Sinfonia Technology Co., Ltd. · Sinfonia Technology Co., Ltd. ... Sinfonia with a Buy rating given...

15

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report. 1 Sinfonia Technology Co., Ltd. November 21, 2016 ◆ Electronics manufacturer with cutting-edge motion-control technologies Sinfonia Technology (Sinfonia) is an electronic company whose main products are Electronic Components for Aircraft, Factory Automation (FA) Equipment, and Semiconductor Transportation Equipment, to name a few. Especially, the company is superior in its high precision motion-control technologies. ◆ The company’s revenues and income will increase for five consecutive FYs Capital Partners Security (CPS) estimates that, thanks to the semiconductor related equipment’s sales growth, the company’s robust results will continue into FY2016 (ending March 2017) as follows: revenue 85,400 million yen (+6.6%, YoY), and operating income 5,600 million yen (+27.0%, YoY). As for the next FY (ending March 2018), CPS anticipates that, due to an expected growth of electronic components for aircrafts, the company will achieve revenues and income of 89,100 million yen (+4.3%, YoY) and 6,720 million yen (+20.0%, YoY), respectably, recording an increase of these figures for five years in a row. ◆ Motion-control technologies are key devises which support aircrafts of the Japan Self-Defense Forces (SDF) and rockets. The company retains advanced technologies enabling a precise and effective control of actuators and motors. These technologies are highly valued in several industries and adopted by aircrafts of the SDF, rockets, and semiconductor production equipment (SPE) where a precise control of devices is indispensable. ◆ Target Price and Investment Rating We expect the company will continue to grow steadily with no crucial issue on their financial conditions. Considering that the estimated average PER of all stocks listed on the Tokyo Stock Exchange’s (TSE) First Section is about 15x, we believe it is appropriate to set Sinfonia’s PER at 15x as well. Taking both such PER and this financial year’s estimated EPS of 24.9 yen into consideration, we derive the target price of 370 yen. We initiate Sinfonia with a Buy rating given that the upside to the target price is about 69%. Investment Rating Buy Target Price (Yen) 370 Stock Price 219 (Closing price on November 18) TSE code 6507 Market Capitalization 32,653 (Million Yen) Outstanding Shares 148,689 (Thousand shares) PBR (curr) 1.1 Dividend Yield (E)(%) 2.3 Capital Partners Securities Research Department Naoki Tsuchiya [email protected]

Transcript of Sinfonia Technology Co., Ltd. · Sinfonia Technology Co., Ltd. ... Sinfonia with a Buy rating given...

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

1

Sinfonia Technology Co., Ltd. November 21, 2016

◆ Electronics manufacturer with cutting-edge motion-control

technologies

Sinfonia Technology (Sinfonia) is an electronic company whose

main products are Electronic Components for Aircraft, Factory

Automation (FA) Equipment, and Semiconductor Transportation

Equipment, to name a few. Especially, the company is superior in

its high precision motion-control technologies.

◆ The company’s revenues and income will increase for five

consecutive FYs

Capital Partners Security (CPS) estimates that, thanks to the

semiconductor related equipment’s sales growth, the company’s

robust results will continue into FY2016 (ending March 2017) as

follows: revenue 85,400 million yen (+6.6%, YoY), and operating

income 5,600 million yen (+27.0%, YoY). As for the next FY (ending

March 2018), CPS anticipates that, due to an expected growth of

electronic components for aircrafts, the company will achieve

revenues and income of 89,100 million yen (+4.3%, YoY) and 6,720

million yen (+20.0%, YoY), respectably, recording an increase of

these figures for five years in a row.

◆ Motion-control technologies are key devises which support

aircrafts of the Japan Self-Defense Forces (SDF) and rockets.

The company retains advanced technologies enabling a precise

and effective control of actuators and motors. These technologies

are highly valued in several industries and adopted by aircrafts of

the SDF, rockets, and semiconductor production equipment (SPE)

where a precise control of devices is indispensable.

