ry p

ensi

on s

avin

gs(in

per

cen

t of n

et w

age)

Total pension at the 2005 level

Total pension at the 2000 level

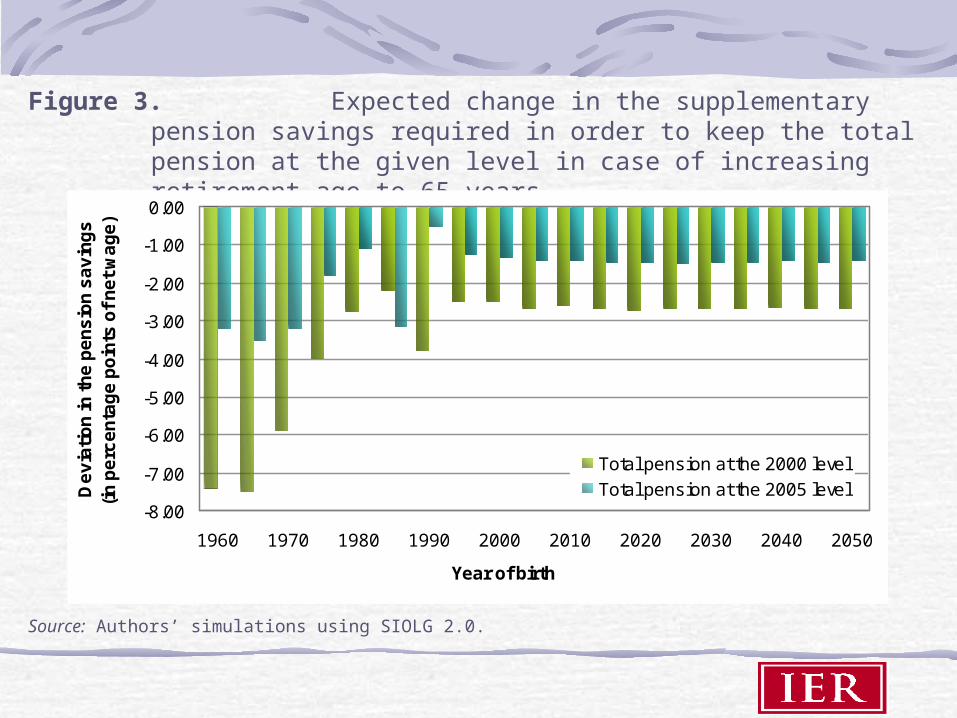

Figure 3. Expected change in the supplementary pension savings required in order to keep the total pension at the given level in case of increasing retirement age to 65 years

Source: Authors’ simulations using SIOLG 2.0.

-8.00

-7.00

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Year of birth

De

via

tio

n in

th

e p

en

sio

n s

av

ing

s(i

n p

erc

en

tag

e p

oin

ts o

f n

et

wa

ge

)

Total pension at the 2000 level

Total pension at the 2005 level

Figure 4. Expected change in the deficit of the Slovenian state pension fund in case of mandatory second pillar keeping the total pension at the 2000 level

Source: Authors’ simulations using SIOLG 2.0.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

De

via

tio

n in

th

e d

efi

cit

(in

pe

rce

nta

ge

po

ints

of

GD

P) REFER

VAT

LABS

Concluding RemarksImplementation of the pension reform not sufficient to compensate expected demographic developmentsThe level of expected deficit of the PAYG-financed state pension fund is worrying

Higher activity levels among elderly and changed indexation rule would substantially decrease state pension fund deficit

The volume of supplementary pension saving is insufficient at present to compensate the deterioration of rights from the first pension pillar (insufficient participation and too low premia)

8,5% of net wage savings for compensation of total effects of pension reform (5% for compensation of the pension legislation from 2005)

Increasing retirement age by one year reduces the additional second pillar savings by 0,4 percentage points