Shipping Market Overview - Clarksons Market Overview... · Shipping Market Overview Presentation to...

30

19/05/2014 1 www.clarksons.com Shipping Market Overview Presentation to Maritime HR Forum 8 th May 2014 (Ref: A3315) May 2014 Steve Gordon, Managing Director, Clarkson Research. Presentation not for circulation outside of Maritime HR Forum attendees. www.clarksons.com 2 About us Broking Clarksons’ shipbroking services are unrivalled: for the number and calibre of our brokers; breadth of market coverage; geographical spread and depth of market intelligence; analysis and support. We aspire to be best-in-class and market leaders in all key sectors. Support Clarkson Port Services provides the highest level of support to vessel owners, operators and charterers at strategically located ports in the UK and Egypt. Offering ship’s agency services, we are also engaged in stevedoring and warehousing at UK ports and support to the Offshore industry. Financial From derivative products that have been pioneered at Clarksons to full investment banking services and tailored debt solutions, we help our clients manage risk and fund and conclude deals that would often be impossible via more traditional routes. Research Up-to-the-minute intelligence is the cornerstone of any shipping organisation and Clarksons Research Services is recognised worldwide as the market-leading provider of comprehensive and reliable maritime information.

Transcript of Shipping Market Overview - Clarksons Market Overview... · Shipping Market Overview Presentation to...

19/05/2014

1

www.clarksons.comwww.clarksons.comwww.clarksons.comwww.clarksons.com

Shipping Market Overview

Presentation to Maritime HR Forum 8th May 2014 (Ref: A3315)

May 2014

Steve Gordon, Managing Director, Clarkson Research.

Presentation not for circulation outside of Maritime HR Forum attendees.

www.clarksons.com 2

About us

BrokingClarksons’ shipbroking services are unrivalled: for the number and calibre of our brokers; breadth of market coverage; geographical spread and depth of market intelligence; analysis and support. We aspire to be best-in-class and market leaders in all key sectors.

SupportClarkson Port Services provides the highest level of support to vessel owners, operators and charterers at strategically located ports in the UK and Egypt. Offering ship’s agency services, we are also engaged in stevedoring and warehousing at UK ports and support to the Offshore industry.

FinancialFrom derivative products that have been pioneered at Clarksons to full investment banking services and tailored debt solutions, we help our clients manage risk and fund and conclude deals that would often be impossible via more traditional routes.

ResearchUp-to-the-minute intelligence is the cornerstone of any shipping organisation and Clarksons Research Services is recognised worldwide as the market-leading provider of comprehensive and reliable maritime information.

19/05/2014

2

www.clarksons.com 3

Research

Offshore and energy

The leading provider of data to the offshore industry for more than 30 years. Providing clients with the key information they need to operate their business more effectively. Market intelligence is available on more than 25,000 structures, vessels and companies and 6,000 oil and gas fields.

Shipping and trade

Market leaders in providing timely and authoritative information on all aspects of shipping. Data is available on over 100,000 vessels either in service or on order, 10,000 companies and 600 shipyards as well as extensive trade and commercial data, and over 100,000 time series.

Valuations

The world’s leading provider of valuations to the shipping industry and financial community. More than 20,000 valuations are handled annually, covering the full range of vessel types.

www.clarksons.com 4

Agenda

1.Shipping Today2.World Trade3.The World Fleet and Orderbook4.Other Issues5.Summary

January 2014

19/05/2014

3

www.clarksons.com 5

1. Shipping Today

January 2014

www.clarksons.com 6

0

10

20

30

40

50

60

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

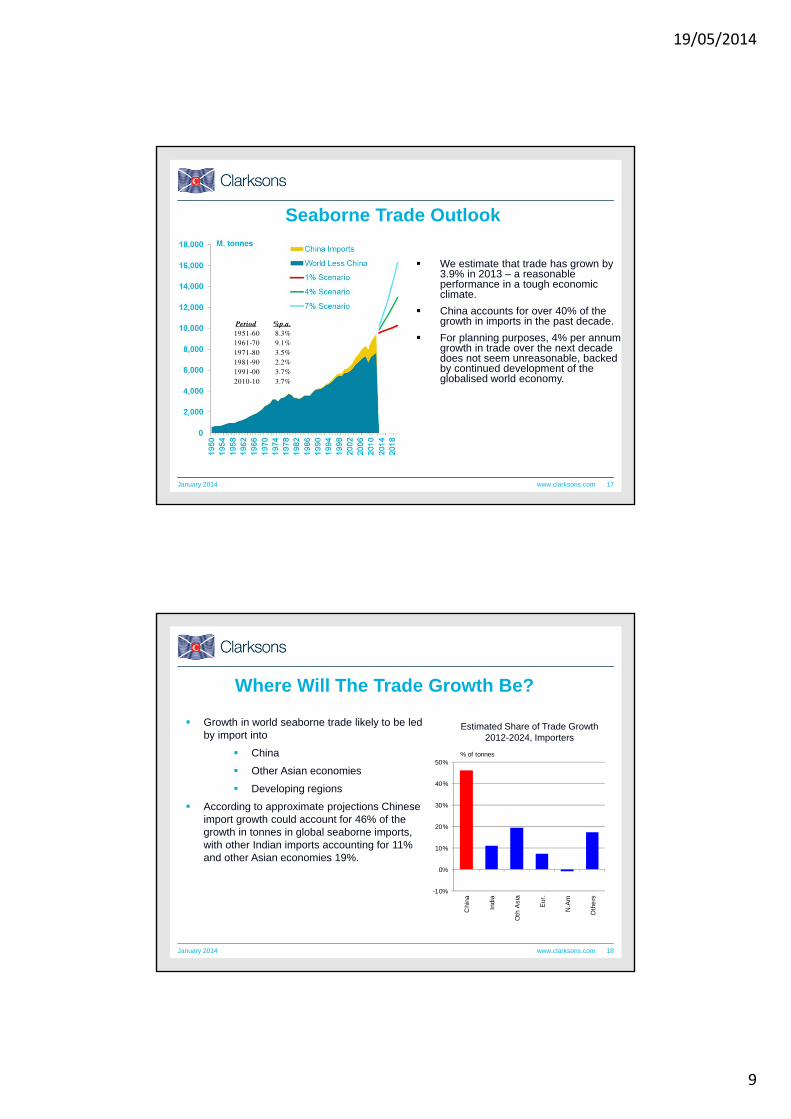

(ClarkSea Index is a weighted average of earnings by tankers, bulkers, containerships & gas carriers)

End 2004c.$40,000/day

End 2007c.$48,500/day

End 2000c.$24,000/day

Shipping Cycle 1965-2014: ClarkSea Index

$000/ day

Index Average Values

1990s: $12,021/day

2000s: $22,251/day

2010-May 2014: $11,936/day

02 May 2014$9,634/day

January 2014

19/05/2014

4

www.clarksons.com 7

0

5

10

15

20

25

30

35

40

45

50

Jan

'08

May

'08

Sep

t '0

8

Jan

'09

May

'09

Sep

t '0

9

Jan

'10

May

'10

Sep

t '1

0

Jan

'11

May

'11

Sep

'11

Jan

'12

May

'12

Sep

'12

Jan

'13

May

'13

Sep

'13

Jan

'14

Five Years of Shipping Downturn

OPEX

$000/day

2nd May 2014 - $9,634 / day but touched

$7,574 / day in February 2013

ClarkSea Index 2008-14

February 2014

1.Huge Cash Pressures & Cost Focus

2.Surplus in the Volume Markets

3.Cash is King

4.Some Sectors Have Done Better e.g. LPG

5.Ships Still Trading & Slow Steaming but Not Laid Up

6.Big Change in Ship Economics – Fuel & Regulations

7.Big change in Financial landscape

8.Recent recovery in part driven by seasonal factors but there are some encouraging signs

www.clarksons.com 8

Earnings versus OPEX

ClarkSeaIndex

OpexIndex

$/day $/day

2008 32,947 6,861

2009 11,407 6,636

2010 15,346 6,830

2011 12,466 6,976

2012 9,588 7,101

2013 10,335 7,229

2014 11,780 7,410

Source: Clarkson Research, Moore Stephens, January 2014

• The Opex index is generated using the same assumptions as the ClarkSea Index for comparison purposes.

• In February 2013, the two indexes reached their smallest differential in the downturn – just $508 per day across the 20,000 ships in the “ClarkSea fleet”.

• In May 2008, the differential was $40,633 per day and equated to $680 million dollars a day across the “ClarkSea” fleet.

May 2014

19/05/2014

5

www.clarksons.com 9

-80% -60% -40% -20% 0% 20% 40% 60% 80% 100% 120%

VLCCSuezmax

AframaxClean Products

CapesizePanamax

HandymaxHandy

Container 3,500 teuContainer 1,700 teu

Offshore - JackupsOffshore - Floaters

Offshore - PSV

LPGLNG

% deviation from 7 year average

Cycle Position May 2014

This chart shows average 1 year TC rate for each ship type, compared to

the average earnings during the last 7

years.

Crosses – x - mark the position in the market cycle one

year ago.

Tankers still tough but Products

better

Earnings still low, but notably less bad

than a year ago

Gas and Offshore positive,

particularly LPG

Improvements in Q4 2013 but markets softening again

x

x

x

x

x

x

x

x

x

x

x

x

x

x

x

www.clarksons.com 10

Source: Compiled from several sources including CRSL, Fearnleys.

Newbuilding Prices – Bottomed Out & Firming

April 2014

19/05/2014

6

www.clarksons.com 11

0

10

20

30

40

50

60

70

80

90

100

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Aframax Tanker 5 Year Old

Panamax Bulk Carrier 5 Year Old

Price $ Million

Panamax bulker peaked at around $90m in 2007/08

Secondhand Price Development

January 2014

Panamax bulker declined 72% from market peak.

Panamax bulker has increased 37% from recent trough.

www.clarksons.com 12

S&P Activity Has Increased

19/05/2014

7

www.clarksons.com 13

2. World Trade

January 2014

www.clarksons.com 14

Seaborne Trade Growth & The World Economy

Historically, world seaborne trade expansion has generally been relatively well correlated to global economic growth.

Sea trade cycles generally follow cycles in world GDP – but not precisely. 2014 – 3.6% GDP growth and 4.2% growth in trade?

-8.0%

-4.0%

0.0%

4.0%

8.0%

12.0%

199

61

997

199

81

999

200

02

001

200

22

003

200

42

005

200

62

007

200

82

009

201

02

011

201

22

013

201

4 (

f)2

015

(f)

Seaborne Trade GrowthWorld GDP Growth

April 2014

0

2

4

6

8

10

12

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

bt tradetonnes pp

Source: Clarkson Research Services

Global Trade per Capita

Trade per Capita (LHS)

Global Seaborne Trade (RHS)

Milestone 12014: Trade reaches 10bt

Milestone 22002: Trade passes

1t per person

19/05/2014

8

www.clarksons.com 15

Two Speed World ?Index

1993=100

IP : Atlantic Economies

IP : Pacific Economies

April 2014

www.clarksons.com 16

World Seaborne Trade Growth in world seaborne trade in

last decade led by

Iron Ore

Containers

LNG

Coal

Vehicles

Average CAGR of 4.1%.

In 2013 growth of 3.9% - a good performance given general economic conditions.

Expected growth of 4.2% in 2014.

Some upside if business cycle improves.

