SIP report

106

SUMMER INTERNSHIP PROJECT REPORT AT THE NEW INDIA ASSURANCE COMPANY LIMITED A Project Report Submitted In Partial Fulfillment of the Requirements For The Award of the Degree of POST GRADUATE DIPLOMA IN MANAGEMENT TO M.S.RAMAIAH INSTITUTE OF MANAGEMENT BY ANAND VINODKUMAR (101203) PGDM(AUTONOMOUS) 2010-12 Under the guidance of 1

-

Upload

anand-kumar -

Category

Business

-

view

1.299 -

download

6

Transcript of SIP report

SUMMER INTERNSHIP PROJECT REPORT

AT

THE NEW INDIA ASSURANCE COMPANY LIMITED

A Project Report Submitted In Partial Fulfillment of the RequirementsFor The Award of the Degree of

POST GRADUATE DIPLOMA IN MANAGEMENT

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENTBY

ANAND VINODKUMAR (101203)

PGDM(AUTONOMOUS) 2010-12

Under the guidance of

Dr. G.P.SUDHAKAR

M.S.RAMAIAH INSTITUTE MANAGEMENTNEW BEL ROAD, BANGALORE-560054

1

STUDENT’S DECLARATION

I hereby declare that the Project Report conducted at The New India Assurance Company Limited

Under the guidance of Dr. G. P. Sudhakar

Submitted in Partial fulfillment of the requirements for the Degree of

POST GRADUATE DIPLOMA IN MANAGEMENT (AUTONOMOUS)

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

is my original work and the same has not been submitted for the award of any other Degree/Diploma/Fellowship or other similar titles or prizes

Place: Bangalore ANAND VINODKUMAR

Date: 11-08-2011 Reg. No 101203

2

3

CERTIFICATE

This is to certify that the Project Report at The New India Assurance submitted in partial fulfillment of the requirements for the award of the

degree of

POST GRADUATE DIPLOMA IN MANAGEMENT (AUTONOMOUS)

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

Is a record of bonafide training carried out under my supervision and guidance and that no part of this report has been submitted for the award of

any other degree/diploma/fellowship or similar titles or prizes.

FACULTY GUIDESignature:

Name: Dr.G.P.Sudhakar

Qualifications: Seal of learning centre

4

ACKNOWLEDGEMENT

I extend my special gratitude to our beloved Dean Dr.M.Chandrashekar & Academic Head Shri.V.Narayanan & Programme Head Mrs.Jayashree Kowtal for inspiring me to take up this project.

I wish to acknowledge my sincere gratitude and indebtedness to my project guide Dr.G. P. Sudhakar of M.S. RAMAIAH INSTITUTE OF MANAGEMENT Bangalore for his valuable guidance and constructive suggestions in the preparation of project report.

ANAND VINODKUMAR

5

Table of Contents

EXECUTIVE SUMMARY

CHAPTER I - INDUSTRY ANALYSIS

Introduction to Insurance…………………………………………………………………...1

Evolution of General Insurance Industry in India………………………………………….1

Competition in the Industry……………………………………………………………..….2

The Potential of New Entrants in the Industry……………………………………………..3

The Power of Suppliers…….……………………………………………………………...4

The Power of Customers…………………………………………………………………...4

The Availability of Substitutes…………………………………………………………….5

CHAPTER II - COMPANY ANALYSIS

The New India Assurance Co. Ltd………………………………………………………...6

Marketing……………………………………………………………………………….….8

Customers………………………………………………………………………………...16

Competitor………………………………………………………………………………..18

Human Resources…………………………………………………………………………22

Operations…………………………………………………………………………………27

Finance……………………………………………………………………………………30

Organizational Hierarchy…………………………………………………………………31

Environment……………………………..………………………………………………..33

SWOT Analysis…………………………………….…………………………………….35

CHAPTER III – DISCUSSION ON TRAINING

Roles and Responsibilities………………………………………………………………38

Description of tasks handled…………………………………………………………….38

Contribution to the organization………………………………………………………...39

CHAPTER IV – ANALYSIS OF RESEARCH

Introduction…………………………………………………………………………….42

Research Design……………………………………………………………………..…42

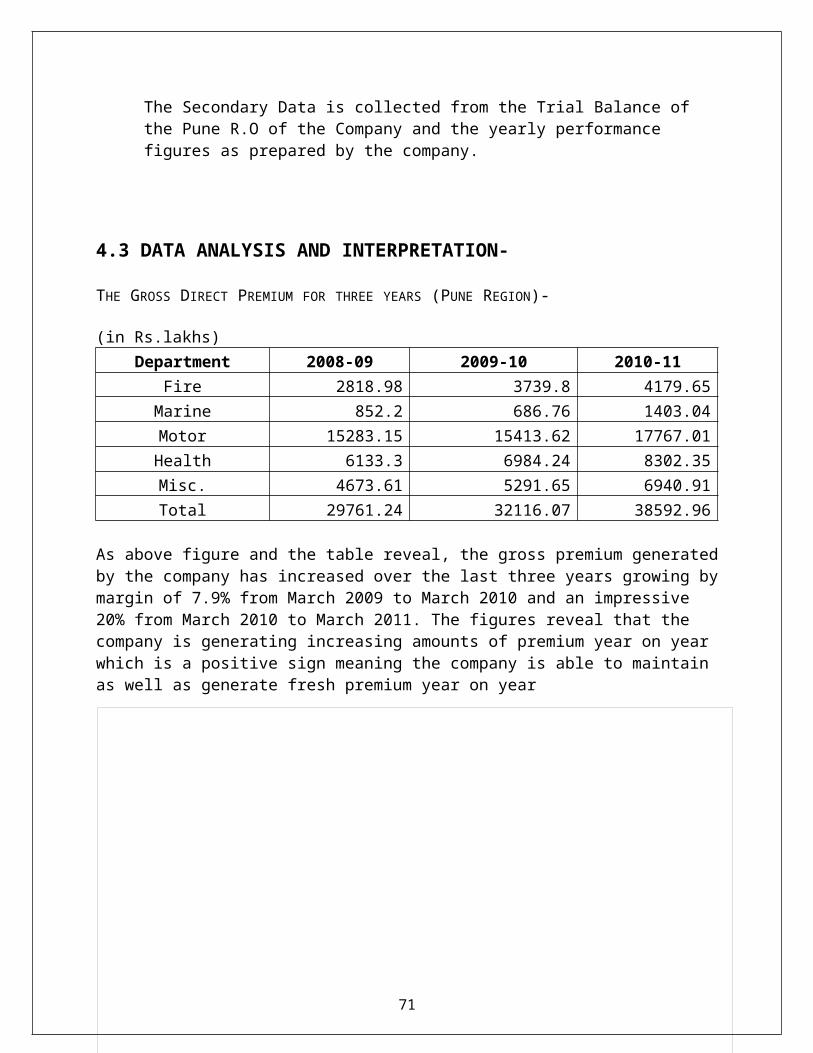

Data Analysis and Interpretations………………………………………………………44

Findings…………………………………………………………………………………64

Recommendations………………………………………………………………………65

Conclusion………………………………………………………………………………67

BIBLIOGRAPHY

6

ANNEXURE

EXECUTIVE SUMMARY

The rapid growth of the Indian middle class strata in terms of both size and wealth has resulted in the tremendous growth of the Indian Insurance Industry over the past decade. They are now playing an increasingly important role in the financial services industry. India's general insurance industry has witnessed a growth of 22% in premium income for the fiscal year ended on March 2011. The industry has collected a total of Rs 425.66 billion from premiums in the last fiscal. According to an industry study conducted by the Federation of Indian Chambers of Commerce and Industry (FICCI) and the US-based Boston Consulting Group, India will be among the top 15 non-life insurance markets by 2020. Indian health insurance represents one the fastest growing and second largest non-life insurance segments in the country. As per estimates, health insurance gross premium is expected to grow at a CAGR of around 26% during 2010-11 – 2013-14. This increasing market is creating considerable competition among Indian insurance companies in an industry that 20 years ago was relatively small. There are twenty four companies vying for market share at present. While the industry has come a long way over the past decade, the big challenge is profitability. The non-life insurance industry has cumulative underwriting losses of nearly Rs.30,000 crore.In such a scenario, it is essential to maintain the market share as well as ensure sustainable growth. Over the past few years companies have run at losses with a view of gaining a foothold in the industry. However, this practice cannot go on for long. Underwriting profitability has emerged as a buzzword. It is of paramount importance that companies focus on prudent underwriting to ensure sustainability.The report is a compilation of all activities and observations carried out during the course of an 8 week internship at The New India Assurance Co. Ltd.Chapter One focuses on the General Insurance Industry in India tracing its evolution and Porter’s Five Force Analysis of the Indian General Insurance Industry.Chapter Two is a study of the New India Assurance Company with emphasis on their Products, Marketing activities, Customers, Finance, HR, Operations. It includes a SWOT analysis of the company.Chapter Three is a discussion on the training undergone and the tasks handled during the course of the internship. It includes a survey to determine the awareness and needs of prospective customers with regard to Health InsuranceChapter Four is a detailed study on the “Profitability Analysis of various lines of business for the past three years”. The study of material facts is followed by observations and suggestions to improve the profitability of the Company.

7

CHAPTER I - INDUSTRY ANALYSIS

1.1 INTRODUCTION TO INSURANCE –

Insurance may be defined as a contract between the insurer and insured under which insurer indemnifies the loss of the insured against the identified perils for which mutually agreed upon premium has been paid by the insured. The contract lays down the time framework within which the losses will be met by the insurer.

Insurance in its present form in India is there for almost a century. People know life insurance more than non life insurance. General Insurance is more known by its motor insurance because third party motor insurance is compulsory. Life insurance is a tax saving, life and accidental insurance and investment. However, general insurance is purely insurance. This has been one of the major reasons for the relative unpopularity of General Insurance in India. However, the entry of new players, the consequent expansion of offices, new channels of distribution, increase in number of tied agents along with increasing awareness and acceptance of insurance have all contributed to the massive expansion of the insurance sector in the last few years.

1.2 EVOLUTION OF GENERAL INSURANCE INDUSTRY IN INDIA –

The history of general insurance dates back to the Industrial Revolution in the west and the consequent growth of sea-faring trade and commerce in the 17th century. It came to India as a legacy of British occupation. General Insurance in India has its roots in the establishment of Triton Insurance Company Ltd., in the year 1850 in Calcutta by the British. In 1907, the Indian Mercantile Insurance Ltd, was set up. This was the first company to transact all classes of general insurance business.

1957 saw the formation of the General Insurance Council, a wing of the Insurance Association of India. The General Insurance Council framed a code of conduct for ensuring fair conduct and sound business practices.

In 1968, the Insurance Act was amended to regulate investments and set minimum solvency margins. The Tariff Advisory Committee was also set up then.

However, insurance for mainly restricted to big business houses and the upper strata of society. With a view of spreading insurance to all sections of the society, the process of nationalization of insurance companies was undertaken.

In 1972 with the passing of the General Insurance Business (Nationalization) Act, general insurance business was nationalized with effect from 1st January, 1973. 107 insurers were amalgamated and grouped into four companies, namely National Insurance Company Ltd., the New India Assurance Company Ltd., the Oriental Insurance Company Ltd and the United India Insurance Company Ltd. The General Insurance Corporation of India was incorporated as a company in 1971 and it commence business on January 1st 1973.

Nationalization led to the rapid spread of offices across the country as well as development of new products such as Cattle Insurance, agriculture Pump Set Insurance etc aimed at the rural sector.

8

This period also saw the hiring of many professionals such as veterinary doctors, legal experts, chartered accountants and H.R professionals as specialists.

Thus, nationalization led to more awareness and penetration of insurance to the semi-urban and rural areas.

