Stack of coins calculator economic growth powerpoint presentation slides.

Upload

muthannCategory

view

487download

0

Growth Theory

PD Dr. M. Pasche

DFG Research Training Group “The Economics of Innovative Change”,

Friedrich Schiller University Jena

Creative Commons by 3.0 license – 2008/2013 (except for included graphics from other sources)

Work in progress. Bug Report to: [email protected]

S.1

Outline:

1. The Empirical Picture of Growth

1.1 Some Stylized Facts1.2 Convergence1.3 Growth Accounting1.4 Regressions on Growth Determinants

2. Some Preliminaries of Growth Theory

2.1 The Harrod-Domar Approach2.2 The Basic Solow Model2.3 Exogenous Technological Change2.4 Intertemporal Optimization2.5 Analyzing Growth Equilibria

3. Models of Endogenous Growth

3.1 Overview: Sources of Growth3.2 AK model and Knowledge Spillovers3.3 Models with Human Capital Accumulation3.4 R&D based Growth with Increasing Product Variety3.5 R&D based Growth with Increasing Product Quality3.6 Technological Progress, Diffusion, and Human Capital3.7 Further Issues

S.2

4. Critique and an Evolutionary Perspective

4.1 Empirical Evidence4.2 Methodological Objections4.3 Evolutionary Approaches: Outline4.4 Evolutionary Approaches: Example

Basic Literature:

* Barro, R.J., Sala-i-Martin, X. (1995), Economic Growth. New York:McGraw-Hill.

* Aghion, P., Howitt, P. (2009), The Economics of Growth. MITPress.

Acemoglu, D. (2008), Introduction to Modern Economic Growth.Princeton University Press.

References to more specific literature can be found in the slide collection.

S.3

1. The Empirical Picture of Growth1.1 Some Stylized Facts

Literature:

Barro, R.E., Sala-i-Martin, X. (1995), Economic Growth.Chapter 1.1-1.2 (chapter 10-12 for a deep empirical analysis)

Kaldor, N. (1963), Capital Accumulation and Economic Growth, in:Lutz, F.A., Hague, D.C. (eds.), Proceedings of a Conference held bythe International Economics Association. London: Macmillan.

Mankiw, N.G., Romer, D., Weil, D.N. (1992), A Contribution to theEmpirics of Economic Growth. Quarterly Journal of Economics107(2), 407-437

Temple, J. (1999), The New Growth Evidence. Journal of EconomicLiterature 37(1), 112-156.

Symbols:

Y = A · F (K ,N) = real output or incomeK = capital stockN = employed laborA = total factor productivityr = real interest ratew = real wages

S.4

1. The Empirical Picture of Growth1.1 Some Stylized Facts

Income per capita y = Y /N is growing with a constant rate (butdeclining growth rate in the 1970ies in most developped countries).

The capital/output ratio (capital coefficient) K/Y is stationary.

The capital/labor ratio (capital intensity) K/N is increasing. This isjust an implication of a growing Y /N and a stationary K/Y .

The rate of return to capital r = ∂Y /∂K is stationary (but has acertain decline in developped countries).

The income distribution is stationary (measured by V = rk/wN orby wN/Y , rK/Y ).

The rate of return to labor w = ∂Y /∂N is increasing. This is justan implication of stationary distribution, stationary K/Y andgrowing Y /N.

The per capita growth rates differ much across countries.

The per capita growth rate cannot be explained solely byaccumulation of capital and growing labor force (→ technicalprogress, human capital, knowledge etc.).

S.5

1. The Empirical Picture of Growth1.1 Some Stylized Facts

A note on growth rates:

Growth with a constant rate g means that the variable growsexponentially:

y(t) = y(0)egt

Logarithm and differentiating with respect to time:

ln y(t) = ln y(0) + gt ⇒ gy ≡d ln y(t)

dt=

1

y·dy

dt= g

For empirical data we use the first differences ∆ ln y(t) todetermine the growth rate.

Growth with a constant rate means that we have a linear trend ofln y(t) in a figure with absolute scale, or, alternatively, a lineartrend of y(t) in a figure with a logarithmic scale.

S.6

1. The Empirical Picture of Growth1.1 Some Stylized Facts

Some illustrating empirical facts on growth dynamics:

From 500 (roman imperium) to 1500: no significant economicgrowth!

1500-1800 about 0.1% growth rate. Moderate growth rates during the industrial revolution

1800-1900, increasing in the late 19th century. Massive acceleration of economic activity in the 20th century,

especially in the post war period. Decline of growth rates (in developped countries) starting

from the 1970ies.

Some illustrating empiricial facts on distribution (base = 2002):

The richest country is Luxembourg with $ 49368 per capita,the poorest country is Kongo with $ 344 (= factor 143!)

If Bangladesh grows with its average post war growth rate of1.1% then it approaches the 2002 level of per capita incomeof the USA in 200 years. S.7

1. The Empirical Picture of Growth1.1 Some Stylized Facts

S.8

1. The Empirical Picture of Growth1.1 Some Stylized Facts

S.9

1. The Empirical Picture of Growth1.2 Convergence

Are less developped countries growing faster(“catching-up”)?

Measuring convergence:

β-convergence: Negative relationship between per capitaincome y = Y /N and growth rate gy .

σ-convergence: Decline of a dispersion measure (likestandard deviation of (logarithmic) per capita income, Ginicoefficient etc.)

S.10

1. The Empirical Picture of Growth1.2 Convergence

Problems:

To be comparable, per capita income has to measured withthe same unit (e.g. Dollar). Hence we have to multiply thevalues with the exchange rate.

The exchange rates are fluctuating and are determined byvariables which are not related to real income (i.e.non-fundamental expectations). Thus, the per capita incomemeasured in a foreign currency may change even if ther realoutput remains the same: distortion of the measure.

Moreover, we have eventually different inflation rates in thecountries. Since we can measure the nominal income and theinflation rate, we have to account for the different purchasingpower when expressing the income in a foreign currency.

Solution: Construcing “purchasing power parity” exchange rates(PPP) to express all values in Dollar (e.g. Penn World tables)

S.11

1. The Empirical Picture of Growth1.2 Convergence

General result: There is no overall β-convergence!(Penn World Tables, x-axis = y1960, y-axis = gy as φ 1960-1992)

S.12

1. The Empirical Picture of Growth1.2 Convergence

Average growth rate of per capita income in 1960-1985 vs. ln(y) in 1960; 117

countries.

S.13

1. The Empirical Picture of Growth1.2 Convergence

Specific results: There is β-convergence within a group ofcountries which are “similar” regarding properties like high humancapital endowment, stable political institutions etc.

⇒ conditional β-convergence

⇒ “convergence clubs”

⇒ the gap between “rich” and “poor” countries is growing.

S.14

1. The Empirical Picture of Growth1.2 Convergence

Frequency of per capita income classes; 117 countries.

In 1960: E [ln(y)] = 7.296,V [ln(y)] = 0.81275,V /E = 0.1114.

S.15

1. The Empirical Picture of Growth1.2 Convergence

Frequency of per capita income classes; 117 countries.

In 1985: E [ln(y)] = 7.7959,V [ln(y)] = 1.2126,V /E = 0.1555.

S.16

1. The Empirical Picture of Growth1.3 Growth Accounting

Literature:

Solow, R.M. (1957), Technical Change and the AggregateProduction Function. Review of Economics and Statistics 39,312-320.

We start from a stylized production function Y = A · F (K ,N), whereA = A(t) is a time-dependend function for the total factor productivity(e.g. A = exp(ηt)).

Y (t) = A(t) · F (K (t),N(t))

lnY (t) = lnA(t) + lnF (K (t),N(t))

Differentiating with respect to time:

gY = gA +FK K

F+

FNN

F

= gA +AFK

YK +

AFN

YN

S.17

1. The Empirical Picture of Growth1.3 Growth Accounting

gY = gA +AFK

YK +

AFN

YN

with AFK = r and AFN = w we have

= gA +rK

Y

K

K+

wN

Y

N

N

and with a linear homogenous production function

= gA + α(t)gK + (1− α(t))gN

This can be transformed into an estimation equation for (non-observable)gA in discrete time.

Measuring Y ,K ,N the growth contributions of the physical inputs K andN can be estimated. The part of output growth which cannot beexplained by K and N is the “residual” which is interpreted as technicalprogress = increase in the total factor productivity (Solow residual).

S.18

1. The Empirical Picture of Growth1.3 Growth Accounting

Measuring Y : usually real GDP (from national statisticsagency)

Measuring N: number of employed and self-employed people,or: time measure (work hours)

Measuring K : This is non-trivial since the accounting systemsmeasure gross investment and depreciation.

