SEPTEMBER 2014 BUSINESS MODELS - Gather...

60

SEPTEMBER 2014 BUSINESS MODELS 50 EXAMPLES FROM THE FTSE 350

Transcript of SEPTEMBER 2014 BUSINESS MODELS - Gather...

SEPTEMBER 2014

BUSINESS MODELS50 EXAMPLES FROM THE FTSE 350

1. 3i Group2. African Barrick Gold3. Anglo American4. AstraZeneca5. Balfour Beatty6. Bank of Georgia Holdings7. Beazley8. BHP Billiton9. BP10. BTG11. Cable & Wireless Communications12. Carphone Warehouse Group13. Catlin Group14. Coca-Cola HBC AG15. CRH16. Dechra Pharmaceuticals17. Domino Printing Sciences18. easyJet19. Entertainment One Ltd20. Fenner, EPS and AEP Divisions21. Foreign & Colonial Investment Trust22. Genus23. Greencore Group24. Hays25. Home Retail Group

26. IMI27. InterContinental Hotels Group28. ITV29. Ladbrokes30. Lloyds Banking Group31. Meggitt32. Mitchells & Butlers33. National Express Group34. Ocado Group35. Pearson36. Petrofac Ltd37. Premier Farnell38. Rank Group39. Renishaw40. Rolls-Royce Holdings41. RPS Group42. Schroders43. Shire44. Spirax-Sarco Engineering45. St Modwen Properties46. Tate & Lyle47. Tesco48. UBM49. Vedanta Resources50. Our choice: REXAM

CONTENTS

The business model is one of the essential elements of the annual report. It is now fundamental to understanding how any business creates, conserves and captures value.

However, it is the one element that causes the most head-scratching in corporate headquarters up and down the land.

What should go in? What do we leave out? What are we trying to show? Do we really want to tell our competitors how we do it? What can we get away with? Does it make us look simple? Or complicated? Should it be round, square, linear or a quadrilateral? Do we already have one in a presentation that we could use?

All these questions have been asked in the last 12 months. But perhaps the one question we’ve been asked most often is, ‘What is everyone else up to?’

So we decided to pull together 50 business models from the most recent annual reports from the FTSE350. We simply chose every seventh company from an alphabetical list, from 3i to WPP. We have not judged them; the book is more a reference guide to provide inspiration.

But there is another question we get asked a lot. ‘Who does the best business model?’ So, on page 50 we finally come o¥ the fence, name the best one, and give you the reasons why.

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

50 EXAMPLES FROM THE FTSE 350

10

3i Group plc Annual report and accounts 2014

Strategic report

In order to assess properly the profitability of our fund management activities, we consider the fees that can be generated by our entire Fund Management platform, treating proprietary capital invested on the same basis as managed third-party funds. To do this, we calculate an internal fee payable to the Fund Management business for managing our proprietary capital and call this a “synthetic fee”. The standalone profitability of our Fund Management platform is then based on measuring the total fund management income (third-party fees plus synthetic fees) against the operating costs allocated to the platform, excluding restructuring and amortisation costs. To help you track this profitability, we have introduced a new key performance indicator called “Underlying Fund Management profit and margin” (further details on page 46). In FY2014, our fund management platform generated an underlying profit and margin of £33 million and 26% respectively, compared to £17 million and 13% in FY2013.

Over time, we believe that our Fund Management platform is capable of generating sustainable and growing annual profits, which in turn should create additional value for shareholders beyond the growth in value of our proprietary investments. This is an important building block of the 3i Value Build which I talked about in my last review and which is shown on page 13.

Improve capital allocation, focusing on enhanced shareholder distributions and re-investment in our core investment businessesAs part of the strategic review, we fundamentally changed our capital allocation approach so that, over time, we aim to use less of our capital to pay operating costs, funding costs and debt repayment, and instead focus our capital on additional shareholder distributions and investment in our core businesses.

The chart below shows the average allocation of our capital over the three years between FY2010-12. On average, 68% of the total proceeds from realisations and cash income was used to pay operating and funding costs and debt repayment, leaving just 32% for shareholder distributions and investment in our core businesses. In FY2014, we improved this picture with 50% going to shareholder distributions and re-investment. We expect further improvement in FY2015.

Capital allocation

Average over FY10-FY12 FY14

Realisations Operating costs, net carried interest and tax

Debt repayment and interest costs

Shareholder distributions

Funds to invest

Realisations Operating costs, net carried interest and tax

Debt repayment and interest costs

Shareholder distributions

Funds to invest

Fees and portfolio income

Fees and portfolio income

27%

41%

29%

19%

31%

36%

14%

3%

50%

32%

Chief Executive’s review

11

3i Group plcAnnual report and accounts 2014

Strategic report

Business model3i’s business is a mix of proprietary capital investing and managing third-party capital. This “hybrid” asset manager business model enables us to combine capital returns from our proprietary balance sheet and recurring management fee income from our fund management activities. We believe that this represents a di�erentiated and attractive value proposition for our shareholders.

Investing from our own balance sheet is part of our heritage. Currently, proprietary AUM amounts to £3.4 billion, accounting for 26% of the Group’s total AUM. 3i is the largest single investor in its own Private Equity and Infrastructure funds. Putting our own capital to work alongside third-party investors is a fundamental part of our business model and strategy, and gives 3i a true competitive advantage. We view our role as both an active owner as well as manager of third-party funds. This further reinforces the alignment between the interests of our shareholders, our co-investors and our fund investors.

So, in addition to generating capital returns from proprietary capital investing (our Proprietary Capital activities), we also consider the profitability of our Fund Management platform. Both parts need to generate value for the Group. Our overall objectives are to maximise investment returns from our Proprietary Capital activities and grow our Fund Management activities profitably.

We are already managing the Group with this much clearer delineation between Proprietary Capital and Fund Management. Going forward, you will be able to track our progress through new disclosures and a combination of KPIs measuring our performance as an investor of Proprietary Capital and separately as a Fund Management business, in addition to overall Group performance. These KPIs are shown on pages 16 and 17. The performance of these activities is discussed in the Financial Review, starting on page 40 and further disclosure on the breakdown between Proprietary Capital and Fund Management is shown in Note 1 to the Audited accounts on page 114.

OutlookWe have continued to be successful in implementing our strategic plan against a backdrop of ongoing challenges in the macroeconomic environment. Further regulation across the financial services industry is also presenting additional challenges for our business through further costs and increased complexity.

Despite this, we see the power of the 3i business model coming back well. Our network of local teams across our key geographies and our proprietary capital are two key competitive advantages. For example, in our mid-market Private Equity business, we have had teams on the ground across Europe for over 30 years and our franchise in those markets is very strong. This enables us to access attractive investment opportunities and using our own capital a�ords us flexibility in our approach and timescale that few of our competitors have.

The current environment is a tricky one for new investments. There is an excess of capital looking for investment opportunities and this has driven up sellers’ price expectations. We have benefited from this in our realisation programme, however as we review new investment we will need to continue to be patient and disciplined. Our proposition can deliver healthy alpha-generating returns if we invest, manage and exit well. Careful investment in mid-market Private Equity using 3i’s competitive advantages will generate significant value for the Group, its shareholders and third-party investors as well as take 3i back to sector-leading performance.

Everyone at 3i is committed and working hard to continue to deliver against our strategic plan. I would like to thank the entire 3i team for their e�orts this year. They are key to our success. We are all looking forward to making further good progress in FY2015.

Simon Borrows Chief Executive

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

1. 3i Group

A single focus: To be a leading African gold producer

CHIEF EXECUTIVE OFFICER’S REPORT

STRATEGY AND BUSINESS MODEL

Single country risk All of our production is located in Tanzania, therefore major in-country developments could have a signi�cant effect on our operations and business.

Costs and capital expenditureIncreased cost pressures, particularly as regards labour, capital equipment and energy costs may affect our ability to manage operating costs and capital expenditures.

Political, legal and regulatory developments Our ability to conduct business is dependent on the consistent interpretation and application of laws and regulations, particularly in Tanzania.

Utilities supplyPower stoppages and disruptions to electrical supply and other utilities impact our ability to operate continuously and can also result in increased costs, particularly power supply costs.

Community relations Failure to engage or manage relations with local communities and stakeholders affects our social licence to operate and can have a direct impact on operations.

Land acquisitionsProgression of mining activities at some of our operations is dependent upon our ability to complete land acquisitions to support life of mine plans timely and successfully.

Loss of critical processesFailures or unavailability of operational infrastructure, such as equipment failure or de�ciencies in supply chain availability, could adversely affect production output or impact exploration and development activities.

Further information on our risk management and mitigation strategies is provided in detail in the Risk management review.

Reserves and resources estimatesOur reserves and resources estimates are based on a range of assumptions and factors; therefore no assurances can be given that anticipated tonnages or grades will be achieved.

Commodity pricesOur �nancial performance is highly dependent on the price of gold and, to a lesser extent, the price of copper and silver. Fluctuations in the pricing of these commodities, particularly rapid price �uctuations, may have a corresponding impact on our �nancial position.

Taxation reviewsOur �nancial position could be adversely affected if Tanzanian tax regimes were revised beyond the �scal stability agreements contained in our Mineral Development Agreements and/or upon unsuccessful discussions with taxation regulators on outstanding tax assessments.

Environmental hazards and rehabilitationOur operations use processes and methods which require the use of chemicals and other hazardous substances and, as such, we may be liable for losses and costs associated with environmental hazards, should they occur.

Employer, contractor and industrial relationsOur business depends on attracting and retaining skilled employees. A loss in skilled employees and/or a breakdown in employee relations could result in a decrease in production levels, increased costs and/or disruptions to operations.

Security, trespass and vandalismWe face risks when dealing with fraud, corruption and wider security matters, e.g. trespass, theft, vandalism or unauthorised small-scale mining near or on our operations, all of which could affect our mine sites and �nancial condition.

Organisational restructuringOur organisational restructuring (including the transfer of certain support functions from South Africa to Tanzania) and related transitional periods may negatively impact the delivery of key operational support services and could also result in deteriorations in certain �nancial and operational controls.

We are focused on maintaining and strengthening our position as a leading African gold producer in order to develop our business for the long term. For this reason we have adopted a consistent strategy of optimise, expand and grow, and have structured our business model on the premise of responsible mining and other foundations that we believe re�ect sound business practices in order to achieve our immediate goal of attaining and maintaining operational excellence.

We believe that satisfying this immediate goal is fundamental to the achievement of our primary objective: generating free cash �ow to provide sustainable returns for all of our stakeholders in the form of shareholder returns and ongoing economic contributions and investment in our host countries.

Managing principal business risks Our principal business risks fall within four broad categories: strategic risks, �nancial risks, external risks and operational risks, as follows:

6 www.africanbarrickgold.com

STRATEG

IC R

EPO

RT

Sustainable stakeholder returns

Operational excellence

Application of strong cost and capital discipline

Commitment to responsible mining

Continued development of our quality asset base

Maintenance of e�ective governance and risk

management practicesin practice this means: in practice this means: in practice this means: in practice this means:

• enhancing supply chain and inventory management

• maintaining appropriate operational cost levels

• adopting stringent capital allocation and expenditure practices

• using robust �nancial management procedures

• developing community and government relationships

• protecting the environment

• safeguarding health and safety in the workplace

• creating development and training opportunities for our employees

• respecting human rights

• enhancing life of mine planning methods

• driving mining and processing ef�ciencies through improved practices

• optimising mining, development and processing rates

• investing in the right exploration opportunities

• fostering strong, effective and experienced leadership

• providing for diversity

• developing sound governance structures and practices

• progressing and maintaining internal controls and risk mitigation strategies

Further information on capital discipline is provided in the following pages of the Strategic report.

Further information on our commitment to responsible mining is provided in the Corporate responsibility section of this report.

Further information on the development of our asset base is provided in the following pages of the Strategic report.

Further information on e�ective governance and risk management is provided in the Governance report and the Risk management review.

Our foundations drive

Which creates

Single country risk All of our production is located in Tanzania, therefore major in-country developments could have a signi�cant effect on our operations and business.

Costs and capital expenditureIncreased cost pressures, particularly as regards labour, capital equipment and energy costs may affect our ability to manage operating costs and capital expenditures.

Political, legal and regulatory developments Our ability to conduct business is dependent on the consistent interpretation and application of laws and regulations, particularly in Tanzania.

Utilities supplyPower stoppages and disruptions to electrical supply and other utilities impact our ability to operate continuously and can also result in increased costs, particularly power supply costs.

Community relations Failure to engage or manage relations with local communities and stakeholders affects our social licence to operate and can have a direct impact on operations.

Land acquisitionsProgression of mining activities at some of our operations is dependent upon our ability to complete land acquisitions to support life of mine plans timely and successfully.

Loss of critical processesFailures or unavailability of operational infrastructure, such as equipment failure or de�ciencies in supply chain availability, could adversely affect production output or impact exploration and development activities.

Further information on our risk management and mitigation strategies is provided in detail in the Risk management review.

Reserves and resources estimatesOur reserves and resources estimates are based on a range of assumptions and factors; therefore no assurances can be given that anticipated tonnages or grades will be achieved.

Commodity pricesOur �nancial performance is highly dependent on the price of gold and, to a lesser extent, the price of copper and silver. Fluctuations in the pricing of these commodities, particularly rapid price �uctuations, may have a corresponding impact on our �nancial position.

Taxation reviewsOur �nancial position could be adversely affected if Tanzanian tax regimes were revised beyond the �scal stability agreements contained in our Mineral Development Agreements and/or upon unsuccessful discussions with taxation regulators on outstanding tax assessments.

Environmental hazards and rehabilitationOur operations use processes and methods which require the use of chemicals and other hazardous substances and, as such, we may be liable for losses and costs associated with environmental hazards, should they occur.

Employer, contractor and industrial relationsOur business depends on attracting and retaining skilled employees. A loss in skilled employees and/or a breakdown in employee relations could result in a decrease in production levels, increased costs and/or disruptions to operations.

Security, trespass and vandalismWe face risks when dealing with fraud, corruption and wider security matters, e.g. trespass, theft, vandalism or unauthorised small-scale mining near or on our operations, all of which could affect our mine sites and �nancial condition.

Organisational restructuringOur organisational restructuring (including the transfer of certain support functions from South Africa to Tanzania) and related transitional periods may negatively impact the delivery of key operational support services and could also result in deteriorations in certain �nancial and operational controls.

Annual Report and Accounts 2013 7

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

2. African Barrick Gold

DESIGNED TO DELIVER NOW

CAPITAL ALLOCATION

We have set ourselves a realistic financial target of delivering at least a 15% attributable ROCE by 2016. Achieving this target will require a renewed focus on capital discipline, our capital deployment to be directed towards high value, low risk projects, and ensuring we manage the balance between growth and shareholder returns.

For more informationSee page 20

BUSINESS EXECUTION

We have a high quality asset base with the potential to deliver better margins and returns. The asset review process has identified operational improvement opportunities and we are working towards executing against our plans while remaining committed to the highest standards of safe and sustainable mining.

For more informationSee page 34

STAKEHOLDER ENGAGEMENT

We understand that we must work together with our stakeholders to partner with them to reach their potential. Our ability to build effective and mutually beneficial partnerships with host communities and governments is of particular importance to us and is a prerequisite for investment.

For more informationSee page 26

ORGANISATION STRUCTURE

We believe that having the right people in the right roles doing the right work is critical to achieving our ambition, and so, we are redesigning our organisation to enable our people and our business to be successful.

For more informationSee page 26

ADDRESSING OUR IMMEDIATE PRIORITIESAs part of our Driving Value change programme we have completed the review of our asset portfolio and now understand what has to be done to achieve both our short term targets and long term ambitions. We have focused on four strategic priority areas to help us deliver now.

1. EXPECTATION SETTING AND OPERATIONAL PLANNING

The first step in understanding how to optimise each of our assets is to determine the gap between the current capabilities of the assets versus budgeted expectations.

2. PERFORMANCE ANALYSIS

We then analyse data and key performance indicators (KPIs) generated by the asset to confirm average performance levels, assuming no changes to the current process.

3. CONTINUOUS IMPROVEMENT

Incremental changes are made to the operation of the assets to deliver a positive and sustainable shift in performance with minimal capital outlay.

HOW WE CREATE VALUE Anglo American finds, develops, mines, processes and markets a range of commodities that meet our customers’ changing needs. We have a diverse portfolio of high quality assets, with many having significant scalability potential. We are committed to running our business all the way from discovery to market in a safe and responsible way, to deliver long term sustainable value to all our stakeholders.

OUR OPERATIONAL MODEL We are developing a new approach to drive and support change across our value chain. Starting with clear and realistic expectations, we will plan appropriately and then put those plans into action, rigorously measuring and analysing successes and failures to learn from both.

ORGANISATIONAL MODEL We want to create a more effective and efficient organisation, where we only carry out the necessary work – the right work – to achieve our strategy. We aim to reduce duplication, eliminate tasks that do not add value, and ensure that the work required is carried out by people with the right capabilities, resources and tools. We are clear who makes decisions across the Group and, therefore, who is accountable for the outcomes of these decisions.

16 Anglo American plc Annual Report 2013

STRATEGIC REPORT OUR BUSINESS MODEL

OUR RESERVES AND RESOURCES

The quality and extent of its mineral resource base is the lifeblood of any mining company, providing it with a range of development and other value creating options for the future. At Anglo American, we have an extensive ore reserve and mineral resource base across all of the commodities in our portfolio and across our wide geographic footprint, providing us with a suite of options for delivering value through different commodities’ economic cycles. The efficient extraction of metals and minerals from these orebodies underpins our ongoing profitability.

COMMUNITIES AND GOVERNMENTS

Governments, as custodians, own the resources we develop and set the tax and regulatory frameworks within which we operate. Our host communities are major providers of employees and suppliers, and without their support we cannot succeed.

Both governments and communities expect us to run safe and environmentally responsible operations, and to contribute to the long term development of our host communities and countries.

OUR EMPLOYEES

Our employees are the business. We can build our mines and our operations, but if we do not have an engaged and committed workforce we will never achieve our true potential. We must participate in every individual’s personal development, to support them to succeed in return for their commitment to give us their best. We believe we can be the Employer of Choice by rewarding our people at market-competitive rates while providing them the opportunity to realise their personal potential.

OUR KEY RESOURCES AND RELATIONSHIPS

ORGANISATIONAL STRUCTURE

We believe that the role of our business units is to carry out core ‘operational work’ and that the role of the Group corporate functions is to provide support to enable this to happen. A basic principle of our new organisation model is that all work should be done at the operations unless there is a clear reason for it to be done elsewhere.

OPERATIONAL WORK

Operational work is the core value-generating work of our business. For Anglo American, this includes finding, mining, processing, and moving and marketing our metals and minerals. We also believe that building relationships with our stakeholders is core to operating effectively. The work of Commercial is considered ‘core operational’ because it is a fundamental part of our value chain and is critical to our ability to deliver value to our shareholders and stakeholders.

FUNCTIONAL SUPPORT

Our mining operations and commercial business cannot achieve the Group’s strategic objectives alone; they require value-adding specialist support and services by the Group functions at the corporate centre. These provide expert advice to our operational managers that helps improve business performance across the Group.

FINDOur exploration teams discover mineral deposits in a safe and responsible way to replenish the mineral resources that underpin our future success.

SECURE Gaining and maintaining our social and legal licence to operate, through open and honest engagement with our stakeholders, is critical to the sustainability of our business.

MINEWe apply more than 95 years of opencast and deep-level mining experience, along with unique in-house technological expertise, to extract mineral resources in the safest, most efficient way.

PROCESSWe generate extra value by processing and refining many of our commodities.

MOVEWhether providing innovative haulage solutions within a mine, or co-ordinating global cargo deliveries, we offer efficient and effective transport of our commodities.

MARKETWe collaborate with our customers around the world to tailor products to their specific needs.

MARKETMOVEPROCESSMINESECUREFIND

17

Strategic report

Anglo American plc Annual Report 2013

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

3. Anglo American

How we add valueIn this section, we describe our business model and the purpose, ambition and values that drive what we do and how we do it.We outline how we add value, our strategic priorities, how we measure our success and the risks we face. We also describe how we are governed and paid, and how this supports our strategy.

Our business model

Cash �ow RevenueRe-

investment

Return to shareholders

Therapy areas

Resources

Strategic priorities

Customers

Life-cycle of a medicine

Promoting and rewarding innovation

Research and Development

Creation and acquisition of intellectual property through innovative R&D

Application for patents to protect the intellectual property assets developed in a potential medicine

Clinical development programmes to determine the safety and efficacy of the potential medicine and generate further intellectual property rights and data for regulatory submissions

Unmet medical

need

Improved health

10 AstraZeneca Annual Report and Form 20-F Information 2013

Strategic Report | Strategy | Business model

Sales and Marketing

Period of intellectual property protection for an innovative medicine which allows a return to be made on the investment undertaken

Expiry of intellectual property rights and commoditisation of knowledge which typically sees generic versions of a medicine entering a market

Unmet medical need We are living in a time when underlying demographic trends are favourable to long-term pharmaceutical industry growth, and innovative scientific research continues to deliver new ways of satisfying unmet medical need. However, as the Our marketplace section from page 13 demonstrates, the economic, social and political environment in which we operate presents major challenges, as well as opportunities. Our strategic priorities section from page 16 defines our response to this environment.

Resources In everything we do, we seek to optimise the value of all our resources. These include both our employees and the relationships we have with our partners, collaborators and suppliers. Our assets also include our intellectual property, our infrastructure and other physical assets. See the Resources Review from page 66 for more information.

Life-cycle of a medicine We are one of very few pure-play biopharmaceutical companies (that is, not involved in consumer or animal healthcare, diagnostics or medical devices) to span the entire value chain of a medicine from research, early- and late-stage development to manufacturing and distribution, and the global commercialisation of primary care, specialty care-led and specialty care

medicines that transform lives. Our life-cycle management process (including line extensions) is designed to ensure a medicine’s continued safe use and to explore its potential for treating other diseases, or for extending its use into additional patient groups. See the Business Review from page 34 for more on our activities across a medicine’s life-cycle. The Therapy Area Review from page 48 describes our activities across our chosen therapy areas.

Return to shareholdersThe revenue we earn from the sale of our medicines generates the cash flow that helps us fund business investment, our progressive dividend policy, and meet our debt service obligations. We aim to strike a balance between the interests of the business, our financial creditors and our shareholders. See the Financial Review from page 74 for more information.

Improved healthWe believe that continuous innovation in medical progress is vital to achieving sustainable healthcare. It adds value by:

> leading to better health outcomes and transforming patients’ lives

> enabling healthcare systems to save costs and be more efficient

> delivering value beyond the medicines themselves by, for example, improving access to healthcare and healthcare infrastructure

> contributing to the development of the communities in which we operate, via local employment, and partnering.

Promoting and rewarding innovationThe creation and protection of our underlying intellectual property assets, as outlined below, are essential elements of our business model. Developing a new medicine is risky, costly and time consuming. It requires significant investment over 10 or more years before product launch, with no guarantee of success. For this to be viable, the new medicine must be safeguarded from being copied, with a reasonable amount of certainty and for an acceptable period of time, so we can generate the returns to reinvest in the business and provide an appropriate return to shareholders.

The loss of key product patents has affected sales significantly in recent years and will continue to do so. A key goal for our planning process is to ensure we sustain the cycle of successful innovation and so continue to refresh our portfolio of patented products that transform lives and generate shareholder value.