This millennium has seen insurance come a full circle in a journey extending to nearly 200 years. The process of opening up of the sector had begun in the early 1990s and the last decade or so has seen it being implemented in a substantial manner. In 1993, the Government set up a committee under the chairmanship of RN Malhotra, former Governor of RBI, to propose recommendations for reforms in the insurance sector. The objective was to complement the reforms initiated in the financial sector. The committee submitted its report in 1994 wherein, among other things, it recommended that the private sector be permitted to enter the insurance industry. They stated that foreign companies be allowed to enter by floating Indian companies, preferably as a joint venture with Indian partners.

Following the recommendations of the Malhotra Committee report, the Insurance Regulatory and Development Authority (IRDA) was constituted as an autonomous body to regulate and develop the insurance industry in 1999. The IRDA was incorporated as a statutory body in April, 2000. The key objectives of the IRDA include promotion of competition so as to enhance customer satisfaction through increased consumer choice and lower premiums, while ensuring the financial security of the insurance market.

The IRDA opened up the market in August 2000 with the invitation for application for registrations. Foreign companies were allowed ownership of upto 26%. The Authority has the power to frame regulations under Section 114A of the Insurance Act, 1938 and has from 2000 onwards framed various regulations ranging from registration of companies for carrying on insurance business to protection of policyholders’ interests.

In December, 2000, the subsidiaries of the General Insurance Corporation of India were restructured as independent board run companies and at the same time GIC was converted into a national re-insurer. Parliament passed a bill de-linking the four subsidiaries from GIC in July, 2002.

1.3 COMPETITION IN THE INDUSTRY-

India with about 200 million middle class household shows a huge untapped potential for players in the insurance industry. Saturation of markets in many developed economies has made the Indian market even more attractive for global insurance majors. The insurance sector in India has come to a position of very high potential and competitiveness in the market.

Today there are 24 general insurance companies including the ECGC and Agriculture Insurance Corporation of India.

In a de-tariffed environment, competition will manifest itself in prices, products, underwriting criteria, innovative sales methods and creditworthiness. Insurance companies will vie with each other to capture market share through better pricing and client segmentation.

9

The General Insurance Industry is an ultra competitive one. Since the products offered by each of the competitors is more or less the same, the companies are focusing more on customer service in order to gain a competitive advantage. The figures show that the four public sector companies together account for 59.14%. The biggest private player in the General Insurance Sector is ICICI Lombard having a share of almost 9.5% followed by Bajaj Allianz which accounts for around 7.2%. The share of the public sector was 58.84% for the financial year 2008-2009. Thus, it has been more or less the same. However, with the increase in the disposable income of the public and the increased awareness, the growth of the private sector in the coming years is inevitable especially specialized institutions viz. Star Health and Allied Insurance, Apollo Munich and Max BUPA which cater solely to the health sector.

There may be room for many more players in a large underinsured market like India with a population of over one billion. But the reality is that the intense competition in the last five years and the impact of the wider network of the public sector companies has made it difficult for new entrants to keep pace with the leaders and thereby struggling to make any impact in the market so far.

The battle has so far been fought in the big urban cities, but in the next few years, increased competition will drive insurers to rural and semi-urban markets.

The private companies showed a growth of 22.49% over the past year while the public companies grew by 21.12%. The industry as a whole grew by 21.68%.

When there are more competing insurance providers in the insurance industry the overall premium rates drop due to market compulsions.

When premium rates drop significantly, the word spreads. Public demand for insurance increases with high correlation in regards to how affordable it is. When premium rates are very low people, who never would have otherwise, purchase insurance policies.

1.4 THE POTENTIAL OF NEW ENTRANTS INTO THE INDUSTRY-

The General Insurance has seen an annual growth of about 15% over the last 10 years and the industry is today at an inflection point and is poised to grow at a much faster pace due to the rapidly growing middle class/high income segment, robust demand for motor cars and two wheelers, huge potential in the health sector and the untapped segments such as personal lines of insurance market and liability insurance.

In recent times, we have seen the advent of many new Insurance companies targeting this lucrative Indian market.

The opening up of insurance sector has seen many overseas brands making a foray into the country’s market mainly due to the lowered entry barriers.

Many famous Indian business houses like Tata, Bharati, Bajaj have also entered into this somewhat virgin market along with their fancied foreign partners viz AIG, AXA and Allianz respectively.

The new entrants are making huge investment in the market since there is potential for long term growth, market share and ultimately profit.

Another threat for many insurance companies is financial services companies like Banks and NBFCs entering the market. For eg- SBI General Insurance.

10

These entities use their existing customer base to market their products and gain a foothold into the insurance sector.

With the ongoing efforts to get the rural India financially included, there is a large opportunity to tap the semi-urban and rural markets which would be open for general insurance.

However, the intense capital requirements and stringent norms are a potential stumbling block for new entrants.

1.5 THE POWER OF SUPPLIERS-

If an insurer were to renege on the written promise it has made, for any reason, then the claim of an insured can only be re-established in a court of law, based on full disclosure of facts and other evidences; and ofcourse, at considerable initial legal expense and delay to the insured.

The delicate power balance that exists in a transaction to dictate performance compliance shifts in favour of an insurer, once the deal is struck between the insurer and the insured.

A certain helplessness is felt by an insured to ensure an insurer’s performance compliance.

The main strength of suppliers lies in the fact that insurance products can be bundled on the spot for sale. There is no need for a manufacturing process or facility.

There is nothing extra needed in designing a cover, by which an insurer can distinguish himself except for his financial strength and service reputation or capability to act smart and fast.

With products being more or less the same in insurance market, customers will gravitate towards subjective criteria in purchasing the insurance cover. Studies show that in 9 out of 10 cases when choosing products that are similar in quality and price, customers will go for a company that has a better image in his mind.

Thus, the image of a company plays a major role in generating business for the company. Its reputation is a valuable asset which is given as much attention as that given to products and services.

This is where the PSUs score over the newly incorporated general insurance companies and why they continue to enjoy a majority of the market share.

Also, unlike the normal market model, it is the not the customers but the suppliers who determine the price of the product.

1.6 THE POWER OF CUSTOMERS –

Insurance as they say is sold not bought. Hence, Consumers remain the most important centre of the insurance sector.

The Customer profile has changed drastically in the last few years. The steady economic growth has ensured augmented banking and insurance services.

The industry now deals with customers who have better buying power, know what they want and when, and are more demanding in terms of better service and speedier responses.

People today don’t want to accept the current value propositions, they want personalized interactions and they look for more and more features and add ons and better service.

11

The insurance companies today must meet the need of the hour for more and more personalized approach for handling the customer. Today managing the customer intelligently is very critical for the insurer especially in the very competitive environment. Companies need to apply different set of rules and treatment strategies to different customer segments. However, to personalize interactions, insurers are required to capture customer information in an integrated system.

With the explosion of Website and greater access to direct product or policy information, there is a need to developing better techniques to give customers a truly personalized experience. Personalization helps organizations to reach their customers with more impact and to generate new revenue through cross selling and up selling activities. To ensure that the customers are receiving personalized information, many organizations are incorporating knowledge database-repositories of content that typically include a search engine and lets the customers locate the all document and information related to their queries of request for services. Customers can hereby use the knowledge database to manage their products or the company information, claim records, and history of the service inquiry.

After the entry of the foreign players the industry is seeing a lot of competition and thus improvement of the customer service in the industry. Computerization of operations and updating of technology has become imperative in the current scenario. Foreign players are bringing in international best practices in service through use of latest technologies.

Customers are offered unbundled products with a variety of benefits as riders from which they can choose. More customers are buying products and services based on their true needs.

Large corporate clients like airlines and pharmaceutical companies etc have a lot more bargaining power with insurance companies since they pay millions of rupees a year in premiums. Insurance companies try extremely hard to get high-margin corporate clients.

1.7 THE AVAILABILITY OF SUBSTITUTES-

There are plenty of substitutes in the insurance industry. Most large insurance companies offer similar suites of services. Whether it is motor, personal line, commercial, health or fire insurance, chances are that there are competitors who can offer similar services.

In some areas of insurance, however, the availability of substitutes is few and far between. For eg- Micro Insurance and Rural Insurance.

Companies focusing on niche areas usually have a competitive advantage, but this advantage depends entirely on the size of the niche and on whether there are any barriers preventing other firms from entering.

The new companies have also introduced many new products hitherto unknown to the Indian Insurance populace. New products and new companies have only expanded the choice of Indian consumers.

12

CHAPTER II - COMPANY ANALYSIS

2.1 THE NEW INDIA ASSURANCE CO. LTD. –

The New India Assurance Co. Ltd was incorporated on July 23rd, 1919. It was founded by Sir Dorab Tata. New India is the first fully Indian owned insurance company in India. Earlier it was a subsidiary of the General Insurance Corporation of India (GIC). But as GIC became a reinsurance company as according to IRDA Act 1999, all of its four primary insurance subsidiaries (New India Assurance, United India Insurance, Oriental Insurance and National Insurance) got sovereignty.The New India Assurance Co. Ltd. is a leading global insurance group, with offices and branches throughout India and various countries abroad. It is the only Indian company which has successfully managed to develop considerable International operations and an extensive record for successfully trading outside India. The company has its presence felt in nearly 27 countries and accounts for more than 80% of the total overseas premium in India. The New India employs approximately 21000 employees, specialists and technically qualified personnel at all levels of management who are empowered to underwrite and settle claims of high magnitude. Government of India is the principal shareholder of the company.With a wide range of policies New India has become one of the largest non-life insurance companies, not only in India, but also in the Afro-Asian region.The company aims to develop insurance business in the best interest of the society by providing

13

financial security to individuals, trade, commerce and other segments of the society with high quality services at an affordable cost. New India is a pioneer among the Indian Companies on various fronts, right from insuring the first domestic airlines to satellite insurance. Lately The New India Assurance Co. Ltd. has insured the INSAT-2E.New India Assurance was the first group to meet with the needs of the Indian Shipping Fleet, and the initiators of engineering insurance and satellite insurances as well. The company was the first to build an Aviation Insurance Department, way back in 1946, to handle the requirements related to insurance of the Indian Shipping Fleet, to establish its own Training School, to introduce the concept of 'Model Office Training', and to create a department in Engineering insurance. It was also the first Indian non-life company to cross Rupees 5000 Crores Gross Premium. In order to maintain being the first always the company aims at continuing the procedure of providing optimized services for individuals and organizations.New India has been rated "A-" (Excellent) by A.M.Best Co., making it the only Indian insurance company to have been rated by an international rating agency.The company is headed by Mr. M. Ramadoss, Chairman and Managing Director of the company. In the recent years it has succeeded in forging tie-ups with some of the leading public sector banks in India like State Bank of India (SBI), Central Bank of India, Corporation Bank and United Western Bank to increase its distribution network.

Mission-

To develop general insurance business in the best interest of the community. To provide financial security to individuals, trade, commerce and all other segments of

the society by offering insurance products and services of high quality at affordable cost.

Values -

Highest priority to customer needs High Standards of Public Conduct Transparency in operations.

