Session 1- SBA 101 MR - Edunomics...

31

SBA 101 Contents and slides may not be reproduced or referenced without permission and citation. Citation should include: Edunomics Lab at Georgetown University, 2017.

Transcript of Session 1- SBA 101 MR - Edunomics...

SBA101

Contentsandslidesmaynotbereproducedorreferencedwithoutpermissionandcitation.Citationshouldinclude:Edunomics LabatGeorgetownUniversity,2017.

1. Welcome!

2. SBA101:WhatisSBA?

3. SBADistrictCollaborativeNetwork:Whyanetwork?

SBA101

Federal$

State$

Local$

District$

School$

School$

School$

School$

Today’sfocus:Allocationofresourcesfromdistrictstoschools

Districtshaveafiduciaryresponsibilitytoapplyfundsequitablyacrossstudents

Comparingschoolsonperformancerequireslevelplayingfieldonspending

Allocationstrategiescandictateresourceuse,especiallyimportantamidstconstrainedresources

Allocationstrategiescaninhibitorenhanceeffortssuchasschoolautonomy,choice,accountabilityandcanaffectbehaviorinschools

Whydoesallocationmatter?

Per Pupil Costs for Each School

$3,000

$3,500

$4,000

$4,500

$5,000

$5,500

$6,000

DPS schools

Per

PU

pil

Exp

en

dit

ure

sForexample,DPSSpendingforeachschool,2005,beforeSBA

Isthisinequitable? Can’ttellbecausestudentmixdiffersacrossschools.

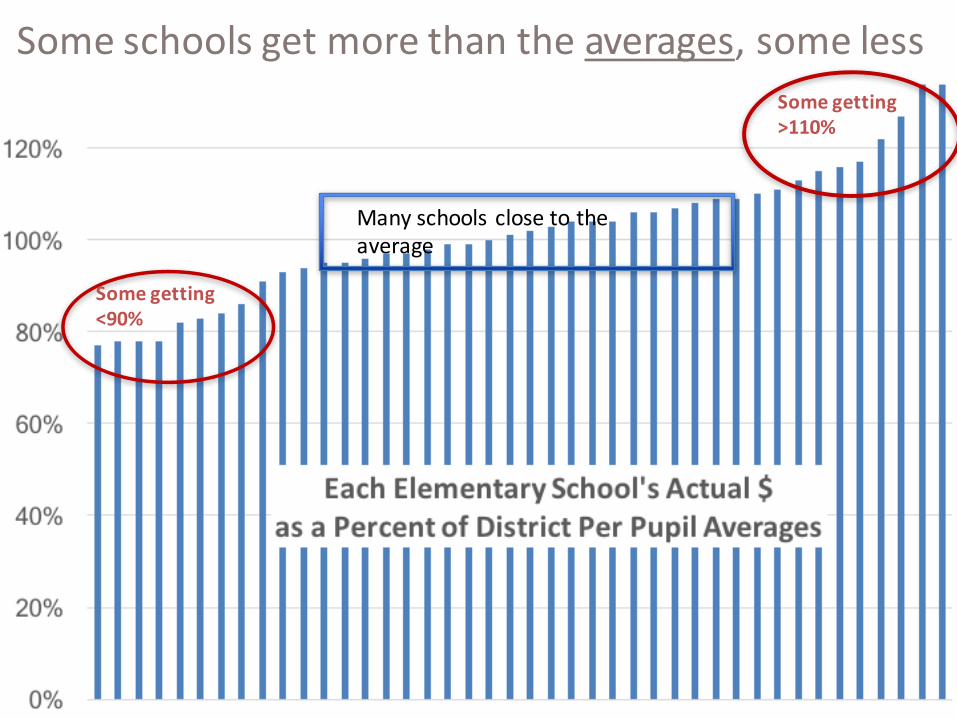

ONAVERAGE,districtwasspending:

$3,943perpupil$677perFRLpupil$407perBilingual$145perGifted

Butsomeschoolsgettingmorethanthoseaverages,andsomegettingless.

Someschoolsgetmorethantheaverages,someless

Manyschoolsclosetotheaverage

Somegetting>110%

Somegetting<90%

Dollarsareallocated(notstaffpositionsorotheringredients)onthebasisofstudents.Studentsareweightedaccordingtoneeds.

