SHOPPERS & RETAILING

8

in Thailand 2021 SHOPPERS & RETAILING

Transcript of SHOPPERS & RETAILING

in Thailand 2021SHOPPERS & RETAILING

2 Shoppers & Retailing in Thailand 2021

Contents

Part 1 Introduction 3

Part 2 Executive Summary 9

Part 3 Impact of COVID-19 in 2020: Retail Sales Index 11

Part 4 Thailand at a Glance 21

Part 5 Thai Shoppers: Income and Expenditure 33

Part 6 Retail Market of Thailand: Overview 47

Part 7 Growth in Retail Channels 59

Part 8 E-Commerce in Thailand 68

About Us 74

2

Tommy

14 Shoppers & Retailing in Thailand 202114

When the state of emergency was imposed, retail sales fell sharply to minus 12.1% year-on-year in March 2020, minus 29.4% in April, and 28.2% in May. From June onwards, the decline became smaller each month, recovering to minus 0.2% year-on-year in December.

Sources: Revenue Department, Ministry of Finance, Bank of Thailand, World Health Organization.

Retail Sales Index (YoY), 2020

-2.1% -0.9%

-12.1%

-29.4% -28.2%-17.4%

-12.1%-5.6% -6.6% -6.6% -2.5% -0.2%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total Retail Sales

Numbers of Daily Confirmed Covid-19 Cases

Tommy

Tommy

37 Shoppers & Retailing in Thailand 202137

17,40318,766 19,061

20,892 21,157 21,144 21,437 21,34620,742

2011 2012 2013 2014 2015 2016 2017 2018 2019

Unit: THB

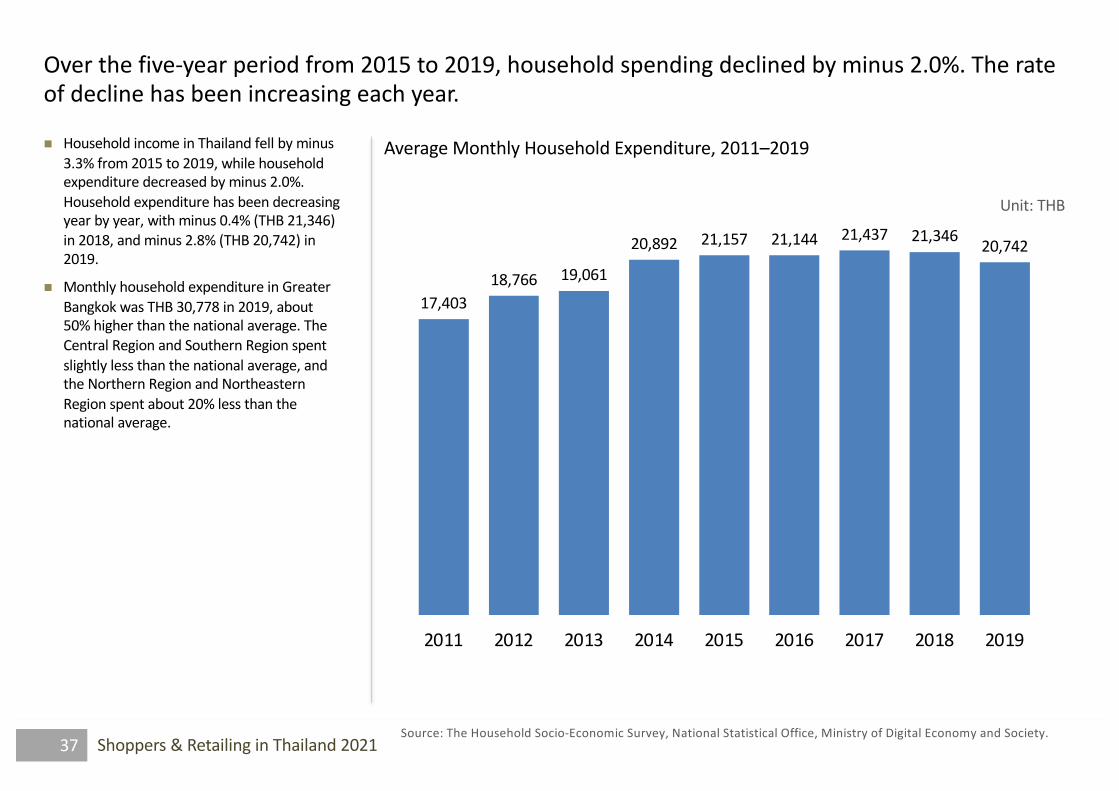

Average Monthly Household Expenditure, 2011–2019

Source: The Household Socio-Economic Survey, National Statistical Office, Ministry of Digital Economy and Society.