14

2.2 MARKETING-

Products-

The company offers a wide portfolio of products which cater to a wide segment of people.They can be classified as follows-Personal-

Pravasi Bhartiya Bima Yojana Policy Mediclaim Policy Family Floater Mediclaim Policy Janata Mediclaim Policy Senior Citizen Mediclaim Policy Personal Accident Policy Overseas Mediclaim Policy Householders Policy Motor Policy Money Insurance Rasta Apatti Kavach (Road Safety Insurance) Suhana Safar Policy TV/VCR/VCP Insurance Mobile/Cellular Phone Insurance Other Personal Insurance Group Mediclaim Policy

Commercial- Jewellers Block Policy Bankers Indemnity Policy Shopkeepers Policy Marine Cargo Policy Plate Glass Insurance Special Contingency Policy Neon Sign Insurance Multi Peril Policy for L.P.G. Dealers Fidelity Guarantee Insurance Policy Marine Hull Policy Aviation Insurance

Liability- Public Liability Policy Products Liability Policy Professional Indemnity Policy Directors and Officers Liability Policy Lift (Third Party) Insurance Employers' Liability Policy Carrier's Liability Insurance Liability Insurance Act Policy Golfers Indemnity Insurance

15

Industrial- Fire Policy Burglary Policy Machinery Breakdown Policy Electronics Equipment Policy Consequential Loss Policy Contractors All Risk Policy Marine cum Erection / Storage cum Erection Policy Advanced Loss of Profit / Delay in Startup Policy Contractor Plant and Machinery Policy Mega Package Policies

Social- Universal Health Insurance Scheme for BPL families Universal Health Insurance Scheme for APL families Jan Arogya Bima Policy Raj Rajeshwari Mahila Kalyan Yojana Bhagyashree Child Welfare Policy Janata Personal Accident Insurance Student Safety Insurance Ashrya Bima Yojana Rural Insurance

Distribution Network-

Marketing is a predominant activity in the general insurance industry. The Insurance product is intangible and requires a considerable amount of explanation of the intricacies of various products. This has necessitated the need for competent, motivated and professional marketing and distribution channels, in addition to direct selling, to communicate with a great number of insured and uninsured customers, with their marketing messages and to expand their current markets in terms of number of customers and premium volumes across the expanse of a vast country like ours. As the customer segment consist of various heterogeneous individuals, corporate insured and other groups, with their own highly individualized insurance needs, the most effective way to reach them has proved to be a big challenge to the insurers.The distribution channel acts as the intermediary and as a personal go-between. It plays a crucial role to build bridges of better understanding between the insurer and the insured.In order to spread the awareness of insurance and increase coverage to the far corners of the country, the opening up of the insurance sector has enlarged distribution from the earlier single channel system of tied agencies to a multiple channel setup comprising Corporate Agents including Bancassurance, Brokers and referrals/introducers and Agents etc. In one sense, the independent surveyors community too is a distribution channel legally recognized under the Insurance Act for claims’ services of assessment and determining the policy liability.Corporate Agents is a concept introduced with a view of taking advantage of the presence of a large number of entities with a sizeable client base, contacts and goodwill already operating in the market with other activities

16

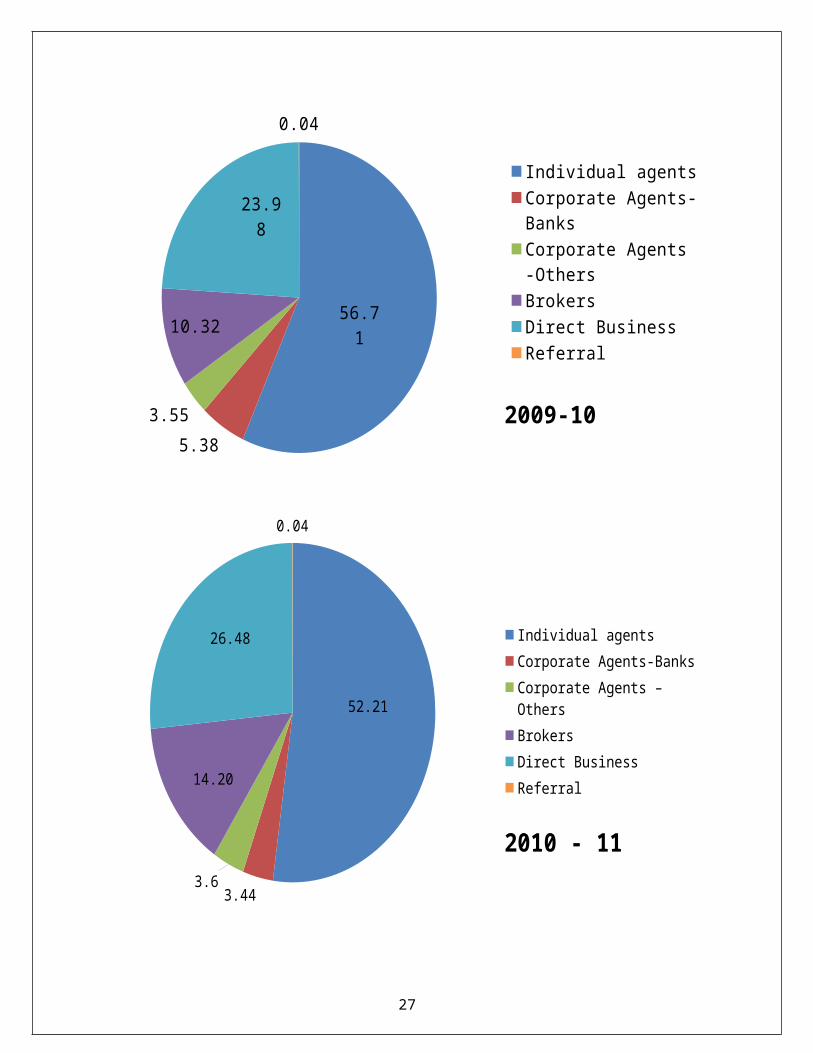

While corporate insured do get attention from direct selling staff of an insurer, the individual insured, whose numbers are larger but the premiums are relatively lower require other secondary distribution channels. Despite, the emergence of new channels of distribution, agency channel remains the mainstay of the sector, still contributing a lion’s share of the business being generated by the insurers. During the year 2010-11, in terms of premium generated, more than 80% of the business is coming from the agency channel, around 3.8 % through brokers, around 0.54 % through corporate agents, around 3.3% through bancassurance in the Pune Region.

Intermediaries

AgentsThe agency system is pre-dominant as historically face to face contact was considered essential in selling an Insurance product. Insurance agents are involved in the selling of one or more lines of insurance policies and products. An agent is required to undergo Practical training of 100 hours and pass in an examination with 50% marks to be conducted by Insurance Institute of India, Mumbai. New India has its own IRDA approved training centers to develop dedicated agents.

BrokersAs per notification dated 16th Oct 2002 and INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY (INSURANCE BROKERS) REGULATIONS, 2002, IRDA has allowed brokers to act as an intermediary to sell insurance policies in India. Though it was introduced only in 203, it has made inroads into the world of corporate insurance. Brokers are gaining ascendancy as professionals, as more and more corporate insured are changing over to them. Brokers traditionally weaken the bargaining powers of insurers because of equality in professional expertise between them and the premium clout of several customers backing their punch. However, with commercial interests guiding everyone involved, all negotiating battles are fought on the price front; and not on improving risk management practices of customers. Professionalism at the level of all selling efforts is lacking. The New India Assurance Company Ltd. has enlisted more than 280 brokers. Some of the brokers operating in Pune are FIRST POLICY Insurance Advisors Pvt. Ltd, Chawla & Associates Insurance Services Pvt. Ltd, Life & General Associates Pvt. Ltd., Nipun Ins. Brokers Pvt. Ltd., Surekh Ins. Services Pvt. Ltd., United Risk Ins. Broking Co. Pvt. Ltd., Vantage Ins. Services Pvt. Ltd.

BancassuranceBancassurance means the sale of insurance products through a bank’s distribution channels. This model offers a seamless service of banking, life and non-life products. Bancassurance in India is developing as an important channel for distribution to a growing class of customers. This is a very customer friendly channel. As per the current regulations, banks can either opt to become a corporate agent or a referral provider to an insurance company. The company has bancassurance tie ups with the following banks-State Bank of India, Central Bank of India, Corporation Bank and United Western Bank to increase its distribution network.

Third Party Administrators (TPA) The job of a TPA is to maintain databases of policy holders and issue them identity cards with unique identification numbers and handle all the post policy issues including claim settlements.

17

In case of a claim, policy holder has to inform TPA. On informing the TPA, policy holder will be directed to a hospital where the TPA has a tied up arrangement. However, policy holder will have the option to join any other hospital of his choice, but in such case payment shall be on reimbursement basis. TPA issues an authorization letter to the hospital, for the treatment wherein the TPA will pay for the treatment. TPA will be tracking the case of the insured at the hospital and at the point of discharge; all the bills will be sent to TPA. TPA makes the payment to the hospital. TPA then sends all the documents necessary for consideration of claims, along with bills to the insurer and Insurer reimburses the TPA. New India has tied up with 18 TPAs viz Mediassist India Pvt.Ltd., M D India Healthcare Services ( P ) Ltd., E Meditek Solutions Ltd., Heritage Health Service Pvt. Ltd., Universal Medi-Aid Services Ltd., Focus Healthcare Medicare TPA Services ( I ) Pvt.Ltd., Raksha TPA Pvt. Ltd., TTK Healthcare Services Pvt.Ltd., East West Assist Pvt. Ltd., Alankit Health Care Limited, Health India, Good Health Plan Ltd., Vipul Med Corp TPA Pvt. Ltd., Safeway Mediclaim Services Pvt. Ltd., Anmol Medicare Ltd., Dedicated Healthcare Services (India)Ltd., Genins India Ltd.

SurveyorsSurveyors play a crucial role between the Policy Holder (Insured) and the Policy issuer or Underwriter or Insurer (Insurance Companies). Surveyor gives their expert report without any prejudice to the Insurer (Insurance Company) with a recommendation specifying whether indemnify or repudiate the claim lodged by the Insured.

Following shows the channel wise distribution of premium over the past two years for the company – (Rs.in lakhs)

Channel 2009-10 2010-11

Individual agents 342689 475259.46

Corporate Agents-Banks 32535 31333.68

Corporate Agents –Others 21467 32757.58

Brokers 62360 129323.4

Direct Business 144931 241063.74

Referral 268.61 436.22

Grand Total 604251 910174.08

18

56.71

5.383.55

10.32

23.98

0.04

Individual agents

Corporate Agents-Banks

Corporate Agents -Others

Brokers

Direct Business

Referral

2009-10

52.21

3.44

3.6

14.20

26.48

0.04

Individual agentsCorporate Agents-BanksCorporate Agents –OthersBrokersDirect BusinessReferral

2010 - 11

19

Pricing-

A fundamental principle of insurance pricing is that if insurers are to sell coverage willingly, they must receive premiums that( 1) are sufficient to fund their expected claim costs and administrative costs and(2) provide an expected profit to compensate for the cost of obtaining the capital necessary to support the sale of coverage."[Harrington 1999]The pricing of insurance products starts from the pure premium calculation of the actuaries. It includes the amount needed to cover expected losses and loss adjustment expenses. It is then loaded for operating expenses including sales commission and other marketing costs, taxes and the cost of handling claims. This component varies from one line of business to another. The law of large numbers principle works while pricing a product i.e determining the premium. The premium is based on rates. There are basically three recognized rating methods.Judgment rating is used when the risk proposed to be bought is so unusual that little or no statistical information about similar risk is available. Each exposure is individually evaluated, and the rate is determined largely by the underwriter's judgment. When the judgment rating is used, each premium is unique and is based on the opinion of the person making it.Class rates are the most common rate in insurance business. Insured risks are classified on the basis of one or several important features and all that belong to the same class are subject to the same rate per unit of exposure. The rate charged reflects the claims experience for the class as a whole. It is based on the assumption that future losses to insured will be determined largely by the same set of factors. Merit rating is a modification of the class rating. It modifies the class rate of a particular class insured based on individual loss experience.

