Session 7 international tax and compensation steve rao

21

INSZOOM Immigration Conference 2015 Empower Employees for Immigration Compliance

Transcript of Session 7 international tax and compensation steve rao

INSZOOM Immigration Conference 2015Empower Employees for Immigration Compliance

• Stephen Rao currently works for Sapient in Gurgaon, India. He is a Director – Regional Mobility Team (India & APAC).

About the Author: Stephen Rao

{

International Tax&

Compensation

Recap

Technology US Visa

Current Updates

International Compensation

and Tax

Introduction to International Compensation & Tax

Assignment Types

Host Country Payroll

•The assignee’s payroll becomes inactive in the home country and becomes active in the host country.

Home country payroll

•The assignee remains on the home country payroll. Host country entity may create a shadow payroll for tax and social security filing obligations

Split pay Model

•The assignee get a part of the payroll in home country and gets assignment allowances in the host country

ResidencyTaxable Income

Domestic Tax Laws

Income Tax

Treaties

Basics for understanding Income tax

Panel Discussion

Exposure due to Business Travelers and Short Term Assignments – Sruthi Ananthachari

Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 – Amarpal Singh

Social Security Tax – Exposure to corporate entities –Ravi Jain

Income tax processing and FBAR – KarthikeyanGangadharan

Exposure due to Business Travelers and Short Term

Assignments

Sruthi Ananthachari

Black Money (Undisclosed Foreign Income and Assets) and

Imposition of Tax Act, 2015

Amarpal Singh

Social Security Tax

Ravi Jain

Income tax processing and Foreign Bank and Financial Records

Karthikeyan Gangadharan

Questions?Slido.com ( #IIC2015)

Background Slides

Resident

For the purposes of this Convention, the term "resident of a Contracting State" means any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of management, place of incorporation, or any other criterion of a similar nature, and also includes that State and any political subdivision thereof.

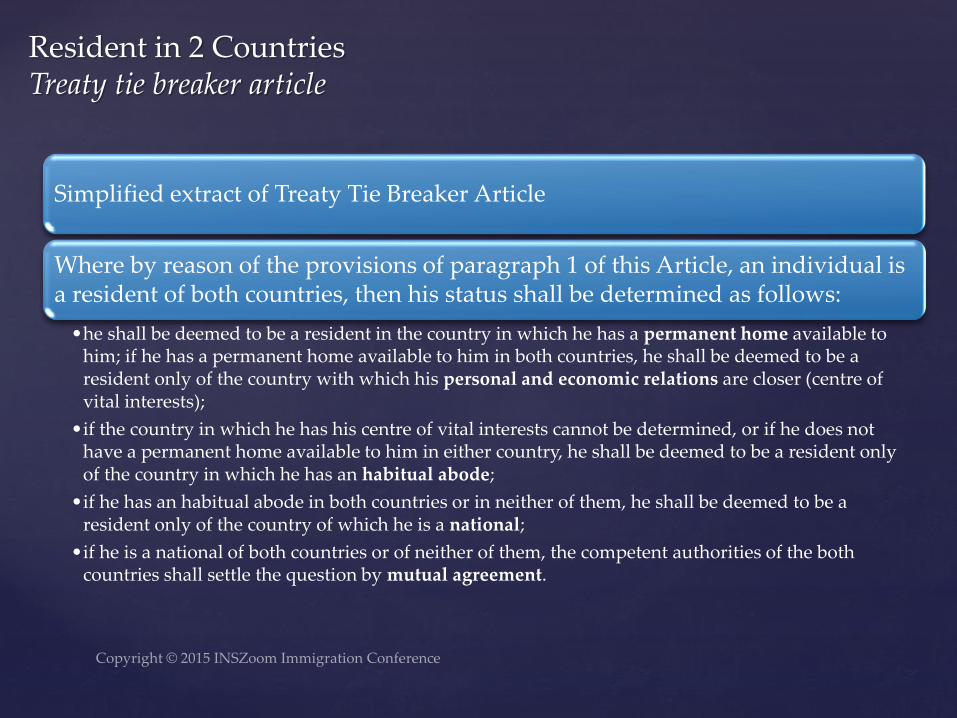

Resident in 2 CountriesTreaty tie breaker article

Simplified extract of Treaty Tie Breaker Article

Where by reason of the provisions of paragraph 1 of this Article, an individual is a resident of both countries, then his status shall be determined as follows:

•he shall be deemed to be a resident in the country in which he has a permanent home available to him; if he has a permanent home available to him in both countries, he shall be deemed to be a resident only of the country with which his personal and economic relations are closer (centre of vital interests);

•if the country in which he has his centre of vital interests cannot be determined, or if he does not have a permanent home available to him in either country, he shall be deemed to be a resident only of the country in which he has an habitual abode;

•if he has an habitual abode in both countries or in neither of them, he shall be deemed to be a resident only of the country of which he is a national;

•if he is a national of both countries or of neither of them, the competent authorities of the both countries shall settle the question by mutual agreement.

Tax Residency and Taxability

• Generally taxable on the worldwide income

Tax Residents

• Generally taxable on income from specific source

Tax Non-Residents

• Employment Income

• Personal Income (eg. Interest, Dividend, capital Gain)

• Deferred Income (eg. Pension, Gratuity, Equity, e

Tax Residency status impacts the taxation of an expatriate

Compensation wage elements

Stay At Home Compensation may include:

•Basic Salary/Wages

•Special Allowances

•Bonus

•Deferred compensation

•Stock options/Share awards

•Group term life insurance

•Education Allowance

Assignment Compensation :

•Cost of living allowance

•Housing

•Family allowance

•Tax reimbursements

•Tax preparation fees

•Hypothetical tax

•Home leave / Flyback

•Foreign service premium

•Foreign taxes

•Relocation allowance

• Time Basis: compensation other than fringe benefits

• Geographical Basis: certain listed fringe benefits

• Alternative Basis: facts and circumstances

Sourcing of income

Time Basis

Base salary

Vacation pay

Incentive awards

Stock option income (special

rules)

Flexible compensation

Reimbursed club dues for a U.S.

club membership

Geographical Basis

Housing:

Education:

Local transportation:

Foreign Tax reimbursements:

US Tax reimbursements:

Hardship duty pay:

Moving expenses:

Cost of Living Allowance

Alternative Basis

Where income may be taxed on

receipt basis- India

Deemed disposition of Capital Asset

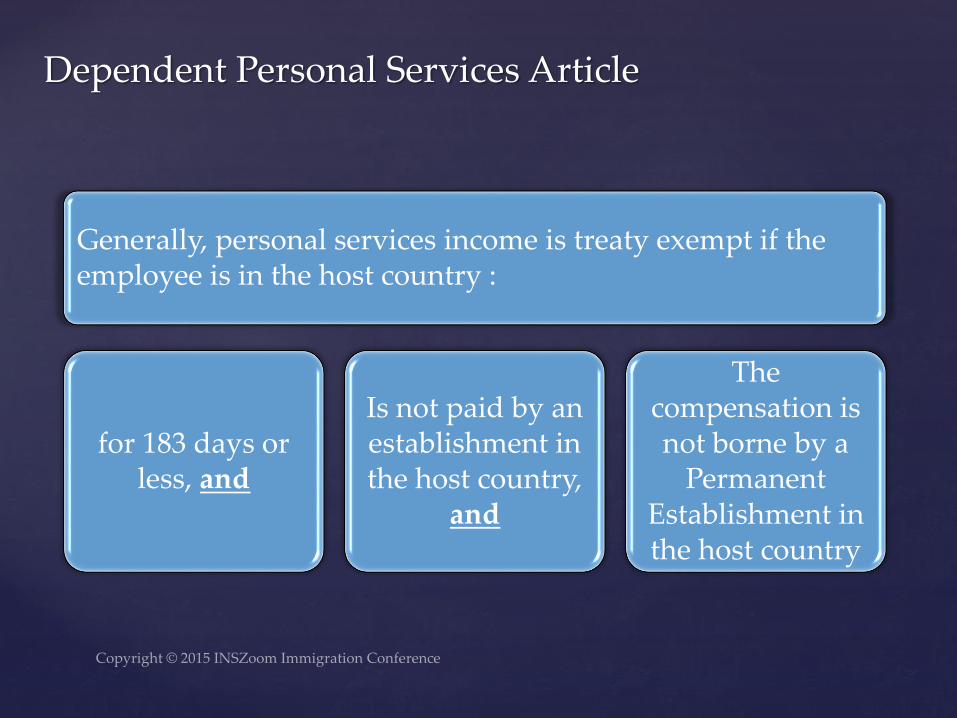

Dependent Personal Services Article

Generally, personal services income is treaty exempt if the employee is in the host country :

for 183 days or less, and

Is not paid by an establishment in the host country,

and

The compensation is not borne by a

Permanent Establishment in the host country

• John Stephen RaoSapient CorporationSector 21Gurgaon, Haryana 122016, INDIA+91 124 4167271 T+91 97111 89970 [email protected]

• INSZoom.com, Inc.2603 Camino Ramon, Suite 375San Ramon, California 94583 USA925 244 0600 [email protected]

Contact Info: