SHAREHOLDER'S GUIDE - total.com · the shareholder's tax return is the gross interim dividend...

24

2017 Issue | 1 2017 Issue SHAREHOLDER'S GUIDE

Transcript of SHAREHOLDER'S GUIDE - total.com · the shareholder's tax return is the gross interim dividend...

2017 Issue | 1

2017 Issue

SHAREHOLDER'S GUIDE

2 | 2017 Issue

ContentsPage 3

Foreword from the Senior Vice President, Investor Relations

Page 4

The Total sharePage 5

Shareholding structurePage 6 - 7

Our dividend policyPage 8 - 9

Types of shareholdingPage 10

Stock exchange orders and shareholder rights

Page 11 - 12

Taxation on capital gains for shares not in a PEA

Page 13 - 14 - 15

Taxation on dividends for shares not in a PEA

Page 16

Shares held in a PEA (French equity saving plan) and their taxation

Page 17 - 18

Gifting sharesPage 19

Annual Shareholders' meetingPage 20 - 21 - 22

Relations with individual shareholders

2017 Issue | 3

Dear Shareholders,

We are pleased to bring you the 2017 issue of our Shareholders' Guide, designed to inform you of your rights and responsibilities as an investor.

In this new issue, we added details on taxation for tax residents outside of France as well as for shares held in a PEA (French equity savings plan).

The Guide also provides information on the types of shareholding and how to transfer or gift shares.

Within the guide, we outlines the competitive shareholder return policy that has characterized our Group for many years.

Transparency, listening and dialogue are key in our relationship with our shareholders. The Individual Shareholder Relations Department organizes multiple events each year to give you the opportunity to share your views, interact and learn. This guide details how we are strengthening our ties with you, the current and future Total shareholders.

We hope you enjoy this guide.

Mike Sangster

Foreword from the Senior Vice President Investor Relations

4 | 2017 Issue

ExchangesParis, New York, London and Brussels

Codes

ISIN FR0000120271

Reuters TOTF.PA

Bloomberg FP FP

Datastream F:TAL

Mnémo FP

Included in the following stock indexesCAC 40, Euro Stoxx 50, Stoxx Europe 50, DJ Global Titans

Included in the following ESG indexes (Environment, Social, Governance)

DJSI World, DJSI Europe, FTSE4Good, Nasdaq Global Sustainability

Weight in the main indexes

CAC 40 10.9 % 1st positionEURO STOXX 50 5.6 % 1st positionSTOXX EUROPE 50 3.1 % 6th positionDJ GLOBAL TITANS 1.6 % 29th position

Market capitalization on Euronext Paris and in the Euro zone

Largest market capitalizations in the Euro zone:

As at December 31, 2016 (in billion euros)

AB InBev 203.0

TOTAL (1) (2) 118.4

Unilever 116.5

SAP SE 101.7

Industria de Diseno Textil 101.1

Siemens 99.3

Source: Bloomberg for all companies other than Total.

Market capitalization(1)

€118.4 billion(2)

$123.8 billion(3)

Percentage of free float

Free float factor determined by Euronext (CAC 40): 95% Free float factor determined by Stoxx (Euro Stoxx 50):

100%

Per value

€2.50

Credit ratings of the long-term and short-term debt(long term/outlook/short term)

Standard & Poor’s: A+/Neg/A-1Moody’s: Aa3/Stable/P-1

(1) Number of shares outstanding on December 31, 2016: 2,430,365,862.(2) Total share price at closing in Paris on December 31, 2016: €48.72.(3) Total ADR price at closing in New York on December 31, 2016: $50.97.

The Total shareData as at December 31, 2016

2017 Issue | 5

By shareholder type

Individual shareholders 7.9%

Institutional shareholders 87.2%

Groupemployees(2)

4.9%

By area

Rest of the world 8.1%

France27.7%

North America36% Rest

of Europe16%

United Kingdom 12.2%

Shareholding structureEstimation as at December 31, 2016(1)

(1) Treasury shares excluded(2) On the basis of employee shareholding as defined in Article L. 225-102 of the French Commercial Code.

The number of French individual Total shareholders is estimated at approximately 450,000.

6 | 2017 Issue

Our dividend policy

Our dividend policy

�An attractive yield for our shareholders (5.7% relative to the average 2016 share price(1)).

�A quarterly dividend payment.�Steady dividend growth.�Dividend payment in shares or in cash.

Dividend per share

(1) Subject to the approval of the Annual Shareholders' Meeting on May 26, 2017.(2) Subject to the decisions of the Board of Directors and Annual Shareholders' Meeting. The tentative schedule concerns the ex-dividend dates of shares

traded on Euronext Paris.

0.83 €

2000

1.62 €

2005

2.28 €

2010

2.44 €

2015

2.45 €(1)

2016

2017 dividend

Tentative schedule of 2017 ex-dividend dates(2):First interim dividend: September 25, 2017Second interim dividend: December 19, 2017Third interim dividend: March 19, 2018Remainder: June 11, 2018

If approved by the Annual Shareholders' Meeting, all interim dividends for 2017 will be paid in new shares or in cash.

The Board of Directors, delegated by the Annual Shareholders' Meeting, determines the issue price of new shares for each interim dividend, including a 0 to 10% discount.

It corresponds to the average opening price of the Total share during the 20 trading days preceding the Board's decision to award the interim dividend, reduced by the amount of the interim dividend, rounded up to the nearest euro cent.

2017 Issue | 7

For further information, we invite you to visit our total.com website, under the heading Investors/Shares and dividends/Dividends

How do you select your choice?