Promotion Strategy-

The aim of the company is to design the products from customer feedback to suit their specific needs. The company focuses on delivering outcome rather than merely products. The company is ramping up its knowledge database and is focusing on the customer base with a view to building long term relationships. The role of field personnel is imperative for the promotion of the various insurance covers and it is their responsibility to scout for these covers. Electronic media, outdoor media and print media were utilized for publicity purpose. Hoardings and glow signs were placed at many major road junctions, highways, railway stations and airports. Advertisements were also displayed on transit media like buses, trains, baggage trolleys and barricades.Banner display at local events helped the company in brand building in rural areas.The company participates in fairs, exhibitions and road shows and also sponsors various social gatherings, sports and cultural events.The company recently forayed into television and radio activities. The company also sponsored the Mumbai Indians IPL T-20 team which has given tremendous visibility to the customers of all ages and various groups not only nationwide but also global-wise.The internet affords widespread access to a pool of new customers. Beyond the traditional means of radio, print and television ads, the internet opens up the audience that insurers might reach. This dimension has to do with delivering a marketing message to more customers than before. Also the internet is an advertising vehicle. A website offers the insurer an opportunity to shape

20

and tailor its particular message to personal computer owners. The website newindia.co.in displays financial ratings and statements, shows press releases and lists a range of product and service offerings. It also showcases the newly developed products of the company. The cost of advertising on the internet on a per reader basis is much lower than television, radio and print advertising. The website also provides toll free numbers of the customer care and details of nearby offices and claims hubs etc.

21

Customer Service-

The company believes in the following dictum-“The customer is the most important visitor on our premises. He is not dependant on us. We are dependent on him. He is not an interruption in our work. He is the purpose of it. He is not an outsider in our business. He is a part of it. We are not doing him a favour by serving. He is doing us a favour by giving us an opportunity to do so.”

Thus, it is evident that the company lays utmost importance to customer service. Customer services and grievance cells are well established at company’s corporate offices and all Regional Offices. “May I Help You?” counters have been provided in all Regional Offices, Divisional Offices and Branch Offices for customer service.In order to ensure better and efficient customer service, the company has decided to launch a toll free number on an All India basis, catering to the needs of the existing as well as prospective clients.

Current Market Structure-

General Insurance Industry was under the complete control of the four Government Companies for nearly three decades. After much deliberation, the market was opened for competition from December 2000. The government delinked the four public sector companies from holding company GIC to operate as independent companies. The IRDA has issued licenses to a number of private General Insurance Companies.List of General Insurance Companies operating in the market as on date –

S.No Name of the Company Headquarters

1.Bajaj Allianz General Insurance Co. Ltd.

Pune

2. ICICI Lombard General Insurance Co. Ltd.

Mumbai

3. IFFCO Tokio General Insurance Co. Ltd.

Gurgaon

4. National Insurance Co.Ltd. Kolkata5. The New India Assurance Co.

Ltd. Mumbai

6. The Oriental Insurance Co. Ltd. New Delhi7. Reliance General Insurance Co.

Ltd.Mumbai

8. Royal Sundaram Alliance Insurance Co. Ltd

Chennai

9. Tata AIG General Insurance Co. Ltd.

Mumbai

10. United India Insurance Co. Ltd. Chennai

11. Cholamandalam MS General Insurance Co. Ltd.

Chennai

22

12. HDFC ERGO General Insurance Co. Ltd.

Mumbai

13. Export Credit Guarantee Corporation of India Ltd.

Mumbai

14. Agriculture Insurance Co. of India Ltd.

New Delhi

15. Star Health and Allied Insurance Company Limited Chennai

16. Apollo Munich Health Insurance Company Limited

Gurgaon

17. Future Generali India Insurance Company Limited

Mumbai

18. Universal Sompo General Insurance Co. Ltd.

Mumbai

19 Shriram General Insurance Company Limited

Jaipur

20 Bharti AXA General Insurance Company Limited

Bangalore

21 Raheja QBE General Insurance Company Limited

Mumbai

22 SBI General Insurance Company Limited

Mumbai

23 Max Bupa Health Insurance Company Ltd.

New Delhi

24 L&T General Insurance Company Limited

Mumbai

2.3 CUSTOMERS-

Globalisation is helping to create wealth for more people around the world. This has spurred the demand for financial products. Newly prosperous people are seeking ways in investments and see their assets grow, as well as to protect those assets and ensure financial security for their families.

The customer profile can be defined as follows- Knowledgeable Increasingly aware of the global scenario Demanding Expect value for money Aware of their rights Expect widest cover at lowest cost Demand promptness be it in policy documents, claims or any other

service. Expect quality service.

23

Since, very individual is susceptible to risk; everyone is a customer or a potential customer for the insurance industry.

In selling an insurance cover, each individual customer is unique both in his specific insurance needs and in his buying preferences.

This uniqueness of each insured customer has put an enormous pressure on an insurer, in terms of demonstrating its individualized insurance expertise of the marketing staff, the time spent accessing and engaging its customers and the relative costs of doing them all to get the business.

Marketing strategies will have specific focus based on the segment to which they are catering to.

The company caters to a large cross section of lower, middle and upper sections of society.

The customers are segmented along the following lines-CorporateSmall IndustriesNew VenturesCooperativesIndividual EntrepreneursRural UnitsPersonal Insurance Lines

Extensive market survey is carried out to determine the needs of the people and specific policies are designed keeping in mind the needs of customers.

The company offers various generic policies which cater to a large number of people such as, motor and basic fire policy.

The company also offers policies for individuals belonging to specific professions. For eg- Doctor’s Protection Shield has been designed keeping in mind the various hazards doctors are exposed to.

The Office Protection Shield (General) offers protection to various items generally found in the offices. However, there are specific Office Protection Shield policies for professionals that provide professional indemnity for loss on material damage to property and/or death or bodily injury to third party whilst rendering professional services.

Also, various tailor made policies are provided for organizations to cover their employees. For eg- Group Mediclaim policy offers cover to a minimum of 100 employees subject to a minimum sum insured of Rs.1 lakh each. The premium in such cases is determined by a number of factors pertaining to that organization alone such as age of the employees, the risk that they are subject to, the claims ratio over the previous years etc.

The rural consumer is now exhibiting an increasing propensity for insurance products. A research conducted exhibited that the rural consumers are willing to dole out anything between Rs 2,900 and Rs 3,500 as premium each year.

2.4 COMPETITORS-

24

Figure below shows the segment wise premium of the 21 General Insurance Companies as on March 2010. (All figures in Rs.crore). The New India Assurance Co. Ltd is the largest non-life insurer in India in terms of premium, having a market share of 17.27% with the gross premium underwritten being 6013.44 crores as on 30th March 2010. The top four spots are occupied by the public sector companies with United India Insurance being second (15.04%) followed by Oriental Insurance (13.55%) and National Insurance (13.27%). The biggest private player continues to be ICICI Lombard with a market share of almost 9.5% followed by Bajaj Allianz with 7.23%. The biggest gainers in the last year were Bharti AXA followed by Universal Sompo which grew by a whopping 797% and 454% respectively. However, their market share continues to be less than 1%. The share of the PSUs was more or less the same over the previous year. The market share New India Assurance Co. Ltd. has increased to.17.62% and gross premium underwritten is 7070.22 crores as per the unaudited and provisional figures available as on 30th March 2011. The specialized institutions managed to make a significant dent in the health sector with Star Health & Allied Insurance showing a growth of 92% and Apollo Munich showing a growth of 134%.

Sl No.

Insurer Fire Marine Motor Health OthersGrand Total

Market Share(%)