Depreciation depends on legal regulation and is only a roughproxy for physical depreciation.

In balance sheets the “capital” is evaluated according todifferent and changing legislation rules.

Perpetual Inventory Method:

Kt = Kt−1 + I grosst − δKt−1

with δ ∈ (0, 1) as the constant depreciation rate.

S.19

1. The Empirical Picture of Growth1.3 Growth Accounting

Results:

S.20

1. The Empirical Picture of Growth1.3 Growth Accounting

Some problems:

Measuring the capital stock (see above), in addition we needestimates about the utilization of the present capital stock.Generally, the estimation results are often not robust for changes inthe measurement concept.

All qualitative changes in capital as well as in labor are capturedindirectly in the TFP. However, much progress is embodied in thephysical inputs. It is reasonable to disaggregate the inputs toaccount for these effects, e.g. including human capital ordistinguishing groups of different skilled worker (with differentaverage wages), or distinguishing capital vintages.

The empirical validity of constant returns of scale and competitivefactor markets is questionable.

Growth is also affected by non-technical determinants like stabilityof political institutions, tax system, integration into global markets,protection of intellectual property rights etc. Hence, institutionalchange is captured as “technological” change.

S.21

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

Literature:

Mankiw, N.G., Romer, D., Weil, D.N. (1992), A Contributionto the Empirics of Economic Growth. Quiarterly Journal ofEconomics 107(2), 407-437

Barro, R.E., Sala-i-Martin, X. (1995), Economic Growth.Chapter 1.1-1.2 (and chapter 12)

Starting point is not a certain production function.

Instead: looking for resonable determinants/regressors

S.22

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

Example from Mankiw/Romer/Weil:

gyi = 3.04(3.66)

−0.289(4.66)

ln yi,1960+0.524(6.02)

ln si−0.505(1.75)

ln(ni+g+δ)+0.233(3.88)

SCHOOLi+ui

gyi per capita GDP in country i in 1960-1990yi,1960 per capita GDP in country i in 1960si saving rate (average 1960-1985)ni population growth rateSCHOOLi schooling rate (secondary school, average 1960-1985)g rate of technical progressδ depreciation rateui error term (iid)

Sample: 98 countries, t-values in brackets

Problems:

Endogenous regressors/multicollinearity

Model uncertainty

S.23

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

Some “stylized” facts from growth regressions:

* Significant positive impact of human capital(Barro, R.J. (1991), Economic Growth in a Cross Section of Countries.

Quarterly Journal of Economics 106(2), 407-443)

* Knowledge as a public good: positive impact(Caballero, R.J., Jaffe, A.B. (1993), How High are the Giants’ Shoulders:

An Empirical Assessment of Knowledge Spillovers and Creative

Destruction .... NBER Working Paper No. 4370)

Life expectancy, health: positive

Governmental consumption: negative

Political instability: negative;quality of political institutions: positive

S.24

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

Financial development (financial institutions): positive

Market distortions (like tariffs): negative

* Integration in global markets: positive(Balassa, B. (1986), Policy Responses to Exogenous Shocks in

Developping Countries. American Economic Review 76(2), 75-78.

etc. etc.

There are also a lot of ambigous/insignificant results.

S.25

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

Are high growth rates always “good”?

no information about income distribution and welfare

no information about welfare improving governemntalacrivities (health care, social insurance etc.) which may dampthe growth rates

environmental degradation and ressource exploitation

increasing “defensive expenditures”: a growing part of theincome is needed to compensate the negative impact ofgrowth on welfare.

S.26

1. The Empirical Picture of Growth

Role of Growth Theory:

Explanation of the stylized facts = explaining the economicmechanisms driving the economic activities, depending onexogenous variables.

Giving advice for growth policy (if there is any); notneccessarily in order to accelerate growth rates but to realize apareto-efficient growth path.

S.27

1. The Empirical Picture of Growth1.4 Regressions on Growth Determinants

An economic theory cannot include all reasonable determinantsand effects: Some variables (like Y and K ) are endogenouslydetermined, others (like N) are exogenous, others are not takeninto considration (like human capital in the standard Solow model).

The question is whether the primary source of growth (“growthengine”) is an endogenous part of the model or not:

“Old” growth theory, where technological progress as aprimary source of growth is exogenous.

“New” growth theory, where different types of technicalprogress are endogenously explained.

S.28

1. The Empirical Picture of Growth

Remarks:

The “old” growth theory is sometimes called “neoclassical” asopposed to the “new” endogenous growth theory. This ismisleading since the “new” models follow the neoclassicalparadigm in a more rigorous fashion (intertemporallyoptimizing representative agents, perfect (future) markets,Walrasian equilibrium).

“New” is not always superior (for a critical assessment see thelast section).

Non-mainstream theorizing like evolutionary or Post-Keynesiangrowth theory does not fit in the scheme of “old” and “new”.

S.29

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Literature:

Harrod, R.F. (1939), An Essay in Dynamic Theory. EconomicJournal 49, 14-33.

Domar, E. (1946), Capital Expansion, Rate of Growth, andEmployment. Econometrica 14, 137-250.

Common Features:

Tradition of Keynesian Macroeconomics; studying the incomeand capacity effects of investments

Linear-limitational production function:

Y = minσK , αL

with constant σ = 1/ν (σ = capital productivity, ν = capitalcoefficient) and a natural growth rate ∆L/L = n = gn

S.30

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

The Domar Growth Model:

Domar considers the income and the capacity effect of investment:

Income effect: Investments are part of the realized output(income) Yt .

Capacity effect: Investment augments the capital stock andtherefore enhance the production capacity Y p

t .

S.31

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Capacity effect: Realized investment have an effect on the potential output

according to the constant capital coefficient:

Kt = νY pt

∆Kt = Kt+1 − Kt = It = ν(Y pt+1 − Y p

t )

∆Y pt = Y p

t+1 − Y pt =

1

νIt (1)

Income effect: Constant saving ratio: St = sYt

Goods market equilibrium: It = St . It follows:

Yt =1

sIt

∆Yt = Yt+1 − Yt =1

s(It+1 − It) (2)

Yt = It (3)S.32

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Assume that additional capacity is utiized:

Then from (1) and (2) we have

∆Yt = Yt+1 − Yt = Y pt+1 − Y p

t = ∆Y pt

1

s(It+1 − It) =

1

νIt

It+1 − ItIt

= It =s

ν

and from (3) we have

Yt =s

ν= σs = gw

This could be called a “balanced growth rate”.

S.33

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Domar paradoxon:

Assume that real investment growth It > gw . Then thedemand Yt grows faster than the capacities Y p

t . That meansthat too large investment implies underutilization ofcapacities.

Assume that real investment growth It < gw . Then thedemand Yt grows slower than the capacities Y p

t . That meansthat too low investment implies overutilization of capacities.

S.34

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Equilibrium and natural growth rate:

Recall, that we have a linear-limitational production function.Then the growth rate of Y p

t is determined by the growth ofthe limiting factor!

The growth rate of labor is gn = n. It is very unlikely thatgn = gw . Note, that n, ν, s are exogenously given parameter.

If gw > gn then we have growing capacities that could not beutilized due to a scarcity of labor.

If gw < gn then the capacity grows slower than population.We have increasing unemployment.

S.35

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Assume a utilization factor

θ =Yt

Y pt

, θ ∈ [0, 1]

θ = Yt − Y pt

From the capacity effect we have

Y pt = σKt

Y pt = Kt =

ItKt

=sθY p

t

Kt

= sθσ

and hence

⇒ θ = I − sσθ

This growth rate of capacity utilization depends linearly on the degree ofcapacity utilization. A steady state solution θ = 0 leads to

θ∗ =Itsσ

< 1

in case of It = Yt < sσ = gw . S.36

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

If growth is lower than the “balanced growth rate” then theeconomy evolves into a stable steady state with underutilization ofproduction capacity which is not desirable.

θ

θ

θ∗

S.37

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

The Harrod Growth Model:

Harrod considers only the income effect of investment. Assumption of linear-limitational production function is not

neccessary. The constant capital coefficient plays a role in the

determination of investment behavior, i.e. ν is a behavioralparameter of the investment function (“accelerator”).

I = ν(Y e − Y )

with Y e as the expected demand. With the saving function asgiven above and I = S we have

I = S = sY = ν(Y e − Y )

⇒Y e − Y

Y=

s

ν= ge (4)

with ge as the expected (“warranted”) growth rate.

S.38

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

If the realized and the expected (constant) growth rate areequal (g = ge) then we have equilibrium growth: The realizedgrowth of Y leads to a growth of S = I which conforms theexpectations of the investors.