◆ Target Price and Investment Rating

We expect the company will continue to grow steadily with no

crucial issue on their financial conditions. Considering that the

estimated average PER of all stocks listed on the Tokyo Stock

Exchange’s (TSE) First Section is about 15x, we believe it is

appropriate to set Sinfonia’s PER at 15x as well. Taking both such

PER and this financial year’s estimated EPS of 24.9 yen into

consideration, we derive the target price of 370 yen. We initiate

Sinfonia with a Buy rating given that the upside to the target price is

about 69%.

Investment Rating Buy

Target Price (Yen) 370

Stock Price 219

(Closing price on

November 18)

TSE code 6507

Market Capitalization 32,653

(Million Yen)

Outstanding Shares 148,689

(Thousand shares)

PBR (curr) 1.1

Dividend Yield (E)(%) 2.3

Capital Partners Securities

Research Department

Naoki Tsuchiya

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

2

【Consolidated Financial Results】 (millions of Yen)

FY Ended March 31 Revenue Operating

Income

Ordinary

Income

Net

Income EPS(Yen) PER(x)

2015 75,796 2,757 2,554 1,820 12.2 18.0

2016 80,080 4,409 4,231 2,850 19.2 11.4

2017E 85,400 5,600 5,460 3,700 24.9 8.8

2018E 89,100 6,720 6,610 4,550 30.6 7.2

2017 Company forecast 85,000 5,500 5,000 3,400 22.9 9.6

Source: Securities report, Estimates by CPS, Company forecast

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

3

Ⅰ. Performance Overview

Expecting the company’s revenues and income will increase for five FYs

in a row Sinfonia is an electronic company whose main products are Electronic Components for Aircraft, Factory Automation (FA) Equipment, Semiconductor Transportation Equipment, and Water and Sanitation Management System. Especially, the company is superior in high precision actuators, motors and their motion-control technologies. These technologies are highly valued in several industries and adopted by aircrafts of the SDF, rockets, and semiconductor production equipment (SPE) where a precise control of devices is indispensable. As for this FY (ending March 2017), given the brisk sales of Semiconductor Transportation Equipment, the company will achieve a robust increase in both revenues and income as follows: revenue 85,400 million yen (+6.6%, YoY), operating

income 5,600 million yen (+27.0%, YoY), and net income 3,700million yen(+29.8%,

YoY). Since CPS expects a sales growth of Electronic Components for Aircraft and

Water and Sanitation Management System in the coming year, the company’s next FY (ending March 2018) results will be as follows: revenue 89,100 million yen (+4.3%, YoY), operating income 6,720 million yen (+20.0%, YoY), and net income 4,550 million

yen (+23.0%, YoY). This marks an increase of revenues and profits for five FYs in a

row.

【Trend of Revenue and Operating Income】

0

2,000

4,000

6,000

8,000

10,000

0

20,000

40,000

60,000

80,000

100,000Revenue(LHS)

Operating Income(RHS)

millions of Yen millions of Yen

Source: Securities report, Estimates by CPS

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

4

Ⅱ. Motion Equipment business

(Compositon ratio 39.2% in FY2016 Projected Revenue)

Growing electrical components for aircrafts of the Self-Defense Forces (SDF) The motion equipment business mainly consists of aerospace-related equipment and motion control equipment (FA equipment). Aerospace-related equipment includes products for civilian aircrafts and rockets, while many are electrical components for aircrafts used by the SDF. Sinfonia supplies electrical equipment such as actuators and generators for the SDF’s fighters and surveillance aircrafts. They are presumably used as critical components for firearms and engines. The motion control device is composed of high-precision direct drive motors and electromagnetic clutches, etc. which are used in factory production lines. Further, the company is superior in such products as motors and controllers for construction machines.

The orders received for this business during 1H of the current FY (ending in Sept. 2016)

were 20,319 million yen (up 37.7% YoY), and the order backlog recorded 23,593 million yen (up 37.7% YoY). In addition to an order related to the new type of antisubmarine surveillance aircrafts (model name: P-1), an increasing demand for maintenance of existing SDF aircrafts would have contributed to a healthy intake of orders. In accordance with a recent sharp increase of scrambles, an operational distance of SDF aircrafts has increased, which seems to have resulted in a growing demand for maintenance.

For FY ending in Mar. 2017, CPS estimates that, thanks to increased aerospace-related equipment, this business will show a recovery with revenue and operating income of 33,500 million yen (up 7.6% year YoY) and 780 million yen (up 20.6% YoY), respectively. For the next FY ending in Mar. 2018, we anticipate that, due to expected expansion of motion control equipment business and a growing market of aerospace-related equipment, the business will show a continued growth with revenue and operating income of 36,200 million yen (up 8.1% YoY) and 1,270 million yen (up 62.8% YoY), respectively.

【Breakdown of Revenue from Motion Equipment business by Product Category(FY ended Mar. 2016)】

Aerospace-

related

equipment,

38%

Motion Control

equipment,

46%

Others, 16%

Source: Sinfonia’s financial report

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

5

【Motion Equipment business: Trend of Revenue and Operating Income】

【Motion Equipment business: Trend of Order backlog】

0

400

800

1,200

1,600

0

10,000

20,000

30,000

40,000

Revenue(LHS)

Operating Income(RHS)

millions of Yen millions of Yen

0

5,000

10,000

15,000

20,000

25,000

Sep.2013 Mar. 2014 Sep.2014 Mar.2015 Sep.2015 Mar.2016 Sep.2016

millions of Yen

Source: Securities report, Estimates by CPS

Source: Securities report

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

6

【Trend of scramble of SDF aircrafts】

【Antisubmarine surveillance aircraft P-1】

0

200

400

600

800

1,000Times

Source: Ministry of Defense website

Source: Ministry of Defense Chief of Staff release

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

7

Ⅲ. Power Electronics Equipment business

(Compositon ratio 43.9% in FY 2016 Projected Revenue)

In addition to Semiconductor Transportation Equipment, Water Supply and Sewerage

Management System expected to grow.

Power Electronics Equipment business mainly consists of Semiconductor Transportation Equipment, Social Infrastructure System, and Automobile Test Equipment. Sinfonia’s semiconductor transportation device is a device connected to an etcher and a CVD, etc., and plays a role to deliver a silicon wafer sealed in a delivery box to etchers and CVDs without being exposed to the air. Technology utilizing a special gas is highly valued, which enables silicon wafers to be precisely positioned while preventing oxidation of silicon wafers. Sinfonia is the top manufacturer in this field of equipment. Social infrastructure system mainly handles Water supply and Sewerage management systems. It provides comprehensive services including Water Supply and Sewerage Control system, Surveillance monitor, Plant Controller, and Receiving & Transforming equipment.

The orders received amounted to 18,711 million yen (up 27.7% YoY), and the order backlog was 20,048 million yen (up 27.2% YoY) for 1H of the current FY (ended in Sept. 2016). Orders received for Semiconductor Transportation equipment have continued to be impressive. Orders for Water Supply and Sewerage management systems have also increased, both of which have contributed to the favorable results. Most of water supply facilities in Japan were developed in the 1970s, and as a result, the demand for renewal of these facilities seems to have increased after 40 years of usage.

For the current FY (ending March 2017), we expect the business results of 37,500 million yen (up 10.7% YoY) in revenue and 3,900 million yen (up 50.6% YoY) in operating income, mainly due to the steady growth of highly profitable semiconductor transportation equipment. For the next FY (ending March 2018), we expect 38,600 million yen (up 2.9% YoY) in revenue and 4,300 million yen (up 10.3% YoY) in operating income, given an additional business of Water Supply and Sewerage management system.

