Slicing The Knowledge Based Economy in Brazil, China and ...€¦ · SAP 124 GER Mahindra BT 113 JV...

27

Globelics Academy June 1, 2004 Slicing The Knowledge Based Economy in Brazil, China and India: A Tale of 3 Software Industries FRANCISCO VELOSO (Carnegie Mellon University & UCP) ANTONIO J BOTELHO (Center for New Economy and Technology, PUC-RIO) TED TSCHANG (Singapore Management University and ADBi) ALICE AMSDEN (Massachusetts Institute of Technology) GIANCARLO STEFANUTO (SOFTEX) – in Brazil Chapter

Transcript of Slicing The Knowledge Based Economy in Brazil, China and ...€¦ · SAP 124 GER Mahindra BT 113 JV...

Globelics Academy June 1, 2004

Slicing The Knowledge Based Economy in Brazil, China and India:

A Tale of 3 Software Industries

FRANCISCO VELOSO (Carnegie Mellon University & UCP)ANTONIO J BOTELHO(Center for New Economy and Technology, PUC-RIO)TED TSCHANG(Singapore Management University and ADBi)ALICE AMSDEN (Massachusetts Institute of Technology)GIANCARLO STEFANUTO(SOFTEX) – in Brazil Chapter

The International Software Market

How to ride the global software & services market?– Value for 2001: USD 300 Billion– Value for 2008: USD 900 Billion (estimate)

Packaged software market– Sales of $ 196 Billion in 2001– Traded share of sales is 15%

Software related services – Market smaller than products– Traded share is 35%

Offshore / outsourcing (BPO) exhibits strongest growth– in the US, 25% per year– In Europe, it will double between 2002 and 2005

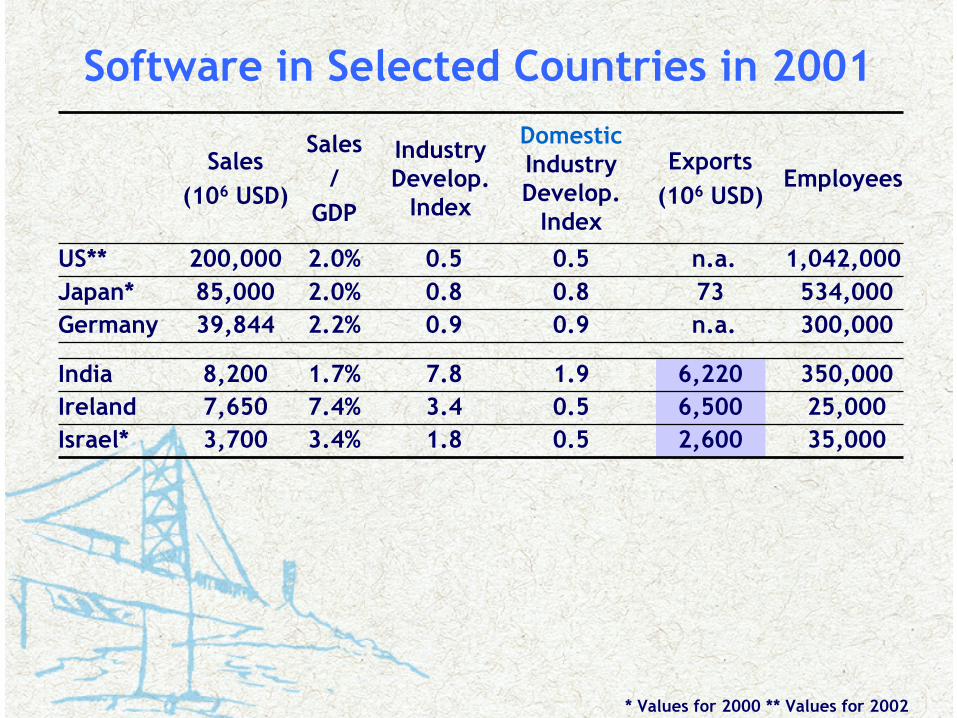

Software in Selected Countries in 2001

35,000 2,6000.51.8 3.4%3,700Israel*25,000 6,5000.53.4 7.4%7,650Ireland 350,000 6,2201.97.8 1.7%8,200India

300,000 n.a. 0.90.9 2.2%39,844Germany534,000 730.80.8 2.0%85,000Japan*

1,042,000 n.a. 0.50.5 2.0%200,000US**

EmployeesExports

(106 USD)

DomesticIndustry Develop.

Index

Industry Develop.

Index

Sales/

GDP

Sales(106 USD)

* Values for 2000 ** Values for 2002

Single Track?

Emerging Prescriptions from the 3 I’s?

