Session 9: Panel on Assets Jeffery Yong IAIS Secretariat Regional Training Seminar IAIS-ASSAL San...

17

Session 9: Panel on Session 9: Panel on Assets Assets Jeffery Yong IAIS Secretariat Regional Training Seminar IAIS-ASSAL San Salvador, 24 November 2010

-

Upload

amanda-hodge -

Category

Documents

-

view

220 -

download

0

Transcript of Session 9: Panel on Assets Jeffery Yong IAIS Secretariat Regional Training Seminar IAIS-ASSAL San...

Session 9: Panel on AssetsSession 9: Panel on Assets

Jeffery YongIAIS Secretariat

Regional Training Seminar IAIS-ASSAL

San Salvador, 24 November 2010

Session 9: Panel on Assets 224 Nov 2010San Salvador

AgendaAgenda

1. Introduction - lessons from the financial crisis

2. International standards

3. Summary

Session 9: Panel on Assets 324 Nov 2010San Salvador

Lessons from the financial crisis – mainly on Lessons from the financial crisis – mainly on asset side of the balance sheetasset side of the balance sheet

Note : This list is not exhaustive.

Session 9: Panel on Assets 424 Nov 2010San Salvador

Proposed structure of the new ICPsProposed structure of the new ICPs

ICP 18

Risk Assessment and Management

ICP 19

Insurance activity

ICP 20

Liabilities

ICP 21

Investments

ICP 22

Derivatives and similar commitments

ICP 23

Capital adequacy and solvency

ICP 14

Valuation

ICP 15

Investment

ICP 16

Enterprise risk management for

solvency purposes

ICP 17

Capital Adequacy

Standard on valuation

Guidance on valuation

Standard on investments

Guidance on investments

Standard on ERM for solvency

purposes

Guidance on ERM for solvency

purposes

Standard on capital

requirements

Standard on internal

models

Guidance on capital

requirements

Guidance on internal

models

EX

IST

ING

ICP

SN

EW

ICP

ST

RU

CT

UR

E

Session 9: Panel on Assets 524 Nov 2010San Salvador

Total balance sheet approach to recognise Total balance sheet approach to recognise interdependenciesinterdependencies

Supervisory assessment of the financial position

Assets Liabilities and capital requirement

Financial position

Assets Liabilities

Te

chn

ica

l pro

visi

on

s

Best estimate

policy obligations

Risk marginValue of

assets for supervisory

purposes

Capital requirement

Liabilities

Available capital

Public financial reporting

Liabilities

Capital

Session 9: Panel on Assets 624 Nov 2010San Salvador

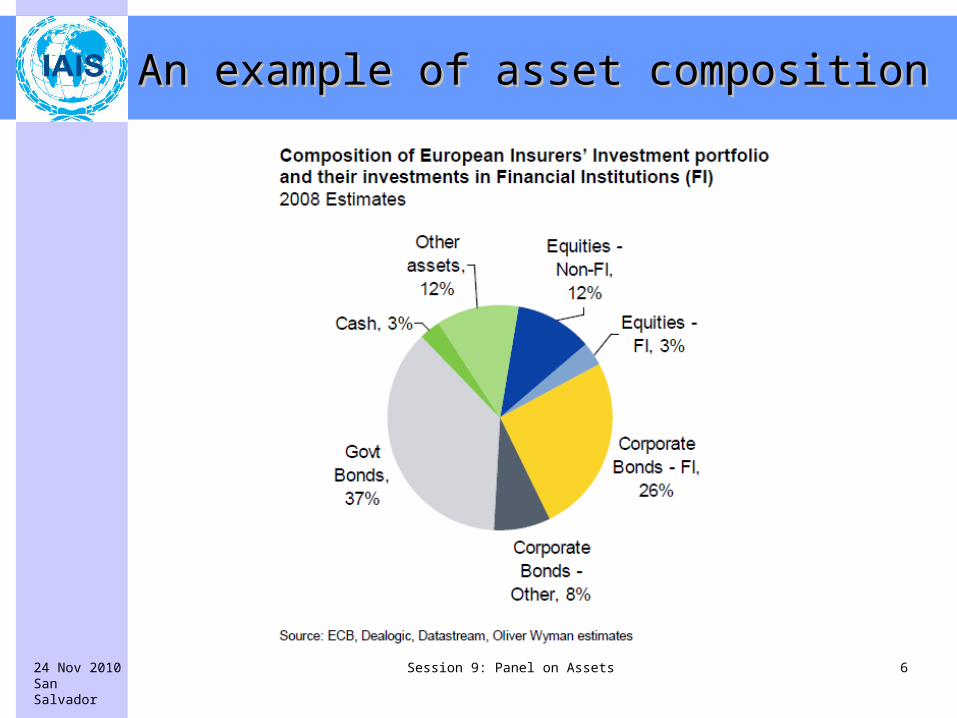

An example of asset compositionAn example of asset composition

Session 9: Panel on Assets 724 Nov 2010San Salvador

AgendaAgenda

1. Introduction - lessons from the financial crisis

2. International standards

3. Summary

Session 9: Panel on Assets 824 Nov 2010San Salvador

Basis for establishing regulatory investment Basis for establishing regulatory investment requirementsrequirements

• The supervisory regime establishes requirements that are applicable to the investment activities of the insurer.

• The supervisory regime is open and transparent as to the regulatory requirements that apply and is explicit about the objectives of those requirements.

Financial requirements alone not sufficient – need to complement with quantitative/qualitative requirements to limit investment risks by insurer.

Factors to consider when setting requirements:

• Quality of risk management and governance

• Quality of capital resources

• Disclosure framework

• Cost of compliance

• Risk sensitivity of solvency regime Transparency facilitates comparisons across jurisdictions – particularly

important for cross-border insurance groups Explicit objectives can help to identify consistency with other requirements

– regulatory capital requirements, determination of capital resources and valuation of assets and liabilities.

Session 9: Panel on Assets 924 Nov 2010San Salvador

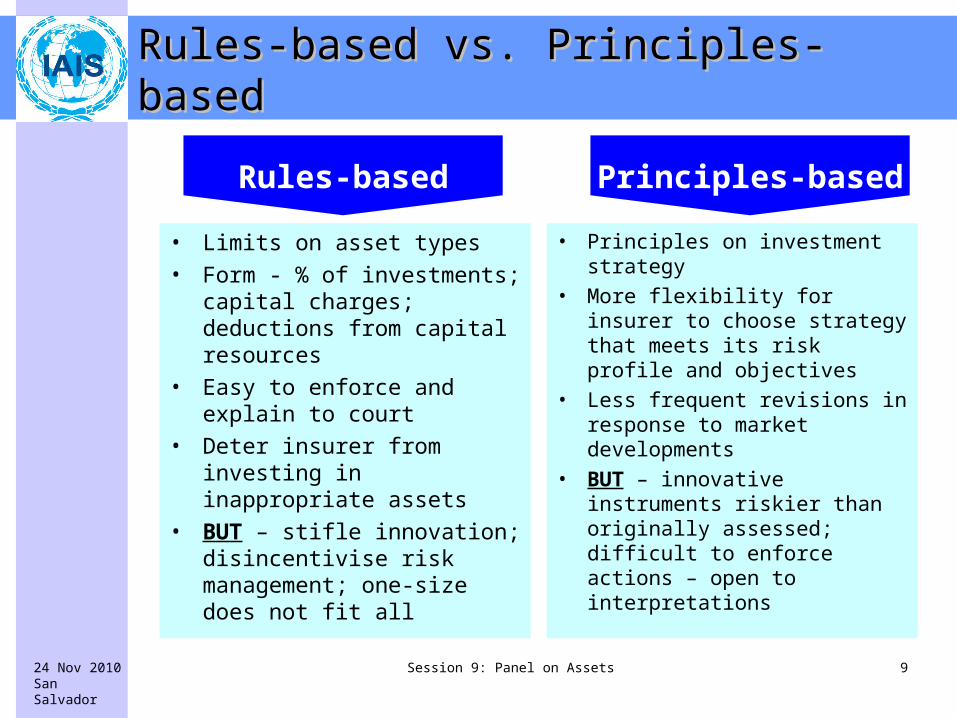

Rules-based vs. Principles-basedRules-based vs. Principles-based

• Limits on asset types

• Form - % of investments; capital charges; deductions from capital resources

• Easy to enforce and explain to court

• Deter insurer from investing in inappropriate assets

• BUT – stifle innovation; disincentivise risk management; one-size does not fit all

• Principles on investment strategy

• More flexibility for insurer to choose strategy that meets its risk profile and objectives

• Less frequent revisions in response to market developments

• BUT – innovative instruments riskier than originally assessed; difficult to enforce actions – open to interpretations

Rules-based Principles-based

Session 9: Panel on Assets 1024 Nov 2010San Salvador

Minimum requirements - security, liquidity and Minimum requirements - security, liquidity and diversificationdiversification

Security

• Restrict investment exposure to high risk investments (default, lost of value, custodianship)

• Limits of using external credit ratings – conduct own due diligence

• Derivatives – assess underlying assets and counterparty risk

Liquidity

• Able to realise/liquidate investments at any point in time

• Insurance groups – due regard to impediments to cross-border transfer of assets particularly in winding up

Diversification

• Diversify within risk category – pooling of same risks (e.g. shares of different companies)

• Diversify between risk categories – uncorrelated investments (e.g. different asset classes, geographical spread etc.)

Session 9: Panel on Assets 1124 Nov 2010San Salvador

Investments should be appropriate to the nature Investments should be appropriate to the nature of liabilitiesof liabilities

ASSETS

Timing of liability

cashflows

Amount of liability

cashflows

Policy guarantees & options

Unit-linked policies

Currency of liabilities

Mismatching risk higher technical provisions and/or capital requirements

Session 9: Panel on Assets 1224 Nov 2010San Salvador

Risk assessibilityRisk assessibility

• The solvency regime requires the insurer to invest only in assets whose risks it can properly assess and manage.

• The solvency regime establishes quantitative and qualitative requirements on the use of more complex/less transparent assets and investments in lightly/non-regulated markets.

Invest only in assets that the insurer can identify, measure, monitor, control and report – including reliable valuation.

Assess maximum loss possible – look through underlying assets.

Particular attention on complex asset classes – implicit obligations of support, increased correlation in times of stress.

E.g.- pre-approval of an insurer’s derivative investment plan – describe controls and test process.

Session 9: Panel on Assets 1324 Nov 2010San Salvador

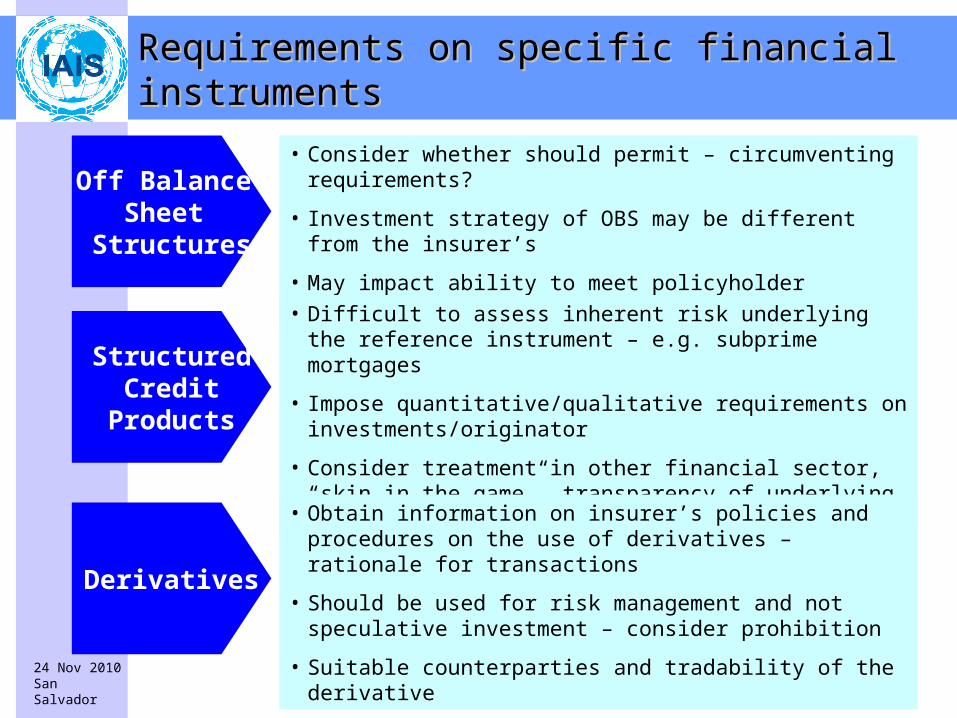

Requirements on specific financial instrumentsRequirements on specific financial instruments

Off Balance Sheet

Structures

• Consider whether should permit – circumventing requirements?

• Investment strategy of OBS may be different from the insurer’s

• May impact ability to meet policyholder obligations especially in times of stress

StructuredCredit

Products

• Difficult to assess inherent risk underlying the reference instrument – e.g. subprime mortgages

• Impose quantitative/qualitative requirements on investments/originator

• Consider treatment in other financial sector, “skin in the game”, transparency of underlying asset, insurer’s control system

Derivatives

• Obtain information on insurer’s policies and procedures on the use of derivatives – rationale for transactions

• Should be used for risk management and not speculative investment – consider prohibition

• Suitable counterparties and tradability of the derivative

Session 9: Panel on Assets 1424 Nov 2010San Salvador

AgendaAgenda

1. Introduction - lessons from the financial crisis

2. International standards

3. Summary

Session 9: Panel on Assets 1524 Nov 2010San Salvador

Summary of key pointsSummary of key points

• During the recent global financial crisis, insurers were mainly affected due to their investment activities.

• Regulatory and supervisory requirements on investments need to incentivise insurers to have sound investment policies without being too restrictive.

• Sound asset-liability management policies has proven to be a powerful tool to manage risk.

Session 9: Panel on Assets 1624 Nov 2010San Salvador

Some final thoughtsSome final thoughts

• Need to avoid insurers becoming too-big-to-manage or too-complex-to-understand

• Insurers should have better understanding on risk interdependencies

• Avoid mistakes in other sectors

Session 9: Panel on Assets 1724 Nov 2010San Salvador

Thank you for your attention. Any questions/ comments?