2000-13 Trade Growth by Commodity, CAGR %

January 2014

4.1% average

19/05/2014

9

www.clarksons.com 17

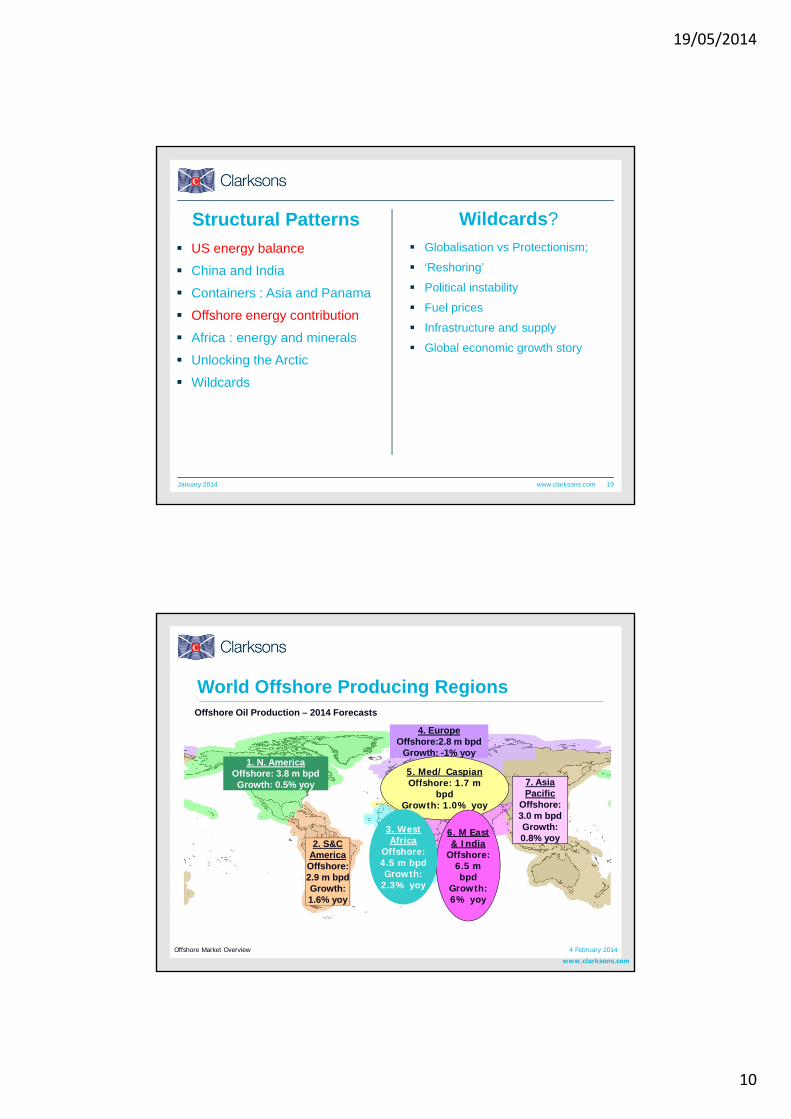

Seaborne Trade Outlook

We estimate that trade has grown by 3.9% in 2013 – a reasonable performance in a tough economic climate.

China accounts for over 40% of the growth in imports in the past decade.

For planning purposes, 4% per annum growth in trade over the next decade does not seem unreasonable, backed by continued development of the globalised world economy.

January 2014

Period %p.a.1951-60 8.3%1961-70 9.1%1971-80 3.5%1981-90 2.2%1991-00 3.7%2010-10 3.7%

www.clarksons.com 18

Where Will The Trade Growth Be?

Estimated Share of Trade Growth 2012-2024, Importers

Growth in world seaborne trade likely to be led by import into

China

Other Asian economies

Developing regions

According to approximate projections Chinese import growth could account for 46% of the growth in tonnes in global seaborne imports, with other Indian imports accounting for 11% and other Asian economies 19%.

-10%

0%

10%

20%

30%

40%

50%

Chi

na

Indi

a

Oth

Asi

a

Eur

.

N.A

m

Oth

ers

% of tonnes

January 2014

19/05/2014

10

www.clarksons.com 19

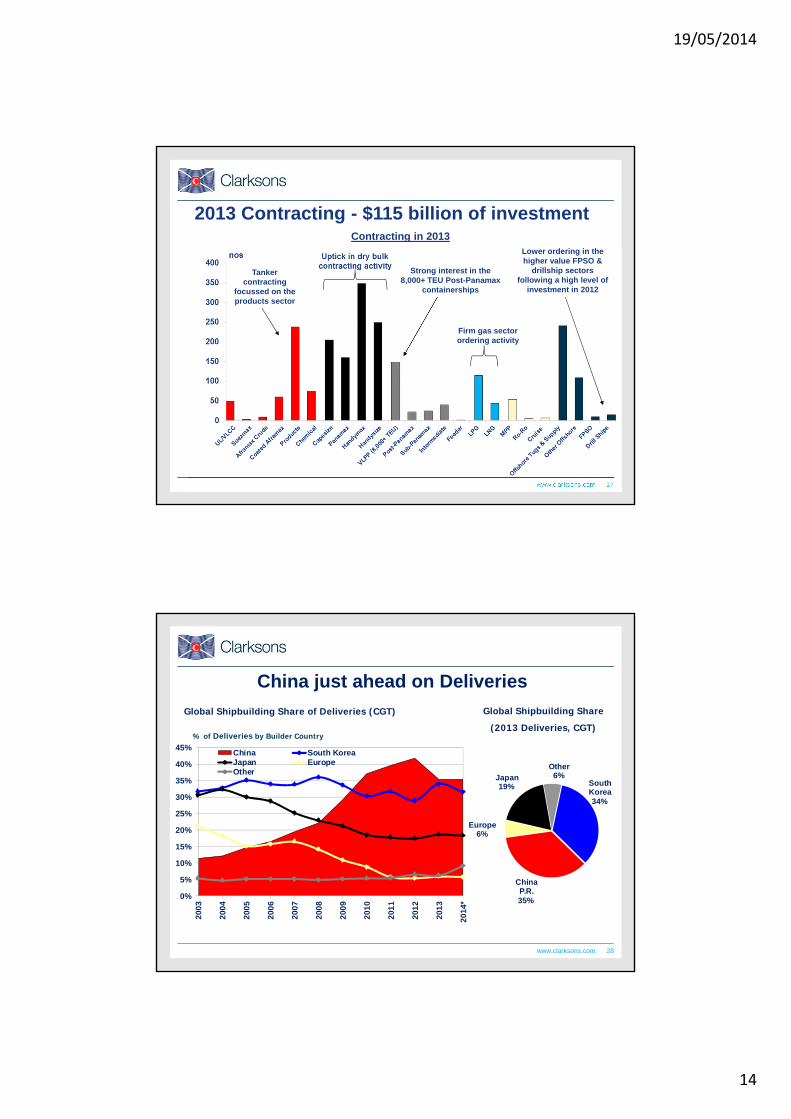

Structural Patterns

US energy balance

China and India

Containers : Asia and Panama

Offshore energy contribution

Africa : energy and minerals

Unlocking the Arctic

Wildcards

Globalisation vs Protectionism;

‘Reshoring’

Political instability

Fuel prices

Infrastructure and supply

Global economic growth story

Wildcards?

