Slide 1 FastFacts Feature Presentation 12/04/2013 To dial in, use this phone number and participant...

37

Slide 1 FastFacts Feature Presentation 12/04/2013 To dial in, use this phone number and participant code… Phone number: 888-651- 5908 Participant code: 182500 To participate via VoIP… You must have a sound card You must have headphones or computer speakers © 2012 The Johns Hopkins University. All rights reserved.

-

Upload

rosalyn-gilbert -

Category

Documents

-

view

216 -

download

0

Transcript of Slide 1 FastFacts Feature Presentation 12/04/2013 To dial in, use this phone number and participant...

Slide 1

FastFactsFeature Presentation

12/04/2013

To dial in, use this phone number and participant code…

Phone number: 888-651-5908 Participant code: 182500

To participate via VoIP…

You must have a sound card

You must have headphones or computer speakers

© 2012 The Johns Hopkins University. All rights reserved.

Slide 2

Today’s TopicWe’ll be taking a look at…

Research Audits: The Inside Scoop

Common Research-Related Audit Findings and Tips for Avoiding Them

Slide 3

Today’s Presenter

Jim JarrellDirector of Research and Operational AuditsOffice of Hopkins Internal AuditsContact: [email protected]

443-997-6393

Slide 4

Session Segments

PresentationJim Jarrell will discuss the role of Internal Audit at Johns Hopkins, what auditors look at when conducting an audit, the high risk areas, and the best practice approach to these areas.

During Jim’s presentation, your phone will be muted.Q&A

After the presentation, we’ll hold a Q&A session. We’ll open up the phone lines, and you’ll be able to ask questions. Jim will answer as many of your questions as time allows.

Slide 5

Contact Us

If you would like to submit a question during the presentation or if you’re having technical difficulties, you can email us at: [email protected] can also send us an instant message!

GoogleTalk – [email protected] Instant Messenger – HopkinsFastFactsMSN – [email protected]

Slide 6

Survey

SurveyAt the end of this FastFacts session, we’ll ask you to complete a short survey. Your honest comments will help us to enhance and improve future FastFacts sessions.

Slide 7

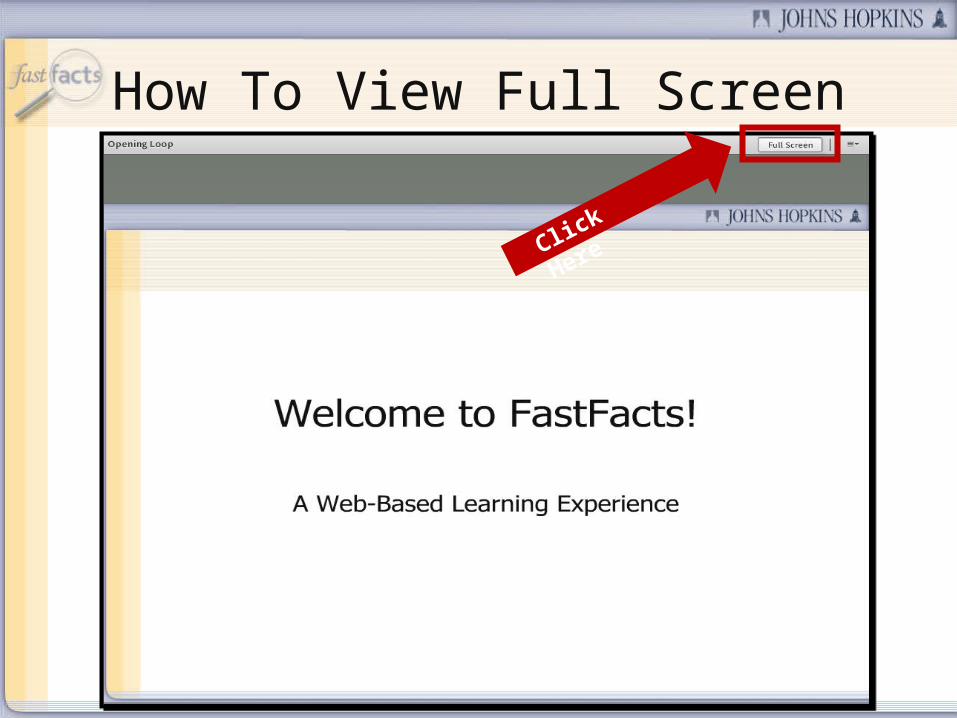

How To View Full Screen

Click Here

Slide 8

Research Audits: The Inside Scoop

Slide 9

Agenda

After today’s presentation you will be able to:

• Describe the role of Internal Audit at Johns Hopkins and the services they provide

• Identify the highest areas of risk in research compliance.• Develop effective internal controls to protect the

institution from adverse risk• Champion best practices for research compliance in your

department.

Slide 10

Who are we..and what do we do?

OHIA – Office of Hopkins Internal Audit

•Shared-Service Organization•Independent•Assess the effectiveness of procedures in place to manage risk•Investigate fraud•Champion of best practices related to internal control

Slide 11

Preventing Fraud

Characteristics of FraudKnowing who to call:

Internal AuditFraud Hotline – 1-877-WE-COMPLY

Establish Effective Control ProceduresProper approvalIndependent and timely reconciliation

Slide 12

Research Compliance Roles

Slide 13

Lessons Learned from Recent Audits

Utilization of Research Compliance DashboardSeparation of Pre- and Post-Award Duties

Removes competing prioritiesProficiency in SAP and BW Reporting Tools

The data is available, use itFinancial expertise of staffAccountability

Include post-award responsibilities in performance evaluations of staffMakes post-award duties a priority

Pro-active approach to Service Centers – don’t simply rely on them

Slide 14

High Research Compliance Risk Areas

Effort Reporting

Cost Transfers

Account Reconciliation

Sub-recipient Monitoring

Other High-Risk Areas Not Included in this Presentation

Human Subjects

Animal Care and Use

Slide 15

Effort Reporting

Effort Reporting

Largest expense charged to Federal awards

High-risk transaction - 2003 settlement - $2.3m

Not limited to 40 hours per week, but includes all time

Should be certified as soon as possible

Managing committed effort

Slide 16

Effort Reporting – What We Look At

Effort Reporting

Timely and proper certification

Allowability of Effort Charged to the Awards

Salary CAP Compliance

Administrative Salaries

Slide 17

Effort Reporting Best Practices

Ways to Avoid Effort Related Findings

Ensure certification by individual with first-hand knowledge

Review/Reconcile salaries charged to awards each pay period

Be knowledgeable of individual’s activities

Engage and train faculty on effort requirements

Escalate when necessary

Slide 18

Cost Transfers

Cost TransfersConsistent area of federal enforcementIndicator of account reconciliation process

– No cost transfers could mean no reconciliation– Late cost transfers indicate untimely reconciliation– Too many cost transfers could mean ineffective front end

controls

Slide 19

Cost Transfers – What We Look At

Cost Transfers

Allowability of cost transfers

Documentation to support costs

Rationale for making transfer

Slide 20

Cost Transfer Best Practices

Ways to Avoid Transfer Related Findings

Document the why’s and how’s

Carefully scrutinize transfers onto the award near the project end

Validate supporting documentation

Don’t transfer unallowable costs to spend down available funding

Slide 21

Account Reconciliation - Project Procurement

No one should control of all aspects of a transaction

A-21 governs grants

All purchases must relate to the award being charged

Competitive bidding to ensure costs are reasonable

Documentation should be maintained

Administrative and clerical costs can only be charged if:Required by project’s scope of workSpecifically identified in approved budgetCan be identified with a high-degree of accuracy

Slide 22

Account Reconciliation – What We Look At

Account ReconciliationDetective ControlDocumented evidence of monthly reconciliationsCorroborating Evidence

Allowability of chargesTimeliness of cost transfersEffort Reporting

Slide 23

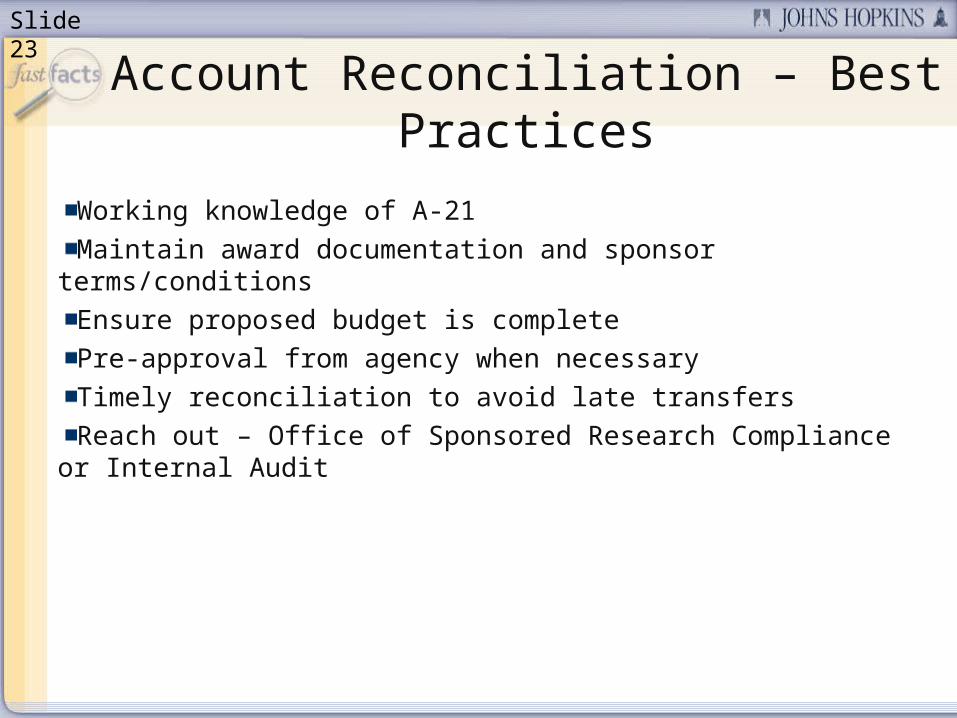

Account Reconciliation – Best Practices

Working knowledge of A-21Maintain award documentation and sponsor terms/conditionsEnsure proposed budget is completePre-approval from agency when necessaryTimely reconciliation to avoid late transfersReach out – Office of Sponsored Research Compliance or

Internal Audit

Slide 24

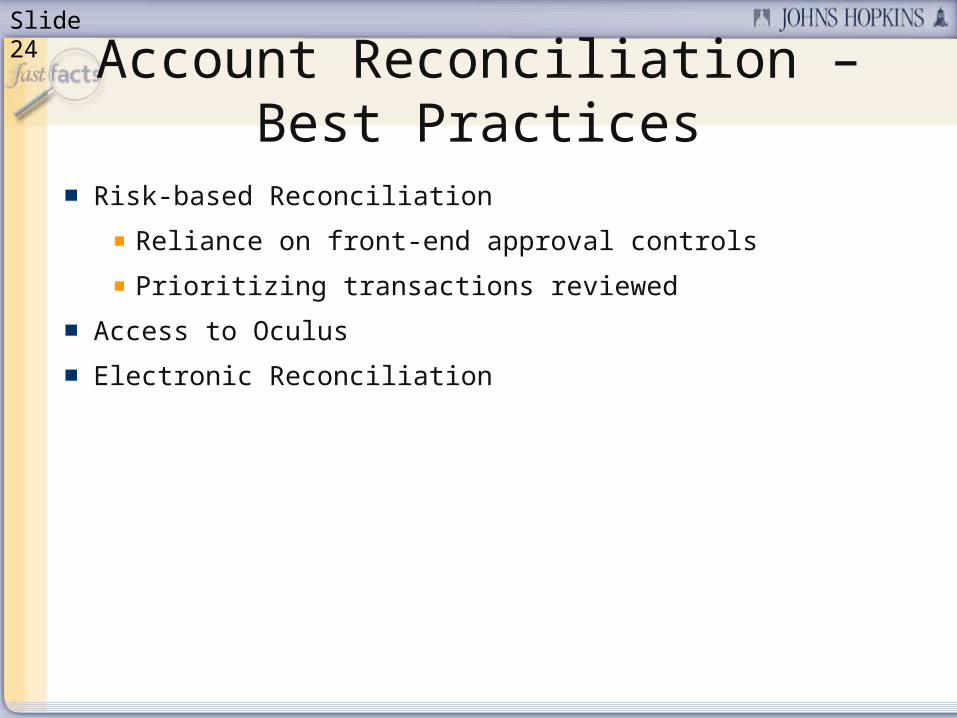

Account Reconciliation – Best Practices

Risk-based Reconciliation

Reliance on front-end approval controls

Prioritizing transactions reviewed

Access to Oculus

Electronic Reconciliation

Slide 25

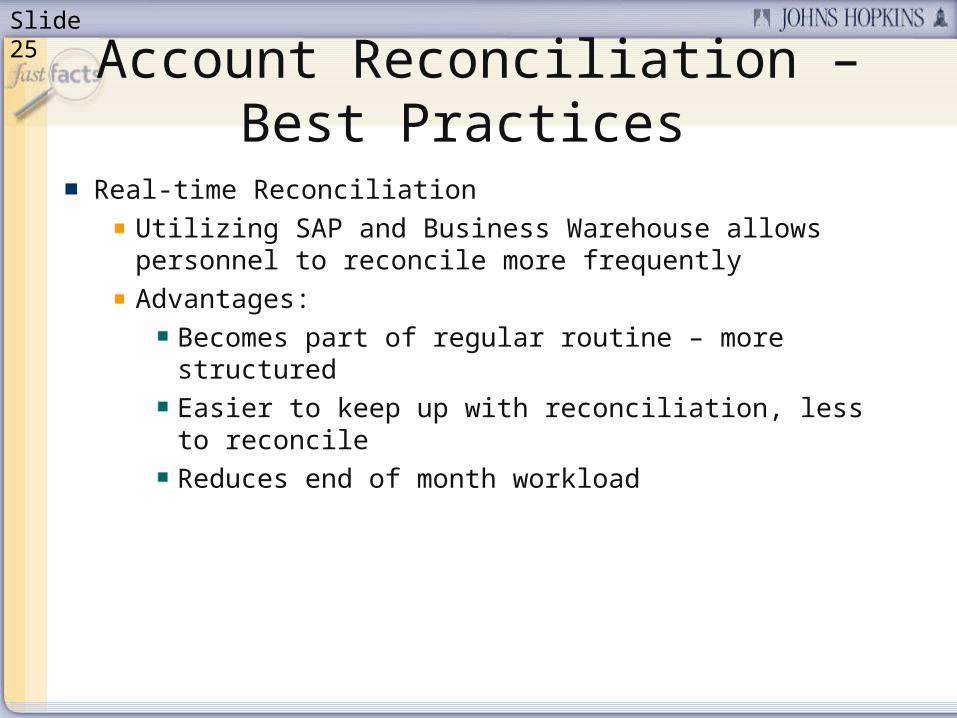

Account Reconciliation – Best Practices

Real-time ReconciliationUtilizing SAP and Business Warehouse allows personnel to reconcile more frequentlyAdvantages:

Becomes part of regular routine – more structuredEasier to keep up with reconciliation, less to reconcileReduces end of month workload

Slide 26

Sub-recipient Monitoring

Sub-recipient Monitoring

Significant area of risk

JHU ultimately accountable to the sponsor for sub-

recipient funding

Principal Investigator (PI) is ultimately responsible

Risk mitigation needs to begin prior to contracting

Slide 27

Sub-recipient Monitoring – What We Audit

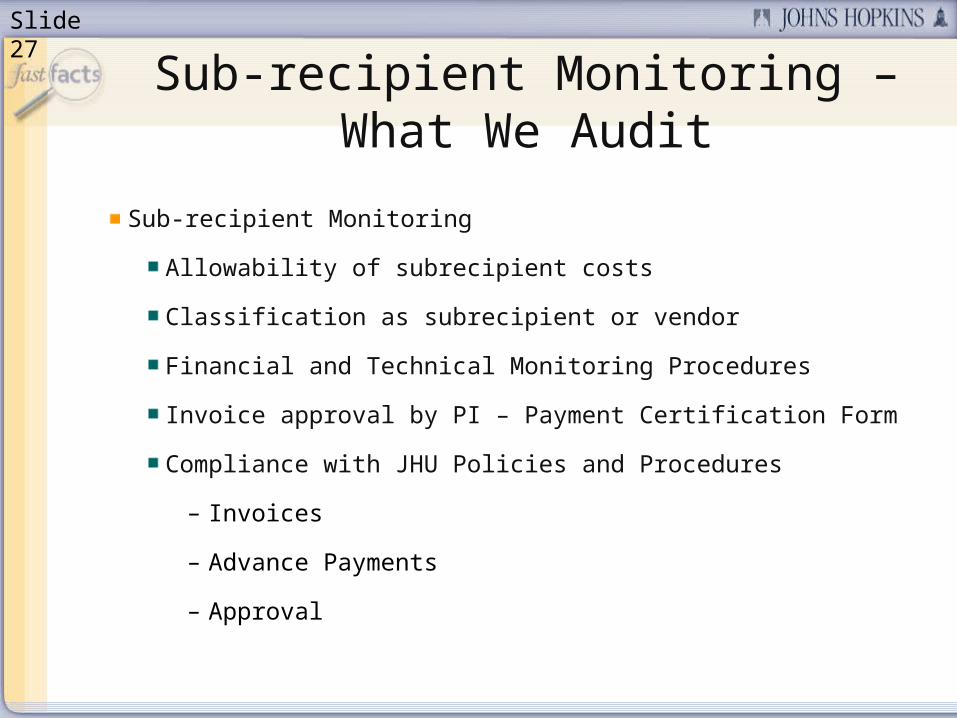

Sub-recipient Monitoring

Allowability of subrecipient costs

Classification as subrecipient or vendor

Financial and Technical Monitoring Procedures

Invoice approval by PI – Payment Certification Form

Compliance with JHU Policies and Procedures

– Invoices

– Advance Payments

– Approval

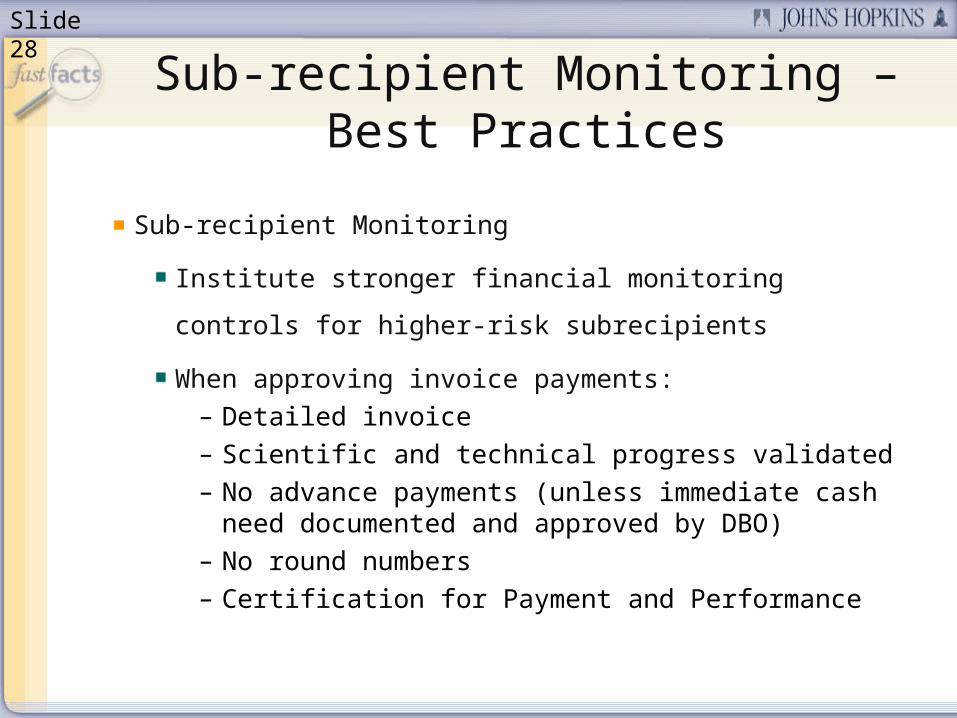

Slide 28

Sub-recipient Monitoring – Best Practices

Sub-recipient Monitoring

Institute stronger financial monitoring controls for

higher-risk subrecipients

When approving invoice payments: – Detailed invoice– Scientific and technical progress validated– No advance payments (unless immediate cash need

documented and approved by DBO)– No round numbers– Certification for Payment and Performance

Slide 29

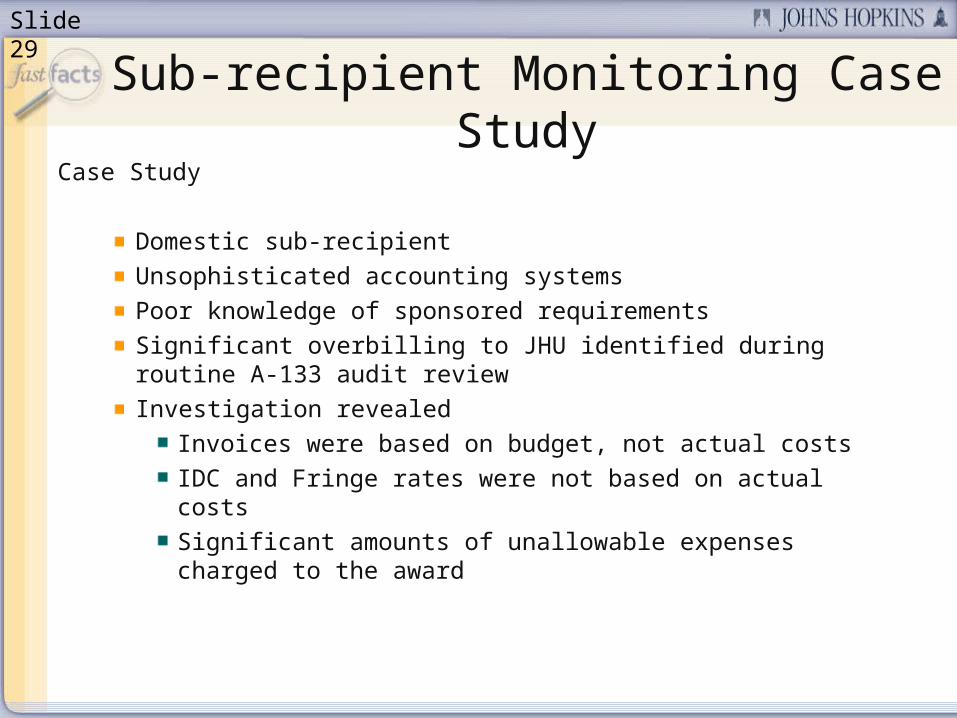

Sub-recipient Monitoring Case Study

Case Study

Domestic sub-recipientUnsophisticated accounting systemsPoor knowledge of sponsored requirementsSignificant overbilling to JHU identified during routine A-133 audit reviewInvestigation revealed

Invoices were based on budget, not actual costsIDC and Fringe rates were not based on actual costsSignificant amounts of unallowable expenses charged to the award

Slide 30

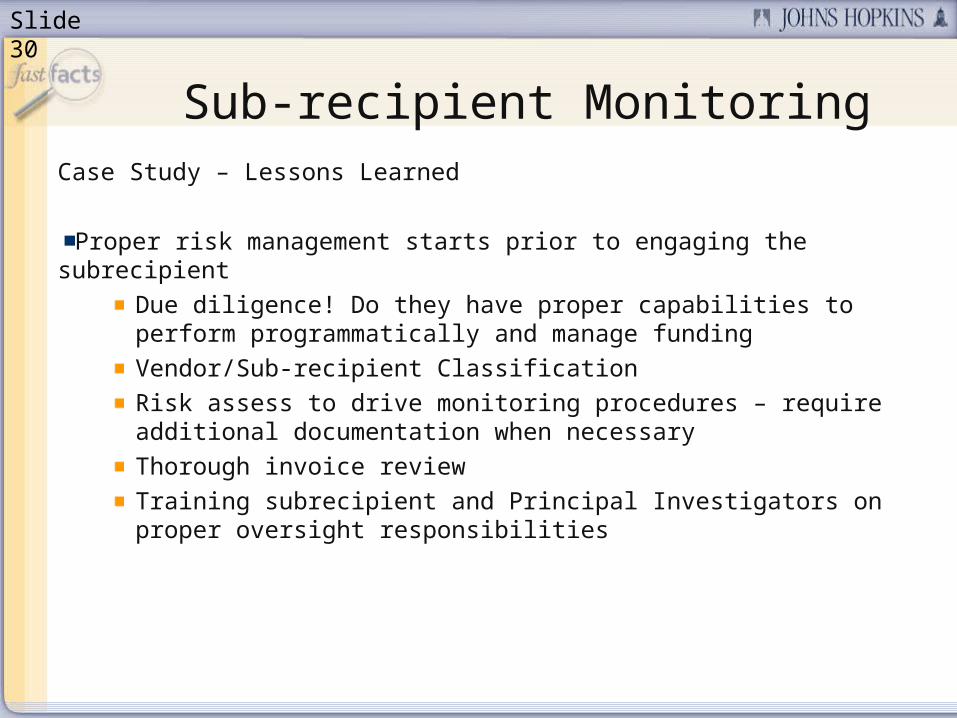

Sub-recipient MonitoringCase Study – Lessons Learned

Proper risk management starts prior to engaging the subrecipientDue diligence! Do they have proper capabilities to perform programmatically and manage fundingVendor/Sub-recipient ClassificationRisk assess to drive monitoring procedures – require additional documentation when necessaryThorough invoice reviewTraining subrecipient and Principal Investigators on proper oversight responsibilities

Slide 31

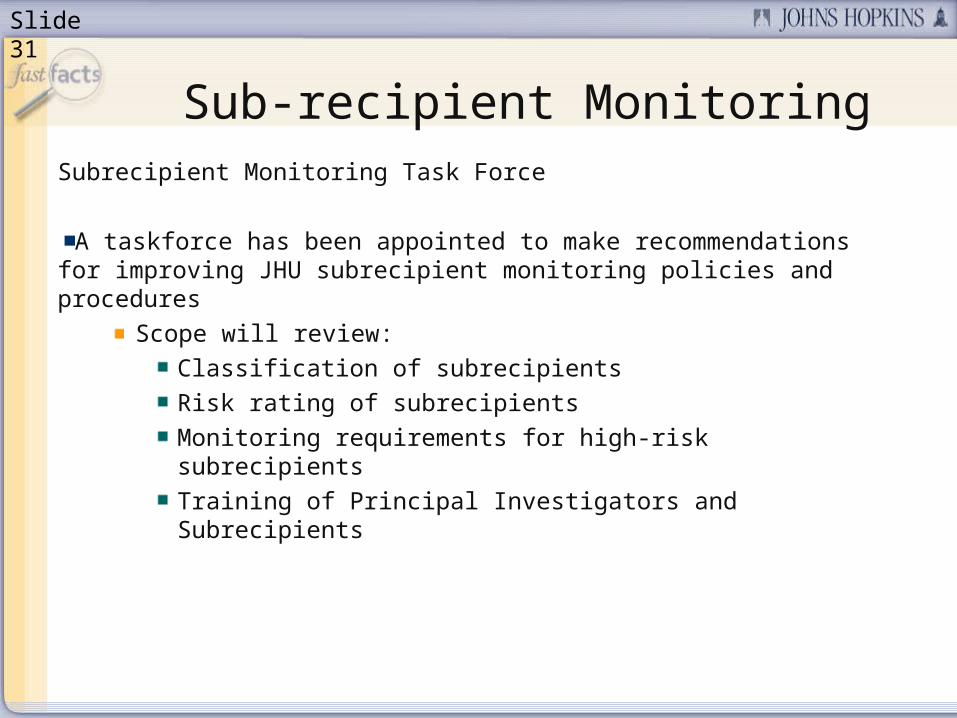

Sub-recipient MonitoringSubrecipient Monitoring Task Force

A taskforce has been appointed to make recommendations for improving JHU subrecipient monitoring policies and procedures

Scope will review:Classification of subrecipientsRisk rating of subrecipientsMonitoring requirements for high-risk subrecipientsTraining of Principal Investigators and Subrecipients

Slide 32

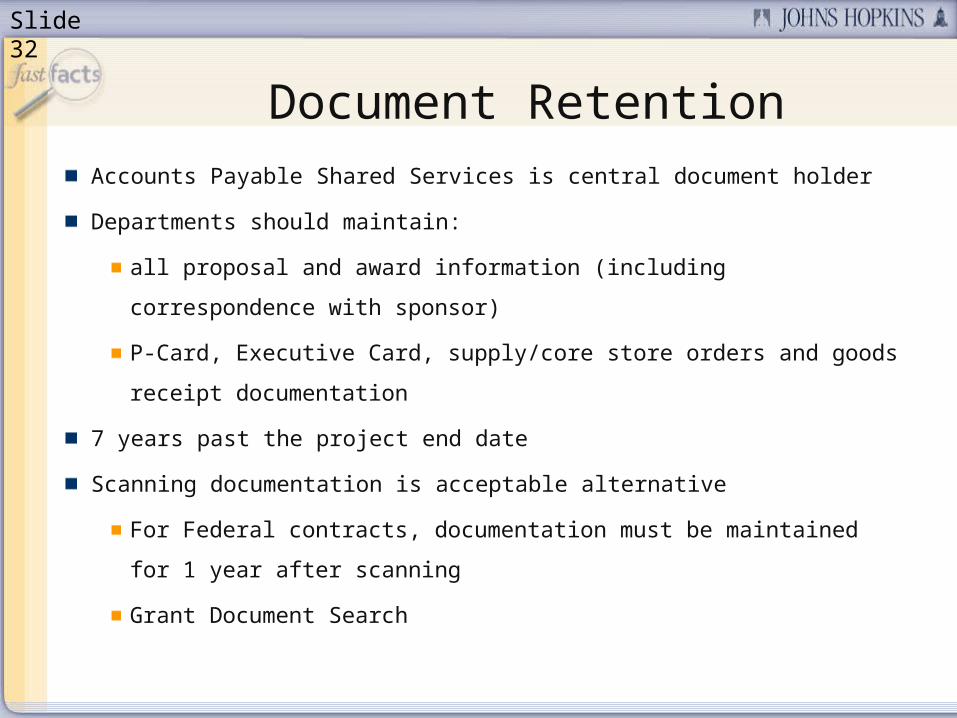

Document RetentionAccounts Payable Shared Services is central document holder

Departments should maintain:

all proposal and award information (including correspondence

with sponsor)

P-Card, Executive Card, supply/core store orders and goods

receipt documentation

7 years past the project end date

Scanning documentation is acceptable alternative

For Federal contracts, documentation must be maintained for 1

year after scanning

Grant Document Search

Slide 33

Conclusion

Internal Audit is a shared service organization championing the value of internal control throughout institutionThere are a number of high risk audit areas in the research compliance world that departmental personnel must be aware ofDepartments must remain vigilant and put procedures in place to reduce the potential for adverse risk eventsIn doing so, departments not only protect themselves, but protect the reputation of the Institution

Slide 34

We’re going to open the phone lines now!

There will be a slight pause, and then a recorded voice will provide instructions on how to ask questions over this conference call line.

We’ll be answering questions in the order that we receive them.

We’ll also be answering the questions that were emailed to us during the presentation.

If there’s a question that we can’t answer, we’ll do some research after this session, and then email the answer to all participants.

Q&A

Slide 35

Thank You!

Thank you for participating!We would love to hear from you.

Are there certain topics that you would like us to cover in future FastFacts sessions?Would you like to be a FastFacts presenter?Please email us at: [email protected]

Slide 36

Survey

Before we close, please take the time to complete a short survey.Your feedback will help us as we plan future FastFacts sessions.Click this link to access the survey… http://connect.johnshopkins.edu/fastfactssurvey/

Thanks again!

Slide 37

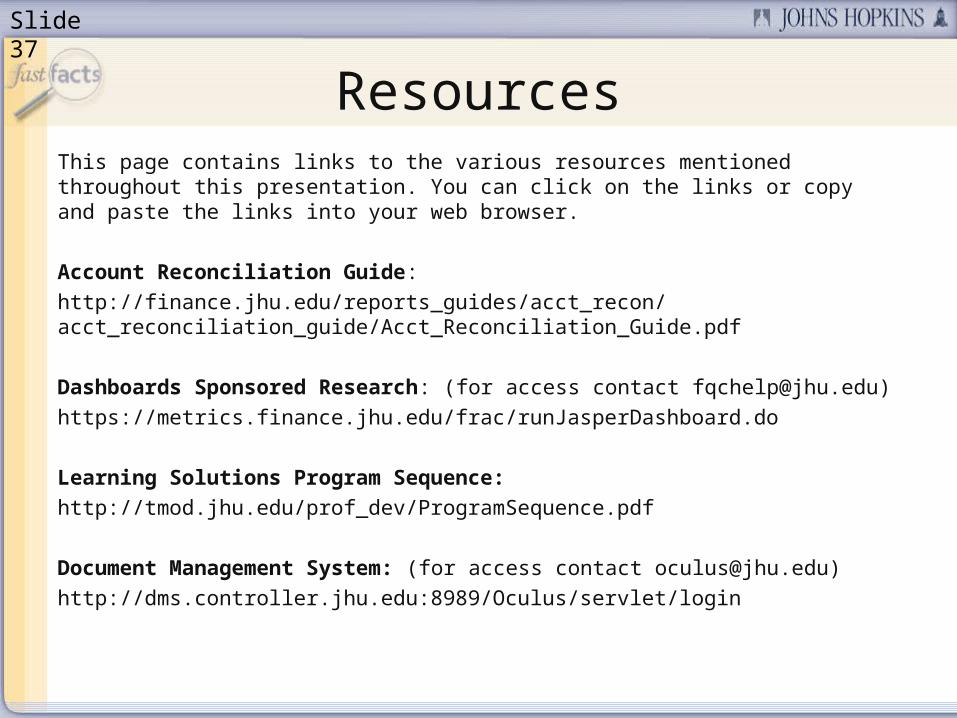

ResourcesThis page contains links to the various resources mentioned throughout this presentation. You can click on the links or copy and paste the links into your web browser.

Account Reconciliation Guide:http://finance.jhu.edu/reports_guides/acct_recon/acct_reconciliation_guide/Acct_Reconciliation_Guide.pdf

Dashboards Sponsored Research: (for access contact [email protected]) https://metrics.finance.jhu.edu/frac/runJasperDashboard.do

Learning Solutions Program Sequence:http://tmod.jhu.edu/prof_dev/ProgramSequence.pdf

Document Management System: (for access contact [email protected])http://dms.controller.jhu.edu:8989/Oculus/servlet/login