"Constellations in the night sky": Mobile Media & the Landscapes of Cinemagoing

Sky Mobile Teach-In29th November 2016

2

Agenda

• Introduction and context Andrew Griffith

• Sky Mobile Stephen van Rooyen

• Sky Mobile network Mohamed Hammady

• Financials Andrew Griffith

• Q & A

3

Forward looking statements

This document contains certain forward looking statements with respect to the Group’s financial condition, results of operations and business, and our strategy,

plans and objectives for the Group. These statements include, without limitation, those that express forecasts, expectations and projections, such as forecasts,

expectations and projections in relation to new products and services, the potential for growth of free-to-air and pay television, fixed line telephony, broadband and

bandwidth requirements, advertising growth, DTH and OTT customer growth, On Demand, NOW TV, Sky Go, Sky Go Extra, Sky+ HD, Sky Q, Sky Store, Sky Online, mobile,

Multiscreen and other services penetration, revenue, administration costs and other costs, advertising growth, churn, profit, cash flow, products and our broadband

network footprint, content, wholesale, marketing, synergies and integration, and capital expenditure.

These statements (and all other forward-looking statements contained in this document) are not guarantees of future performance and are subject to risks,

uncertainties and other factors, some of which are beyond the Group's control, are difficult to predict and could cause actual results to differ materially from those

expressed or implied or forecast in the forward-looking statements. These factors include, but are not limited to, the fact that the Group operates in a highly

competitive environment and faces competition from a broad range of organisations, the effects of laws and government regulation upon the Group's activities, the

fact that the Group’s business is based on a subscription model and its future success relies on building long-term relationships with its customers, its reliance on a

complex technical infrastructure which is subject to risk of failure, change and development, failure of key suppliers, the Group’s exposure to financial market risks, the

fact that the Group must protect its customer and corporate data and prevent breaches of security, risks inherent in the implementation of large-scale capital

expenditure projects, the fact that the Group relies on intellectual property and proprietary rights which may not be adequately protected under current laws or

which may be subject to unauthorised use and the fact that people at Sky are critical to the Group’s ability to meet the needs of its customers and achieve its goals

as a business.

Information on the significant risks and uncertainties is provided in the “Principal risks and uncertainties” section of Sky’s Annual Report for the full year ended 30

June 2016. Copies of the Annual Report are available from the Sky plc web page at www.sky.com/corporate and in hard copy from the Company Secretary, Sky plc,

Grant Way, Isleworth, Middlesex TW7 5QD. All forward looking statements in this document are based on information known to the Group on the date hereof. The

Group undertakes no obligation publicly to update or revise any forward looking statements, whether as a result of new information, future events or otherwise.

VERSION 2: 23 November 15:00

Fortitude

Series 2

Andrew GriffithGroup COO and CFO

5

Pay TV broadcaster

Entertainment for everyone

Broad range of packages

DTH, IPTV, OTT, Mobile

Every screen, everywhere

Triple play/quad play

Service to suit customers needs

Sports and movies centric

High reliance on big bundle

Exclusively DTH

Main TV in living room

Single play

Customer service on the phone

Broader, consumer-led business

6UK and Ireland revenue excluding Sky Bet

1 94233

380550

7761,008

1,249 1,4341,545

1,847

2,231

2,681

3,069

3,4653,810

4,111

4,504

4,908

5,2755,854

6,4966,627

7,018

7,3777,820

8,371

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

+£3.1bn

+£2.6bn

+£1.9bn

+£0.8bn

Organic revenue (£m)

