SHAPING A SUSTAINABLE FUTURE - Flybe · Aircraft Aircraft

43

FLYBE GROUP PLC Copyright 2017 SHAPING A SUSTAINABLE FUTURE Full Year Results – Year ended 31 March 2017 Analyst and Investor Presentation 8 June 2017

-

Upload

trinhnguyet -

Category

Documents

-

view

220 -

download

1

Transcript of SHAPING A SUSTAINABLE FUTURE - Flybe · Aircraft Aircraft

FLYBE GROUP PLC Copyright 2017

SHAPING A SUSTAINABLE FUTURE Full Year Results – Year ended 31 March 2017

Analyst and Investor Presentation 8 June 2017

FLYBE GROUP PLC Copyright 2017 2

Agenda Introduction

Christine Ourmieres-Widener Financial Review

Philip de Klerk Performance Review and Priorities

Christine Ourmieres-Widener Summary and Q&A

FLYBE GROUP PLC Copyright 2017

Introduction

PASSIONATE ABOUT THE AIRLINE INDUSTRY TRULY PASSIONATE ABOUT FLYBE

“Tremendous opportunities for Flybe to connect and engage with communities and to establish a

reputation for excellence in serving our customers”

FLYBE GROUP PLC Copyright 2017

Financial review

FLYBE GROUP PLC Copyright 2017

2016/17 Group financial summary Revenue

13.4% increase in Group revenue

Metrics per seat 3.6% reduction in passenger revenue 5.2% reduction in costs including fuel (constant currency) 2.0% increase in costs including fuel

Profit & loss £(6.7)m adjusted loss before tax1

£(19.9)m reported loss before tax £(26.7)m reported loss after tax

Robust balance sheet £153.5m net assets, £(64.0)m net debt and £124.3m total cash

1. Adjusted profit before tax is before revaluation gains or losses on USD aircraft loans

FLYBE GROUP PLC Copyright 2017

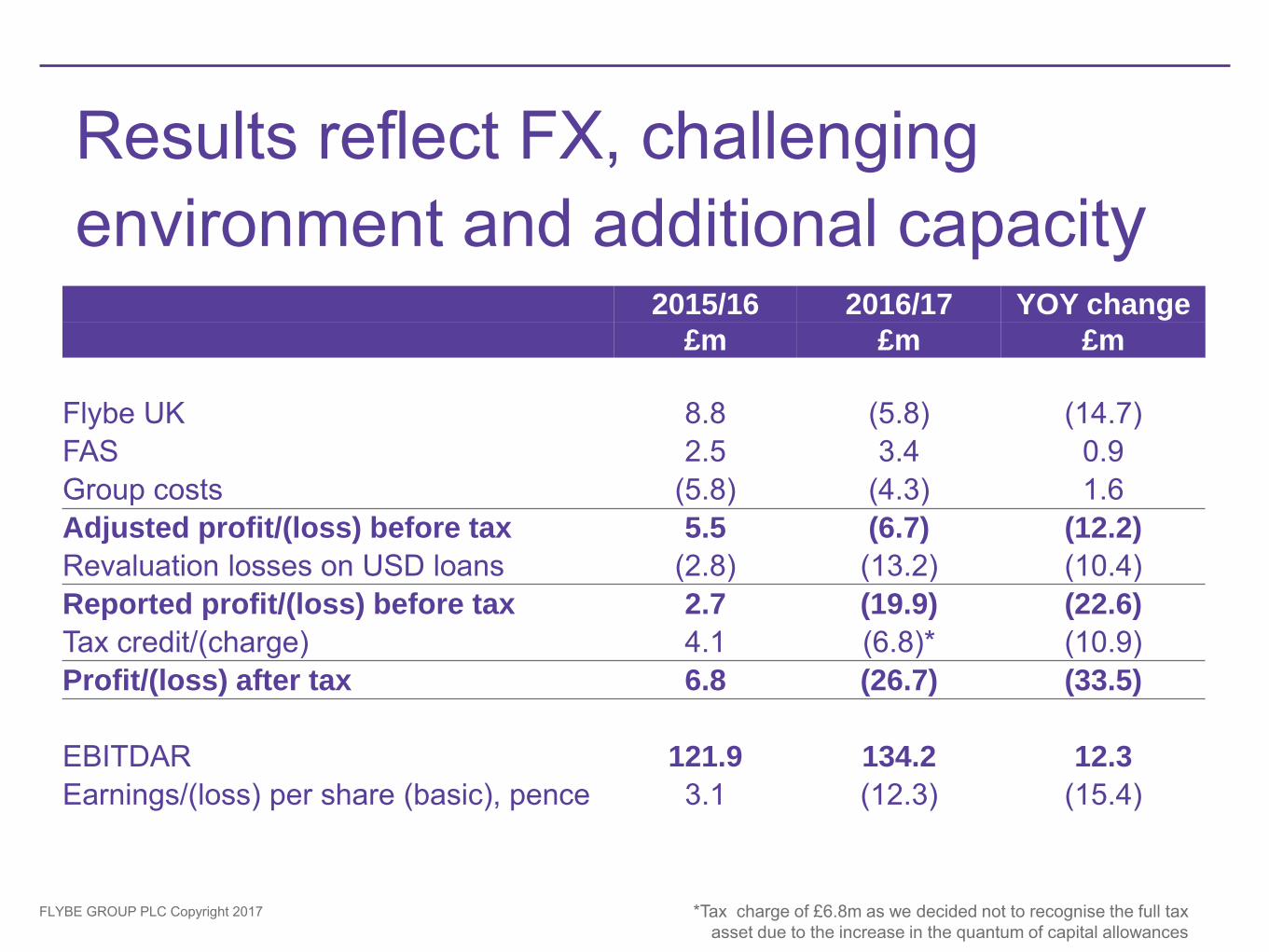

Results reflect FX, challenging environment and additional capacity

2015/16 2016/17 YOY change

£m £m £m

Flybe UK 8.8 (5.8) (14.7) FAS 2.5 3.4 0.9 Group costs (5.8) (4.3) 1.6 Adjusted profit/(loss) before tax 5.5 (6.7) (12.2)

Revaluation losses on USD loans (2.8) (13.2) (10.4) Reported profit/(loss) before tax 2.7 (19.9) (22.6)

Tax credit/(charge) 4.1 (6.8)* (10.9) Profit/(loss) after tax 6.8 (26.7) (33.5)

EBITDAR 121.9 134.2 12.3

Earnings/(loss) per share (basic), pence 3.1 (12.3) (15.4)

*Tax charge of £6.8m as we decided not to recognise the full tax asset due to the increase in the quantum of capital allowances

FLYBE GROUP PLC Copyright 2017

Group revenue increased by 13.4%

2015/16

£m

2016/17

£m

YOY %

change

Passenger revenue 571.7 619.3 8.3%

White Label revenue 13.9 33.0

Revenue from other activities 15.4 23.3

FAS revenue (third party) 22.8 31.8

Revenue 623.8 707.4 13.4%

FLYBE GROUP PLC Copyright 2017

Stable yield but lower load factor

2015/16 2016/17 YOY % change

Seats, m 11.3 12.7 12.3%

Passengers, m 8.2 8.8 7.6%

Load factor, % 72.6% 69.6% -3.0ppts

Average passenger sector length, km 468.1 503.1 7.5%

Passenger Yield 70.23 70.20 0.0%

£ per seat 2015/16 2016/17 YOY % change

Passenger revenue 50.64 48.84 -3.6% Other revenue, incl. White Label 2.59 4.44 Total Flybe UK revenue 53.23 53.28 0.1%

FLYBE GROUP PLC Copyright 2017

Cost per seat up 2%, but 5.2% reduction at constant currency

52.67

56.67 56.39

53.74

(4.00)

(0.46)

(0.47) 0.50

0.85

(0.14)2.65

50

51

52

53

54

55

56

57

58

2015/16Op. cost per

seat

FX impact 2015/16Constantcurrency

StaffCosts

Airport, En-route & Ground

Ops

Aircraft RentalCharges

OtherOperating

gains/(losses)

Other 2016/17Op. costexcl. fuelsaving

Fuel 2016/17Op.

cost per seat

£m

Mainly E195 flying

Fuel price saving

Hedging benefits

More owned aircraft

Change in FX rates YoY

Mostly increase in White Label staff costs

Including maintenance cost

FLYBE GROUP PLC Copyright 2017

FLYBE GROUP PLC Copyright 2017

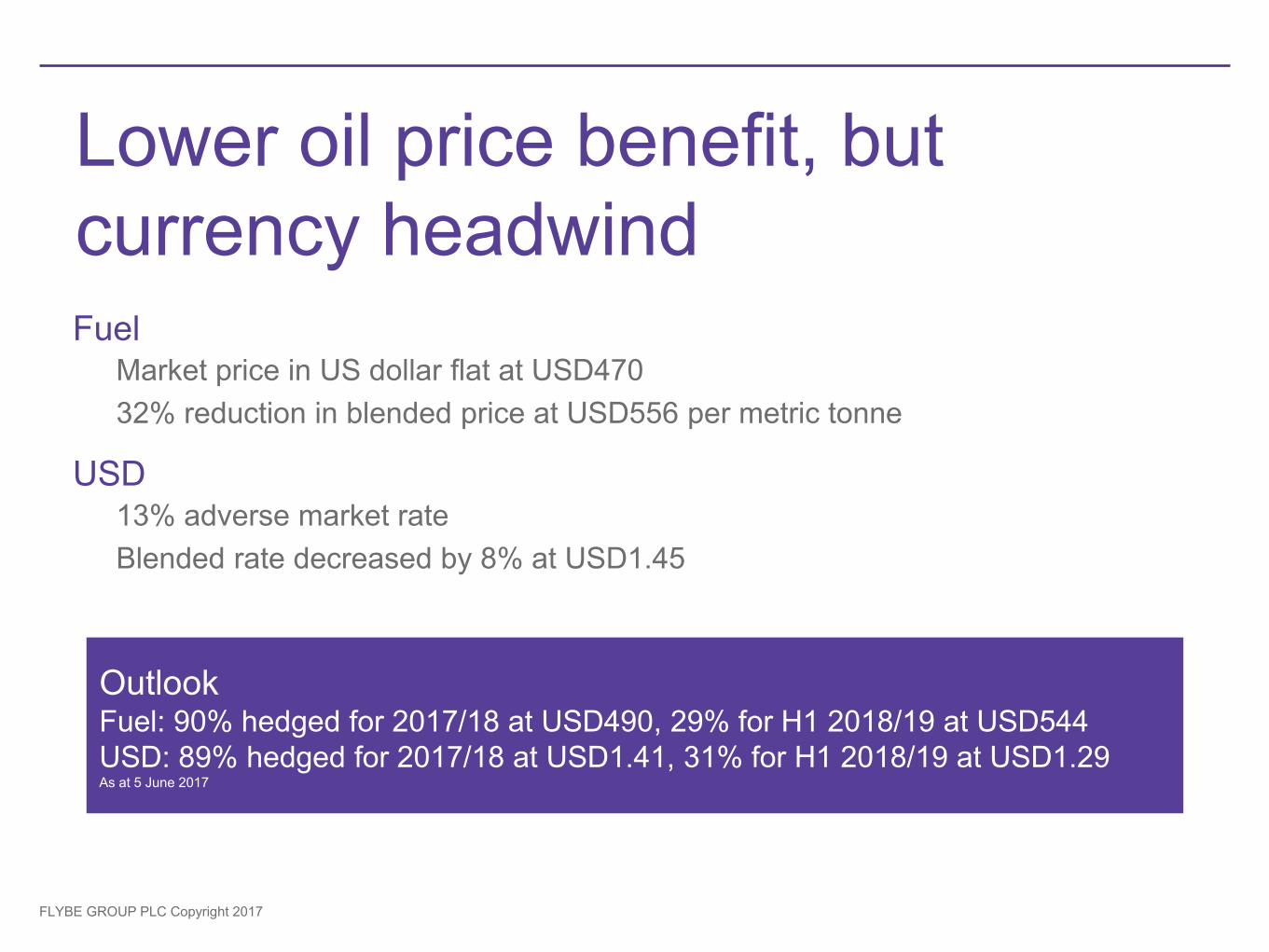

Outlook Fuel: 90% hedged for 2017/18 at USD490, 29% for H1 2018/19 at USD544 USD: 89% hedged for 2017/18 at USD1.41, 31% for H1 2018/19 at USD1.29 As at 5 June 2017

Fuel Market price in US dollar flat at USD470 32% reduction in blended price at USD556 per metric tonne

USD 13% adverse market rate Blended rate decreased by 8% at USD1.45

Lower oil price benefit, but currency headwind

FLYBE GROUP PLC Copyright 2017

£124.3m total cash at 31st March 2017 (31st March 2016: £171.4m) £(64.0)m of net debt (31st March 2016 net funds: £62.2m) £153.5m net assets (31st March 2016: £154.2m)

Pension scheme closed Triennial actuarial valuation completed; £12m deficit agreed over 12 years Deficit recovery contributions increase from £0.5m to £0.83m p.a. IAS19 pension deficit increased to £20.8m

Capital restructure implemented to increase distributable reserves

Balance sheet

FLYBE GROUP PLC Copyright 2017

45

50

55

60

65

70

75

80

85

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16Fe

b-16

Mar

-16

Apr

-16

May

-16

Jun-

16Ju

l-16

Aug

-16

Sep

-16

Oct

-16

Nov

-16

Dec

-16

Jan-

17Fe

b-17

Mar

-17

Apr

-17

May

-17

No

. o

f A

ircra

ft

E195 Surplus AC Republic Deliveries

Fleet peaked in May 2017 2015/16 2016/17

Excludes ATRs

2014/15

FLYBE GROUP PLC Copyright 2017

Took ownership of 10 used Q400 aircraft, out of operating lease for c£98m

C£8m p.a. saving from increasing the number of owned aircraft and reducing the number of leased aircraft over the last two years

Added flexibility to manage fleet size

As at 31ST March Total Aircraft* % Owned

2015/16 70 24%

2016/17 78 35%

2017/18 74 36%

2018/19 69 43%

2019/20 65 48%

Fewer aircraft and reduced cost

assumes all lease aircraft returned at end of lease and no new purchases off lease, ATRs excluded

FLYBE GROUP PLC Copyright 2017

Net debt of £(64.0)m

62.357.0

(64.0)

34.9 (25.1)

(7.7)(107.8)

(7.4)

(13.2)

(80.0)

(60.0)

(40.0)

(20.0)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Net funds 31 Mar2016

Operating cash MaintenanceCapex & Into

service

Intangible andother Capex

Net Financing Underlying netfunds

Aircraft & EnginePurchases

FX on USD loans Net funds 31 Mar2017

£m

FLYBE GROUP PLC Copyright 2017

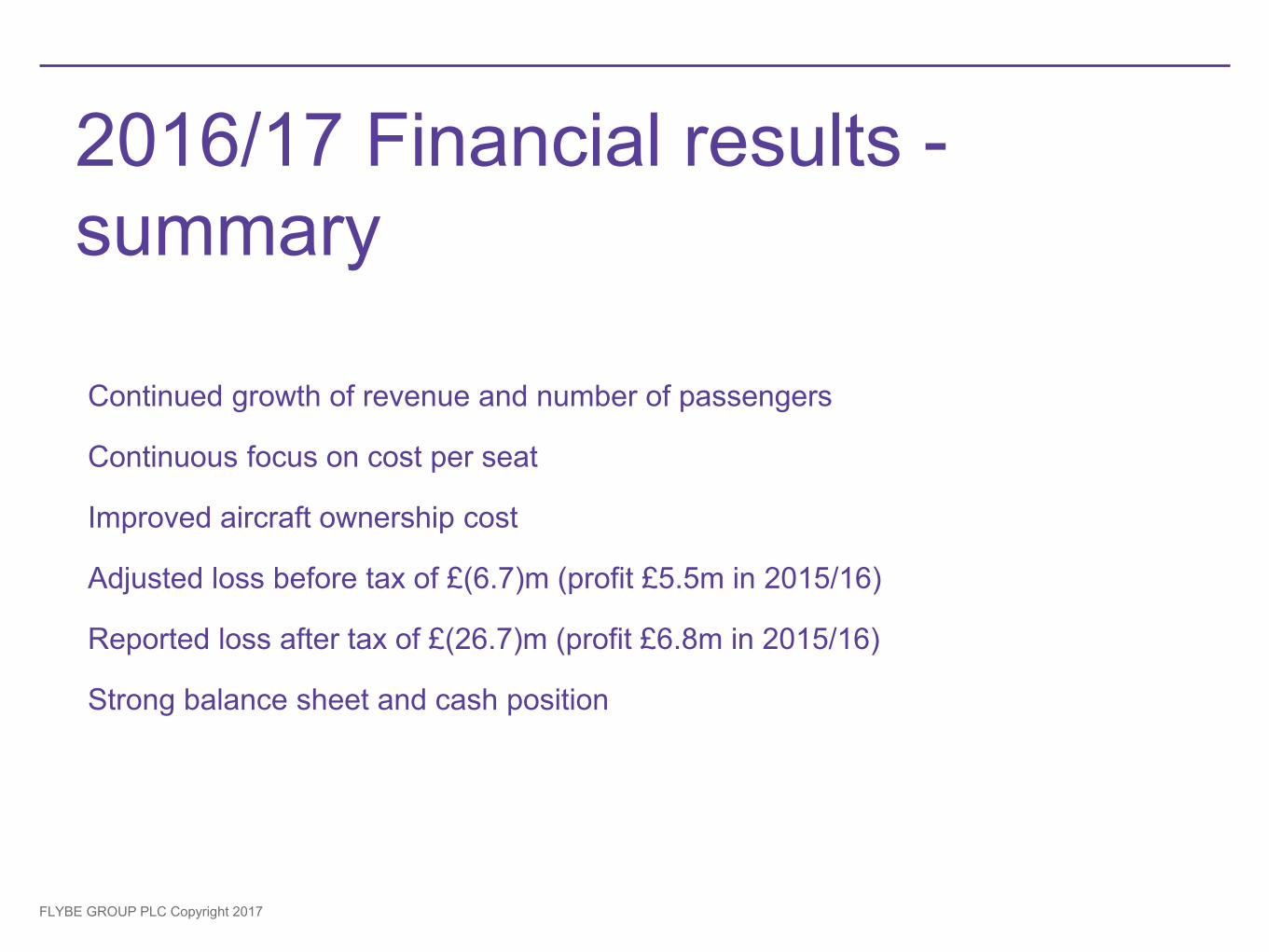

Continued growth of revenue and number of passengers

Continuous focus on cost per seat

Improved aircraft ownership cost

Adjusted loss before tax of £(6.7)m (profit £5.5m in 2015/16)

Reported loss after tax of £(26.7)m (profit £6.8m in 2015/16)

Strong balance sheet and cash position

2016/17 Financial results - summary

FLYBE GROUP PLC FLYBE GROUP PLC

2016/17 Performance and Priorities 2017/18

FLYBE GROUP PLC FLYBE GROUP PLC

2016/17 Performance

FLYBE GROUP PLC Copyright 2017 18

2016/17 Performance Serving more customers with a stable yield 33 new routes in 2016/17, 13 routes cancelled 199 Total routes // 64 airports // 152,064 flights 8.8m passengers and 12.3% more capacity Revenue growth, lower load factor and stable yield Reliability mixed 82.7% OTP arrivals, down from 85.4% 99.0% TDR, up from 98.8% Aircraft utilisation improved 6h 54m per day, up by 5% Employees 3 year pay deal 5% share deal, aligning interests with shareholders

FLYBE GROUP PLC Copyright 2017 19

Flybe diagnosis A sound business model for the airline With other business opportunities Capacity control to enable a demand led business A strong brand but strategy should be focused on the UK However …. More focus on operational and organisational excellence More customer centric Enhanced digital platform Creating better shareholder value

FLYBE GROUP PLC Copyright 2017

Sound business model

A leading regional airline serving UK regions

FLYBE GROUP PLC Copyright 2017

34 42

78 88

118

156

180 189

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

SAAB340 ATR42 ATR72/Q400 E175 E195 A319 A320 B737

Thinner routes can only be served economically by regional aircraft Flybe analysis of minimum route thickness by aircraft type for a daily frequency

Note: Analysis assumes: 70% Load Factor on SAAB340, ATR, Q400, E175 and E195, 89% on A319 and A320 and 85% on B737-800 Flight frequency at 3 rotations a day, 7 days per week. No. in bars are avg. seats per aircraft type (Source: Flybe analysis)

Competitors Main Area

Flybe Sweet Spot

Flybe Partners

FLYBE GROUP PLC Copyright 2017 22

Other business opportunities

White Label

A long term partnership with SAS Brussels airline contract expires in October Selective investment in profitable opportunity

MRO

Retain it and integrate it A400M contract very successful Prime role in supporting Flybe

Training Academy Becoming a profit centre

FLYBE GROUP PLC FLYBE GROUP PLC

Priorities 2017/18

© DAVID SCHILCHER 2016

FLYBE GROUP PLC Copyright 2017

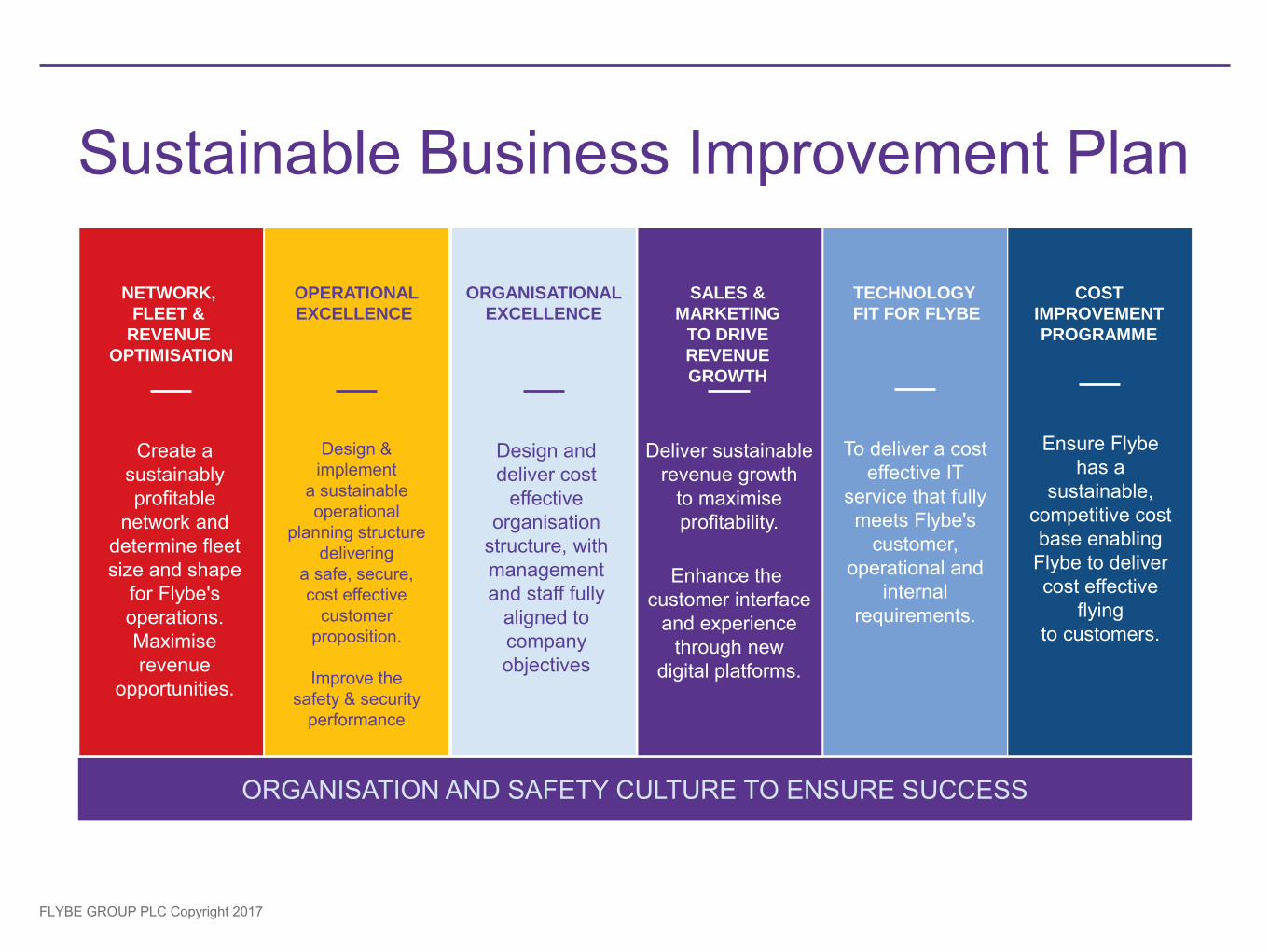

Sustainable Business Improvement Plan

SALES &

MARKETING

TO DRIVE

REVENUE

GROWTH

Deliver sustainable revenue growth

to maximise profitability.

Enhance the customer interface

and experience through new

digital platforms.

NETWORK,

FLEET &

REVENUE

OPTIMISATION

Create a sustainably profitable

network and determine fleet size and shape

for Flybe's operations. Maximise revenue

opportunities.

OPERATIONAL

EXCELLENCE

Design & implement

a sustainable operational

planning structure delivering

a safe, secure, cost effective

customer proposition.

Improve the

safety & security performance

ORGANISATIONAL

EXCELLENCE

Design and deliver cost

effective organisation

structure, with management and staff fully

aligned to company objectives

TECHNOLOGY

FIT FOR FLYBE

To deliver a cost effective IT

service that fully meets Flybe's

customer, operational and

internal requirements.

COST

IMPROVEMENT

PROGRAMME

Ensure Flybe has a

sustainable, competitive cost base enabling

Flybe to deliver cost effective

flying to customers.

ORGANISATION AND SAFETY CULTURE TO ENSURE SUCCESS

FLYBE GROUP PLC Copyright 2017

Taking control of our fleet

8 78 2 (6)

(3) (1) (4)70

74(5)

3 69

1 65

0

10

20

30

40

50

60

70

80

90

2015/16Fleet

Q400delivery

2016/17Fleet

Q400delivery

Q400expire

2017/18Fleet

Q400expire

E195expire

E175delivery

2018/19Fleet

Q400expire

E195expire

E175delivery

2019/20Fleet

24% 35% 36% 43% 48%

Excludes 5 ATRs deployed in Stockholm for SAS White Label and assuming all leases returned at the end of lease and no additional purchases off lease % shows the owned aircraft in our fleet

48%

84

Expectations unchanged from H1

FLYBE GROUP PLC Copyright 2017 26

Focus on UK

Concentrate on routes starting and finishing in UK Cancelled intra European routes for W17 Brexit risk & opportunity Balanced focus on leisure travelers

FLYBE GROUP PLC Copyright 2017

Codeshare / Franchise

FLYBE GROUP PLC Copyright 2017 28

Flybe loves Scotland 31% of total passengers Eastern Airways partnership Loganair no longer to be part of the Flybe Franchise 2 New routes launched to LHR 79 Flights per week from Scotland to London Flybe will remain Scotland’s best airline

FLYBE GROUP PLC Copyright 2017 29

Operational excellence Improved reliability

Additional modifications to Q400 aircraft Well planned and executed maintenance Improved third party management Integrated maintenance organisation

Improved on time performance

Better availability of spare aircraft Better availability of standby crew Working closer with airport partners

Implement new systems

AMOS Electronic Flight Bag

FLYBE GROUP PLC Copyright 2017 30

Organisational excellence

Design Flybe’s Future Organisation

Leaner organisation, more responsibility Less duplication, more accountability Consistent with fleet & network strategy and

company priorities Develop Flybe’s culture

Embed refreshed values Strengthen safety, security and compliance

culture Reward based on performance

FLYBE GROUP PLC Copyright 2017 31

Flybe must be better at digital

Over 80% of booking via the web Non standard & Lack of flexibility Poor customer experience

Limited customer communication Limited customer data Restricted upselling opportunity

A 3 year roadmap A great opportunity to improve revenues and decrease costs

FLYBE GROUP PLC Copyright 2017

The new digital platform will support the customer life cycle

FLYBE GROUP PLC FLYBE GROUP PLC

Outlook and summary

FLYBE GROUP PLC Copyright 2017 34

H1 2017/18 Outlook H1 forward sales as of 5th June

2017: 2.7% capacity increase vs. prior year 45% of capacity sold vs. 44% prior year 2.6% increase in yields helped by timing of

Easter 4.6% increase in passenger revenue per seat

We expect c4% capacity reduction in Winter

FLYBE GROUP PLC Copyright 2017

We have slowed capacity growth, leading to improved load factor

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Q1 16/17 Q2 16/17 Q3 16/17 Q4 16/17 Q1 17/18

Capacity growth (seats)

Load Factor

YoY

chan

ge

Capacity

expected

to reduce

in H2

FLYBE GROUP PLC Copyright 2017 -10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Q1 16/17 Q2 16/17 Q3 16/17 Q4 16/17 Q1 17/18

Cost per seatIncl. fuel

Revenue per seatCost per seatExcl. fuel

Revenue per seat is recovering, and benefit of oil price annualises

YoY

cha

nge Benefit of lower Oil prices

FLYBE GROUP PLC Copyright 2017

Summary Business resilient in tough market Growth in capacity, passenger volume and revenue Reduction in unit cost Partnerships

Control of capacity growth Capacity will be reduced over the coming years Optimise route network Enhance reliability and efficiency Digital & customer centric Digitalise Improve marketing and sales Serving our customers better will create value for

shareholders

FLYBE GROUP PLC Copyright 2017

Q&A

FLYBE GROUP PLC Copyright 2017

Legal disclaimer

FLYBE GROUP PLC Copyright 2017

Appendix

Fleet evolution

The fleet peaks in May 2017 before Flybe starts to return end-of-lease aircraft to its lessors in Autumn 2017. Six Bombardier Q400 aircraft will be handed back later in 2017 at, or slightly ahead of, lease expiry. The number of owned aircraft moved from 17 to 27 year-on-year with owned aircraft now representing 32.5% (2015/16: 23.0%) of the fleet . (Excluding ATRs 34.6% of the fleet is owned)

Bombardier Q400 turboprop 58 2 -6 54

Embraer E175 regional jet 11 - - 11

Embraer E195 regional jet 9 - - 9

ATR72 turboprop (SAS contract) 5 - - 5

Total 83 2 -6 79

Held on operating lease 56 2 -6 52

Owned 27 - - 27

Total 83 2 -6 79

Total seats in fleet 6,904 156 -468 6,592

Average seats per aircraft 83.2 83.4

At 31st

March

2017

Aircraft

Handbacks

At 31st

March

2018

Aircraft

Deliveries

Group Balance Sheet £m March 2017 March 2016 YOY change

£m £m £m

Aircraft 287.3 192.3 95.0

Other property, plant and equipment 21.8 21.4 0.4

Intangibles 11.9 13.3 (1.4)

Net (debt)/funds (64.0) 62.2 (126.2)

Derivative financial instruments 24.5 (9.9) 34.4

Other working capital - net (117.2) (123.5) 6.3

Deferred taxation (0.6) 11.3 (11.9)

Defined benefit pension scheme deficit (20.8) (15.3) (5.5)

Other non-current assets and liabilities 10.6 2.4 8.2

Net assets and shareholders' funds 153.5 154.2 (0.7)

Total cash of £124m

171.5

124.3

(25.1)

(7.4)

58.2

34.9

(107.8)

0.00

50.00

100.00

150.00

200.00

250.00

Opening Cash 31 Mar2016

Operating cash Maintenance Capex Intangible Capex Financing activities Aircraft & EnginePurchases

Closing cash 31 Mar2017

£m