Silicon Valley in Transition from Global Innovation Summit

24

Silicon Valley in Transition Global Innovation Summit + Week February 19, 2015 Mark Radcliffe, DLA Piper, Silicon Valley Office [email protected] , 650-833-2266

-

Upload

mark-radcliffe -

Category

Technology

-

view

87 -

download

1

Transcript of Silicon Valley in Transition from Global Innovation Summit

Silicon Valley in Transition

Global Innovation Summit + Week

February 19, 2015

Mark Radcliffe, DLA Piper, Silicon Valley Office

[email protected], 650-833-2266

Global Platform

Largest law firm in the

world with 4,200 lawyers in

31 countries and 77 offices

throughout Asia, Europe,

the Middle East and the US

Ranked #1 among the

world’s leading global law

firms

More than 145 DLA Piper

lawyers in IP transactions

1st in Venture Capital and

Private Equity deal volume

More than 550 DLA Piper

lawyers ranked as leaders

in their fields

2

Mark Radcliffe

Background

B.S. Chemistry, magnum cum laude, University of Michigan

Harvard Law School (l1996, Distinguished Alumni)

Practicing in Silicon Valley for over 30 years

Corporate securities and intellectual property licensing

US Private Sector Co-Chair (US Department of State/METI),

US-Japan Innovation and Entrepreneurship Council

Chair, Corporate Venture Group

Chair, International Startup Group

3

Disruptive Change

Symbian market share: 60% (2007) to >10% (2011)

We too, are standing on a “burning platform,” and we must decide how we are

going to change our behaviour.

Nokia CEO Stephen Elop (2011)

4

Silicon Valley in Transition

Lower barrier to entry for new startups: 90% decrease for IT:

Lisa Gansky of Ofoto: she raised $60m in 90s but could do the same

company today for $6m

Factors

Cloud: no hardware/”rent” software

Open source software

Increase in funding sources:

Individual angels/angel groups/angel syndicates/super angels

Micro-VC

Corporations (more than 1,000 are investing)

Hedge funds/mutual funds

Decrease in financial venture capital funds from 1225 (2006) to 425 (with

many fewer venture capital funds actively investing)

5

Major Technology Trends

Speed of innovation increasing: adapt or die

Sun

Nokia

Open source/collaboration

Linux (operating system)

OpenStack Foundation (cloud)

IT Changes

Cloud

Mobile

Increase in data

Rise of “interconnected world” (Internet of Things)

6

“Software is eating the world.”

Marc Andreessen - 2012

7

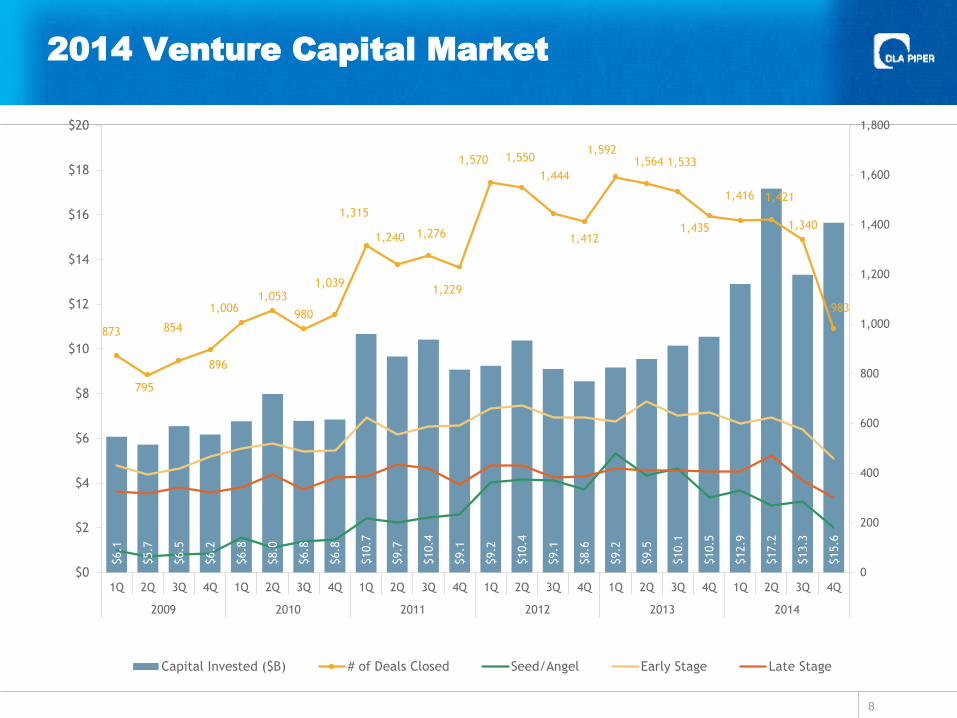

2014 Venture Capital Market

8

$6.1

$5.7

$6.5

$6.2

$6.8

$8.0

$6.8

$6.8

$10.7

$9.7

$10.4

$9.1

$9.2

$10.4

$9.1

$8.6

$9.2

$9.5

$10.1

$10.5

$12.9

$17.2

$13.3

$15.6

873

795

854

896

1,0061,053

980

1,039

1,315

1,240 1,276

1,229

1,570 1,550

1,444

1,412

1,5921,564 1,533

1,435

1,416 1,421

1,340

983

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2009 2010 2011 2012 2013 2014

Capital Invested ($B) # of Deals Closed Seed/Angel Early Stage Late Stage

2014 Deal by Stage

9

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

2012

2013

2014

Seed/Angel Early Stage Late Stage

2014 Seed/Angel Stage

10

$72

$50

$73

$156

$143

$184

$152

$211

$217

$341

$306

$274

$343

$303

$414

$349

$269

$332

$323

$296

139

102

125132

217203

223

234

362

375

370

332

480

391

420

300329 270

287

180

0

50

100

150

200

250

300

350

400

450

500

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2010 2011 2012 2013 2014

Capital Invested ($M) # of Deals Closed

2014 Early Stage

11

$2.9

$2.6

$2.9

$2.3

$3.3

$2.9

$3.5

$3.7

$3.0

$3.8

$3.0

$2.9

$3.1

$3.7

$3.5

$4.1

$4.5

$5.2

$4.8

$4.6

497

518

485490

622

554

589

590

662

674622 624 609

689

632

645

601

625

575

460

0

100

200

300

400

500

600

700

800

$0

$1

$2

$3

$4

$5

$6

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2010 2011 2012 2013 2014

Capital Invested ($B) # of Deals Closed

Angel Group Update: Halo Report Q2 2014

Highlights

Round size drops in angel-only

deals, while syndicated round

size increases

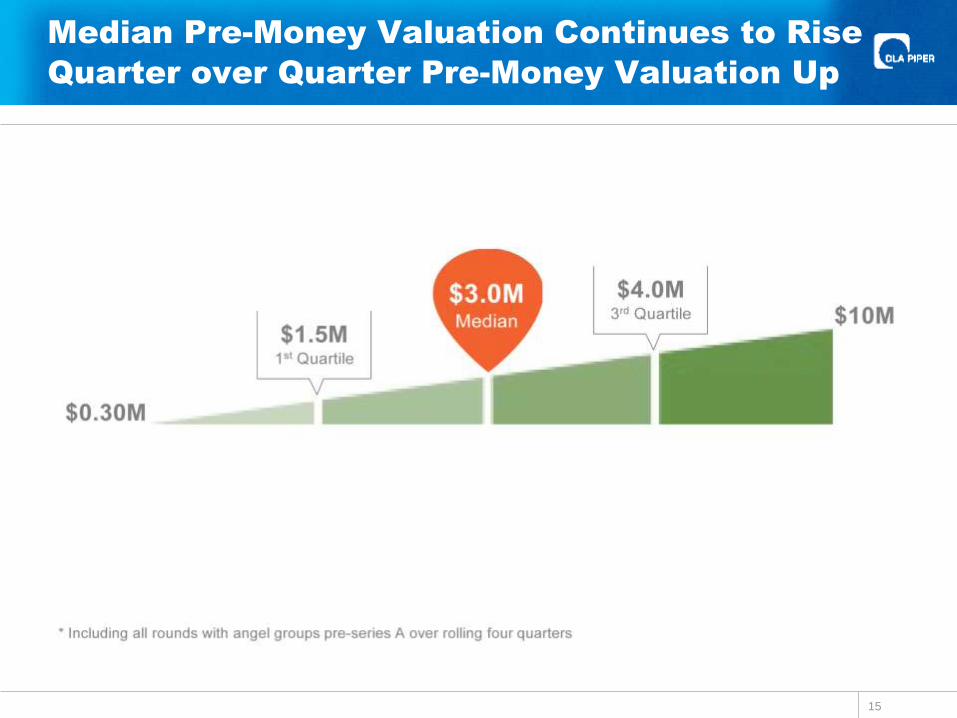

Median pre-money valuation

continues to rise, jumping to

$3.0M from $2.7M in Q1 2014

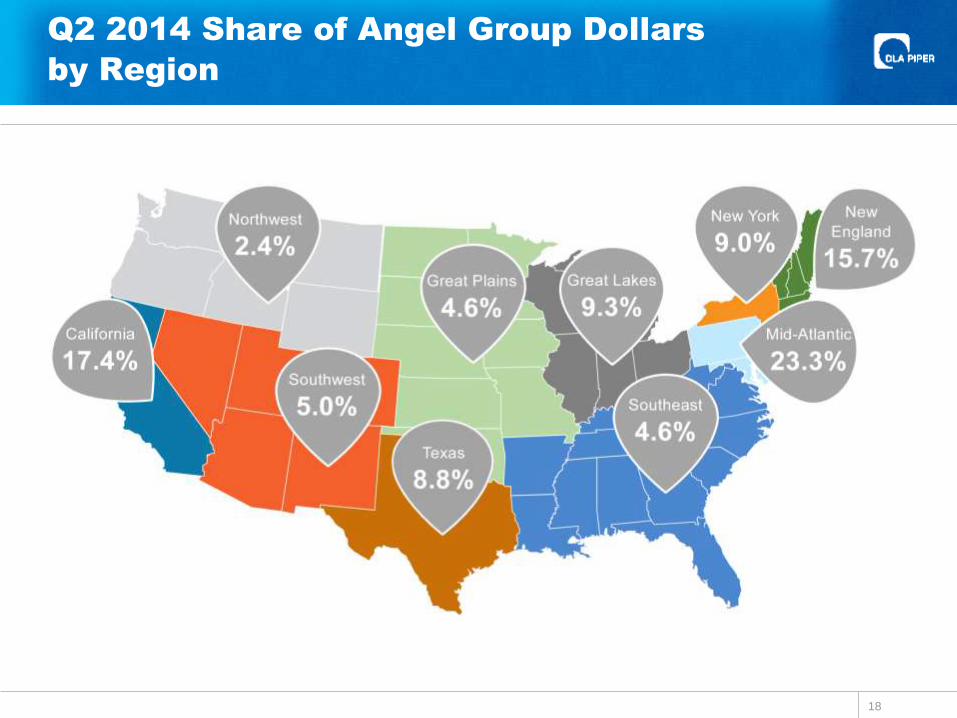

Texas breaks into top three

most active regions; Mid-

Atlantic leads in dollars

invested

Median healthcare round size

jumps by $1M, while median

Internet round size falls by $1M

Most Active Angel Groups

Total Deals Q2 2014 (Alpha

Order)

Alliance of Angels

Central Texas Angel Network

Desert Angels

Golden Seeds

Houston Angel Network

Launchpad Venture Group

Maine Angels

Tech Coast Angels

12

Median/Mean Angel Round Size Falls in

Q2 2014

13

Angels Co-Investing With Non-Angels

Leads to an Increase in Median/Mean Size

14

Median Pre-Money Valuation Continues to Rise

Quarter over Quarter Pre-Money Valuation Up

15

Q2 2014 Share of Angel Group Deals by Region

16

Texas Breaks Top 3 With the Mid-Atlantic

Region Close Behind

17

Q2 2014 Share of Angel Group Dollars

by Region

18

Healthcare & Internet Remain Stable While

Mobile Down Slightly

19

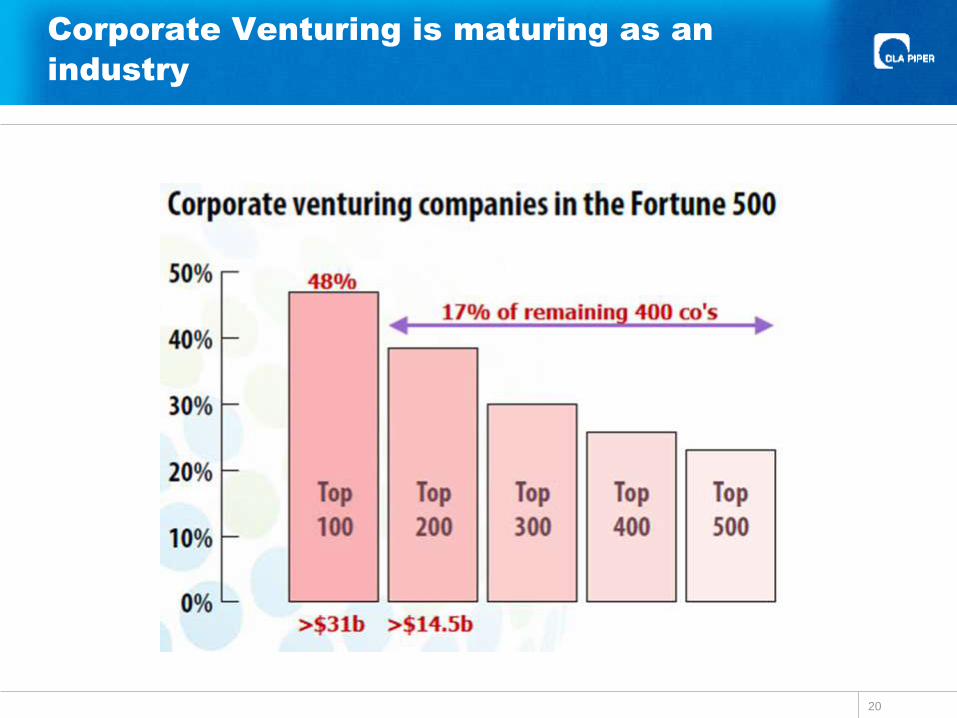

Corporate Venturing is maturing as an

industry

20

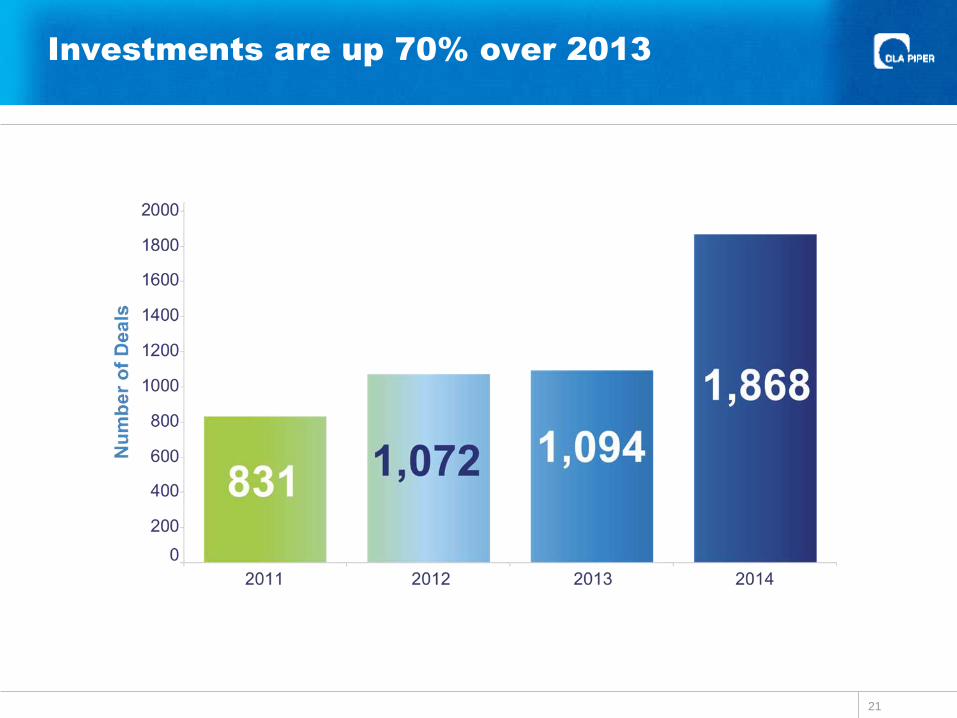

Investments are up 70% over 2013

21

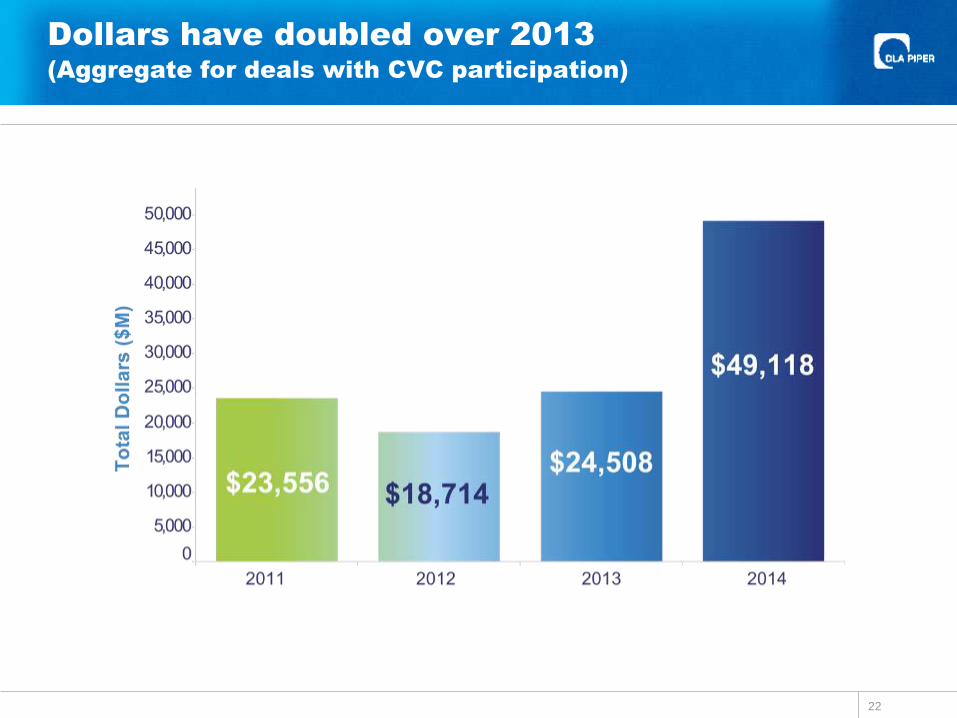

Dollars have doubled over 2013

(Aggregate for deals with CVC participation)

22

2014 Investments

Seed and Series A – D Rounds

23

Summary

IT critical in more industries

Cars: mobile computers

Smart Phones: displacing PCs and now tablets

Disruptive technology changes in IT

Innovation is accelerating in multiple industries

Startups emerging across the globe

Funding ecosystem becoming more complex

Silicon Valley retains its primary position

24