Slides for International Finance - American University value of any given amount of imports in terms...

132

Introductory Concepts Short-Run Model: DD and AA Liquidity Trap Macro Policy and CA Slides for International Finance Aggregate Demand and the SR (KOM Chapter 17) Alan G. Isaac American University 2012-10-22 Alan G. Isaac Slides for International Finance

Transcript of Slides for International Finance - American University value of any given amount of imports in terms...

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Slides for International FinanceAggregate Demand and the SR (KOM Chapter 17)

Alan G. Isaac

American University

2012-10-22

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

PREVIEW

AA Curvereview SR model of asset market equilibriumAA: ^Y � _E (to maintain asset mkt eq)

DD CurveSR model of output market equilibriumDD: ^E � ^Y (to maintain asset mkt eq)

SR ModelAA + DD: simultaneous output market and asset marketequilibriumtemporary v permanent changes in monetary and fiscal policiesliquidity trap (zero interest rates, deflation, stimulus)Adjustment of the current account over time.

IS-LM modelalternative perspective on the same results

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

SR vs. LR Models

LR models

all prices of inputs and outputs have time to adjust.

predict future exchange rate tendencies

suggest ways of thinking about how market participants formexpectations

SR modelssome prices of inputs and outputs do not fully adjust

labor contractscosts of adjustmentimperfect information about market demand.

Goal

show how macroeconomic policies affect E, Y, and CA

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Short-Run Equilibrium in Asset Markets

Consider two related asset markets:

money market: M/P = L(R, Y)^Y � ^L � (M/P < L) � ^R

foreign exchange market: R = R* + (Ee - E)/E^R � _E

When income (production) increases:

the demand for real liquidity increases,driving up the domestic interest rate,causing an appreciation of the domestic currency.

Summary: ^Y � _E

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Output and the Exchange Rate in Asset Market Equilibrium

L(R,Y1) L(R,Y2)

R1 R2

E

E1

E2

M/P

R

Q

Compare KOM 9 Figure 17-6Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Short-Run Equilibrium in Asset Markets: AA Curve

AA Curve

equilibrium in financial markets (money market and foreignexchange market)

inverse relationship between output and exchange rates (asdervied above)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

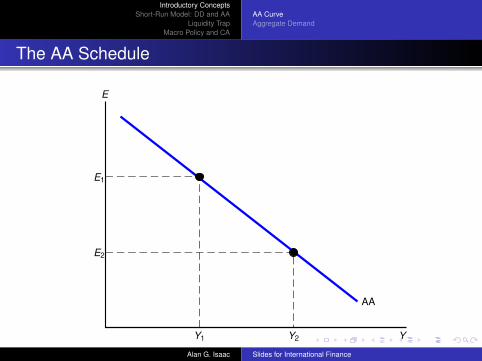

The AA Schedule

E

Y

AA

E1

Y1

E2

Y2

Compare KOM 9 Figure 17-7Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Shifting the AA Curve

1 ^M � _R (in the short run) � ^E (for every Y): the AA curveshifts up

2 ^P � _M/P � ^R � _E (given Y): the AA curve shifts down3 ^L (exogenously) � ^R � _E (given Y): the AA curve shifts

down4 ^R* � foreign currency deposits more attractive � ^E (given Y):

the AA curve shifts up5 ^ Ee: if market participants expect the future domestic currency

to be depreciated, foreign currency deposits become moreattractive, � ^E (given Y): the AA curve shifts up

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

^M � ^E in Assets Markets

L(R,Y1)

R1R2

E

E1

E2

M2/P

R

Q

M1/P

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

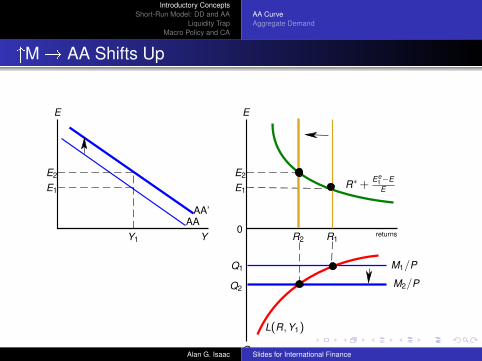

^M � AA Shifts Up

E

YAA

E1

Y1

AA’

E2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

^M � AA Shifts Up

E1

Q

L(R,Y1)

Q2

R10 returns

R∗+ Ee1−EE

E2

E

E1

E2

E

YY1

AAAA’

R2

M1/P

M2/P

Q1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

^Ee � AA Shifts Up

E1

Q

L(R,Y1)

Q1

R10 returns

R∗+ Ee1−EE

R∗+ Ee2−EE

E2

E

E1

E2

E

YY1

AAAA’

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of Aggregate Demand

Aggregate demand the aggregate amount of goods and servicesthat individuals and institutions are willing and able to buy

C: consumption expenditure

I: investment expenditure

G: government expenditure (purchases of final goods andservices)

CA: net expenditure by foreigners (the current account)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of Consumption Demand

disposable income (Yd = Y - T)^(Y-T) � ^C (mpc < 1)

real interest ratestheoretically indeterminate (conflicting income and substitutioneffects)empirically hard to detectwe will ignore

Wealthimportant theoretically and empiricallynevertheless, we assume that wealth is relatively constant andthus a relatively unimportant consideration

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

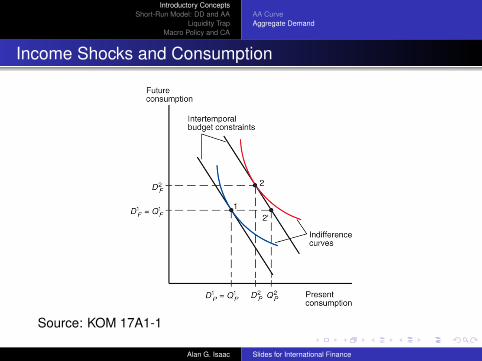

Income Shocks and Consumption

Source: KOM 17A1-1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of the Current Account

disposable income (Yd = Y - T)^(Y-T) � ^Im (mpm < 1)

real exchange rate (q = EP*/P)theoretically indeterminant, but we assume:^q � ^Ex, _Im � ^(Ex-Im)expenditure shifting: expenditure on domestic products rises, andexpenditure on foreign products falls.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Real Depreciation and the Current Account: More Details

CA = EX - IM the value of exports relative to the value of imports

Real depreciation: a rise in q (i.e., ^ EP*/P) prices of foreignproducts rise relative to the prices of domestic products.

