SEPC Format Company Overview Apr 09 - Shriram … Process industry Mr. G Sugathan Sr. Vice President...

34

Company Presentation April 2009

Transcript of SEPC Format Company Overview Apr 09 - Shriram … Process industry Mr. G Sugathan Sr. Vice President...

Company PresentationApril 2009

2

Contents

• Key Highlights• Company Overview• Business Segments

3

Key Highlights

4

Key Highlights

Diversified client profile across multiple verticals – Industrial Capex, Renewable Energy and Municipal Services with backlog of ~INR 20 bn (as of Dec08) over the next ~24 months

Ability to forge technical partnerships with leading international companies on project specific consortium basis or JVs (Hamon, Danieli, Siemens, Envirotherm, CPT, Angerlehner and others)

50:50 JV with leading European company, Leitner for gearless wind turbines with similar reliability and superior yield at near similar prices – TUV certifications in place

Capacity of 120 MW ~ INR 8 bn in potential revenues at 100% utilization and at current prices

Strong order pipeline for MW-class machines; production already commenced

Holding Company for ~300 MW of clean energy portfolio (wind, biomass and hydel) ~ 100 MW already operational and balance expected on-stream by CY2010 before potential listing

USD 75 mn equity raised, debt at various stages of tie-up

Current order backlog at over 2x TTM revenues (Jan08-Dec08 revenues)

3-year Revenue and PAT CAGR of 120% and 117% respectively

Reputed and diversified client base from the Steel, Power (incl. renewable) & Urban Infrastructure

Strong EPC play and multiple partnerships

Wind Turbine manufacturing to lead future growth

Orient Green Power ownership to unlock value

Strong order book and financial performance

Part of the diversified and reputed Shriram group

Experienced management team with proven capabilities

Demonstrated engineering and project management expertise with high quality workforce consisting majority of technical personnel with strong execution skills

Reputed promoter background and strong management team

5

Company Overview

6

Corporate Structure

4. JV with Hamon Group since Apr 2007 (SEPC holds 50% + 1 share)5. JV with Leitner [Manufacturing - Leitner (51%) SEPC (49%), Marketing – Leitwind (49%) and SEPC (51%)] since Jan 2007 and Feb 2007

Effective 50%

EPC BusinessSegment

Renewable EnergySegment

Process&

Metallurgy

Air Pollution Control

& Cooling Towers

WaterTreatment

&Pipe

Rehabilitation

Biomass Plants

Wind TurbinesManufacturing

RenewableAsset

Ownership

1 2 3 4 5 6

50% + 1 share

Business Divisions

SHRIRAM EPC

7

Brief History

IncorporationExecution of 1st biomass power plant in AP

20082003 2004 2005 2006 20072000

Commencement of Process & Metallurgy business

Foray into Air Pollution Control with Hamon through JV

Execution of JV with Leitner Technologies for manufacture and marketing of megawatt class wind turbines

Commencement of Pipe Rehabilitation business

Acquisition of the cooling towers business of Shriram Tower Tech Limited

First contract for setting up coal gasification plant

Execution of MoU with Leitner for MW class turbines

Investment by ChrysCap

Investment by UTI & BVP

Certification by DEWI-OCC for designing and manufacturing 250 KW wind turbine

Listing of Shriram EPC on NSE & BSE49% JV – Shriram SEPC Composites for GRP pipes55% stake in Blackstone Group Technologies Pvt Ltd

Installation of 1.35MW capacity wind electric generatorOrient Green Power

2009

Commercial operation of MW class WT manufacturing plant

8

Diversified EPC company with multiple technical partnerships

Technology Partners

Process & Metallurgy – Danieli (Italy), Siemens, SMS, Waterbury (Canada)

Coal Gasification – Envirotherm (Germany)

Pipe – CPT (Hong Kong), Perco (UK), Angerlehner (Austria)

Joint Ventures/ Subsidiaries/ Associates

Wind Turbines – JV with Leitwind BV for manufacturing of MW-class wind turbines and its components