Banks or brokers automatically send a form to all shareholders, specifying the number of shares for which they are eligible to subscribe and asking them to select their choice.

The form mentions the deadline before which the bank or broker must receive the completed answer sheet.

If no choice has been stated or if the answer sheet is sent too late, the shareholder automatically receives the dividend due in cash.

Shareholders who have not received the form allowing them to select payment in shares should contact their bank or broker.

How is the number of shares calculated?

For shareholders with administered registered or bearer shares, the number of shares they are allowed to receive is based on the gross interim dividend. The bank withholds the amount corresponding to tax and social contributions from the shareholder's checking account.

For shareholders with pure registered shares, the number is based on the net interim dividend, i.e. the amount minus the social contributions and mandatory taxes, or on the gross interim dividend (in which case the shareholder must pay the social contributions and taxes to BNP Paribas Securities Services), as the shareholder prefers.

If the dividend amount does not correspond to an even number of shares, the shareholder can chose one of the following possibilities:

The "lower" option: the shareholder receives the number of shares directly below, plus a balancing cash adjustment.

The "higher" option: the shareholder receives the number directly above and pays the difference in cash on the day of the choice.

IMPORTANT NOTE:

In the case of administered registered shares, the new shares received are bearer shares. The shareholder's bank or broker is in charge of registering them as administered shares, but only if requested by the shareholder.

Example

The shareholder resides in France and holds 500 Total bearer shares. The interim dividend amounts to 0.62€/share.• 2016 gross interim dividend due:

500 x €0.62 = €310.• Subscription price: €45(1).• Theoretical calculation of the number of shares:

€310 / €45 = 6,9 shares.• The "lower" option: 6 new shares received plus a

balancing cash adjustment of €310 - (6x€45) = €40.• The "higher" option: 7 new shares received and

(7x€45) - €310 = €5 to be paid in cash.

If the shares are not in a PEA (French equity savings plan), the shareholder's bank or broker draws €65.1 from the shareholder's cash account as an instalment for the 21% income tax (except for exemptions) and €48.05 for the 15.5% social contributions. The amount reported on the shareholder's tax return is the gross interim dividend earned, i.e. €310 in this example (further information on dividend taxation is provided on page 13).

(1) Assumption that does not prejudge the actual subscription price set for future dividend payments. For each interim or final dividend payable in shares, a press release specifying the subscription price and the deadline for expressing a choice will be published a few days before the ex-divi-dend date.

8 | 2017 Issue

Types of shareholdingShares

�Can be registered, which means that shareholders can be identified by the issuing Company with two possibilities: ln the case of pure registered shares, the issuing

Company holds the shares in a custodial account and manages them directly (BNP Paribas Securi-ties Services manages the shares on Total's be-half).

In the case of administered shares, the shares are registered with the issuing Company but managed by a bank or broker chosen by the shareholder.

Can be held by the bearer, which means that only the bank or broker knows the shareholder’s identity. However, according to the Company's statutes, the identifiable bearer shareholder analysis procedure (TPI in French) allows it to obtain the list of bea-rer shareholders registered with French banks and brokers.

Registered shares

Advantages of holding Total pure registered shares

No custodial fees.

A dedicated toll-free number for all your commu-nications with BNP Paribas Securities Services:

From outside France: +33 1 40 14 80 61.

Easier placement of market orders(1) (by phone, mail, fax, internet).

�Preferential brokerage fees(1): 0.20% (before tax) of the gross amount of the transaction, with no minimum charge and up to €1,000 per transaction.

�A personal invitation to Total's Shareholders' Meetings.

Double voting rights if the shares are held for more than two consecutive years.

�All the shareholder information published by the Group is sent to the shareholder's home address or by internet.

Internet access to the shareholder's account.

How can you convert your shares?

BNP Paribas Securities Services manages registered shares on our behalf. To convert your shares into registered shares, complete the registration form, that can be downloaded on total.com, under the heading Investors / Individual shareholders / Being a Total shareholder, and send it to your financial advisor.

Once BNP Paribas Securities Services receives the shares, they will send you a certificate of account registration and will request the following:

Bank account details (or postal account or savings account details) for payment of dividends.

�A brokerage service contract if you wish to trade your Total shares on the stock exchange.

(1) If the shareholder has signed a brokerage service contract, which is free of charge.

IMPORTANT NOTE : • It is difficult to include pure registered shares in

PEA (French equity saving plan), because of the administrative procedures involved.

• Converting shares to pure registered shares may be subject to slight delays depending on the bank or broker processing time frame.

• The system is suited to those who do not make frequent transactions.

• Shareholders who are registered shareholders for their entire portfolio of shares receive as many statements as securities accounts they own.

0 800 11 70 00

0 800 11 70 00

0 800 039 039 Service & toll free

For further information, we invite you to visit our total.com website, under the heading Investors/Individual Shareholders

2017 Issue | 9

PURE REGISTEREDADMINISTERED

REGISTEREDBEARER

CustodianBNP Paribas Securities Services manages the shares.

Your bank or broker manages your securities account.

Managementfees

No custodian or management fees, but only a brokerage fee of 0.2% (before tax) on the gross amount of the transaction, with no mini-mum charge and up to €1,000 per transaction.

Tariffs of your bank or broker.

Information about Total

You receive all the documents published by the Company for its individual shareholders.

You need to request some of the documents from Total.

Invitation to the Annual Shareholders’ Meeting

All the documents needed to participate in the Annual Shareholders' Mee-ting are sent to you. You can receive your invitation and vote by internet.

You need to complete the formalities with your bank or broker.

Admissionto the Annual Shareholders' Meeting

By presenting your admission card or your ID.By presenting your admission card.

Voting rightsDouble voting rights for all shares held for more than two consecutive years.

Simple voting right: one share = one vote.

Stock market orders

You can send your orders directly to BNP Pari-bas Securities Services. This service does not apply to shares held in a PEA (French equity savings plan). Only "market" orders or "limited price" orders are accepted.

You send your orders to your bank or broker.

Annual tax reporting

You receive a French tax form (IFU) to declare the dividend income on your Total shares.

Your bank or broker sends you the French tax form listing all the operations on your securities account.

Capital gains on shares

The French tax form specifies the amount of Total shares sold during the prior year. Capital gains are calculated only when the market price is known (spontaneous declaration or all transactions made in registered shares).

The French tax form (IFU) received specifies the amount of Total shares sold during the previous year. Some banks or brokers offer to calculatethe capital gains (usually for a fee).

Eligibility for the SRD deferred settlement system

No. Yes.Yes. Your bank or broker may refuse though.

Inclusion in a PEA (French equity savings plan)

Total cannot hold a PEA account. We strongly discourage shareholders from declaring PEA-account shares as registered shares, conside-ring the complexity of the regulations involved.

Your bank or broker may claim higher mana-gement fees than for bearer shares.

Your bank or broker determines the manage-ment fees.

Types of shareholdingRegistered vs. bearer shareholding

10 | 2017 Issue

Stock exchange orders and shareholder rightsThe main types of orders

Limited price orderThe order determines a maximum limit to the purchase price and a minimum limit to the sale price. It is only executed when the price falls below the purchase limit or rises above the sale limit. Execution may also be partial.

Order at best limitThe price is not determined; the order is executed at the best price available as soon as it reaches the market. What makes this order different from the market order is that once the price has been determined by the best seller, the order becomes a limited price order on that value, and the purchase will be made only at that price. Execution may therefore be partial.

Market orderNo price limit has been set and it has priority over all the other orders. The order can only be completed in total form (i.e. cannot be split).

How is an order submitted?

All stock market orders must specify:The Total ISIN code: FR0000120271.The type of operation: purchase or sale.The number of shares.�The validity period of the order.Price conditions. The type of payment: immediate or SRD deferred

settlement system.

Is the purchase of Total shares taxed?

The purchase of Total shares is subject to the French Financial Transaction Tax. The tax rate is 0.3% of the average purchase price (excluding brokerage fees) and is fully charged to the purchaser.

Note: this tax does not apply to Total shares purchased free of charge, nor to share transfers.

Shareholder rights

Financial rights

All shareholders are entitled to receive a share of the income generated by the Company, if it is distributed. This decision is submitted by the Board of Directors to the Annual Shareholders' Meeting, where annual accounts and the allocation of the fiscal year's income are approved. The Company is not paid a dividend for the shares it holds.

Right to vote in the Shareholders’ Meeting

All shareholders are entitled to take part in the Annual Shareholders' Meeting. They have the right to vote (one share corresponds to one vote) at these meetings. Total statutes allow two votes (one share corresponds to two votes) for all registered shares held for at least two consecutive years. The shares held by the Company and its affiliates do not grant any right to vote.

Information rights

Shareholders own a share of the Company, therefore its executives are required to inform them, at any moment and as soon as possible, of any information that could have an impact on the stock market price.This right entitles the shareholder to have access to different documents on the management of social affairs and corporate life in general.

The French Financial Markets Authority (AMF in French) provides general information on the purchase of shares on the stock exchange on its website www.amf-france.org, under the heading Epargne info Service / Autres informations et guides pratiques / A savoir avant d'investir.

2017 Issue | 11

IN BRIEF:

Capital gains are taxed on a progressive scale.

A tax allowance is applied to net capital gains when shares are held for more than two years.

Capital gains are also subject to a 15.5% social contribution.

If the securities are of the same nature, capital losses are deducted from capital gains realized during the same year and the next 10 years.

1) Capital gains on shares are subject to an income tax

Capital gains realized on the sale of shares(1) must be reported on your annual tax return. If your bank or broker does not calculate them, you are responsible for doing so and for entering the results on your tax return.

Capital gains realized from January 1, 2013 are taxed on a progressive scale.

Capital losses on the sale of securities and on social contributions, can be offset by gains of the same nature realized during the same year and the next 10 years.

2) A tax allowance is applied de-pending on the length of holding

Net capital gains are taxed on a progressive scale, but a tax allowance is applied to capital gains realized as from January 1, 2013.

The tax allowance rate applied depends on the holding period:

Length Rate

Less than 2 years 0%

Between 2 and 8 years 50%

More than 8 years 65%

The holding period is counted from the date on which the shares were acquired.� The tax allowance does not apply to capital losses

but to the net gain after capital loss allocation(2).

IMPORTANT NOTE:

��This tax allowance does not apply to capital gains realized before January 1, 2013 and deferred from income tax.

��Capital gains from selling Total shares, which are deferred from income tax cannot benefit from a tax allowance based on the length of holding.

Taxation on capital gains for shares not in PEA (French equity savings plan)(1)

I. You are a tax resident in France

(1) Shareholders who are tax residents in France must be aware that the information provided regarding capital gains on the sale of shares can in no way be considered exhaustive and is simply a summary of the tax system applicable to them in the current state of tax law, and that their specific situation will need to be examined with their financial advisor.

(2) In its decree dated November 12, 2015, the French Council of State nullified the administrative doctrine by which the tax allowance for length of holding applies to both capital gains and capital losses on the sale of securities.

12 | 2017 Issue

3) Social contributions are due on capital gains realized on the sale of shares

These capital gains are subject to social contributions, at an overall rate of 15.5% (since January 1, 2013: 8.2% for the CSG, 0.5% for the CRDS, 4.5% social security payment, 0.3% for additional contributions, 2% solidarity levy).

Social contributions are withheld from the entire net capital gain realized, before application of the tax allowance for length of holding.

The amounts due are determined by assessment (on the basis of the tax return you have completed, tax authorities send you an assessment of the amounts due).

For capital gains 5.1% of the CSG will be deductible from the total taxable income of the year the CSG was paid.

1) Your capital gains are not taxed in France

2) The tax system of the country of residence applies

In your country of residence, capital gains could be taxed. You need to contact the tax authorities of your

country of residence or your financial advisor to ob-tain more information about your situation.

A few examples• In Germany - Above €801 for individuals and

€1,602 for married couples, your capital gains are subject to income tax at a global flat rate

of 26.375% (plus church tax if applicable), or, if you elect to do so, at your income tax rate. Note: Capital losses realized on shares sold from January 1, 2009 can be allocated to capital gains acquired from that date.

• In Belgium - In principle, your capital gains are not taxed, but you must pay a 0.27% tax on stock exchange transactions, capped at €1,600.

• In the United Kingdom - You do not need to pay tax on capital gains when shares are not in an ISA or any other specific tax framework, if the total gains of this nature do not exceed a capital gains tax allowance of £11,300 for 2017-2018 fiscal year. In principle, capital gains not exempted are subject to a 10% tax rate applying to “basic-rate taxpayers” and a 20% tax rate to “higher and additional-rate taxpayers”.

II. You are a tax resident outside of France

IMPORTANT NOTE:

If your Total shares are pure registered, BNP Paribas Securities Services holds them and will inform you of the capital gain (or loss) realized when they were sold, so that you can report it in your tax return.

2017 Issue | 13

Taxation on dividends for shares not in a PEA(1)(2)

I. You are a tax resident in France

IN BRIEF:

Your dividends are taxed on a progressive scale. A 21% instalment on the income tax is withheld at

source from your dividend income, unless you are exempted.

A social contribution of 15.5% is also withheld at source from your dividends.

1) The dividends received are taxed on a progressive scale For tax purposes, your dividends are considered as

an income, and therefore need to be declared as income for the year in which they were earned. You will need to report them on your annual tax return under the category "Securities and investment income" (Revenus des valeurs et capitaux mobiliers). The amount taxed is the gross dividend income

after a 40% tax allowance (share acquisition and retention costs are deducted afterwards).

Example

In 2016, a shareholder who was paid a gross dividend of €100, reports this amount in 2017 in his 2016 tax return. After applying the 40% tax allowance, €60 will be added to his taxable income and the acquisition and retention costs will be deducted.

IMPORTANT NOTE:

The bank holding your shares will send you a document every year summarizing the amounts to be declared as dividends earned the previous year, i.e. the French IFU tax form.

2) Dividends are subject to a mandatory 21% levy The 21% levy (calculated on the gross dividend

income) represents a tax instalment. The levy paid

by the shareholder in 2016 will be taken into account in 2017, when calculating the tax on his 2016 income. If it exceeds the tax due, the shareholder will be reimbursed the difference. However, a taxpayer whose reference taxable income,

two years before, was less than €50,000 (for a single person) or €75,000 (for a couple filing a joint return) can obtain an exemption by sending a request to their bank or broker each year, certifying that they meet these conditions. The financial institution holding the shares must receive the request no later than November 30 for the shareholder to benefit from it the next year.

Example

To obtain the exemption in 2018 of the instalment withheld on the dividend income, the taxpayer had to have a reference 2016 income that met the conditions above, and had to send the exemption request to his bank before November 30, 2017.

3) Social contributions are applied to dividends

Social contributions are withheld at source by the paying financial institution (even when the shareholder is exempted from the mandatory levy). They are applied to the gross amount earned at an overall rate of 15.5% (8.2% for the CSG, 0.5% for the CRDS, 4.5% social security payment, 0.3% for additional contributions, 2% solidarity levy).

However, 5.1% of the CSG are deductible from the total taxable income on the year of the payment.

(1)These measures apply to dividends and interim dividends. (2) Shareholders must be aware that the information provided can in no way be considered exhaustive and is simply a summary of the tax sys-

tem applicable to them in the current state of tax law, and that their specific situation will need to be examined with their financial advisor.

IMPORTANT NOTE:

A fine equal to 10% of the levy amount is applied to any natural person who requested to be exempted from paying the instalment without meeting the conditions (a reference taxable income above the specified limit).

14 | 2017 Issue

4) Example of dividend taxationIn 2016, a gross dividend of €2 per share is paid to a shareholder with 200 shares, which equals a gross amount of €400.

Social contributions

They are withheld at source, at an overall rate of 15.5%, amounting to: €400 x 15.5% = €62.

Income tax

An instalment on the income tax, at a rate of 21%,is withheld at source from the gross dividend income, amounting to: €400 x 21% = €84.

But this amount will be deducted in 2017 from the tax amount due on income earned in 2016. If it exceeds the tax due, the difference will be reim-bursed. In 2017, the shareholder will report the gross dividend income earned (i.e. €400 in this example) in his 2016 tax return.

> For taxation:• Gross taxable amount: €400.• Amount after a 40% tax allowance:

€400 x 60% = €240.• Amount after deduction of custodian fees:

€240 - €40(1) = €200.• Amount of dividend income, taxable according

to a progressive scale, in the 2016 income: €200.

• Amount deductible from the 2016 total taxable income, corresponding to the 5.1% deductible CSG: €400 x 5.1% = €20,40.

5) Taxation of dividends paid in shares

�The dividend paid in shares is subject to the same income tax as a dividend paid in cash. The amount to be reported on your tax return is specified on the French tax form (IFU) sent by your bank. The 21% income tax instalment and social contributions are calculated on the gross dividend amount.

For shareholders with administered registered or bearer shares, the gross dividend amount is used to determine the number of shares that the shareholder can reinvest. The financial institution draws the applicable social contributions and taxes from the shareholder's cash account.

For shareholders with pure registered shares, it can either be the net dividend (i.e. after deduction of the social contributions and taxes) or the gross dividend (i.e. before deduction of the social contributions and taxes), as the shareholder prefers. In the latter case, the shareholder will need to pay to BNP Paribas Securities Services the amount corresponding to the social contributions and taxes.

(1) Hypothesis that does not prejudge the actual custodian or management fees.

2017 Issue | 15

1) Dividends are subject to a withholding tax

In France, a 30% tax is withheld at source from your dividends, but it can be reduced if there is a tax agree-ment between France and your country of residence. The dividend withholding tax rate is reduced to 15% in most cases though.

In that case:

You can immediately be taxed at a reduced rate of 15%, if you take the necessary measures before dividend payment. You will need to fill out a declaration proving your residency (form 5000), have it stamped by the tax authorities of your country, and send it signed to the French tax center for non-residents: Centre des impôts des non-résidents -10 rue du Centre - TSA 10010 - 93 465 Noisy le Grand Cedex - France. You need to repeat this procedure every year.

Or you can ask to be reimbursed the difference no later than December 31 of the second year following dividend payment. You will need to fill out a declaration proving your residency (form 5000) and the form 5001, have them stamped by the paying agent and the tax authorities of your country of residence, and send them signed to the French tax center for non-residents.

2) The tax system of the country of residence applies

You can be taxed in your country of residence.

You need to contact the tax authorities of your country of residence or your financial advisor to obtain more information about your situation.

A few examples• In Germany - Above €801 for individuals and

€1,602 for married couples, your capital gains are subject to income tax at a global flat rate of 26.375% (plus church tax if applicable), or, if you elect to do so, at your income tax rate.

• In Belgium - Your dividends are taxed at source at a rate of 30%. In most cases, this withholding tax is the final one. Dividends therefore do not need to be declared in the tax return. However, in the case of lower incomes, dividend income can be declared in order to have the tax already paid taken into account and obtain reimbursement of any excess tax paid. Some types of dividend income must always be declared in your tax return, such as foreign income, received directly outside of Belgium.

• In the United Kingdom - If your shares are not held in an ISA (Individual Savings Account) or another specific fiscal framework, dividends are not taxed up to £5,000 per fiscal year (i.e. between April 6, 2016 and April 5, 2017). If you are paid more than £5,000 in dividends, you need to assess your other incomes and determine whether the excess is exempt from tax after application of the annual personal allowance of £11,500 (Standard personal allowance for 2017-2018 fiscal year) on your different sources of income, or if applicable, on the amount remaining subject to income tax, and determine in that case, the tax rate that will be applied to that excess depending on your financial situation (7.5%, 32.5% or 38.1%).

II. You are a tax resident outside of France

16 | 2017 Issue

Shares held in a PEA(1) (French equity savings plan) and their taxationThe PEA was introduced in 1992. It is a tax system that allows taxpayers to own a portfolio of European shares that are not subject to income tax, provided that no withdrawals are made within a minimum pe-riod of five years from the first payment.If this condition is met, dividends and capital gains are exempt from tax.

A PEA account can be opened with any financial ins-titution. The maximum investment is €150,000, and payments are required to be made in cash, at any time, with no mandatory legal minimum.

Shares acquired through a PEA can only be paid from the cash held in that account, and must be eligible for that type of account, which is the case for Total shares.

IMPORTANT NOTE:

Operations in deferred settlement (SRD) are not allowed for PEA shares (no overdrafts are there-fore allowed).

The capital losses on PEA shares cannot be offset by, or transferred to capital gains of the same na-ture on shares not in the PEA.

PEA income remains subject to social contribu-tions, which are withheld on gains at PEA closure.

Are my PEA shares blocked?

Total shares purchased as part of a PEA are not blocked. If they are sold and the sale amount remains in the

PEA, they are not taxed. If they are transferred and the shares or transfer

amounts are withdrawn from the PEA, the tax conse-quences imposed by regulations apply.

According to these regulations, if shares or funds are withdrawn: • Within two years: the PEA is closed(2) on the date of

withdrawal and taxed at a rate of 22.5%.

• Between two and five years: the PEA is closed(2) on the date of withdrawal and taxed at a rate of 19%.

• After the fifth year and before the end of the eighth year: any withdrawal of amounts or values closes the account(2).

• Beyond eight years: the account is not closed but

new funds cannot be paid in.

Can my Total PEA shares be regis-tered?

Total shares held in a PEA account can be registered if you request your bank or broker to do so, we dis-courage, shareholders from declaring PEA-account shares us registered shares though (see page 9).

(1) Applies only to individual shareholders being tax resident in France.(2) Under certain conditions, withdrawals from PEA can be made prior to the end of the eighth year without closing it if the purpose is to set up

or take over a business.