Additional Inform

ationFinancial S

tatements

Corporate G

overnanceS

trategic Report

11AstraZeneca Annual Report and Form 20-F Information 2013

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

4. AstraZeneca

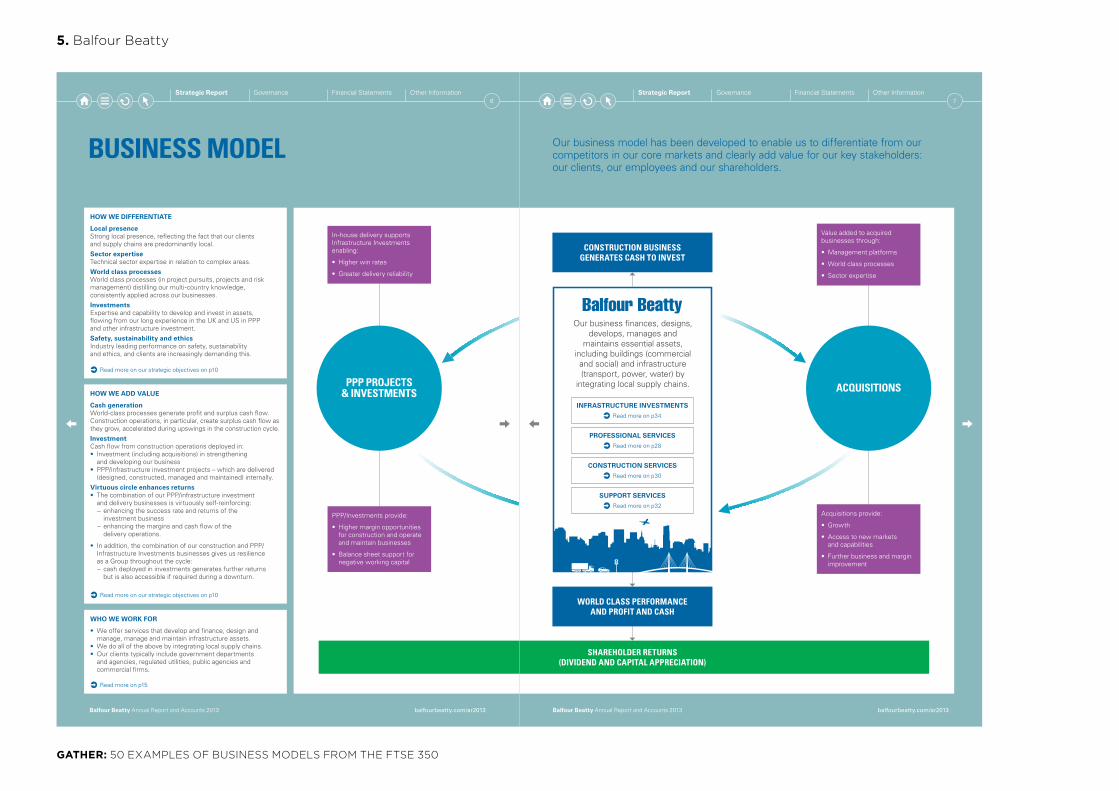

BUSINESS MODEL

HOW WE DIFFERENTIATE

Local presenceStrong local presence, reflecting the fact that our clients and supply chains are predominantly local.

Sector expertiseTechnical sector expertise in relation to complex areas.

World class processesWorld class processes (in project pursuits, projects and risk management) distilling our multi-country knowledge, consistently applied across our businesses.

InvestmentsExpertise and capability to develop and invest in assets, flowing from our long experience in the UK and US in PPP and other infrastructure investment.

Safety, sustainability and ethicsIndustry leading performance on safety, sustainability and ethics, and clients are increasingly demanding this.

HOW WE ADD VALUE

Cash generationWorld-class processes generate profit and surplus cash flow. Construction operations, in particular, create surplus cash flow as they grow, accelerated during upswings in the construction cycle.

InvestmentCash flow from construction operations deployed in:• Investment (including acquisitions) in strengthening

and developing our business• PPP/infrastructure investment projects – which are delivered

(designed, constructed, managed and maintained) internally.

Virtuous circle enhances returns• The combination of our PPP/infrastructure investment

and delivery businesses is virtuously self-reinforcing: − enhancing the success rate and returns of the investment business

− enhancing the margins and cash flow of the delivery operations.

• In addition, the combination of our construction and PPP/ Infrastructure Investments businesses gives us resilience as a Group throughout the cycle:

− cash deployed in investments generates further returns but is also accessible if required during a downturn.

Read more on our strategic objectives on p10

Read more on our strategic objectives on p10

WHO WE WORK FOR

• We offer services that develop and finance, design and manage, manage and maintain infrastructure assets.

• We do all of the above by integrating local supply chains.• Our clients typically include government departments

and agencies, regulated utilities, public agencies and commercial firms.

Read more on p15

In-house delivery supports Infrastructure Investments enabling:

• Higher win rates

• Greater delivery reliability

PPP/Investments provide:

• Higher margin opportunities for construction and operate and maintain businesses

• Balance sheet support for negative working capital

PPP PROJECTS & INVESTMENTS

balfourbeatty.com/ar2013Balfour Beatty Annual Report and Accounts 2013

6Strategic Report Governance Financial Statements Other Information

WORLD CLASS PERFORMANCE AND PROFIT AND CASH

Our business model has been developed to enable us to differentiate from our competitors in our core markets and clearly add value for our key stakeholders: our clients, our employees and our shareholders.

Our business finances, designs, develops, manages and

maintains essential assets, including buildings (commercial and social) and infrastructure (transport, power, water) by

integrating local supply chains.

Value added to acquired businesses through:

• Management platforms

• World class processes

• Sector expertise

Acquisitions provide:

• Growth

• Access to new markets and capabilities

• Further business and margin improvement

ACQUISITIONS

CONSTRUCTION BUSINESS GENERATES CASH TO INVEST

PROFESSIONAL SERVICES

Read more on p28

CONSTRUCTION SERVICES

Read more on p30

SUPPORT SERVICES

Read more on p32

INFRASTRUCTURE INVESTMENTS

Read more on p34

SHAREHOLDER RETURNS (DIVIDEND AND CAPITAL APPRECIATION)

balfourbeatty.com/ar2013Balfour Beatty Annual Report and Accounts 2013

7Other InformationFinancial StatementsGovernanceStrategic Report

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

5. Balfour Beatty

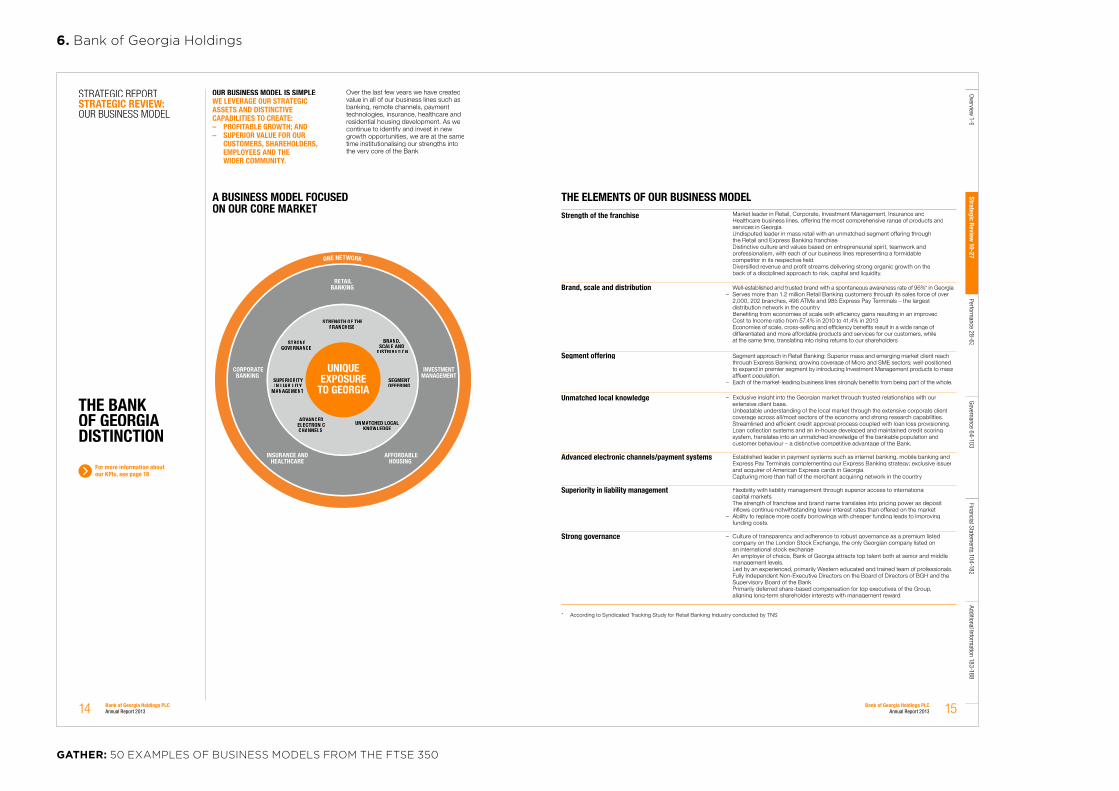

ONE NETWORK

RETAILBANKING

CORPORATEBANKING

INSURANCE ANDHEALTHCARE

AFFORDABLEHOUSING

INVESTMENTMANAGEMENT

STRENGTH OF THEFRANCHISE

BRAND, SCALE AND

DISTRIBUTION

ADVAVAV NCED ELECTRONIC CHANNELS

UNMATATA CHED LOCAL KNOWLEDGE

SEGMENTOFFERING

SUPERIORITYIN LIABILITY

MANAGEMENT

UNIQUEEXPOSURE

TO GEORGIA

STRONGGOVERNANCE

OUR BUSINESS MODEL IS SIMPLE:WE LEVERAGE OUR STRATEGIC ASSETS AND DISTINCTIVE CAPABILITIES TO CREATE:– PROFITABLE GROWTH; AND– SUPERIOR VALUE FOR OUR

CUSTOMERS, SHAREHOLDERS, EMPLOYEES AND THE WIDER COMMUNITY.

Over the last few years we have created value in all of our business lines such as banking, remote channels, payment technologies, insurance, healthcare and residential housing development. As we continue to identify and invest in new growth opportunities, we are at the same time institutionalising our strengths into the very core of the Bank.

THE BANK OF GEORGIA DISTINCTION

For more information about our KPIs, see page 18

STRATEGIC REPORTSTRATEGIC REVIEW: OUR BUSINESS MODEL

THE ELEMENTS OF OUR BUSINESS MODELStrength of the franchise – Market leader in Retail, Corporate, Investment Management, Insurance and

Healthcare business lines, offering the most comprehensive range of products and services in Georgia.

– Undisputed leader in mass retail with an unmatched segment offering through the Retail and Express Banking franchise.

– Distinctive culture and values based on entrepreneurial spirit, teamwork and professionalism, with each of our business lines representing a formidable competitor in its respective �eld.

– Diversi�ed revenue and pro�t streams delivering strong organic growth on the back of a disciplined approach to risk, capital and liquidity.

Brand, scale and distribution – Well-established and trusted brand with a spontaneous awareness rate of 96%* in Georgia.– Serves more than 1.2 million Retail Banking customers through its sales force of over

2,000, 202 branches, 496 ATMs and 985 Express Pay Terminals – the largest distribution network in the country.

– Bene�ting from economies of scale with ef�ciency gains resulting in an improved Cost to Income ratio from 57.4% in 2010 to 41.4% in 2013.

– Economies of scale, cross-selling and ef�ciency bene�ts result in a wide range of differentiated and more affordable products and services for our customers, while at the same time, translating into rising returns to our shareholders.

Segment offering – Segment approach in Retail Banking: Superior mass and emerging market client reach through Express Banking; growing coverage of Micro and SME sectors; well-positioned to expand in premier segment by introducing Investment Management products to mass af�uent population.

– Each of the market-leading business lines strongly bene�ts from being part of the whole.

Unmatched local knowledge – Exclusive insight into the Georgian market through trusted relationships with our extensive client base.

– Unbeatable understanding of the local market through the extensive corporate client coverage across all/most sectors of the economy and strong research capabilities.

– Streamlined and ef�cient credit approval process coupled with loan loss provisioning. Loan collection systems and an in-house developed and maintained credit scoring system, translates into an unmatched knowledge of the bankable population and customer behaviour – a distinctive competitive advantage of the Bank.

Advanced electronic channels/payment systems – Established leader in payment systems such as internet banking, mobile banking and Express Pay Terminals complementing our Express Banking strategy; exclusive issuer and acquirer of American Express cards in Georgia.

– Capturing more than half of the merchant acquiring network in the country.

Superiority in liability management – Flexibility with liability management through superior access to international capital markets.

– The strength of franchise and brand name translates into pricing power as deposit in�ows continue notwithstanding lower interest rates than offered on the market.

– Ability to replace more costly borrowings with cheaper funding leads to improving funding costs.

Strong governance – Culture of transparency and adherence to robust governance as a premium listed company on the London Stock Exchange, the only Georgian company listed on an international stock exchange.

– An employer of choice, Bank of Georgia attracts top talent both at senior and middle management levels.

– Led by an experienced, primarily Western educated and trained team of professionals. – Fully Independent Non-Executive Directors on the Board of Directors of BGH and the

Supervisory Board of the Bank.– Primarily deferred share-based compensation for top executives of the Group,

aligning long-term shareholder interests with management reward.

* According to Syndicated Tracking Study for Retail Banking Industry conducted by TNS.

A BUSINESS MODEL FOCUSED ON OUR CORE MARKET

Overview

1-9Strategic Review

10-27Perform

ance 28-63Governance 64-103

Financial Statements 104-182

Additional Information 183-188

Bank of Georgia Holdings PLC Annual Report 2013 1514 Bank of Georgia Holdings PLC

Annual Report 2013

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

6. Bank of Georgia Holdings

4 Beazley Annual report 2013

www.beazley.com

Our business model Our strategy

Reconfirmed annually through the business planning process, our business model is as follows:

•Beazley is a specialist insurer. We have a targeted product set, very largely in commercial lines of business, and underwrite each risk on its own merits

•We employ highly skilled, experienced and specialist underwriters and claims managers

•We tend to write capped liabilities•We operate through specific insurance hubs rather

than seeking a local presence in every country in which we do business

•We transact business through brokers and work with selected managing general agencies and managing general underwriters to improve distribution in specialist niches

Our strategy is directed towards the achievement of our vision, which is to become, and be recognised as, the highest performing specialist insurer. To this end, our strategy comprises:

•Prudent capital allocation to achieve a well diversified portfolio that is resistant to shocks in any individual line of business

•The creation of an environment in which talented individuals with entrepreneurial spirit can build successful businesses

•The ability to scale our operations to ensure that client and broker service keeps pace – and wherever possible improves – as the company grows

•Consistent investment in product innovations to provide better products and services to improve our clients’ risk transfer

A business model and strategy that support high performance

4 Beazley Annual report 2013

www.beazley.com 5Beazley Annual report 2013

www.beazley.com

Financial statementsGovernanceStrategic report

Our key performance indicators

KPIs

Financial highlightsEarnings per share (c)

20132012201120102009

52.4

28.9

42.1

13.0

42.4

0102030405060

Basic EPS is at 2.0x total dividend cover for 2013. Average EPS over the last five years is at 4.5x average dividend cover (excluding the special dividends).

Net assets per share (c)

20132012201120102009

18.2

21.7 23.2 25.823.0

248.3

169.8 191.4 185.9217.5

050

100150200250300

Tangible Intangible

0

20

40

60

80

100

Great Place to Work survey (%)

201320112008

81 76 83

11% growth in net assets per share during 2013.

Since 2008, Beazley has run an employmentengagement survey (now every two years)managed by the Great Place to Work® organisation. In 2013, for the third time ina row, a large majority of employees rated Beazley a great place to work.

0

500

1000

1500

2000

Gross premiums written ($m)

20132012201120102009

1,9

70.2

1,75

1.3

1,74

1.6

1,71

2.5

1,89

5.9

Growth of 4% in 2013 and 12% since 2009.

0

5

10

15

20

25

Dividends per share (p)

20132012201120102009

16.12.5 8.48.87.0 7.5 7.9 8.3

Interim and final Special

The second interim dividend in 2013 is in line with our dividend strategy and has grown by 6%. In addition we are paying a special dividend of 16.1p.

0

5

10

15

20

25

Return on equity (%)

20132012201120102009

2124

19

6

19

Cumulative five year return on equity of 89%.

0

20

40

60

80

100

Combined ratio (%)

20132012201120102009

3935 36

3738

8490 8899

91

4555 52

6253

Claims ratio Expense ratio

Our combined ratio has averaged 90% over five years.

For further details go to page 104

Non-financial highlights

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

7. Beazley

Extraction, processing and transportation Marketing and logistics

Across our global operations, the diversification of our portfolio of assets by commodity, geography and market continues to be one of our differentiating features. Our goal is to safely operate all of our assets at capacity through mining, extracting, processing and transporting commodities.

We continue to set production records at a number of assets. Through the development and use of standard operating practices and technology, we are driving efficiencies through improved capital intensity, labour productivity and increased utilisation of plant and machinery.

Our extraction and processing activities apply our ongoing sustainability obligations, including rehabilitation at the end of the asset life.

In order to develop customer and market-focused solutions, we have divided our marketing organisation between mineral marketing, centralised in Singapore and petroleum product marketing, based in Houston, United States. Marketing manages the Group’s product sales and the purchase of all major raw materials. It achieves market clearing prices for our products and is responsible for managing our credit and price risks.

Marketing also manages the supply chain of our products from assets to markets and the raw materials from suppliers to assets. This includes managing our in-house freight requirements so as to procure high-quality, cost-effective shipping.

• open-pit and underground mining• extracting conventional and

unconventional oil and gas • processing and refining

• selling our products• purchasing major raw materials• managing the supply chain• managing credit and price risk

1.5.3 External factors and trendsGlobal economyEconomic conditions during the second half of FY2013 were affected by lower than expected growth in emerging economies. Weaker trade and soft manufacturing activity pulled growth rates slightly below expectations in China. However, with employment conditions and income growth remaining resilient, the Chinese Government has room to pursue reforms that support its agenda of stable, long-term growth.

Significant cuts in government spending affected growth in the United States, however this was offset by improved private sector demand, leading to modest rates of economic growth overall. Housing and stock market prices have also strengthened household balance sheets over the past year. As a result, we are confident the recovery will continue, although risks remain regarding the unwinding of monetary policy stimulus.

The renewed policy push in Japan is also positive for medium-term growth expectations, if the government can achieve its stated objectives. Europe remained relatively stable during FY2013; however, we do not anticipate a strong or rapid recovery while fundamental structural problems remain.

Overall, we expect more balanced global growth over the long term as China continues to develop its economy and large developed economies, such as the United States, grow despite fiscal challenges. We expect the rebalancing of the Chinese economy to be significant in terms of the nature of domestic demand, as well as the types of goods and services the economy will produce. We expect these changes to take place gradually, particularly in relation to savings behaviour and levels of fixed asset investment. We also see India and South East Asia as significant sources of economic growth in the long term.

Commodity pricesDuring FY2013, commodity markets were impacted by a slower pace of growth in China that was balanced in part by increased stability in European sovereign debt markets and an improved private sector performance in the United States. In the case of most steelmaking raw materials, demand growth rates outside China decreased, and combined with robust supply growth from seaborne sources, resulted in lower raw material prices than the previous year. The metals commodities attracted lower prices than the previous year as a result of supply growing faster than demand. Conversely for energy commodities, geopolitical tensions and United States economic improvements provided price support for crude oil, while the US gas prices increased due to increased seasonal demand in the residential and commercial sector and decreased storage inventories from the previous year.

Exchange ratesWe are exposed to movements in exchange rates in relation to foreign currency sales and purchases as well as in relation to foreign currency denominated monetary assets and liabilities, including debt. We believe that active currency hedging does not provide long-term benefits to our shareholders. Because a majority of our sales are denominated in US dollars, and the US dollar plays an important role in our organisation, we borrow and hold surplus cash predominantly in US dollars to provide a natural hedge. Operating costs and costs of locally sourced equipment are influenced by fluctuations in local currencies, primarily the Australian dollar, Brazilian real, Chilean peso and South African rand. Foreign exchange gains and losses reflected in operating costs owing to fluctuations in the local currencies relative to the US dollar may potentially offset one another. In addition, exchange rate markets often provide a theoretical natural hedge against movements in commodity prices. Volatility increased during the year, with a strengthening of the US dollar in the last quarter of FY2013. Overall, the Australian dollar, Brazilian real and South African rand ended FY2013 weaker against the US dollar, while the Chilean peso strengthened.

1 Key information

2 Information on the Com

pany3 O

perating and financial review

and prospects4 Board of D

irectors and G

roup Managem

ent Comm

ittee5 Corporate G

overnance Statement

6 Remuneration Report

BHP BILLITON ANNUAL REPORT 2013 | 9

1 Key information continued

1.5 Our strategy and business model

1.5.1 Our consistent strategyOur purposeOur purpose is to create long-term shareholder value through the discovery, acquisition, development and marketing of natural resources.

Our strategyOur strategy is to own and operate large, long-life, low-cost, expandable, upstream assets diversified by commodity, geography and market.

We sell into globally integrated markets and aim to produce at full capacity throughout the economic cycle. Our leading position in the resources industry is due to our unique, proven and consistent strategy. In line with our strategy, we pursue growth opportunities consistent with our core skills of:• evaluating, developing and extracting our resources

in our Businesses;• distributing and selling our products, and managing financial

risk associated with the revenue line through Marketing;• through our Group Functions, defining and governing world-class

functional standards, which are implemented Group-wide.

This strategy means more predictable company performance over time which, in turn, underpins the creation of long-term sustainable value for our shareholders, customers, employees and the communities in which we operate. We aim to deliver long-term sustainable value rather than being focused on short-term returns.

Our valuesIn pursuing our strategy through all stages of the economic and commodity cycle, we are guided by Our Charter values of Sustainability; Integrity; Respect; Performance; Simplicity; and Accountability.

Our overriding commitment is ensuring the safety of our people, and respecting our environment and the communities in which we work. This commitment informs everything we do and influences every aspect of our work.

Operational capability is fundamental to our strategy and is reflected in Our Charter. In particular, our values of Performance – achieving superior business results by stretching our capabilities, and Simplicity – focusing our efforts on the things that matter most.

Our success factorsWe are successful when our people start each day with a sense of purpose and end the day with a sense of accomplishment; our communities, customers and suppliers value their relationships with us; our asset portfolio is world-class and sustainably developed; our operational discipline and financial strength enables our future growth; and our shareholders receive a superior return on their investment.

1.5.2 Our business model

Exploration and evaluation Development

Over the past five years, brownfield exploration has increased our resource base around our portfolio of existing assets in large resource basins, which now provides us with significant growth opportunities. This has allowed us to reduce brownfield exploration expenditure and rationalise our greenfield exploration program to focus on copper in Chile and Peru and conventional oil and gas predominantly in the Gulf of Mexico and Western Australia.

We evaluate the results of our brownfield and greenfield exploration to identify future growth projects consistent with our strategy to own and operate large, long-life, low-cost, expandable, upstream assets. We also continually evaluate our portfolio and consider acquisition and divestment opportunities.

The evaluation and development of large-scale resource projects generates significant value for BHP Billiton. We have a number of high-quality growth projects currently under development. We also have a large number of growth opportunities in our project pipeline in varying stages of evaluation. In our development process, these projects progress through feasibility to execution only after external approvals and rigorous internal review.

Potential expansion projects must compete for capital in BHP Billiton and are only approved if they meet our strict criteria for investment.

• discovery through brownfield and greenfield exploring

• acquiring and divesting• evaluating our portfolio

• evaluating and developing projects

8 | BHP BILLITON ANNUAL REPORT 2013

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

8. BHP Billiton

We aim to create shareholder value across the hydrocarbon value chain.

Our business model

Our businessesFor more information on our upstream, downstream and alternative energy businesses, see pages 25, 31 and 37 respectively.

A rising global population and increasing levels of prosperity are set to create growing demand for energy for years to come. We can help to meet that demand by producing oil and gas safely and reliably.

We believe that the best way to achieve sustainable success as a group is to act in the long-term interests of our shareholders, our partners and society. We aim to create value for our investors and benefits for the communities and societies in which we operate, with the responsible supply of energy playing a vital role in economic development.

Every stage of the hydrocarbon value chain offers opportunities for us to create value – both through the successful execution of activities that are core to our industry, and through the application of our own distinctive strengths and capabilities in performing those activities. In renewable energy our focus is on integrating biofuels into the hydrocarbon value chain, and on wind operations in the US.

Our approach spans everything from exploration to marketing. Integration across the group allows us to share functional excellence more efficiently across areas such as safety and operational risk, environmental and social practices, procurement, technology and treasury management.

A relentless focus on safety remains the top priority for everyone at BP. Rigorous management of risk helps to protect the people at the front line, the places in which we operate and the value we create. We understand that operating in politically complex regions and technically demanding geographies requires particular sensitivity to local environments.

Toledo refinery in Ohio has been in constant operation since 1919. The facility has the capacity to process up to 160,000 barrels of crude per day.

The redevelopment project at Valhall was one of BP’s most complex field expansion developments and gives the field a further 40-year design life.

Our business model

Finding oil and gas

First, we acquire the rights to explore for oil and gas. Through our exploration activities we are able to renew our portfolio, discover new resources and replenish our development options.

Developing and extracting

When we find hydrocarbon resources, we create value by seeking to progress them into proved reserves or by divesting if they do not fit with our strategy. If we believe developing and producing the reserves will be advantageous for BP, we produce the oil and gas, then sell it to the market or distribute it to our downstream facilities.

Transporting and trading

We move oil and gas through pipelines and by ship, truck and train. Using our trading and supply skills and knowledge, we buy and sell at each stage in the value chain. Our presence across major trading hubs gives us a good understanding of regional and international markets and allows us to create value through entrepreneurial trading.

Manufacturing and marketing

Using our technology and expertise, we manufacture fuels and products, creating value by seeking to operate a high-quality portfolio of well-located assets safely, reliably and efficiently. We market our products to consumers and other end-users and add value through the strength of our brands.

Our illustrated business model see page 2.

BP Annual Report and Form 20-F 201312

Strategic report

Financial discipline

$

Time(Not to scale)

Free cash flow

Operating cash flow

Net investment

Our goal is to be a focused oil and gas company that delivers value over volume.

Our strategy

We are pursuing our strategy by setting clear priorities, actively managing a quality portfolio and employing our distinctive capabilities. Our financial objective is to create shareholder value by generating sustainable free cash flow (operating cash flow less net investment). This disciplined approach enables us to invest for the future while aiming to increase distributions to our investors.

Clear prioritiesFirst, we aim to run safe, reliable and compliant operations – leading to better operational efficiency and safety performance. We also aim to achieve competitive project execution, which is about delivering projects efficiently so they are on time and on budget. And we aim to make disciplined financial choices, so we can achieve continued growth in operating cash from our underlying businesses and disciplined allocation of capital.

Quality portfolioWe undertake active portfolio management to concentrate on areas where we can play to our strengths. This means we continue to grow our exploration position, reloading our upstream pipeline. We focus on high-value upstream assets in deepwater, giant fields and selected gas value chains. And, with our downstream businesses, we plan to leverage our newly upgraded assets, customer relationships and technology to grow free cash flow.

Our portfolio of projects and operations is focused where we can generate the most value, and not necessarily the most volume, through our production.

Distinctive capabilitiesOur ability to deliver against our priorities and build the right portfolio depends on our distinctive capabilities. We apply advanced technology across the hydrocarbon value chain, from finding resources to developing energy-efficient and high-performance products for customers. We rely on our strong relationships – with governments, partners, civil society and others – to enable our operations in around 80 countries across the globe. And, the proven expertise of our employees comes to the fore in a wide range of disciplines.

Our strategy in actionSee page 14 for more information on how we are going to measure our progress.

1 A relentless focus on safety and managing risk through the systematic application of global standards.

2 We will play to our strengths in exploration, deep water, giant fields and gas value chains.

3 Stronger and more focused with an asset base that is high graded and higher performing.

4 4 4 Simpler and more standardized with fewer assets and operations in fewer countries; more streamlined internal reward and performance management processes.

5 Improved transparency through reporting TNK-BP as a separate segment and breaking out the numbers for the three downstream businesses.

6 Active portfolio management to continue by completing $38 billion of disposals over the four years to the end of 2013, in order to focus on our strengths.

7 We expect to bring new upstream projects onstream with unit operating cash marginsf

around double the 2011 average by 2014.g

8 We are aiming to generate an increase of around 50% in net cash provided by operating activities by 2014 compared with 2011.h

9 We intend to use half our incremental operating cash for reinvestment, half for other purposes.

10 Strong balance sheet with intention to target our level of gearingi in the lower half of the 10-20% range over time.

a See footnote a on page 56.b Equivalent to net cash used in investing activities.c See footnote c on page 56.d See footnote h on page 24.e Excludes acquisitions and asset exchanges.f Unit cash margin is net cash provided by operating activities bythe relevant projects in our Upstream segment, divided by the total number of barrels of oil equivalent produced for the relevant projects.

g Assuming a constant oil price of $100 per barrel.h See footnote b on page 56.i See footnote d on page 56.

10-point plan 2011-2014In 2011 we laid out a 10-point plan designed to stabilize the company and restore trust and value in response to the tragic Deepwater Horizon accident. Our priority was to make BP a safer, more risk-aware business. The plan included a series of milestones by which our progress could be tracked, from 2012 through to 2014. Information on our progress during 2013 can be found in Group performance on page 22.

• Operating cash flow – we aim to continue growing our operating cash flow, with an expected delivery of $30 billion to $31 billion in 2014.d

• Capital expenditure – we expect our annual capital expendituree to remain between $24 billion and $25 billion in 2014 and to be in the range of $24 billion to $26 billion in the years 2015 to 2018.

• Divestments – we intend to divest $10 billion of assets before the end of 2015.

• Free cash flow – delivering sustainable free cash flow underpins our ability to deliver increasing shareholder returns.

This chart illustrates the expected relationship between operating cash flowa, net investmentb

(includes capital expenditure offset by any divestments) and free cash flowc. It is not a projection of future performance.

BP Annual Report and Form 20-F 2013 13

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

9. BP

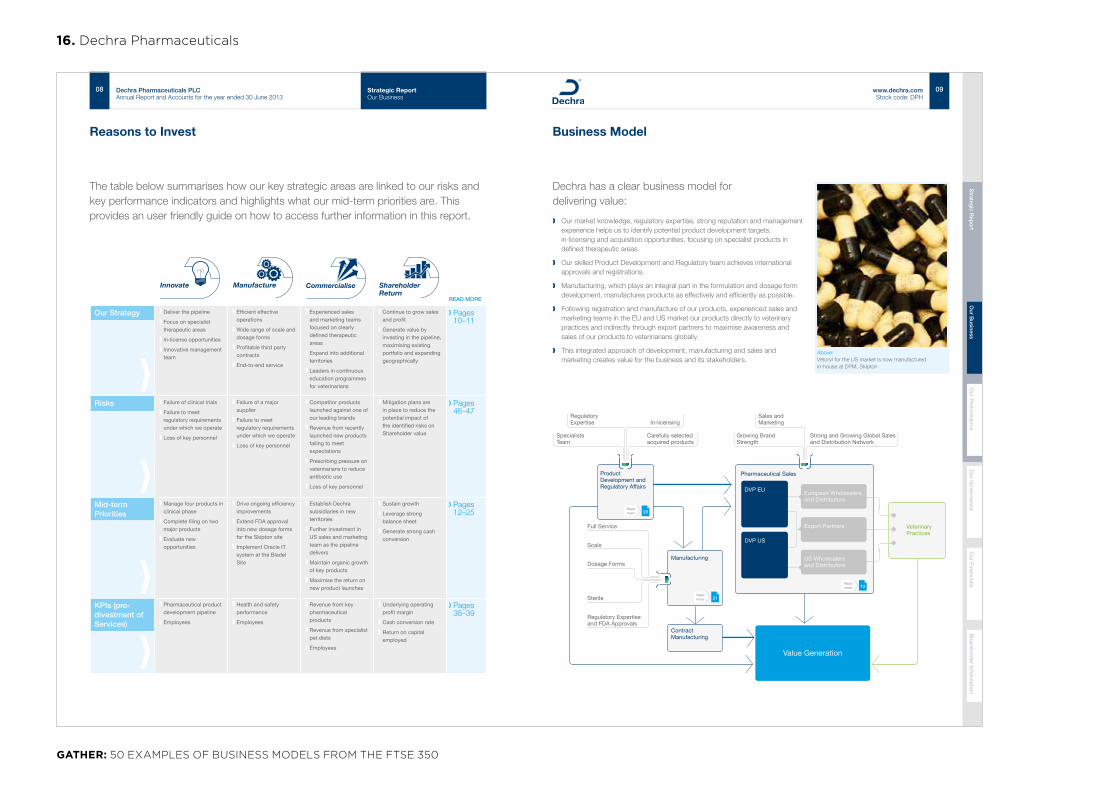

Our business modelOur core purpose is to advance the treatment of people with cancer, vascular disorders and critical care needs. We create value by acquiring, developing and commercialising innovative, differentiated products that meet the needs of our specialist physician customers and their patients.

Development products

Financial management

Learning and growth

In

tern

al p

roce

ss a

nd c

apab

ilitie

s

Core purpose

Cust

omer in

sight Acquire & develop

Comm

ercialise Manufact

ure

18

Our activities

We create value by identifying unmet medical needs, acquiring and developing new products, manufacturing them to high standards and commercialising them through direct sales or through distributors.

Our priorities

We monitor our performance against a number of strategic objectives.

BTG plc Annual Report and Accounts 2014 19

Str

ateg

ic re

port

“ We have multiple organic growth drivers and continue to seek M & A opportunities in both Interventional Medicine and Specialty Pharmaceuticals.”

Louise Makin CEO

Our products are used by specialist groups of physicians with whom we engage in a number of ways. We promote the approved uses of our products and we provide training in the use of our products. To protect patient safety we offer dedicated medical support to physicians regarding the use of our products and we invite proposals for funding or other support to explore the potential use of our products in different patient populations to inform our R&D strategy. We also approach physicians with our own ideas for studies to invite them to participate.

In these interactions we gain valuable knowledge about how physicians use our products in practice, why they might choose not to use our products in certain patient populations, where they require more data to support use within approved indications, and where they see gaps in current treatment options. Our innovation team specifically engages with customers and the wider scientific and medical community to gain insights into treatment practice and trends and to identify unmet medical needs where we may focus our development efforts.

We supplement these insights from customers and others with formal market research, using the information to identify potential new opportunities. These may be addressable with our current products and technology platforms, or they may require us to acquire and/or develop new technologies.

When sourcing technologies, we look for opportunities where we can add value. These include products (or late-stage programmes) that we can sell through our existing sales channels, or through a new sales team that can be supported by our existing infrastructure. We also seek to exploit our strong capabilities in areas of technology convergence, such as drug-device-procedure combination products. We look for opportunities where we can drive further growth by investing in development and commercial activities.

For every technology, whether developed in-house or acquired, we create a lifecycle plan to maximise value. This may include product innovation, clinical trials to expand the indicated uses, and commercial activities to expand the geographical availability.

Most of our development programmes are intended to expand the approved uses of products that are already approved in a primary indication. We believe this is a lower-risk approach as safety and efficacy profiles have already been established in the initial indication.

Having identified additional patient populations that may benefit we liaise with clinicians, regulators and others to determine the appropriate trial designs. Our development personnel manage these activities and oversee the contract research organisations and others involved in conducting many of our studies in order to obtain the requisite regulatory approvals to access new commercial opportunities.

Case study

Clinicians who use our embolisation and drug-eluting beads identified situations where a smaller average bead size than was available could be beneficial in the treatment of certain liver tumours. In response, our Innovation team developed LC BeadM1™ and DC BeadM1™, which have a unique size range and distribution and may allow the doctor to be more selective and penetrate deeper into the tumour, so protecting the healthy liver and reducing stress to cirrhotic livers.

Case study

As Varithena™, a treatment for varicose veins, was progressing towards approval in the US, we sought opportunities to acquire complementary interventional vascular products. This resulted in the acquisition of EKOS Corporation, which makes and sells a leading blood clot treatment. BTG has an acute care sales force that visit emergency rooms, where 50% of blood clots present. In addition, EKOS customers include clinicians who also treat varicose veins. These overlaps provide significant team-selling opportunities across our portfolio.

Acquire and developCustomer insight

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

10. BTG

Returns toshareholders

Community

Community

Our

colleagues

serviceCustomer

acqu

isit

ion

Cus

tom

er

(products/services)

Propositions

Networks

Ope

ratin

g co

sts

Gross m

argin

Cost of goods sold

Revenue

Investment

Cash �owPro�tability

Customer

Financial model�e way our businessmakes returns.

Operating modelHow we manage ourbusiness, servingcustomers.

Chief Executive’s strategic review

2013/14 performance � e past year has been an important one for the Group. We have sold our Islands, Macau and most recently Monaco business units – and have opened an operating hub in Miami. � ese have all been major steps to focus the business on the Caribbean and Latin America.

Although we were not able to obtain regulatory approval to complete the sale of our asset in the Seychelles, we will continue to review our options. As a strong business – cash generative and performing solidly – we will only dispose of this asset if such a transaction will generate attractive shareholder returns.

Collectively our disposals raised US$1,753 million, monies that

were used to reduce our level of indebtedness and provide the headroom for increased investment in our core markets.

Our � nancial results in the 2013/14 year have shown early signs of our turnaround, as we become more geographically-focused. At the beginning of 2013/14 we announced a cost reduction programme targeted to reduce our run-rate operating costs by US$100 million by the end of 2014/15. During the year we have made good progress with operating costs down US$43 million against the prior year, with an exit run rate in 2013/14 of US$77 million of cost savings achieved.

Group revenue continued its long run trend, declining a further 4% to US$1,873 million as growth in mobile and broadband

Chief Executive’s statement continued

A business model that delivers value

Our business model is based on providing customers with communications, information and entertainment services, at a price which delivers value to them, while enabling our business to make a fair return for our shareholders.

08 Cable & Wireless Communications08 Cable & Wireless Communications08 Cable & Wireless Communications

revenue across each of our businesses was more than o� set by declining � xed voice and enterprise, data and other revenue. It is this revenue decline that our new strategy is targeted to reverse.

� e US$52 million growth in mobile data revenue (up 23% in the year) indicates our customers’ increasing demand for data and their desire to access the internet anywhere, anytime, and on any device. However, at the same time both mobile and � xed voice revenue is declining across our industry; growth in broadband and TV is therefore vital for our future. Our B2B and B2G operations also experienced a slower year.

In Panama, we maintained our mobile market share above 50%, and delivered a 4% rise in mobile revenue, led by mobile data.

In the Caribbean, our Jamaica mobile business continued to gain market share as we competed on price and value. However, � xed line and enterprise businesses and adverse currency movements weighed down overall revenue by US$32 million. � e performance of BTC in � e Bahamas, our largest Caribbean market, continued to improve over the year as we launched new mobile and � xed networks, and prepared the business for mobile competition which is expected to arrive later this year. Our performance was weaker in several of the other Caribbean countries – a function of our existing network. With increased investment, and continued cost focus, we are con� dent that we can turn these businesses around; reversing this decline through increased investment is a priority.

Drive to mobile leadership

Fixed-mobile convergence

Reinforce our TV o� ering

Grow B2B and B2G business

Optimise our operating model

Strengthen unique government/stakeholder relationships

Grow top line revenue Maintain cost e� ciency Deliver unparalleled customer service

Increase returns on capital

1 2 43

And two critical enablers:

Delivery of those objectives is built upon four strategic imperatives:

Our business has four strategic objectives:

Our strategy for growth

Our overarching objectiveGrow customer relationships and lifetime value by delivering unparalleled customer experience, where our customers de� ne ‘excellence’.

Annual report 2013/14 09Annual report 2013/14 09Annual report 2013/14 09

GATHER: 50 EXAMPLES OF BUSINESS MODELS FROM THE FTSE 350

11. Cable & Wireless Communications

Carphone Warehouse Group plcAnnual Report 201414

STRATEGIC REPORT

Business model

SIMPLIFYING

For 25 years we have been offering the best choice, advice, price and support for our customers. Our retailing, systems and process expertise provides a strong platform for growth.CPW is committed to prioritising long-term value creation for shareholders.

COMPLEX TECHNOLOGY FOR CUSTOMERS AND BUSINESSES

+ Experts in our field + Unique systems and core capabilities that are difficult to imitate

+ Committed to investing in our people

+ Driven, entrepreneurial management team

+ Optimal supplier terms + Ability to leverage existing cost base and explore new opportunities at home and abroad, in turn driving scale

HOW WE ADD VALUE

+ Partnering with device manufacturers and major networks

+ Creating ongoing mutual economic benefits

RELA

TIO

NSHIPS SCALE

CAPABILITIE

SPEOPLECONNECTED TECHNOLOGY

MAKING MORE LIVES BETTER THROUGH

LONG-TERM APPROACH TO CREATE SHAREHOLDER VALUEOver the past 25 years, we have built the largest independent telecommunications retailer in Europe, attracting consumers and businesses looking for simple, impartial, expert advice about the complexities of mobile technology. Our long-standing purpose is to help customers understand technology.

Our long-term approach to investing creates a sustainable opportunity to continue to add value for a wide range of stakeholders, from our customers, through employees, communities, suppliers, partners, and fundamentally, for our shareholders.

UNIQUE RETAILER WITH PLATFORM FOR GROWTHCPW has an unusual revenue model compared to traditional retailers. A significant proportion of our revenue is derived from MNOs, for delivering new customers and upgrades. The business generally receives a share of future customer revenues, and/or commissions, which are typically used to subsidise the sales values of a range of connected devices. Other revenue streams include value-enhancing products such as accessories, insurance and assurance products.

Adapting to changing market dynamics, CPW has realised the potential to grow new revenue streams by leveraging its unique relationships, core systems and expertise to provide a range of managed services to businesses, including MNOs, other service providers and manufacturers.

CUSTOMER PROPOSITION

+ Committed to delivering value for our customers

+ Independent, impartial, expert advice + Widest choice of devices, connections

and services + Truly multi-channel offering

+ Subsidised and innovative propositions

+ Trusted brand

Carphone Warehouse Group plcAnnual Report 2014 15

STRATEGIC REPORTADAPTING TO AN

MARKETEVOLVINGDEVICE INNOVATIONMobile devices have been transformed in recent years by the development of smartphone technology, evolving rapidly from simple devices used to make and receive calls, to sophisticated hardware with advanced computing functionality. The market has seen continuous innovation, with ever-improving processing speeds and ever-evolving functionality, and increasing choice of screen sizes. Alongside competition between manufacturers of devices, competition has also developed between operating systems, providing broader choice for customers and making CPW’s expert and impartial proposition particularly relevant.

NETWORK EVOLUTIONIn recent years, Western European MNOs have been subject to significant regulatory intervention, particularly on charges to terminate calls from other network operators and on international roaming charges, causing downward pressure on MNO ARPUs. Mobile termination rate cuts have caused MNOs to reduce subsidies on prepay phones, making them increasingly more expensive for consumers, causing a shift towards postpay in some markets.