January 2014

www.clarksons.com

World Offshore Producing Regions

Offshore Market Overview 4 February 2014

1. N. AmericaOffshore: 3.8 m bpdGrowth: 0.5% yoy

2. S&C America

Offshore:2.9 m bpdGrowth: 1.6% yoy

4. EuropeOffshore:2.8 m bpd

Growth: -1% yoy

7. Asia Pacific

Offshore: 3.0 m bpdGrowth: 0.8% yoy

5. Med/ CaspianOffshore: 1.7 m

bpdGrowth: 1.0% yoy

6. M East & India

Offshore: 6.5 m bpd

Growth: 6% yoy

3. West Africa

Offshore: 4.5 m bpdGrowth:

2.3% yoy

Offshore Oil Production – 2014 Forecasts

19/05/2014

11

Oil & Gas ProductionLong-Term Oil Production Long-Term Gas Production

May 2014

Projected offshore oil production growth 2013-23 :World 2.4% paNorth America -2.5% paLatin America 5.2% pa

Projected offshore gas production growth 2013-23 :World 4.3% paNorth America 1.3% paLatin America 5.4% pa

www.clarksons.com 22

3. The World Fleet and Orderbook

January 2014

19/05/2014

12

www.clarksons.com 23

The World Fleet: GT

1. Long-term: 1986-2013 CAGR: 3.9%.

2. Medium-term: 1996-2013 CAGR: 5.0%.

• Largest growth in containerships (CAGR of 9.0%) and gas carriers (7.4%).

3. Short-term: 2006-2013 CAGR: 6.7%.

• In 2010, the fleet increased by 8.7%, the fastest rate of growth in recent history. In 2013, the fleet has grown by a further 3.8%, indicating a marginal slow-down in the rate of deliveries.

• At the start of January 2014, the fleet totalled 1,133 million GT.

The Size of the World Fleet (GT)

Numbers

% Share

Tonnage

(GT)%

Share

Growth 2009-12

(GT) 2014

(f)

O/B as % Fleet

Crude and Products Tankers

9,243 10% 265.0 23% 13% 1% 13%

Bulkers 10,046 11% 403.00 36% 48% 4% 21%

Containerships 5,087 6% 188.0 17% 24% 5% 22%

MPP 3,237 4% 21.0 2% 6% 0% 7%

Ro Ro 1,315 1% 15.0 1% -2% -2% 7%

Other Dry 15,837 23% 28.2 6% -3% 0% 2%Chemical and Specialised

4,034 2% 26.93 2% 12% 1% 8%

LPG 1,255 1% 14.0 1% 7% 6% 34%

LNG 387 0% 38.5 3% 13% 9% 30%

PCC 757 1% 35.1 3% 20% 3% 13%

Reefer 1,439 2% 4.9 0% -28% -7% 0%

Offshore 10,199 12% 49.8 4% 25% 5% 23%

Dredgers 2,186 2% 4.5 0% 20% 4% 4%

Tugs 16,297 18% 4.5 0% 16% 3% 2%

Cruise 360 0% 17.7 2% 15% 4% 17%

Ferries 6,034 7% 15.8 1% -2% -2% 3%

Other 617 1% 1.0 0% 1% 3% 12%

Merchant Fleet

1. 88,000 vessels over 100 GT

2. 1,138 million GT

3. $944 billion value

April 2014

19/05/2014

13

Contracting, Deliveries & DemolitionsMillion GT

April 2014

Orderbook As & % Of Fleet

Orderbook % Fleet By (Dwt), Start Year

Orderbook % Fleet

Orderbook has increased – up to

17% in March 2014 from a low of 14.8%

February 2014

O/B as at January 2014 was 284m

dwt $ 292bn

19/05/2014

14

www.clarksons.com 27

2013 Contracting - $115 billion of investmentContracting in 2013

Tanker contracting

focussed on the products sector

Strong interest in the 8,000+ TEU Post-Panamax

containerships

Firm gas sector ordering activity

Lower ordering in the higher value FPSO &

drillship sectors following a high level of

investment in 2012

www.clarksons.com 28

China just ahead on Deliveries

Global Shipbuilding Share of Deliveries (CGT)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

*

China South KoreaJapan EuropeOther

South Korea34%

China P.R.35%

Europe6%

Japan19%

Other6%

Global Shipbuilding Share

(2013 Deliveries, CGT)% of Deliveries by Builder Country

19/05/2014

15

www.clarksons.com 29

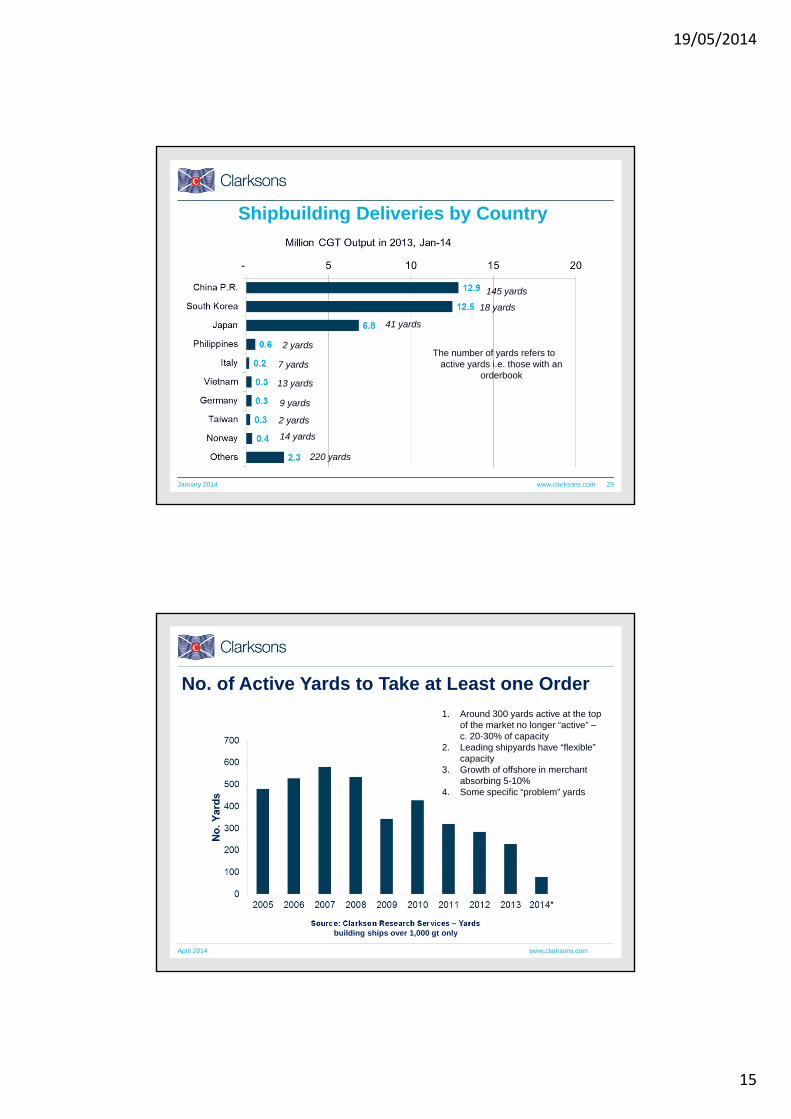

Shipbuilding Deliveries by Country

145 yards

18 yards

41 yards

2 yards

7 yards

13 yards

9 yards

2 yards

14 yards

220 yards

The number of yards refers to active yards i.e. those with an

orderbook

January 2014

www.clarksons.com

No. of Active Yards to Take at Least one Order

April 2014

Source: Clarkson Research Services – Yards building ships over 1,000 gt only

1. Around 300 yards active at the top of the market no longer “active” –c. 20-30% of capacity

2. Leading shipyards have “flexible” capacity

3. Growth of offshore in merchant absorbing 5-10%

4. Some specific “problem” yards

19/05/2014

16

www.clarksons.com

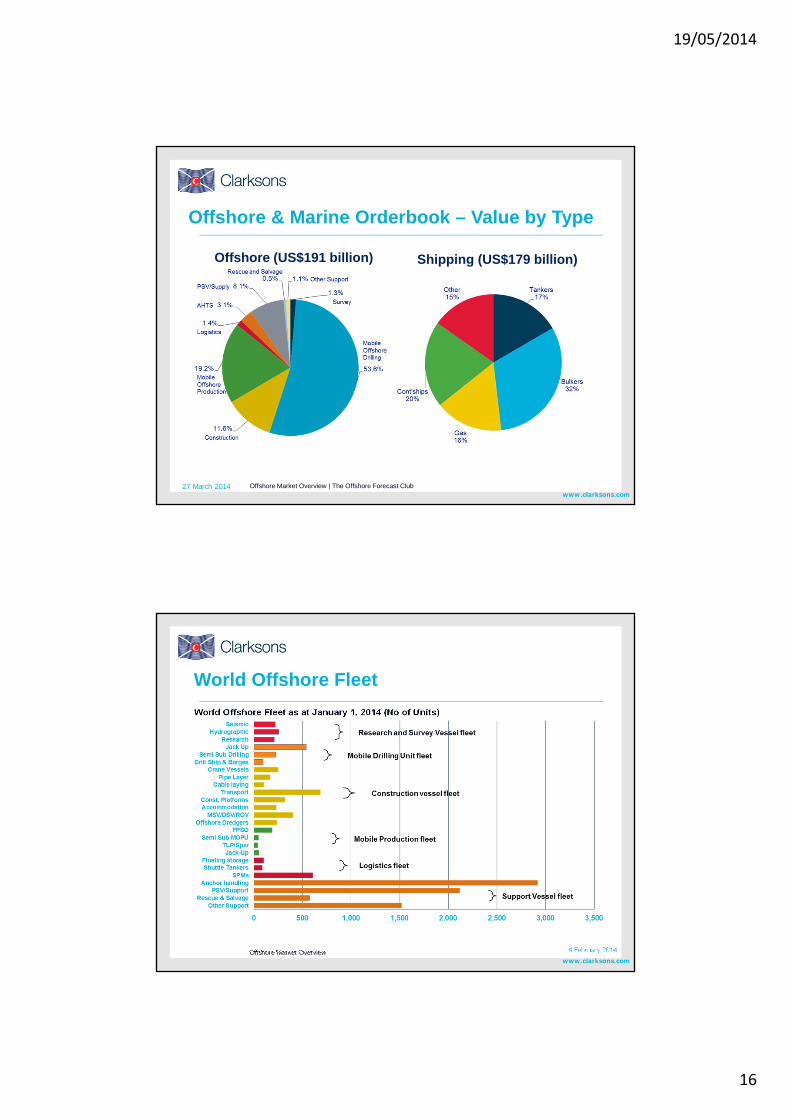

Offshore & Marine Orderbook – Value by Type

Offshore (US$191 billion)

27 March 2014 Offshore Market Overview | The Offshore Forecast Club

Shipping (US$179 billion)

www.clarksons.com

World Offshore Fleet

World Offshore Fleet as at January 1, 2014 (No of Units)

Offshore Market Overview 4 February 2014

19/05/2014

17

www.clarksons.com

Mobile Offshore Age Profile

www.clarksons.com 34

Age Profile – 8% of fleet above 25 years

0

10

20

30

40

50

60

70

80

90

100

110

1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2015

Mill

ion

GT

De

live

rie

s

Orderbook

Deliveries

Note: Owing to slippage and cancellation, not everything on

order as of 1st Jan-14 will deliver into the fleet.

Relatively few vessels built in the 1980s so limited replacement requirement

January 2014

19/05/2014

18

www.clarksons.com 35

Model makes allowance for vessel productivity trends.

Vessel speed estimates focus on the key volume sectors.

Less clear picture in the more industrial/niche sectors.

It appears that compared to pre-recession standard speeds, current average speeds for bulkers and tankers are around 2.0 knots down and containerships around c.4.0 knots down.

Compared to six months ago we have adjusted 2013 bulker speeds down by 0.5 knots and containership speeds down by 0.25 knots.

Vessel requirement projections assume trending out of average service speeds for containerships at around current speed levels, with averages for tankers and bulkers trending back to around 2010/11 levels in the long-term.

Vessel Productivity TrendsVessel Speed Indices

www.clarksons.com 36

0%

2%

4%

6%

8%

10%

12%

0

200

400

600

800

1,000

1,200

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Fleet, end year

Fleet Growth % (RHS)

World Fleet Growth Development

Million GT

1. Fleet growth peaked at c. 9% in 2010

2. In numeric terms growth is ½ to a third of tonnage growth

Projected deliveries based on current orderbook.

By 2023 our forecasts

suggest the fleet will top 1.5 billion GT

Shipbuilding production down 20% in 2013 in dwtand 2012 a record demolition year.

19/05/2014

19

www.clarksons.com 37

Estimated World Cargo Fleet Supply-Demand Growth

Supply growth projected to move back below demand growth

Challenge : Surplus Capacity

May 2014

www.clarksons.com

Newbuild Investment Forecast

Average Annual Investment $billion

Including Merchant & Offshore investment, forecasts suggest a trillion US dollars of newbuild investment needed 2014 – 2020!

19/05/2014

20

www.clarksons.com 39

4. Other Issues

January 2014

www.clarksons.com 40

Regional Ownership – Europe v Asia• During the market boom, European ownership

grew strongly and maintained market share with around 45% of global fleet by GT.

• There has been a long term trend towards Asia/Pacific ownership which topped 40% in 2013.

• Greece and Japan are the two biggest fleets, with the Greek fleet overtaking the Japanese fleet in 2013. China has overtaken Germany to take third position and the fleet is growing rapidly. German fleet declined in 2013.

• In the past five years, Brazil, China, Turkey, South Korea and Indonesian fleets have grown the most in percentage terms.

• 70% of the world is in Open Registries compared to 30% in the 1980s,

Asian Owners Growing Market Share

19/05/2014

21

www.clarksons.com 41

The World Fleet: By Owner Nationality

0 50 100 150 200 250 300 350 400

Others

Denmark

Italy

Singapore

Norway

United States

South Korea

Germany

China P. R.

Japan

Greece

January 2014

Chinese owned fleet: up 7.5% in 2013

German owned fleet: down 2.4% in 2013

www.clarksons.com 42

Regional Ownership – Top Five Nations• The Greek fleet grew by 8.4% in 2013, following

on from growth of 5.8% in 2012.

• The Japanese fleet increased by 2.4% in 2013, the lowest level of annual growth since 2009. Japanese owners were net sellers in 2013.

• China’s fleet has grown by 92.4m GT since the start of 1996, increasing by 24.4% in 2009 and 25.5% in 2010. Whilst the rate of growth was much lower at 6.9% in 2013, this was still relatively strong globally.

• Owners from the top five nations control over 50% of global capacity in GT terms.

Top Nations

19/05/2014

22

www.clarksons.com

Three European “Heavyweights”

Wet & Dry

Greek Fleet

Bulkers

Gas

Norwegian Fleet

Specialised

German Fleet

Containerships

www.clarksons.com 44

World Fleet by Company Size

Company SizeNumber of Companies

Number of vessels

m.GT% of fleet

(no. of vessels)% of fleet

(GT)Ships per Company

Small (1-5) 5,577 9,818 167.0 25% 15% 1.8

Small (6-10) 999 5,878 124.5 15% 11% 5.9

Medium (11-20) 657 7,405 192.0 19% 17% 11.3

Large (21-50) 373 8,326 300.3 21% 27% 22.3

Very Large (51-100) 101 5,196 183.7 13% 17% 51.4

XXL (100+) 22 2,899 141.2 7% 13% 131.8

Total 7,729 39,522 1108.7 5.1

*Based on Beneficial Owner, excludes unknown owners

For vessels >2,000 GT

19/05/2014

23

www.clarksons.com 45

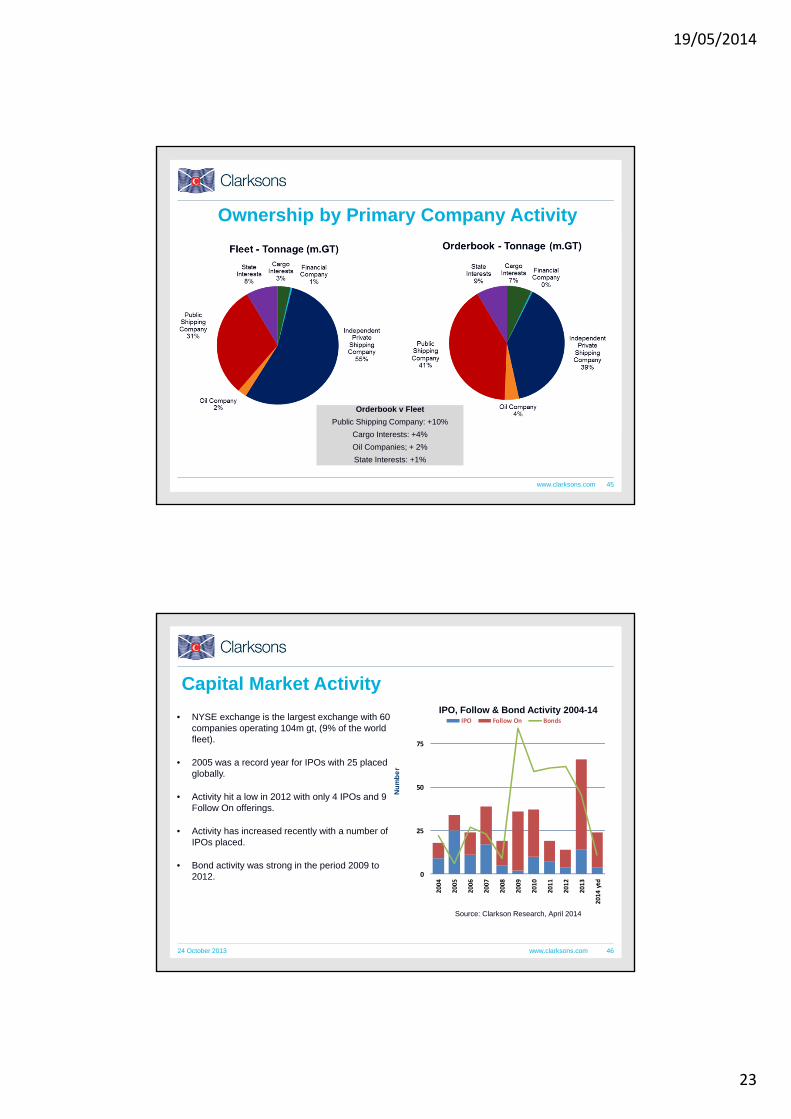

Ownership by Primary Company Activity

Orderbook v Fleet

Public Shipping Company: +10%

Cargo Interests: +4%

Oil Companies; + 2%

State Interests: +1%

www.clarksons.com 46

0

25

50

75

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

ytd

Nu

mb

er

IPO Follow On Bonds

IPO, Follow & Bond Activity 2004-14• NYSE exchange is the largest exchange with 60

companies operating 104m gt, (9% of the world fleet).

• 2005 was a record year for IPOs with 25 placed globally.

• Activity hit a low in 2012 with only 4 IPOs and 9 Follow On offerings.

• Activity has increased recently with a number of IPOs placed.

• Bond activity was strong in the period 2009 to 2012.

Capital Market Activity

24 October 2013

Source: Clarkson Research, April 2014

19/05/2014

24

www.clarksons.com 4726 March 2014 Shipbuilding Forecast Club

Number of Private Equity Deals

Capital Markets & Private EquityNumber of Maritime IPOs and Follow-Ons

www.clarksons.com 48

0

100

200

300

400

500

600

700

800

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Rising Fuel Costs Turning Shipping Economics On Its Head

Bunker Prices

Bunker prices take off In early 2005

Bunker $/tonne

Bunker price below $150/tonne

Bunkers $700/tonne

April 2014

19/05/2014

25

www.clarksons.com 49

0

5,000

10,000

15,000

20,000

25,000

30,000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Fuel Economics $/day

MR 1 Year Timecharter Rate $/day

MR Bunker Cost $/day

January 2014

1. Consumption improvements stabilising.

2. Monitoring very important.

3. Micro Management

4. Cost Control

www.clarksons.com 50

Environmental Legislation: Timeline

* Draft amendments delaying implementation to 2021 will be considered, with a view to adoption, at the MEPC 66 in 2014.** Subject to review into availability of low sulphur fuel, with option to delay implementation to 2025.

19/05/2014

26

www.clarksons.com 51

Environmental Issues: OverviewIssue Regulation Overview Latest Position

Vessel Design/ Efficient

Technology

MARPOL Annex VI - Energy Efficiency Design Index (EEDI)

Economic factors: High Bunker Prices

Low Vessel Earnings

Energy-efficiency and regulatory concerns have seen a number of developments in vessel design and

technology in recent years. These include hull, propeller, rudder and engine improvements.

E.g. Ulstein X-Bow, Becker Mewis Duct, rudder bulb, Kappel Propeller, bulbuous bows, diesel-electric engines, Waste Heat Recycling System,

Mitsubishi Air Lubrication System.

Emission Control Areas (ECAs)

MARPOL Annex VI "Regulations for the Prevention of Air Pollution from

Ships"

Vessels operating within ECAs are subject to stricter emission (SOx and NOx) limits

Current ECAs: Baltic Sea (SOx, 2006), North Sea (SOx, 2008), North American Sea (SOx, NOx and PM, 2012), US Caribbean Sea (SOx,

NOx and PM, 2014)

NOx MARPOL Annex VI NOx emission limits are set in three tiers for diesel

engines depending on the engine maximum operating speed and year of build

Tier I - 2008, Global limit for ships built 2000 – 2011

Tier II -2011, Global limit for ships built > 2010

Tier III – 2016*, ECA limit for ships built > 2015 (Tier II outside ECAs)

SOX and Particulate

Matters (PM)MARPOL Annex VI

Caps on the sulphur content of fuel oil to control SOx

emissions and, indirectly, PM emissions Sulphur Limit in Fuel (% m/m) Inside ECAs - 1.0% (0.1% in 2015)

Global - 4.5% trimmed to 3.5% with effect in 2012 (0.5% in 2020**)

CO2 MARPOL Annex VI

Introduction of an EEDI for newbuilds > 400 GT, with an aim to reduce a vessel's CO2 emissions per capacity

mile, and a SEEMP for existing vessels, so as to improve operational efficiency

EEDI for newbuilds & SEEMP for existing vessels mandatory - 2013 Reduction of EEDI reference line in three stages (2015, 2020, 2025)

Ballast WaterInternational Convention for the

Control and Management of Ships' Ballast Water and Sediments

Aims to prevent the transfer of harmful aquatic organisms and pathogens through the control and management of ships´ ballast water and sediments

Adopted by IMO in 2004, the convention will enter into force 24 months after the date on which 15 states (40% of global GT) have ratified it.