Air Pollution Control & Cooling Towers – Hamon Shriram Cottrell Private Limited, a JV with Hamon Group, a Belgium-based international player in the field of heat exchangers, cooling towers and air pollution control systems

OGPL Singapore – Equity investments from Bessemer Venture Partners and Olympus Capital

Met Coke – Ennore Coke Limited (31% SEPC shareholding) an Indian listed Company engaged in the manufacture of

metallurgical coke

Manufacturing Plants

Wind turbine manufacturing facilities: Chennai & Gummidipoondi (near Chennai), Puducherry

Cooling tower manufacturing plant: Umbergaon (Gujarat)

Project specific as well as strategic partnerships with a view to emerge as a strong player in every segment

9

Over 35 years of consulting experienceCA, ICWA; PriceWaterhouse Coopers, IBM Consulting

Independent Director

Mr. Sunil Varma

Over 50 years of experience in the steel industry

M. Tech (Mech) – Anantapur Engg.; Commercial Director – SAIL

Independent Director

Mr. S.R. Ramakrishnan

Over 34 years of experience as IAS and over 10 years as Consultant in the field of Environment, Clean Energy

PGD (Mathematics/ Statistics); IAS – TN/Central Government, UN Environment

Independent Director

Mr. K. Madhava Sarma

Over 30 years of experience in Pharma industry with Operations and Corporate Planning & Strategy

M. Tech (Mech) – JU, MBA – IIM (A); ED/EVP - Matrix Laboratories

Independent Director

Mr. R. Sundararajan

Over 20 years of experience in Fund management, Capital markets

M.Sc, M.Phil, AMP (Harvard); MD – UTI Ventures, Senior roles at SEBI/UTI

Nominee Director (UTI)

Mr. K.E.C Raja Kumar

Over 20 years of experience in Consulting and Private Equity

BA (University of California), MBA (Harvard); Commonwealth Capital, McKinsey, Accenture

Non Executive Director

Mr. R. S. Chandra

Over 20 years of experience in various roles at Shriram group companies

PGD (Econ.) – Madras University; Shriram Transport Finance, Shriram City Union

Promoter Director

Mrs. V. Ranganathan

Over 23 years of experience in Project execution, marketing, corporate planning

PGD (Chem) – IIT Madras Joint Managing Director

Mr. M. A. Shariff

Over 18 years of experience in technical handling of projects, project feasibility and in charge of technical tie-ups

B.Tech (Chem), MS – IIT Madras; ICI Limited

Managing Director & CEO

Mr. T. Shivaraman

Over 35 years experience in Strategy, M&A, Capital raising

B. Tech (Mech) – IIT Delhi, MBA – IIM (A); Bank of America, HCL Technology

Chairman & Non-Executive

Mr. A. Duggal

Areas of expertise Education / Prior experiencePositionName

Backed by a strong Board…

10

B. Tech (Kerala University), Over 37 years of experience in Metallurgical and Process industry

Sr. Vice President – MetallurgyMr. G Sugathan

B. Tech (Annamalai University); Over 20 years of experience and in charge of Trenchless Pipe Rehabilitation Division

Vice President, Pipe RehabilitationMr. D. Arivalagan

B. Tech (Andhra University), PGDM (Mumbai University); Over 33 years of experience and responsible for the Engineering division of all projects

Sr. Vice President, EngineeringMr. T. Shreedhar

B. Tech (Madurai University), Over 30 years of industry experience and responsible for OGPL business

MD, Orient Green PowerMr. P. Krishnakumar

B. Tech (Calicut University), PGDM (IGNOU); Over 25 years of experience and Head of Cooling Towers division

CEO, Hamon Shriram CottrellMr. N. Suryanarayanan

B. Tech (Calcutta University); Over 27 years of experience and in charge of execution of Power projects

Vice President – Power Mr. M. Radhakrishnan

B. Tech (Madras University); Over 30 years of experience and in charge of the Water Division

Vice President - WaterMr. R. Parthasarathy

PGD Engineering, National Institute of Technology (Rourkela); Over 28 years of experience and in charge of Business development

Vice President – Process & Metallurgy

Mr. Akhil Behari Das

B. Tech (Annamalai University); Over 30 years of experience in cement, steel and aluminium

COO - Leitner Shriram Manufacturing

Mr. P Thyagarajan

B. Tech. - IIT (Roorkee), MBA, IIM (Calcutta) ; Over 16 years of experience and in charge of corporate finance, HR & Administration, MIS & Corp Com.