2017 Issue | 17

Gifting sharesI. You are a tax resident in France

Several options are available to you to transfer the ownership of your Total shares free of charge to your child, spouse, partner or any other person of your choice.

Informal gift

You can make an informal gift (présent d'usage) on family occasions (birthday, etc.). It is not taxed but must be limited to small amounts in proportion to your estate and income. The informal gift cannot be returned to the estate to be included in the inheritance.

You can make a gift ”hand to hand” (don manuel) that does not require any formalities or the presence of a notary, but can be recorded in a written document confirming that shares have been transferred and possibly include conditions.Tax authorities must be informed of the gift even if no taxes are paid on it.

A “hand to hand” gift is declared to the tax authorities of the giver's residency, using tax forms 2735 or 2734 (downloadable on the website: www.impots.gouv.fr). As long as the tax authorities are not aware of the “hand to hand” gift, it is not taxed, but once they are aware of it, it must be declared within the following month. The tax authorities may become aware of the gift if you declare it in a notarial deed or following a tax inspection, or if it is included in a declaration of inheritance after your death. A “hand to hand” gift can be declared within the month following the giver's death, if its amount is higher than €15,000.

Formal gift

The shared gift (donation-partage) al lows shareholders to transfer ownership of their assets while they are still alive. It is an excellent way of rewarding your children in the long term. The shared gift is recorded in an authentic deed signed before a notary, and the giver can continue to receive the dividends on the assets transferred.

The gift to a spouse (or to the last survivor) must be signed in the presence of a notary. Its distinctive feature is that it can be overturned (if no marriage contract exists), even without the other spouse's knowledge. It takes effect on the day of the giver's death.

How are share gifts taxed?

Gift tax is calculated on the net taxable amount (the amount received by each recipient after possible deduction of tax allowances) and depends on the family relationship with the recipients. In some cases, a reduction may be granted (such as a reduction for providers of large families or war-disabled persons).Note: contact your tax authorities or a notary to obtain more precise and up-to-date information on gift tax amounts.

Gift tax allowancesIn the case of a gift, tax allowances are appliedevery 15 years as follows:

€100,000for each living or represented child, and from each parent

€80,724for a spouse or civil partner

€31,865for each grandchildt

€15,932 for each brother and sister

€7,967 for each nephew or niece

€5,310 for each great-grandchild

A person with a disability is eligible for a tax allowance of €159,325 that can be cumulated with the other tax allowances.

IMPORTANT NOTE:

On the death of the giver, some gifts may be re-turned to giver's estate: this is the case for “hand-to-hand” gifts in particular, depending on the cir-cumstances.

A gift is likely to be taxed if it is declared by the giver in an official deed.

18 | 2017 Issue

IMPORTANT NOTE:

Capital gains: in the case of a gift of shares, the deferred capital gains are not taxed if the tax authorities are aware of the operation, i.e. they have been informed of the gift. A gift of shares can therefore erase a deferred capital gain.

Shares held in a PEA (French equity savings plan): a gift of shares held in a PEA automatically closes the plan, with the consequences that entails. If the gift is made within five years from the time the plan was open, the net gain realized in the PEA will be taxed under the same conditions as an early withdrawal, and will be liable to late interest and penalties for willful neglect. Any income earned from the date of the gift is taxable under the conditions of ordinary law.

�Estate and gift tax exemptions or reductions: Total shares gifted to public benefit organizations are exempted from tax under the conditions set out by the applicable regulations. These gifts can in addition give rise to a tax reduction equal to 66% of the value of the gift, and up to 20% of the giver's taxable income (this threshold can be higher depending on the beneficiary organization).

FURTHER INFORMATION CAN BE OBTAINED FROM THE FOLLOWING:

�BNP Paribas Securities Services* for all holders of Total pure registered shares.

�Tax authorities to find out about required tax pay-ments.

Notaries who can explain the procedure for transfer-ring ownership of shares.

* BNP Paribas Securities Services manages registered shares on behalf of Total (see page 8)

If you wish to transfer ownership of your Total shares, request our gift card

If you decide to transfer ownership of your shares, send a request to Total's Individual Shareholder Relations Department, and we will offer you a gift card to make your donation more tangible.

You can transfer Total shares free of charge to your spouse/partner or your relatives if you are not a tax resident in France.However, as each country has its own laws, you need

to find out the procedures that apply to your case and the different tax implications, and possibly ask for your situation to be assessed by professionals (tax authorities, legal and financial advisors, etc.).

II. You are a tax resident outside France

2017 Issue | 19

Annual Shareholders' Meeting

Next Total S.A. General Meetings: • Friday, May 26, 2017• Friday, June 1, 2018

How can I be informed of the Annual Shareholders' Meeting?

On March 22, 2017, Total published the notice of meeting for the 2017 Shareholders' Meeting in the French Bulletin des annonces légales obligatoires (BALO). A notice of meeting must be published at least 15 days before the Shareholders' Meeting in the BALO and in a newspaper allowed to carry legal notices. The notice specifies the conditions for participating and the text of the resolutions submitted to the vote.

Registered shareholders receive all the documents needed to take part in the Shareholders' Meeting from BNP Paribas Securities Services on Total's behalf (notice of meeting, voting form / request for an admission card). They can receive them in digital form by making an online request on the Planetshares website.

Holders of 250 or more bearer shares receive all the documents needed to take part in the Shareholders' Meeting from their bank or broker (notice of meeting, voting form / request for an admission card). Holders of less than 250 bearer shares must request them from their bank or broker.

How can I participate in the Annual Shareholders' Meeting?

