Session 127 Panel Discussion, Life and Annuity In … · IV. Spin-off / run-off / exit ......

36

Session 127 PD, Life and Annuity In-Force Management Moderator: David J. Weinsier, FSA, MAAA Presenters: Jennifer L. McGinnis, FSA, CERA, MAAA Brock E. Robbins, FSA, FCIA, MAAA David J. Weinsier, FSA, MAAA

Transcript of Session 127 Panel Discussion, Life and Annuity In … · IV. Spin-off / run-off / exit ......

Session 127 PD, Life and Annuity In-Force Management

Moderator:

David J. Weinsier, FSA, MAAA

Presenters: Jennifer L. McGinnis, FSA, CERA, MAAA

Brock E. Robbins, FSA, FCIA, MAAA David J. Weinsier, FSA, MAAA

Life and Annuity In Force Management2 015 SOA Annual Meeting Session 127 PD

Jennie McGinnis, FSA, MAAA, [email protected]

2015 SOA Annual Meeting | Session 127 | J. McGinnis

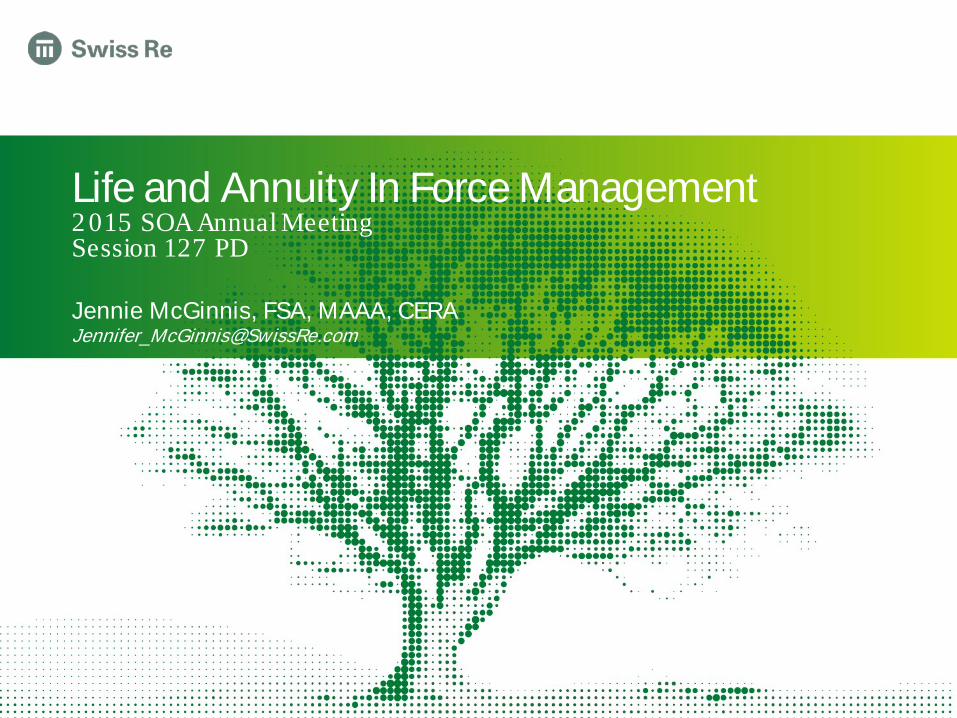

In Force Options Management

2

Who has options?

• Policyholders• Insurance companies• Reinsurance

companies

What options are available?

• Contractual• Non-contractual

2015 SOA Annual Meeting | Session 127 | J. McGinnis

• Strong commitment from top leaders

• Recognizes the importance of new business and in force management

• Key priorities

– Better understand the performance of our business

– Proactively manage our in force business to

– improve our financial performance

– and create new opportunities with our clients

• Recruited s taff to improve the quality of our data, models and assumptions

Creation of Swiss Re’s Liability Management Team

3

2015 SOA Annual Meeting | Session 127 | J. McGinnis

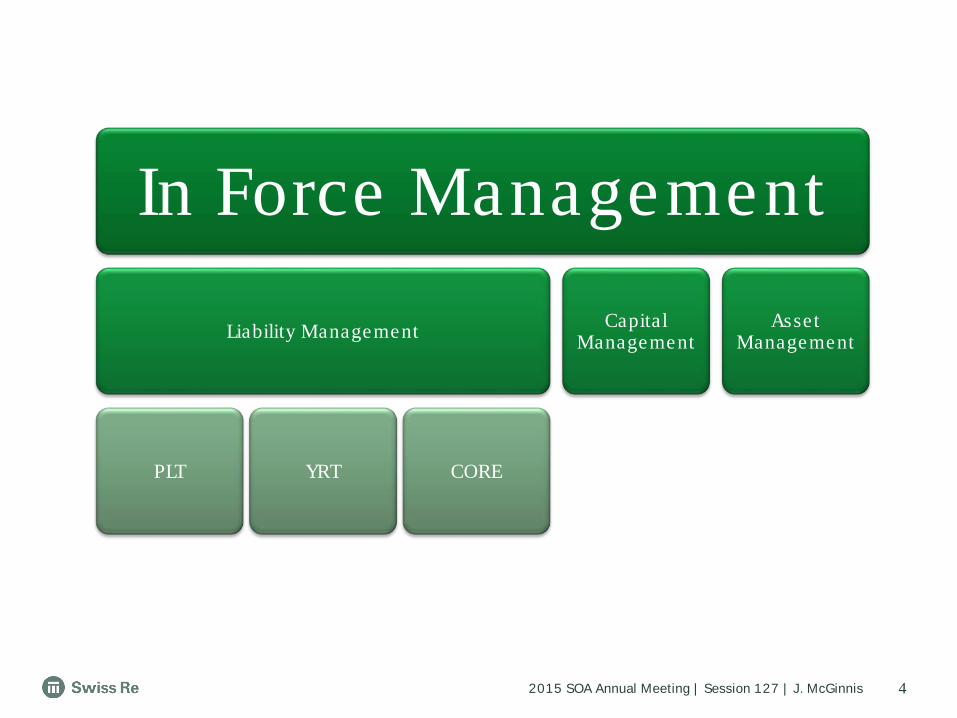

In Force Management

Liability Management

PLT YRT CORE

Capital Management

Asset Management

4

2015 SOA Annual Meeting | Session 127 | J. McGinnis

• The 2 013 SOA survey shows only a few companies vary assumptions by the primary driver – premium jump ratio

• Swiss Re’s experience, affirmed by the SOA survey

– Actively managing PLT business s ince 2 010 , supporting more than 5 0 implementations

– At least 2 5 companies have implemented a PLT management program

– Programs exis t to address in force , new business , or both

– The number of companies interested in evaluating their options is growing

• Considerations for implementation

– Cross functional teams

– Resource allocation

– Communication

Post Level Term (PLT) Management

5

2015 SOA Annual Meeting | Session 127 | J. McGinnis

Performance Management

6

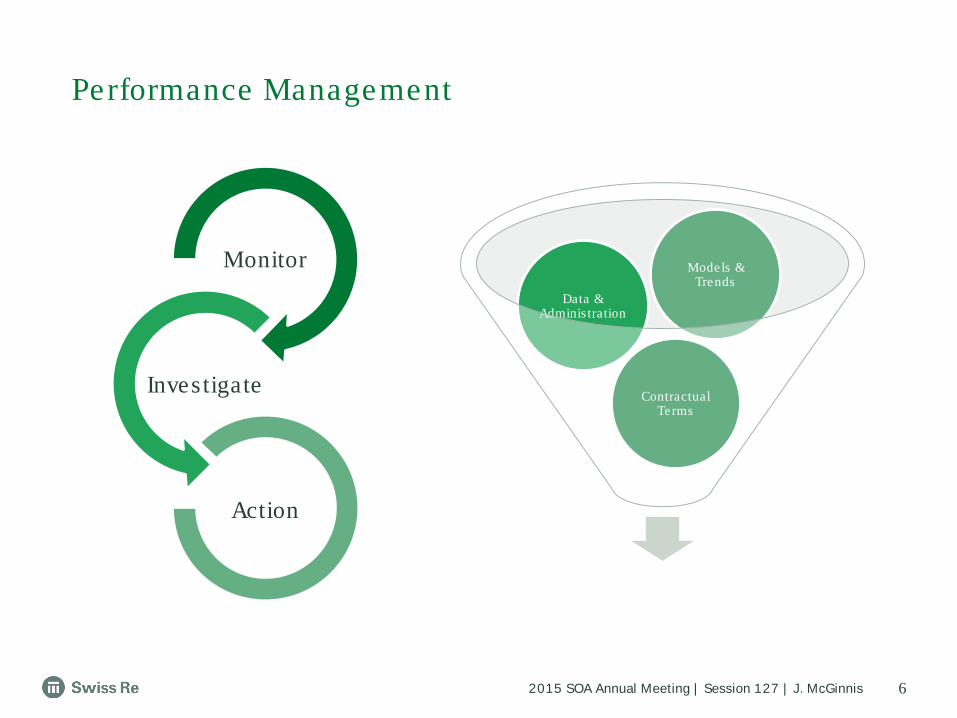

Monitor

Investigate

Action

Contractual Terms

Data & Adminis tration

Models & Trends

2015 SOA Annual Meeting | Session 127 | J. McGinnis

• Consolidating his torical financial reports

• Ensuring appropriate administration

• Responding to recapture requests

• Managing non-guaranteed e lements

• Testing long term assumptions

• Exploring bi-lateral liability portfolio management with our clients

Examples of CORE activities

7

2015 SOA Annual Meeting | Session 127 | J. McGinnis

Legal notice

8

©2015 Swiss Re. All rights reserved. You are not permitted to create any modifications or derivative works of this presentation or to use it for commercial or other public purposes without the prior written permission of Swiss Re.