Over the five-year period from 2015 to 2019, household spending declined by minus 2.0%. The rate of decline has been increasing each year.

n Household income in Thailand fell by minus 3.3% from 2015 to 2019, while household expenditure decreased by minus 2.0%. Household expenditure has been decreasing year by year, with minus 0.4% (THB 21,346) in 2018, and minus 2.8% (THB 20,742) in 2019.

n Monthly household expenditure in Greater Bangkok was THB 30,778 in 2019, about 50% higher than the national average. The Central Region and Southern Region spent slightly less than the national average, and the Northern Region and Northeastern Region spent about 20% less than the national average.

Tommy

43 Shoppers & Retailing in Thailand 202143

-180

-130

-80

-30

20

70

120

-20% -10% 0% 10%

Mon

thly

Hou

seho

ld E

xpen

ditu

re G

row

th V

alue

, 20

15–2

019

(THB

)

Monthly Household Expenditure Growth Percentage, 2016–2019

CommunicationThailand

Non-ConsumptionExpenditure

Housing/Utilities/Household Equipment

Personal Care/Clothing/Footwear

Food/Beverages/Tobacco

Medical/Healthcare

Vehicle/Transportation

Religious Activities

EducationRecreation/

Entertainment

From 2015 to 2019, only three categories saw increases in spending: Non-Consumption Expenditure, Communication and Housing/Utilities/ Household Equipment.

Monthly Household Expenditure Growth (Value & Percentage), 2015–2019

Source: The 2019 Household Socio-Economic Survey Whole Kingdom, National Statistical Office, Ministry of Digital Economy and Society.

55 Shoppers & Retailing in Thailand 202155

Major Retail Groups and Store Brands in Thailand (Part 1 of 4)

Supermarket Discount Store/Supercenter/Hypermarket Convenience Store

Central Group

Department Store Category Specialist & Others

n The characteristics of the retail market in Thailand are influenced by several key multi-channel retail company groups.

n Among them, Central Group has the largest number of multi-channel operations in nearly all the mixed merchandise channels, many category specialist channels and shopping malls. In 2020, Central Group launched JD CENTRAL, an e-commerce site jointly operated with China’s e-commerce company, Jingdong Group. The following belongs to Central Group: l Supermarkets (Tops Market, Central Food

Hall)l Hypermarkets (Tops Super Store, Tops

Super Koom)l Convenience Stores (Tops Daily, Family

Mart)

Ø Family Mart became wholly owned by Central Retail in May 2020.

l Department stores (Central, Zen, Robinson)Ø The merging of Central and Robinson

was announced in September 2020l Drugstores (Matsumoto Kiyoshi)l DIY household goods (Thaiwatsadu,

homeWork, baan & BEYOND)l Discount Store/Single-Price (Just Buy)l Others (Payless Shoesource, babyshop, etc.)