Nurture a Strong Human Capital Base

Foster Entrepreneurship

Develop a Large Export Base

Establish Strong Anchor to the US Market– Export Base– Multinational Investment

Leverage the US Links– Diaspora– English– Culture

Size and Growth of Software

8,2007,4007,700Sales in 2001

3906951,100Sales in 1992

40%30%24%Annual Growth Rate

IndiaChinaBrazilMillion of USD*

*Conversions of Local Currency to USDEvolution of values in USD highly influenced by exchange rate fluctuations during decade

Software in Selected Countries in 2001

35,000 2,6000.51.8 3.4%3,700Israel*

25,000 6,5000.53.4 7.4%7,650Ireland

n.a.35 1.11.1 1.8%7,694Korea158,000 1002.22.2 1.5%7,700Brazil

n.a.n.a. 0.20.2 <0.2%<1,000Mexico15,000350.40.4 0.5%1,340Argentina*

n.a.349 0.60.7 1.2%3,801Taiwan186,000 4001.71.8 0.6%7,400China

350,000 6,2201.97.8 1.7%8,200India

300,000 n.a. 0.90.9 2.2%39,844Germany534,000 730.80.8 2.0%85,000Japan*

1,042,000 n.a. 0.50.5 2.0%200,000US**

EmployeesExports

(106 USD)

DomesticIndustry Develop.

Index

Industry Develop.

Index

Sales/

GDP

Sales(106 USD)

* Values for 2000 ** Values for 2002

Preconditions:Education, Research and Technology

2nd1st5th3rdWorld Rank (2001)Population

170159292700/ 106 pop (1997)NS&Eng Grad

51644585/ 1,000 pop (2001)PCs

3.9%5.7%8.3%7.9%% GDP (2001)ICT Expenses

6932101180/ 106 pop (2000)IT Graduates

71,00041,00017,84751,236Total / Year (2000)IT Graduates

176,000203,23850,233199,057Total / Year (1997)NS&Eng Grad

IndiaChinaBrazilUSUnits (year)Variable

Market Structure in Brazil, China & India

8,2007,4007,700Sales

350,000186,000158,000Employees

2,8005,7005,400Software Firms

n.a.10,00010,700Firms w/ Software Activity

76%5.5%1.5%Exports

20%42%44%ProductsMarket Focus

80%58%56%Services

IndiaChinaBrazil

Leading Firms in the 3 Nations CHINAINDIABRAZIL

US26InformixIN64MasconBR52ProcedaUS30SybaseIN66MphasisBR57CITSUS58OracleIN82I-Flex BR62DBAUS65MicrosoftIN84NIITBR64CPqDUS78IBMIN84MascotBR72MicrosigaCN93TopJV94HCL PerotUS77ConsistCN94CVICIN96PentasoftBR104PolitecCN107YianTaiJV113Mahindra BTGER124SAPCN115T.DongFangIN126SilverlineUS182OracleCN125ChangTianIN153PatniUS194AccentureCN126ChongRanIN277HCL TechBR204CPMCN134DongFangIN357SatyamUS240EDSCN175LegendIN481WiproUS260Comp. As.CN186PuTianIN535InfosysBR372SERPROCN438FounderIN813TCSUS362Microsoft

OriginSalesCompanyOriginSalesCompanyOriginSalesCompany

Understanding Role of Multinationals

Local competitors in products and services– May affect local producers – but also strengthens market

• e.g. SAP competes with local ERP Producers

– The realities…• Stronger in Brazil• Moderate in China and India

Local market as base for development in international arena– Supports local industry and is welcomed

• e.g. Siemens PBX in Brazil or TI development center in India

– The realities• Strong in India• Moderate to low in Brazil and China

India – China – Brazil Considerations

•Export Higher Level Services in Verticals

•Export Products

•Export Services•Hardware Links•Multinationals

•Business Process Outsourcing

•High Level Export Services

Opportunities

•Small Firms•International Visibility

•No Active Policy

•Domestic Market•Strong Client Sectors

•Verticals –Prod+Serv

•ProductsBrazil

•Process Capability•Small Firms•Open Market Experience

•Government Action•Strong Domestic Market

•System Integration

•ProductsChina

•Wage Pressure•Domain Knowledge•Low-End Competition

• Deep Labor Pool• English•Process Maturity• Global Links

•Low Tech Services

•ExportsIndia

BarriersDifferentiatorsFocus

Conclusions & Takeaways for 3 Nations

Large and over-developed industries– Sell USD 8 Billion in Software– Annual growth rates on the order of 30%

Preconditions for past success & bright future– Demand at home and/or abroad– Human and financial capital– Government policy - can have stifling or leveraging effects

Industry development may follow different paths– Critical to find the right development anchor!– Strong service exports for India– Vibrant domestic products/services for Brazil and China

Challenges ahead remain…– Competition between nations will become more acute– Important to leverage industry strengths – Multinationals will play increasing role– NO SET WINNERS!

Paths for China and India

CHINA: A low level but strengthening industry

Sector Linkages – Users and manufacturersExport Services – Replacing India in low levelSpillovers of multinational interest in China

NEED: Process Capabilities & International Marketing

INDIA: Tension between value and volume

Climbing service value chain & enter product marketsInvest in BPO, ITES and other Face multinational competition with domestics

NEED: Product/Domain Knowledge

What About Brazil?

The Brazilian Software Industry

0%

5%

10%

15%

20%

25%

CAGR 1991/2001

GDP (USD) IT (USD) SW (USD)*

4.1Software Services

(Outsourcing, Development, Integration and Consultancy)

3.6Software Products (Package, Custom and Embedded)

7.7Total Software (Products and Services)

Billion of USD

Sales in 2001

* 1992/2001

Indicators of Domestic Competitiveness

11%~300%Growth 1995-2000 (%)

3.8%8%R&D / Sales* (%)

1130Average Salary (103 R$/Year)

2697VA / Employee (103R$)

IndustrySoftware

*Probably Includes Substantial Costs Associated to Product Development

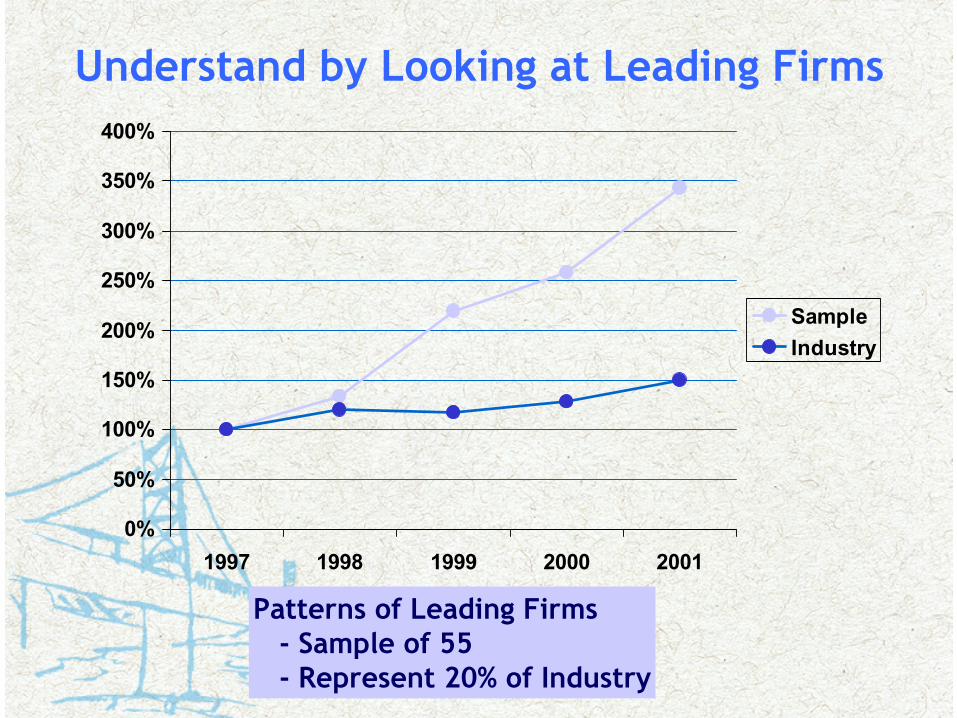

Understand by Looking at Leading Firms

0%

50%

100%

150%

200%

250%

300%

350%

400%

1997 1998 1999 2000 2001

SampleIndustry

Patterns of Leading Firms - Sample of 55- Represent 20% of Industry

Nature of the Leading Firms

14%7%Low Value Services

62%35%High Value Services

42%Services

10%20%Customizable Product

13%34%Embedded/Component

58%Products

Share of Revenue

Share of FirmsBusiness Model

Share of Firms

Main Revenue Source

Sample: 56 Firms

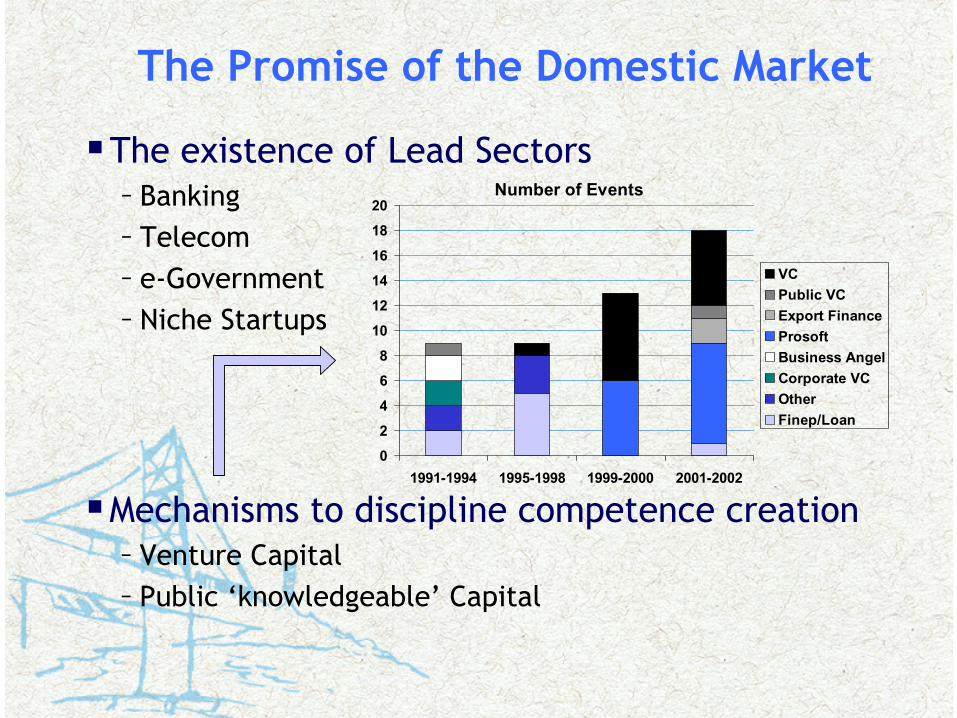

The Promise of the Domestic Market

The existence of Lead Sectors– Banking– Telecom– e-Government– Niche Startups

Internationalized and Competitive

Large IT investment – 30% of Brazil Total

Important Market for Software companies– Foreign, Local Large & Small-Specialized

Test bed for Innovation

The Promise of the Domestic Market

The existence of Lead Sectors– Banking– Telecom– e-Government– Niche Startups

Mechanisms to discipline competence creation– Venture Capital– Public ‘knowledgeable’ Capital

Number of Events

0

2

4

6

8

10

12

14

16

18

20

1991-1994 1995-1998 1999-2000 2001-2002

VCPublic VCExport FinanceProsoftBusiness AngelCorporate VCOtherFinep/Loan

The Effects of External Financing

Definition of a Clear Business Model– Preparation of Detailed Business Plans– Work with Outside Consultants– Positive Impact of both Private and Public VC

Restructuring of the Management Structure– Hiring of Professional Managers– Restructuring of Management Responsibilities