The volume of exports that are bought by foreigners rises.

The volume of imports that are bought by domestic residents falls.

The value of any given amount of imports in terms of domesticproducts rises (i.e., the relative price of imports rises, foreignproducts becomes relatively expensive)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Marshall-Lerner Condition

Real current account:

CA = EX - IM = EX - q Immeasured in domestic goodsConflicting volume and valuation effects

Marshall-Lerner Condition

Condition for ^q � ^CAvolume effects outweigh value effectneed sum of export and import elasticities > 1

εX + εM > 1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

SR Effect of Depreciation: Value Effects and Volume Effects

SR volume effects

volume of imports and exports is relatively fixed in SR

value effects

sticky prices: P and P* relatively fixed in the short runpass through: ^E � ^EP* (imports cost more)^ (EP*/P)

SR net effect

domestic currency value of exports does not change.domestic currency value of imports rises_CA

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

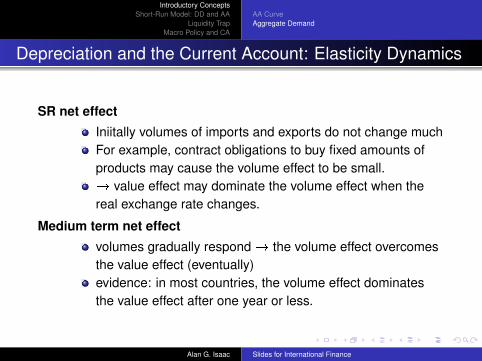

Depreciation and the Current Account: Elasticity Dynamics

SR net effect

Iniitally volumes of imports and exports do not change muchFor example, contract obligations to buy fixed amounts ofproducts may cause the volume effect to be small.� value effect may dominate the volume effect when thereal exchange rate changes.

Medium term net effect

volumes gradually respond � the volume effect overcomesthe value effect (eventually)evidence: in most countries, the volume effect dominatesthe value effect after one year or less.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

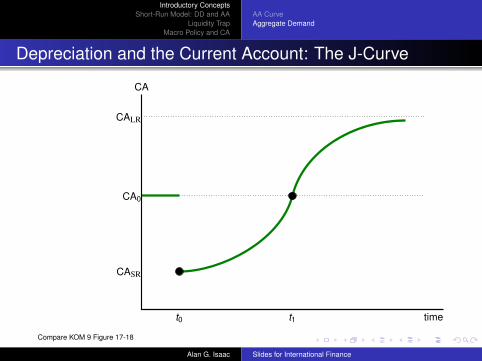

Depreciation and the Current Account: The J-Curve

time

CA0

CASR

CALR

t0 t1

CA

Compare KOM 9 Figure 17-18

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Exchange-Rate Pass Through

Exchange-rate pass through: the percentage by which import priceschange when the value of the domestic currency changes by 1%.pass through may be less than 100% due

price discrimination in different countries.price-setting firms may decide not to match changes in theexchange rate with changes in prices of foreign products

Pass through less than 100% dampens the effect of depreciationor appreciation on the current account.

smaller decline in CA (smaller J-curve)but also: smaller volume effects

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

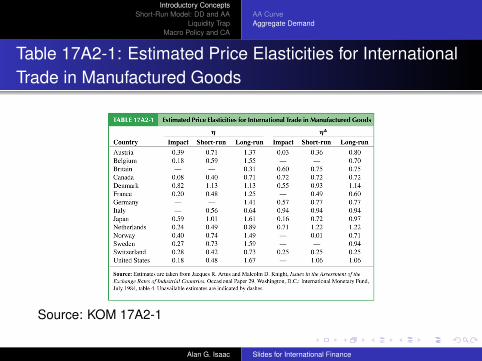

Table 17A2-1: Estimated Price Elasticities for InternationalTrade in Manufactured Goods

Source: KOM 17A2-1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

DD-AA model assumptions

pass through rate is 100%:import prices in domestic currency exactly match a depreciationof the domestic currency.prices fixed in domestic currency: nominal depreciation impliesreal depreciationML condition is satisfied:

the volume effect dominates the value effect.a real depreciation improves the current account

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

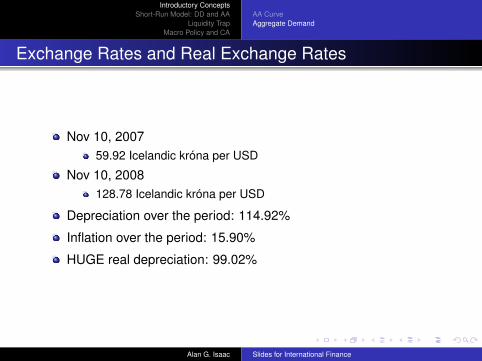

Exchange Rates and Real Exchange Rates

Nov 10, 200759.92 Icelandic króna per USD

Nov 10, 2008128.78 Icelandic króna per USD

Depreciation over the period: 114.92%

Inflation over the period: 15.90%

HUGE real depreciation: 99.02%

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Depreciation in Iceland

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of Aggregate Demand

Determinants of the current account include:Real exchange rate: an increase in the real exchange rateincreases the current account.Disposable income: an increase in the disposable incomedecreases the current account.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

CA/GDP vs. EP*/P in the US

Compare KOM Figure p.451 (which inverts the real exchange rate).

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of Aggregate Demand (cont.)

I, G and T are exogenous

G and T determined by political factors we do not modelI is determined by exogenous business decisions (for now)

(later we let I depend on the interest rate (i.e., on the cost ofborrowing to finance investment)

Consumption = C(Y-T)Current account = CA(EP*/P, Y-T)Therefore aggregate demand = C(Y-T) + I + G + CA(EP*/P, Y-T)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA CurveAggregate Demand

Determinants of Aggregate Demand (cont.)

Summarize the determinants of aggregate demand:

D = D(EP* /P, Y-T, I, G)^q � ^CA � ^D^(Y-T) � ^C � ^D (even though ^IM)mpm < mpc < 1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Short-Run Equilibrium for Aggregate Demand and Output

Aggregate demand is a function of:

the real exchange rate (EP*/P)disposable income (Y-T)investment expenditure (I)government purchases of final goods and services (G)

Equilibrium: our aggregate output (Y) equals the aggregate demandfor our output (D)Y = D(EP*/P, Y- T, I, G)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Aggregate Demand as a Function of Output

D

Y

D(EP*/P, Y-T, I, G)

D1

Y1 Y2

D1

45◦

Compare KOM 9 Figure 17-1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

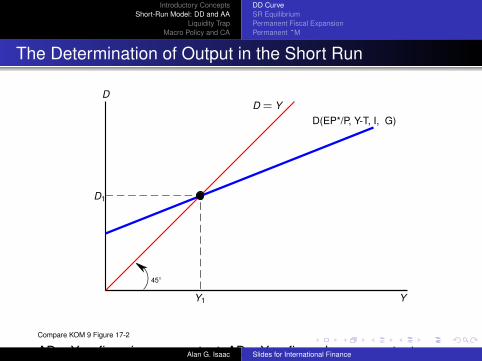

The Determination of Output in the Short Run

D

Y

D(EP*/P, Y-T, I, G)

D1

Y1

D = Y

45◦

Compare KOM 9 Figure 17-2

AD > Y -> firms increase output; AD < Y -> firms decrease outputAlan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Short-Run Equilibrium and the Exchange Rate: DDSchedule

Q: How does E affect AD?

A depreciation makes foreign goods and services relativelyexpensive (given domestic and foreign prices).

Aggregate demand shifts toward domestic products.

In equilibrium, production will increase to match the higher aggregatedemand.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Output Effect of ^E with Fixed Output Prices

D

Y

D(E1P ∗/P, . . .)

D1

Y1

D = YD(E2P ∗/P, . . .)

D2

Y2

Compare KOM 9 Figure 17-3

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

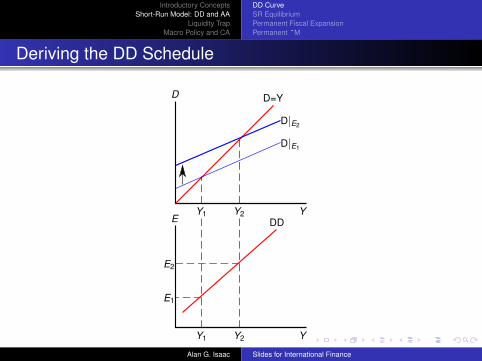

Deriving the DD Schedule

D

EY

YY2Y1

Y1 Y2

E1

E2

DD

D|E1

D|E2

D=Y

Compare KOM 9 Figure 17-4Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Short-Run Equilibrium and the Exchange Rate: DDSchedule (cont.)

DD schedule

shows combinations of output and the exchange rate at which theoutput market is in short run equilibrium (such that aggregatedemand = aggregate output).

slopes upward because a rise in the exchange rate causesaggregate demand and aggregate output to rise.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Shifting the DD Curve

Changes in the exchange rate cause movements along the DD curve.Other changes cause shifts of the DD curve.Exogenous ^D � DD shifts right:

^G � ^ AD � ^ Y.

^I � ^ AD � ^ Y.

^Cd (exog) � ^ AD � ^ Y. (expenditure increase or switching)

_T � ^ C � ^ AD � ^ Y.

_P � ^ q � ^ CA � ^ AD � ^ Y.

^ P* � ^ q � ^ CA � ^ AD � ^ Y.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

^G Shifts the DD Curve to the Right

D

EY

YY2Y1

Y1 Y2

E1

DD

D|G1

D|G2

D=Y

DD’

Compare KOM 9 Figure 17-5Output increases for every exchange rate: the DD curve shifts right.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

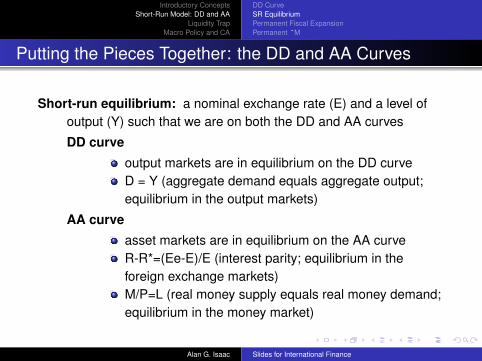

Putting the Pieces Together: the DD and AA Curves

Short-run equilibrium: a nominal exchange rate (E) and a level ofoutput (Y) such that we are on both the DD and AA curves

DD curve

output markets are in equilibrium on the DD curveD = Y (aggregate demand equals aggregate output;equilibrium in the output markets)

AA curve

asset markets are in equilibrium on the AA curveR-R*=(Ee-E)/E (interest parity; equilibrium in theforeign exchange markets)M/P=L (real money supply equals real money demand;equilibrium in the money market)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Short-Run Equilibrium in the DD-AA Model

E

Y

DD

AA

E1

Y1

Compare KOM 9 Figure 17-8Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

DD-AA Model: Very Short Run Disequilibrium Adjustment

E

Y

DD

AA

ESR

YSR

1

2

3

Compare KOM 9 Figure 17-9E adjusts immediately; asset markets are always in equilibrium.Y adjusts more slowly; commodity markets may be in temporary disequilibrium.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary Changes in Monetary and Fiscal Policy

Monetary policy: the monetary authority (e.g., central bank)influences conditions in the money markets (e.g., the supply ofmonetary assets)

Fiscal policy the fiscal authority (e.g., treasury) influences aggregatedemand via taxation and spending

Temporary policy changes:

expected to be reversed in the near futuredo not affect Ee

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

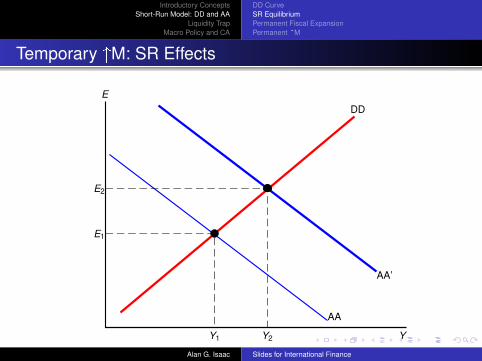

Impact of Temporary ^M

AA shifts up: ^M � _R � ^E

Move along DD ^E � ^EP*/P � ^D � ^Y

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary ^M: SR Effects

E

Y

DD

AA’

E2

Y1

AA

E1

Y2

Compare KOM 9 Figure 17-10Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary Changes in Fiscal Policy

Exogenous changes in aggregate demand

may result from fiscal changes^G � ^AD or _Tx � ^AD^AD � equilibrium Y (at each E)i.e., the DD curve shifts right.

^Y�^L

increased demand of real monetary assets increasesequilibrium interest rates,� _E (domestic currency appreciation)we move along the AA curve

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary Fiscal Expansion: SR Effects

E

Y

DD

AA

E1

Y1

DD’

E2

Y2

Compare KOM 9 Figure 17-11Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

How Big (Small?) Are Fiscal Multipliers?

Robert Barro (WSJ, 2009): Peacetime multipliers are essentially zero

Christina Romer (2009): Multiplier is around 1.5

Difference: 3.7 million jobs by the end of 2010

Existing studies mainly confined to OECD countries: Blanchardand Perotti (2002), Perotti (2004), Uhlig and Mountford (2005),Ramey (2008), Barro and Redlik (2009)

Exception: Ilzetzki, Mendoza, and Vegh (2009):

45 country panel (19 high-income, 26 developing)quarterly data (1960Q1 - 2007Q4)focus on the factors/characteristics that affect the size of themultipliers

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Fiscal Multipliers

Question: What is the impact on GDP of a $1 increase in governmentexpenditure?

Impact Multiplier: ∆GDP0/∆G0

Cumulative Multiplier ∑t0 ∆GDPt/∑

t0 ∆Gt

Long-run multiplier: the cumulative multiplier once both impulseresponses have died down.

Ilzetzki, Mendoza, and Vegh (2009) find characteristics matter:

High income versus emerging/developing

Fixed (predetermined) versus flexible exchange rate regimes

Open versus closed

High-debt versus low debt

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Policy conclusion:

Size of fiscal multipliers depends on key country characteristics:

high income versus developing

fixed versus flex

closed versus open

high debt versus low debt

Worst combination: developing, open, exchange rate flexibility� Not much scope therefore for countercyclical fiscal policy

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Potential Output (Yf)

Potential output

resources are used effectively and sustainablyproduction is at the “potential” or “natural” level

Under utilization

resources not used effectively, orresources are underemployed (e.g., high unemployment,few hours worked, idle equipment)� lower than normal production of goods and services.

Over utilization

resources are not used sustainablyresources are over-employed (e.g., unusually lowunemployment, overtime hours, over-utilized equipment)� unsustainably high production of goods and services.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary Fall in Aggregate Demand: SR Effects

E

Y

DD’

AA

ESR

YSR

DD

E0

Yf

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Monthly Unemployment

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

^G as Policy Response to Temporary _D

E

Y

AA

ESR

YSR

DD|G2

E0

Yf

DD|G1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

^M as Policy Response to Temporary _D

E

Y

DD

AA|M1

ESR

YSR

E0

Yf

AA|M2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Fig. 16-12: Maintaining Full Employment After a TemporaryFall in World Demand for Domestic Products

Source: KOM Figure 17-12

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Temporary ^L: SR Effects

E

Y

DD

AA

E0

YSR

AA’

ESR

Yf

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

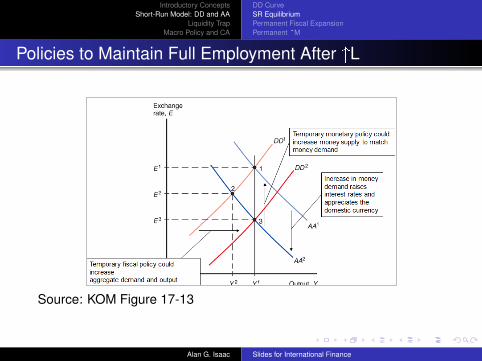

Policies to Maintain Full Employment After ^L

Source: KOM Figure 17-13

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Policies to Maintain Full Employment: Difficulties

Our model suggests it is easy to maintain full employment.In practice, it is difficult.Expansionary fiscal and monetary policies may induce inflation andhigher inflation expectations, preventing high output and employment.(Ignoring this leads to inflationary bias.)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Policies to Maintain Full Employment: Difficulties

Model assumptions:expectations given

but people may anticipate the effects of policy changes andmodify their behavior.

all prices stickyworkers may require higher wages if they expect overtimeand easy employmentproducers may raise prices if they expect higher wages andstrong demand

we know about the contractionary shock

but economic measurement is difficult and andeconomic data hard to understand.policy makers must guess the state of the assetmarkets and aggregate demand; they makemistakes.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Policies to Maintain Full Employment: Difficulties

Model assumptions:

policy changes are implemented immediately and haveimmediate effects

but changes in policies take time to beimplemented and to affect the economy.expansionary policy may affect the economy afterthe the shock has dissipated.

policy choices not influenced by political or bureaucraticinterests

but policies may be influenced by political or bureaucraticinterests.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

US Economic Stimulus Act of 2008

Feb 13, 2008

Bush signs into law

Response to

2007 subprime mortgage crisis and credit crunchincreasing evidence of economic slowdown

Tax rebates and investment incentives

$152 B budget cost projected for 2008$124 B additional cost over 10 years

Evidence of substantial stimulus effect?

limited, but Broda and Parker (2008) find some evidence ofincreased household spending immediately following receiptof the rebate.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

China (PRC) Fiscal Stimulus 2008

November 2008

Announced $586 B over two years

Reaction to

global economic crisisgrowth slowdown (perhaps to 6%, vs. 10% p.a.)factory closing and mass layoffs in the south

Comment:

G/Y in China low relative to EU and US

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

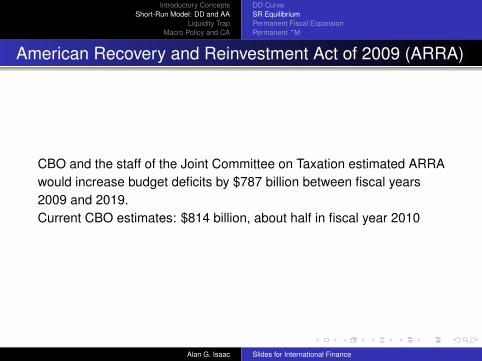

American Recovery and Reinvestment Act of 2009 (ARRA)

CBO and the staff of the Joint Committee on Taxation estimated ARRAwould increase budget deficits by $787 billion between fiscal years2009 and 2019.Current CBO estimates: $814 billion, about half in fiscal year 2010

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Effect of 2009 Stimulus on Employment and Output

CBO’s model-based estimates say ARRA:Raised the level of real (inflation-adjusted) gross domesticproduct (GDP) by between 1.7 percent and 4.5 percent,Lowered the unemployment rate by between 0.7 percentagepoints and 1.8 percentage points,Increased the number of people employed by between 1.4 millionand 3.3 million, andIncreased the number of full-time-equivalent (FTE) jobs by 2.0million to 4.8 million compared with what those amounts wouldhave been otherwise. (Increases in FTE jobs include shifts frompart-time to full-time work or overtime and are thus generallylarger than increases in the number of employed workers.)

The effects of ARRA on output and employment are expected to belargest during 2010.Source: http://cboblog.cbo.gov/?p=1326

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

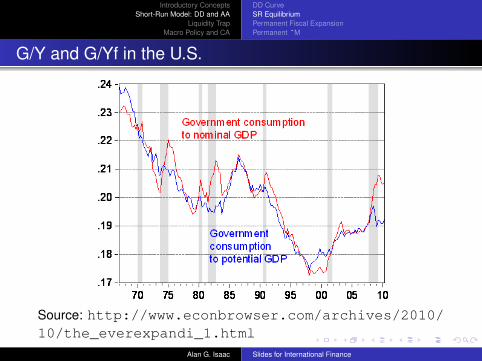

G/Y and G/Yf in the U.S.

Source: http://www.econbrowser.com/archives/2010/10/the_everexpandi_1.html

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Quantitative Easing

Quantitative Easing (QE):

policy to expand the high-powered money supply even whenSR interest rates are unresponsive (e.g., already near zero)especially: substantial expansion of bank reserves (and thusthe monetary authority’s balance sheet)goals: ease credit; lower long bond rates; affect expectationsterm often used to include “qualitative easing” or “crediteasing”

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

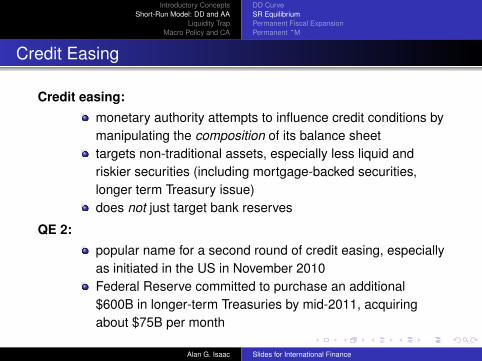

Credit Easing

Credit easing:

monetary authority attempts to influence credit conditions bymanipulating the composition of its balance sheettargets non-traditional assets, especially less liquid andriskier securities (including mortgage-backed securities,longer term Treasury issue)does not just target bank reserves

QE 2:

popular name for a second round of credit easing, especiallyas initiated in the US in November 2010Federal Reserve committed to purchase an additional$600B in longer-term Treasuries by mid-2011, acquiringabout $75B per month

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Permanent Changes in Monetary and Fiscal Policy

“Permanent” shock: changes expectations about the futureexchange rate

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Permanent Fiscal Expansion

Permanent change in fiscal stanceincrease in G or decrease in TChanges aggregate demand

subject to usual qualifications

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

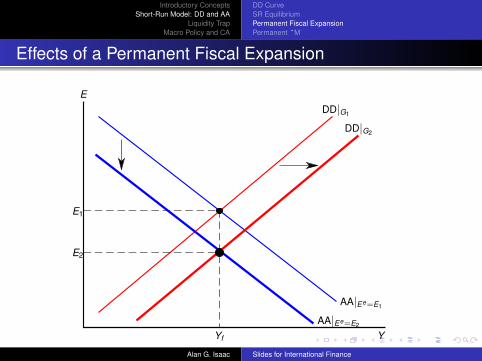

Effects of a Permanent Fiscal Expansion

E

Y

DD|G1

AA|Ee=E1

E1

Yf

DD|G2

E2

AA|Ee=E2

The AA curve also shifts: a permanent fiscal expansion appreciates Emore.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Fig. 16-16: Effects of a Permanent Fiscal Expansion

Source: KOM Figure 17-16

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

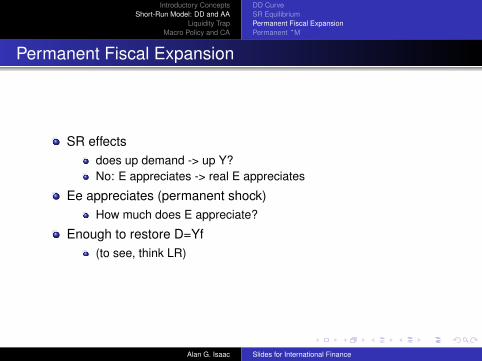

Permanent Fiscal Expansion

SR effectsdoes up demand -> up Y?No: E appreciates -> real E appreciates

Ee appreciates (permanent shock)How much does E appreciate?

Enough to restore D=Yf(to see, think LR)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Permanent Fiscal Expansion (LR)

LR outcomes and SR outcomes are the same!

M=M0, Y = Yf, R=R*so P is unchanged!But then D(EP*/P,Y-T,I,G)=Yf� ^G must “crowd out” private demand through CA!

Twin deficits once again

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

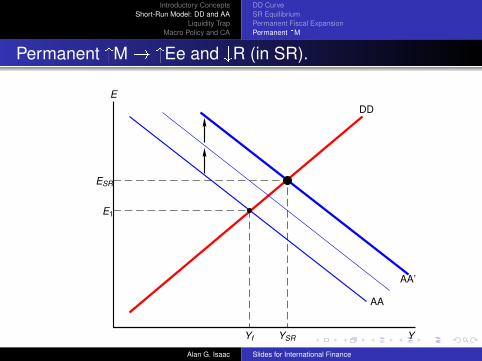

Permanent Changes in Monetary Policy

Permanent ^M1 makes people expect future depreciation of the domestic

currency (increases the expected rate of return on foreigncurrency deposits at each E)

2 causes ^M/P and _R (in the short run)

Two forces for depreciation combine:

E rises more than when expectations are constant (see ourstatic expectations results).the AA curve shifts up more than the case whenexpectations are held constant.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Permanent ^M � ^Ee and _R (in SR).

E

Y

DD

AA

E1

Yf

AA’

ESR

YSR

Compare: KOM Figure 17-14Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Effects of Permanent Changes in Monetary Policy in theLong Run

With employment and hours above their normal levels, there is atendency for wages to rise over time.

With strong demand of goods and services and with increasingwages, producers have an incentive to raise prices over time.

Both higher wages and higher output prices are reflected in ahigher level of average prices.

What are the effects of rising prices?

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

DD CurveSR EquilibriumPermanent Fiscal ExpansionPermanent ^M

Long-Run Adjustment to a Permanent Increase in the MoneySupply

Source: KOM Figure 17-15

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates, Exchange Rates and a Liquidity Trap

A liquidity trap occurs when nominal interest rates fall to zero andthe central bank cannot encourage people to hold more liquid(monetary) assets.

Nominal interest rates can not fall below zero, or else depositorswould have to pay to put their money in banks.When interest rates fall to zero, people are indifferent betweenholding monetary and interest-bearing assets, so that central bankcan not encourage them to spend or borrow more money.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

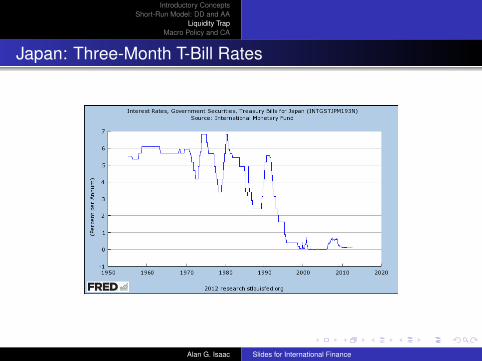

Japan: Three-Month T-Bill Rates

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

US: Three-Month T-Bill Rates

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Three-Month Interest Rates on Dollar and Yen Deposits

Source: KOM 9 Fig 14-2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates, Exchange Rates and a Liquidity Trap

R = R∗+ (Ee−E)/E

1 + R−R∗ = Ee/E

E = Ee/(1 + R−R∗)

If the domestic interest rate is reduced to zero, then

E = Ee/(1−R∗)

With fixed expectations about the exchange rate (and inflation)and fixed foreign interest rates, the exchange rate is fixed.

A purchase of domestic assets by the central bank does not lowerthe interest rate, nor does it change the exchange rate.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Temporary ^M with a Liquidity Trap

E

Y

DD

AA

Ee

1−R∗

Y1

Compare KOM 9 Figure 17-19Compare: KOM 9 Figure 17-19If nominal interest rates are zero, a temporary monetary expansion will not lower interest rates and will not affect exchange ratesnor output: a liquidity trap.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

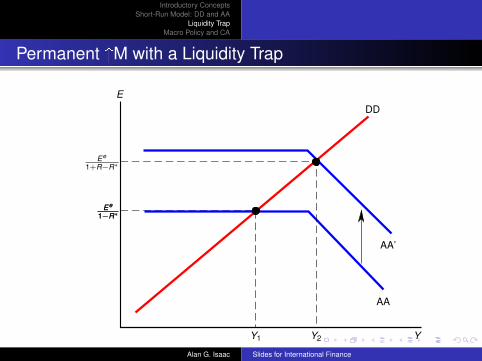

Permanent ^M with a Liquidity Trap

E

Y

DD

AA

Ee

1−R∗

Y1

Ee

1−R∗

AA’

Y2

Ee

1+R−R∗

A permanent monetary expansion will raise expectations of inflationand cause markets to expect a depreciation of the domestic currency:inflationary money policy depreciates the currency and raises output.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Devaluation and a Liquidity Trap (cont.)

A devaluation of the currency could achieve the same goals if marketexpectations do not change: a devaluation raises output.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates, Exchange Rates and a Liquidity Trap (cont.)

Prices and wages have fallen (deflation), allowing a realdepreciation of Japanese products.

Low output and employment has gradually risen as prices, wagesand the value of Japanese products have fallen.

In addition, Japan has maintained low interest rates, hasincreased the growth rate of its money supply and has tried todepreciate the yen by purchasing international reserves.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates, Exchange Ratesand a Liquidity Trap

Liquidity trap nominal interest rates fall so low that the central bankcannot encourage people to hold more liquid assets (money).

At some low interest rate, people are indifferent between holdingmoney and interest bearing assets

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Negative Interest Rates

Traditional wisdom: R < 0 impossiblePeople would just hold cash (� 0 rate of return )

Reality:holding cash is riskycompare: people pay for depositories for valuables

Reality (1970s):Switzerland paid negative interest on foreign deposits

response to speculative interest in owning Swiss Francs

traditionally considered a very special case

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Negative Interest Rates: Japan

Reality (late 1998, early 1999):Western banks paid negative interest on yen interbank deposits

Note: Japanese banks chose Western over local institutionsbased on perceived risk

negative interest rates on short-term Japanese gvt bills

Reality (February 1999):BoJ adopts “zero interest rate policy”)Note arbitrage opportunity:

foreign banks increased their holdins at BoJ!

(BoJ imposes limits)Reality (January 2003):

Japanese interbank rate <0

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Liquidity Trap and Monetary Policy

Temporary Monetary Expansionshifts out M/Pbut no effect on Rtherefore completely ineffective

Permanent Monetary Expansionhas effects by changing expectationspermanent M increase� increase expected E

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Japan’s Policy Choices

Many observers urged monetary expansion or active devaluation.New BoJ governors (since March 2003)

increased the growth of the money supplypurchased international reserves

Did Japan court deflation (price adjustment policy)?prices and wages fall over time (deflation)produce a real depreciation of Japanese productsstimulate demand� expand economy

Fiscal Expansiona fiscal expansion could workhigh public debt made policy makers cautiousprimary deficit actually showed signs of tightening in early noughts

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Another Option

Export expansion - Japan got lucky: 2002 export boomlargely due to China’s growth

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Macro Policy and CA

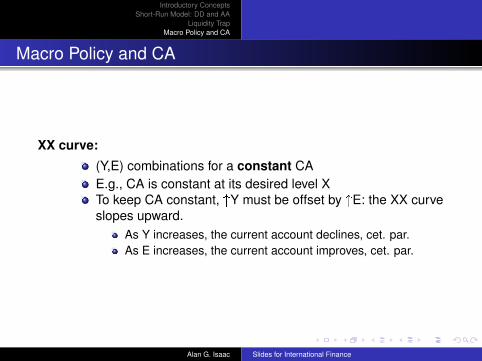

XX curve:

(Y,E) combinations for a constant CAE.g., CA is constant at its desired level XTo keep CA constant, ^Y must be offset by ^E: the XX curveslopes upward.

As Y increases, the current account declines, cet. par.As E increases, the current account improves, cet. par.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Macroeconomic Policy and the Current Account

E

Y

CA = 0

E1

Y1

E2

Y2

CA < 0

CA > 0

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

AA, DD, and XX

E

Y

DD

XX

AA

E1

Y1

Note: compare KOM 9 Figure 17-7.Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Why XX is Flatter than DD

To keep the current account constant, the domestic currencymust depreciate as income and output increase

the XX curve slopes upward.

To keep the goods market in equilibrium, domestic income mustrise as our currency depreciates

the DD curve slopes upward.

Which is flatter?Start with CA = XRaise E and Y so that CA=X (still on XX)No change in AD via CA, but up AD and AS due to up Y, -> excesssupply

so DD is above XX

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Macroeconomic Policies and the Current Account (cont.)

Policies affect the current account through their influence on thevalue of the domestic currency.

An increase in the quantity of monetary assets supplieddepreciates the domestic currency and often increases the currentaccount in the short run.An increase in government purchases or decrease in taxesappreciates the domestic currency and often decreases thecurrent account in the short run.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Temporary Fiscal Expansion and the Current Account

E

Y

DD

XX

AA

E1

Yf

DD’

E2

Y2

temporary fiscal expansion � DD shifts right � _E � _CAAlan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Permanent Fiscal Expansion and the Current Account

E

Y

DD

XX

AA

E1

Yf

DD’

E2

Y2

AA’

The AA curve also shifts: a permanent fiscal expansion decreases CAmore.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

^M � ^CA

Increase in the money supply

shifts up the AA curvecauses a movement along the DD curve, which is steeperthan XX� depreciates the domestic currency� ^CA

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Temporary Monetary Expansion and the Current Account

E

Y

DD

XX

AA

E1

Y1

AA’

E2

Y2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Permanent Monetary Expansion: the Short Run

E

Y

DD

XX

AA

E1

Y1

AA’

ESR

YSR

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary: Macroeconomic Policy and the Current Account

Source: KOM Figure 17-17b

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Bond yields (missing part of our story)

Source: IMF 2009, Global Financial Stability Report

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

US: Debt and Debt/GDP

Source: Wikipedia

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

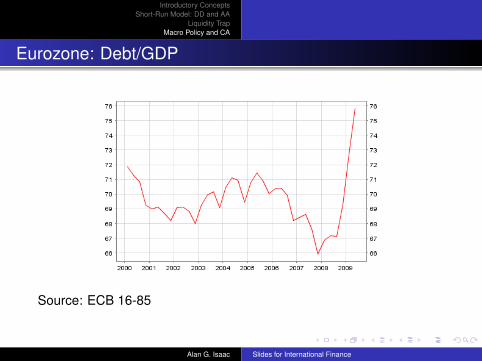

Eurozone: Debt/GDP

Source: ECB 16-85

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

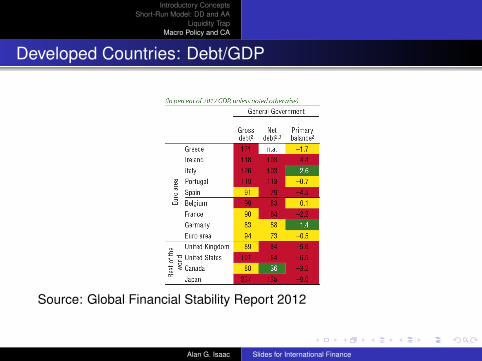

Developed Countries: Debt/GDP

Source: http://www.imf.org/external/pubs/ft/spn/2010/spn1013.pdf

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Developed Countries: Debt/GDP

Source: http://www.imf.org/external/pubs/ft/spn/2010/spn1013.pdf

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Developed Countries: Debt/GDP

Source: Global Financial Stability Report 2012

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates

Our DD-AA model assumed investment expenditure isexogenous.Some parts of investment clearly respond to interest rate

Residential fixed investment

Investment projects funded by saved or borrowed fundsinterest rate represents the (real) opportunity cost costA higher interest rate means less investment expenditure.

But see Chetty (2004 REStud)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates

Other expenditure may depend on the interest rate.A higher interest rate makes saving more attractive andconsumption expenditure (on domestic and foreign products) lessattractive.