CFO Mr. Vivek Sharma

CA, B.Com (University of Mumbai); Over 30 years of experience and in charge of Corporate planning and strategy, project feasibility & evaluation

Senior Vice President, Corporate Planning & Strategy

Mr. S. Ramnath

B. Tech (Annamalai University); Over 28 years of experience and in charge of overall project management, operations

MD, Leitner Shriram ManufacturingMr. P. Ashok

Education / Prior experiencePositionName

…experienced management team

11

…and high quality technical personnel

Employee Classification (Technical/ Non-Technical)

Technical Non-Engineers

40%

Non Technical25%

Technical Engineers

35%

Employee Classification (Segment / Experience)

Average experience for the key management personnel ~ 25 years ~60% of employees have over 10 years of experience Over 75% of employees comprise of technical personnel, of which almost 35% is engineers

27

66

20 143

29

17

22

6 9

11

54

49

7 2012

49

58

1114

18

1 14

Corporate Process & M et Water Pipe Rehab OGPL Leitner Biomass

below 5 yrs 5-10 years

10-20 years 20 years +

Note: Excludes JV with Leitner and Hamon

12

141271

705

5039.7% 9.0%

10.0%8.1%

FY06 FY07 FY08 9 mthsDec08

EBITDA Margin

CAGR: 117%CAGR: 124%

74.7131

353

2435.2%

4.4%5.0%

3.9%

FY06 FY07 FY08 9 mthsDec08

PAT Margin

…with a demonstrated financial track record

Income (INR mn)

1,455

3,006

7,0306,173

FY06 FY07 FY08 9 mthsDec08

EBIDTA (INR mn) PAT (INR mn)

Order Book (INR mn)

Source: Annual Report, Prospectus

3,518

13,320

21,021 20,000

FY06 FY07 FY08 9 mthsDec08

0.28

0.12

0.36

FY06 FY07 FY08

10.0%

13.7%

20.6%

FY06 FY07 FY08

Debt/ Equity (x) Average RoCE (%)

CAGR: 120%

2.4 4.4 3.0

Order book /sales (x)

3.2

13

…marquee client base

Ahemedabad Urban Development Corporation

Birla White Neyveli Lignite Corporation

National Mineral Development Corporation

Reliance Industries

Delhi Jal Board Steel Authority of India

ETA Engineering Private

Shriram City Union Finance

Gujarat Water Supply and Sewerage Board

Sterlite Industries (India)

Tata Steel Jindal Steel & Power Tamilnadu Water Supply and Drainage Board

Laxmi Energy & Foods Limited

Vedanta Alumina Madras Aluminium

Bharat Heavy Electricals

Chennai Petroleum Corporation

Larsen & Toubro

14

Others7%

Unit Trust of India 9%

Reliance Capital

4%

Bessemer Venture Partners

24%

Galleon 5%

Promoter & Promoter

Group42%

Argonaut Ventures

3%

New Vernon 6%

Key Market Metrics

Share Price Movement Shareholding Pattern (Dec 08)

Fund raising from private equity investors

1,00012.679Mar-06Bessemer 4663.80123Dec-06UTI Ventures&3621.25290Nov-07Argonaut*5802.00290Nov-07Galleon* 5071.75290Nov-07New Vernon*

3005.060Mar-05ChrysCapTotal Value (INR mn)No of shares (mn)Price (INR)YearInvestor

*Pre-IPO investors (secondary stake) & Stake sale by the Promoters

Source: BSE, Prospectus, Bloomberg as of 31Mar09Debt & Cash as of Dec08

Key Market Data

~INR 5,250 mnMarket Cap

~INR 2,450 mnCurrent Debt

~INR 654 mnCash

43.2 mnNo. of shares

INR 290/7752 Week H/L

INR 121Market Price

Market Data

0

40

80

120

Feb-08 May-08 Aug-08 Dec-08 Mar-090

100

200

300

Volume in '000s Last Price

15

Business Segments

16

Biomass Power Plants (1/3)

