Sequenal decisions under uncertainty

24

Sequen&al decisions under uncertainty KTH/EES PhD course Lecture 7

Transcript of Sequenal decisions under uncertainty

Sequen&al decisions under uncertainty

KTH/EES PhD course Lecture 7

Lecture 7

• MDP: extensions – POMDP

– Limit theorems

• Mul&‐armed bandit problems – Introduc&on – Lower regret bound

POMDP

Present state Next state Ac&on

Reward

• Set of states: • Set of ac&ons available in state s: • These sets are finite, countably infinite, or compacts subsets

of a Euclidian space (finite dimension)

• Time horizon

S

As, A = ∪s∈SAs

Observa&ons

Present state Next state Ac&on

Reward

• The state is not fully observable • Observa&on at &me t: • Observa&on probabili&es:

Ot

o(a, s, z) = P [Ot = z|Xt = s, Yt−1 = a]

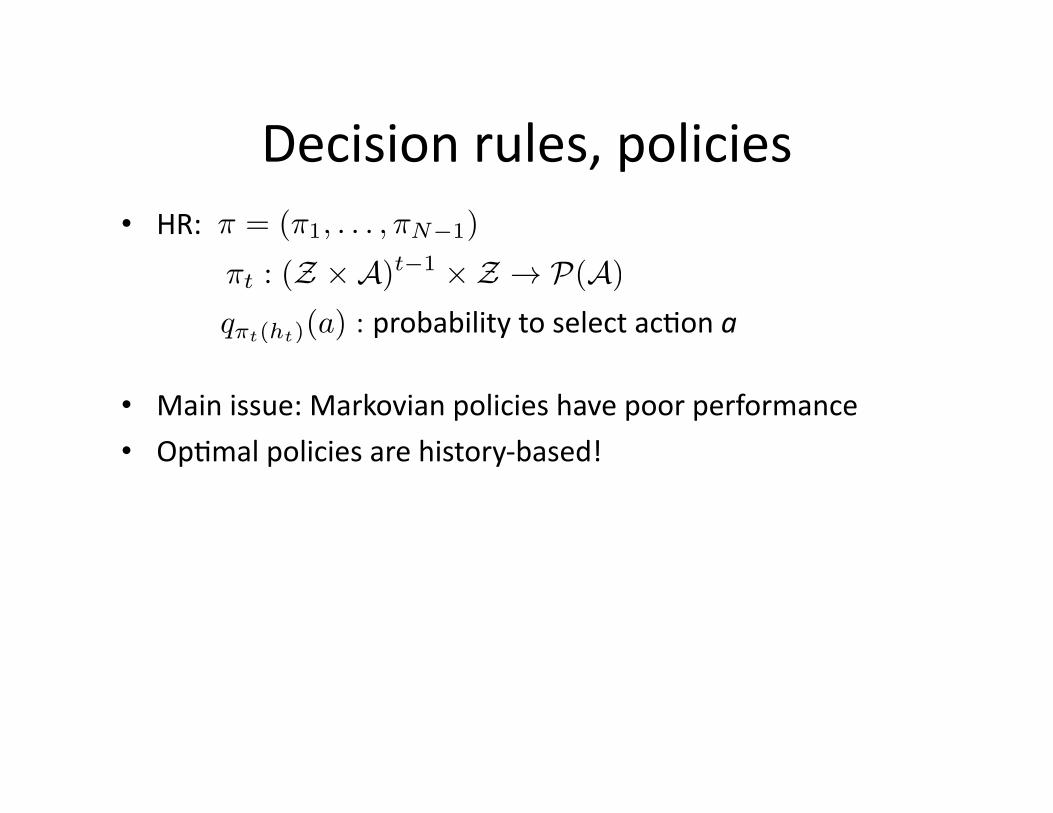

Decision rules, policies • HR:

• Main issue: Markovian policies have poor performance

• Op&mal policies are history‐based!