1Royal Sundaram

42.49 23.02 617.19 116.11 108.27 907.08 2.61

2 TATA-AIG156.75 113.84 236.36 83.39 301.51 891.84 2.56

3 Reliance129.78 44.42 1,318.71 238.75 248.00 1,979.65 5.69

4 IFFCO Tokio202.38 135.12 849.01 164.22 288.83 1,639.56 4.71

5 ICICI Lombard270.06 146.57 1,379.16 911.81 587.47 3,295.06 9.46

6 Bajaj Allianz261.40 74.76 1,445.77 295.39 438.37 2,515.70 7.23

7 HDFC ERGO142.78 25.01 289.92 268.74 201.96 928.42 2.67

8Cholamandalam

47.77 42.39 450.10 149.51 95.08 784.85 2.25

9 Future Generali 42.38 15.50 210.40 69.32 49.11 386.72 1.11

10Universal Sompo

42.15 3.84 79.10 17.40 46.86 189.36 0.54

11 Shriram1.74 0.01 410.51 0.00 3.65 415.91 1.19

12 Bharti Axa27.29 5.44 179.97 35.20 42.75 290.65 0.83

13 Raheja QBE0.16 0.02 0.17 0.00 1.60 1.94 0.01

14 New India 914.80 477.79 2,067.42

1,541.90

1,011.53 6,013.44 17.27

15 National429.16 239.91 2,168.76

1,021.71 761.37 4,620.92 13.27

25

16 United India 647.93 451.97 1,817.13

1,256.14

1,064.15 5,237.32 15.04

17 Oriental575.03 390.45 1,610.19

1,063.51

1,079.57 4,718.75 13.55

Grand Total

3,934.07

2,190.06

15,129.88

7,233.10

6,330.06

34,817.17 100.00

18 ECGC 813.71 813.71

19

Star Health & Allied Insurance

965.53 14.51 980.04

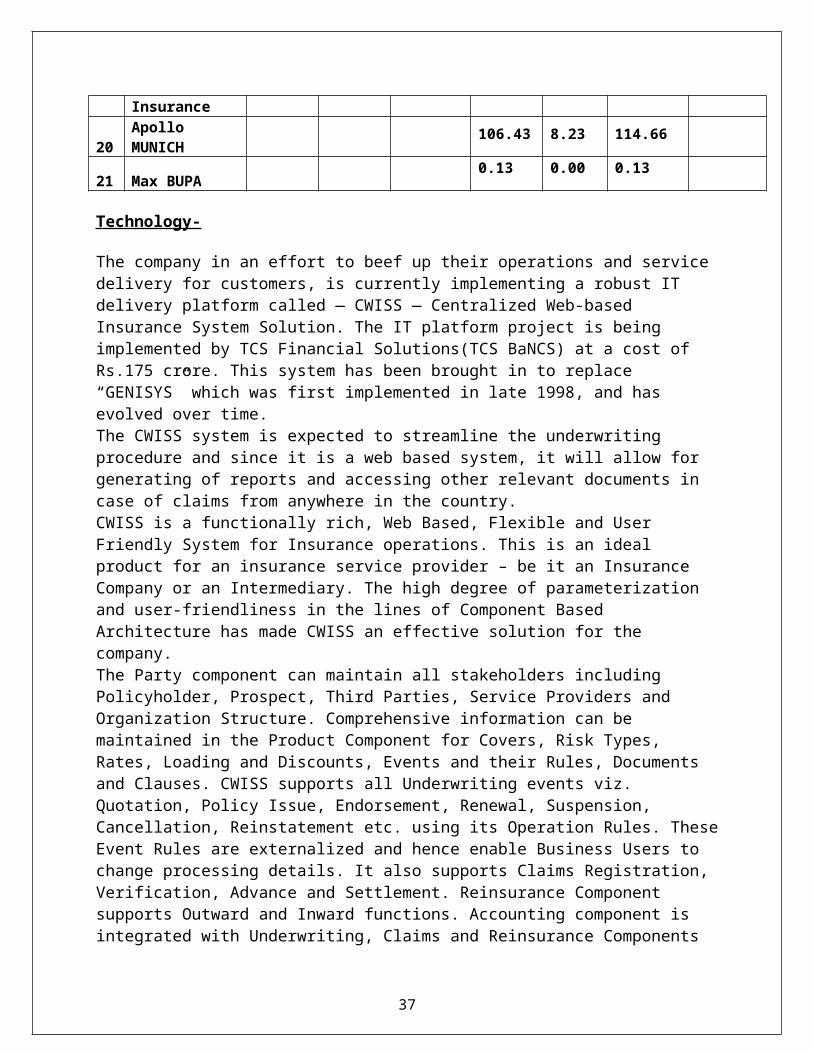

20 Apollo MUNICH 106.43 8.23 114.66

21 Max BUPA 0.13 0.00 0.13

Technology-

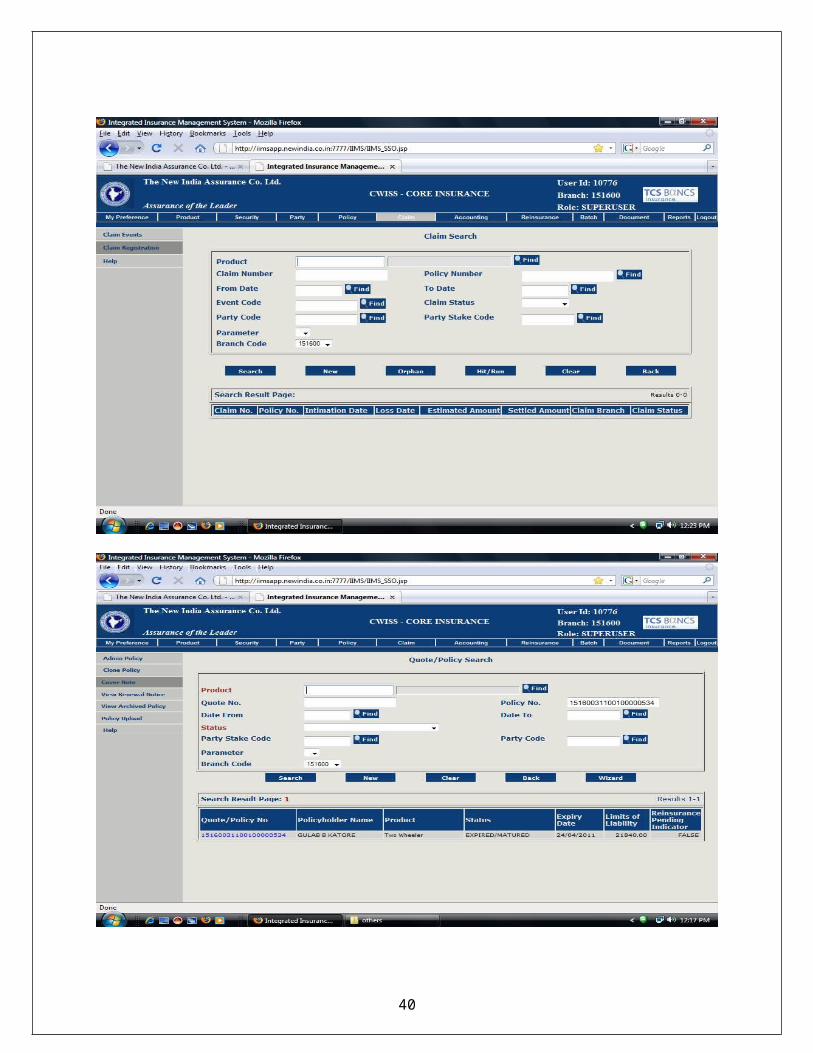

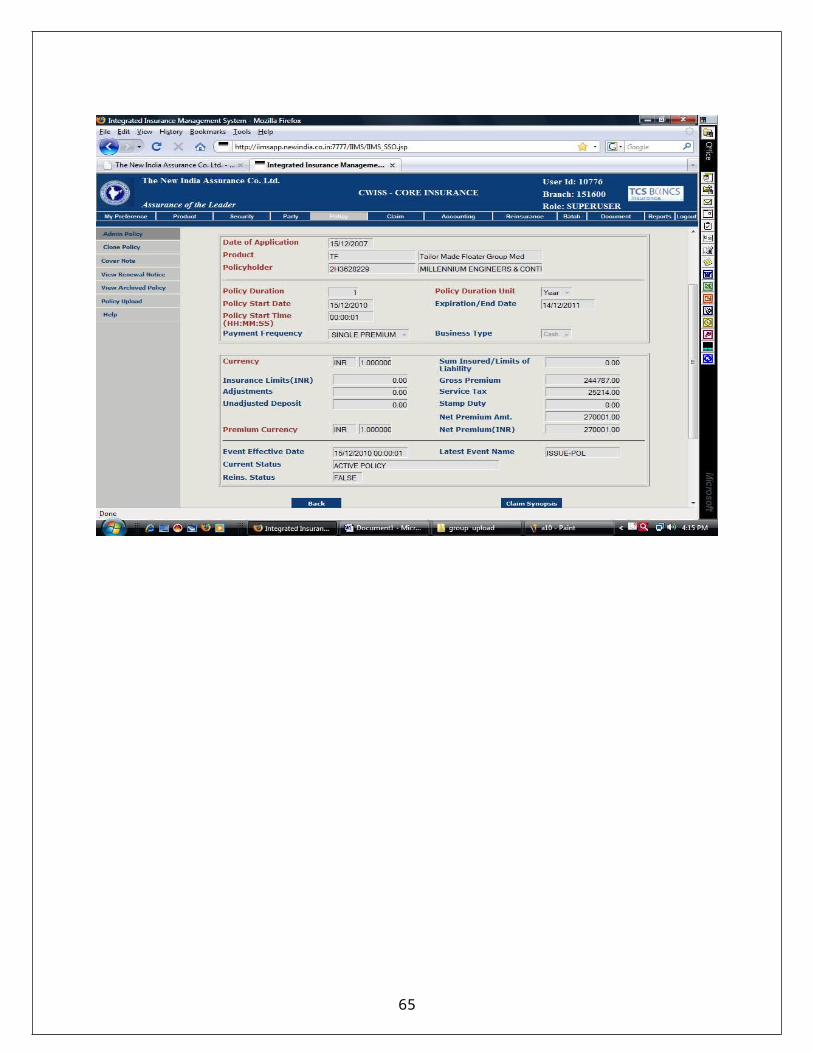

The company in an effort to beef up their operations and service delivery for customers, is currently implementing a robust IT delivery platform called — CWISS — Centralized Web-based Insurance System Solution. The IT platform project is being implemented by TCS Financial Solutions(TCS BaNCS) at a cost of Rs.175 crore. This system has been brought in to replace “GENISYS” which was first implemented in late 1998, and has evolved over time.The CWISS system is expected to streamline the underwriting procedure and since it is a web based system, it will allow for generating of reports and accessing other relevant documents in case of claims from anywhere in the country.CWISS is a functionally rich, Web Based, Flexible and User Friendly System for Insurance operations. This is an ideal product for an insurance service provider – be it an Insurance Company or an Intermediary. The high degree of parameterization and user-friendliness in the lines of Component Based Architecture has made CWISS an effective solution for the company.The Party component can maintain all stakeholders including Policyholder, Prospect, Third Parties, Service Providers and Organization Structure. Comprehensive information can be maintained in the Product Component for Covers, Risk Types, Rates, Loading and Discounts, Events and their Rules, Documents and Clauses. CWISS supports all Underwriting events viz. Quotation, Policy Issue, Endorsement, Renewal, Suspension, Cancellation, Reinstatement etc. using its Operation Rules. These Event Rules are externalized and hence enable Business Users to change processing details. It also supports Claims Registration, Verification, Advance and Settlement. Reinsurance Component supports Outward and Inward functions. Accounting component is integrated with Underwriting, Claims and Reinsurance Components in a seamless fashion. Document Management, Diaries and an access & limit based Application Security are infrastructure features that are available. Historical Data and comprehensive Audit Trail are available for all transactions.CWISS includes rolling out the core insurance applications for the various lines of business and Oracle Financials for the complete accounting and financial package and also encompasses the peripheral applications including CRM with a Grievance Module and Call Centre, Customer’s portal, Dealer’s portal, Broker’ and Agent’s portal, Employee’s portal, Business Intelligence

26

portal, Document Management Systems and various modules of an Integrated HRMS package with People Soft Payroll etc. CWISS has been linked to the main server at Thane in Maharashtra.

The value proposition of CWISS over GENISYS are- Ease of maintaining products Integration of Reinsurance and Accounting with other components which reduces

inefficiency due to separate systems. The workflow in Underwriting and Claims components being configurable, it is easy to

make necessary changes. Facilities of new properties on request in Underwriting and Claims ease the problems to

adopt regulatory changes. Flexible, externalized Rating and Event Rules maintainable by Users reduce IT

involvement in Business Rule Change. Flexibility is the key in all components of this solution.

Role based Security, Authorization and Audit features ensure high level of Transaction and Data Security.

Availability of Document Manager features let the User come up with new Document Templates within Short Time. It also allows the User to maintain all communications (received and sent) inside the system – this enhances the traceability. The following are a few screenshots of the CWISS system.

27

28

29

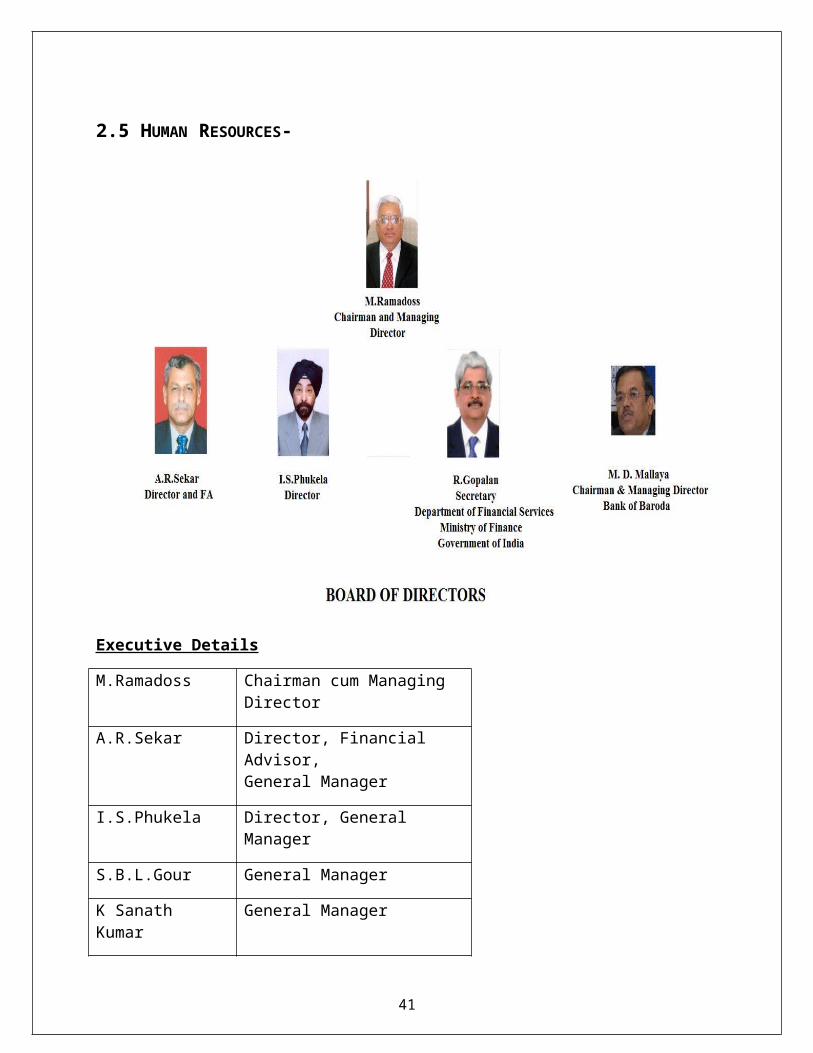

2.5 HUMAN RESOURCES-

Executive Details

M.Ramadoss Chairman cum Managing Director

A.R.Sekar Director, Financial Advisor, General Manager

I.S.Phukela Director, General Manager

S.B.L.Gour General Manager

K Sanath Kumar General Manager

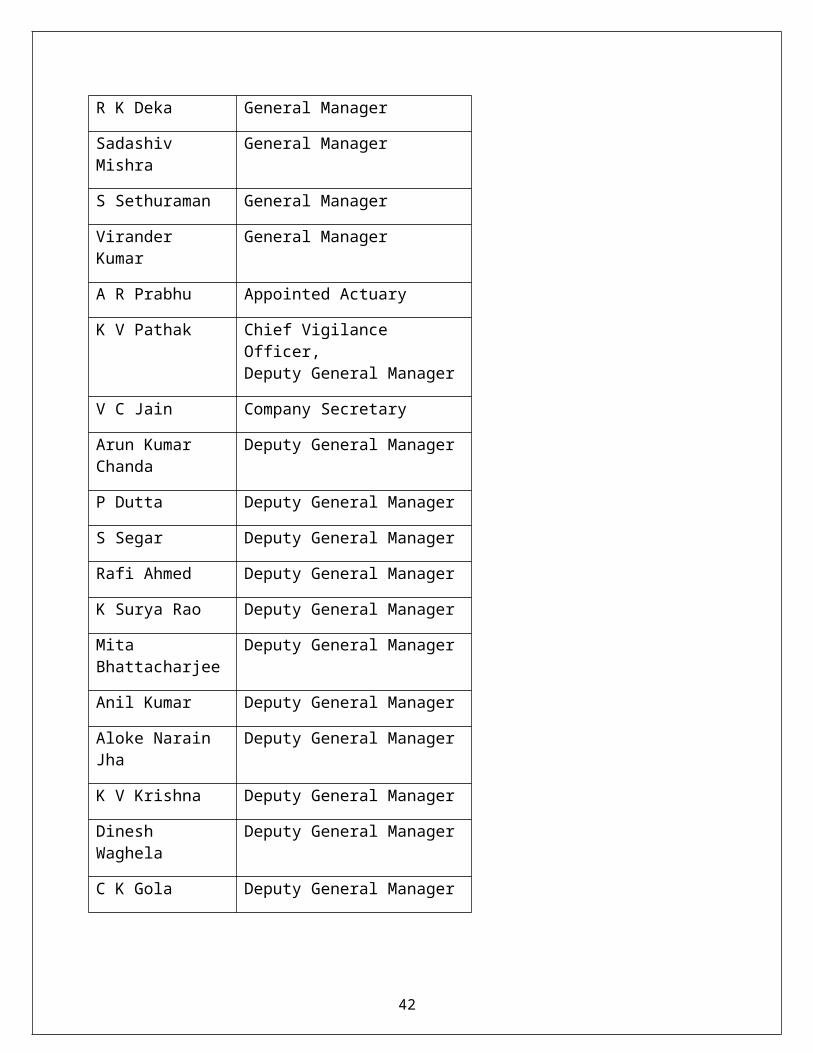

R K Deka General Manager

Sadashiv Mishra General Manager

S Sethuraman General Manager

Virander Kumar General Manager

30

A R Prabhu Appointed Actuary

K V Pathak Chief Vigilance Officer, Deputy General Manager

V C Jain Company Secretary

Arun Kumar Chanda

Deputy General Manager

P Dutta Deputy General Manager

S Segar Deputy General Manager

Rafi Ahmed Deputy General Manager

K Surya Rao Deputy General Manager

Mita Bhattacharjee Deputy General Manager

Anil Kumar Deputy General Manager

Aloke Narain Jha Deputy General Manager

K V Krishna Deputy General Manager

Dinesh Waghela Deputy General Manager

C K Gola Deputy General Manager

Departments-

Sl.No Departments

1 Agency Perfomance Enhancement Programme

2 Agency, Class II Cell, IBD (Admn), Publicity, Marketing

3 Auto Tie-up

4 Aviation

5 Business Process Redesigning, R & D

6 Brokers, Bancassurance, Corp Agency

7 Central Accounts

8 Chief Liaison Officer, I.D.D.

9 Corporate HRM- Class I, III & IV & Training

31

10 Corporate Training College

11 Credit Insurance Risk Office

12 Estate and Establishment

13 EWS, Legal, Library, MBS

14 Fire

15 Foreign Business

16 Grievance Cell, Customer Service, R.I.D.

17 Health

18 Information Technology

19 Investment

20 Investment, Board Secretariat

21 Legal O.D

22 Legal TP

23 Legal, CPI cell

24 Marine Cargo

25 Marine Hull

26 Miscellaneous Accident Technical

27 Motor Technical

28 Performance Management System, De-tariffing Business

29 Property Cell

30 Reinsurance

31 Reinsurance (Accounts)

32 RID, Health Insurance

33 Techno Marketing

34 Vigilance

32

Employee Strength-

Category Total number of Employees Function

Class I 5941 SupervisoryClass II 2547 Development ForceClass III 9032 Clerical/SecretarialClass IV 2049 Sub staff/DriversP. T. S. 389

Total 19558

Staff Position at Pune R.O-

Officers(DGM+CRM+MGR+Dy.MGR+A.M+A.O

)

Development Officers

Class III Employee

s

Class IV Employee

s

PTS

Total

307 171 668 114 17 1277

Training-

For Agents:In addition to their Corporate Training College (CTC), Mumbai, Zonal Training Centres (ZTC) at Kolkata and Chennai and 19 Regional Training centres (RTC) at Regional offices; the company have received accreditation for 23 other Agencies training centres in interior parts of the country. The training is for pre-licencing exam preparation and subsequent trainings for skill developments.

For Staff:RTC and ZTC caters training to the employees under the zone/ regions, from time to time. ZTCs generally conduct trainings on special topics for which faculties are rare.College of Insurance (Under GIC ,Mumbai) also imparts training programmes for staff from Mumbai and Pune Regions only.On Management topics and specialized topics , there are external agency's training centers at various places throughout India.

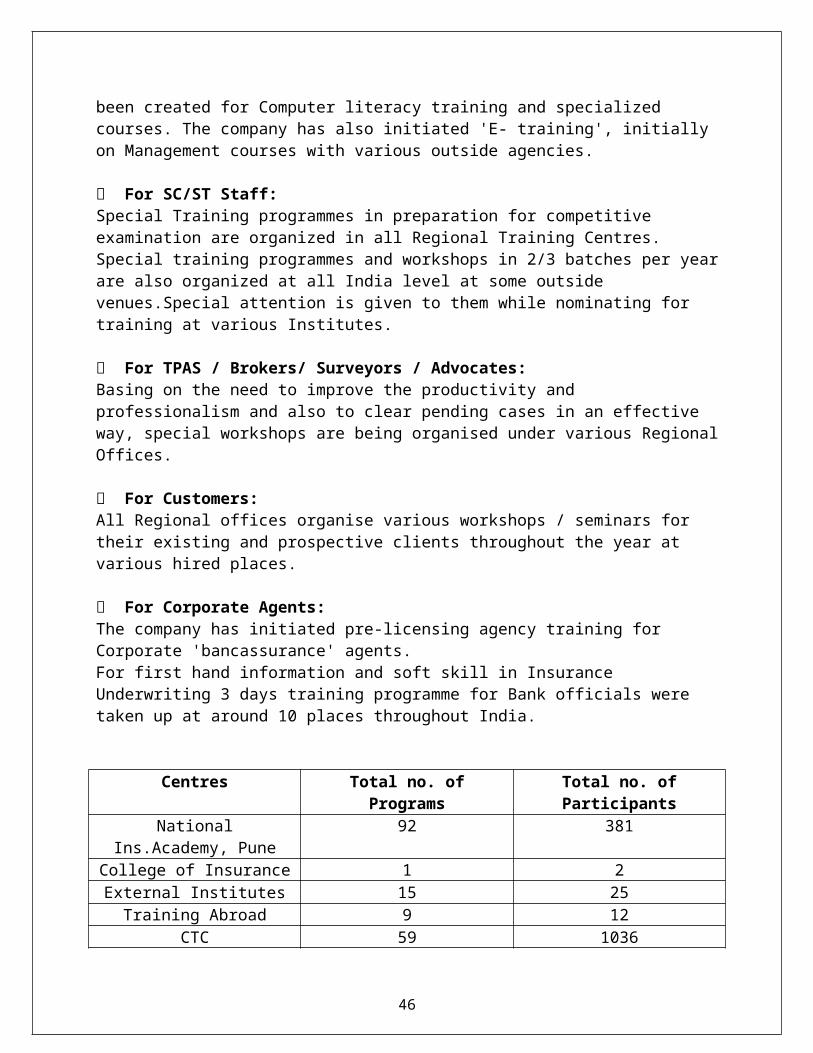

For Officers:RTC, ZTC & CTC make their yearly calendar for regular training, and special trainings on technological changes, departmental changes, for transfers and promotions. National Insurance Academy (NIA), Pune takes up specialized training programme on Insurance, IT, Law and Management topics. Officers are also nominated to various external institutions for training programmes/seminars and conferences. College of Insurance also caters to the needs of officers of Mumbai & Pune region. Being an International Company, the top executives and officers are nominated for overseas training, around 10 cases per year. 10 Computer Learning centres in large cities like Ahmedabad, Kanpur and Mumbai CTC etc have been created for Computer literacy training and specialized courses. The company has also initiated 'E- training', initially on Management courses with various outside agencies.

33

For SC/ST Staff:Special Training programmes in preparation for competitive examination are organized in all Regional Training Centres. Special training programmes and workshops in 2/3 batches per year are also organized at all India level at some outside venues.Special attention is given to them while nominating for training at various Institutes.

For TPAS / Brokers/ Surveyors / Advocates:Basing on the need to improve the productivity and professionalism and also to clear pending cases in an effective way, special workshops are being organised under various Regional Offices.

For Customers:All Regional offices organise various workshops / seminars for their existing and prospective clients throughout the year at various hired places.

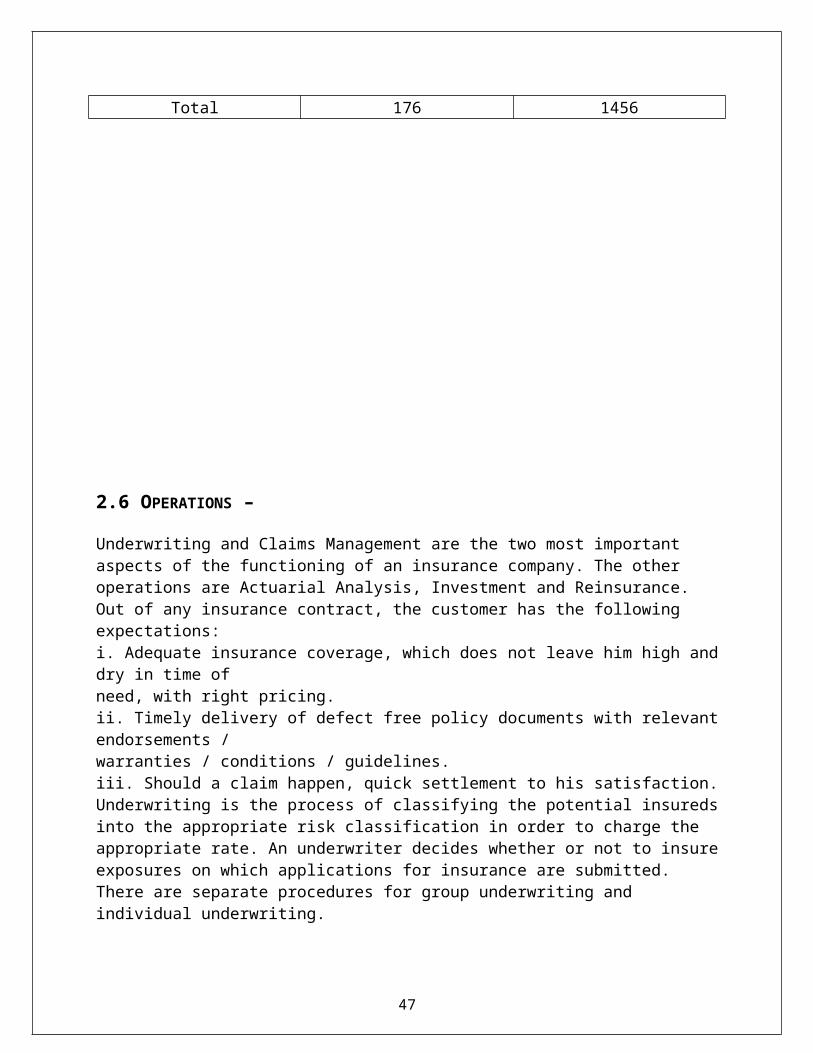

For Corporate Agents:The company has initiated pre-licensing agency training for Corporate 'bancassurance' agents.For first hand information and soft skill in Insurance Underwriting 3 days training programme for Bank officials were taken up at around 10 places throughout India.