You can participate in the Annual Shareholders' Meeting by being physically present, by voting before the meeting, or being represented. In all cases, you may express your choice by completing the voting form that will be sent to you in hard copy or via the internet using the online VOTACCESS platform.

If you use the printed form, you must send it to:• BNP Paribas Securities Services, if your shares are

registered.• Your bank or broker, if you hold bearer shares.

If you use VOTACCESS:

If your shares are pure or administered registered, you can access VOTACCESS via the Planetshares website.

If you hold bearer shares, and your financial institution is connected to VOTACCESS, you can have access to it by logging into its website, and into your securities account or PEA (French equity savings plan). If your financial institution is not connected to the VOTACCESS platform, you cannot vote online.

How can I attend the Annual Shareholders' Meeting?

You are admitted upon presentation of an admission card previously requested using the printed form or via VOTACCESS.

How can I vote before the Meeting or be represented?

You can express your choice on the printed form or on VOTACCESS. You can vote for each resolution, or give proxy to the Chairman or be represented by any other person designated by you.

Shareholders who have requested their admission card on VOTACCESS can print it out themselves or have it sent by mail.

For further information, we invite you to visit our total.com website, under the heading Investors/Shareholders meetings

20 | 2017 Issue

Individual Shareholder Relations Department

The Individual Shareholder Relations Department is dedicated to assisting individual shareholders by providing a complete range of services from dedicated phone lines for shareholders in France and overseas to organizing interactions between Group executives and the Shareholder e-Advisory Committee (e-CCA), frequent shareholder meetings, exhibits or events with the Shareholders' Club. In 2016, the team met with more than 10,000 individual shareholders.

Total's Individual Shareholder Relations Department is the only shareholder service in France to have obtained ISO 9001 certification (version 2015) for its communication policy with individual shareholders. In 2017, certification was renewed by the French AFNOR standardization organization for an additional three years, after an in-depth audit of the different processes implemented to ensure smooth communication with individual shareholders.With this certification, the Individual Shareholder Relations Department shows the commitment made by the Group to provide its shareholders with ongoing financial information.

In 2016, the quality of this information was recognized once again by the specialized press. The French Magazine Le Revenu awarded Total the Super Gold Trophy for the best Shareholders' Relations of the CAC 40 companies as well as the Gold Trophy for the best Shareholders' Meeting.

The Shareholders' e-Advisory Committee

The Shareholders' e-Advisory Committee was set up to support the Individual Shareholder Relations Department's ongoing efforts to improve the quality of its communication. A quarter of its twenty members are renewed every year. To facilitate regular and in-depth interaction and discussions, members of the e-Advisory Committee and the Individual Shareholder Relations team communicate via an online platform.

The Committee met three times in 2016 and gave advice on different tools used to communicate with individual shareholders, and more particularly on the redesign of the Investors headin of the total.com website.

The Shareholders' Club

The purpose of the Shareholders' Club is to forge closer ties between Total and its shareholders, by improving their knowledge of Total and its activities.The Club is open to shareholders who hold at least 50 registered shares or 100 bearer shares. It organized 26 special events in 2016 for its 7,000 members. Club members have visited industrial facilities, natural and cultural sites supported by the Total Foundation and attended conferences on the Group.

At the beginning of 2017, the Club went all-digital with the publication of its website, https://e-cercle.total.com, where members can find information about the program, receive reminders when events are open for registration, and sign up for them in just a few clicks...

Relations with individual shareholders

For further information, we invite you to visit our total.com website, under the heading Investors/Individual Shareholders

2017 Issue | 21

Relations with individual shareholders

March 28 Online shareholders' meeting

April 27 First quarter 2017 Results

May 26 Annual Shareholders' meeting 2017 in Paris (France)

June 19 Shareholders' meeting in Biarritz (France)

June 20 Shareholders' meeting in Toulouse (France)

June 28 Participation at the Investors fair, Les Rendez- Vous de Votre Argent, in La Rochelle (France)

July 27 Second quarter 2017 Results

September 25 Investors Day in London (UK)

September 30 VFB Investor Event in Ghent (Belgium)

October 5 Shareholders' meeting in Reims (France)

October 27 Third quarter 2017 Results

November 7 Shareholders' meeting in Rennes (France)

�November 23-24 Actionaria exhibition in Paris (France)

November 24 Shareholders' meeting in Paris (France)