Currently 38 signatories (30.6% of global GT)

Inert GasSOLAS "International Convention

for the Safety of Life at Sea"

Tankers >20,000 dwt are required to protect cargo tanks by a fixed inert gas system in compliance with the IMO's

Fire Safety Systems Code

Effective as of 1974. Draft amendments, which will lower the dwtrequirement to 8,000 dwt for newbuilds, have been discussed

OilSTS Plan Ship-to-Ship transfer plan

New chapter and clearer definition of tanks (regulation 1) entered into force January 1, 2011

Heavy Grade Oil Prohibition of heavy grade oil in the Antarctic Sea. Effective as of August 1, 2011

Ship RecyclingThe Hong Kong Convention for the Safe and Environmentally Sound

Recycling of Ships

Once ratified, shipowners will need: an inventory of hazardous materials, a ship recycling plan, permission from the flag state to to conduct a final survey and an

international ready for recycling certificate

The convention will enter into force 24 months after the date on which 15 states (40% of global GT) have ratified it. Norway is currently the

only signatory (1.5% of global GT)

* draft amendments delaying implementation to 2021 will be considered, with a view to adoption, at the MEPC 66 in 2014 ** subject to review into availability of low sulphur fuel due to be completed in 2018, with option to delay implementation to 2025

www.clarksons.com 52

Emission Control Areas (ECAs)

North SeaSOx

Baltic SeaSOx

North AmericaSOx, NOx and PM

US Caribbean SeaSOx, NOx and PM

19/05/2014

27

www.clarksons.com 53

Global Crewing RequirementsAverage

CrewTotal Crew

Example Crew

Oil Tankers 18 120,705 VLCC ‐ 21

Bulkers 21 209,158 Capesize‐ 20

Container 19 98,933 Handy – 19

LPG 16 19,997 VLGC – 21

LNG 27 10,567 LNG – 26

PCC & Ro Ro 20 32,366 6,000 cars – 20

Passenger 164 245,260Large Cruise

1,246

Offshore 14 148,596

World Fleet 21 1.2 million

Source: Clarkson Research / International Labour Organization, January 2014

• Across the global fleet above 2,000gt (50,000 ships), the global crewing requirements are approximately 1.2 million.

• In numeric terms the global fleet is growing at around at approximately one third to a half of the growth in tonnage terms due to upsizing.

• This suggests the rate of growth in crew requirements is slowing

www.clarksons.com

Shipping Industry OPEX – $90 billion a year

Shipping OPEX (USD 90 billion per year)

• Across the global cargo fleet of 50,000 vessels, total annual OPEX is approximately $90 billion per year.

• $37.4 billion is crew costs followed by $9 billion in management fees

Source: Clarkson Research, Moore Stephens, May 2014

19/05/2014

28

www.clarksons.com

Vessel Earnings, OPEX and Wages 2008-2013

• Wage data for UK, Greece, Norway and Germany from OECD – https://stats.oecd.org – basis 2012 US$ Ex Rates, 2012 Prices.• Wage data for China and Singapore from Trading Economics – www.tradingeconomics.com – annual wage series.• Clarksea Index data is the annual average for each year from 2008-2013, indexed to 2008.

www.clarksons.com 56

5. Summary

January 2014

19/05/2014

29

www.clarksons.com 57

Summary• In 2013 we were at the bottom of the cycle and while market conditions are still challenging there are a few

encouraging signs. Some of the niche sectors have been better positioned – Offshore, Gas, Chemicals, Products. The year ended with some better markets - in part driven by seasonal demand.

• Following the demand shock in 2009, trade has recovered well and we estimate 3.9% growth in full year 2013. In 2014 we forecast trade will top 10 billion tonnes for the first time and there is upside on 2013 growth if the business cycle moves forward. 4% is a reasonable base case for the future assuming globalisation but watch out for “wildcards”. Offshore activity has been growing strongly but recent oil major “push back” on cost.

• Fleet growth is slowing, from 8% in 2011 to 5% in 2012. We recorded growth of 3.8% in 2013 - this was 1% lower than our forecast in December 2012 due to slower output at Chinese yards. Our forecast for 2014 and 2015 is region 3.6% but keep an eye on increased ordering and speed.

• Despite the difficult spot market conditions, there was a significant increase in newbuilding contracting and sale and purchase activity during 2013. Financing remains difficult for smaller owners and has limited investment but availability improving for “top tier” and Private Equity & Capital Markets are important.

• Some consolidation trends and growth of public listed fleets. Asian owners growing market share with double the fleet growth of Europeans in 2013. Greeks and Japanese the largest owners but China has surged past Germany. Norwegian’s, Greeks and Chinese have topped investment charts in recent years.

• Fuel economics has had a major impact on investment decisions and monitoring now important – large owners able to micro manage and have an advantage. Regulation a large and growing issue but decisions are difficult.

May 2014

www.clarksons.com 58

Contact

Stephen Gordon or James Coldwell

Clarkson Research Services Ltd.

Tel: + 44 (0)207 334 3439

Email: [email protected]

Trial Shipping Intelligence Network (SIN) at: www.clarksons.net

Trial World Fleet Register (WFR) at: www.clarksons.net/wfr

For more information on our product range, please visit: www.crsl.com

January 2014

19/05/2014

30

www.clarksons.com 59

Disclaimer

January 2014

The information supplied herewith is believed to be correct but the accuracy thereof is not guaranteed and the Company and its employees cannot accept liability for loss suffered in consequence of reliance on the information provided. Provision of this data does not obviate the need to make further appropriate enquiries and inspections.

The information is for the use of the recipient only and is not to be used in any document for the purposes of raising finance without the written permission of Clarkson Research Services Ltd.

The statistical and graphical information contained under the heading is drawn from the Clarkson Research Services Limited ("CRSL") database and other sources. CRSL has advised that: (i) some information in CRSL's database is

derived from estimates or subjective judgments; and (ii) the information in the databases of other maritime data collection agencies may differ from the information in CRSL's database; and (iii) whilst CRSL has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data

compilation is subject to limited audit and validation procedures and may accordingly contain errors; and (iv) CRSL, its agents, officers and employees do not accept liability for any loss suffered in consequence of reliance on such information or in any other manner; and (v) the provision of such information does not obviate any need to make

appropriate further enquiries; (vi) the provision of such information is not an endorsement of any commercial policies and/or any conclusions by CRSL; and (vii) shipping is a variable and cyclical business and any forecasting

concerning it cannot be very accurate.