Centres Total no. of Programs Total no. of ParticipantsNational Ins.Academy, Pune 92 381

College of Insurance 1 2External Institutes 15 25Training Abroad 9 12

CTC 59 1036Total 176 1456

34

2.6 OPERATIONS –

Underwriting and Claims Management are the two most important aspects of the functioning of an insurance company. The other operations are Actuarial Analysis, Investment and Reinsurance. Out of any insurance contract, the customer has the followingexpectations:i. Adequate insurance coverage, which does not leave him high and dry in time ofneed, with right pricing.ii. Timely delivery of defect free policy documents with relevant endorsements /warranties / conditions / guidelines.iii. Should a claim happen, quick settlement to his satisfaction.Underwriting is the process of classifying the potential insureds into the appropriate risk classification in order to charge the appropriate rate. An underwriter decides whether or not to insure exposures on which applications for insurance are submitted. There are separate procedures for group underwriting and individual underwriting.For any insurance contract to exist there has to be a proposal form. Any individual wishing to take an insurance policy has to first fill the proposal form. Different forms are available for different types of policy. (See Annexure for a Motor Proposal form)The parties to the insurance contract are required to observe utmost good faith (Uberrimae fidei) by disclosing all material information. Examples of material information are type of construction of building in case of fire insurance, type of packing goods and material used in case of marine cargo insurance, cubic capacity of vehicle in motor insurance, physical disabilities if any while taking a personal accident policy. This allows the insurer to decide for a)acceptance of risk b) fixing rate of premium c)terms and conditions of the contract. The proposal forms the basis for any contract and any non disclosure of material facts makes the contract voidable. In case of motor policies where there is a break in policy, a vehicle inspection is done. In case of high risk proposals, technically qualified staff are enlisted to inspect the risk and provide an assessment on the basis of which the policy is underwritten. A medical examination is also necessary in case of Mediclaim policy for clients above the age of 45.Once the proposal is accepted by the competent authority, it is underwritten. The underwriters use the proposal form to fill in the prescribed details in the CWISS system. The underwriter must employ sound judgment based on his or her years of experience to read beyond the basic facts and get a true picture of the applicant and his lifestyle in case of health policies. Of course, the underwriter certainly cannot - and isn't expected to - foresee all possible circumstances. The underwriter's primary function is to protect the insurance company insofar as is possible against adverse selection (very poor risks) and those parties who may have fraudulent intent. Once the underwriter determines that risk can be accepted, the next decision is to apply the proper premium rate. Premium rates are determined for classes of insured by the actuarial department. An underwriter’s role is to decide which class is appropriate for each insured. The business of insurance inherently involves discrimination; otherwise, adverse selection would make insurance unavailable. Once the premium is calculated, the draft is saved and then sent for collection.The client then has to pay the premium to the cashier who then generates a collection receipt and the policy. The policy then becomes active.

35

Actuarial analysis is a highly specialized mathematic analysis that deals with the financial and risk aspects of insurance. Actuarial analysis takes past losses and projects them into the future to determine the reserves an insurer needs to keep and the rates to charge. An actuary determines proper rates and reserves, certifies financial statements, participates in product development, and assists in overall management planning. The rates or premiums for insurance are based first and foremost on the past experience of losses. Actuaries calculate the rates using various procedures and techniques. The most modern techniques include sophisticated regression analysis and data mining tools. In essence, the actuary first has to estimate the expected claim payments. Investment income is a significant part of total income in most insurance companies. The company invests in Government securities and Government guaranteed bonds including Treasury Bills, Other Approved Securities, Debentures/Bonds, Infrastructure and Social Sector projects.Reinsurance is an arrangement by which an insurance company transfers all or a portion of its risk under a contract (or contracts) of insurance to another company. The company transferring risk in a reinsurance arrangement is called the ceding insurer. The company taking over the risk in a reinsurance arrangement is the assuming reinsurer. In effect, the insurance company that issued the policies is seeking protection from another insurer, the assuming reinsurer. Typically, the reinsurer assumes responsibility for part of the losses under an insurance contract; however, in some instances, the reinsurer assumes full responsibility for the original insurance contract.A ceding company (the primary insurer) uses reinsurance mainly to protect itself against losses in individual cases beyond a specified sum (i.e., its retention limit), but competition and the demands of its sales force may require issuance of policies of greater amounts. A company that issued policies no larger than its retention would severely limit its opportunities in the market. Many insureds do not want to place their insurance with several companies, preferring to have one policy with one company for each loss exposure. The national insurer is GIC

36

RISK

ACCEPTANCE

INSURER

QUOTE

PREMIUM

JOB OF PAYING PREMIUM

PROPOSER

OFFER

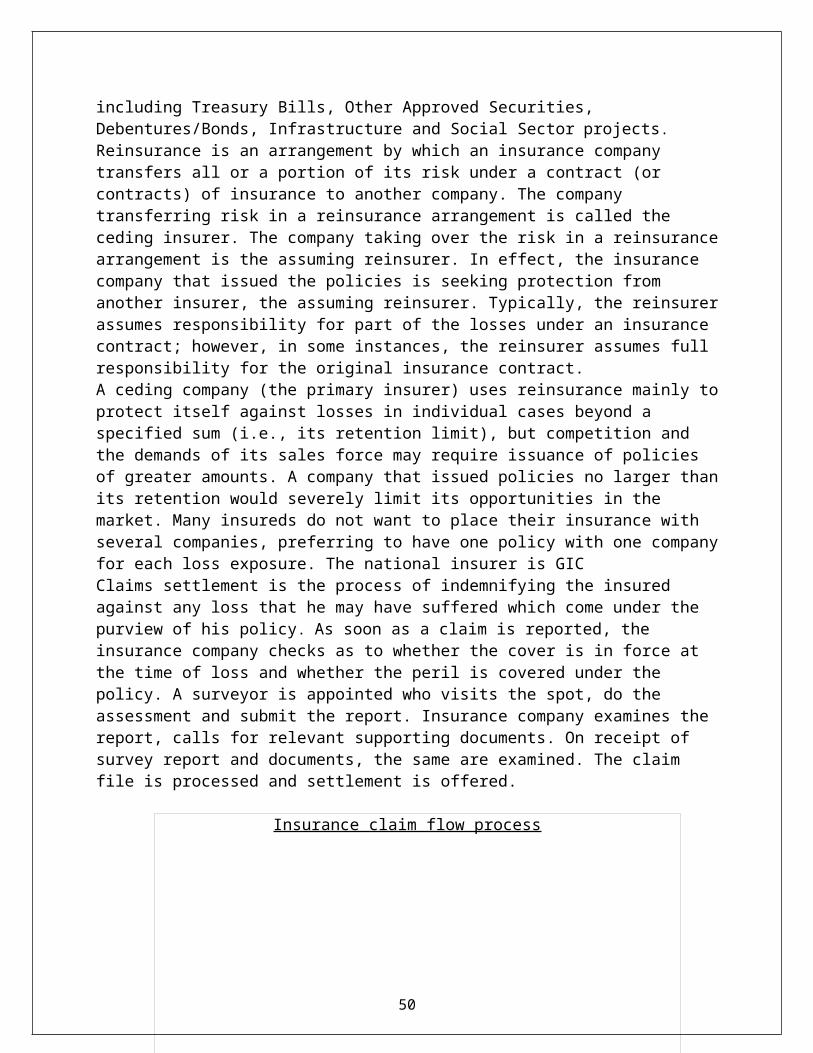

Claims settlement is the process of indemnifying the insured against any loss that he may have suffered which come under the purview of his policy. As soon as a claim is reported, the insurance company checks as to whether the cover is in force at the time of loss and whether the peril is covered under the policy. A surveyor is appointed who visits the spot, do the assessment and submit the report. Insurance company examines the report, calls for relevant supporting documents. On receipt of survey report and documents, the same are examined. The claim file is processed and settlement is offered.

Insurance claim flow process

2.7 FINANCE-

37

INTIMATE CLAIM

SUBMIT CLAIM FORM WITH RELEVANT DOCUMENTS

VERIFY COVERAGE

ASSIGN SURVEYOR FOR ASSESSMENT

SURVEYOR REPORT +

DOCUMENTS

ACCEPT CLAIM

ARCHIVE

REPUDITE CLAIM

CLOSED

(in %)

Sl.No. Particulars

Upto the Quarter

Ending 31st Mar.,2011

Upto the Quarter

Ending 31st Mar.,2010

1 Gross Premium Growth Rate 15.87 9.97

2 Gross Premium to Shareholders' Fund Ratio 34.70 30.77

3 Growth Rate of Shareholders' Fund 2.75 56.53

4 Net Retention Ratio 87.44 84.55

5 Net Commission Ratio 9.02 9.35

6Expense of Management to Gross Direct Premium Ratio

32.78 34.61

7 Combined Ratio 104.97 108.66

8 Technical Reserves to Net Premium Ratio 177.84 177.29

9 Underwriting Balance Ratio -36.75 -28.64

10 Operationg Profit Ratio -17.68 -8.38

11 Liquid Assets to Liabilities Ratio 49.07 48.28

12 Net Earning Ratio -5.86 6.74

13 Return on Net Worth Ratio -1.78 1.75

14Available Solvency Margin to Required Solvency Margin Ratio

2.97 3.55

Equity Holding Pattern

1 (a) No. of shares 200000000 200000000 200000000 200000000

2(b) Percentage of shareholding (Indian / Foreign)

100/0 100/0 100/0 100/0

3( c) %of Government holding (in case of public sector insurance companies)

100 100 100 100

4(a) Basic and diluted EPS before extraordinary items (net of tax expense) for the period (not to be annualized)

-21.08 -21.08 20.23 20.23

5(b) Basic and diluted EPS after extraordinary items (net of tax expense) for the period (not to be annualized)