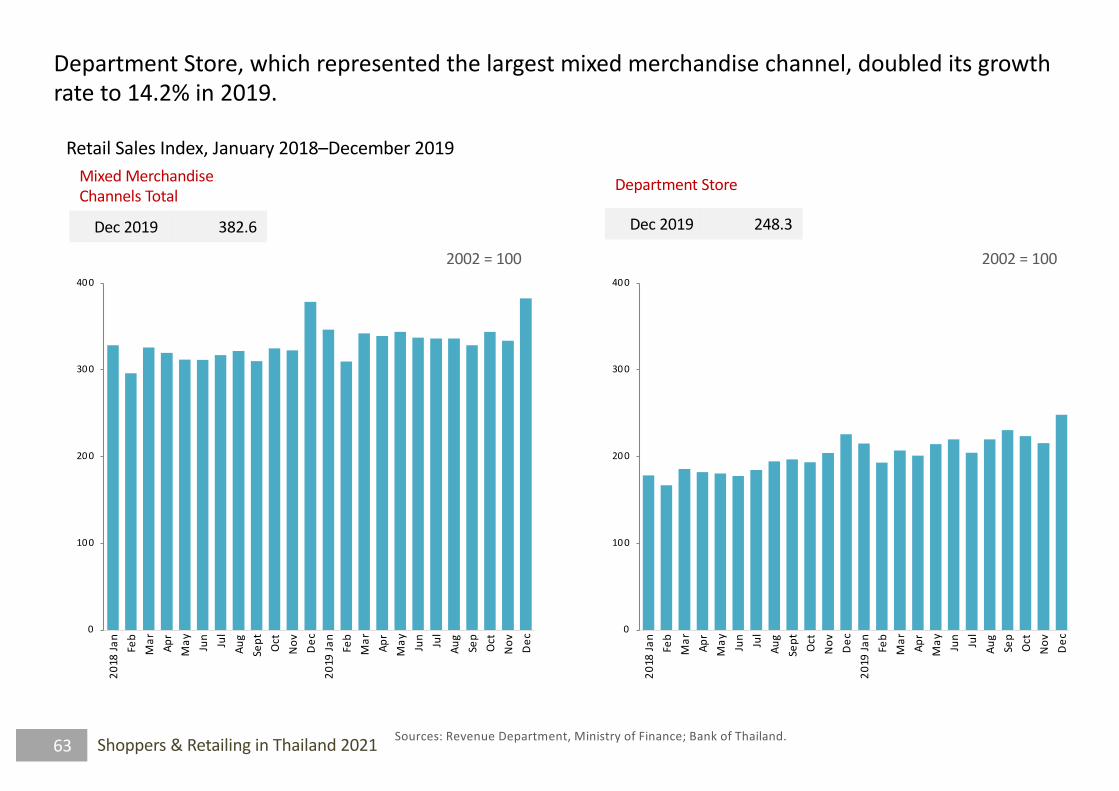

63 Shoppers & Retailing in Thailand 202163

Retail Sales Index, January 2018–December 2019

Sources: Revenue Department, Ministry of Finance; Bank of Thailand.

0

100

200

300

400

2018

Jan

Feb

Mar Ap

rM

ay Jun Jul

Aug

Sept Oc

tNo

vDe

c20

19 Ja

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

2002 = 100

Mixed Merchandise Channels Total

Dec 2019 382.6

0

100

200

300

400

2018

Jan

Feb

Mar Ap

rM

ay Jun Jul

Aug

Sept Oc

tNo

vDe

c20

19 Ja

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

2002 = 100

Department Store

Dec 2019 248.3

Department Store, which represented the largest mixed merchandise channel, doubled its growth rate to 14.2% in 2019.

73 Shoppers & Retailing in Thailand 202173

Major E-Commerce Stores in Thailand and Average Number of Website Visitors, Q4 2020

E-Commerce Store Monthly Traffic

1. Shopee

51,242,700

2. Lazada

38,539,000

3. JD Central

2,203,700

4. Central Online

2,131,500

5. Advice

1,995,000

E-Commerce Store Monthly Traffic

6. Power Buy

1,940,700

7. HomePro

1,656,700

8. JIB

1,332,500

9. Banana Store

1,114,100

10. ShopAt24

1,051,900

Source: https://ipricethailand.com/insights/mapofecommerce/en/ (Q4 2020 updated 9 February 2021).

In terms of web traffic, Shopee and Lazada soared ahead of other e-commerce sites in Thailand in Q4 2020.

n In the last quarter of 2020 (October to December), Shopee was the most accessed Thai online shopping site with an average monthly traffic of 51,242,700 visitors, followed by Lazada with 38,539,000. Central Group’s JD Central, which recently started joint operations with China’s JingdongGroup, was already the third most visited site with an average monthly traffic of 2,203,700.

n The fourth most visited site, Central Online, is the online site of Central Group’s flagship department stores, while seventh-ranked Power Buy is their online store for home appliances.

Tommy