Problem: What happens if realized and expected/warrantedgrowth rate differs?

S.39

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

If the realized growth rate is larger, g > ge , then the investorscorrect their expectations Y e upwards and invest more. Dueto the income effect this fosters the growth rate: Theeconomy diverges from the balanced growth path.

If the realized growth rate is lower, g < ge , then theexpectations are corrected downwards, this lowers the realizedgrowth rate: The economy also diverges from the balancedgrowth path.

The equilibrium growth path is dynamically unstable!(“growth on a knife edge”)

S.40

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

t

logYt

S.41

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Analytical description:

Define:

gt ≡Yt − Yt−1

Yt(5)

g et ≡

Y et − Yt−1

Y et

(6)

Solving (6) to Yt−1 and employing into (5) yields

gt =Yt − (Y e

t − g et Y

et )

Yt

= 1− (1− g et )

Y et

Yt(7)

Recall that from (4) and (6) we have

Y et − Yt

s/ν= Yt ,

Y et − Yt

g et

= Y et

S.42

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Enployng these expressions into (7) we have

gt = 1−(1− g e

t )

g et

s

ν(8)

Now assume adaptive expectations:

g et+1 = g e

t + α(gt − g et ), α ∈ (0, 1) (9)

Employing (8) for gt we have

g et+1 − g e

t = α1− g e

t

g et

(

g et −

s

ν

)

Obviously, we are on a balanced growth path, when gt = g et = s/ν.

S.43

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

With g et < s/ν we have g e

t−1 − g et < 0,

i.e. growth expectations becomes more and more pessimistic,inducing a growing (negative) deviation from the balancedgrowth path.

With g et > s/ν we have g e

t−1 − g et > 0,

i.e. growth expectations becomes more and more optimistic,inducing a growing (positive) deviation from the balancedgrowth path.

S.44

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

g et

sν

g et+1 − g e

t

S.45

2. Some Preliminaries of Growth Theory2.1 The Harrod-Domar Approach

Some problems:

The empirical findings contradict Harrod’s result of a “knifeedge” growth path.

The stable growth with underutilization of capacitiesaccording to Domar does not take into account that in thelong run labor and physical capital should be regarded assubstitutional rather than complementary factors.

⇒ From Keynesian to Neoclassical Growth Theory: Solow Model.

S.46

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Literature: Solow, R.M. (1956), A Contribution to the Theory of Economic

Growth. Quarterly Journal of Economics 70, 65–94. Swan, T.W. (1956), Economic Growth and Capital Accumulation.

Economic Record 32, 334-361.

Assumptions: Closed economy without government. Identical profit-maximizing firms are producing a homogenous good

Y which can either be consumed or invested Y = C + I gross . Perfect competition on goods and factor markets, full-employment,

flexible factor prices according to their marginal return, the goodsprice index is normalized to one.

Labor supply A (and due to full employment also the demand forlabor N) is growing with the rate n:

gA =A

A= gN = n

S.47

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

There is no investment function. Since we have goods marketequilibrium, it is always I = S . By definition we have

K = I = I gross − δK , δ ∈ (0, 1) depreciation rate

There is a production technology Y = F (K ,N) with thefollowing properties:

FK ,FN > 0,FKK ,FNN < 0,FKN > 0 Linear homogeneity: λY = F (λK , λN).

Then the output per capita can be expressed by

y =Y

N= F

(K

N, 1

)

≡ f (k)

with k = K/N, fk > 0, fkk < 0. Inada conditions: limk→0 f (k) = 0, limk→∞ f (k) = ∞,

limk→0 fk(k) = ∞, limk→∞ fk(k) = 0

Constant savings: S = Y − C = sY , s ∈ (0, 1)

S.48

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Derivation of the dynamic equation:

From derivation of k with respect to time we have (quotient rule)

k =K

N− nk

From Y = C + I gross = C + I + δK = C + K + δK we have

K = Y − C − δK

Inserting K into k (with y = Y /N = f (k)) we have

k =Y − C − δK

N− nk

⇒ k = sf (k)− (n + δ)k (10)

For the per capita income we have

y = f (k(t))

y = fk k = fk(sf (k)− (n + δ)k) (11)S.49

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

k

kk∗

k

f (k)

sf (k)

(n + δ)k

S.50

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

The steady state k∗ is defined as an equilibrium where all valuesare growing with a constant rate (and all per capita values areconstant).

Steady state condition k = 0 leads to

sf (k∗) = (n + δ)k∗ (12)

Since k = KN

doesn’t change in time, we have gK = gN = n anddue to linear homogeneity we have also gY = n. Hence the percapita output y = Y /N is constant in steady state (as it can alsoseen directly in (11)).

S.51

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Existence and uniqueness of the equilibrium:

The linear function (n + δ)k is starting in the origin and has apositive finite slope (n + δ).

Due to the Inada condition the saving function sf (k) alsostarts in the origin but has an infinite slope near to the origin.With k → ∞ the slope of the saving function decreases tozero. Both functions are monotonously increasing.

Hence there must exist a unique intersection point with thelinear function (n + δ)k .

S.52

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Stability of the equilibrium:

The equilibrium is stable if dk(k∗)/dk < 0:

dk(k∗)

dk= sfk − (n + δ)

Inserting the steady state condition (12)

= sfk − ssf (k)

k< 0

⇒ fk <f (k)

k

This is ensured by the concavity of the function (see assumptionfk > 0, fkk < 0) [gradient inequality condition].

S.53

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Compatible with stylized facts?

Growing y = Y /N cannot be explained without technicalprogress!

Growing capital/labor ratio k = K/N cannot be explained.

Constant ratio K/Y is compatible with the model.

Constant income distribution is compatible with the model.

In a transient phase (before approaching the steady state) weshould observe growing per capita income, growing K/N, andβ-convergence, but a changing income distribution.

S.54

2. Some Preliminaries of Growth Theory2.2 The Basic Solow Model

Convergence:

For an economy which has not yet reached the steady state equilibriumwe can calculate the per capita growth rate from (11):

gy =y

y=

fky(sf (k)− (n + δk))︸ ︷︷ ︸

k

> 0

This is positive as long k < k∗ ⇐⇒ k > 0 (before reaching the steadystate). The dependency of gy from k is negative:

dgydk

=fkk

f (y)2((sf (k)− (n + δ)k)︸ ︷︷ ︸

k

f (k)− fk(n + δ) (f (k)− kfk))︸ ︷︷ ︸

>0

< 0

This inequality holds true since k > 0 because ykk < 0. Furthermore fk isthe return to capital and hence kfk is the capital income per capita. Thusf (k)− kfk is the (positive) labor income.

As a result the growth rate gy is high for a low k and vice versa. This

implies unconditional β-convergence!S.55

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

In a widely used form technical progress enters the productionfunction by enhancing the total factor productivity A:

Y = A · F (K ,N)

In the “old” growth theory the sources and economicmechanisms driving the technical progress are not part of themodel.

Technical progress (TP) is modeled as an exogenouslydetermined process A(t) = A(0)eγt .

S.56

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

TP – Hicks concept:

TP affects the productivity of both, capital and labor. Theproductivity growth has the same impact on the output likean augmentation of both input factors.

As the growth of (marginal) productivity affects both factorsuniformly, the TP does not affect the relation between factorprices (wages, interest rate)!

TP is called Hicks-neutral, if the income distributionV = rK/wN remains unchanged. Since TP does not changethe ratio r/w this implies that capital intensity K/N does alsonot change.

TP is called Hicks-labor augmenting if K/N and V increase,and it is called capital-augmenting if K/N and V decrease.

S.57

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

N

K

Yt

Y TPt

tanα = K/N

V = tanαtan β = rK

wN

tanβ = w/r

S.58

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Growth rates in case of Hick-neutral TP and a linearhomogenous Cobb-Douglas production function:

TP is measured by an efficiency factor η(t) = η(0)eγt (withη(0) = 1) which is multiplied with capital and labor

Y = F (ηK , ηN) = (ηK )α(ηN)1−α

= ηKαN1−α = eγtKαN1−α

lnY = γt + α lnK + (1− α) lnN

gY = γ + αgK + (1− α)gN

Since Hicks-neutrality implies gK = gN

gY = γ + gN

S.59

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Compatibility with stylized facts?

Per capita income grows with the positive rategy = gY − gN = γ.

Income distrbution is constant.

The constant capital intensity K/N does not conform stylizedfacts!

With gY > gN = gK the capital coefficient K/Y declines.This does not conform the stylized facts!

An increasing capital intensity K/N would require Hicks laboraugmenting TP. Unfortunately, then we would have a trend inincome distribution which contradicts the stylzed fact.Furthermore, the decline of the capital coefficient would be stillconflict with the stylized facts.

