Setting Reserves Under Heightened Government and...

53

presents Sales and Use Tax Reserve Strategies presents Setting Reserves Under Heightened Government and Audit Scrutiny A Live 110-Minute Teleconference/Webinar with Interactive Q&A Today's panel features: Vytenis Kirvelaitis, Senior Manager, SALT Group, Grant Thornton, Chicago Mark Nachbar, Principal, Ryan, Downers Grove, Ill. Robert Schulte, Vice President of Product Management, Taxcient Inc., San Diego Thursday, May 27, 2010 The conference begins at: 1 pm Eastern 12 pm Central 11 am Mountain 10 am Pacific You can access the audio portion of the conference on the telephone or by using your computer's speakers. Please refer to the dial in/ log in instructions emailed to registrations.

Transcript of Setting Reserves Under Heightened Government and...

presents

Sales and Use Tax Reserve Strategies

presents

Setting Reserves Under Heightened Government and Audit Scrutiny

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Today's panel features:Vytenis Kirvelaitis, Senior Manager, SALT Group, Grant Thornton, Chicago

Mark Nachbar, Principal, Ryan, Downers Grove, Ill.Robert Schulte, Vice President of Product Management, Taxcient Inc., San Diego

Thursday, May 27, 2010

The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific

You can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

For Continuing Education purposes, gplease let us know how many people are listening at your location by g y y

• closing the notification box • and typing in the chat box your• and typing in the chat box your

company name and the number of attendeesattendees.

• Then click the blue icon beside the box to sendto send.

For live event only.For live event only.

• If the sound quality is not satisfactory• If the sound quality is not satisfactory and you are listening via your computer speakers please dial 1-866-258-2056speakers, please dial 1 866 258 2056 and enter your PIN when prompted. Otherwise, please send us a chat or e-, pmail [email protected] so we can address the problem.

• If you dialed in and have any difficulties during the call, press *0 for assistance.

Sales And Use Tax ReserveSales And Use Tax Reserve Strategies Webinar

May 27, 2010

Mark Nachbar, [email protected]

Robert Schulte, Taxcient Inc. [email protected]

Vytenis Kirvelaitis, Grant [email protected] @g

Today’s ProgramToday s Program

Initial Decisions About A Sales And Use Tax Reserve Slides 6-7 (Mark Nachbar)

Background On Role Of FAS 5, FAS 109 And FIN 48 Slides 8-31

In Establishing A Reserve (Mark Nachbar)

Lessons From Hypothetical Taxpayer Scenarios Slides 32-53

(Robert Schulte and Vytenis Kirvelaitis)

5

I iti l D i i Ab t AInitial Decisions About A Sales And Use Tax

Reserve

Mark Nachbar, RyanMark Nachbar, Ryan

Identifying Use Tax Uncertaintiesy g

1. Flow-chart the existing purchasing cycle2. Review procedures for determining whether a tax

inquiry is made when an item is purchased and inquiry is made when an item is purchased and there is no tax on the invoice

3. Review procedures for determining whether tax is due when items are transferred within or between companies

4. Review materials used for taxability determinations (e.g. matrix, rate tables)

5. Review procedures for reporting and remitting tax due

If any of these procedures are deficient, a reserve may need to be established

7

Identifying Sales Tax Uncertainties

1. Flow-chart the existing sales cycle2. Review procedures for determining whether sales

tax needs to be chargedi. Nexusii. Item/service soldiii. Exemption certificate

3. Review materials used for taxability decisions (e.g. matrix, rate tables)

4. Review procedures for collecting, reporting and remitting collections and tax due

If any of these procedures are deficient, a reserve may need to be established

8

Background On Role Of gFAS 5, FAS 109 And FIN

48 I E t bli hi A48 In Establishing A Reserve

Mark Nachbar, RyanMark Nachbar, Ryan

Statement Of Financial Accounting Standards No. 5 (FAS 5)( )

FAS 5 addresses recording and reporting contingencies for reporting contingencies for financial accounting purposes. It is the principal standard governing the principal standard governing recording and reporting sales and use tax uncertaintiesuse tax uncertainties.

10

What Standard Determines A Reserve?

• FASB Statement No.109 (FAS 109) establishes th fi i l ti li i t b d t the financial accounting policies to be used to report the effects of income taxes resulting from an enterprises activities.p

• Financial Interpretation No. 48 (FIN 48) interprets FAS 109 and gives guidelines for taxpayers to identify and measure benefits taxpayers to identify and measure benefits associated with tax positions and disclose any uncertainties about federal or state income tax positions in financial statements.

11

FIN 48 - Recognitiong

• Standard for recognitionUnder FIN 48 a taxpayer only has to recognize – Under FIN 48, a taxpayer only has to recognize a tax position in the financial statements if it will “more likely than not” be sustained on audit, appeals, litigation or other resolution, based on pp , g ,its technical merits.• “More likely than not” means a greater than

50% probability.U d FIN 48 th i ti f dit – Under FIN 48, there is an assumption of audit detection.• Taxpayer must assume:

The position will be examined by relevant – The position will be examined by relevant taxing authority, and

– Taxing authority has “full knowledge of all relevant information ”

12

relevant information.

FIN 48 - Measurement

• Measurement standard–Under FIN 48, a tax position that Under FIN 48, a tax position that

“more likely than not” be upheld means measuring at the largest benefit that is greater than 50% likely to be realized upon ultimate settlementsettlement.

13

FIN 48 - Disclosure

• FIN 48 insists on disclosing “risks and uncertainties that might substantially affect numbers in financial statements ” statements.” – It includes the supplemental disclosure

requirements of Statement of Position 94-6– New disclosure requirements include:

• Reconciling unrecognized tax benefits• Unrecognized tax benefits that, if recognized, g , g ,

would affect the effective tax rate• Interest and penalties recognized in

statement of operations and statement of pfinancial position

• Description of open tax years

14

FAS 5, Accounting For Contingenciesg g

• Statement of Financial Accounting Standards N 5 (FAS 5) di ti t No. 5 (FAS 5) covers recording or reporting tax and other contingencies, for financial accounting purposes.

• A contingency means an existing condition, situation or set of circumstances that involves uncertainty about possible gain or lossuncertainty about possible gain or loss.

• Uncollected sales tax or unremitted use tax lt i ti f hi h i results in a contingency for which a reserve is

required under FAS 5. In addition, collected but unremitted sales taxes would also be covered under FAS 5

15

covered under FAS 5.

Treatment Of Loss Contingenciesg

• Possible ways to address loss contingencies under FAS 5 include:

– Accruing: Recognizing an expense and liability in the financial statementsliability in the financial statements

– Disclosing: Providing a financial statement footnote that identifies the contingency

– Neither accruing nor disclosing a loss contingency

16

Recognizing Loss Contingenciesg g g

• Estimated loss contingencies must • Estimated loss contingencies must be accrued if the following two conditions are met:conditions are met:

1. The loss is probable2 The amount of the loss can be 2. The amount of the loss can be

reasonably estimated

17

Recognizing Loss Contingencies (Cont.)g g g ( )

• FAS 5 utilizes a range of likelihoods that future events will impair or lose an asset or incurred liability.

– Probable: Usually interpreted as “highly likely” that future events will occur

– Reasonably possible: Higher probability than remote but still less than likely

Remote: Slight probability of future events– Remote: Slight probability of future events

• Taxpayers are allowed, under FAS 5, to consider audit detection in recognizing a loss contingency.g g g y

• However, the risk of audit cannot be used to determine whether the loss contingency can be estimated or to calculate the appropriate reserve

18

calculate the appropriate reserve.

Measuring Loss Contingenciesg g

• Under FAS 5, the amount of a loss must be reasonably estimated to must be reasonably estimated to accrue the loss contingency.

19

Disclosing Loss Contingenciesg g

• FAS 5 requires that a contingency be • FAS 5 requires that a contingency be disclosed, even lacking a reserve, “when there is at least a reasonable when there is at least a reasonable possibility that a loss or an additional loss may be incurred.”y

• A contingency must be disclosed if necessary to make sure financial ystatements do not mislead.

20

FAS 5 Decision-Making Processg

21

Key Distinctions Under FAS 5 And FAS 109y

• Recognition– FAS 5: Consider audit detection– FAS 109: Assume audit detection

• MeasurementFAS 5: Reasonable estimate– FAS 5: Reasonable estimate

– FAS 109: Largest amount of benefit that has a greater than 50% probability of being sustainedsustained

• Disclosure– FAS 5: When necessary to ensure that

fi i l t t t t i l difinancial statements are not misleading– FAS 109: Disclose risks and uncertainties

that could significantly affect amounts t d i th fi i l t t t

22

reported in the financial statements

FASB Project – Disclosure Of Certain Loss ContingenciesContingencies

• Objective – Enhance disclosure requirementsrequirements–Qualitative and quantitative

InformationInformation• Nature of loss • Potential timing for settlement• Potential timing for settlement• Magnitude

23

Disclosure Principlesp

• Once a contingency is identified, the initial nature and potential magnitude h ld b d l d

gshould be disclosed.

• As more information becomes available, it should also be disclosedit should also be disclosed

• Disclosures may be aggregated for similar contingencies to make them understandable and not too detailedunderstandable and not too detailed.

• If disclosures are aggregated, the basis for aggregation should be explained.

24

Disclosure Threshold

• Disclosure of remote loss contingencies may be necessary based on the following factors:

Th t ti l ff t th tit ’ ti – The potential effect on the entity’s operations – The cost to the entity for defending its contentions – The amount of efforts and resources management

may have to devote to resolve the contingencymay have to devote to resolve the contingency– When assessing the materiality of loss contingencies

to determine whether disclosure is required, the entity should not consider the possibility of recoveries from insurance or other indemnification from insurance or other indemnification arrangements.

25

Quantitative DisclosuresQ

• Publicly available quantitative information• An estimate of the possible loss or range of p g

loss and the amount accrued• Other non-privileged information that would

be relevant to financial statement-users to be relevant to financial statement users to enable them to understand and/or assess the possible loss

• Information about possible recoveries from • Information about possible recoveries from insurance and other sources

26

Qualitative Disclosures (Cont.)Q ( )

• Qualitative information to enable users to understand the nature and risks of a contingency or group of contingencies

– During early stages, disclosure should include the contentions of h

g gthe parties.

– In subsequent reporting periods, disclosure should be more extensive, including the likelihood and magnitude of loss.

– An entity should also disclose the anticipated timing of, or the next steps in the resolution of individually material next steps in, the resolution of individually material contingencies.

• The disclosure should provide information from publicly available sources such as court records.

• When disclosure is provided on an aggregated basis, an When disclosure is provided on an aggregated basis, an entity should disclose the basis for aggregation.

27

Tabular Reconciliation

• A public entity should disclose reconciliations by class, in a tabular format:

– The carrying amounts of the accruals at the beginning and end of the period

– Increases for new loss contingencies recognized during the period – Increases for changes in estimates for loss contingencies

recognized in prior periods recognized in prior periods – Decreases for changes in estimates for loss contingencies

recognized in prior periods – Decreases for cash payments or other forms of settlements during

the period p• An entity should describe the significant activity in the

reconciliation and disclose the line items in the statement of financial position in which recognized loss contingencies are included.

28

Scopep

• Disclosures should apply to all entities except that the tabular entities, except that the tabular reconciliation is not required for non-public entitiespublic entities.

• Initial draft released 6/5/08Comments received by 8/8/08• Comments received by 8/8/08

29

Public Comments

• The majority of respondents did not express j y p psupport for the exposure draft. – Would be too difficult to implement – Force entities to waive attorney-client privilege Force entities to waive attorney client privilege – Hinder a reporting entity’s ability to defend itself in

litigation proceedings

• Users generally supported the exposure draft, Users generally supported the exposure draft, with several suggestions that the Board should require even more disclosure.

30

Status

• Re-exposure draftIssue the Re exposure draft in the – Issue the Re-exposure draft in the second quarter of 2010. The re-exposure Draft will have a 30-day p ycomment period.

• Effective date–Fiscal years ending after Dec. 15,

2010

31

L FLessons From Hypothetical Taxpayer yp p y

Scenarios

Robert Schulte, Taxcient Inc.Robert Schulte, Taxcient Inc.Vytenis Kirvelaitis, Grant Thornton

Case Study: Application Of FAS 5y pp

Sales and use tax reserves have come under more scrutiny as a result of the

f h b lenactment of the Sarbanes-Oxley Act and pressure on state and local jurisdictions to raise revenue. Senior jmanagement has become aware of internal controls to understand what is in each reserve, and sales/use taxes in each reserve, and sales/use taxes have greater visibility before the C-suite now.

33

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Case Study

Corporation A

Corporation A is a publicly traded nationwide Corporation A is a publicly traded nationwide manufacturer and retailer of consumer electronics and software with $51 billion of annual revenue. The company has both retail p yand online distribution channels. In 2008, the Tax Department was charged with developing and implementing new policies and procedures for dealing with sales and use tax procedures for dealing with sales and use tax due to large FAS 5 contingencies and audit assessments.

34

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Step 1—Fact Finding:Step 1 Fact Finding:Review historical SUT auditsR i l l t tReview legal structureReview business strategy/plansExamine sales policies/behaviorExamine purchase policies/behaviorExamine purchase policies/behaviorExamine inventory movementsE i G/L l ti

35

Examine G/L accrual postings

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Historical sales/use audit findingsHistorical sales/use audit findingsPrimary assessment/exposure areas

Disallowed exempt sales- Disallowed exempt sales- Product taxability errors- Use tax on inventory movesUse tax on inventory moves- Use tax on consumable supplies

It was determined that the errors were caused due to a lack of a consistent policy, employee turnover rates and misunderstanding of tax law.

36

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Review legal structureReview legal structureOrganization chartInter-relationships between entitiesInter relationships between entitiesLocations and tax registrations“Doing business”g

It was determined that the company has a relatively complex legal structure, is situated throughout the U.S. complex legal structure, is situated throughout the U.S. with a significant amount of inter-relationships particularly on the sales side of the business.

37

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Review business strategy/plans10-K and annual reportRecent press releasesIndustry trends and activity

It was determined that the company has consistently grown, particularly with its online business. It is focused on customer service and branding The industry is on customer service and branding. The industry is continuing to experience consolidation and tremendous pricing pressures for the certain segments of the business.

38

Case Study: Application Of FAS 5 (Cont.)

Review sales behavior

y pp ( )

Retail (POS) salesInternet (consumer) salesInternet (consumer) salesOrder entry ERP sales

It was determined that both taxable and exempt sales were made through all three channels without collecting mandated documentation, creating the disallowed exempt sales exposure.

39

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Review product taxabilityReview product taxabilityProduct linesB dl d d tBundled productsDelivery model

It was determined that the product lines needed pto be re-categorized and maintained to reflect current taxing legislation and to account for modern delivery mechanisms (i e internet

40

modern delivery mechanisms. (i.e. internet delivery of intangibles/services).

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Review purchase behaviorReview purchase behaviorPurchase order processA/P t ti l iA/P transaction analysisThree-way matching controls

It was determined that the PO process did not paccount for use tax properly, A/P transactions followed a improper uniform use tax rule, and controls were out of date

41

controls were out of date.

Case Study: Application Of FAS 5 (Cont.)y pp ( )

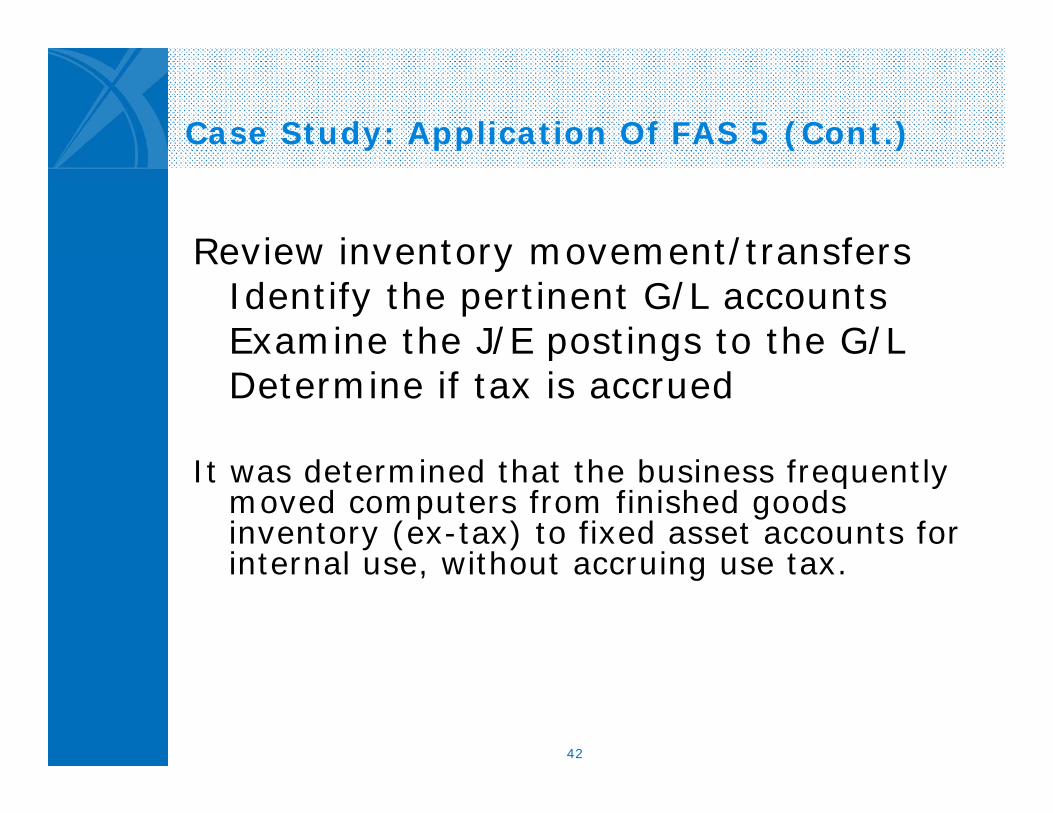

Review inventory movement/transfersReview inventory movement/transfersIdentify the pertinent G/L accountsExamine the J/E postings to the G/L/ p g /Determine if tax is accrued

fIt was determined that the business frequently moved computers from finished goods inventory (ex-tax) to fixed asset accounts for internal use without accruing use taxinternal use, without accruing use tax.

42

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Review G/L sales/use tax accrualsReview G/L sales/use tax accrualsAd-hoc postingsReversal of tax accrualsReversal of tax accrualsAutomated credit memo postings

It was determined that entries were made to the wrong jurisdiction sub-accounts, improper reversals for credits were used, and credit memo postings did not reference original

43

e o pos gs d d o e e e e o g atransaction.

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Step 2— Action planAnalyze potential exposure and

develop a standard sales and use tax policy based on findings, including implementation of imp o ed polic th o gh the improved policy through the company across functional boundaries boundaries.

44

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Build electronic audit modelIn cooperation with IT resources

1. Created sales transactions report queryp q y2. Created an A/P transactions report query3. Created an inventory transactions query4. Created a G/L sales/use accruals query

An Access DB was created to import these An Access DB was created to import these reports and perform detailed analysis through the use of queries and macros to determine monthly exposure and corrective actions

45

monthly exposure and corrective actions.

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Create taxability matrixExported product listing from ERPCreated spreadsheet matrix for all products, services and bundlesDetermined taxability based on nexus, product/service delivery methodproduct/service, delivery methodDetermined special and/or partial statutory exemptionsstatutory exemptionsCited statutes and regulations for determining taxability

46

g y

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Nexus determination modelExported business locations, outlets, physical locations from ERPInterviewed operations personnel and reviewed sales policies

It was determined that, due to the retail store locations, that nexus had been created in every U.S. taxing jurisdiction.

47

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Step 3—ImplementationStep 3 Implementation- Used electronic audit results to highlight exposure areashighlight exposure areas- Exemption certificate software- Product taxability maintenance- Inventory use tax modely- A/P use tax model

48

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Electronic audit resultsElectronic audit results- Extracted all transactions to customers with no tax on invoicecustomers with no tax on invoice

- Product-based exemption?- Customer-based exemption?

- Created customer-based exemption list to gather exemption certificate documentation

49

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Electronic audit results (Cont )Electronic audit results (Cont.)- Extracted all transactions from specific G/L inventory accounts specific G/L inventory accounts representing inventory transfers

C t d d h t f - Created spreadsheet for calculating the accruals for i t t finventory transfers

50

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Electronic audit results (Cont )Electronic audit results (Cont.)- Extracted all transactions from specific G/L fixed asset and supply specific G/L fixed asset and supply accounts with use tax implications

C t d d h t f - Created spreadsheet for calculating the accruals for fixed

t d bl liassets and consumable supplies

51

Case Study: Application Of FAS 5 (Cont.)y pp ( )

Policies and procedures were then pimplemented in the sales-ordering process, in order to obtain

d fappropriate documentation from each new customer.

d fAn automated exemption certificate management software was implemented to gather maintain implemented to gather, maintain and store exemption certificate documentation

52

documentation.

Case Study: Application Of FAS 5 (Cont.)y pp ( )

The tax department developed use The tax department developed use tax accrual worksheets that included the appropriate use tax included the appropriate use tax rates, to facilitate the accrual process To reduce manual process. To reduce manual calculations, the electronic audit results and Excel macros were results and Excel macros were utililized to facilitate compliance.

53