Services · PDF fileFinancial Services Board Slide 4 Don’t assume exemptions &...

14

July 2015

Transcript of Services · PDF fileFinancial Services Board Slide 4 Don’t assume exemptions &...

July 2015

Financial

Services

Board

RELATIONSHIPS WITH STAKEHOLDERS

Rosemary Hunter

Deputy Registrar, Pension Funds

Annual conference of the Institute for

Retirement Funds Africa, Cape Town,

July 2015

Financial

Services

Board

Slide 3

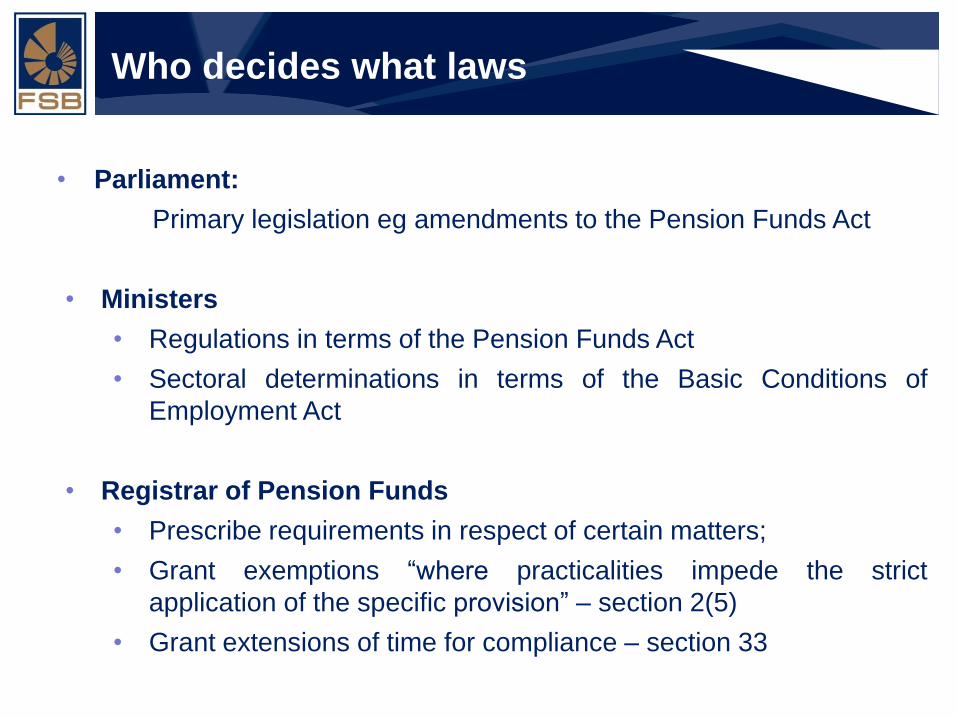

Who decides what laws

• Parliament:

Primary legislation eg amendments to the Pension Funds Act

• Ministers

• Regulations in terms of the Pension Funds Act

• Sectoral determinations in terms of the Basic Conditions of

Employment Act

• Registrar of Pension Funds

• Prescribe requirements in respect of certain matters;

• Grant exemptions “where practicalities impede the strict

application of the specific provision” – section 2(5)

• Grant extensions of time for compliance – section 33

Financial

Services

Board

Slide 4

Don’t assume exemptions &

extensions will be granted

• Exemptions

o No exemptions from obligation to give members the right to elect

board members, other than in terms of section 7B.

o Don‟t let your section 7B exemption lapse before applying for its

renewal.

• Extensions

o Don‟t let time periods for compliance to expire before applying for

extension – will only be granted in special circumstances. May still

consider main application but will impose administrative penalty for

non-compliance

Financial

Services

Board

Slide 5

Who is being represented

• Requests for exemptions and extensions often made by service

providers, usually fund administrators

• They are also those who have complained the loudest about

changes in registrar’s approach to

• the granting of exemptions and extensions;

• the governance, closure and cancellations of the registrations of

dormant and shell funds;

• the commencement and termination of employer participation in

umbrella funds.

Financial

Services

Board

Slide 6

For whose benefit are these

complaints made?

• This is understandable – particularly if they have made

arrangements to conduct business on the assumptions that past

practices would continue;

• But also not understandable – service providers and funds should

operate on the basis of legal compliance, even if non compliance has

been condoned in the past.

• Registrar’s changes designed to improve protection of members

and beneficiaries per his mandate.

Financial

Services

Board

Slide 7

Registrar as guardian

„[176] … one of the reasons why the legislature has seen fit to grant

extensive powers of supervision and control to the registrar is that the

members of pension funds often do not have the knowledge, skill or

resources to take adequate steps to protect themselves. Their right to do

so is, of course, not taken away by the PF Act, but this does not detract

from the conclusion which in my view can fairly be drawn from the

provisions of the PF Act and the FI Act, namely that the registrar fulfils an

important function as the guardian of the interests of members of pension

funds.

Financial Services Board & another v De Wet (in his capacity as liquidator

of the Pepkor Pension Fund) & others [2002] 4 BPLR 3259 (C) or [2002]

JOL 9319 (C) at paragraphs [176]

• But the registrar cannot protect all members and beneficiaries

• And we cannot assume that the boards of their funds, or even their

trade unions, are mandated by those members and beneficiaries to act

as they do in relation to retirement fund matters

Financial

Services

Board

Slide 8

Who represents members?

• Not the boards of retirement funds

“Section 7C deals with the object of the board which is to direct and control

the operations of the fund. Subsection (2) then proceeds to give guidance

to the board as to how that object should be pursued. Insofar as the

section enjoins the trustees to act in the interests of members, it must

therefore be understood in the context of steps taken in the direction,

control and oversight of the fund. It does not appoint the board as the

agent or representative of members to conduct litigation on their behalf,

even against the wishes of individual members. As illustrated by the facts

of this case, the interests of all the members of a fund do not always

coincide. Furthermore, there is the obvious potential of a conflict between

the interests of the fund, on the one hand and those of its members. on the

other.”

City of Johannesburg & others v SALA Pension Fund & others, judgment of

the Supreme Court of Appeal dated 9 March 2015

Financial

Services

Board

Slide 9

Who represents members?

• Not trade unions

o Not all members of a retirement fund will be members of a trade

union.

o And, even if they are, they may not have specifically mandated the

trade union to represent them in regard to matters relating to the

conduct of the retirement fund‟s business.

Financial

Services

Board

Slide 10

Who should the registrar consult before

prescribing new rules and standards?

• Answer: The public as a whole.

• But whose voices do we hear? o Service providers

o Industry bodies

The Actuarial Society of Southern Africa (ASSA);

The Association for Savings and Investments South Africa (ASISA);

The Council of Retirement Funds for South Africa (Batseta);

The Independent Regulatory Authority for the Auditing Profession

(IRBA);

The Institute for Retirement Funds Africa (IRFA):

The Municipal Retirement Organisation (MRO);

The Pension Lawyers Association (PLA);

The South African Institute for Chartered Accountants (SAICA) o Trade unions (but not often enough)

o Employer associations (although very seldom)

o Financial journalists

o ;

Financial

Services

Board

Slide 11

Whose voices does the registrar

hear?

• All of these bodies are important – the registrar needs the insights

derived from their knowledge, skill and experience.

• But only a few can be said to be truly “representative” of any

particular stakeholder group.

• We all need to accept our limitations

• We cannot assume that the registrar and/or any of these bodies

always knows what is in the best interests of members

• Let us acknowledge – as the IRFA leadership has done – that

bodies like IRFA are not “representative” of any specific

stakeholder groups. IRFA provides important forums for

discussion and debate and policymakers need to consider the

various views expressed.

Financial

Services

Board

Slide 12

All of us should help to empower

financial customers

• Consumer education and empowerment

• High school curricula

• Personal finance information conveyed through the media

• Community events

• Advice centres

• Education and empowerment of trade unions

• Education and empowerment of employers and their

associations

• Education and empowerment of community organisers

Note that some calling themselves community organisers are dodgy –

eg those claiming to represent thousands of people entitled to

unclaimed benefits, unclaimed surplus allocations and the like.

Financial

Services

Board

Slide 13

Education and empowerment of

board members & POs

• The effective governance, management and operation of

retirement funds is still the most important mechanism by which

the rights of members and beneficiaries of retirement funds will

be protected.

• Registrar will be prescribing training requirements for board members

– this must not be seen as promoting the replacement of member-

elected board members by professional trustees.

• Registrar will also be prescribing other governance requirements.

• But the main legal duties of board members and POs are clear – and

each board member and each PO must be able to account for his or

her conduct as such – some are already being required to do so in

relation to contentious decisions taken by boards collectively.

Qu

esti

on

s?