S.60

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

TP – Harrod concept:

TP affects the productivity of labor. The (marginal)productivity of labor increases and hence the ratio of factorprices r/w decreases due to TP.

TP is called Harrod-neutral if the income distributionV = rK/wN remains unchanged. Since r/w decreases, K/Nmust increase with the same rate. Furthermore,Harrod-neutrality implies a constant capital coefficient K/Y .

Harrod-capital or labor augmenting TP could also be definedbut are of minor interest in this context.

S.61

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

N

K

Yt

Y TPt

V = tanαtan β = tanα′

tanβ′= rK

wN

tanβtanα tanβ′

tanα′

S.62

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Growth rates in case of Harrod-neutral TP and a linearhomogenous Cobb-Douglas production function:

TP is measured by an efficiency factor η(t) = η(0)eγt (andη(0) = 1) which is multiplied with labor

Y = F (K , ηN) = Kα(ηN)1−α

= η1−αKαN1−α = e(1−α)γtKαN1−α

lnY = (1− α)γt + α lnK + (1− α) lnN

gY = (1− α)γ + αgK + (1− α)gN

Since Harrod-neutrality implies gK = gY

gY = (1− α)γ + αgY + (1− α)gN

(1− α)gY = (1− α)γ + (1− α)gN

gY = γ + gN

(the same result as in case of Hicks-neutral TP).S.63

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Compatibility with a steady state:

Obviously, a steady state cannot be defined as an equilibriumwhere all per capita values are constant. It is more generallydefined as an equilibrium, where all per capita values growwith a constant rate (in case of the standard Solow model:zero).

From the Solow model we have the steady state condition:

k

k= s

f (k , η)

k− (n + δ) = const (= γ)

Since s, n, δ are constant, this condition holds true only iff (k , η)/k = Y /K is also constant which requiresHarrod-neutral technical progress.

As we have seen, it is gY = n + γ. From Harrod-neutrality itfollows gY = gK = n + γ and hence gk = k/k = γ.

S.64

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Compatibility with stylized facts?

Per capita income grows with the positive rategy = gY − gN = γ.

Income distrbution is constant.

Increasing capital intensity K/N since gK = gY > gN .

Constant capital coefficient K/Y .

⇒ most stylized facts are compatible with Harrod-neutral TP.

S.65

2. Some Preliminaries of Growth Theory2.3 Exogenous Technological Change

Remarks:

In practice it is not possible to discriminate which part ofoutput growth is due to capital or due to labor augmentingTP.

If we interpret growing output as a result of inreased laborproductivity and therefore increase real wages and hence w/r(e.g. as a result of “productivity-oriented wage policy”) thenwe treat TP as if it is Harrod-neutral.

It is unsatisfactory that the TP itself is not explained, i.e. TPis not generated by economic activity which requires someressource input.

S.66

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

In the standard Solow model, the saving rate s is assumed tobe exogenously given, i.e. the households do not maximizetheir utility (problem of missing “microfoundation”).

In a first step, we determine the optimal saving rate in asimple comparative-static framework :

Households maximize their utility from per capitaconsumption in the steady state. Since the utility function isunique up to positive-affin transformation, we could maximizethe per capita consumption in steady state, instead.

S.67

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

From the steady state condition (k = k∗(s)) we have

sf (k) = (n + δ)k (13)

⇒ f (k)− c = (n + δ)k

maxs

c = f (k)− (n + δ)k

⇒dc

ds=

dk

ds(fk − (n + δ)) = 0 (FOC)

Dividing by dk/ds and inserting the condition (13) yields

fk =sf (k)

k

⇒ s = fk ·k

f (k)(14)

which is known as the “golden rule” of optimal growth.S.68

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

k

f (k)

(n + δ)k

k∗

sf (k)

C/Y

⇒ fk = (n + δ)

S.69

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Assumptions for intertemporal maximization:

Arrow-Debreu economy: There exist complete (future) markets for all goods. The representative agents (household, firm) are perfectly

informed about all present and future prices. In each t it is possible to arbitrage goods between all present

and future markets. Perfect competition on all present and future goods and factor

markets (implying compensation by marginal product). There are no externalities or other market imperfections

(otherwise intertemporal optimization is possible but yieldspareto-inferior outomes).

Households maximize the net present value of the utility flowfrom consumption according to an intertemporal budgetconstraint.

S.70

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Firms are maximizing their profits, they are price-takers ongoods and factor markets. They produce the homogenousgood Y with constant returns to scale.

Since all present and future markets are in equilibrium, wehave an equilibrium path of goods price, wages and interestrates.

It is sufficient in case of perfect foresight that all optimalplans are contracted in t = 0. Afterwards there is no need torevise any decision (markets are open in t = 0, afterwards thecontracts are executed for all t).

If there are stochastic elemets (like technical progress oruncertainty about the outcome of an R&D process) then wehave no perfect foresight, and the model has to operate withrational expectations. Agents will immediately adapt theirplans to the stochastic shocks.

S.71

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Introduction into Intertemporal Optimization

The representative agent has a control variable c(t). Thedecision about consumption implies a decision about savingsan hence capital accumulation.

The state of the economy is represented by a state variablek(t).

In each time the present value of the utility (objective) isgiven by v(c(t), k(t), t).

A typical example is v(c(t), k(t), t) = e−ρtu(c(t))with ρ > 0 as the time preference.

S.72

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

The agent’s goal in t = 0 is to maximize the present value:

Finite time horizon:

∫ T

0v(c(t), k(t), t)dt

Infinite time horizon:

∫ ∞

0v(c(t), k(t), t)dt

which requires that utility is additive-separable in time.

Maximization under the constraint that the state variabledevelops according to a differential equation (“law of motion”,transition equation):

k = g(k(t), c(t), t)

A typical example is k = f (k(t))− c(t)− δk(t).

Of course, for the state variable we have to define the initialvalue: k(0) = k0 > 0.

S.73

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

We need a condition about the value of k at the end of thetime horizon: Typically,

Finite time horizon: k(T )e−r(T )T ≥ 0

Infinite time horizon: limt→∞

k(t)e−r(t)t ≥ 0

where r(t) ∈ (0, 1) is the average discount rate, defined as

r(t) =1

t

∫ t

0r(v)dv

This means that the present value of the state variable shouldbe non-negative at the end of the planning horizon. Usually,the discount rate is the net interest rate = fk(k(t))− δ.

S.74

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

The complete problem:

maxc(t)

∫ T

0v(c(t), k(t), t)dt

subject to k(t) = g(k(t), c(t), t)

k(0) = k0 > 0 given

k(T )e−r(T )T ≥ 0

or for an infinite time horizon:

maxc(t)

∫ ∞

0v(c(t), k(t), t)dt

subject to k(t) = g(k(t), c(t), t)

k(0) = k0 > 0 given

limt→∞

k(t)e−r(t)t ≥ 0

S.75

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

For solving this problem we build the Hamiltonian function:

H(c(t), k(t), t, µ(t)) = v(c(t), k(t), t) + µ(t)g(c(t), k(t), t)

where µ(t) is a Lagrangian multiplier for each t.

[This expression could be derived from principles of optimizationtheory which is not part of the course.]

S.76

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Economic interpretation of the multiplier:

In each t the agent consumes c(t) and owns k(t).

Both affects the utility: Choice of consumption (and eventually k(t)) enters directly

the utility function Choice of consumption affects the savings and hence the

development of k(t) according to the law of motion. Thisaffects the future output/income and hence futureconsumption and therefore the present value of utility.

The multiplier µ(t) is therefore a shadow price (oropportunity cost) of a unit of capital in t expressed in units ofutility at time t = 0.

For a given value of µ(t) the Hamiltonian expresses the totalcontribution of the choice of c(t) to present utility.

S.77

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Solution of the problem:

Let c∗(t) a solution (time path) of the optimization problem, andk∗(t) is the associated time path of the state variable. Then thereexists a function µ∗(t) (so-called costate variable) so that for all tfollowing statements hold true:

a) First order condition (FOC):

∂H

∂c(t)= 0

b) Canonical equations (CE):

∂H

∂µ(t)= g(c(t), k(t), t) = k(t)

−∂H

∂k(t)= µ(t)

The latter is the law of motion for the shadow price.S.78

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

c) Transversality condition (TC):

µ(T )k(T ) = 0

This means that if the inequality restriction of the problem isnot binding = the final state variable k(T ) has a positivevalue, then its shadow price must be zero. Otherwise theagent would leave a positive capital stock unused which couldcontribute positively to the present utility. Hence, the TC isan dynamic efficiency condition!

In case of an infinite time horizon the transversality conditionreads

limt→∞

µ(t)k(t) = 0

[We do not discuss the case of non-discounting which requiresanother type of TC; see Barro/Sala-i-Martin, appendix 1.3 fordetails,]

S.79

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

How to proceed (this will be demonstrated by an example):

From the FOC and the CE we obtain differential equations forstate variable k and the costate variable µ.

Since the FOC relates c to µ it is possible to eliminate µ andto derive a differential equation for c instead (the“Keynes-Ramsey rule”).

Both differential equations c and k have steady state (c∗, k∗)where k = c = 0.

Depending on the initial conditions, it is usually not clearwhether the system converges to the steady state(“saddle-point equilibrium”). Since the initial conditions arechosen by the optimizing agents, they will choose c(0) (for agiven k(0)) which is consistent with the FOC, CE and thetransversality condition. This ensures that the system will beon a stable path to the steady state.

S.80

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

An example: Cass-Koopman-Ramsey Model

Cass, D. (1965), Optimum Growth in an Aggregate Model ofCapital Accumulation. Review of Economic Studies 32 (3),233–240.

Koopmans, T.C. (1965), On the Concept of Optimal Growth.In: The Econometric Approach to Development Planning,225–287, North–Holland, Amsterdam.

The basic idea is to provide a microfoundadtion for the neoclassicalSolow model by assuming an intertemporal maximizing household.

It is assumed that the assumptions of the standard Solow modelhold true (with except for the constant consumption/saving ratewhich will be replaced by c(t)).

S.81

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

a) The household:

The household has a time-separable utility function u(c) withuc > 0, ucc < 0 (1. Gossen Law). He maximizes

maxc

U(0) =

∫∞

0

u(c)e−ρtentdt =

∫∞

0

u(c)e−(ρ−n)tdt

subject to k = w + rk − (n + δ)k − c

k(0) > 0

where w is the wage, r the interest rate. Therefore w + rk is the percapita income from labor and holding an individual capital stock.Subtracting consumption, w − rk − c is the (gross) saving percapita which increases the capital stock. However, depreciation δand the growth of the population diminishes the capital per capita.

In the objective function, ρ is the time-preference rate. Therepresentative household has to take into account that the“members” of the household grow with the rate n. We must assumeρ > n, otherwise the integral diverges.

S.82

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Solution:

The Hamiltonian is

H(c , k , t, µ) = u(c)e−(ρ−n)t + µ · (w + rk − (n + δ)k − c)

The conditions for an optimum are

∂H

∂c= uc(c)e

−(ρ−n)t − µ = 0 (15)

−∂H

∂k= −(r − n − δ)µ = µ (16)

∂H

∂µ= w + rk − (n + δ)k − c = k (17)

S.83

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

Differentiating (15) with respect to time

ucc(c)ce−(ρ−n)t − (ρ− n)uc(c)e

−(ρ−n)t = µ

Substituting µ (r.h.s.) by condition (16):

ucc(c)ce−(ρ−n)t − (ρ− n)uc(c)e

−(ρ−n)t = −(r − n − δ)µ

Substituting µ by condition (15) finally eliminates µ:

ucc(c)ce−(ρ−n)t − (ρ− n)uc(c)e

−(ρ−n)t = −(r − n − δ)uc(c)e−(ρ−n)t

Dividing by e−(ρ−n)t and rearranging leads to

ucc(c)c = uc(c)(r − (ρ+ δ))

Dividing by ucc(c)c yields the Keynes-Ramsey rule:

gc =c

c= −

uc(c)

ucc(c) · c︸ ︷︷ ︸

σ

(r − ρ− δ)

S.84

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

The expression −uc/(ucc · c) = σ is the intertemporalelasticity of substitution of the utility function.

In many growth models it is assumed that the utilitiy functionis isoelastic (constant σ). Examples:

u(c) =c1−θ − 1

1− θ, θ > 0, σ = 1/θ

u(c) = log(c) (σ = 1)

The Keynes-Ramsey rule implies that we have a positivegrowth rate for the per capita consumption as long as the netreturn to capital r − δ exceeds the timepreference rate ρ.Since there are decreasing returns to capital and hence adecreasing r the growth rates will also decrease until the pathapproaches the steady state.

S.85

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

b) The Firm:

The representative firm is a price taker (price level isnormalized to 1) and maximizes its period profit:

maxK ,N

π(t) = N(t) · [f (k(t))− r(t)k(t)− w(t)]

From the first order conditions we have

r(t) = fk(k(t))

w(t) = f (k(t))− fk(k(t))k(t)

In the optimum there are zero profits and the factors arecompensated by their marginal product.

Alternatively, the firm’s objective could also be seen inmaximizing the firm’s present value (net present value of theproft flow).

S.86

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

c) Market equilibrium:In equilibrium all produced goods are demanded either asconsumption or as investment goods:

y = f (k) = k + (n + δ)k + c

Summing up, the optimization behavior of households and firmsleads to a two-dimensional system of differential equations(Keynes-Ramsey rule, intertemporal budget restriction):

c = −uc(c)

ucc(c)(fk(k)− (ρ+ δ)) (18)

k = f (k)− (n + δ)k − c (19)

S.87

2. Some Preliminaries of Growth Theory2.4 Intertemporal Optimization

All time paths c(t)∞t=0 and k(t)∞t=0 generated by this system mustadditionally obey the transversality condition

limt→∞

µ(t)k(t) = 0

From (16) we have (note that r = r(t))

µ

µ= −(r − n − δ)

⇒ µ(t) = µ(0)e−(r(t)−n−δ)t

and from (15) we have for t = 0

µ(0) = uc(c)e−(ρ−n)0 = uc(c)

hence the transversality condition reads

limt→∞

uc(c)k(t)e−(r(t)−n−δ)t = 0

Obviously, this requires that average net return of capital exceeds the

growth rate of population: r(t)− δ > n.S.88

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Each growth model with intertemporal optimization yields asystem of differential equations – e.g. the law of motion forthe per capita capital stock (k) and the Keynes-Ramsey rulefor the development of the per capita consumption (c).Furthermore, the transversality condition must hold true.

We are interested in the steady state = fixpoint of thedynamic system

existence of a (non-trivial) steady state stability of the steady state

The analysis is demonstrated by the example of theCass-Koopman-Ramsey model.

S.89

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

The Cass-Koopman-Ramsey model has three fixpoints:

(a) c∗ = k∗ = 0. This is the trivial solution will not be discussed

(b) c∗ = 0, k∗ = k with f (k) = (n + δ)k . In this case the outputis used only to maintain the capital stock, there is noconsumption. This contradicts the TVC.

(c) c∗, k∗ as the solution of c = k = 0.

Equalizing (18) and (19) with zero yields the steady state

fk(k∗) = ρ+ δ (20)

c∗ = f (k∗)− (n + δ)k∗ (21)

In equilibrium the net return to capital equals the time preferncerate, and the per capita savings maintain the equilibrium capitalstock.

S.90

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Graphical reresentation:

Phase diagramm: (k , c)-space, each point (vector) is acertain state of the model. The dynamic equations determinehow this state evolves in time. For a marginal time step thiscould be represented by a vectorfield in the (k , c)-space.

Trajectory: Time path of (k(t), c(t)) starting from anyinitial value.

Isocline: The implicit function of all (k , c)-combinationswhere c = 0 or k = 0. The intersection point of both isoclinesis the steady state.

S.91

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

k

c = 0

k = 0

k∗ k

c∗

c

S.92

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

The isoclines k = 0 separates the regions with k > 0 andk < 0 (and analogous for c).

We have

∂c

∂k= −

uc(c)

ucc(c)fkk < 0

∂k

∂c= −1 < 0

Hence, we obtain the arrow directions of the vector field forthe development of an arbitrary trajectory.

We see the trivial solution c∗ = 0, k∗ = 0 as well as theTVC-violating solution c∗, k∗ = k in the diagramm.

Since the isoclines have a unique intersection point (steadystate) which is a “saddle point”.

S.93

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Since we assumed ρ > n the steady state consumption is lower than inthe golden rule due to time preference.

k

c = 0

k = 0

k∗ k

c∗

c

k

f (k)

(n + δ)k

S.94

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Stability of the steady state:

[A detailed introduction into the analysis of dynamical systems isprovided by the course “Economic Dynamics” by Prof. Lorenz!]

The standard analysis of stability is based on linear systems.Therefore, we linearize the nonlinear Cass-Koopman-Ramsey modelaround the steady state. This is a Taylor approximation (1. degree)of the original system at (c∗, k∗).