Industry Highlights

India is one of the top 5 countries in generating power through biomass and poised to become a world leader due to its favorableclimatic conditions and agriwaste availability

Current availability of biomass in India is ~ 400 MPTA of which, surplus biomass availability is estimated to be around 145 MPTA, comprising agriculture and forest residues and offering a power generation potential of around 18,000 MW

Additional 5,000 MW of cogeneration potential exists from sugarcane bagasse

An increasingly attractive option

• Year round availability

• Environmental- friendly power generation due to CO2 neutrality & lack of greenhouse gas production

• Incentivizes rural development

Key growth drivers

• Increasing electricity demand

• Cost competitiveness

• Environmental awareness & Government initiatives

An addition of 136% of current capacity to drive the capex requirements in this space

5001,2001,70011th plan additions (2007-2012)

5636901,253As on March 2008

Biomass power projectsCo-gen bagasse basedCapacityMW

Source: Crisil

17

Biomass Power Plants (2/3)

Competitors

Key Financials

Thermax, Areva, Greensol Power

8-10% (pricing is cost plus as project risk is low)

Typical EBIDTA margins

Neutral to slightly positive WC

Typical Working Capital requirements

30-60 daysTypical Collection Period

Segment Overview

Provides design, engineering and construction of biomass based power plants with expertise to handle variety of fuel inputs including rice husk, bagasse, cotton/maize stalk, wood chips and agri waste

Enters into cost plus contracts for work covering project conception, feasibility study, obtaining approvals, detailed engineering, project management and supply, erection and commissioning

• Boilers, turbines, generators, transformers and other electrical systems procured from manufacturers while civil works is outsourced

• Typical size ~ 7.5 – 10 MW (INR 300 – 400 mn)

Successfully implemented 30 MW rice husk based power plant for Lakshmi Energy & Foods

Strong growth outlook on account of the captive client base and advanced discussions with others