StudentBasedAllocation(SBA)models

Incontrast,traditionalallocationpractices distributepurchasedschoolingitems(staffpositions,supplies,books,etc.)toschools.

Chicago2005

Lookingatwhat’sspentateachschoolalsodoesn’t enablerelativecomparisons.

Traditionalstaffing-basedallocationmodel

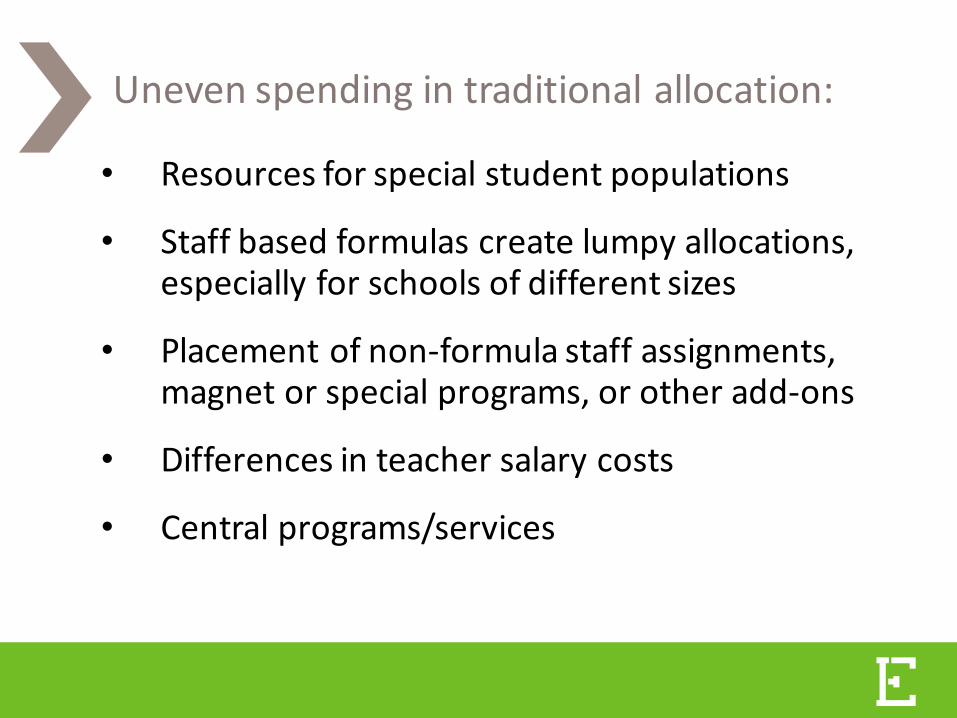

• Resourcesforspecialstudentpopulations

• Staffbasedformulascreatelumpyallocations,especiallyforschoolsofdifferentsizes

• Placementofnon-formulastaffassignments,magnetorspecialprograms,orotheradd-ons

• Differencesinteachersalarycosts

• Centralprograms/services

Unevenspendingintraditionalallocation:

Incontrast,student-basedallocationdivviesupfundsonthebasisofstudents.

StudentBasedAllocation(SBA)models

• Weightsaredeliberate• Formuladetailcanbesummarizedononepage• Districtleadersmanagetheweights,noteach

school’sallocationsorhowfundsareused• Spendingacrossschoolscanbecomparedin

percentagesintermstheirSBAallocation• Thedistrictspendsthesameamountona

studentregardlessofwherethatstudentattendsschool.

HowdoesSBAwork?The”averages”foreachstudentbecometheactualallocations:

$3,943perpupil$677perFRLpupil$407perBilingual$145perGifted

Districtscanrevisethebaseorweightstocreatemorepurposefulallocations

=BASE=.17or17%FRLweight=.10or10%Bilingualweight=.04or4%Giftedweight

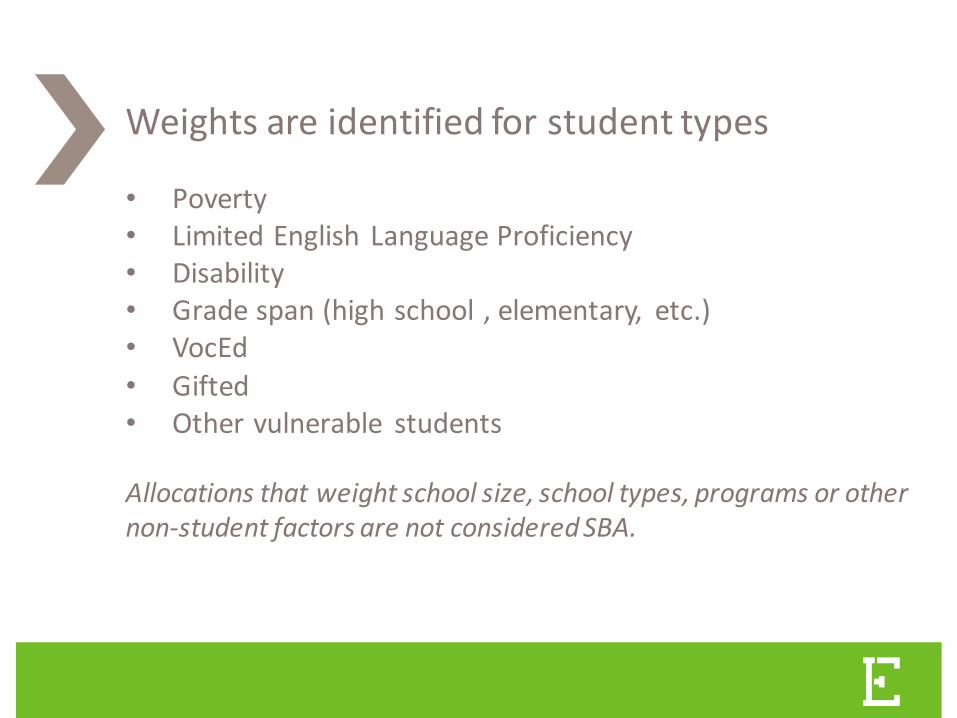

• Poverty• LimitedEnglish LanguageProficiency• Disability• Gradespan(highschool,elementary, etc.)• VocEd• Gifted• Othervulnerable students

Allocationsthatweightschoolsize,schooltypes,programsorothernon-studentfactorsarenotconsideredSBA.

Weightsareidentifiedforstudenttypes

E DUN OM I C S LAB AT GE ORGE TOWN UN I V E RSI TYE DUN OM I C S.GE ORGE TOWN .E D U

MetroNashvillePublicSchools

14

InitialstudentweightsinNashville.

PrinceGeorge’sCountyPublicSchoolDistrict

FY14Formula

• Equity• Transparency• Flexibilityinresourceuse• Accountability/Ownership• Studentchoiceandfundingportability• Financialsustainability• Service-orientedcentraldepartments

WhySBAmodelsaregainingtractioninU.S.

EDUNOMICS LAB AT GEORGETOWN UNIVERSITYEDUNOMICS.GEORGETOWN.EDU

Beyond equity, what value is there from school-level engagement in financials?

17

0

10

20

30

40

50

60

70

80

90

$2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000

Per

cent

of

stud

ents

mee

ting

wri

ting

sta

ndar

d

Per pupil spending by school (salary/benefits expenditures only)

Spending Vs Performance across WA state's high poverty elmentary schools

0

10

20

30

40

50

60

70

80

90

$2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000

Per

cent

of

stud

ents

mee

ting

wri

ting

sta

ndar

d

Per pupil spending by school (salary/benefits expenditures only)

Spending Vs Performance across WA state's high poverty elmentary schools

A. Weakrelationshipbetween$andoutcomesB. Twoschoolscouldspendsame$andget

differentoutcomesC. Couldspendsame$insameway andget

differentoutcomes(e.g.substantialschooleffects).

D. Verylittleawarenessatschoollevelofschooleffects

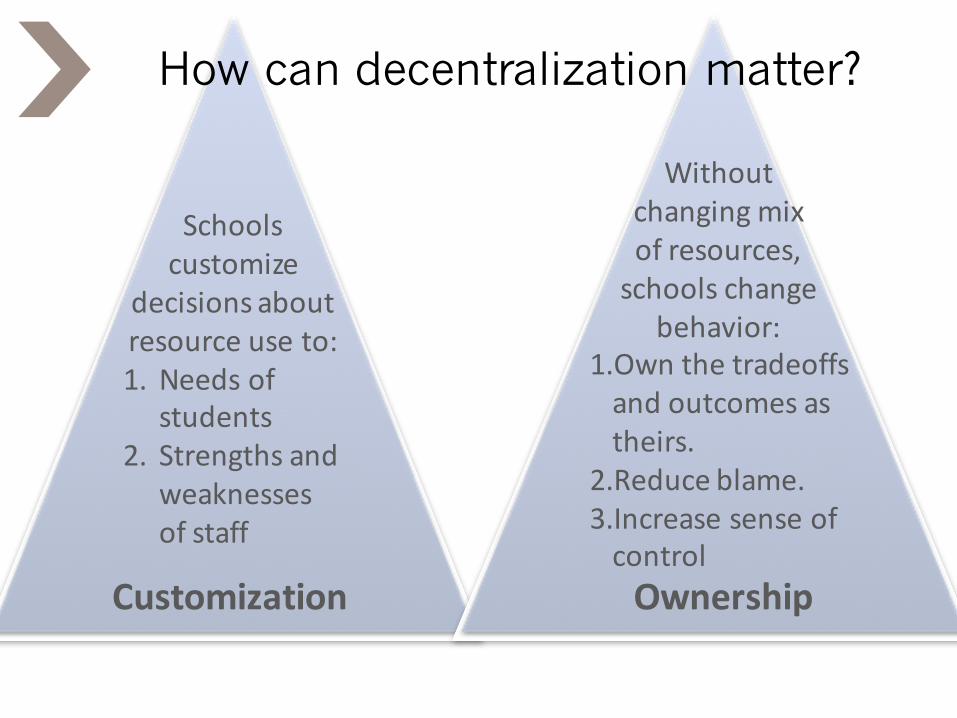

Schoolscustomize

decisionsaboutresourceuseto:1. Needsof

students2. Strengthsand

weaknessesofstaff

Customization

Withoutchangingmixofresources,schoolschange

behavior:1.Ownthetradeoffsandoutcomesastheirs.

2.Reduceblame.3.IncreasesenseofcontrolOwnership

How can decentralization matter?

EDUNOMICS LAB AT GEORGETOWN UNIVERSITYEDUNOMICS.GEORGETOWN.EDU

Onaverage,theylist____ barriersperprincipal! *

*Miller(2014). Policy barrierstoschool improvement:What’s realandwhat’simagined?CRPE.http://www.crpe.org/publications/policy-barriers-school-improvement-whats-real-and-whats-imagined

Whenprincipalsareaskedwhatstandsinthewayofleveragingtheirdollarstogetgreateroutcomesforstudents

21

Resource allocation

37%

Instructional innovation

40%

Teacher quality23%

16

• Notasmuchbenefitforsmalldistricts.

• Somedistrictsdon’thaveaplanforschoolswithdecliningenrollment. (Unwilling tocloseorallow flexible staffingwhenschoolshaveinsufficient resourcesforprototypicalstaffing).(Seattle)

• Createsadisconnectindistrictswantinglargecentraloperations.

• Notcompatiblewithdistrictswantinguniformity inservices

WhatisthecaseagainstSBA?

• Weightsinitiallyreflectexistingaverages(tominimizewinners/losers).

• Somedistrictsuseapilot.• Someallowholdharmless.• Ofteninitiallyuseaveragesalariesin

budgeting.• Overtime,moremoneyaddedtothe

“formula”

WhatdoesSBAimplementationlooklike?

Initially, most schools make only modest changes with their budgeting flexibility.

Changes that do take place, do so on the margin.

Principalsknowwhatstuffcosts

• Identify highest and lowest paid staff and examine workloads

• Consider costs of all functions in per pupil terms

• Are some services costing too much?• Consider tradeoffs. What else could this

money buy?• Changes will come from REALLOCATION

(vs. new monies).

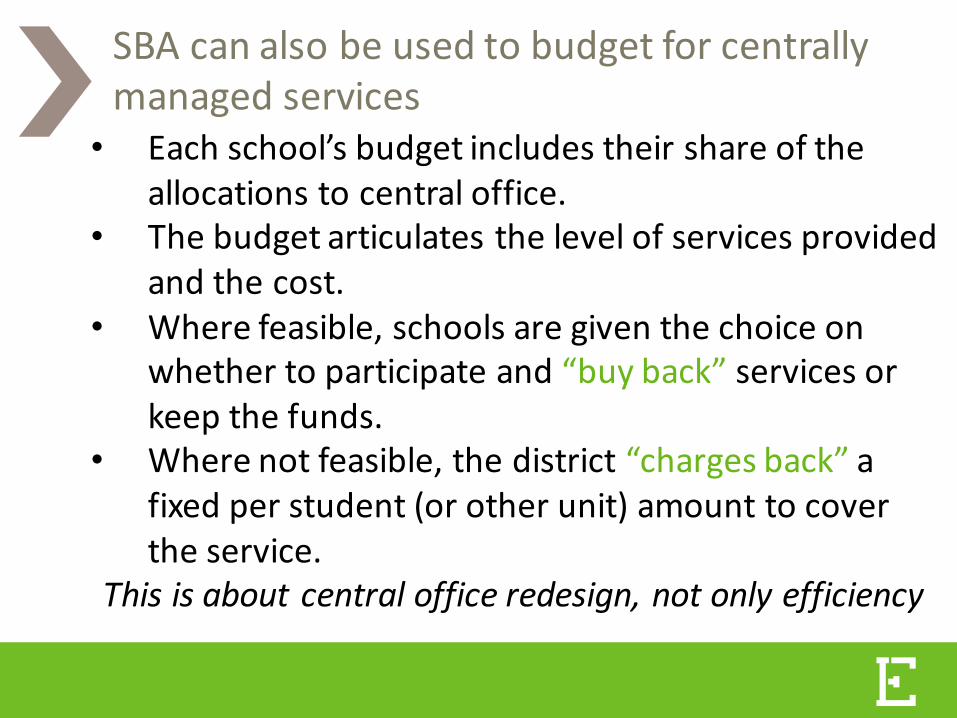

• Eachschool’sbudgetincludestheirshareoftheallocationstocentraloffice.

• Thebudgetarticulatesthelevelofservicesprovidedandthecost.

• Wherefeasible,schoolsaregiventhechoiceonwhethertoparticipateand“buyback”servicesorkeepthefunds.

• Wherenotfeasible,thedistrict“chargesback”afixedperstudent(orotherunit)amounttocovertheservice.

Thisisaboutcentralofficeredesign,notonlyefficiency

SBAcanalsobeusedtobudgetforcentrallymanagedservices

Pricingexamplesforcentrallymanagedservices

• Superintendent’soffice– $8.56perpupil,Chargeback

• Boardofdirectors– $5.02perpupil,Chargeback

• Accountability,research/datasupport– $6.80perpupil,Chargeback

• C&I:Educationalplanreview– $3082perschool,Buyback

• Grantwriting– $80perhour,Buyback

• Maildelivery– $2200for5days/wk,$900for2days/wk,$500for1day/wk

Districtfinanceleadsmeetviawebinar1Xmonth.Edunomics Labhosts

Dynamicandevolvinggroup—topicsdrivenbytheneedsofthepartnerdistricts

Threeprimarygoals:

• ToshareknowledgetosolvedistrictchallengesaroundproblemsofSBApractice

• Tocollectivelyproduceresearchdistrictsneedandwant• Toserveasatrustedprofessionalnetworkfordistrictfinanceleaders

specifictoaninnovativestudent-basedfinancialstrategy

SBADistrictCollaborativeNetwork

StudentBasedAllocationWorkingGroup

Atlanta Public SchoolsAustin Independent School DistrictBaltimore City Public SchoolsBoston Public SchoolsCamden City SchoolsChicago Public SchoolsCleveland Metropolitan School DistrictDenver Public SchoolsD.C. Public SchoolsDurango School DistrictHartford Public SchoolsHouston Independent School DistrictIndianapolis Public Schools

Metropolitan Nashville Public SchoolsMilwaukee Public SchoolsMinneapolis Public SchoolsNew Haven Public SchoolsNew York City DoENewark Public SchoolsOrleans Parish School BoardShelby County SchoolsSpokane Public SchoolsSyracuse City SchoolsTulsa Public Schools

NextMeetings

November14,2017

Possibleupcomingtopics• ESSAimpactondistricts• California’sLCFFresearchupdate• Takingstockofsalaryimpacts– andpossibleremedies• Communitybasedpartnerships• Achallengeposedbyonedistricttothegroup• Otherideas– [email protected]

Contentsandslidesmaynotbereproducedorreferencedwithoutpermissionandcitation.Citationshouldinclude:Edunomics LabatGeorgetownUniversity,2017.