Our communication tools

3 issues of the Shareholders' Newsletter every year

A special sectionfor shareholders on the www.total.com website

The Total Investors app for iPad and Android tablets and smartphones

The Shareholders' Cluband its website: e-cercle.total.com

Shareholders’ Webzineon the www.total.com website

The Shareholder'sGuide

Major events in 2017

22 | 2017 Issue

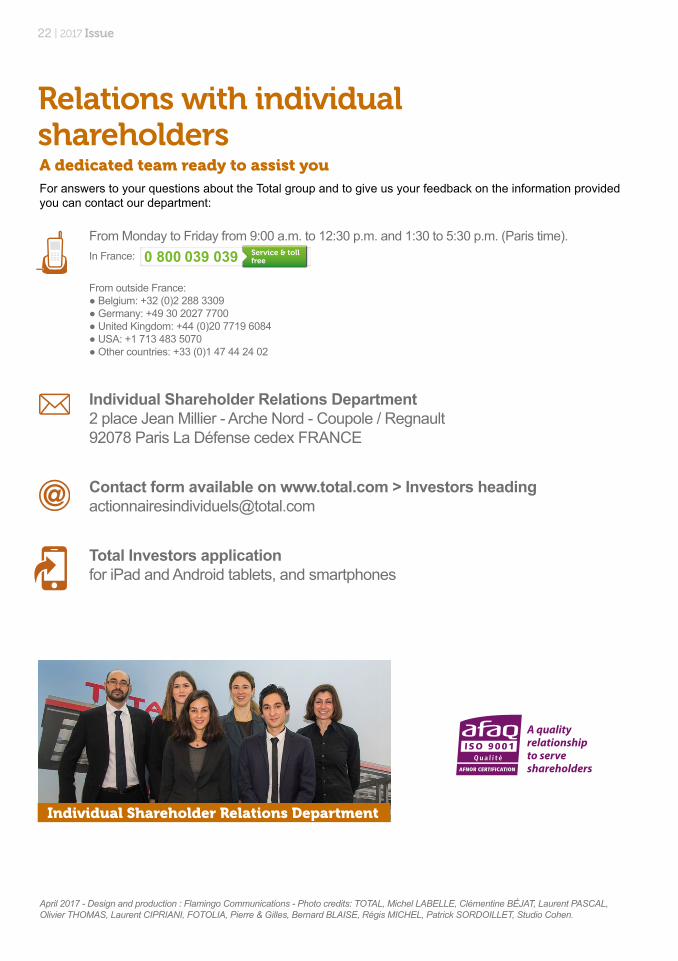

A dedicated team ready to assist youFor answers to your questions about the Total group and to give us your feedback on the information provided you can contact our department:

April 2017 - Design and production : Flamingo Communications - Photo credits: TOTAL, Michel LABELLE, Clémentine BÉJAT, Laurent PASCAL, Olivier THOMAS, Laurent CIPRIANI, FOTOLIA, Pierre & Gilles, Bernard BLAISE, Régis MICHEL, Patrick SORDOILLET, Studio Cohen.

From Monday to Friday from 9:00 a.m. to 12:30 p.m. and 1:30 to 5:30 p.m. (Paris time). In France: From outside France: ● Belgium: +32 (0)2 288 3309 ● Germany: +49 30 2027 7700 ● United Kingdom: +44 (0)20 7719 6084 ● USA: +1 713 483 5070 ● Other countries: +33 (0)1 47 44 24 02

Individual Shareholder Relations Department 2 place Jean Millier - Arche Nord - Coupole / Regnault 92078 Paris La Défense cedex FRANCE

Contact form available on www.total.com > Investors heading [email protected]

Total Investors applicationfor iPad and Android tablets, and smartphones

Individual Shareholder Relations Department

Relations with individual shareholders

FOR YOU, ALL OUR ENERGY IN ACTION

(1) Please refer to the Registration Document available on total.com or Form 20-F filed with the United States Securities and Exchange Commission and available on sec.gov and total.com for information on risks associated with our activities. (2) Based on the 2016 dividend and average market price of Total shares on Euronext Paris in 2016. Past performance is not a reliable indicator of future performance.

Current and future shareholders

© V

ON

DE

R F

EC

HT

FLO

RIA

N -

GO

NZ

ALE

Z T

HIE

RR

Y -

PA

SCA

L LA

UR

EN

T -

DU

FOU

R M

AR

CO

- Z

YLB

ER

MA

N L

AU

RE

NT,

GR

AP

HIX

IM

AG

ES

- T

OTA

L

MOST PROFITABLE

EUROPEAN MAJORBenefit from Total’s solid

portfolio and outlook underpinned by highly

profitable assets(1)

ATTRACTIVE SHAREHOLDER PROPOSITIONInvest in a company

which generated a 5.7% dividend yield in 2016(2)

STRONG INTERNATIONAL

COMPANYChoose a fully-integrated oil

and gas major involved in low-carbon businesses with

a presence in more than 130 countries(1)

A quality relationship to serve shareholders

0 800 11 70 00

0 800 039 039 Service & toll free

FOR YOU, ALL OUR ENERGY IN ACTION

(1) Please refer to the Registration Document available on total.com or Form 20-F filed with the United States Securities and Exchange Commission and available on sec.gov and total.com for information on risks associated with our activities. (2) Based on the 2016 dividend and average market price of Total shares on Euronext Paris in 2016. Past performance is not a reliable indicator of future performance.

Current and future shareholders

© V

ON

DE

R F

EC

HT

FLO

RIA

N -

GO

NZ

ALE

Z T

HIE

RR

Y -

PA

SCA

L LA

UR

EN

T -

DU

FOU

R M

AR

CO

- Z

YLB

ER

MA

N L

AU

RE

NT,

GR

AP

HIX

IM

AG

ES

- T

OTA

L

MOST PROFITABLE

EUROPEAN MAJORBenefit from Total’s solid

portfolio and outlook underpinned by highly

profitable assets(1)

ATTRACTIVE SHAREHOLDER PROPOSITIONInvest in a company

which generated a 5.7% dividend yield in 2016(2)

STRONG INTERNATIONAL

COMPANYChoose a fully-integrated oil

and gas major involved in low-carbon businesses with

a presence in more than 130 countries(1)

Transfer ownership of your Total shares to your loved ones and allow them to benefit from the Group's growth prospects, its attractive dividend policy, and services tailored to our shareholders, while taking advantage of the tax benefits associated with a gift.

If you decide to transfer ownership of your shares, send us a request and we will offer you a gift card to make your donation more tangible.

Do not hesitate to contact us at

0 800 11 70 00

0 800 039 039 Service & toll free

or send an email to [email protected].

SHAREmore than your shares.

© P

hoto

cre

dit:

Foto

lia /

Des

ign: