Shadow Banking1

26

Shadow Banking Sainatth Wagh Sameer Sanghavi Parvez Rangwalla

Transcript of Shadow Banking1

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 1/26

Shadow Banking

Sainatth Wagh

Sameer Sanghavi

Parvez Rangwalla

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 2/26

Agenda

Shadow Credit Intermediation

Shadow Credit Intermediation Process

The shadow banking system

Funding shadow banking system

Backstopping shadow banking system

Conclusions

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 3/26

Shadow Banking ??

System of non-financial institutions that borrow money in

short term and then use the same in the long term assets.

Shadow banking systems are able to avoid standard banking

regulations. The concept is to make the credit cheaper for the ultimate

borrower and more available.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 4/26

Shadow Banks V/S Traditional Banks

Shadow Banking Traditional Banking

1) Unregulated 1) Regulated

2) No government protection 2) Government protection

3) Credit Intermediation through 3) Under one single roof

chain of NBFC

4) Capital reserve is not mandatory 4) Capital Reserve mandatory as

per stipulated by RBI

5) Participants are savers, borrowers and 5) Participants are savers, banks

NBFC. and borrowers.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 5/26

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 6/26

Shadow Credit Intermediation

Savers

MoneyMarket

ShadowBanks

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 7/26

Contd..

Involves following characteristics:

Credit Transformation

Maturity Transformation Liquidity Transformation

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 8/26

Shadow Credit Process

Seven steps which are performed:

1) Loan Origination: applying for new loan.

2) Loan Warehousing: the borrowing of the funds bylender on short term basis keeping mortgage as

collateral

3) ABS issuance: done by the brokers

4) ABS warehousing: facilitated through trading booksand is funded through repurchase agreement (repo)

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 9/26

Contd..

5) ABS CDO Issuance: Pooling of funds into ABS CDO is

done through dealers.

6) ABS Intermediation: performed by limited purpose

finance companies which are funded in variety of

ways.

7) Wholesale funding: the funding of all above activities

is considered to be part of wholesale funding

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 10/26

Shadow banking.avi.flv

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 11/26

The Shadow Banking System

Govt. Sponsored Shadow Banking System

Internal Shadow Banking System

External Shadow Banking System

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 12/26

Govt. Sponsored Shadow Banking

System

Not Funded using public deposits

Capital Market

Techniques

a. Loan ware housing

b. Credit risk Transfer & Insurance

c. Originate to distribute securitizationd. Maturity

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 13/26

Evolution in Nature of Lending

No dependence on Bank

Network of Bank,BD,AMC

Bank are involved at origination level

Lending became capital efficient, fee rich ,

high Roe for originators, structures and ABS

investors

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 14/26

Internal Shadow Banking - EU

Step (2) Loan Warehousing

Step (4) ABS Warehousing

Step (6) ABS Intermediation

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 15/26

External Shadow Banking

The credit intermediation process of diversified

broker-dealers

The credit intermediation process of independent,

non-bank specialist intermediaries

The credit puts provided by private credit risk

repositories.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 16/26

External shadow banking

Global shadow banking

Origination , warehousing, securitization US

Funding & structuring & maturitytransformation UK,EU various offshore

centres.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 17/26

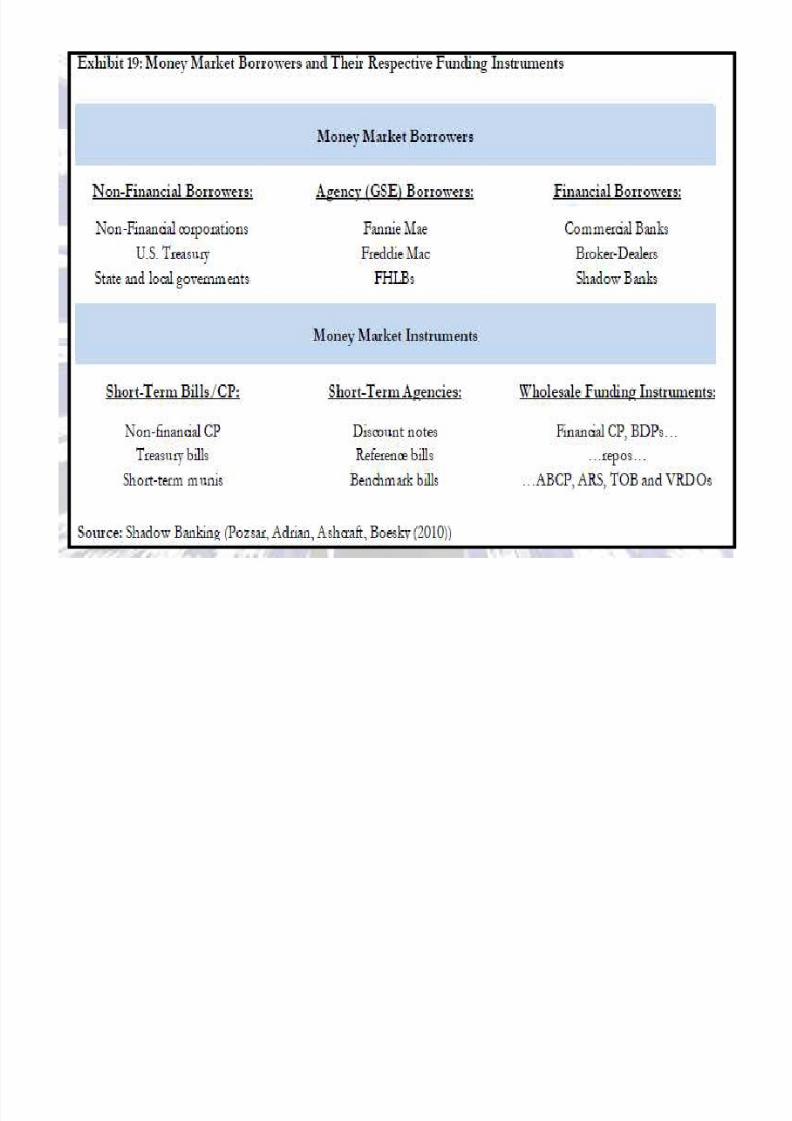

Funding the Shadow Banking System:

Funding the Shadow Banking System:

Traditional Banking system relies on the deposits gathered through

Bank branches for funding.

The shadow banking system relies on the issuance of money

market instruments (such as CP, ABCP& Repo) to money market

investors (such as money market mutual fund), as well as the

issuance of longer-term, medium-term notes (MTNs) & public bonds

to medium to long term investor such as pension funds, insurance

companies etc.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 18/26

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 19/26

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 20/26

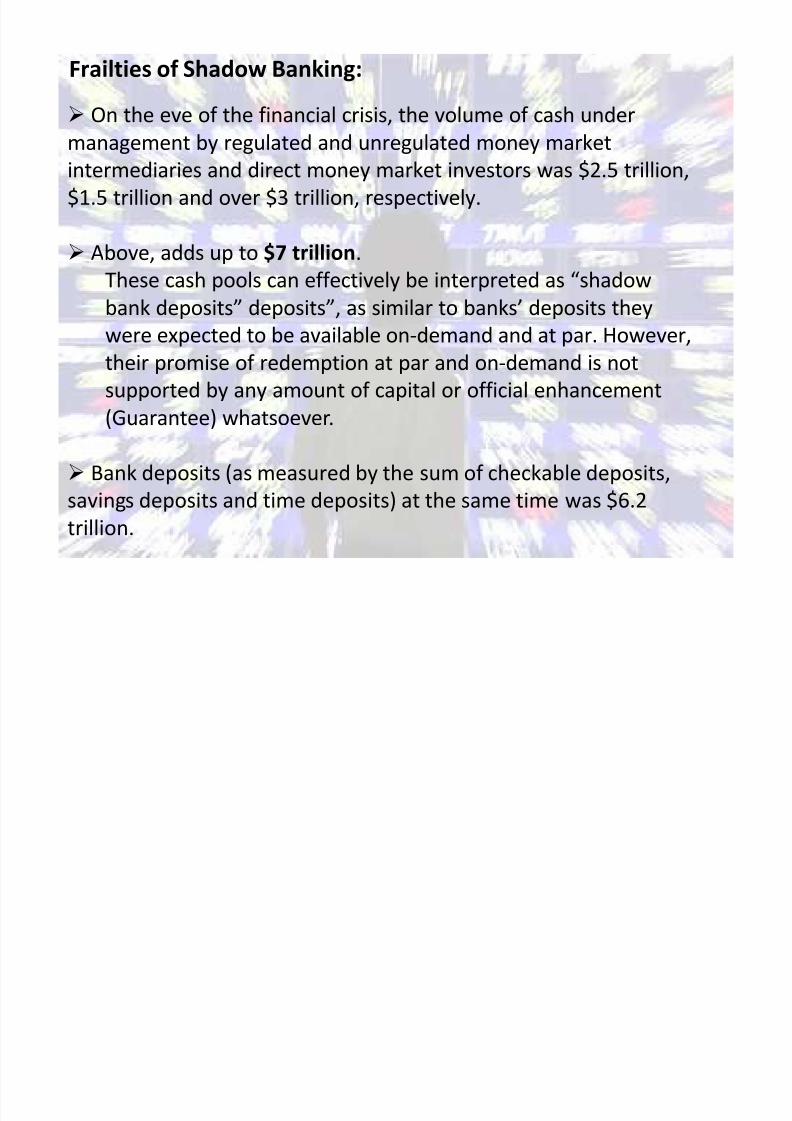

On the eve of the financial crisis, the volume of cash under

management by regulated and unregulated money marketintermediaries and direct money market investors was $2.5 trillion,

$1.5 trillion and over $3 trillion, respectively.

Above, adds up to $7 trillion.

These cash pools can effectively be interpreted as shadowbank deposits deposits, as similar to banks deposits they

were expected to be available on-demand and at par. However,

their promise of redemption at par and on-demand is not

supported by any amount of capital or official enhancement

(Guarantee) whatsoever.

Bank deposits (as measured by the sum of checkable deposits,

savings deposits and time deposits) at the same time was $6.2

trillion.

Frailties of Shadow Banking:

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 21/26

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 22/26

Post 2008 Financial Crisis:

Term asset backed loan facility (TALF):

It was program created by the U.S. Federal Reserve in

November, 2008 to boost consumer spending to help jumpstart

the economy.

This is accomplished through the issuance of asset-backedsecurities. The collateral for these securities is made up of

student, personal auto and credit card loans.

Backing for these loans comes from the (up to) $1 trillion

provided by the New York Federal Reserve Bank.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 23/26

Conclusions:

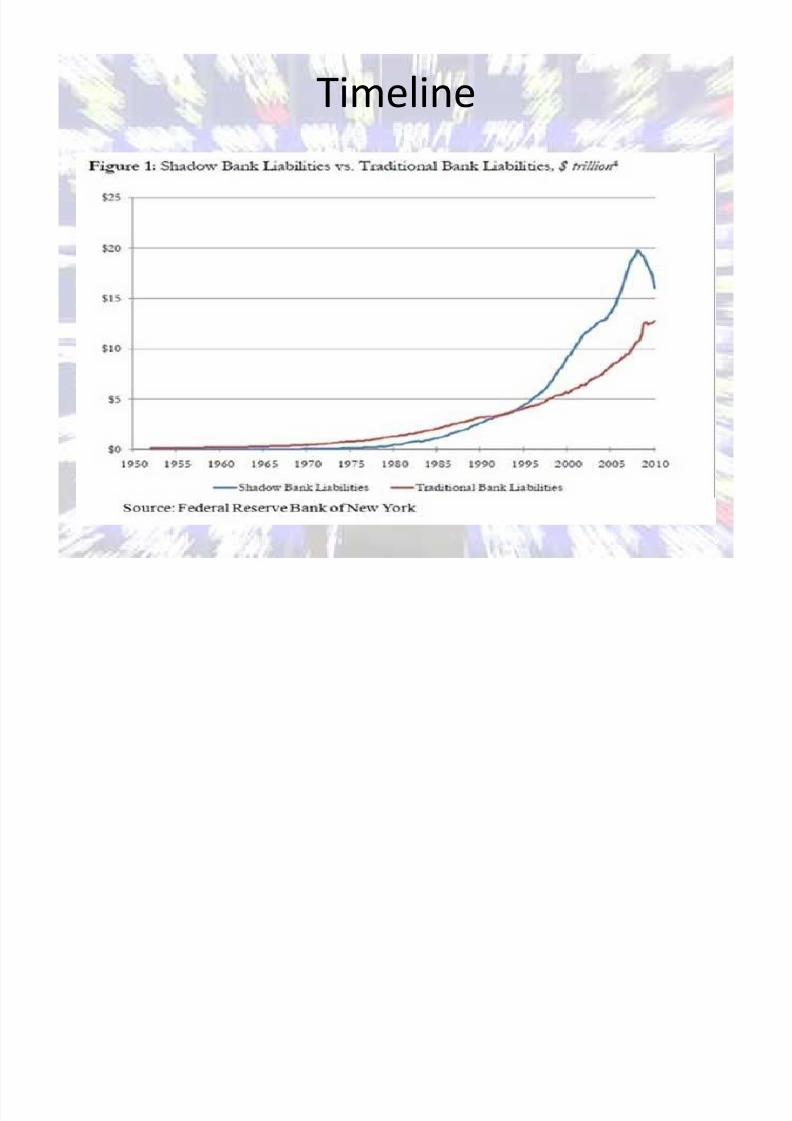

1.The volume of credit intermediated by the shadow banking system is just

as large as the volume of credit intermediated by the traditional banking

system.

At the eve of the financial crisis, the volume of credit intermediated by the

shadow banking system was close to $20 trillion, or nearly twice as large as

the volume of credit intermediated by the traditional banking system at

roughly $11 trillion. Today, the comparable figures are $16 and $13 trillion,

respectively.

2. The collapse of the shadow banking system is not unprecedented in the

context of the bank runs of the 19th century:

The collapse of the shadow banking system during the global financial crisis

of 2007-09 has many parallels to the bank runs of the 19th century. For one,

we can argue that todays traditional banking system used to be aninherently fragile shadow banking system until its activities became

enhanced with official liquidity and credit puts by the Federal Reserve and

FDIC, respectively. Before the creation of these public backstops, bank runs

were frequent.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 24/26

3. Private sector balance sheets will always fail at internalizing systemic risk.

The official sector will always have to step in to help :

Collapse of the balance sheet capacity of one institution impacts the balance

sheet capacity of similar institutions (performing the same functional step)through the revaluation of asset prices. Balance sheet shrinkage to perform

certain functions of the shadow credit intermediation process might in turn clog

the arteries of the shadow banking system, impede the asset flows in it, and, by

extension, the flow of credit to households and businesses.

4. The shadow banking system was temporarily brought into thedaylight of public liquidity and liability insurance, but was then pushed back into the

shadows:

The sum total of the emergency liquidity facilities, lending programs and large-

scale asset purchases by the Federal Reserve, and the guarantee schemes of the

FDIC and U.S. Treasury during the financial crisis provided a near-complete

backstop of the shadow banking system. This backstop meant that the shadowbanking system temporarily stepped out of the shadows, into the sunlight of

the officially enhanced part of the financial system, just as the traditional

banking system.

Upon the expiry of these facilities, however, the system reverted back into the

shadows once again, operating without explicit official enhancements.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 25/26

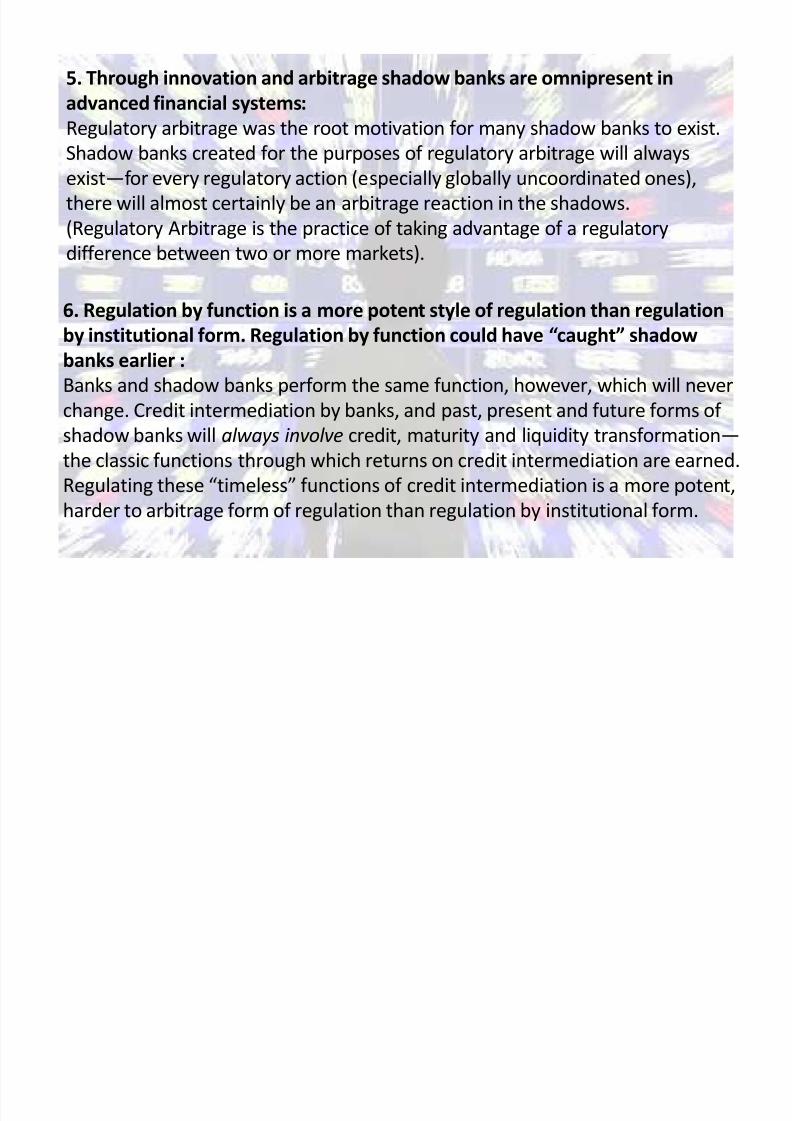

5. Through innovation and arbitrage shadow banks are omnipresent in

advanced financial systems:

Regulatory arbitrage was the root motivation for many shadow banks to exist.

Shadow banks created for the purposes of regulatory arbitrage will always

existfor every regulatory action (especially globally uncoordinated ones),

there will almost certainly be an arbitrage reaction in the shadows.

(Regulatory Arbitrage is the practice of taking advantage of a regulatory

difference between two or more markets).

6. Regulation by function is a more potent style of regulation than regulation

by institutional form. Regulation by function could have caught shadow

banks earlier :

Banks and shadow banks perform the same function, however, which will never

change. Credit intermediation by banks, and past, present and future forms of shadow banks will always involve credit, maturity and liquidity transformation

the classic functions through which returns on credit intermediation are earned.

Regulating these timeless functions of credit intermediation is a more potent,

harder to arbitrage form of regulation than regulation by institutional form.

8/9/2019 Shadow Banking1

http://slidepdf.com/reader/full/shadow-banking1 26/26