[kc

]

=

[∂k/∂k ∂k/∂c∂c/∂k ∂c/∂c

]

·

[k − k∗

c − c∗

]

S.95

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

From (19) and (20) we have

∂k

∂k= fk(k

∗)− (n + δ) = (ρ+ δ)− (n + δ) = ρ− n > 0

Furthermore,

∂k

∂c= −1 < 0

∂c

∂k= −

uc(c∗)

ucc(c∗)· fkk(k

∗) < 0

∂c

∂c=

[ucc(c∗)]2 − uccc(c

∗) · uc(c)

[ucc(c∗)]2· [fk(k

∗)− (ρ+ δ)]︸ ︷︷ ︸

=0, see (20)

= 0

Thus we have[kc

]

=

[

ρ− n −1

− uc (c∗)ucc(c∗)

· fkk(k∗) 0

]

︸ ︷︷ ︸

J

·

[k − k∗

c − c∗

]

S.96

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

The determinant of the Jacobian matrix J is

det J = −uc(c

∗)

ucc(c∗)· fkk(k

∗) < 0

The characteristic polynom is

λ2 − (ρ− n)λ+ det J

with the roots (eigenvalues)

λ1,2 =ρ− n

2±

1

2

√

(ρ− n)2 − 4 det J

Since the determinant det J is negative the square-root is takenfrom a positive term (real valued ⇒ non-cyclical behavior) and wehave two different real-valued roots.

S.97

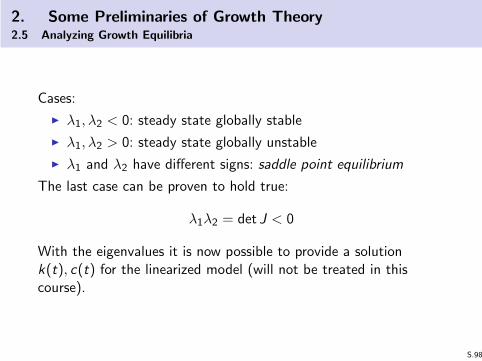

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Cases:

λ1, λ2 < 0: steady state globally stable

λ1, λ2 > 0: steady state globally unstable

λ1 and λ2 have different signs: saddle point equilibrium

The last case can be proven to hold true:

λ1λ2 = det J < 0

With the eigenvalues it is now possible to provide a solutionk(t), c(t) for the linearized model (will not be treated in thiscourse).

S.98

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Consequence of saddle-point stability:

In the intertemporal maximization problem we have an initial valuek(0) > 0. To determine a starting point we need a value c(0). Asthe vector field shows, an in-appropriate choice of c(0) will let thetrajectory diverge from equilibrium!

From the solution of the linearized model it can be seen that forevery given k(0) there exists one specific c(0)∗ which leads thetrajectory along the saddle path to the steady state.

The transitory dynamic in case of c(0) 6= c(0)∗ are depicted in thefollowing graphic by the thin dashed lines (example). The transitorydanmic for c(0) = c(0)∗ is depicted by the bold dashed line.

A choice of the initial c(0) 6= c(0)∗ either contradicts theKeynes-Ramsey rule or it contradicts the transversality condition.By rationality assumption, the representative agent will henceproperly choose c(0)∗ and therefore the saddle-point stability of thesteady state is ensured.

S.99

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

stable saddle−pathc=0

k=0

k

c

(with f (k) = k0.6, u(c) = log(c), (n + δ) = (ρ+ δ) = 0.2)

S.100

2. Some Preliminaries of Growth Theory2.5 Analyzing Growth Equilibria

Further properties of the Cass-Koopman-Ramsey model(details see Barro/Sala-i-Martin, chapter 2)

Pareto-Optimality: Sinde the markets are perfect and there are noexternalities, the intertemporal decisions and hence the growth path ofthe model is pareto-optimal. Due to the time preference rate the savingration in the steady state is below the “golden rule” in the StandardSolow model.

Transitory dynamics: The saddle point stability of the steady stateimplies a certain policy function c(k), i.e. for each k the policy functionensures that the economy is on the saddle path to the steady state. Itdescribes the transitory dynamnics on the saddle path. c(k(t)) could becomputed numerically by approximation technologies.

Convergence:Compared to the Solow model the saving rate is nowendogenously determined but we have to additional stratcturalparameters: intertemporal elasticity of substitution σ and time preferencerate ρ. These parameters shape the rate of convergence but the Solowresults for β- and σ-convergence also hold true for the CKR- model.

Policy implications: Policy may change preference parameters (taxinghousehold income andb governmental expenditures = changing the savingratio). This affects only the per capita income level, not the growth rate! S.101

3. Models of Endogenous Growth3.1 Overview: Sources of Growth

In the “neoclassical” growth theory (Solow,Cass-Koopman-Ramsey) we have no steady state growthneither of per capita income nor of labor productivity.

Extending these models with Harrod-neutral technologicalprogress lacks an explanation of such a progress. Progresstakes place without any economic activities and withoutspending ressources (opportunity cost) to promote thisprogress.

Technically spoken, the absence of steady state of per capitagrowth is a result from decreasing returns of capital. In atransitory phase we have an incentive to accumulate capitalbut with decreasing r = fk(k) (Inada conditions) the percapita growth rates diminish and fall to zero in the steadystate (see Keynes-Ramsey rule).

S.102

3. Models of Endogenous Growth3.1 Overview: Sources of Growth

Solution: Y = K · N1−α?

Increasing returns of scale: not compatible with perfectcompetition, no factor compensation according marginalproductivity, Euler theorem not valid!

⇒ No solution!

Looking for models...

with non-diminishing returns of capital

which are compatible with perfect competition (ormonopolistic competition)

with endogenous explanation for technological progress

with policy advice

S.103

3. Models of Endogenous Growth3.1 Overview: Sources of Growth

Some sources of endogenous growth

a) (Technical) Knowledge: may be embodied in humans (→ human capital) or

disembodied (“blue prints”, knowledge stock) in case of disembodied knowledge: non-rival in use,

(non-) disclosure regulated by intellectual property rights (patents) high firm specifity limited absorbability

to the extent where we have disclosure and free access toknowledge there are positive spillover effects (externalities)

externalities imply that the price system is incomplete andmarket based allocation is pareto-inferior

to the extent of non-disclosure there is a private return fromproducing knowledge and hence an incentive for R&D

increasing knowledge regarding new products (variety approaches) higher product quality (quality approaches) production efficiency

S.104

3. Models of Endogenous Growth3.1 Overview: Sources of Growth

b) Human Capital:

skills and specific knowledge of human beings rival in use, excludability ⇒ private good with a positive return

⇒ incenive to invest into HC. Accumulation of HC by

learning by doing by schooling (investment)

Not all effects of HC may be appropriatable, positiveexternalities possible

one-sector versus two-sector models

S.105

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Literature:

King, R.G., Rebelo, S. (1990), Public Policy and EconomicGrowth: Developing Neoclassical Implications. Journal ofPolitical Economy 98 (5), S126–S150.

Rebelo, S. (1991), Long–Run Policy Analysis and Long–RunGrowth. Journal of Political Economy 99, 500–521.

Barro/Sala-i-Martin (chapter 4.1)

In all models of endogenous growth we assume n = 0, i.e. there isno population growth!

S.106

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

a) Households maximize:

maxc

U(0) =

∫ ∞

0u(c(t))e−ρtdt (22)

conditional to k = f (k)− δk − c

k(0) > 0

and furthermore the TVC holds true:

limt→∞

[µ(t)k(t)] = 0

The solution leads to the Keynes-Ramsey rule

gc = σ(r(t)− (ρ+ δ))

where σ is assumed to be constant.S.107

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

b) Firms produce the output only with capital (constant laborforce is neglected here). Capital includes physical as well as humancapital (“broad measure of capital”, Romer (1989))

y = Ak , A > 0

Hence we have r = fk(k) = A for all t (non-diminishing retuirns ofcapital).

The Keynes-Ramsey rule thus reads

gc = σ(A− ρ− δ)

and gc > 0 if net return to capital A− δ exceeds the timepreference rate ρ.

S.108

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

All values are growing with a constant steady state rate

gy = gc = gk = σ(A− δ − ρ)

Observe that the Keynes-Ramsey rule implies a time-independentgrowth rate for c(t) (and henceforth for k(t)). Therefore there isno transitory dynamic! If TVC holds true, the model starts int = 0 in the steady state, i.e. for a given k(0) the initial c(0) isdetermined.

S.109

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Convergence:

Since there is no transitory dynamic, there is no “catchingup”.

Similar countries (technology, time preference, intertemporalelasticity of substitution) grow with the same rate.

Growth rate differences have to be explained by differentstructural parameters.

S.110

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

How to justifiy such an AK technology?