The information and opinions contained in the presentation are provided as at the date of the presentation and are subject to change without notice. Although the information used was taken from reliable sources, Swiss Re does not accept any responsibility for the accuracy or comprehensiveness of the details given. All liability for the accuracy and completeness thereof or for any damage or loss resulting from the use of the information contained in this presentation is expressly excluded. Under no circumstances shall Swiss Re or its Group companies be liable for any financial or consequential loss relating to this presentation.

© Oliver Wyman

Life and Annuity Inforce Management

October 13, 2015

David J. Weinsier, FSA, MAAA

Session 127 PD2015 SOA Annual Meeting

1© Oliver Wyman 1

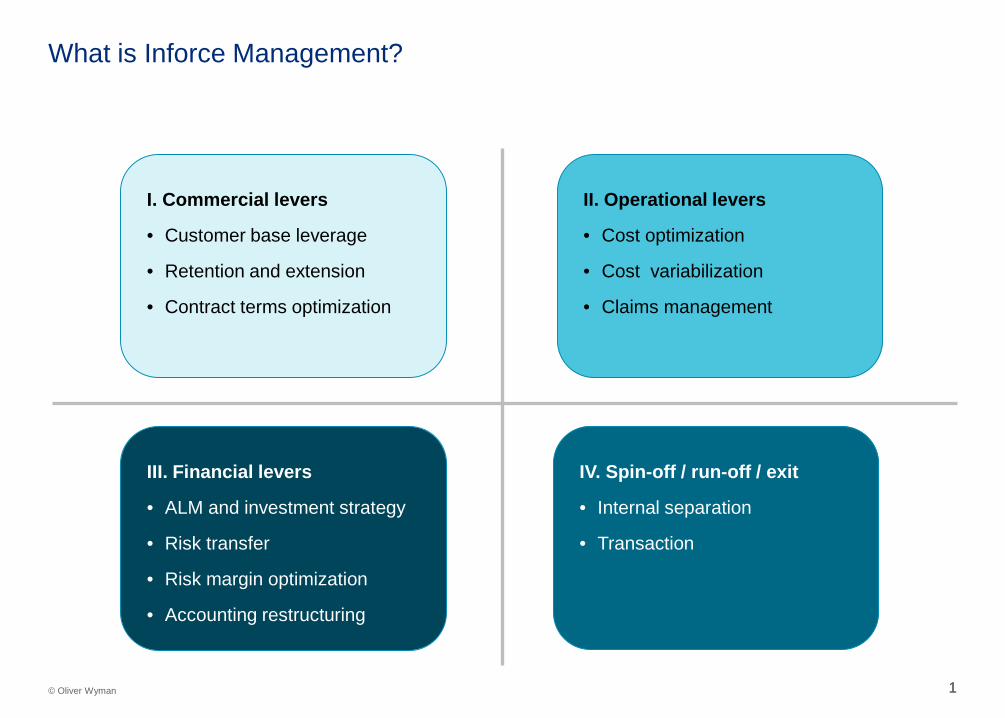

What is Inforce Management?

IV. Spin-off / run-off / exit

• Internal separation

• Transaction

I. Commercial levers

• Customer base leverage

• Retention and extension

• Contract terms optimization

II. Operational levers

• Cost optimization

• Cost variabilization

• Claims management

III. Financial levers

• ALM and investment strategy

• Risk transfer

• Risk margin optimization

• Accounting restructuring

22© Oliver Wyman

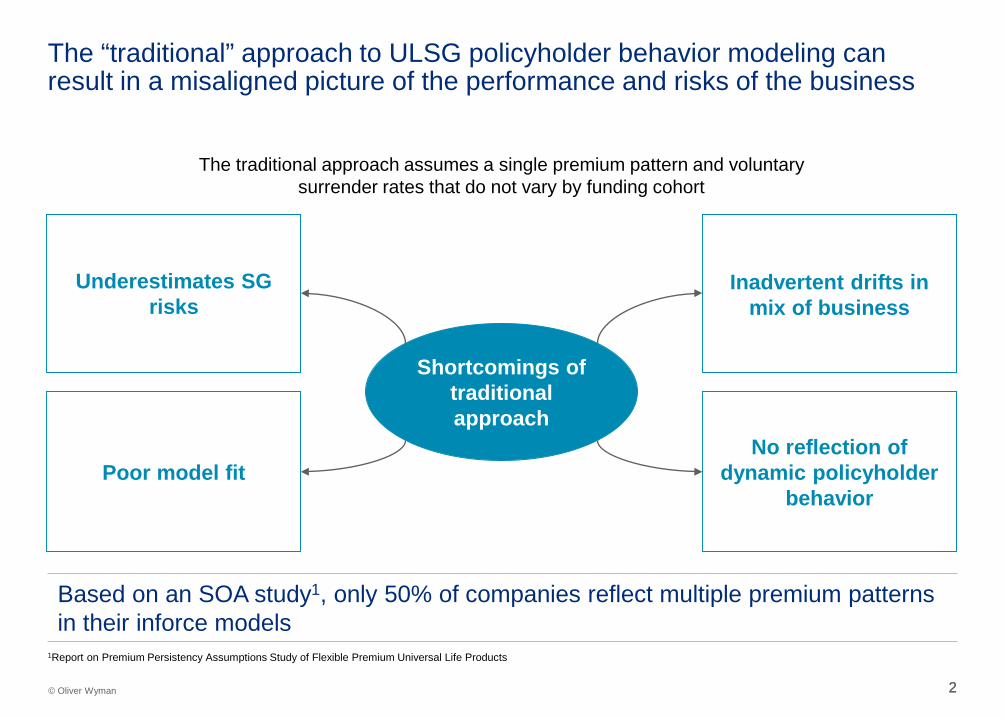

Underestimates SG risks

Inadvertent drifts in mix of business

Poor model fitNo reflection of

dynamic policyholder behavior

Shortcomings oftraditional approach

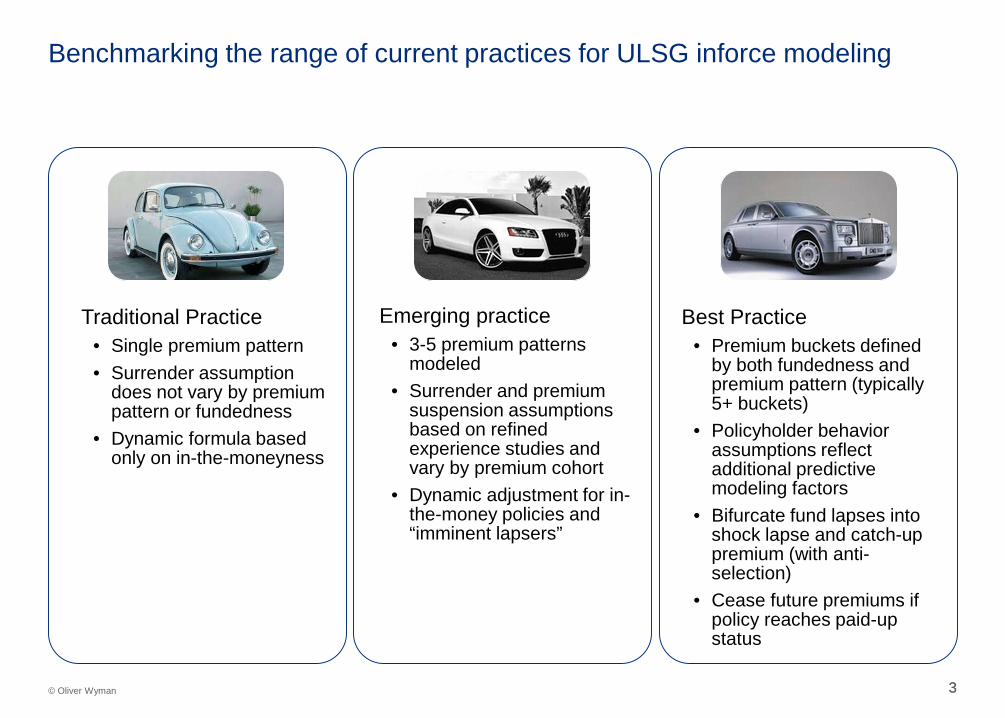

Based on an SOA study1, only 50% of companies reflect multiple premium patterns in their inforce models

The “traditional” approach to ULSG policyholder behavior modeling can result in a misaligned picture of the performance and risks of the business

1Report on Premium Persistency Assumptions Study of Flexible Premium Universal Life Products

The traditional approach assumes a single premium pattern and voluntary surrender rates that do not vary by funding cohort

3© Oliver Wyman 3

Benchmarking the range of current practices for ULSG inforce modeling

Traditional Practice• Single premium pattern• Surrender assumption

does not vary by premium pattern or fundedness

• Dynamic formula based only on in-the-moneyness

Emerging practice• 3-5 premium patterns

modeled• Surrender and premium

suspension assumptions based on refined experience studies and vary by premium cohort

• Dynamic adjustment for in-the-money policies and “imminent lapsers”

Best Practice• Premium buckets defined

by both fundedness and premium pattern (typically 5+ buckets)

• Policyholder behavior assumptions reflect additional predictive modeling factors

• Bifurcate fund lapses into shock lapse and catch-up premium (with anti-selection)

• Cease future premiums if policy reaches paid-up status

4© Oliver Wyman 4

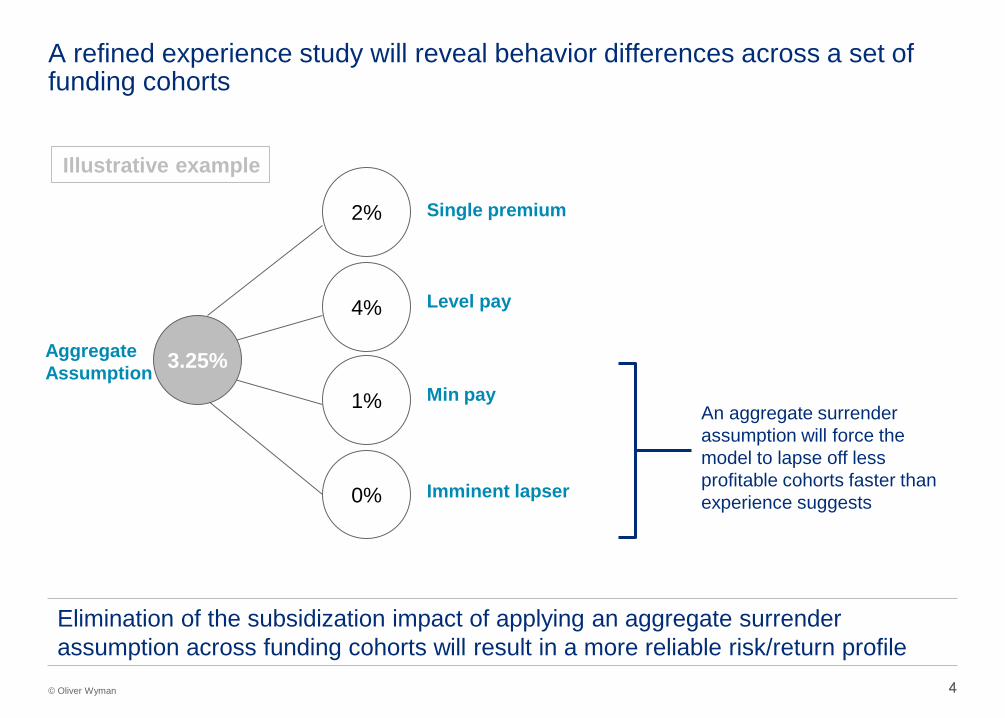

A refined experience study will reveal behavior differences across a set of funding cohorts

0%

1%

4%

2%

3.25%

Single premium

Level pay

Min pay

Imminent lapser

AggregateAssumption

An aggregate surrender assumption will force the model to lapse off less profitable cohorts faster than experience suggests

Elimination of the subsidization impact of applying an aggregate surrender assumption across funding cohorts will result in a more reliable risk/return profile

Illustrative example

55© Oliver Wyman

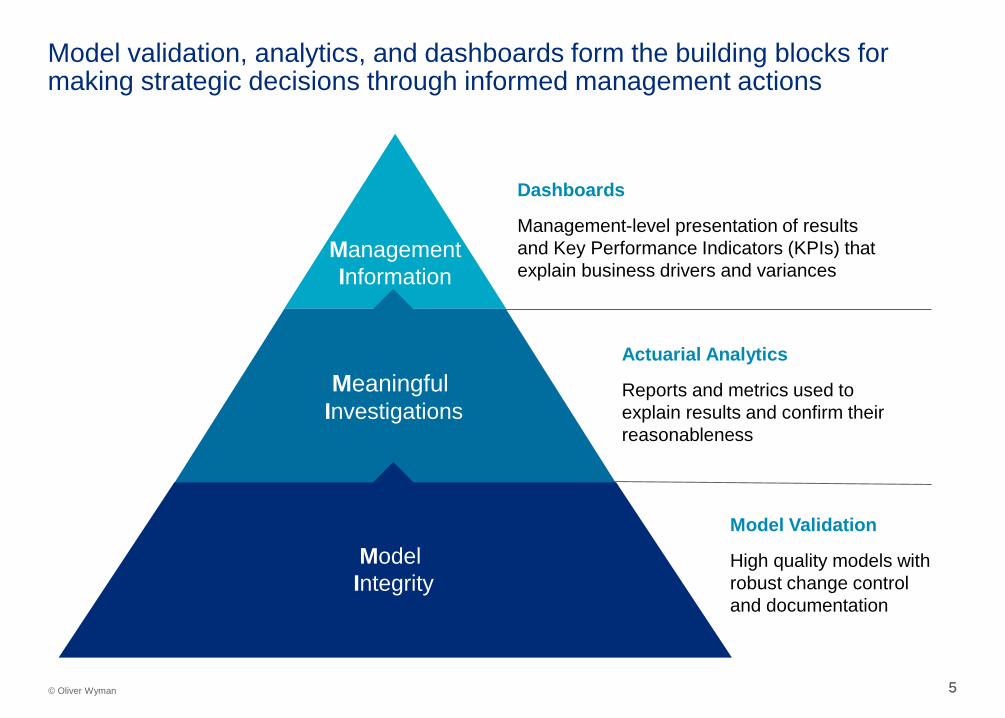

Model validation, analytics, and dashboards form the building blocks for making strategic decisions through informed management actions

Dashboards

Management-level presentation of results and Key Performance Indicators (KPIs) that explain business drivers and variances

Actuarial Analytics

Reports and metrics used to explain results and confirm their reasonableness

Model Validation

High quality models with robust change control and documentation

ManagementInformation

Meaningful Investigations

Model Integrity

66© Oliver Wyman

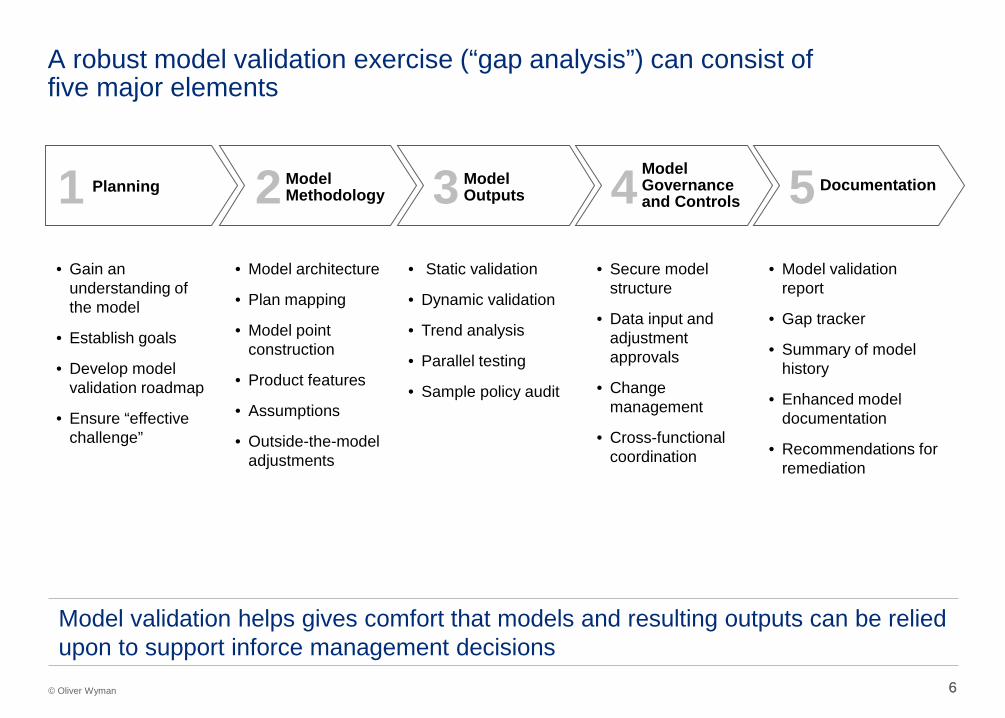

A robust model validation exercise (“gap analysis”) can consist offive major elements

Planning1 Model Methodology2 Model

Outputs3 Model Governance and Controls4 Documentation5

• Gain an understanding of the model

• Establish goals

• Develop model validation roadmap

• Ensure “effective challenge”

• Model architecture

• Plan mapping

• Model point construction

• Product features

• Assumptions

• Outside-the-model adjustments

• Static validation

• Dynamic validation

• Trend analysis

• Parallel testing

• Sample policy audit

• Secure model structure

• Data input and adjustment approvals

• Change management

• Cross-functional coordination

• Model validation report

• Gap tracker

• Summary of model history

• Enhanced model documentation

• Recommendations for remediation

Model validation helps gives comfort that models and resulting outputs can be relied upon to support inforce management decisions

77© Oliver Wyman

Model remediationInsurers are forced to balance the benefits of model refinement against several obstacles

1 2 3 4Data availability and credibility

Model run time Resources/ model maintenance

Software limitations/ coding complexity

SOA 2015 Annual Meeting & Exhibit

Session 127 PD: Life and Annuity Inforce Management

Brock Robbins, FSA, MAAAOctober 13, 2015

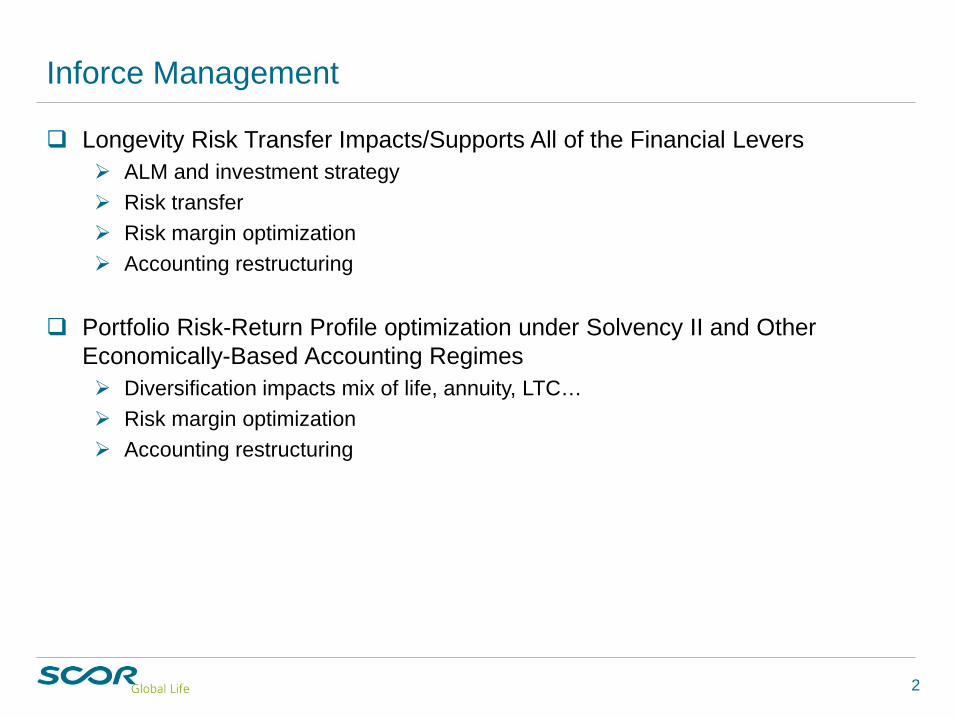

Inforce Management

Longevity Risk Transfer Impacts/Supports All of the Financial Levers ALM and investment strategy Risk transfer Risk margin optimization Accounting restructuring

Portfolio Risk-Return Profile optimization under Solvency II and Other Economically-Based Accounting Regimes Diversification impacts mix of life, annuity, LTC… Risk margin optimization Accounting restructuring

2

3

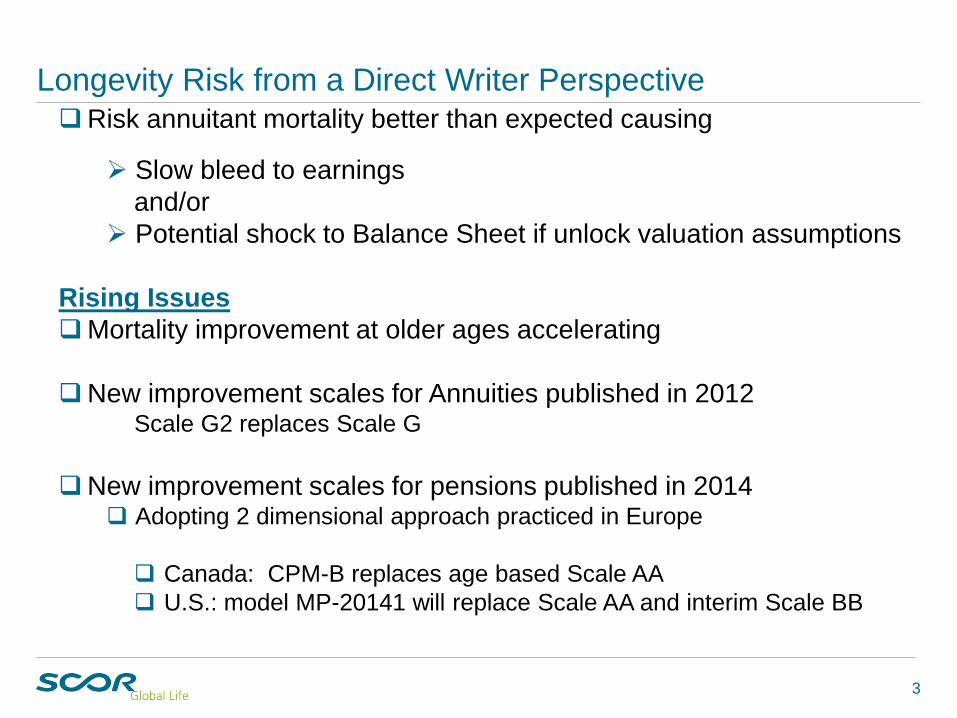

Longevity Risk from a Direct Writer PerspectiveRisk annuitant mortality better than expected causing

Slow bleed to earningsand/or

Potential shock to Balance Sheet if unlock valuation assumptions

Rising IssuesMortality improvement at older ages accelerating

New improvement scales for Annuities published in 2012Scale G2 replaces Scale G

New improvement scales for pensions published in 2014 Adopting 2 dimensional approach practiced in Europe

Canada: CPM-B replaces age based Scale AA U.S.: model MP-20141 will replace Scale AA and interim Scale BB

4

Pros and Cons of Managing Longevity Risk

ConsNo NAIC RBC C2

Requirements (U.S.)