An Example of a Lead Firm: Modulo– One of the top 30 Brazilian Firms– Got 2 rounds of VC financing from 1997 to 2001– From security software development to security component– Hired former CEO of American Express Latin America– Files Reports according to US GAAP rules

The Curse of the Domestic Market

Fast Growth of Domestic DemandLarge Captive Markets – Private and PublicJump to Foreign SolutionsHigh Interest Rates

Anti-Specialization Bias– Diversified activities for growing regional market – Not specialized work for whole country

Poor Institutions– Limited cooperation and no voice for the industry– Absence of a structured development policy

Small National Firms– Difficult to compete with foreign firms locally– Difficult to compete in international market

Going Abroad

Software Exports

0102030405060708090

100

1995 2000

Mill

ions

of U

SD

Export Strategy

Other6% VAR's

16%

Delegations Abroad

28% Internal/MNC Channels

50%

Software Exports

0500

10001500200025003000350040004500

Brazil1995

Brazil2000

China2000

India2000

Mill

ions

of U

SD

Lessons from Brazilian Observations

Alternative paths to the export path– Rely on Lead Client Sectors– Develop mechanisms that induce competence structuring

Recognize pitfalls created by domestic orientation– Anti-specialization bias– Limits to growth…

Important Challenges Remain– Have not succeeded the test of internationalization– Leaders in vertical segments are entering in higher level segments

more populated with large international suppliers

But outsourcing up scaling trend should benefit Brazil– Domain knowledge requirements and experience…

Development Paths for Brazil

BRAZIL: Exploring the International Market

Secure vertical Service exports (higher level)Exploit component & embedded softw. ProductsStimulate investment of software multinationalsStrengthen national positions…

NEED: Larger players – integrationNEED: Process certification or reputationNEED: International marketing/visibility – FlagNEED: Policy to influence specialization pattern

Policy Mechanisms and Tools for Brazil

Services Driven Policy– Process qualification– Use purchasing power to generate critical mass– Export benefits– Policy to support Multinational investment Brazil

Product Driven Policy– Stimulate Technology Transfer at all levels– Foster Entrepreneurial Capability– Support Development Costs– Generate export and foreign Installation benefits

Generic Policy– Continue support for ‘smart disciplining capital’– Create incentives for mergers– Continue education support – Help to generate ‘national software flag’– Reduce ‘Brazil Cost’

Thank You!

Support for this research:

Softex, IBM, Intel, Ministry of Science & Technology – BrazilADBi – India and China