-21.08 -21.08 20.23 20.23

6 (iv) Book value per share (Rs) 348.71 348.71 371.51 371.51

2.8 ORGANIZATIONAL HIERARCHY

38

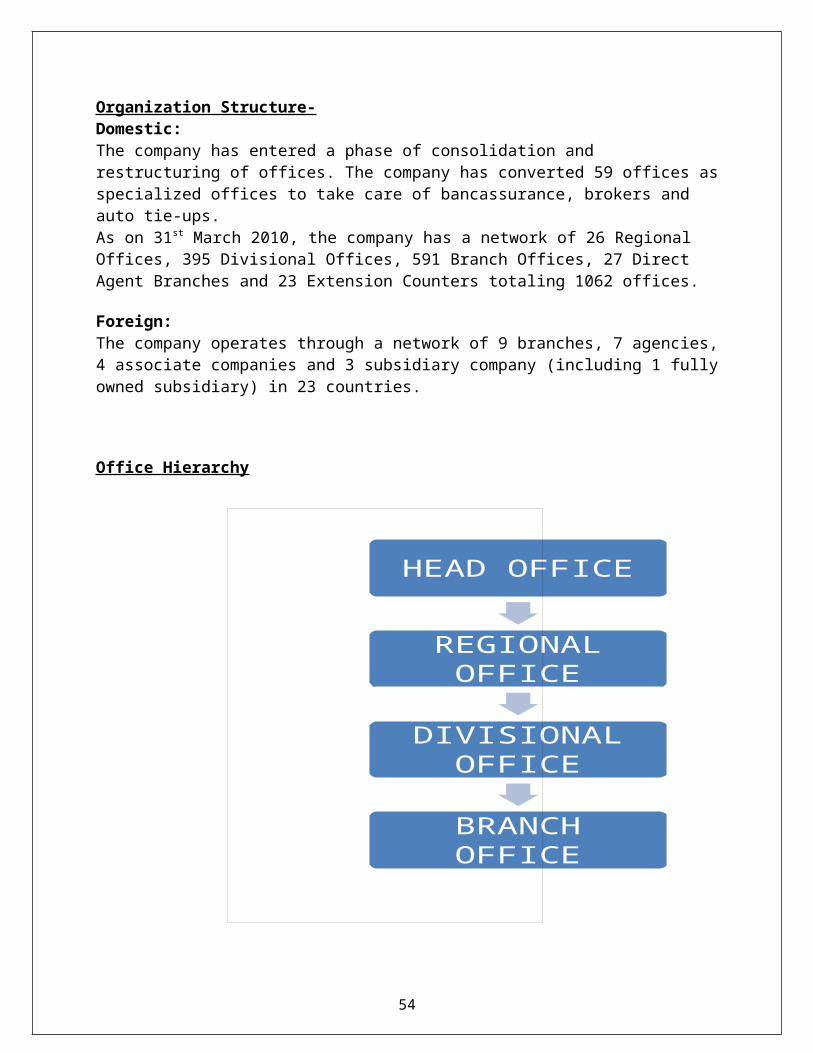

Organization Structure-Domestic:The company has entered a phase of consolidation and restructuring of offices. The company has converted 59 offices as specialized offices to take care of bancassurance, brokers and auto tie-ups.

39

CHAIRMAN CUM MANAGING DIRECTOR

GENERAL MANAGERS

DEPUTY GENERAL MANAGERS

CHIEF MANAGERS

MANAGERS

DEPUTY MANAGERS

ASSISTANT MANAGERS

ADMINISTRATIVE OFFICERS

As on 31st March 2010, the company has a network of 26 Regional Offices, 395 Divisional Offices, 591 Branch Offices, 27 Direct Agent Branches and 23 Extension Counters totaling 1062 offices.

Foreign:The company operates through a network of 9 branches, 7 agencies, 4 associate companies and 3 subsidiary company (including 1 fully owned subsidiary) in 23 countries.

Office Hierarchy

2.9 ENVIRONMENT -

Social Environment – Profit is not the first criterion of public sector units. Social welfare is the ultimate goal of development of insurance sector. The government has devised a lot of social security measures

40

HEAD OFFICE

REGIONAL OFFICE

DIVISIONAL OFFICE

BRANCH OFFICE

for India’s rural, socially backward classes of people. Prices of such products are reduced.Insurers are obliged to provide insurance to atleast 20000 lives each year. In case of general insurance, this obligation includes the insurance of crops ( Sec.32 B and 32C of Insurance Act,1938 and the IRDA regulations 2000.) The government has also introduced various schemes such as ‘Rashtriya Krishi Bima Yojana’ to provide insurance coverage to farmers in case of failure of crops. ‘Solatium Scheme’ for payment of compensation to victims of hit and run accidents. In addition to this the company provides policies such as ‘Universal Health Insurance Scheme’ and ‘Jan Arogya Bima Policy’ at nominal rates to the less-privileged. In a democratic setup, insurance companies are accountable to the public through 1.)Parliament 2.)Audit and3.)Annual reports as a social measure.

Social responsibilities of insurance business

Legal Environment - The IRDA Act of 1999 was enacted with a view to regulate the Insurance Companies irrespective of private and nationalized companies. Any insurance company is obliged to abide by the rules and follow the guidelines as prescribed by IRDA from time to time. These include the IRDA Regulation 2000 on ‘Appointed Actuary’ and the ‘Obligations of Insurance to Rural

41

Insurance BusinessInsurers

Promoters/Shareholders

Consumer Insured

Workers

Managers

TPAs

Reinsurers

Suppliers

Surveyors,Lawyers,Actuaries

Social sectors’ which specifies that the company has to undertake certain obligations pertaining to the persons in Rural and Social Sectors in each financial year. ‘Assets, Liabilities and Solvency Margin of Insurance’ also specifies that the insurer has to maintain a solvency margin as prescribed by IRDA. The ‘Investment Regulation’ deals with type of investment in the following segments – central government securities, state government securities and other approved securities. The Motor Vehicles Act 1988 specifies the third party liability arising out of the use of motor vehicles in a public place and compensation for the same.

Political Environment - The Central Government being satisfied that it is necessary in the public interest to do so, exempts the taxes leviable for schemes such as Cattle Insurance under IRDP (Irrigated Rural Development Program), Janata Personal Accident Scheme, Agriculture Pump Set Insurance and other such social welfare schemes.

Economic Environment - Insurance is the result of various economic activities causing employment and is dependant on the total net income, national economic and industrial development. On the other hand insurance also has the responsibility to provide stability and security to economy and industry. The company cannot behave with sole profit motives. Policies with less demand have become costlier to the insurer but due to social obligations, the pricing remains subsidized. The premium collected is not even sufficient to cover the cost of issuing the policies (stationery, man hours involved, stamp duty) in case of certain schemes as such is operating at a loss ratio of above 100%. An insurer is not permitted to invest in private limited companies. Insurer is also not permitted to keep more than 10% of his assets in fixed and current deposit or both in one banking company.

Physical Environment – If one area is endemic to one peril (For eg – Kutch, Gujarat is prone to earthquakes, Khopoli, Maharashtra is prone to landslides) then to cover the insurance risk of that area, premium rates will be higher than other areas.

Technological Environment - The company introduced its first automated system ‘Genisys’ in 1998. However, this was an rudimentary system and the spread of technology for insurance services such as underwriting and claims management was slow. It was only recently that the company has entered into online transaction of business. It is needless to say that the technology provides better quality, quickness, better space utilization and easier data storage. The spread of technology has also helped improve the customer service.

2.10 SWOT ANALYSIS-

Strengths- The Company is without doubt the largest non-life insurance company in India. It is the market leader in terms of premium underwritten in the fire (23% market share), marine (22%),

42

engineering (18%), health (21%) and liability (15%) sectors. The New India Assurance is a pioneer non-life insurance company insuring all types of assets, belongings and lives of rural and social sector in the country. A leading market position gives a company a stronghold within the industry. Financially the company is in a strong position with the profits after tax for the financial year 2009-10 being Rs.404 crores, an increase of 80% from the previous year. The gross direct premium also recorded a good growth rate of 9.69% as against 4.39% growth registered during 2008-09. Continued good investment performance enabled the company to earn an investment income of 2139 crores as against 1686 crores in the previous year.The company has an available solvency margin of 6621 crores while the required solvency margin under IRDA regulations is 1429.33 crores. Its widespread network of 1062 offices across the country helps in its product distribution to all corners of the country. The company has experienced and technically competent staff who understand the nuances of the insurance industry. Claim hubs have been created for centralized claim processing in all Regional Office centres. This has helped the company achieve a very high claims settlement ratio. The company has been able to bring down the average claim settlement time from 137 days in 2008-09 to 88 days in 2009-10. It has been able to reduce its Motor T.P losses which are severely affecting the profitability of all insurance companies thanks largely to the diligent efforts taken to settle as many claims promptly through Lok Adalats and conciliation.Large Corporate Regional Offices have helped provide dedicated service and organizational focus to corporate clients and government accounts

Weakness- During the financial year 2009-10 the underwriting deficit has gone up by 255 crores mainly due to increased operating expenses and adjustments for the previous year. In these times of intense competition where premium rates have bottomed out and companies are struggling for their very survival due to a high combined ratio, the employees fail to realize the importance of customer service in not only retaining but also generating fresh premium. Customers are made to wait for service and are sometimes shunted from one counter to another.Another major weakness is the treatment of agents who generate a majority of the premium for the company. As per their own admission, they are treated worse than the sub staff and not accorded the respect that they deserve from the employees. Also, there is a delay in payment of the Agent’s fees which is effectively the salary of the Agents.The employees are not particularly well versed in the use of computers and in this day and age; this is a major drawback. Also the computer systems in use are outdated and infested with problems. The connectivity of the system is quite poor causing inordinate delay to the customers who are made to wait for no fault of theirs.The company recently implemented a new ERP package called CWISS. However, proper planning has not been done before implementing this change. The employees weren’t adequately trained and a number of them are facing difficulties while working in the new system. Also, all the existing policies have not been fully migrated to the new system. Hence, employees have to use both the systems (GENISYS and CWISS) simultaneously which is a major hassle. The underwriters also face difficulties due to this. The HR policies in practice are out of date and not in sync with the current times. Profit linked incentives are provided to all employees and hence, there is hardly any motivation for the people who work hard and those who don’t. The company is losing productive man hours due to the

43

absence of a mechanized attendance system. Since there is no individual accountability, there seems to be a certain lethargy in the attitude of a majority of the employees. There is a certain lack of professionalism.In quite a few cases, premium has been accepted from the customer. However the policy has not been underwritten. This causes major issues in accounting and in the event of claims; the insurer find themselves in a position where they are unable to register a claim.

Opportunity-Insurance is a business of distress management and the process of claims management is the final moment of truth. The claims manager should be sensitive to the needs of the claimant. When it is obvious that the claim is legitimate, less importance should be laid on a slew of formalities and the intent should be on settling the claim swiftly. If the company follows the dictum of “low on promise and high on delivery”, it will lead to customer delight and result in a long and lasting relationship between the insurer and the insured.Being the largest company, New India has the built-in strength and the capacity to underwrite big businesses. The company has the potential to focus on huge projects such as large infrastructure projects, mega power plants. We are seeing rapid development across the country with express highways, metro rails, international standard airports, port development, power plant projects coming up across the country. These projects demand insurance cover of international standard and the company will do well to tap into this new market by providing tailor made all risk package policies.The auto industry is also growing at rapid pace. As motor policies are compulsory in India, this portfolio can give incremental rise to the premium of the company.With rising awareness, all kinds of insurance especially health is now at the precipice of an explosion. The penetration of insurance is hardly 3% of the population. This means there is a potential of market of over 97% of the population. The company is now facing losses in the Health Sector and the major reason for this is the small spread of risk and the problem of anti-selection. Once this is sorted, this sector has the potential to be a source of immense profit for the organization. Also an increase in the disposable income of individuals will give a boost to health and other personal lines of insurance. The insurance industry is seeing a double digit growth every year and new talent should be recruited to take the business forward. The company needs to reinvent itself along the lines of many nationalized banks.If the company gains a more professional approach, it will help the company survive the intense competition. If every claim is attended to with compassion and enthusiasm and the claim settlement duration is brought down further, it will enhance the reputation of the company.The thrust on liability policies have not been much so far and not many people are aware of these policies. There is tremendous potential if the company focuses on this untapped segment.

Threats- When the customers are not afforded the service that they demand; it is but natural that they will tend to go elsewhere. No doubt, this has been one of the major factors for the stupendous growth of private sector insurance companies that pride themselves on providing excellent customer service. The company risk losing out on corporate clients who can provide crores of rupees in premium due to a perceived lack of support from the insurer.

44

If the management does nothing to ease the complaints of the Agents, they are likely to jump ship and switch over to the private sector.The non life insurance industry today faces its biggest challenge of mounting underwriting losses. This has been primarily because of the lack of focus on prudent underwriting and effective claims management.

CHAPTER III-DISCUSSION ON TRAINING

3.1 ROLES AND RESPONSIBILITIES – During the initial phase of the internship, my role as an intern was to get acquainted with the various terms and concepts of the insurance industry. It was my responsibility to read up as much

45