【Breakdown of Revenue from Power Electronics Equipment business by Product Category

(FY ended Mar. 2016)】

Semiconductor

Transportation

Device, 28%

Social

Infrastructure

System, 20%

Automobile Test

Equipment,

13%

Industrial

Infrastructure

System, 13%

Others, 26%

Source: Sinfonia’s financial report

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

8

【Trend of Revenue and Operating Income from Power Electronics Equipment business】

【Trend of Order backlog from Power Electronics Equipment business】

Source: Securities report

0

1,000

2,000

3,000

4,000

5,000

6,000

0

10,000

20,000

30,000

40,000Revenue (LHS)

Operating Income (RHS)

millions of Yen millions of yen

0

5,000

10,000

15,000

20,000

25,000

Sep.2013 Mar.2013 Sep.2014 Mar.2015 Sep. 2015 Mar.2016 Sep.2016

millions of Yen

Source: Securities report, Estimates by CPS

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

9

【Sinfonia‘s Semiconductor transportation devices】

【World Trend of Orders received of Semiconductor equipment devices】

0

2,000

4,000

6,000

8,000

10,000

12,000

1Q2013 3Q2013 1Q2014 3Q2014 1Q2015 3Q2015 1Q2016

Million US$

Source: Sinfonia Technology Co., Ltd. website

Source: SEMI

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

10

【Trend of Investment amount in Domestic Water Supply】

【Ratio of Water utility facilities after legal durable life】

0

5,000

10,000

15,000

20,000100 millions of Yen

0%

5%

10%

15%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Ministry of Health, Labor and Welfare “Outline of Water Supply business Policy”

Source: Ministry of Health, Labor and Welfare “Outline of Water Supply business Policy”

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

11

Ⅳ. Target Price and Investment Rating As a result of its efforts to improve operations besides favorable external environment, it is expected that Sinfonia will expand its business on a continuous basis. Based on the company’s expected healthy financials, we have made a judgement that this stock could be valued at the same level as the market average. Considering the average value of projected PER for companies listed on the TSE First Section is approximately 15x (based on the Bloomberg data), we believe that 15x would be justified as Sinfonia’s expected PER for the current FY. With an expected EPS of 24.9 yen, we derive our target price of 370 yen. Given the upside to the target price is approximately 69%, we initiate Sinfonia with a “BUY” rating.

【Revenue and Operating Income by Segment】

(millions of Yen)

FY ended in March 2014 2015 2016 2017 (E) 2018 (E)

(Revenue)

Motion Equipment 32,486 33,835 31,121 33,500 36,200

Power Electronics Equipment 26,501 28,110 33,880 37,500 38,600

Support & Engineering 22,348 21,370 22,779 22,300 22,600

Adjustment -7,020 -7,519 -7,700 -7,900 -8,300

Total 74,315 75,796 80,080 85,400 89,100

(Over previous FY)

Motion Equipment 6.7% 4.2% -8.0% 7.6% 8.1%

Power Electronics Equipment 3.8% 6.1% 20.5% 10.7% 2.9%

Support & Engineering 19.4% -4.4% 6.6% -2.1% 1.3%

Adjustment 35.3% 7.1% 2.4% 2.6% 5.1%

Total 6.9% 2.0% 5.7% 6.6% 4.3%

(Operating Income)

Motion Equipment 1,185 830 647 780 1,270

Power Electronics Equipment 290 968 2,589 3,900 4,300

Support & Engineering 926 968 1,208 1,010 1,250

Adjustment 13 -9 -35 -90 -100

Total 2,414 2,757 4,409 5,600 6,720

(Operating Margin)

Motion Equipment 3.6% 2.5% 2.1% 2.3% 3.5%

Power Electronics Equipment 1.1% 3.4% 7.6% 10.4% 11.1%

Support & Engineering 4.1% 4.5% 5.3% 4.5% 5.5%

Adjustment -0.2% 0.1% 0.5% 1.1% 1.2%

Operating Margin 3.2% 3.6% 5.5% 6.6% 7.5%

Source: Securities report, Estimates by CPS

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

12

【Consolidated Statement of Income】

(millions of Yen)

FY ended in March 2014 2015 2016 2017(E) 2018(E)