7

Formula 1®

• Winning content portfolio

• Delivering direct to consumers at scale

• Clear brand leadership and happy customers

• Best in class sales capability

• Deep customer insights providing advantage

8

Advertising

Customers

Home communications

Transactional, Rent and Buy

Mobile

Efficiency

Programme sales

TV products

HD

TV

Channel sales

9

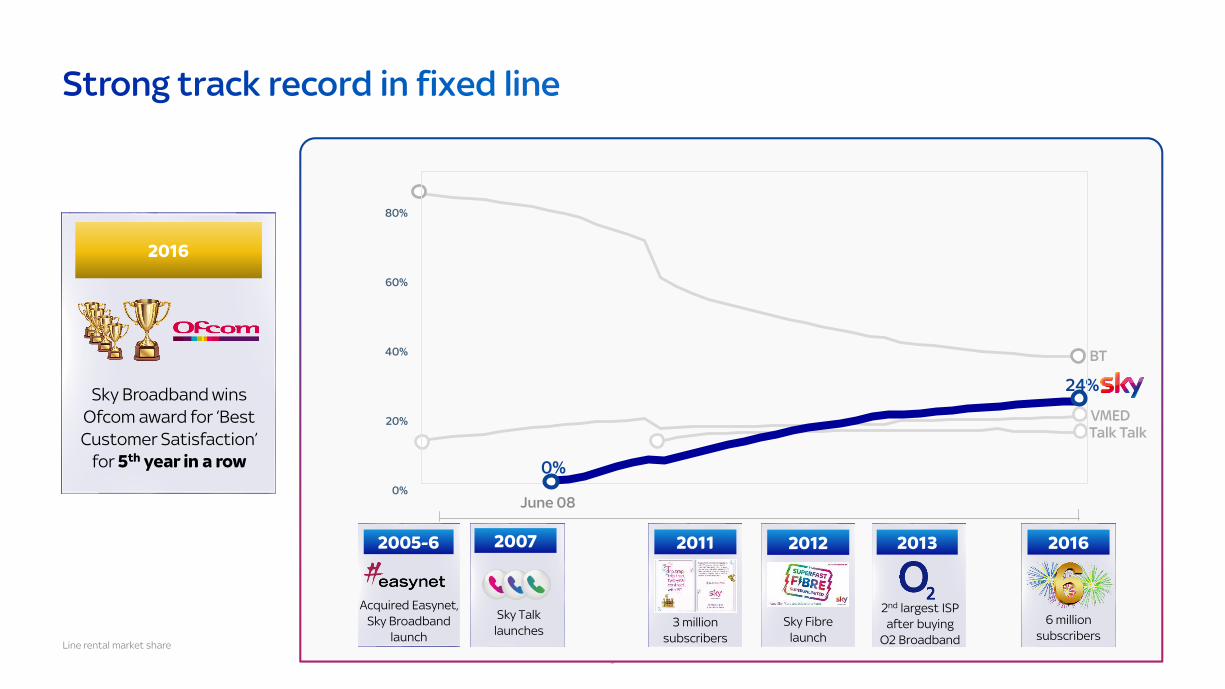

0%

20%

40%

60%

80%

June 08

VMED

BT

Talk Talk

24%Sky Broadband wins

Ofcom award for ‘Best

Customer Satisfaction’

