Session 8.3: Business Work Improvement Course (Financial Statements and Analysis)

21

SESSION 8.3: FINANCIAL STATEMENTS AND FINANCIAL ANALYSIS Business Work and Improvement Course

-

Upload

lym-relampagos-ongoy -

Category

Business

-

view

46 -

download

0

Transcript of Session 8.3: Business Work Improvement Course (Financial Statements and Analysis)

SESSION 8.3: FINANCIAL STATEMENTS

ANDFINANCIAL ANALYSIS

Business Work and Improvement Course

II. Financial Statements

•Financial statements are the end-product of the financial accounting process.

•Major financial statements:• Income Statement•Statement of Cash Flows•Balance Sheet

Financial Statements

a. Income Statement – tells how much money does the business earn over a given period of time.

Gross Profit = Sales – C0st of Sales

Net Profit = Gross Profit – Expenses

Options to increase profit

1. Increase Sales – how? Quantity/Volume Sold

Or Selling Price

2. Decrease Expenses – how ?Reduce overhead expenses Reduce maintenance/repair costs

How to Determine the Cost of Sales

Trading BusinessBeginning Inventory xxxAdd: Purchases xxxTotal Inventory xxxLess: Ending Inventory xxxCost of Sales xxx

Beginning Inventory xxxAdd: Direct Materials, Direct Labor, overhead expenses (light, water, power, rents, indirect labor etc.) xxxTotal InventoryLess: Ending Inventory xxxCost of Sales xxx

Manufacturing

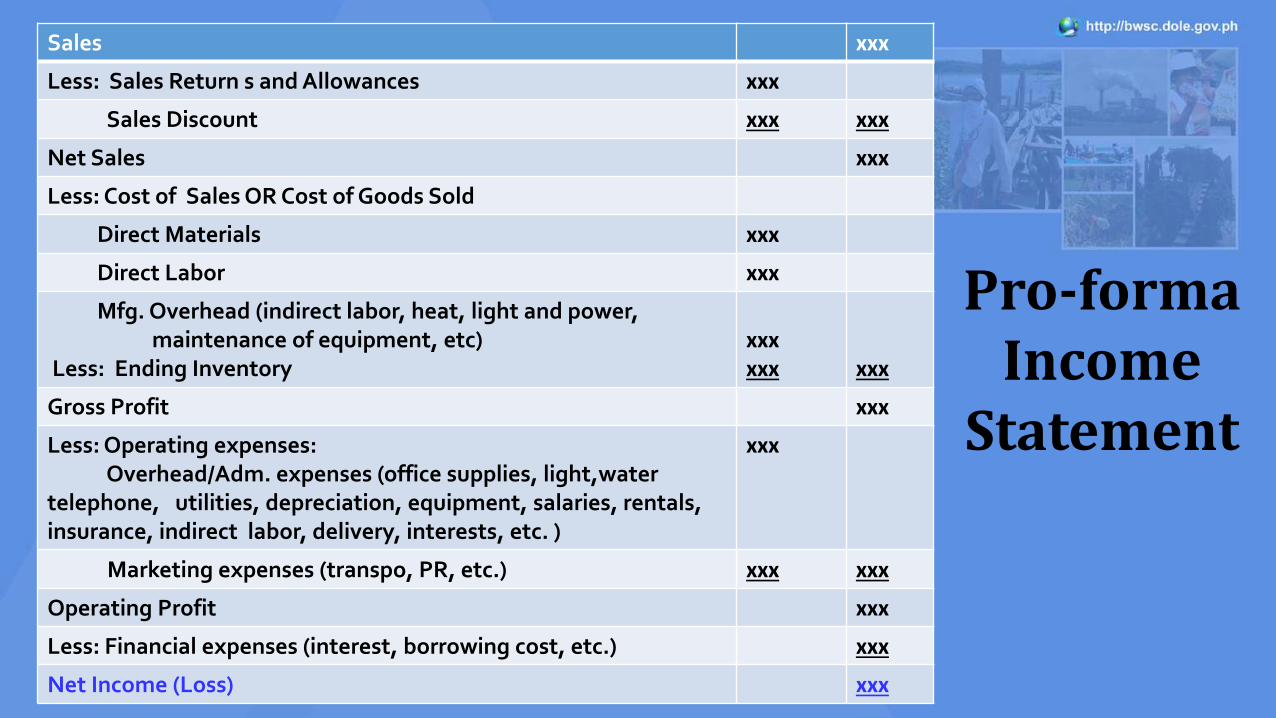

Sales xxx

Less: Sales Return s and Allowances xxx

Sales Discount xxx xxx

Net Sales xxx

Less: Cost of Sales OR Cost of Goods Sold

Direct Materials xxx

Direct Labor xxx

Mfg. Overhead (indirect labor, heat, light and power, maintenance of equipment, etc)

Less: Ending Inventoryxxxxxx xxx

Gross Profit xxx

Less: Operating expenses:Overhead/Adm. expenses (office supplies, light,water

telephone, utilities, depreciation, equipment, salaries, rentals, insurance, indirect labor, delivery, interests, etc. )

xxx

Marketing expenses (transpo, PR, etc.) xxx xxx

Operating Profit xxx

Less: Financial expenses (interest, borrowing cost, etc.) xxx

Net Income (Loss) xxx

Pro-forma Income

Statement

Financial Statements

b. Cash Flow Statement – tells how much cash is needed to meet obligations, when it is needed, and where it is coming from.

• Cash in-flow – cash coming INTO the business i.e. financial investment, sales revenues, interest on savings, etc.

• Cash out-flow – cash coming OUT of the business i.e. disbursements on: a. operating expenses (direct materials, direct labor), b. overhead costs (heat, light water, indirect labor, rental, etc.), c. acquisition of assets, and d. dividends and income tax payments.

• Covers pre-operating period

ParticularsDay/Week/Month

1 2 3 4 5 6 7 8 9

Cash at the beginning of the Period

Add: CASH INFLOW

Assistance from DOLE

Equity from ACP / proponent

Cash Sales /Interest

Income/collections

TOTAL CASH INFLOW

Less: CASH OUTFLOW

Direct Costs (direct materials and

labor, supplies, equipment, etc.)

Indirect Costs(rent, interest, electricity

telephone, depreciation)

Any other cash out (pre-operating

expenses, loan repayment, etc.)

TOTAL CASH OUTFLOW

Cash at the end of the month

Pro-forma Cash Flow Statement

Financial Statements

c. Balance Sheet – shows the snapshot of a company’s financial condition at a given period of time showing the business’ growth in terms of Net Worth. It shows the assets, liabilities and capital/equity at a given date.

Assets = Liabilities + Capital/Owner’s Equity

ASSETS LIABILITIES OWNER’S EQUITY

Current AssetsFixed AssetsOther Assets

Current LiabilitiesLong-term LiabilitiesAccrued expenses

Amount invested (DOLE, ACP, Beneficiaries, loans)Retained earningsreinvested

ASSETSCurrents Assets:

Cash Accounts Receivables Notes Receivables Inventories Prepaid Expenses

Total Current Assets

Fixed Assets (Net of Depreciation):

Land Building (Workplace) Equipment Machineries

Total Fixed Assets Other Assets

TOTAL ASSETS

xxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxx

LIABILITIES AND OWNER’s EQUITY

LIABILITIES:Current Liabilities:

Accounts PayableNotes Payable

Other Liabilities Total Liabilities

OWNER’S EQUITY (Capital)DOLE Equity ACP Equity Beneficiary Counterpart Retained Earnings Total Owner’s Equity

TOTAL LIABILITIES AND OWNER’ EQUITY

xxxxxxxxxxxxxxx

xxxxxxxxxxxxxxx

xxx

Pro-forma Balance

Sheet

Financial Analysis

Test of Profitability: Return of Investment (ROI)

Test of Liquidity: Current Ratio

Test of Operating Leverage: Break-even Analysis

ROI - is the expected rate of return on the total cost invested to

the project.

ROI = Net Income/ Total Project Cost

Sources of data:1. Projected Net Income to be derived from the Projected Income

Statement2. Total Project Cost to be derived from the Total Project Cost

Schedule

What is ROI and How To Compute It?

Computation of ROI ( illustration)

Assumptions: Net Income - P 72,000.00Total Project Cost - P 215,000.00

ROI = Net Income/Total Project Cost= P72,000/P215,000.00 = .33 or 33%

This indicates that the livelihood is expected to generate a return of P33.00 for every P 100.00 invested in the project (DOLE + ACP +beneficiaries’ equity).

The higher the ROI, the more the project is profitable.

What is a Current Ratio and How To Compute It?

Current Ratio = Current Assets / Current Liabilities

Cash P11,572Short-term investments 76,853Receivables 14,921Inventory 1,920Other current assets 3,740Total Current Assets P109,006

Accounts Payable P 9,958Short-term debt 2,000Other Current Liab 21,945Total Current Liabi P33,903

The higher the ratio, the business is more able to pay its obligations. A ratio between 1.5 and 3 is generally considered healthy.

CR = P109,006 / P33,903 = 3.22

Current Assets Current Liabilities

Current Ratio (CR) - is a financial ratio which shows the liquidity of a business and its ability to generate sufficient funds (monetize products) to meet current operating needs and current debts

What is Break-even Analysis / Break-even Point?

Break-even Analysis (BEA)

is a tool in determining the point at which the project’s revenue (sales) equals the costs (fixed and variable costs) associated with it, with emphasis on the Break-even Point. It helps determine how much volume of product will be sold in order to make a profit.

Break-even Point (BEP)

is the point at which the company’s sales exactly cover its expenses in producing and selling its products, without making a profit or taking a loss.

Factors in Figuring out Break-even Point

1. Direct or Variable Costs – are costs that go into creating the product or service (direct materials and direct labor).

2. Indirect or Fixed Costs – are costs that do not depend on the volume of production (rents, water, light and power, advertising, office supplies, wages of office staff, staff)

Calculating Break-even Point

Break-even Point Volume/Units (BEV):

BEV = Fixed CostPrice per Unit- Variable Cost Per Unit

Break-even Point Sales (BES):

BES = BESP x Break-even Sales Units

Break-even Point Selling Price (BE SP):

BESP = Total Cost (Variable + Fixed Costs)Unit Volume

Sales:

Sales price per unit P12.50

Sales volume 1,000

Total Sales P12,500.00

Total Variable Costs P7,600.00

Total Fixed Costs 3,400.00

Net Profit/Loss P1,500.00

Illustration (figures in peso)

1. BEP Vol = ________Fixed Cost______________Price per Unit- Variable Cost Per Unit

= P 3,400.00 = P 3,400.00 P 12.50-P 7.60 P 4.90

= 694 units

3. BEP Sales = Price per Unit x Break-even Sales Volume = P 11.00 x 694 units= P 7,634.00

2. BEP SP = Total CostUnit Volume

= P 11,000.001,000 units

= P 11.00 per unit

Computation of BEP (illustration)

References:

• BRW Manual on Development of Self-Reliant Organization

• Technical Paper on Break-even Analysis

• Start Your Business Flyers of the DTI

• Rasul and Macalindong PPT on Project Development and Management

• https://cnx.org/contents/0OlLxNru@1/Basic -Accounting-Concepts---De

• http://definitions.uslegal.com/b/bookkeeping/

SALAMAT PO!

Financial Statements and Financial Analysis

Business Work and Improvement Course