Revenue 74,315 75,796 80,080 85,400 89,100

Growth, YoY 6.9% 2.0% 5.7% 6.6% 4.3%

COGS 58,316 59,464 62,575 66,120 68,310

Gross Profit 15,999 16,332 17,505 19,280 20,790

Gross Profit Margin 21.5% 21.5% 21.9% 22.6% 23.3%

SGA 13,585 13,575 13,096 13,680 14,070

Operating Income 2,414 2,757 4,409 5,600 6,720

Operating Margin 3.2% 3.6% 5.5% 6.6% 7.5%

Non-Operating Revenue 215 291 324 330 320

Non-Operating Expense 536 494 502 470 430

Current Profit 2,093 2,554 4,231 5,460 6,610

Extraordinary Profit 0 309 0 0 0

Extraordinary Loss 0 62 239 80 0

Pretax Income 2,093 2,801 3,992 5,380 6,610

Corporate tax, etc. 711 981 1,142 1,680 2,060

Net Income 1,382 1,820 2,850 3,700 4,550

EPS(Yen) 9.3 12.2 19.2 24.9 30.6

BPS(Yen) 172.0 201.8 201.8 221.9 247.2

Number of Outstanding Shares 148,726 148,708 148,696 148,690 148,690

(thousands)

Source: Securities report, Estimates by CPS

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

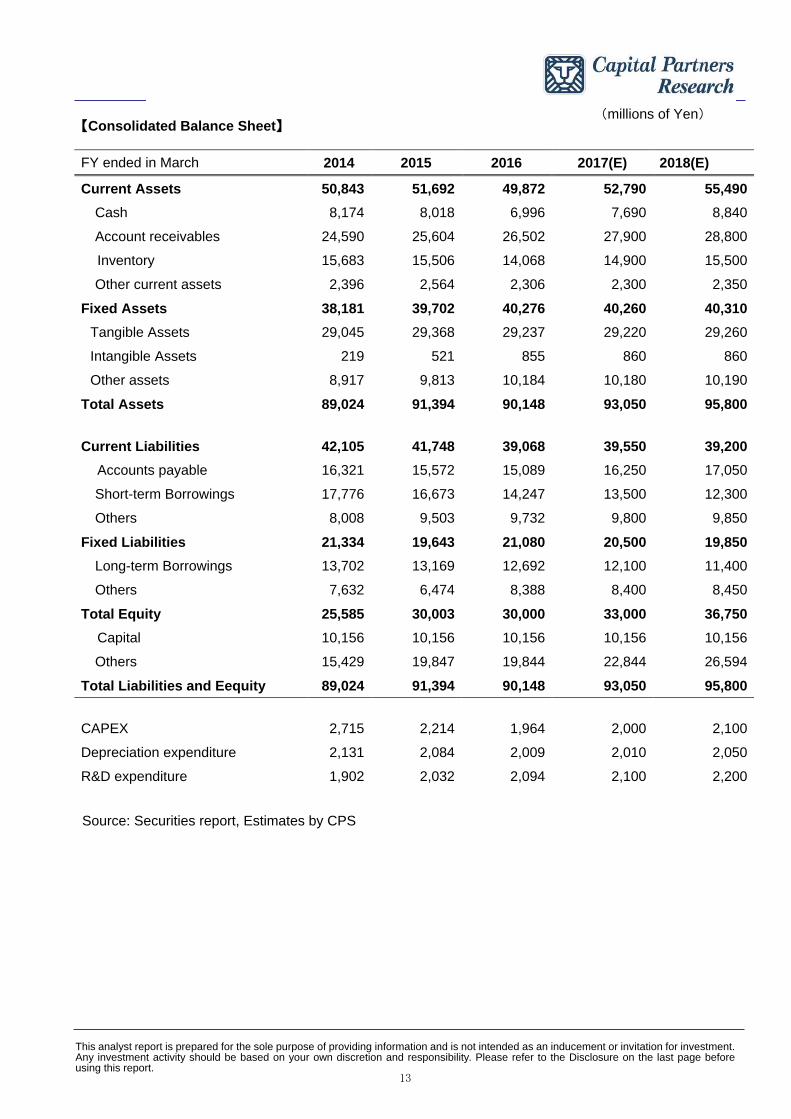

13

【Consolidated Balance Sheet】 (millions of Yen)

FY ended in March 2014 2015 2016 2017(E) 2018(E)

Current Assets 50,843 51,692 49,872 52,790 55,490

Cash 8,174 8,018 6,996 7,690 8,840

Account receivables 24,590 25,604 26,502 27,900 28,800

Inventory 15,683 15,506 14,068 14,900 15,500

Other current assets 2,396 2,564 2,306 2,300 2,350

Fixed Assets 38,181 39,702 40,276 40,260 40,310

Tangible Assets 29,045 29,368 29,237 29,220 29,260

Intangible Assets 219 521 855 860 860

Other assets 8,917 9,813 10,184 10,180 10,190

Total Assets 89,024 91,394 90,148 93,050 95,800

Current Liabilities 42,105 41,748 39,068 39,550 39,200

Accounts payable 16,321 15,572 15,089 16,250 17,050

Short-term Borrowings 17,776 16,673 14,247 13,500 12,300

Others 8,008 9,503 9,732 9,800 9,850

Fixed Liabilities 21,334 19,643 21,080 20,500 19,850

Long-term Borrowings 13,702 13,169 12,692 12,100 11,400

Others 7,632 6,474 8,388 8,400 8,450

Total Equity 25,585 30,003 30,000 33,000 36,750

Capital 10,156 10,156 10,156 10,156 10,156

Others 15,429 19,847 19,844 22,844 26,594

Total Liabilities and Eequity 89,024 91,394 90,148 93,050 95,800

CAPEX 2,715 2,214 1,964 2,000 2,100

Depreciation expenditure 2,131 2,084 2,009 2,010 2,050

R&D expenditure 1,902 2,032 2,094 2,100 2,200

Source: Securities report, Estimates by CPS

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

14

Disclosure

Explanation of Valuation Grade

BUY: Target price is expected to be greater than 20% the current stock price

NEUTRAL: Difference between target price and current stock price is ±20%

SELL: Target price is expected to be less than 20% of the current stock price

Definition and Risks in Achieving the Target Price

The target price is a stock price level that the analyst is expecting to reach over the next six

months based on the business operations and financial forecasts of the company. There

are also risks for achieving the target price such as changes in the business environment

and its competitive state, changes in domestic and foreign economic conditions and

financial market, stock market volatility and exchange rate fluctuations, changes in

regulatory requirements, occurrence of accidents and large-scale disasters. In addition to

these factors, unforeseeable events might also make it difficult to achieve the target price.

Other Considerations

This analyst report is written based on data Capital Partners Securities believes reliable, but

we do not guarantee accuracy or completeness of its contents. The contents of this report

are made based on data and information available at the time of reporting and are subject

to change without notice. Capital Partners disclaims any and all liability for any

consequence caused by using this report. Please use this report based on your own

judgment and at your own risk.

This analyst report is prepared for the sole purpose of providing information and is not intended as an inducement or invitation for investment. Any investment activity should be based on your own discretion and responsibility. Please refer to the Disclosure on the last page before using this report.

15

Trade Name: Capital Partners Securities Co., Ltd.

Member of Japan Securities Dealers Association and registered

as Financial Instruments Business Operator with the Kanto Local

Finance Bureau (Registration No. 62)

http://www.capital.co.jp/

◆Head Office

8th

Floor Shikoku Building, 1-13-7 Uchikanda, Chiyoda Ku, Tokyo, 101-0047

Tel. No.: +81-3-3518-9300 (General Line)

◆Osaka Branch

Umeda Pacific Building, 2-5-10 Sonezaki, Kita-ku, Osaka 530-0057

Tel. No.: +81-6-6232-8370 (General Line)

◆Nagoya Branch

Hirokoji Center Place, 2-19-19 Nishiki, Naka-ku, Nagoya, Aichi 460-0003

Tel. No.: +81-52-220-3690 (General Line)

◆Fukuoka Branch

KDC Fukuoka Building, 5-5-13 Nakasu, Hakata-ku, Fukuoka 810-0801

Tel. No.: +81-92-272-0873 (General Line)