π = (π1, . . . ,πN−1)

qπt(ht)(a) : probability to select ac&on a

πt : (Z ×A)t−1 × Z → P(A)

Informa&on states • An informa&on state is a distribu&on on the state space: it is

our belief for the state distribu&on, given the history

• Bayesian approach. Upda&ng belief distribu&on: – At &me t: belief b

– At &me t+1, given that ac&on a was chosen, and observa&on z has just been made,

• Markovian structure recovered (MDP)

baz(s′) =

o(a, s′, z)∑

s p(s′|s, a)b(s)∑

s,s′′ o(a, s′′, z)p(s′′|s, a)b(s)

More on POMDP • Read Anthony Cassandra’s thesis: “Exact and Approximate Algorithms for POMDP”

Limit theorems • Read Kushner Dupuis book: “Numerical methods for stochas&c control problems in con&nuous &me”

• … or Kushner’s paper (same &tle), SIAM J. Control and Op&miza&on, 1990

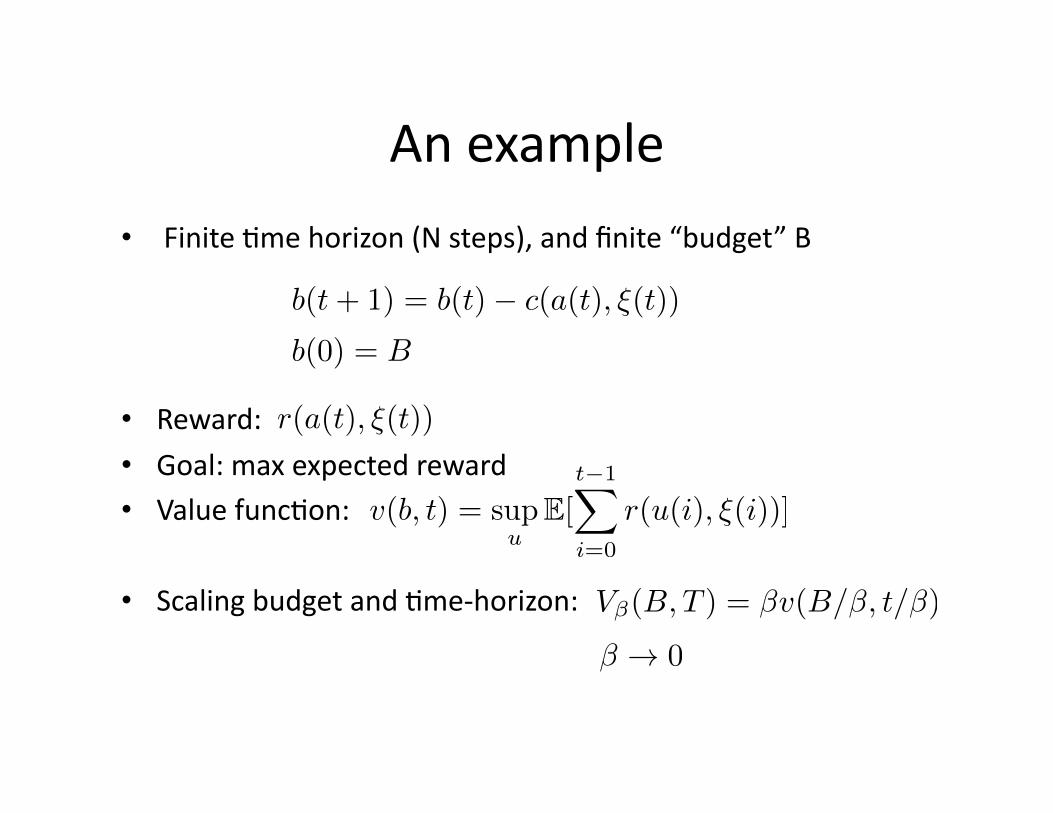

An example

• Finite &me horizon (N steps), and finite “budget” B

• Reward: • Goal: max expected reward • Value func&on:

• Scaling budget and &me‐horizon:

b(t+ 1) = b(t)− c(a(t), ξ(t))

r(a(t), ξ(t))

b(0) = B

v(b, t) = supu

E[t−1∑

i=0

r(u(i), ξ(i))]

Vβ(B, T ) = βv(B/β, t/β)

β → 0

An example

• Result: exists and solves V (B, T ) = limβ→0

Vβ(B, T )

V (B, T ) = supu

∫ τ∧T

0r̄(u(t))dt

τ = inf{t ≥ 0 : B(t) = 0}

dB

dT= −c̄(u(t))

r̄(a) = Eξ[r(u, ξ(0)], c̄(a) = Eξ[c(u, ξ(0)]

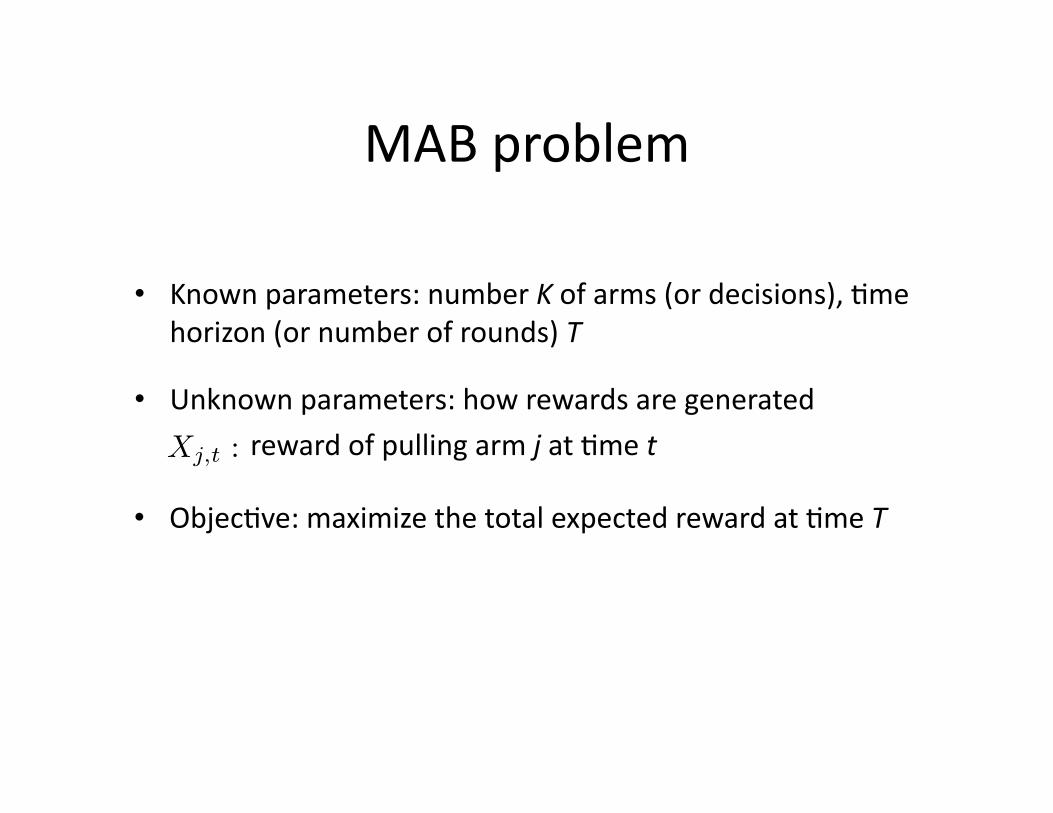

Mul&‐Armed Bandit (MAB)

MAB problem

• Known parameters: number K of arms (or decisions), &me horizon (or number of rounds) T

• Unknown parameters: how rewards are generated

reward of pulling arm j at &me t

• Objec&ve: maximize the total expected reward at &me T

Xj,t :

Stochas&c vs. Adversarial

• Stochas&c: rewards sampled from an unknown distribu&on – Example: IID case,

• Adversarial sedng: rewards chosen by an adversary ‐ Oblivious adversary:

‐ Adap&ve adversary: rewards depend on the history (selected arms so far)

(Xj,t, t = 1, 2, ...) µjIID random variables with mean

(Xj,t, t = 1, 2, ...) chosen ini&ally (at &me 0)

Applica&ons

• Clinical trials (Thompson 1933)

• Ads placement on webpages • Rou&ng problems

• …

Outline of the next lectures

• Asympto&cally op&mal policies for IID MAB + UCB policies

• Finite‐&me analysis of IID MAB • Large number of arms

– Unstructured rewards – Structured rewards

• Adversarial MAB

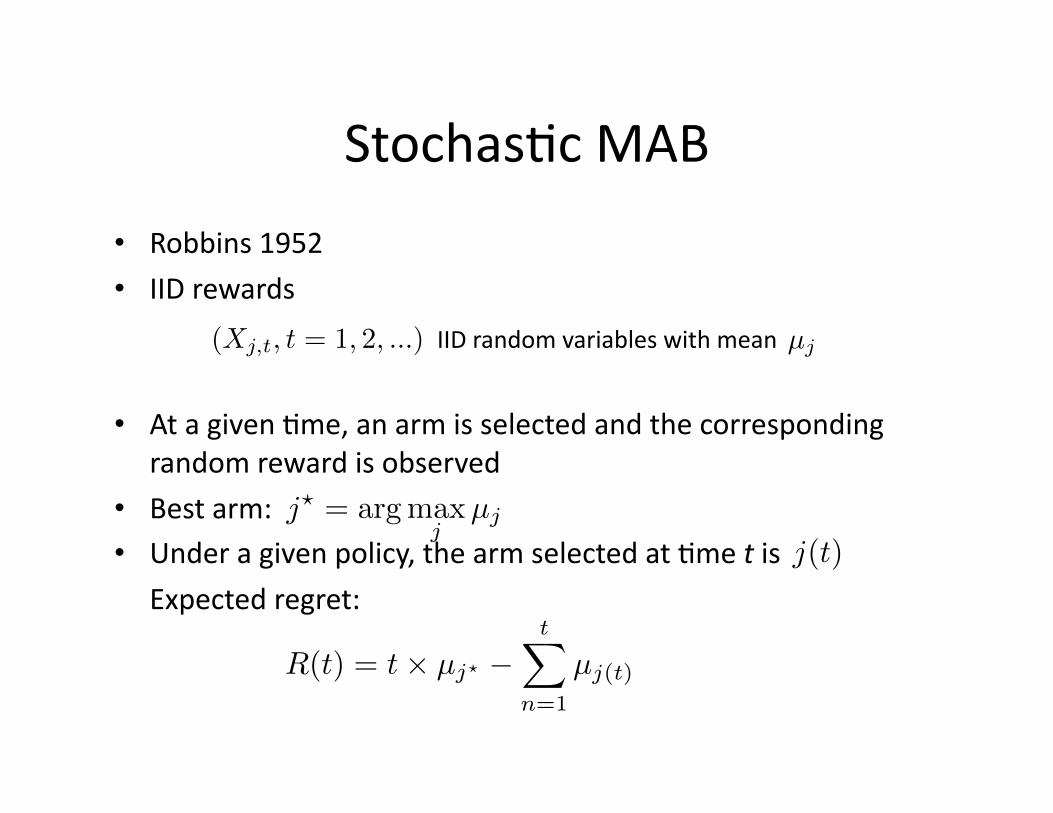

Stochas&c MAB

• Robbins 1952 • IID rewards

• At a given &me, an arm is selected and the corresponding random reward is observed

• Best arm: • Under a given policy, the arm selected at &me t is

Expected regret:

(Xj,t, t = 1, 2, ...) µjIID random variables with mean

j! = argmaxj

µj

j(t)

R(t) = t× µj! −t∑

n=1

µj(t)

Parametric model

• Measure on

• Reward distribu&ons parametrized by • Configura&on: • Arm j reward distribu&on:

• Kullback‐Leibler divergence:

R : ν

θ ∈ RC = (θ1, . . . , θK)

Xj,t ∼ f(x, θj)dν(x)∫|x|f(x, θj)dν(x) < ∞

∫xf(x, θj)dν(x) = µ(θj)

I(θ,λ) =

∫log

[f(x, θ)

f(x,λ)

]f(x, θ)dν(x)

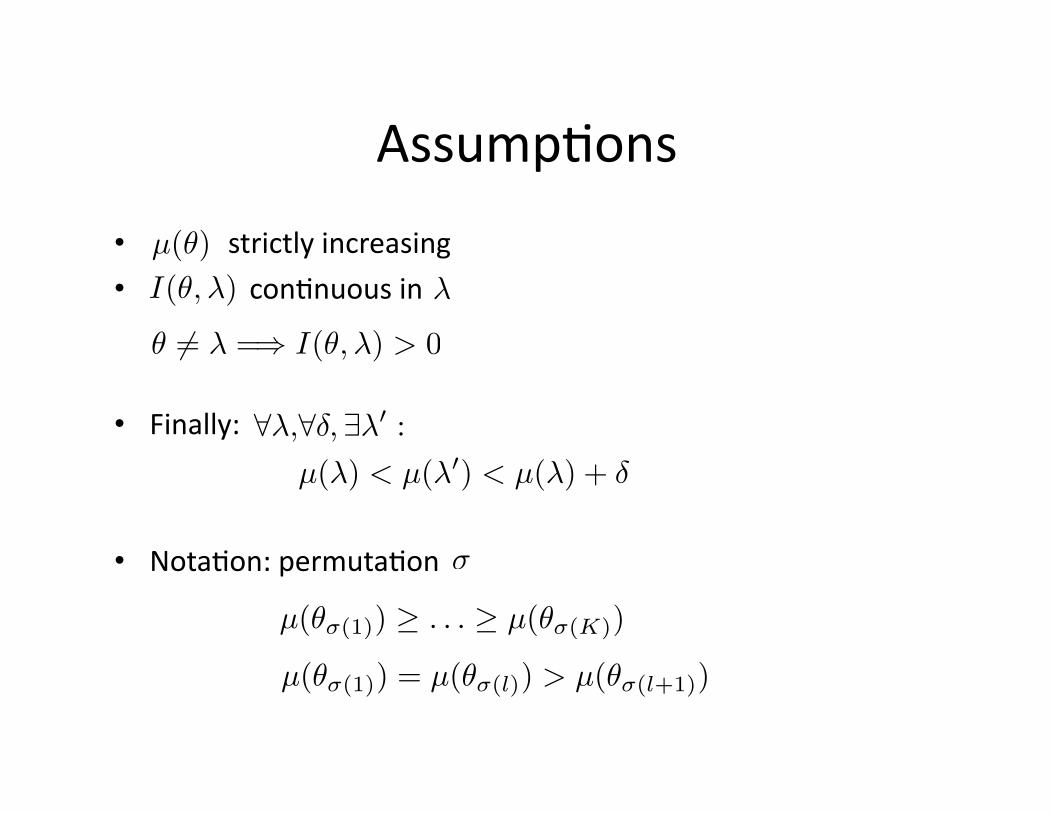

Assump&ons

• strictly increasing • con&nuous in

• Finally:

• Nota&on: permuta&on

µ(θ)

θ != λ =⇒ I(θ,λ) > 0

I(θ,λ) λ

∀λ,∀δ, ∃λ′ :

µ(λ) < µ(λ′) < µ(λ) + δ

σ

µ(θσ(1)) ≥ . . . ≥ µ(θσ(K))

µ(θσ(1)) = µ(θσ(l)) > µ(θσ(l+1))

Example: Bernoulli rewards

• Rewards take values in {0,1} • Measure : • We have:

ν

θ ∈ [0, 1]

ν = δ0 + δ1

µ(θ) = θ

I(θ,λ) = θ log

[θ

λ

]+ (1− θ) log

[1− θ

1− λ

]

Regret and uniformly good rules

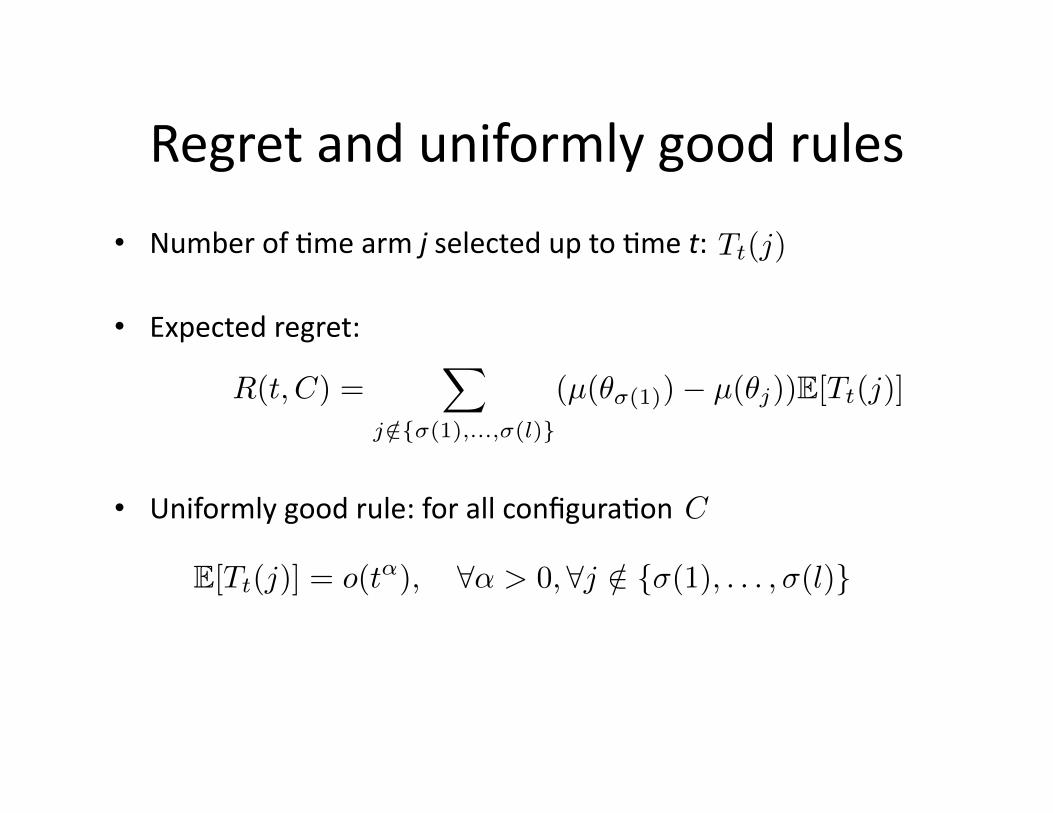

• Number of &me arm j selected up to &me t:

• Expected regret:

• Uniformly good rule: for all configura&on

Tt(j)

R(t, C) =∑

j /∈{σ(1),...,σ(l)}

(µ(θσ(1))− µ(θj))E[Tt(j)]

C

E[Tt(j)] = o(tα), ∀α > 0, ∀j /∈ {σ(1), . . . ,σ(l)}

Lower bound on regret Lai and Robbins 1985

Theorem Consider any uniformly good rule.

Configura&on:

Hence:

C = (θ1, . . . , θK)

∀ε > 0, ∀j /∈ {σ(1), . . . ,σ(l)},

limt→∞

PC

[Tt(j) ≥

(1− ε) log t

I(θj , θσ(1))

]= 1.

lim inft→∞

R(t, C)

log(t)≥

∑

j /∈{σ(1),...,σ(l)}

µ(θσ(1))− µ(θj)

I(θj , θσ(1)).

Universality of the bound

• Similar bound can be derived for controlled Markov chains, i.e., for parametrized average reward MDP

• Graves‐Lai 1996. Asympto&cally efficient adap&ve choice of control laws in controlled Markov chains.

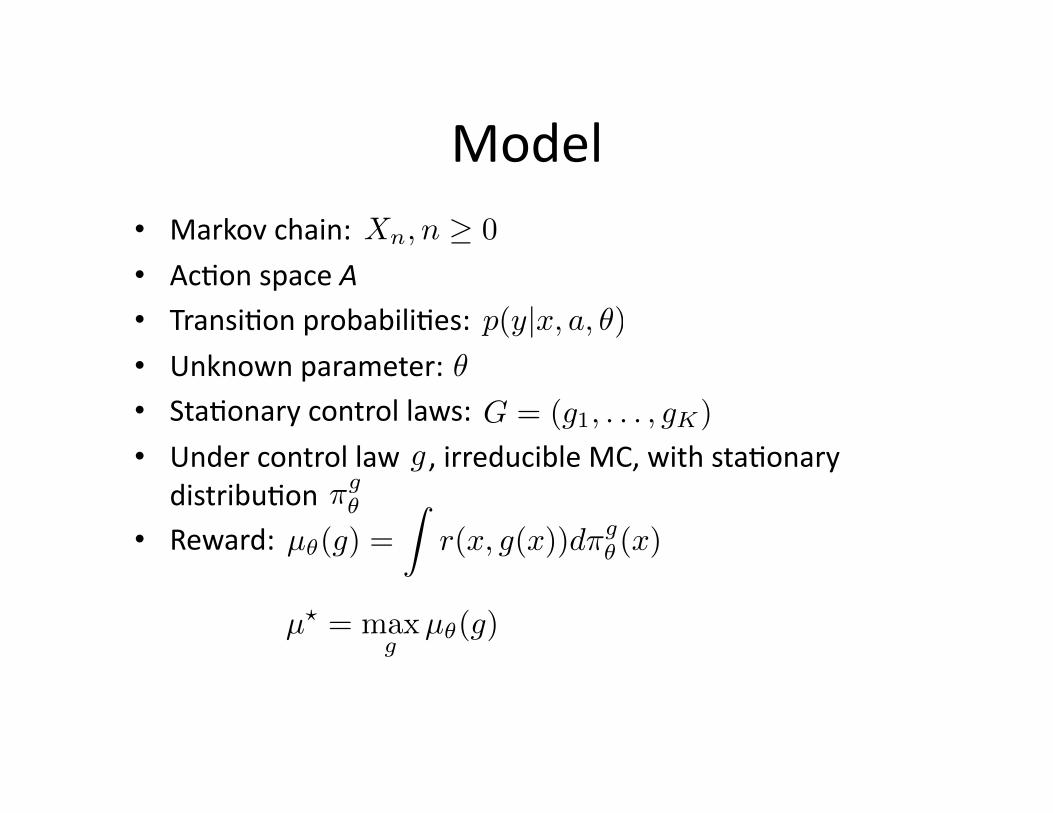

Model • Markov chain:

• Ac&on space A • Transi&on probabili&es: • Unknown parameter: • Sta&onary control laws: • Under control law , irreducible MC, with sta&onary

distribu&on • Reward:

Xn, n ≥ 0

p(y|x, a, θ)θ

G = (g1, . . . , gK)

gπgθ

µθ(g) =

∫r(x, g(x))dπg

θ (x)

µ! = maxg

µθ(g)

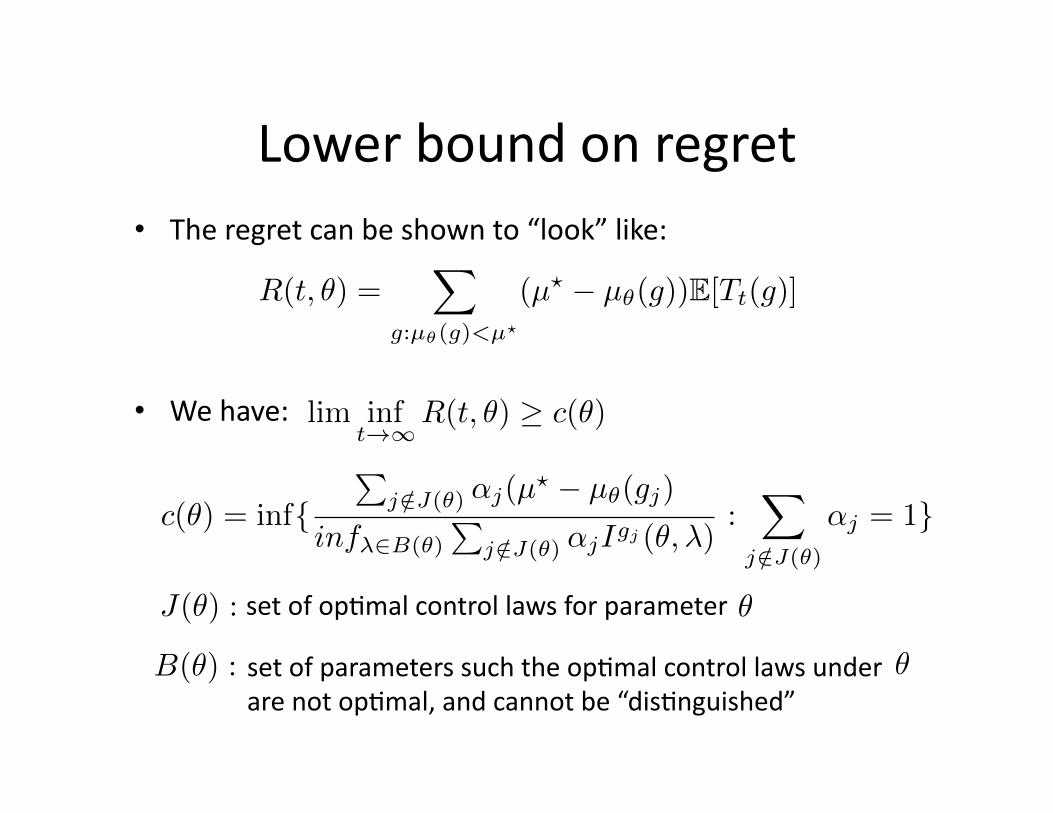

Lower bound on regret • The regret can be shown to “look” like:

• We have:

R(t, θ) =∑

g:µθ(g)<µ"

(µ! − µθ(g))E[Tt(g)]

lim inft→∞

R(t, θ) ≥ c(θ)

c(θ) = inf{∑

j /∈J(θ) αj(µ" − µθ(gj)

infλ∈B(θ)

∑j /∈J(θ) αjIgj (θ,λ)

:∑

j /∈J(θ)

αj = 1}

J(θ) :

B(θ) :

set of op&mal control laws for parameter θ

set of parameters such the op&mal control laws under are not op&mal, and cannot be “dis&nguished”

θ