Arrow, Kenneth J. (1962), The Economic Implications of Learningby Doing. Review of Economic Studies 29, 155–173.

Romer, Paul M. (1986), Increasing Returns and Long–Run Growth.Journal of Political Economy 94, 1002–1037.

Basic idea: There is no explicit “investment” into HC and noexplicit income share for this production factor. HC ismodelled as an external effect or as a by-product of physicalinvestment. Operating with physical capital goods leads to“learning by doing” effects which increase human capital K .

S.111

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Here HC/knowledge is non-rival in use and there is noexcludability (public good). Each investor also contribute to apublic good.

As for a small firm the influence on the human capital stock ismarginal, it takes K as given.

Profit maximizing implies that the capital cost equals theprivately appropriatbale marginal returns of capital (ignoringthe external effect). Social return exceeds private return ofcapital.

S.112

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Production function (Cobb-Douglas technology):

Y = f (K , K , L)

In case of Arrow (1962):

y = f (k , K ) = K ηkα = Nηkηkα

(where η + α = 1 yields the standard AK model)

In case of Romer (1986):

Y = f (K , K · N) = Kα(KN)1−α

⇒ y = kαK 1−α = N1−αkαk1−α

S.113

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

a) Households maximize (22) and we have the Keynes-Ramseyrule

gc = σ(r(t)− (ρ+ δ))

where σ is assumed to be constant.

b) Firms maximize

maxK ,N

π(k) = N · [kαK 1−α − rk − w ] (23)

From the first order conditions we have (with K = Nk)

r = αkα−1K 1−α = αN1−α (24)

w = (1− α)kαK 1−α = (1− α)kN1−α (25)

The marginal returns depend on firm specific k as well as on thegiven human capital stock K .

S.114

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

c) Decentral planning (market solution):

With a given labor force N the return to capital r in (24) isconstant.

The Keynes-Ramsey rule with decentralized planning reads

gc = σ(αN1−α − (ρ+ δ))

which is also the steady state growth rate for k .

Since there are positive externalities = the social returns ofcapital by inducing growing human capital are neglected inthe factor price r . Hence, the 1. theorem of welfare economicsdoes not hold true, and the growth path is pareto-inefficient.

S.115

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

d) Social planner:

A social planner is aware of the externalities, she does nottake K as given. Hence the profits according to (23) reads

maxK ,N

π(k) = N · [Kα

NαK 1−α − rk − w ] = N · [

K

Nα− rk − w ]

She calculates the FOC as

r = N1−α

and hence the Keymes-Ramsey rule is

g∗c = σ(N1−α − (ρ+ δ)) > gc

S.116

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Policy implications:

Since the decentralied planning leads to pareto-inefficientsteady state growth rates, there is room for welfare increasingpolicy.

Generally, incentives for economic activities with positivespillovers must be increased (e.g. by subsidies), the incentivesfor activities with negative spillovers have to be reduced (e.g.by taxes).

In each case it has to be taken into account that subsidieshave to be financed and taxes generate expenditures. Bothhas an economic impact on welfare.

S.117

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Since physical investment have positive spillovers by creatinghuman capital, there should be subsidies θ to increase the incentiveto invest. The marginal return is then:

r = α(1 + θ)N1−α

and the Keynes-Ramsey rule is

g∗∗c = σ(α(1 + θ)N1−α − (ρ+ δ))

By the “method of eyeballing” it is obvious that the optimal rateof subsidies is

θ∗ =1− α

α

because then g∗∗c = g∗

c .

S.118

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

How to finance this subsidy?

Income tax: In most democratic systems such a tax is perceived as“fair”. However, it lowers the marginal returns of the productionfactors. As a response, an intertemporally maximizing agent wouldthen shift his consumption expenditures from the future to thepresence = lower saving = lower capital accumulation = lowersteady state growth rate!

Per capita tax: This tax is perceived as “unfair” because it doesn’tregard the agent’s ability to pay taxes. However, such a tax doesnot affect allocation and has no negative impact on the steady stategrowth rate.

Consumption tax: This would not affect the intertemporal decisionbetween consumption and saving, but it would affect the decisionbetween working and leisure time. In our model (unelastic laborsupply) this doesn’t play a role.

A subsidy θ∗ combined with a per capita tax is therefore theoptimal tax-transfer system in this model.

S.119

3. Models of Endogenous Growth3.2 AK model and Knowledge Spillovers

Convergence:

There is no transitory dynamic.

Countries with similar characteristics grow with the samegrowth rate.

Countries with different scale of labor force N grow withdifferent rates: Large countries are growing faster than smallcountries (see Keynes-Ramsey rule!). There is no (or onlyweak) empirical support for this effect.

This scale effect could be avoided by assuming that theexternal effect depends on the average human capital K/N.

S.120

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Literature:

Lucas, R.E. (1988), On the Mechanics of Economic Development.Journal of Monetary Economics 22, 3–42.

Barro/Sala-i-Martin (chapter 5.2)

Basic idea:

In the models of Romer and Arrow knowledge or human capital hasbeen represented as a positive externality of physical investment.Lucas suggests that HC is a specific producable factor. It isproduced in a separate education sector (2-sector model).

Producing HC requires ressources (opportunity costs) ⇒ allocationbetween physical production and human capital accumulation.

HC is treated as a private good. Investments into HC yield apositive marginal return. In an extension of the model there are alsopositive externalities.

S.121

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The representative household decides about intertemporal consumption/saving allocation of human capital to both sectors

education

production

k

h

y

c

mh

(1−m)h

S.122

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Simplifying assumptions:

To avoid too much notation, we assume no population growthand no depreciation of physical and human capital (which isassumed to be identical in the original Lucas-model).

The constant labor force is normalized to one (N = 1).

Accumulation of human capital (schooling) only leads toopportunity costs since the houshold could either spend timein the schooling sector or in the production sector. There is nomarket price for schooling.

Human capital H is a private good. Hence it is possible todefine the per capita human capital (individual skill level) ash(t) = H(t)/N.

S.123

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The two sectors:

Human capital (schooling) sector:

h(t) = A(1−m(t))h(t), A > 0,m(t) ∈ [0, 1] (26)

where A is the productivity of the sector, and m(t) is the fraction ofhuman capital which is allocated to physical production. HC(output) is produced only with the factor HC (input).

Therefore, H(t) = m(t)H(t) = m(t)h(t)N is the effective humancapital stock used in physical production (note that N = 1).

Production sector:

Y (t) = K (t)αH(t)1−α

⇒ y(t) = k(t)α(m(t)h(t))1−α

S.124

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

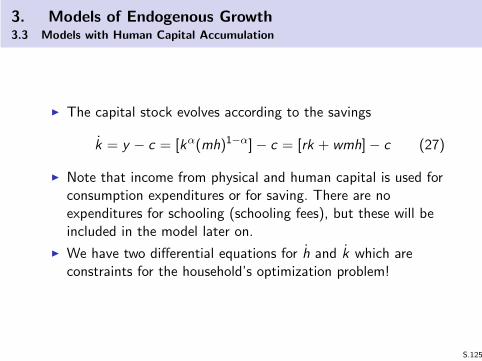

The capital stock evolves according to the savings

k = y − c = [kα(mh)1−α]− c = [rk + wmh]− c (27)

Note that income from physical and human capital is used forconsumption expenditures or for saving. There are noexpenditures for schooling (schooling fees), but these will beincluded in the model later on.

We have two differential equations for h and k which areconstraints for the household’s optimization problem!

S.125

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

a) Households have the following optimization problem:

maxc,m

U(0) =

∫ ∞

0u(c)e−ρtdt

conditional to k = y − c

h = A(1−m)h

m ∈ [0, 1], k(0) > 0, h(0) > 0

The Hamiltonian is now

H = u(c)e−ρt + µ1[[kα(mh)1−α]− c] + µ2[A(1−m)h]

S.126

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The optimality conditions are

∂H

∂c= uc(c)e

−ρt − µ1 = 0 (28)

∂H

∂m= µ1(1− α)kαh1−αm−α − µ2Ah = 0 (29)

−∂H

∂k= µ1 = −µ1αk

α−1(mh)1−α (30)

−∂H

∂h= µ2 = −µ1(1− α)kαm1−αh−α − µ2(1−m) (31)

The partial derivatives to µ1 and µ2 yields the known differentialequation for k and h. The transversality conditions for k(t) andh(t) are defined in the usual way.

S.127

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Again, we derive the growth rate for consumption(Keynes-Ramsey rule) and obtain the growth rates gc , gk , ghand gy . A steady state is defined where all growth rates areconstant and gm = 0 (constant human capital allocationbetween production and schooling).

An equilibrium growth path is characterized by identicalconstant growth rates.

Defining q = c/k and z = k/h (capital structure) then anequilibrium growth path implies

gq = gz = gm = 0 ⇐⇒ gy = gc = gh = gk

S.128

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Using the new terms the marginal return to capital can berewritten as

y = kα(mh)1−α

⇒ r = yk = αkα−1(mh)1−α

= αkα−1(mk/z)1−α = α(m/z)1−α

Differentiating (28) with respect to time and inserting (30) tosubstitute µ1 leads to the Keynes-Ramsey rule

gc = σ(r − ρ) = σ(αm1−αz−(1−α) − ρ) (32)

S.129

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

From the differential equation k and h (using the new terms) wehave

gk = m1−αz−(1−α) − q

gh = A(1−m)

Obviously, gq = gc − gk and gz = gk − gh holds true.

S.130

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

We have not yet discussed the evolution of m (human capitalallocation):

Differentiating (29) with respect to time and then inserting(30), (31) and the differential equations (27) and (26) inorder to substitute µ1, µ2, k and h leads to a differentialequation for m.

The resulting growth rates are:

gq = (σα− 1)m1−αz−(1−α) + q − σρ

gz = m1−αz−(1−α) − q − A(1−m)

gm =(1− α)A

α+mA− q

S.131

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

An equilibrium growth path with gq = gz = gm = 0 leads tothe steady state:

q∗ = σ(ρ− A) +A

α(33)

z∗ =(α

A

) 11−α

·(σρ

A+ 1− σ

)

(34)

m∗ =σρ

A+ 1− σ (35)

An economically reasonable (positive) solution requiresσ < A/(A− ρ).

An equilibrium allocation of human capital between schoolingand production sector requires identical marginal returns:⇒ r = A

Therefore the equilibrium growth rate is (similar AK)

gc = σ(A− ρ) = gy = gk = gh

S.132

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

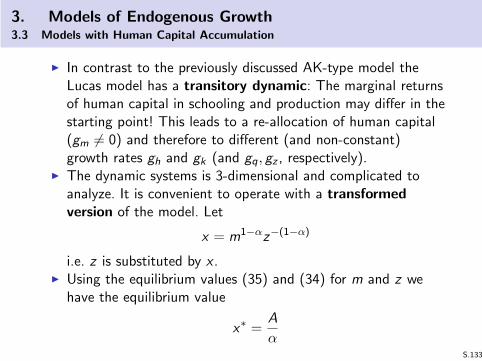

In contrast to the previously discussed AK-type model theLucas model has a transitory dynamic: The marginal returnsof human capital in schooling and production may differ in thestarting point! This leads to a re-allocation of human capital(gm 6= 0) and therefore to different (and non-constant)growth rates gh and gk (and gq, gz , respectively).

The dynamic systems is 3-dimensional and complicated toanalyze. It is convenient to operate with a transformedversion of the model. Let

x = m1−αz−(1−α)

i.e. z is substituted by x . Using the equilibrium values (35) and (34) for m and z we

have the equilibrium value

x∗ =A

αS.133

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The transformed model is

gq = (σα− 1)(x − x∗) + (q − q∗) (36)

gx = −(1− α)(x − x∗) (37)

gm = A(m −m∗)− (q − q∗) (38)

Instead of system (33) – (35) where gq and gz dependnonlinearly on q, z ,m, we have now a linear system ofdifferential equations!

The steady state value of the new variable x is stable sincegx > 0 ⇐⇒ x < x∗ and vice versa.

Since gq does not depend on m and gm does not depend on xit is possible to portray the isoclines in a 2-dimensionalgraphic.

S.134

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

q = 0m = 0

x = 0

S.135

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The transitional dynamics and the behavior of growth rates isextensively studied in Barro/Sala-i-Martin (chapter 5.2) and willnot discussed here. The equilibrium is a saddle point. A stable pathto the equilibrium requires that e.g. for a given q(0) determinesthe appropriate choice of x(0) and m(0).

S.136

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

One famous implication of the Lucas model:

The growth rate for consumption c (and also for y and for thecapital stock K ) depends negatively on the capital structure term z(see eq. (32).

This implies that a disequilibrium z < z∗, e.g. by destroying physicalcapital (“war”) leads to higher (transitory) growth rates for c andy . The marginal return of the remaining physical capital increasesand this stimulates capital accumulation.

A disequilibrium z > z∗, e.g. by destroying human capital(“epidemy”, migration) leads to lower (transitory) growth rates. Thelogic is, that the education sector operates only with human capital.If the latter decreses by a shock, the marginal returns increase. Thisreallocates human capital away from the physical sector.

One policy implication is that for low developped countries it ismore important to support the local human capital stock ratherthan physical investments. The Lucas model emphasizes theimportance of education policy.

S.137

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

A version with positive externalities:

Similar to the Arrow (1962) or Romer (1986) model, positiveexternal effects are modelled by

y = kα(mh)1−αhη, η ∈ (0, 1)

where a single firm treats h as exogenously given. Hence themarginal return from physical and human capital arecalculated, neglecting the external effect.

It can be shown that with decentralized planning the steadystate growth rates are (with σ = 1!):

gy = gc = gk =1− α+ η

1− α(A− ρ)

gh = A− ρ < gy

The growth rate gc is larger than in the model without theexternality.

S.138

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The growth rates gh and gy are constant but different. Theexternal effect of human capital enlarges the returns in thephysical production. Hence, the households work too muchbut learn too less!

Therefore, gz = gk − gh = η1−α

(A− ρ) > 0 increases, i.e.physical assets accumulate faster than intellectual assets.

A social planner treats h = h not as exogenously given andincludes the external effect when maximizing the welfare. Shecalculates the social return of human capital.

S.139

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Solution with a social planner:

g∗y = g∗

c = g∗k =

1− α+ η

1− αA− ρ

g∗h = A−

1− α

1− α+ ηρ

The policy advice is to change the incentives in order to reallocatea part of human capital from the physical to the education sector.This could be done by a tax-transfer-system.

S.140

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

A design for a tax-transfer system:

Since we have two production factors with a specific return,we have two income taxes:

interest rate tax τr ≥ 0 for physical capital wage tax τw ≥ 0 for human capital

Furthermore the incentive to allocate human capital to theeducation sector depends on the opportunity cost w(1−m)h.The government defines a fees/grants for education which areproportional to the opportunity cost

ω = θw(1−m)h

where θ > 0 menas that the household has to pay fees ω > 0and θ < 0 menas that the household receive grants ω < 0.

S.141

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

The intertemporal budget constraint can now written as

k = (1− τr )rk + (1− τw )wuh − θw(1−m)h − c

Also the government has a budget constraint:

τr rk + τwwuh + θw(1−m)h = 0

S.142

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Solving the model with these additional assumptions leads to:

g∗∗y = g∗∗

c = g∗∗k =

1− α+ η

1− α

(1− τw

1− τw + θA− ρ

)

g∗∗h =

1− τw1− τw + θ

A− ρ

Observe that τr has no influence on these growth rates!

S.143

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Result:

For θ > 0 (schooling fee) it is gy > g∗∗y for all τw . The

dparture from the pareto-efficient solution increases!

For θ = 0 (free acess to education) also the tax on laborincome has no effect on the growth rates. Hence, we have thesame pareto-inefficient result as in the unregulated case.

For θ < 0 (schooling grants) the pareto-efficiency is improveddue to the incentive to allocate more human capital to theeducation sector.

S.144

3. Models of Endogenous Growth3.3 Models with Human Capital Accumulation

Optimal tax-transfer system:

There is a continuum of (θ, τw )-combinations which internalize theexternalities of human capital and lead to pareto-efficiency:

θ∗ = (τ∗w − 1) ·ηρ

(1− α+ η)A+ ηρ

S.145

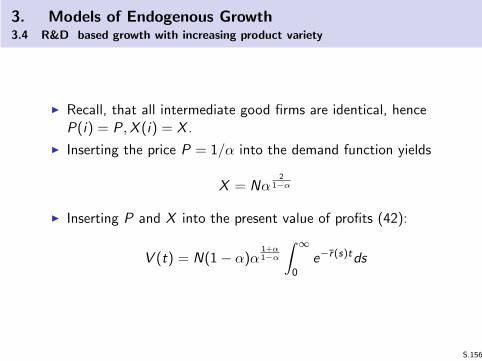

3. Models of Endogenous Growth3.4 R&D based growth with increasing product variety

Literature:

Romer, P.M. (1990), Endogenous Technological Change.Journal of Political Economy 98 (5), S71–S102.

Barro/Sala-i-Martin (chapter 6.1)

Basic Idea: