MSOB: MBA Placements Preparation, MBA Placements, Business School Placements |

Upload

eric-higginsCategory

view

213download

1

Shareholder wealth effects ofprivate placements of debtmade by REITsReceived: 26th January, 2004

Eric Higginsis an assistant professor of finance at Kansas State University. He received his PhD in

finance from Florida State University in 1995 and has published articles in journals

including Journal of Financial Research, Financial Review, Quarterly Journal of Business

and Economics, Journal of Banking and Finance and Journal of Real Estate Portfolio

Management.

Shawn Howtonis an associate professor of finance at Villanova University. He received his PhD in

finance from Florida State University in 1996 and has published articles in a wide

variety of academic journals including Financial Management, Journal of Derivatives,

Journal of Business, Finance, and Accounting and Journal of Real Estate Portfolio

Management.

Shelly Howtonis an associate professor of finance at Villanova University. She received her PhD in

finance from Florida State University in 1996 and has published articles in journals

including Real Estate Economics, Journal of Real Estate Portfolio Management,

Financial Management, Financial Review and Journal of Financial Research.

AbstractThis study examined both the short-run and long-runshareholder wealth effects of private placements of debt madeby Real Estate Investment Trusts (REITs). The authors foundthat there is no significant market reaction to the placement.One-year and three-year adjusted abnormal returns were foundto be negative and significant for placing REITs. This suggeststhat REITs do not benefit from added monitoring associatedwith the private placement. The results also suggest that REITmanagers issue in order to grow the asset size of the firm tothe detriment of shareholder wealth.

Keywords:Real Estate Investment Trust (REIT), debt, private placements, wealtheffects

INTRODUCTIONWhile the shareholder wealth effects of initial and seasoned equityofferings for REITs have been examined extensively, only Howe andShilling (1988) and Howton and Howton (2001) have examined thewealth effects associated with debt offering announcements. Howeand Shilling (1988) found a small, positive market response to REIT

Shelly HowtonDepartment of FinanceVillanova University800 Lancaster Ave.Villanova, PA 19085-1678, USATel: +1 610 519 6111E-mail: [email protected]

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 3 NO . 4 P P 3 0 5 – 3 1 4 305

debt issues from 1970 to 1985. Howton and Howton (2001),however, found no significant market response to debt issues from1991 to 1997. They also found, in contrast to what is found forindustrial firms, that the market response is inversely related to theissuer’s level of existing cash and investment opportunities. To date,no study has examined the long-run shareholder wealth effects ofdebt issues made by REITs. The purpose of this study was to extendthe work on debt offerings made by REITs by examining bothshort-run and long-run shareholder wealth effects of privateplacements of debt.Carey et al. (1994) argue that the market for private placements

of debt is very information intensive, requiring thorough duediligence by lenders and active loan monitoring. If this is the case,REITs should benefit from debt private placements through theaddition of an external monitor. Also, the private placement may beviewed as a certification of the credit quality of a placing REIT.These facts would lead to the conclusion that REIT privateplacements of debt should lead to increases in shareholder wealth.REIT security issuances are, however, viewed much differently by

the market. This results from two unique characteristics of REITs.First, if REITs distribute 95 per cent of net taxable income toshareholders, they are not required to pay income tax at thecorporate level. Secondly, the 95 per cent distribution requirementlimits the ability of a REIT to use retained earnings to finance newinvestments. Thus, REITs may not have a preference for issuingdebt over equity and are forced to make frequent trips to the capitalmarkets. These characteristics generally cause the market to respondmuch differently to security issuances made by REITs, comparedwith security issuances made by industrial companies. Thus, it is notentirely clear how the market will respond to private placements ofdebt made by REITs.It is also unclear how the presence of an external monitor affects

the performance of REITs. Chan et al. (1998) suggest that thepresence of increased institutional investing will reduce some of theextensive agency problems that exist in REITs. The empiricalevidence regarding the benefits of outside monitoring of REITs,however, has been mixed. Friday et al. (1999) find that the presenceof an outside blockholder does not necessarily increase value. Infact, for equity REITs, increased outside ownership concentration isassociated with decreases in value. While these results relate to thepresence of an external equity holder, they may also apply to thepresence of an external debt holder. Therefore, the presence of anactive, outside debt holder may not necessarily translate intoincreases in shareholder wealth.Additionally, REIT managers may have compensation-related

incentives to grow the assets under their control. This may leadREIT managers to issue as much capital as possible in order togrow the size of the REIT. As a result, REIT managers might bepunished by the market when debt is issued, due to the likelihood

REIT debt offerings

External monitors

Higgins, Howton and Howton

# HENRY S T EWART PUB L I C A T I ONS 1473 ^ 189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VOL . 3 NO . 4 P P 3 0 5 – 3 1 4306

that issue proceeds are to be used to simply grow asset size and notto increase the wealth of current shareholders. Some support for thisargument can be found by looking at the performance of externallyadvised REITs. Capozza and Seguin (2000) found that REITs thatare externally advised underperform those that are internallyadvised. A key reason for this underperformance is shown to be theextensive use of debt by external managers. Capozza and Seguin(2000) suggest that this extensive use of debt may be related to theexternal manager’s desire to grow firm assets in order to maximisecompensation. Thus, it is possible that private placements of debtmay actually be viewed negatively by the market and may decreaseshareholder wealth if the managers do use the placement proceedsfor negative net present value investments.Given the arguments above, the authors feel that the

examination of the shareholder wealth effects associated withprivate placements of debt by REITs extends the existing literaturein four ways. First, the examination of debt private placementsprovides further evidence regarding the way in which the marketresponds to REIT security issuances. Secondly, the authorsdocument the long-run, post-issue performance of REITs followingdebt issues. Thirdly, they provide further evidence regarding thebenefits of external monitoring for REITs. Finally, they providemarket-based evidence of a REIT manager’s propensity toexpropriate wealth from shareholders in order to increase the sizeof the REIT.The authors found that the market reaction to the private

placement of debt by REITs is insignificant. This is consistent withprevious research on public debt issues made by REITs. They alsofound, however, that the long-run adjusted market performance ofREITs declines following the private placement. This is consistentwith the hypothesis that REIT managers use the debt issue toincrease the asset size of the firm in order to maximisecompensation. Long-run underperformance is shown to beconsistent across time, differences in book to market equity ratiosand differences in market values.

DATA AND METHODOLOGYThe authors obtained a sample of REIT debt private placementsfrom the Securities Data Corporation (SDC) new issues databaseover the time period from 1993–2001. Due to the sparse nature ofpublicly available information regarding the placements, they usedthe placement date from the SDC database as the announcementdate for their study. Initially, 116 debt private placements werefound. To be included in the final sample, it was necessary for thefirm to have return information available from the daily Center forResearch in Security Prices (CRSP) database and to have totalassets available from Compustat. These screens eliminated only twoplacements made by the same REIT. The final sample consisted of114 placements made by 48 different REITs.

Private placementsof debt

Performance declines

Sample REITs

Shareholder wealth effects of private placements of debt made by REITs

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 3 NO . 4 P P 3 0 5 – 3 1 4 307

Using standard market model event study techniques, the authorsanalysed short-term abnormal returns around the 114 availableprivate placements of debt made by REITs. Equity returns weregathered for the placing REITs from the daily CRSP database.Abnormal returns were calculated for the placing REITs using amarket model: Ri,t = ai + biRm,t + ei,t , where Ri,t is the return onday t for the placing firm and Rm,t is the equally-weighted CRSPindex return on day t. The placement day was defined as day 0. Themarket model parameters, ai and bi, were estimated over the 200-day window ending ten days prior to the announcement (day –210to day –10). The significance of the abnormal returns in the eventwindow, defined as day –10 to day +10, was tested using the eventstudy test statistic developed by Brown and Warner (1985).Using a procedure similar to that of Loughran and Ritter (1995)

and Spiess and Affleck-Graves (1995), the authors computed long-run holding period returns for the placing REITs. They specificallyexamined one-year and three-year holding period returns for eachplacing REIT. One year was defined as 250 trading days, and threeyears was defined as 750 trading days. They also computed a one-year holding period return for the year prior to the placement.Holding period returns were computed to avoid potential biasesinduced by cumulating short-term returns. In addition to calculatingholding period returns for each placing REIT, they calculatedholding period returns for an index of REITs that did not makedebt private placements during their sample time period.1 They

Return calculation

Table 1: Abnormal stock returns for the ten days prior to and the ten days following the private

placement of a debt issue made by REITs. The placement date is defined as day 0. There are 114

placements included in the sample.

Days Averageabnormal return (in %)

t-statistic

–10 –0.080 0.564

–9 –0.063 –0.451

–8 –0.091 –0.822

–7 –0.063 –0.677

–6 –0.039 0.075

–5 0.098 0.272

–4 –0.032 –0.068

–3 0.025 0.174

–2 –0.019 –0.027

–1 –0.020 –0.003

0 –0.148 –1.453

1 –0.002 –0.327

2 0.132 0.954

3 –0.211 –1.530

4 –0.062 –1.198

5 –0.161 –1.084

6 –0.128 –0.754

7 0.063 –0.264

8 0.098 0.563

9 –0.219 –1.954

10 0.073 0.356

Higgins, Howton and Howton

# HENRY S T EWART PUB L I C A T I ONS 1473 ^ 189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VOL . 3 NO . 4 P P 3 0 5 – 3 1 4308

defined the adjusted return as the REITs’ return minus the return onthe REIT index, and used a non-parametric sign test to determine ifthe percentage of placing REITs underperforming the benchmarkREIT index was significantly different from 50 per cent.2

RESULTSTable 1 contains the results of the event study analysis conductedfor the private placements of debt made by REITs. As can be seen,none of the abnormal returns in the event window are significant.Thus, the placement does not convey any information to the marketabout the value of the REITs. While these results are consistent withthose found by Howton and Howton (2001) for public debt issuesmade by REITs, they are somewhat surprising. The lack of a marketresponse suggests that the additional monitoring and the creditquality certification provided by the external debt holder are notconsidered to be valuable information in the eyes of shareholders. Apossible explanation for this lack of a positive market response maybe that the debt issues are not competitively priced. Capozza andSeguin (2000) found that externally managed REITs issue more debtand issue the debt at an interest rate substantially higher thaninternally managed REITs. They suggest that the externallymanaged REITs want to issue debt at unfavourable rates becausethe REIT manager wants to increase the asset size of the REIT inorder to maximise compensation. Thus, it is possible that the privateplacements are not issued at competitive rates and, thus, the addedbenefits of external monitoring and credit quality certification aremitigated. Unfortunately, given that the issues in this study wereprivate placements, the authors do not have information on theyields of the debt issues in order to make comparisons between theyields on the privately placed debt relative to publicly placed debt.Table 2 contains a summary of the long-run pre- and post-

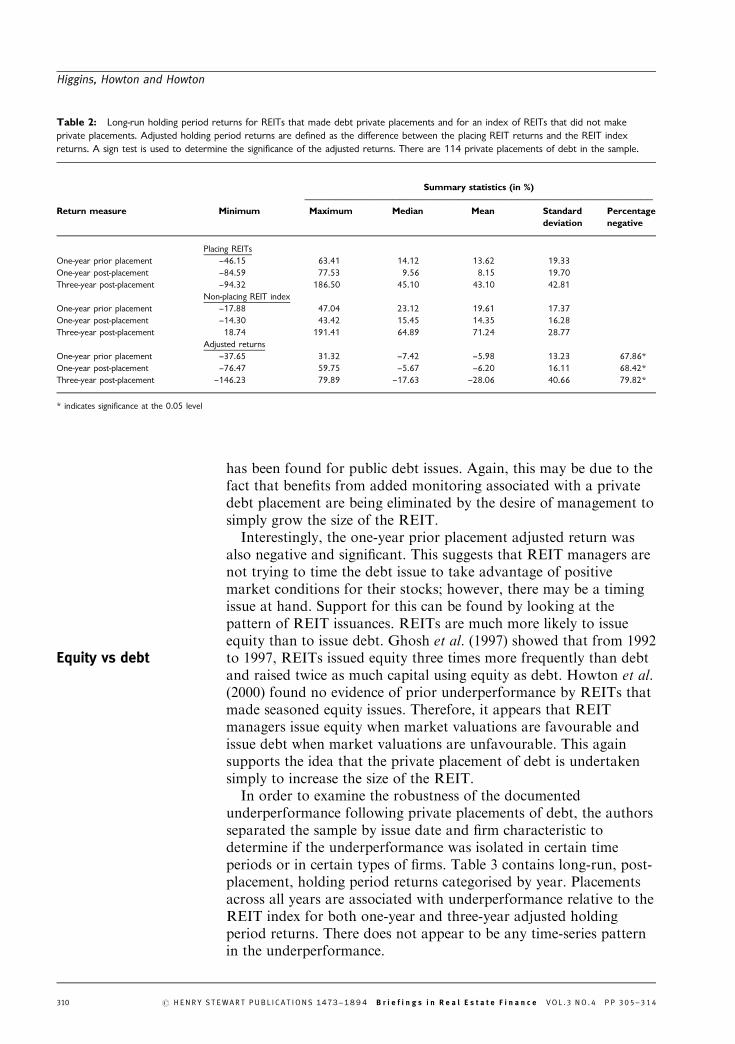

placement holding period returns for REITs making a privateplacement of debt. Both the one-year and three-year adjustedholding period returns are negative and significant following theplacement. The three-year adjusted holding period return has amean of –28.06 per cent, and almost 80 per cent of the sample showsunderperformance relative to the REIT index used as a benchmark.While there has been no previous research on the long-runperformance of REITs following a debt issue, this result issomewhat different from that found for other companies. Using abalance-sheet method to determine private placements of debt,Dichev and Piotroski (1999) found no evidence of abnormalperformance after a private placement. The findings of Dichev andPiotroski (1999) for private placements differ from those of Spiessand Affleck-Graves (1999) for announced public debt issues. Spiessand Affleck-Graves (1999) found significant underperformance aftera public debt issue and proposed that the underperformancesuggests that debt issues are signals of overvaluation similar toequity issues. Thus, the results for REITs are consistent with what

No initial marketresponse

Negative long-runreturns

Shareholder wealth effects of private placements of debt made by REITs

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 3 NO . 4 P P 3 0 5 – 3 1 4 309

has been found for public debt issues. Again, this may be due to thefact that benefits from added monitoring associated with a privatedebt placement are being eliminated by the desire of management tosimply grow the size of the REIT.Interestingly, the one-year prior placement adjusted return was

also negative and significant. This suggests that REIT managers arenot trying to time the debt issue to take advantage of positivemarket conditions for their stocks; however, there may be a timingissue at hand. Support for this can be found by looking at thepattern of REIT issuances. REITs are much more likely to issueequity than to issue debt. Ghosh et al. (1997) showed that from 1992to 1997, REITs issued equity three times more frequently than debtand raised twice as much capital using equity as debt. Howton et al.(2000) found no evidence of prior underperformance by REITs thatmade seasoned equity issues. Therefore, it appears that REITmanagers issue equity when market valuations are favourable andissue debt when market valuations are unfavourable. This againsupports the idea that the private placement of debt is undertakensimply to increase the size of the REIT.In order to examine the robustness of the documented

underperformance following private placements of debt, the authorsseparated the sample by issue date and firm characteristic todetermine if the underperformance was isolated in certain timeperiods or in certain types of firms. Table 3 contains long-run, post-placement, holding period returns categorised by year. Placementsacross all years are associated with underperformance relative to theREIT index for both one-year and three-year adjusted holdingperiod returns. There does not appear to be any time-series patternin the underperformance.

Equity vs debt

Table 2: Long-run holding period returns for REITs that made debt private placements and for an index of REITs that did not make

private placements. Adjusted holding period returns are defined as the difference between the placing REIT returns and the REIT index

returns. A sign test is used to determine the significance of the adjusted returns. There are 114 private placements of debt in the sample.

Summary statistics (in %)———————————————————————————————————————————————————————————

Return measure Minimum Maximum Median Mean Standard Percentagedeviation negative

Placing REITs

One-year prior placement –46.15 63.41 14.12 13.62 19.33

One-year post-placement –84.59 77.53 9.56 8.15 19.70

Three-year post-placement –94.32 186.50 45.10 43.10 42.81

Non-placing REIT index

One-year prior placement –17.88 47.04 23.12 19.61 17.37

One-year post-placement –14.30 43.42 15.45 14.35 16.28

Three-year post-placement 18.74 191.41 64.89 71.24 28.77

Adjusted returns

One-year prior placement –37.65 31.32 –7.42 –5.98 13.23 67.86*

One-year post-placement –76.47 59.75 –5.67 –6.20 16.11 68.42*

Three-year post-placement –146.23 79.89 –17.63 –28.06 40.66 79.82*

* indicates significance at the 0.05 level

Higgins, Howton and Howton

# HENRY S T EWART PUB L I C A T I ONS 1473 ^ 189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VOL . 3 NO . 4 P P 3 0 5 – 3 1 4310

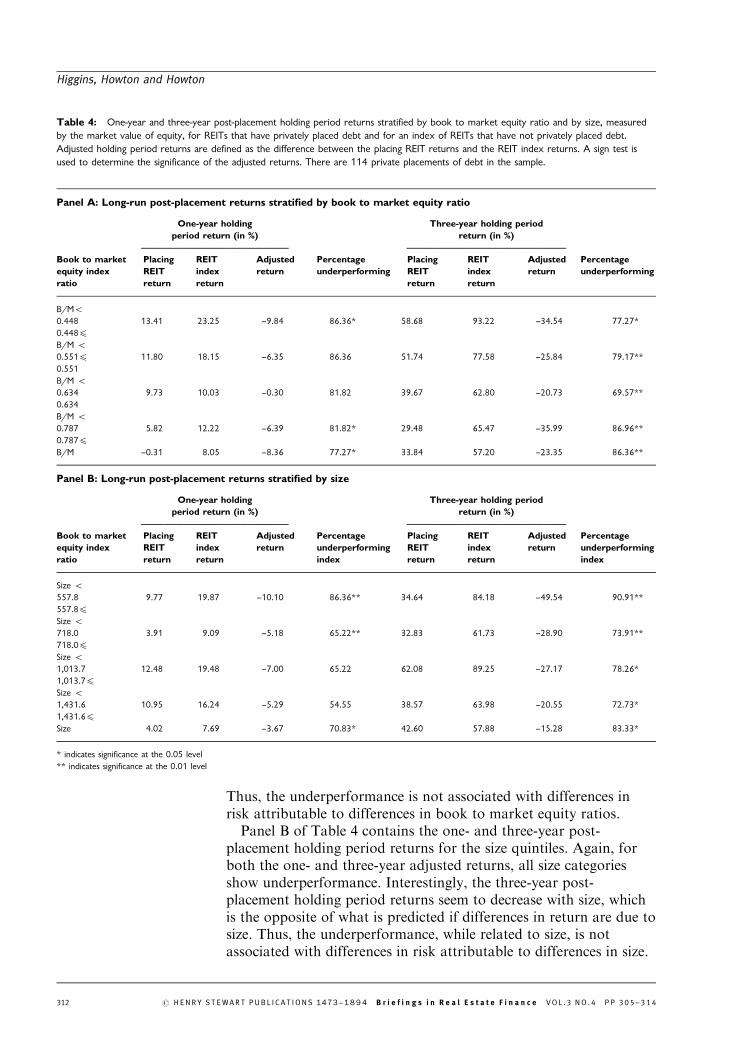

One potential explanation of the observed underperformance isthat the placing firms are less risky than the firms in the REIT indexbeing used as a benchmark. While it is unlikely that the placingREITs are less risky, on average, than the non-placing REITS in thebenchmark, the authors stratified both the sample and the REITindex based on the risk proxies described by Fama and French(1993). Following Fama and French (1993), they used the book tomarket equity ratio and the market value of equity as risk proxies,and stratified the sample into quintiles based on these two riskproxies. Fama and French (1993) found that high book to marketfirms outperform low book to market firms. If REITs that privatelyplace debt are generally firms with strong previous performance, theplacing REITs might have low book to market ratios, and theobserved under-performance might be an artefact of the Fama andFrench findings. Also, Fama and French (1993) showed that size hasa significant role in explaining cross-sectional differences in returns.Specifically, size and return are inversely related. If the observedunder-performance is an artefact of size, the smallest size quintilesshould not have any underperformance, and the level ofunderperformance should be increasing as size increases.Panel A of Table 4 contains a summary of the one- and three-year

post-placement holding period returns for the book to marketquintiles. For both the one-year and three-year adjusted holdingperiod, returns of all the book to market quintiles showunderperformance. Three of the one-year adjusted returns aresignificant and all of the three-year adjusted returns are significant.In looking across the book to market categories, there does notappear to be any discernable pattern in the underperformance.

Robustness checks

Table 3: One-year and three-year post-placement holding period returns, separated by year, for REITs that have privately placed debt, and

for an index of REITs that have not privately placed debt. Adjusted holding period returns are defined as the difference between the placing

REIT returns and the REIT index returns. A sign test is used to determine the significance of the adjusted returns. There are 114 private

placements of debt in the sample.

One-year holding Three-year holding periodperiod return (in %) return (in %)

————————————————————————— ———————————————————————————

Year Sample Placing REIT Adjusted Percentage Placing REIT Adjusted Percentagesize REIT index return underperforming REIT index return underperforming

return return index return return index

1993 3 –10.60 16.61 –27.20 100.00 61.84 132.38 –70.54 100.00

1994 2 13.72 15.81 –2.08 50.00 72.46 99.09 –26.62 50.00

1995 13 16.50 26.82 –10.31 100.00** 64.89 106.66 –41.78 84.62*

1996 16 21.57 38.66 –17.10 93.75** 68.73 107.37 –38.64 87.50**

1997 30 6.65 8.13 –1.48 56.67 28.99 66.88 –37.89 93.33**

1998 23 –6.21 –5.04 –1.16 47.83 33.03 52.23 –19.20 78.26*

1999 15 2.75 6.40 –3.65 66.67* 50.83 60.68 –9.85 73.33

2000 12 19.99 27.30 –7.31 75.00 30.64 41.07 –10.44 66.67**

2001 3 13.63 18.94 –5.31 66.67 - - - -

* indicates significance at the 0.05 level

** indicates significance at the 0.01 level

Shareholder wealth effects of private placements of debt made by REITs

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 3 NO . 4 P P 3 0 5 – 3 1 4 311

Thus, the underperformance is not associated with differences inrisk attributable to differences in book to market equity ratios.Panel B of Table 4 contains the one- and three-year post-

placement holding period returns for the size quintiles. Again, forboth the one- and three-year adjusted returns, all size categoriesshow underperformance. Interestingly, the three-year post-placement holding period returns seem to decrease with size, whichis the opposite of what is predicted if differences in return are due tosize. Thus, the underperformance, while related to size, is notassociated with differences in risk attributable to differences in size.

Table 4: One-year and three-year post-placement holding period returns stratified by book to market equity ratio and by size, measured

by the market value of equity, for REITs that have privately placed debt and for an index of REITs that have not privately placed debt.

Adjusted holding period returns are defined as the difference between the placing REIT returns and the REIT index returns. A sign test is

used to determine the significance of the adjusted returns. There are 114 private placements of debt in the sample.

Panel A: Long-run post-placement returns stratified by book to market equity ratio

One-year holding Three-year holding periodperiod return (in %) return (in %)

————————————————————————— ———————————————————————————

Book to market Placing REIT Adjusted Percentage Placing REIT Adjusted Percentageequity index REIT index return underperforming REIT index return underperformingratio return return return return

B/M50.448 13.41 23.25 –9.84 86.36* 58.68 93.22 –34.54 77.27*

0.4484B/M 50.5514 11.80 18.15 –6.35 86.36 51.74 77.58 –25.84 79.17**

0.551

B/M 50.634 9.73 10.03 –0.30 81.82 39.67 62.80 –20.73 69.57**

0.634

B/M 50.787 5.82 12.22 –6.39 81.82* 29.48 65.47 –35.99 86.96**

0.7874B/M –0.31 8.05 –8.36 77.27* 33.84 57.20 –23.35 86.36**

Panel B: Long-run post-placement returns stratified by size

One-year holding Three-year holding periodperiod return (in %) return (in %)

————————————————————————— ———————————————————————————

Book to market Placing REIT Adjusted Percentage Placing REIT Adjusted Percentageequity index REIT index return underperforming REIT index return underperformingratio return return index return return index

Size 5557.8 9.77 19.87 –10.10 86.36** 34.64 84.18 –49.54 90.91**

557.84Size 5718.0 3.91 9.09 –5.18 65.22** 32.83 61.73 –28.90 73.91**

718.04Size 51,013.7 12.48 19.48 –7.00 65.22 62.08 89.25 –27.17 78.26*

1,013.74Size 51,431.6 10.95 16.24 –5.29 54.55 38.57 63.98 –20.55 72.73*

1,431.64Size 4.02 7.69 –3.67 70.83* 42.60 57.88 –15.28 83.33*

* indicates significance at the 0.05 level

** indicates significance at the 0.01 level

Higgins, Howton and Howton

# HENRY S T EWART PUB L I C A T I ONS 1473 ^ 189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VOL . 3 NO . 4 P P 3 0 5 – 3 1 4312

CONCLUSIONSThis study examined private placements of debt made by REITs.The authors obtained a sample of 114 private placements made overthe time period from 1993–2001. They calculated both short-run andlong-run abnormal returns associated with the placements. Long-run adjusted holding period returns were calculated using an indexof non-placing REIT returns. They controlled for time trends, bookto market equity effects and size effects when calculating the long-run adjusted returns.They found no significant market response at the time of the

placement. This result is consistent with the findings of Howton andHowton (2001) for public debt issues made by REITs. Given theinformation-intensive nature of private debt placements, however,the authors were surprised to find that the reaction was not positive.They attribute the non-positive result to the ambiguity surroundingthe use of the funds raised in the placement. Following Capozza andSeguin (2000), they suggest that their results are consistent withREIT managers issuing debt in order to grow the size of the REITwith the ultimate goal being the maximisation of compensation.The authors found support for the compensation maximisation

hypothesis when looking at long-run returns. They found significantunderperformance relative to a non-placing REIT index after theplacement for one year and three years post-placement. Thisindicates that the REIT did not benefit from the additionalmonitoring by external debt holders. Also, this shows that the REITmanagers did not make effective use of the funds raised in theplacement. The documented underperformance was not sensitive totime and was not associated with the Fama and French (1993) riskfactors. Interestingly, they found that the REITs that privatelyplaced debt were also underperforming in the year prior to the debtissue. This leads the authors to conclude that the managers were nottrying to time markets when making the placement. This lendsfurther support to the argument that the managers simply issue thedebt in order to grow the asset size of the REIT.

ReferencesBrown, S. J. and Warner, J. B. (1985) ‘Using daily stock returns: The case of event studies’,

Journal of Financial Economics, 14, 1, 3–31.

Capozza, D. R. and Seguin, P. (2000) ‘Debt, agency, and management contracts in REITs: The

external advisor puzzle’, Journal of Real Estate Finance and Economics, 20, 2, 91–116.

Carey, M., Prowse, S., Rea, J. and Udell, G. (1994) ‘The economics of the private placement

market’, Federal Reserve Bulletin, 80, 5–6.

Chan, S., Leung, W. and Wang, K. (1998) ‘Institutional investment in REITs: Evidence and

implications’, Journal of Real Estate Research, 16, 3, 357–374.

Dichev, I. D. and Piotroski, J. D. (1999) ‘The performance of long-run stock returns following

issues of public and private debt’, Journal of Business Finance and Accounting, 26, 9/10,

1103–1132.

Fama, E. and French, K. (1993) ‘Common risk factors in the returns on stocks and bonds’,

Journal of Financial Economics, 33, 1, 3–56.

Friday, H. S., Sirmans, G. S. and Conover, M. (1999) ‘Ownership structure and the value of

the firm: The case of REITs’, Journal of Real Estate Research, 17, 1/2, 71–90.

Support forcompensationmaximisationhypothesis

Shareholder wealth effects of private placements of debt made by REITs

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 3 NO . 4 P P 3 0 5 – 3 1 4 313

Ghosh, C., Nag, R. and Sirmans, C. F. (1997) ‘Financing choice by equity REITs in the

1990s’, Real Estate Finance, 26, 3, 41–50.

Howe, J. S. and Shilling, J. D. (1988) ‘Capital structure theory and REIT security offerings’,

Journal of Finance, 43, 4, 983–993.

Howton, S. D. and Howton, S. W. (2001) ‘The wealth effects of REIT straight debt issues’,

Journal of Real Estate Portfolio Management, 7, 2, 151–157.

Howton, S. D., Howton, S. W. and Friday, H. S. (2000) ‘Long run underperformance in

REITs following seasoned equity offerings’, Journal of Real Estate Portfolio

Management, 6, 4, 355–363.

Loughran, T. and Ritter, J. R. (1995) ‘The new issues puzzle’, Journal of Finance, 50, 1, 23–51.

Spiess, D. K. and Affleck-Graves, J. (1995) ‘Underperformance in long-run stock returns

following seasoned equity offerings’, Journal of Financial Economics, 38, 3, 243–267.

Spiess, D. K. and Affleck-Graves, J. (1999) ‘The long-run performance of stock returns

following debt offerings’, Journal of Financial Economics, 54, 1, 45–73.

Notes1. Both Loughran and Ritter (1995) and Spiess and Affleck-Graves (1995) use matching

samples to calculate adjusted returns. Since their samples are over several industries,

however, there are more matching firm candidates, and the problem of having one firm

match several sample firms is less severe than in the present authors’ case. Due to the

industry-specific nature of the authors’ sample, they believe that an index of non-placing

REITs is an appropriate benchmark for measuring long-run REIT returns.

2. Wilcoxon rank-sum tests were also used to test the significance of the underperformance.

The significance levels were the same using either test. Sign test results are reported

because the sign test makes no assumptions regarding the nature of the underlying

distribution of the abnormal returns.

Higgins, Howton and Howton

# HENRY S T EWART PUB L I C A T I ONS 1473 ^ 189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VOL . 3 NO . 4 P P 3 0 5 – 3 1 4314