Slide 13.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education...

47

Slide 13.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education 2011 Chapter 13 Ratio analysis

-

Upload

maryann-potter -

Category

Documents

-

view

217 -

download

1

Transcript of Slide 13.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education...

Slide 13.1

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Chapter 13

Ratio analysis

Slide 13.2

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Summary of the chapter

• Overview

• Ratio analysis

• Interpretation of ratio analysis

• Formal calculations are only the start

• Ratios must be interpreted

Slide 13.3

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Overview

Identification of important trends over time.Five year period, consider trends in key

indicators:• Sales (revenue)• Net assets• Operating profit• Profits after tax• Earnings per share

Slide 13.4

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Year 7 Year 6 Year 5

£m £m £m

Sales (revenue)

2,100 2,260 2,149

Growth (160) 111

% Growth (160/2260) × 100 (111/2149) × 100

= −7.1% = 5.2%

One-year growth – Craigielaw

Slide 13.5

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Purpose of ratio analysis

Absolute figures are of little value. They only provide insights if they can be compared with other relevant amounts in ratios, for example,

• Sales as a percentage of gross profits.

Allows prediction of likely increase in profit given an increased level of sales.

• Profit as a percentage of sales.

• Is the profit level satisfactory?

Need ‘standards’ for comparison.

Slide 13.6

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Comparisons

(i) Compare with earlier years.

• Identification of a trend?

• Does it represent an improvement?

Slide 13.7

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Comparisons (Continued)

(ii) Compare it with the company's plan.

• Is it in line with the company’s expectations as budgeted?

• Not generally available in detail to an outside investor.

• But company might indicate forward-looking aspects in OFR.

Slide 13.8

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Comparisons (Continued)

(iii) Compare with those of other companies in the same industry.

• External standard.

• No two companies are exactly alike, in products or in markets.

• Different accounting policies used, for example, depreciation, inventory (stock) valuation.

Slide 13.9

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Comparisons (Continued)

(iv) Compare with industrial average.

• All the disadvantages of average figures.

• Our company might be placed in a particular part of the market and so it is of limited value to compare with average of the industry.

• Accounting policies may be different.

• But provides a starting point.

Slide 13.10

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Accounting policies

Ensure that the company has used consistent accounting policies over time, especially:• inventory (stock) valuation.• non-current (fixed) asset revaluation.• depreciation.Normally, companies will adjust earlier reported profit figures (comparative figures) if a major change has taken place.

Slide 13.11

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Inflation

No explicit attempt to take into account the effect of inflation:

• Sales last year £100m, this year £105m.

• Company claims growth rate 5%.

• Is adjustment needed?– Inflation, say, 2%, then real growth 3%.

– Costs, for example, average earnings rising 5% per annum.

Slide 13.12

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Other sources

Many sources of information about competing companies’ performance, for example,• trade journals• industry surveys• press comment• competitors and customers tell tales• commercial analysis services• Centre for Interfirm Comparison• Reuters and Bloombergs

Slide 13.13

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Ratio’s only a starting point

• What did we expect? What did we find?

• How does the company explain the difference?

• Do we believe it?

• What is our intuition?

• Look for corroboration, e.g. link to cash flow statement

Slide 13.14

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Ratio’s only a starting point (Continued)

Indicates questions to ask.

For example, why has profit margin fallen?

Might be due to product market conditions; or specific problems of the company; or change in product mix.

Very often segmental information is needed.

Slide 13.15

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Systematic analysis

Investor ratios: An aid to judging a company as a stock market investment.

Management performance: An aid to judging how well the company is being run by management.

Liquidity: Aids judgement of the adequacy of company's cash and near cash resources.

Gearing: (called ‘Leverage’ in American texts) Measure of the company's financial risk.

Slide 13.16

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Peter Television example

Slide 13.17

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Year 1

£m £m £m

Sales (revenue) 720 600

Cost of sales 432 348

Gross profit 288 252

Distribution costs (72) (54)

Administrative expenses (87) (81)

(159) (135)

Operating profit 129 117

Interest payable (24) (24)

Profit before tax 105 93

Taxation 42 37

Profit for the period 63 56

Year 2

£m

Income statement

Slide 13.18

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Year 1

£m £m £m

Land and buildings

600 615

Plant and equipment 555 503

1,155 1,118

Inventory (stock) 115 82

Trade receivables (debtors) 89 61

Prepayments 10 9

Bank 6 46

220 198

Statement of financial position

Year 2

£m

Slide 13.19

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

842 880

342 380Retained profits

500 500Ordinary shares of £1

842 880

(400)(400)6% debentures

1,2421,280

124 125Net current assets

(74)(95)

(25) (29)Accruals

(19) (21)Taxation

(30) (45)Trade payables (creditors)

Year 2 Year 1 £m £m £m £m

Statement of financial position (Continued)

Slide 13.20

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

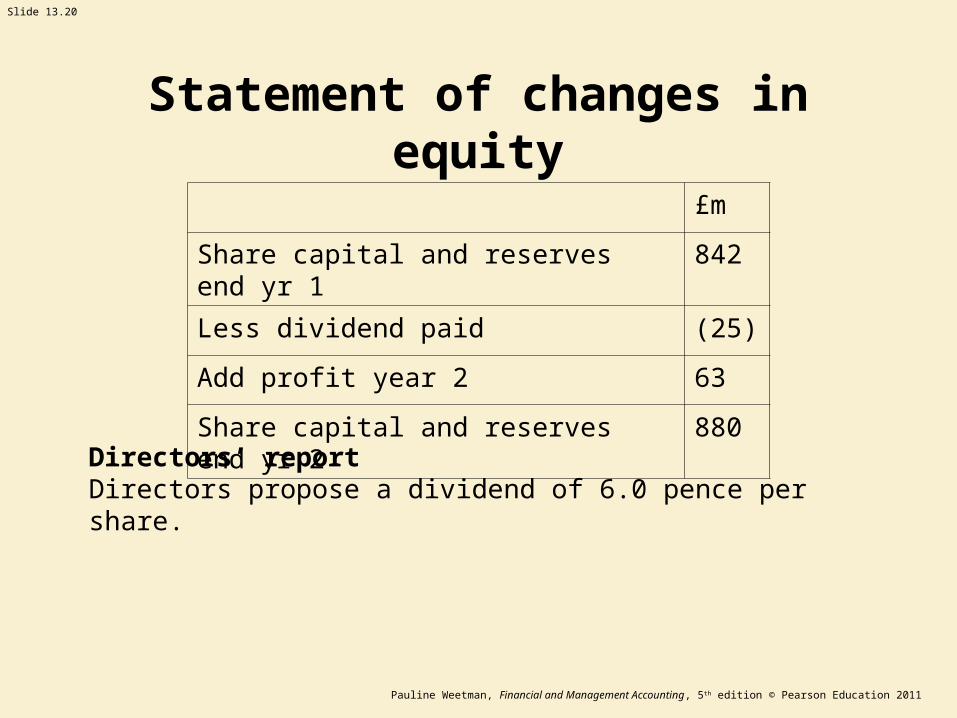

£m

Share capital and reserves end yr 1 842

Less dividend paid (25)

Add profit year 2 63

Share capital and reserves end yr 2 880

Statement of changes in equity

Directors’ reportDirectors propose a dividend of 6.0 pence per share.

Slide 13.21

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Share prices

Share price used in ratio analysis is the value soon after the profits of the company have been announced to the market.The announcement is by press release called the Preliminary Announcement. For a 31 December year end the press release might be in the following March. Market price at 1 March Year 2 202 penceUse to evaluate Year 1 figuresMarket price at 1 March Year 3 277 pence Use to evaluate Year 2 figures

Slide 13.22

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Investor ratios

Slide 13.23

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

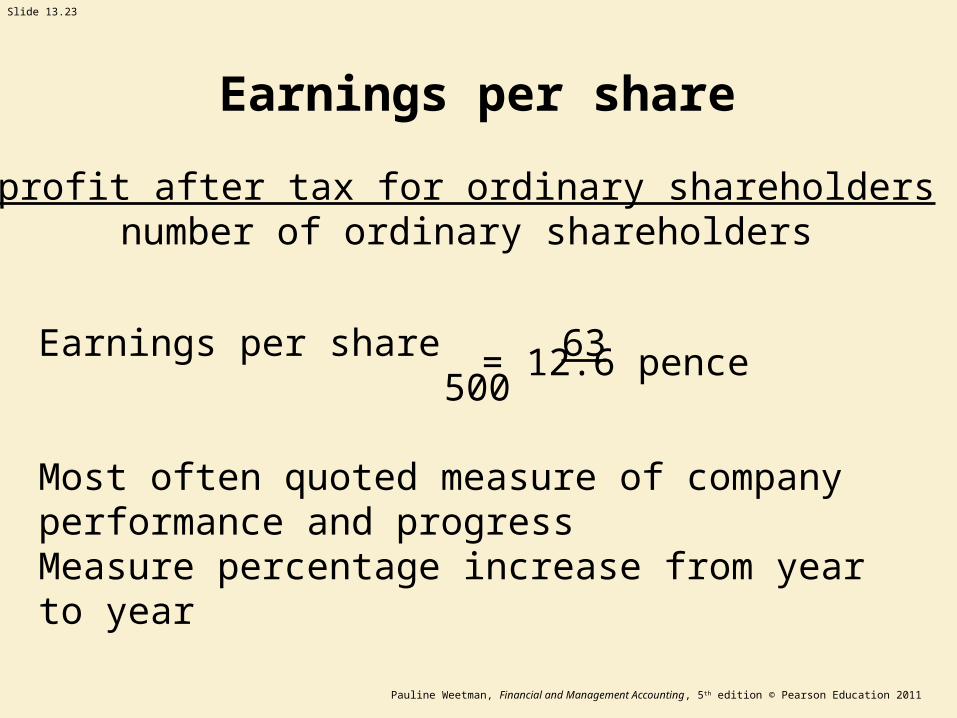

Earnings per share

Earnings per share 63 500

Most often quoted measure of company performance and progress Measure percentage increase from year to year

profit after tax for ordinary shareholdersnumber of ordinary shareholders

= 12.6 pence

Slide 13.24

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Price earnings ratio

Price earnings ratio 277 pence 12.6 pence

• Compares the amount invested by the shareholder in the company with the earnings per share. Number of years current profit represented by share price.

• Reflects market's confidence in future prospects of the company.

• Compare with average P/E for the industry, given daily in the Financial Times.

• Commonly used as a basis for investment decisions.

share priceearnings per share

= 22 times

Slide 13.25

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dividend per share

Dividend payable to ordinary shareholdersNumber of issued shares

• Of immediate interest to many investors. Dividend is the most immediate reward for share ownership.

• Most companies attempt to maintain a consistently increasing trend.

• Reduction in dividend per share is often only proposed by management as a last resort.

Dividend per share 30 = 6 pence per share 500

Slide 13.26

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dividend cover 12.6 p = 2.1 times 6.0 p

• Number of times dividend can be paid out of current earnings.

• The higher the dividend cover, the ‘safer’ the dividend.

Dividend cover (payout ratio)

earnings per sharedividend per share

Slide 13.27

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dividend yield 6.0 x 100% = 2.17% 277

• Compares dividend per share with the amount invested by the shareholder.

• Might seem low yield compared to other types of investment.

• Dividends are not the only benefit from share ownership. There is an expectation of an increase in share price. Retained profits generate growth in future profits.

Dividend yield

Dividend per share x 100% Share price

Slide 13.28

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Management performance

Slide 13.29

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Return on shareholders’ equity

Profit after tax x 100%Share capital + reserves

Return on shareholders’ equity 63 x 100% = 7.2% 880

•Performance of company from the shareholders' perspective.

•Essential to use profit after tax and after interest charges.

Slide 13.30

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Return on capital employed

Operating Profit (before interest and tax) x 100% (Total assets – current liabilities)

Return on capital employed

129 x 100 = 10.1%1,280

•Performance of company as a whole. •Measure of management efficiency. •Relates to all sources of long term finance.

Slide 13.31

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Operating profit on sales

Operating profit (before interest and tax) x 100% Sales (revenue)

Operating profit on sales129 x 100 = 17.9%720

‘Operating profit margin’ the higher the better. Reflects • degree of competitiveness in the market economic

situation. • ability to distinguish products.• ability to control expenses.

Slide 13.32

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Gross profit percentage 288 x 100 = 40%720

• Concentrates on costs of making goods and services ready for sale.

• Small changes in this ratio can be highly significant. • There tends to be a ‘normal’ value for each industry.

Gross profit ratio

Gross profit x 100%Sales (revenue)

Slide 13.33

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Total assets usage 720 = 0.52 times (1,155 + 220)

• Indicates how well a company has used its productive capacity.

• Use in trends of what has happened over time.

Total assets usage

Sales (revenue) Total assets

Slide 13.34

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Non-current (fixed) assets usage

Sales (revenue)_____ Non-current (fixed) assets

Non-current (fixed) assets usage 7201,155

Interpreted as how many £s of sales have been generated by each £ of assets i.e. 62 pence of sales for each £1 of non-current (fixed) asset investment.

= 0.62 times

Slide 13.35

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Liquidity and working capital

Slide 13.36

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Current Ratio 220:95 = 2.3:1Are short-term assets adequate to settle short-term liabilities? If less than 1:1, look closely at cash flow. Ability to generate daily cash might make this ratio adequate, for example, a retailer selling to the publicmust look at norm for the industry.Usually between 1.5:1 and 2:1 for manufacturing industry.

Current assets:current liabilities

Current ratio

Slide 13.37

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Acid test

Current assets minus inventory (stock):Current liabilities

The acid-test (220 – 115) : 95 = 1.11:1

Places emphasis on the most liquid assets.

Excludes inventory (stock).

Expected around 1:1 but varies from industry to industry.

Slide 13.38

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

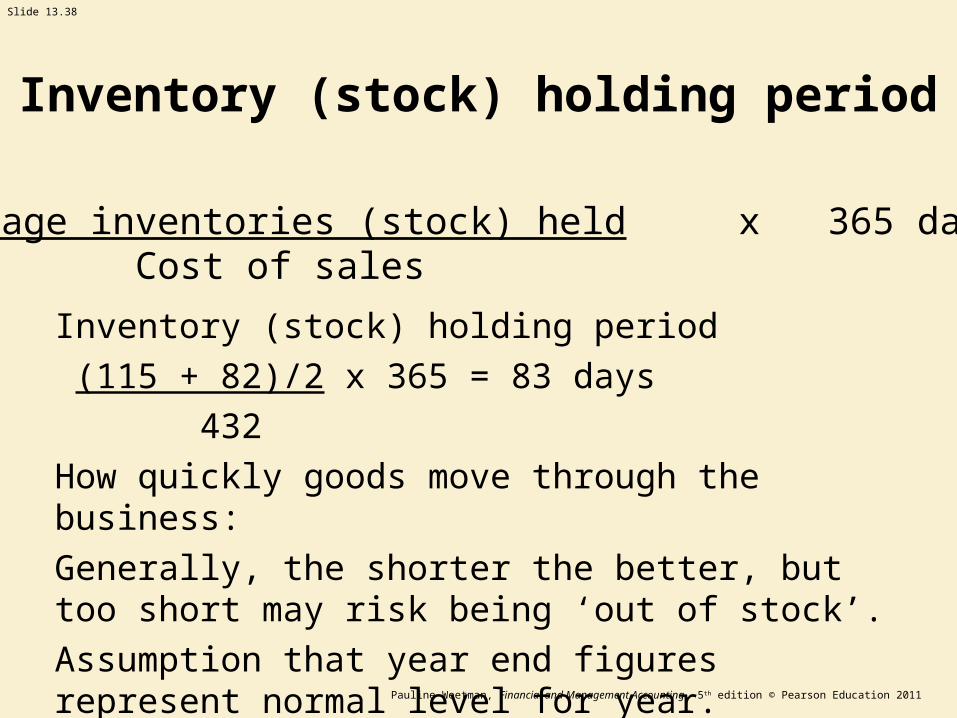

Inventory (stock) holding period

(115 + 82)/2 x 365 = 83 days

432

How quickly goods move through the business:

Generally, the shorter the better, but too short may risk being ‘out of stock’.

Assumption that year end figures represent normal level for year.

Inventory (stock) holding period

Average inventories (stock) held x 365 days Cost of sales

Slide 13.39

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Customers collection period 89 x 365 = 45.1 days720

Speed of collecting from credit customers.

Compare with the credit period given, or the normal credit period for the industry.

Customers (debtors) collection period

Trade receivables (debtors) x 365 Credit sales (revenue)

Slide 13.40

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Purchases = Cost of sales + closing inventory (stock) – opening inventory (stock)432 + 115 – 82 = 465(If no purchases figure, use cost of sales)

Suppliers payment period45 x 365 = 35.3 days465

Suppliers payment period

Trade payables (creditors) x 365 Credit purchases

Slide 13.41

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Suppliers payment period (Continued)

(If no purchases figure, use cost of sales)Suppliers payment period45 x 365 = 35.3 days465

• Paying too fast – risk of cash shortage.• Paying too slowly – risk of losing supplier.• Companies must disclose this information in

the directors’ report.

Slide 13.42

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Working capital cycle Inventory (stock) holding period +Customers collection period –Suppliers payment period

Inventory (stock) holding 83.2 days

Debtor collection 45.1 days

127.3 days

Creditor payment 35.3 days

Finance needed for 92.0 days

Working capital cycle

Slide 13.43

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Gearing

Slide 13.44

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Gearing

Long-term loans x 100%Ordinary share capital + reserves

Debt/equity ratio 400 x 100 = 45.5% 880Most often quoted in the financial press. A high figure indicates reliance on sources of long-term loan finance. ‘Long-term loan’ includes short-term portion of loans, in current liabilities in balance sheet.Also, bank overdraft, if a permanent feature.Interest payments must always be met, so company has exposure to interest rate movements.

Slide 13.45

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Interest cover

profit before interest and taxes interest charge

Interest cover 129 = 5.38 times 24Indicates how ‘safe’ the annual interest payments are in relation to profit.Indicates how many times profits can fall before the company is unable to cover payments out of current profits.

Slide 13.46

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Cash flow statement

• See Supplement to Chapter 13 in the book

Slide 13.47

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Definitions

EBITDAEarnings before deducting:• Interest• Taxation• Depreciation• Amortisation• An approximation to cash flowFree cash flow• No precise definition but used to reflect operating

cash flow minus capital expenditure – ‘free’ for future investment or for paying dividends.