for 5th year in a row

2016

2007

Sky Talk

launches6 million

subscribers3 million

subscribers

2011

Sky Fibre

launch

2012 20162013

2nd largest ISP

after buying

O2 Broadband

2005-6

Acquired Easynet,

Sky Broadband

launch

0%

Line rental market share

Stephen van RooyenCEO UK and Ireland

11

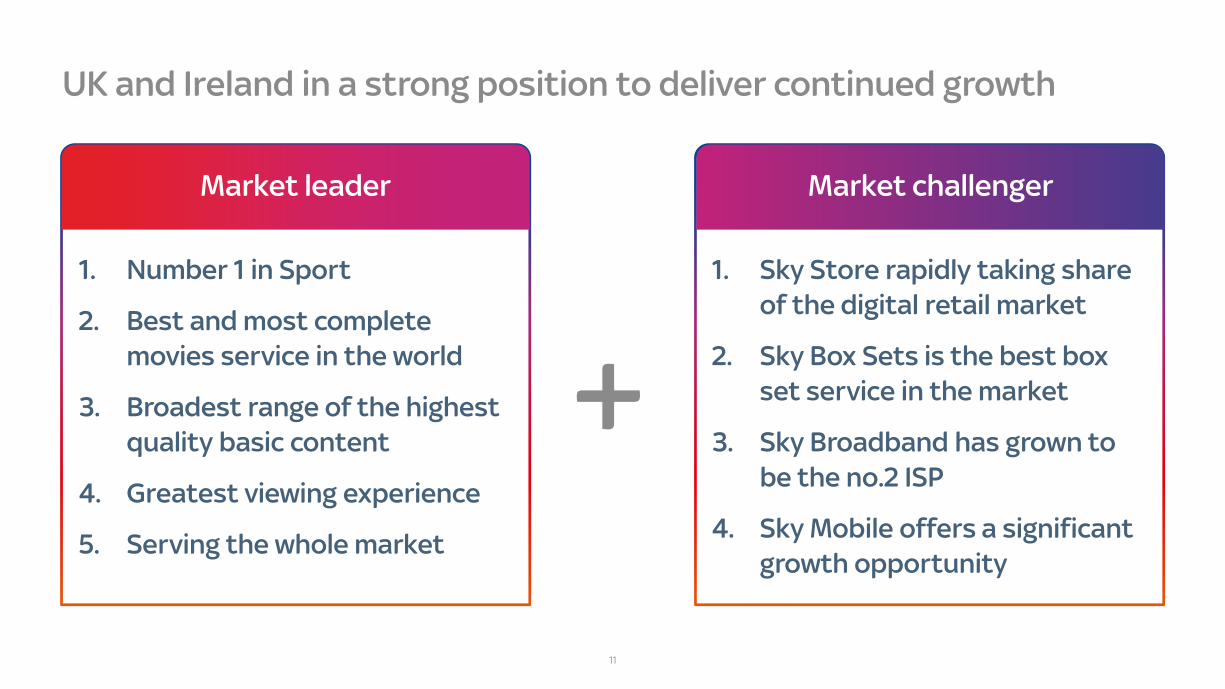

UK and Ireland in a strong position to deliver continued growth

Market leader

1. Sky Store rapidly taking share

of the digital retail market

2. Sky Box Sets is the best box

set service in the market

3. Sky Broadband has grown to

be the no.2 ISP

4. Sky Mobile offers a significant

growth opportunity

1. Number 1 in Sport

2. Best and most complete

movies service in the world

3. Broadest range of the highest

quality basic content

4. Greatest viewing experience

5. Serving the whole market

Market challenger

+

12

Sky Mobile is a significant growth opportunity

• The market is large and we have no legacy

• We have the customer appetite

• We have the brand

• We have the proposition – that’s fresh, unencumbered,

anchored in what our customers expect and love about Sky

• We have the right infrastructure in place

• We have the capabilities to succeed and

the experience to deliver

13

Our view of

the market,

our brand

and

customer

appetite

Our

proposition

Our go to

market

strategy

1. 2. 3.

Our pricing

4.

14

1. The market

Our brand

Customer appetite

15

1. Mobile is a significant growth opportunity for Sky

>2 per Sky HH

Cross-sell

52m PAYM

Customer GrowthRevenue Growth

£15bn

Source: OFCOM Communications Market Report 2016, Experian and internal data sources

16

1. Mobile is a significant growth opportunity for Sky

Active monthly mobile subscriptions

in Sky homes to target

50+23m

and growing

17

1. Market trends are making it even more attractive for us

Growth in

subscription

Growth in

SIM-Only

Growth in data

usage

Growth in online

purchasing

Aligns with Sky’s

subscription model

Easier to sell online

and to families

Aligns with Sky’s

leadership in content

Convergence around

key handset

manufacturers

Emerging “offload”

opportunity

Improved customer

experience & economics

through voice over WiFi

Consumer driven trends Technology trends

18

1. Our extensive customer research identified clear pain points

for customers

Source: Mobile Positioning Qual research Dec 2015

Opaque tariffing Expensive data Loyalty unrecognised

Inflexible contracts Unloved brands Poor service

19

Translating into very high ITP

1. Our research showed spontaneous credibility for Sky and

very high intention to purchase once brand revealed

Intent to Purchase in next 12 months

of ‘8-10’ in consumer research

(indexed to Sky Go)

Sky Mobile Sky BB Sky Go Sky Store

Sky spontaneously named across all three key

requirements for new mobile provider

20

2. Our Proposition

21

22

Sky Mobile based around five key pillars

All backed by Sky’s unrivalled Customer Service

23

23

Your data is yours to keep.

At the end of every month we’ll automatically

Roll over whatever’s left into your piggybank

for you to use whenever you like.

24

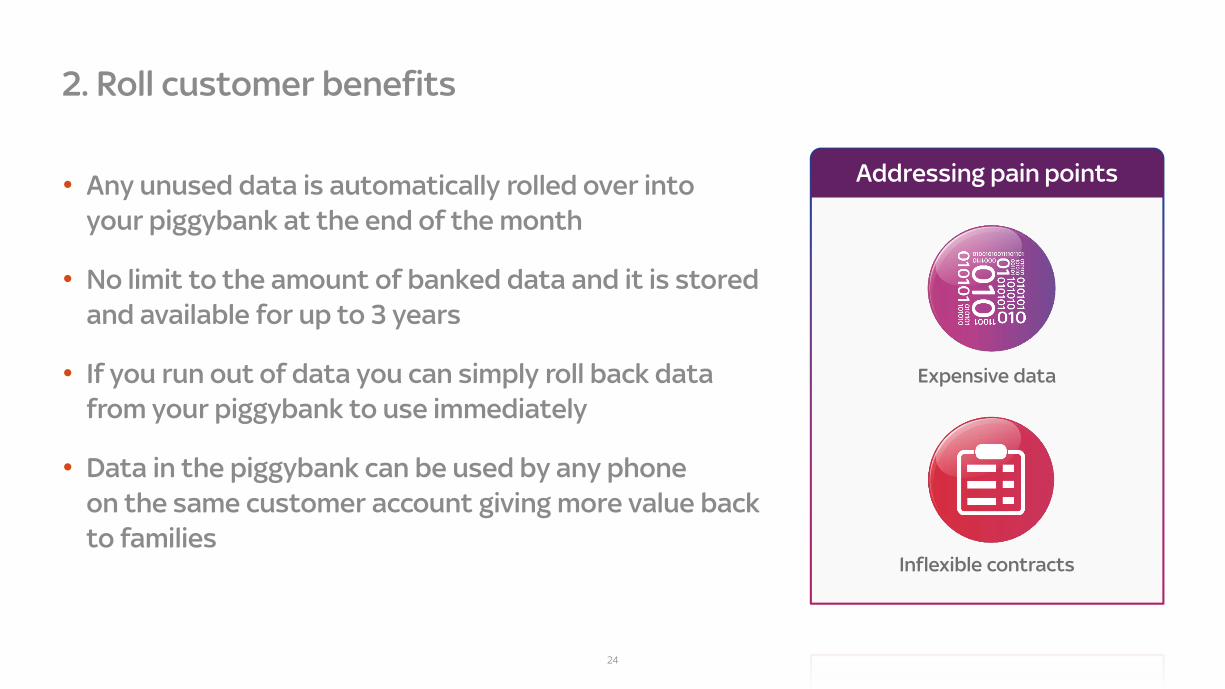

2. Roll customer benefits

• Any unused data is automatically rolled over into

your piggybank at the end of the month

• No limit to the amount of banked data and it is stored

and available for up to 3 years

• If you run out of data you can simply roll back data

from your piggybank to use immediately

• Data in the piggybank can be used by any phone

on the same customer account giving more value back

to families

Addressing pain points

Expensive data

Inflexible contracts

25

25

Create a plan that’s just right for you.

Pick your data, calls and texts. And no

matter what you decide you can choose

to change your Mix whenever you like.

26

2. Mix customer benefits

• Can change plan to meet your needs as many

times as you want during your contract

• Ability to instantly upgrade to larger data pack

mid month if needed

• Uniquely allows customers to buy data only plans

with PAYU Calls and Texts

• No expensive out of bundle charges for excess

data usage

Addressing pain points

Inflexible contracts

Opaque tariffing

27

Sky TV families don’t have to

pay for another call or text with

any Sky Mobile plan

28

2. More value for Sky TV customers

• Free Unlimited Call and Texts for all Sky TV customers

• Appeals universally to both high and low call users

• Switch and Save

– Families can save hundreds of pounds per year when

they switch to Sky Mobile

Addressing pain points

Loyalty unrecognised

Opaque tariffing

29

For the first time, Sync Sky+ recordings

with your phone to create your own

personal Sky playlist of shows you love

to watch wherever you are.

30

2. Sync customer benefits

• Create your own playlist by synching your Sky+

planner to view when you’re out and about

• Instantly find your favourite shows

• And download via WiFi allowing you to make the

most of your data allowance

• Or if you need to just click to stream instantly

over our 4G network

Addressing pain points

Unloved brands

Loyalty unrecognised

31

3. Our go to market approach

32

HIGH

3. Focused on needs of core segments that over-index in

Sky households

DA

TA

US

AG

E

LOW

CALLS & TEXTSLOW

Medium Data / Low Comms Users

12m

Low Data / Low

Comms Users

14m

Medium Data /

Comms Users

20m

unlimited everything

6mc40%

CAGR

Source: Internal segmentation

33

3. We have adopted a digital first approach to sales

• Efficient and low cost

route to market

• Buy online or via mobile

• Dynamic data driven sales

platform

34

3. And offer customers simple ways to manage their account online

000000150054520

07780 000 000

000000150054520

35

3. We have an unrivalled set of marketing capabilities

Europe’s only targeted

TV platform

Existing marketing assetsReach and frequency

OBTM

EmailSMS

Direct Mail

£400mMedia value

4½hrsDaily viewing

36

3. Leverage Sky’s capabilities to drive upsell and cross-sell at scale

Customer

interactions

Home visits Retail kiosk

footfallNet products

sold per annum

3m3m 55m 2.6240m

Deep customer

insight

petabytes of consumer data

37

4. Our pricing will be simple

and transparent

38

39

Free for Sky TV customers

40

Customer Illustration 1

Kathleen, 43

Single parent, 2 young children

Samsung Galaxy S5 o2,

1 GB/1000mins/UL texts

Sky Original

Tight household budget

50+£60Annual saving

• Gets full value from her data plan– Doesn’t lose unused data

• Doesn’t worry about calls– Free calls and texts

Sky Mobile

1 GB, free UL calls/texts

41

50+£288Annual savingThe Edwards family

• Gets the unlimited calls and texts

he and his wife need

– Free calls and texts

• No worries about kids running up

large out of bundle charges– Family share piggybank

2 adults, 3 children at secondary school

iPhone 6, Vodafone

2 x 5 GB/UL, 3 x 1 GB

/1000 mins/UL texts

Sky Sports, Sky Cinema, Family (inc box sets)

Comfortable but need to live to a budget

Customer Illustration 2

Sky Mobile

1 x 5GB , 1 x 3GB, 3 x 1GB

All free UL calls/texts

42

• No wasted spend on comms– Only pay for calls and texts used

• Gets full value from his data plan– Right sized data plan with comfort to Roll unused

50+£96Annual savingDuncan, 34

Single

iPhone 6, EE

4 GB, Unlimited

calls/texts

Freeview, Netflix

Enough to fund lifestyle, no savings

Customer Illustration 3

Sky Mobile

3GB PAYU calls/texts

43

4. Phased approach to sales ramp up

Now Mid December January 2017 Spring 2017

Sales to Staff Sales to pre registered customers

Sales to everyone Handset Sales

44

In conclusion

• The market is large and we have no legacy

• We have the customer appetite

• We have the brand

• We have the proposition - that's fresh, unencumbered,

anchored in what our customers expect and love about Sky

• We have the capabilities to succeed and

the experience to deliver

• We have the right infrastructure in place

Mohamed HammadyCTO UK and Ireland

46

Since our broadband launch 10 years ago we have built a

world class fixed telecoms network

• 7,250km of nationwide fibre optic network

• 64 points of presence (PoPs)

• Metro rings in London, Birmingham, Glasgow and Edinburgh

• IP based voice switching platform and scaled data core

delivering 6Tbps at peak

• Switching over 7 billion minutes of traffic a year

• Over 100m calls originated monthly on our network

• Over 4,000 circuits carry voice traffic in and out of our network

47

Reflected in customer growth and the quality of service delivered

Best quality service delivered for data and voice

Sky

BT

Virgin Media

Talk Talk

Source: Internal estimates based on company reports adjusted for M&A activity.

0708 0809 0910 1011 1112 1213 1314 1415

Cumulative organic net broadband adds

48

We have now extended that expertise into creating our own state

of the art mobile service as a ‘Deep’ MVNO

MNO

Traditional

Thick MVNO

Thin MVNO

Reseller

Degree of integration

Time to market

Upfront investment

LOW HIGH

Flexibility

/ Control

-

+

Sky Deep

MVNO

Brand, Pricing

& Customer

Management

SIM, SMS, MMS

and VoicemailMobile Core

Evolved IMS

architectureBearer Control

Towers and

Spectrum

49

Leveraging our existing fixed network capabilities to optimise cost

CDN optimisation

for video

Transit and switching

cost efficiencies

Voicemail

Use existing operations

and support

Billing Public WiFi

50

Full mobile core enables future innovation and flexibility

Session control Use WiFi or

own spectrum

Direct handset

relationships

Full IMS Core

Ability to switch

host MNOApplication

awareness

51

Online Charging System and billing integration gives full control of

plans and pricing

Real time fraud

and credit control

Visibility to avoid

bill shock

End to end

customer service

Change plans and

rates easily

Tariff innovation

52

Roaming coverage in over 190 destinations, prioritising bilateral

relationships with top 25 countries to improve economics

Targeting Bilateral

relationships

Roaming coverage

No roaming coverage

53

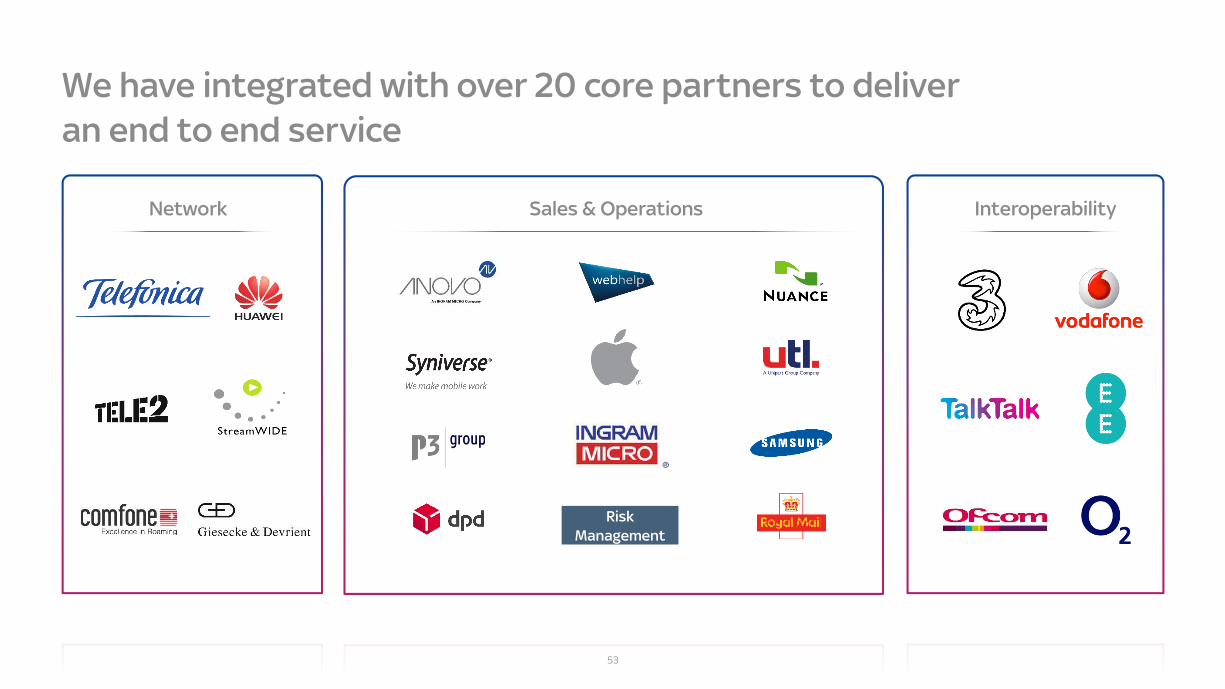

We have integrated with over 20 core partners to deliver

an end to end service

Network Sales & Operations Interoperability

Risk

Management

54

Deep MVNO architecture gives full control with limited up

front investment

• Own the SIM with full control over setting tariffs, bundles and services independently

• Full end to end operational control including sales, provisioning, billing and customer service

• Leverage existing core competences in data and voice and extend to our own international

roaming services

• State of the art core mobile platform enables Sky to manage and implement adoption of new

mobile technologies

• Ability to switch rapidly to alternate network provider with minimal impact on customers

• Deliver attractive margins with limited investment and no need to build capital intensive

national macro radio network

Andrew GriffithGroup COO and CFO

56

Significant opportunity

For customers For shareholders

• Opportunity for incremental

revenues, profits and

cash flows

• Excellent ROCE

• Profitable standalone business

• Great value

• Quality service from a

trusted brand

• Flexibility

57

Underpinned by four key components of our plan

Flexible MVNO agreement

Low cost customer acquisition model

Attractive customer economics

Loyalty benefit

58

Flexible MVNO agreement

• Modern ‘data first’ agreement

• 99% data coverage1 of UK from day one

• Launch with 4G as standard

• Full equivalence of service quality and future functionality

• Built in protections against declining retail pricing and

escalating usage

• Long term contract with Telefonica

1. Refers to in-door, coverage

59

• Proposition targeted at existing

Sky TV customers

• Acquisition model will leverage

– Online only

– No retail shops

– AdSmart

– Existing Sky channels

Existing TV

customer

Non-TV

customer

SAC range £1 to £70 £1 to £120

Average c.£33 c.£99

Acquisition mix 80%-90% 10%-20%

Low cost customer acquisition model

Illustrative only

SAC includes cost of SIM, number porting, call centre costs and direct marketing

60

Attractive customer economics

Illustrative only. Monthly revenue includes data, calls, texts, roaming, international and premium charges and termination revenue.

Direct costs include network operator costs (Telefonica) and termination costs.

Gross margin excludes any allocation of Sky fixed costs (e.g. customer service, ATL marketing, bad debt, billing).

Kathleen Edwards Family Duncan

Sky TV customer Sky TV customer Non-Sky TV customer

Monthly ARPU (excl VAT) £15 £80 £24

Direct Costs £(10) £(65) £(11)

Gross Margin £5 £16 £13

Gross Margin percentage 32% 20% 55%

Gross margin payback 7 months 2 months 8 months

61

Summary of key assumptions

Modest

fixed costs

• Limited dedicated ATL marketing and brand spend

(between £20-£25m p.a.)

•Dedicated customer service to manage mobile customers

• Sky Mobile core network operating costs

• Even ‘fixed costs’ are scalable with success

Limited

capex

• Estimated £20-£30m per annum capex going forward

• Total investment of £80m by end of 30 June 2017

(including £35m this year, £45m in prior years)

• Average UEL of c5 years – expect depreciation of £15-£20 million p.a.

62

Summary of key assumptions

Clear

guidance on

handsets

• SIM only launch – handsets to follow in 2017

• No handset subsidy - c10% handset margin

•Handsets fully unbundled from airtime tariff

• Two easy options for customers:

– Buy handset outright upfront, or

– Spread payments via a Consumer Credit Agreement

• Working capital impact limited to three months only

• Use of third party financing for handset receivable

63

Bringing it all together

• Standalone profitable with

3 million customers

• Excludes loyalty benefit to Sky

• 1% point reduction in TV churn

worth c.£50m EBIT

Illustrative economics@ 3 million

customers

@ 5 million

customers

Airtime Revenue 550 970

Direct costs (370) (620)

Net handset margin 100 160

Gross Profit 280 510

Variable marketing – i.e. SAC (50) (50)

Fixed costs – inc ATL marketing,

overheads, technology, depreciation and

customer service

(200) (300)

EBIT 30 160

EBIT margin %

(before loyalty benefit)3% 8%

Illustrative only

64

Attractive financial returns

1Calculated using the methodology of Barclays 15 June 2015 – European Telecom Services report

• Low risk, high return investment

• Standalone profitable in FY20 (third full year)

• ROCE of >20% by year five1, growing thereafter

• Accretive to earnings every year in FY20 and onwards

• All excluding value of loyalty benefits

Autumn internationals

65

Summary

• The market is large and we have no legacy

• We have the customer appetite and the brand

• Deep MVNO delivers attractive margins with limited

capital investment

• Sky Mobile will benefit broader business

– Provide great value to customers

– Improve loyalty

• Profitable business, excellent returns

66

Q&A