Low exposure

Act as mortality hedge

ProsLack of Expertise

Longevity Risk is long-dated

5

Longevity Risk Management Approaches

Self-Insure

Buy-Out / sale

Buy-In / Coinsurance Immediate

Deferred income

Longevity Swap / Longevity Reinsurance

Capital Markets

6

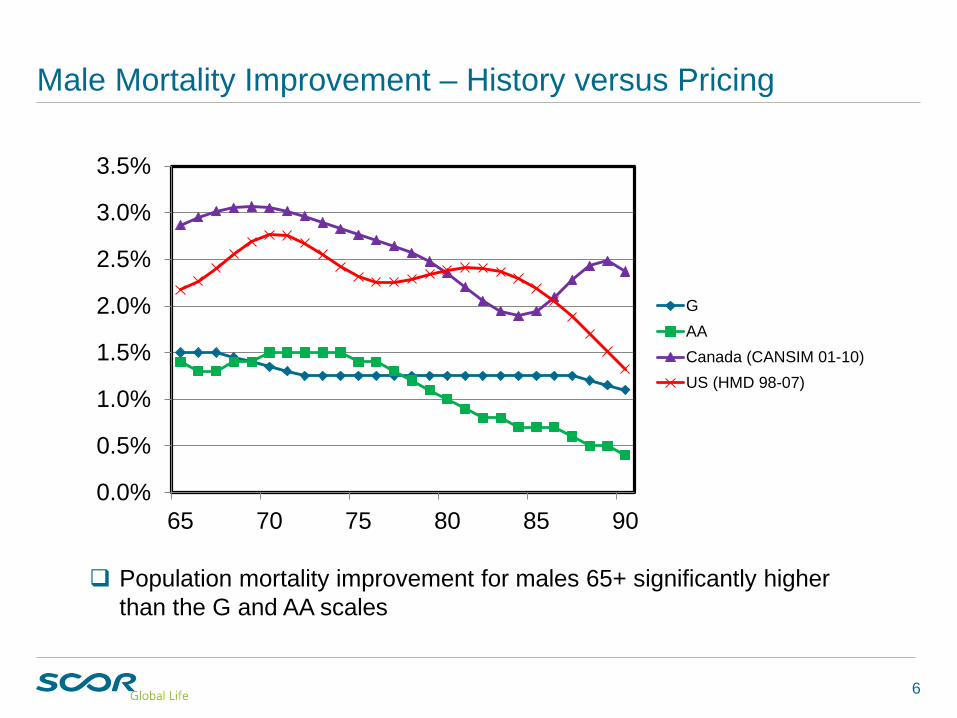

Male Mortality Improvement – History versus Pricing

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

65 70 75 80 85 90

GAACanada (CANSIM 01-10)US (HMD 98-07)

Population mortality improvement for males 65+ significantly higher than the G and AA scales

7

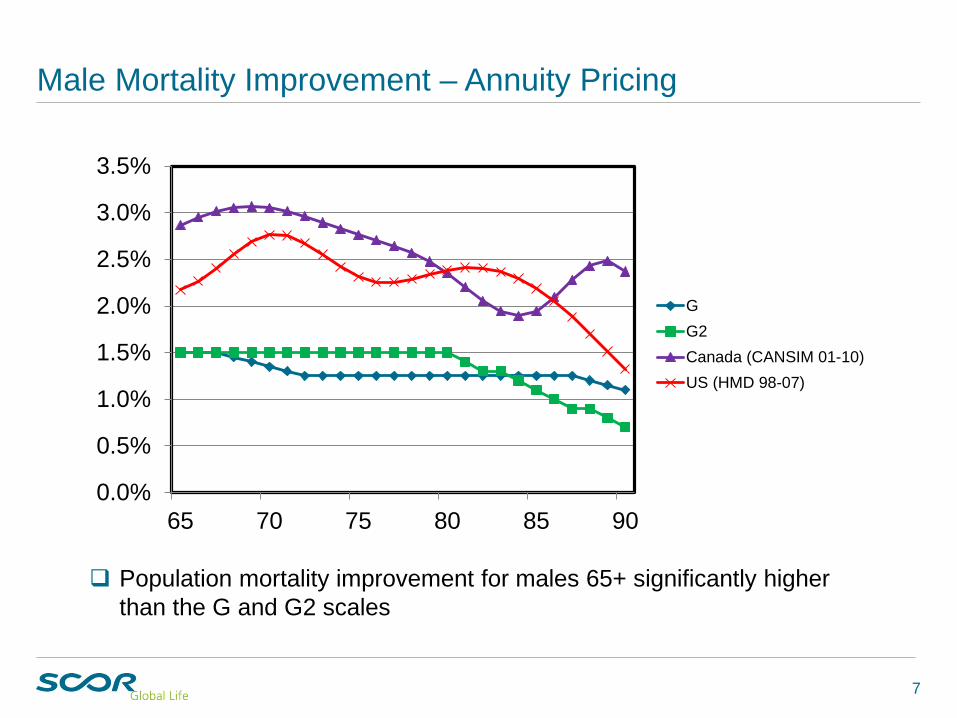

Male Mortality Improvement – Annuity Pricing

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

65 70 75 80 85 90

GG2Canada (CANSIM 01-10)US (HMD 98-07)

Population mortality improvement for males 65+ significantly higher than the G and G2 scales

8

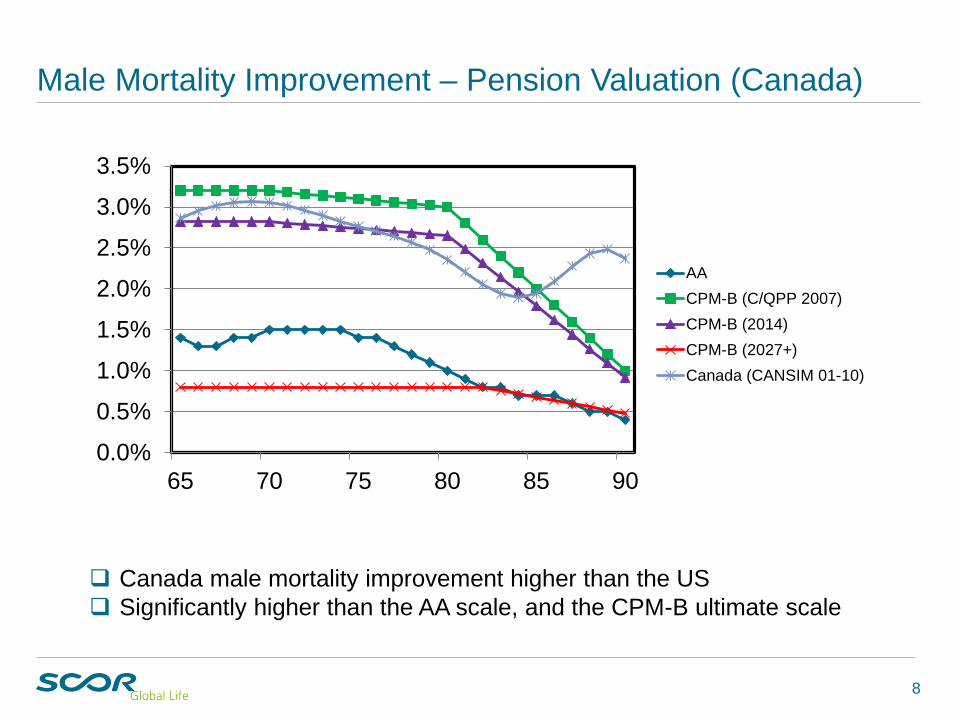

Male Mortality Improvement – Pension Valuation (Canada)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

65 70 75 80 85 90

AACPM-B (C/QPP 2007)CPM-B (2014)CPM-B (2027+)Canada (CANSIM 01-10)

Canada male mortality improvement higher than the US Significantly higher than the AA scale, and the CPM-B ultimate scale

9

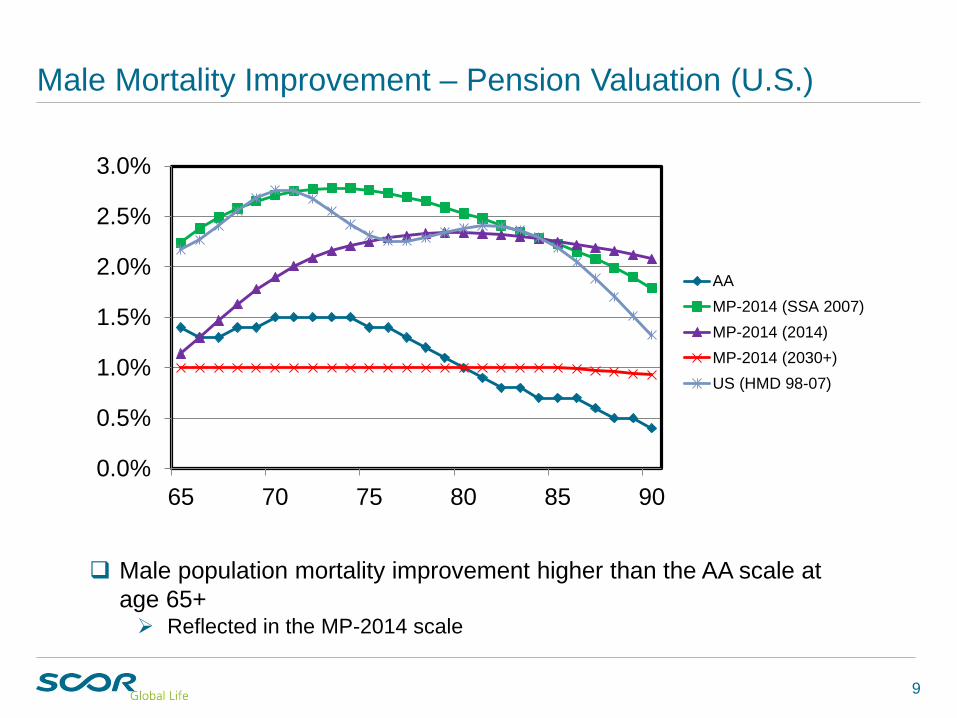

Male Mortality Improvement – Pension Valuation (U.S.)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

65 70 75 80 85 90

AAMP-2014 (SSA 2007)MP-2014 (2014)MP-2014 (2030+)US (HMD 98-07)

Male population mortality improvement higher than the AA scale at age 65+ Reflected in the MP-2014 scale

10

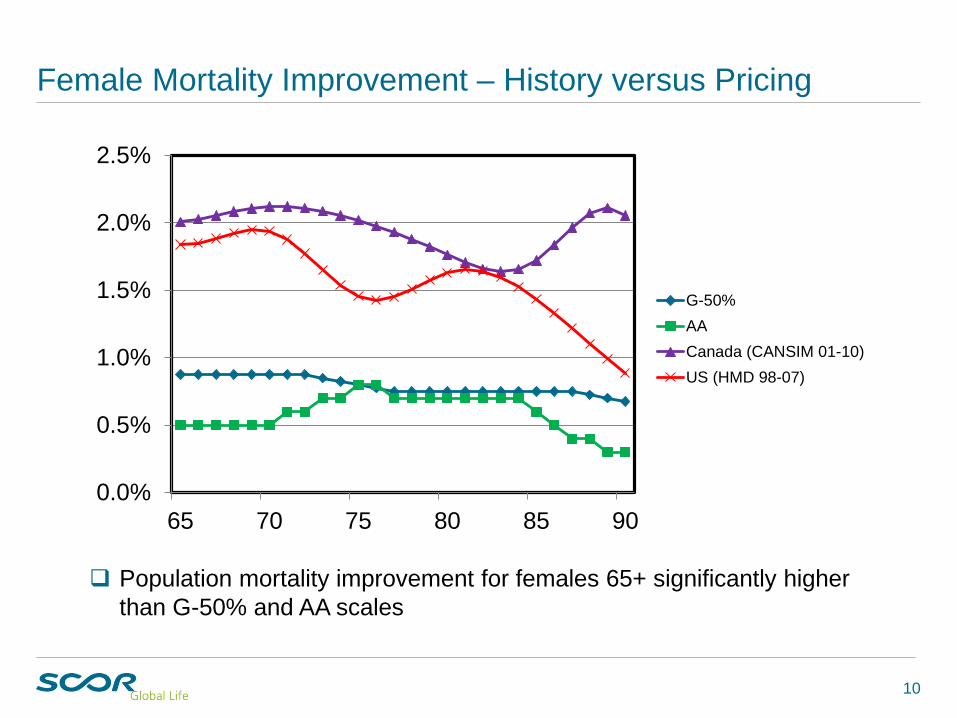

Female Mortality Improvement – History versus Pricing

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

65 70 75 80 85 90

G-50%AACanada (CANSIM 01-10)US (HMD 98-07)

Population mortality improvement for females 65+ significantly higher than G-50% and AA scales

11

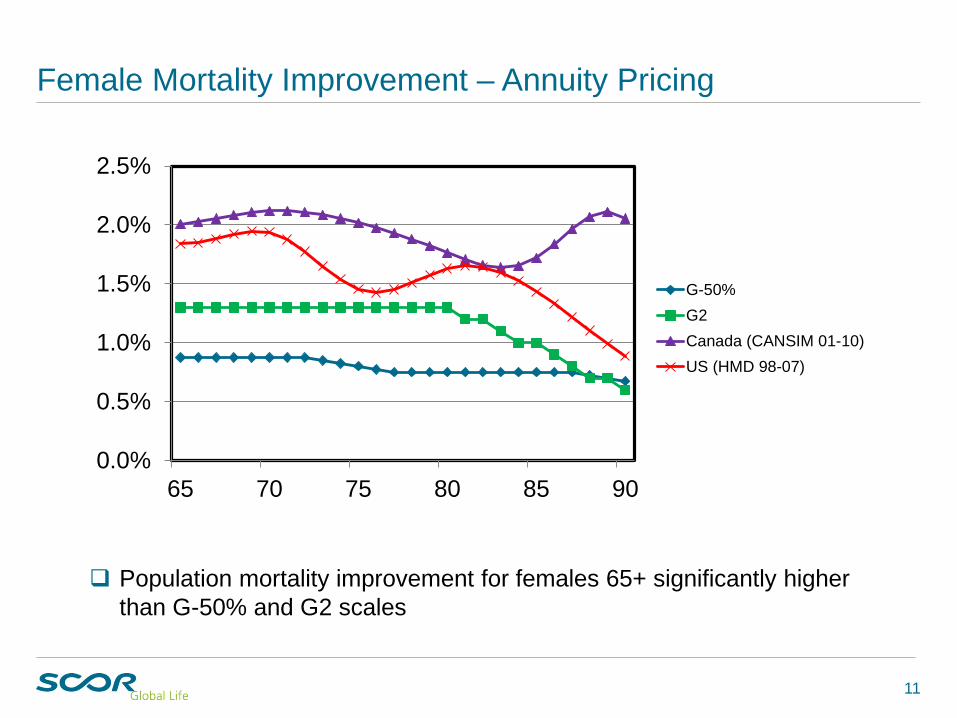

Female Mortality Improvement – Annuity Pricing

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

65 70 75 80 85 90

G-50%G2Canada (CANSIM 01-10)US (HMD 98-07)

Population mortality improvement for females 65+ significantly higher than G-50% and G2 scales

12

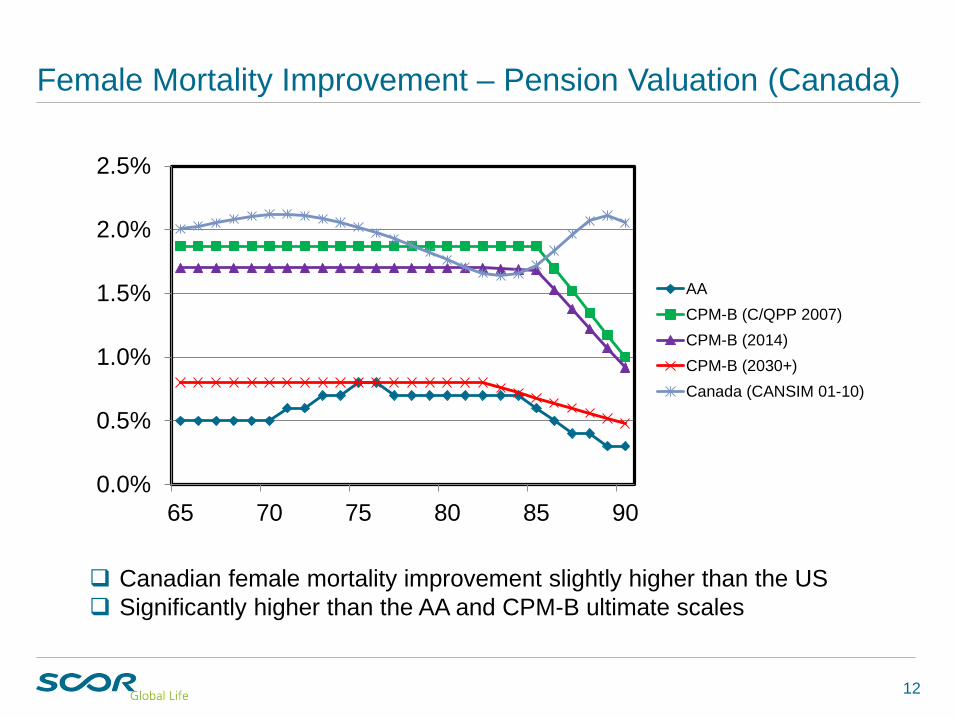

Female Mortality Improvement – Pension Valuation (Canada)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

65 70 75 80 85 90

AACPM-B (C/QPP 2007)CPM-B (2014)CPM-B (2030+)Canada (CANSIM 01-10)

Canadian female mortality improvement slightly higher than the US Significantly higher than the AA and CPM-B ultimate scales

13

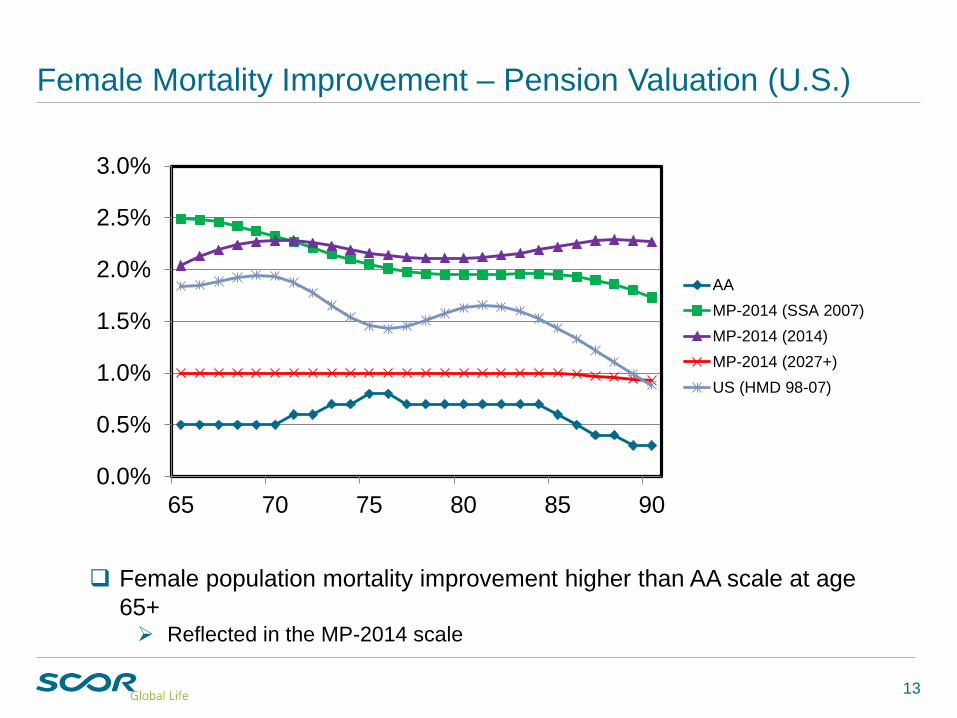

Female Mortality Improvement – Pension Valuation (U.S.)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

65 70 75 80 85 90

AAMP-2014 (SSA 2007)MP-2014 (2014)MP-2014 (2027+)US (HMD 98-07)

Female population mortality improvement higher than AA scale at age 65+ Reflected in the MP-2014 scale

14

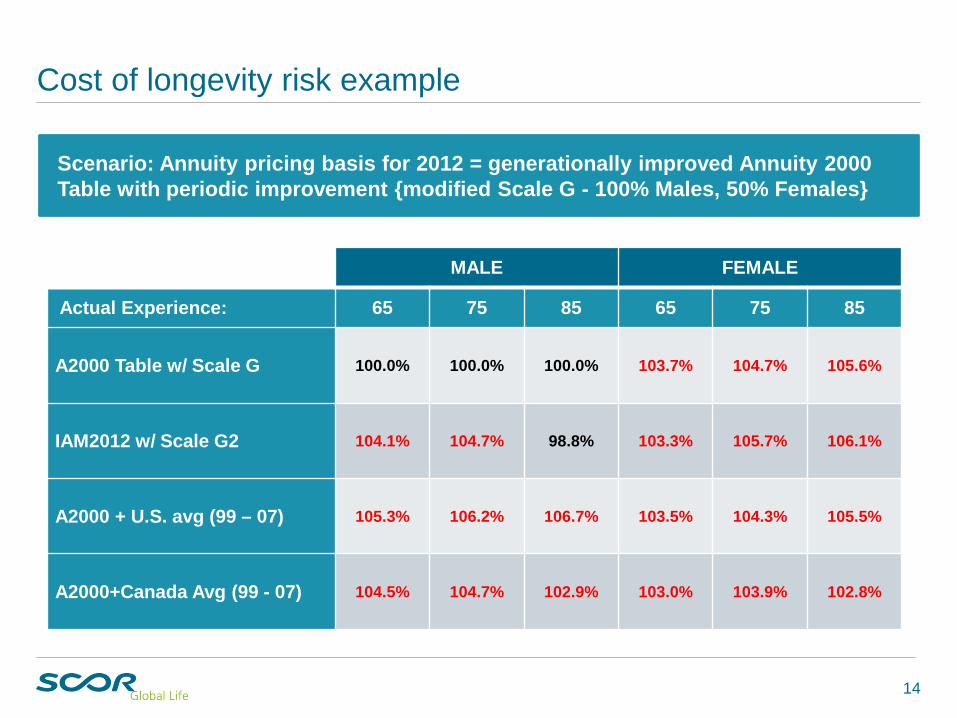

Cost of longevity risk example

Scenario: Annuity pricing basis for 2012 = generationally improved Annuity 2000 Table with periodic improvement {modified Scale G - 100% Males, 50% Females}

MALE FEMALE

Actual Experience: 65 75 85 65 75 85

A2000 Table w/ Scale G 100.0% 100.0% 100.0% 103.7% 104.7% 105.6%

IAM2012 w/ Scale G2 104.1% 104.7% 98.8% 103.3% 105.7% 106.1%

A2000 + U.S. avg (99 – 07) 105.3% 106.2% 106.7% 103.5% 104.3% 105.5%

A2000+Canada Avg (99 - 07) 104.5% 104.7% 102.9% 103.0% 103.9% 102.8%

2Q 2015 YOY % Change YTD YTD % Change

Single Premium Products

• Buy-outs $3828.4 729.6% $4718.0 606.2%

• Buy-ins 0 N/A 0 N/A

• Total $3828.4 591.8% $4718.0 520.8%

Terminal Funding $165.1 (2.1)% $330.4 2.4%

Insured/Guaranteed LDI $0.8 N.A $0.8 NA

Group Annuity Risk Transfer $3994.2 453.2% $5049.2 366.4%

Recent Deal Activity

Sales ($000,000)

Source: LIMRA International

15

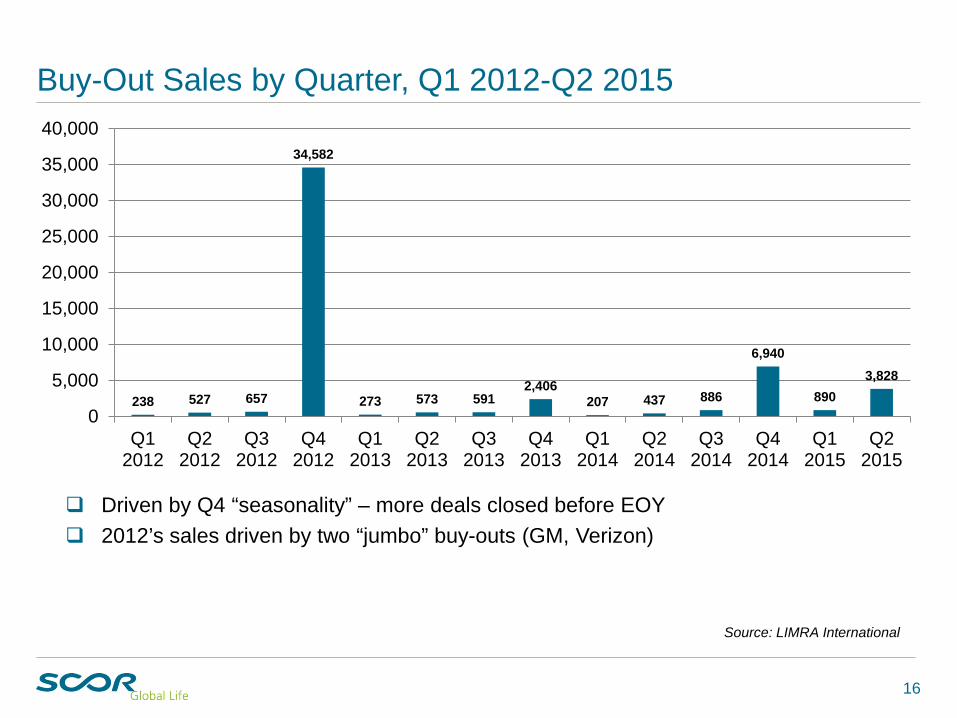

16

Buy-Out Sales by Quarter, Q1 2012-Q2 2015

238 527 657

34,582

273 573 5912,406

207 437 886

6,940

8903,828

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Driven by Q4 “seasonality” – more deals closed before EOY 2012’s sales driven by two “jumbo” buy-outs (GM, Verizon)

Source: LIMRA International

17

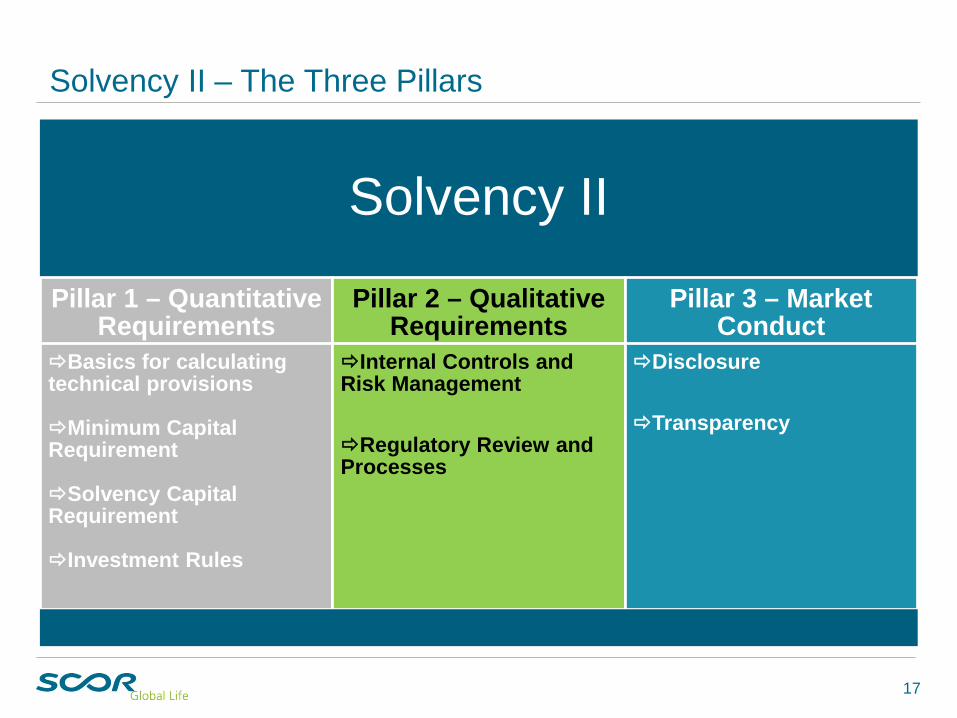

Solvency II – The Three Pillars

Solvency II

Pillar 1 – Quantitative Requirements

Basics for calculating technical provisions

Minimum Capital Requirement

Solvency Capital Requirement

Investment Rules

Pillar 2 – Qualitative Requirements

Internal Controls and Risk Management

Regulatory Review and Processes

Pillar 3 – Market Conduct

Disclosure

Transparency

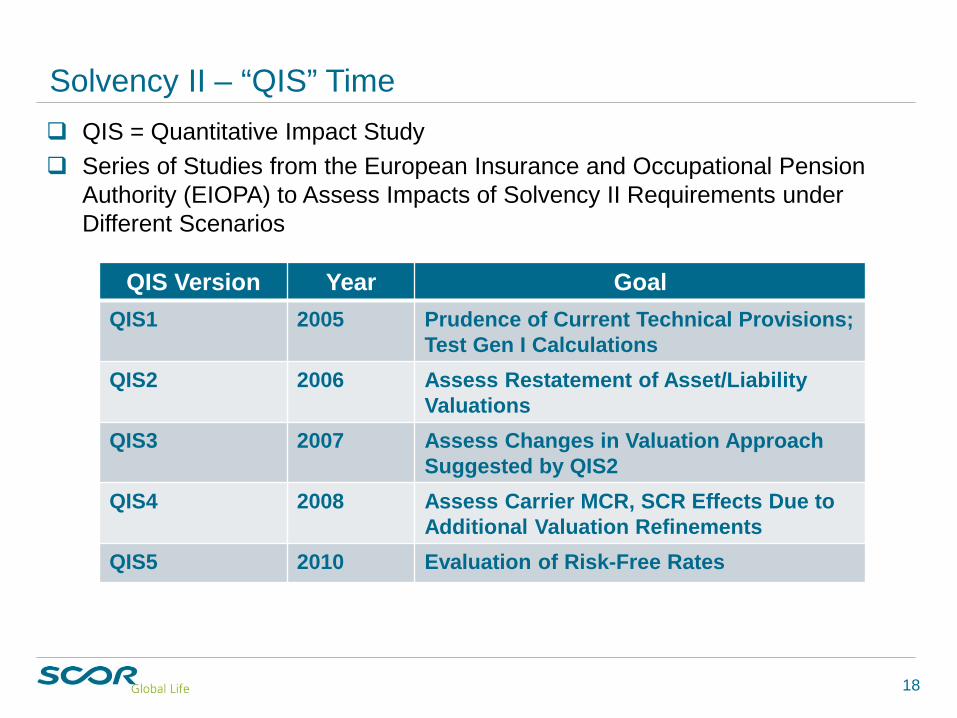

Solvency II – “QIS” Time QIS = Quantitative Impact Study Series of Studies from the European Insurance and Occupational Pension

Authority (EIOPA) to Assess Impacts of Solvency II Requirements under Different Scenarios

QIS Version Year GoalQIS1 2005 Prudence of Current Technical Provisions;

Test Gen I CalculationsQIS2 2006 Assess Restatement of Asset/Liability

ValuationsQIS3 2007 Assess Changes in Valuation Approach

Suggested by QIS2QIS4 2008 Assess Carrier MCR, SCR Effects Due to

Additional Valuation RefinementsQIS5 2010 Evaluation of Risk-Free Rates

18

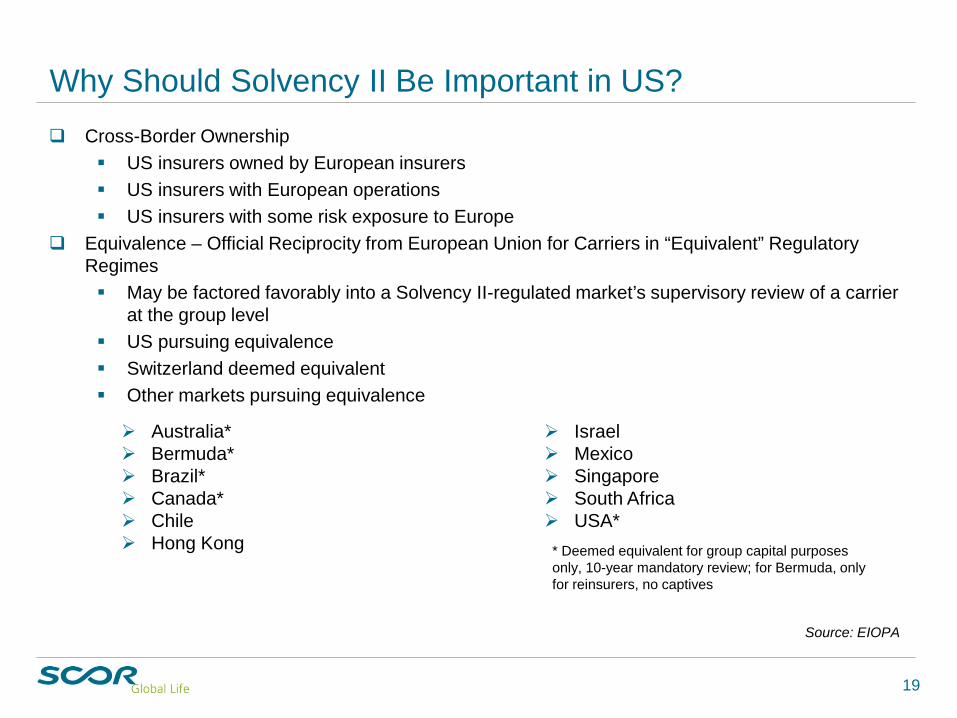

Why Should Solvency II Be Important in US? Cross-Border Ownership

US insurers owned by European insurers US insurers with European operations US insurers with some risk exposure to Europe

Equivalence – Official Reciprocity from European Union for Carriers in “Equivalent” Regulatory Regimes May be factored favorably into a Solvency II-regulated market’s supervisory review of a carrier

at the group level US pursuing equivalence Switzerland deemed equivalent Other markets pursuing equivalence

Source: EIOPA

Australia* Bermuda* Brazil* Canada* Chile Hong Kong

Israel Mexico Singapore South Africa USA*

19

* Deemed equivalent for group capital purposes only, 10-year mandatory review; for Bermuda, only for reinsurers, no captives