But there are conflicting income and substitution effects

And the effect of the interest rate appears to be much larger oninvestment expenditure than it is on consumption expenditure andimports.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

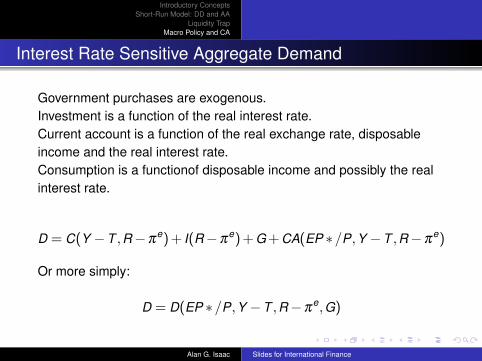

Interest Rate Sensitive Aggregate Demand

Government purchases are exogenous.Investment is a function of the real interest rate.Current account is a function of the real exchange rate, disposableincome and the real interest rate.Consumption is a functionof disposable income and possibly the realinterest rate.

D = C(Y −T ,R−πe) + I(R−π

e) + G + CA(EP ∗/P,Y −T ,R−πe)

Or more simply:

D = D(EP ∗/P,Y −T ,R−πe,G)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Interest Rates

Treat expected inflation as exogenous for nowI = I(R) I’<0R = R* + Ee/E -1I = I(R* + Ee/E -1)

Now up E => down R => up I (extra stimulus)DD flatterAlso: R* and Ee become shift factors for DD curve

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

IS-LM Model

Instead of relating exchange rates and output, the IS-LM relatesinterest rates and output.

In equilibrium, aggregate output = aggregate demand

Y = D(EP ∗/P,Y −T ,R−πe,G)

In equilibrium, interest parity holdsR = R* + (Ee-E)/EE(1+R) = ER* + EeE(1+R- R*) = EeE = Ee/(1+R- R*)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

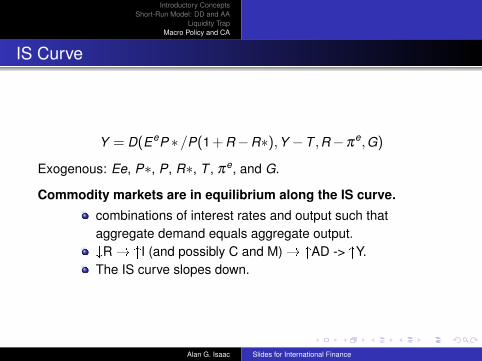

IS Curve

Y = D(EeP ∗/P(1 + R−R∗),Y −T ,R−πe,G)

Exogenous: Ee, P∗, P, R∗, T , πe, and G.

Commodity markets are in equilibrium along the IS curve.

combinations of interest rates and output such thataggregate demand equals aggregate output._R � ^I (and possibly C and M) � ^AD -> ^Y.The IS curve slopes down.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

IS Curve

R

Y

IS

R2

Y1 Y2

R1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

LM Curve

The money market is in equilibrium along the LM curve.

Ms/P= L(R,Y)combinations of interest rates and output such that themoney market is in equilibrium, given exogenous P and M

The LM curve slopes up.

^Y � ^L � ^R (in equilibrium)

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

IS Curve

R

Y

LM

R1

Y1 Y2

R2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Equilibrium in the IS-LM Model

Commodity markets are in equilibrium along the IS curve.Money market is in equilibrium along the LM curve.Both markets are in equilibrium where the two curves intersect.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Equilibrium in the IS-LM Model

R

Y

LM

IS

R1

Y1

Commodity and money markets are in equilibrium at Y1, R1Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Effects of Temporary Changes in the Money Supply

R

Y

LM’

IS

R2

Y2

LM

R1

Y1

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Effects of Temporary Changes in the Money Supply

R

Y

LM’

IS

Y2

LM

Y1E1E2E

R2

R1

Compare: KOM Figure 17-ISLM01

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

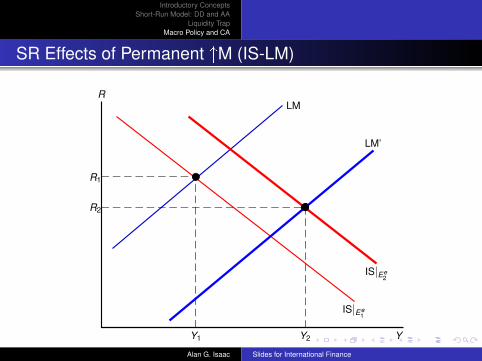

SR Effects of Permanent ^M (IS-LM)

R

Y

LM’

IS|Ee1

R2

Y2

LM

R1

Y1

IS|Ee2

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

SR Effects of Permanent ^M (IS-LM)

R

Y

LM’

IS|E1

Y2

LM

Y1E1E2E

R2

R1

IS|Ee2

Compare: KOM Figure 17-ISLM02

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Effects of Temporary Changes in Fiscal Policy

Source: KOM Figure 17-ISLM03

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Effects of Permanent Changes in Fiscal Policy

Source: KOM Figure 17-ISLM04

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary

Aggregate demand (D) responds to disposable income (Y-T) andthe real exchange rate (q=EP*/P).

The AA illustrates asset markets equilibrium: (Y,E) combinationssuch that M/P=L and interest parity holds.

The DD curve illustrates goods market equilibrium: (Y,E)combinations such that D=Y

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary

In the DD-AA model, we assume the Marshall-Lerner condition issatisfied

so a depreciation of the domestic currency improves the currentaccount and increases aggregate demand)in reality we may have a J-curve, where CA initially deterioratesbecause the value effect initially dominates the volume effect.

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary: Temporary Policy Shocks

Temporary ^M � temporary ^Y and temporary ^E

Temporary ^G � temporary ^Y and temporary _E

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary: Permanent Policy Shocks

Permanent ^M � temporary ^Y and temporary overshooting,with permanent ^E

Permanent ^G � no change in Y but permanent _E

Alan G. Isaac Slides for International Finance

Introductory ConceptsShort-Run Model: DD and AA

Liquidity TrapMacro Policy and CA

Summary: IS-LM

The IS-LM model compares interest rates with output.

The IS curve illustrates (Y,R) combinations such that D=Y

The LM curve illustrates (Y,R) combinations such that M/P=L(R,Y)The IS-LM model gives basically the same results

tends to underplay Eecaptures interest rate effects on D, which our model ignored

Alan G. Isaac Slides for International Finance