18

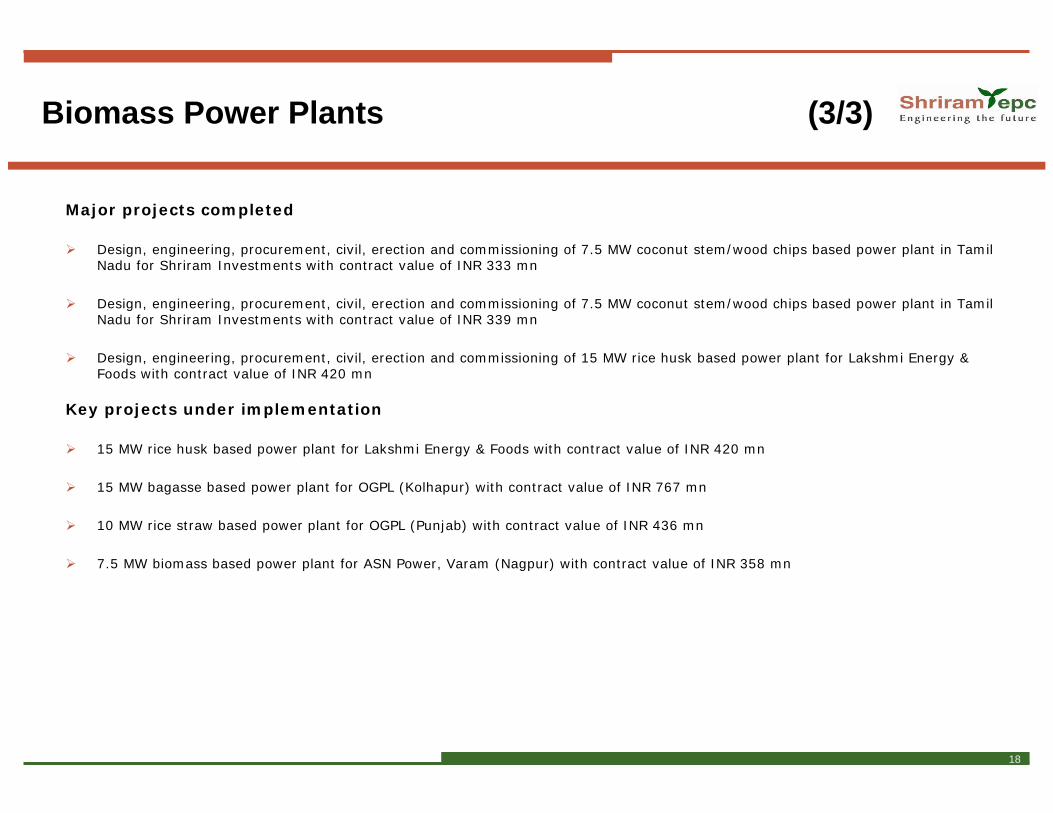

Biomass Power Plants (3/3)

Major projects completed

Design, engineering, procurement, civil, erection and commissioning of 7.5 MW coconut stem/wood chips based power plant in TamilNadu for Shriram Investments with contract value of INR 333 mn

Design, engineering, procurement, civil, erection and commissioning of 7.5 MW coconut stem/wood chips based power plant in TamilNadu for Shriram Investments with contract value of INR 339 mn

Design, engineering, procurement, civil, erection and commissioning of 15 MW rice husk based power plant for Lakshmi Energy & Foods with contract value of INR 420 mn

Key projects under implementation

15 MW rice husk based power plant for Lakshmi Energy & Foods with contract value of INR 420 mn

15 MW bagasse based power plant for OGPL (Kolhapur) with contract value of INR 767 mn

10 MW rice straw based power plant for OGPL (Punjab) with contract value of INR 436 mn

7.5 MW biomass based power plant for ASN Power, Varam (Nagpur) with contract value of INR 358 mn

19

Process and Metallurgy (1/3)

Planned Power Capacity Additions (2007-2012E) MW

Source: Nomura Power Reports Dec & Aug08, CEA

All India Cement Capacity (2007-2011E) MT

Crude Steel Capacity (2007-2012E) MT Key Highlights

Power sector however should continue with capacity additions as planned; some delays on account of financial closure of projects could impact albeit marginally

% of typical capex per MW addressable by SEPC for

Power ~ 40% of cost of setting up, i.e. INR 15 mn 51

6270

86

103

127

FY07 FY08E FY09E FY10E FY11E FY12E

12,704

4,477

11,62314,390 15,450

2,751

1,305

1,445

3,857

7,195

1,000

1,000

500

880

2007-08 2008-09E 2009-10E 2010-11E 2011-12E

Thermal Hydro Nuclear

166 176

218

254288

FY07 FY08 FY09E FY10E FY11E

20

Process and Metallurgy (2/3)

Segment Overview

Provides turnkey solutions for steel (mills + hot metals), cement, thermal power plants and coal gasification Enters into LSTK contracts for work covering basic and detailed engineering, project planning and management, equipment procurement, erection, construction and commissioning Strategy to bid for projects as part of a larger project-specific consortium with international players has resulted in high strike rate with respect to steel segment Exclusive partnership with Envirotherm for coal gasification for 1st of its kind project in India for Jindal Steel Strong focus on thermal power plants and foray into BOP projects Diversified across industries with reputed customer base • SAIL (almost all plants), Jindal, OPG Energy,

Ennore Coke Current order backlog comprising of projects in sectors such as steel, cement, thermal power and coal gasification Strong growth outlook for thermal power plant, BOP projects and coal gasification over the short to medium term and steel/cement over the long term

Competitors

Key Financials

Key Associations/ Technological Partnerships

L&T, McNally Bharat, MECON, Simplex

Steel Mills – Danielli, Siemens, SMS Meer (Project specific)

Coal Gasification – Envirotherm (Exclusive)

10-15% (Steel and Coal gasification), 10% (Thermal Power Plant)

Typical EBIDTA margins

5-10% fund based, 10-15% non-fund based (Steel)

Typical Working Capital requirements

45-60 daysTypical Collection Period

21

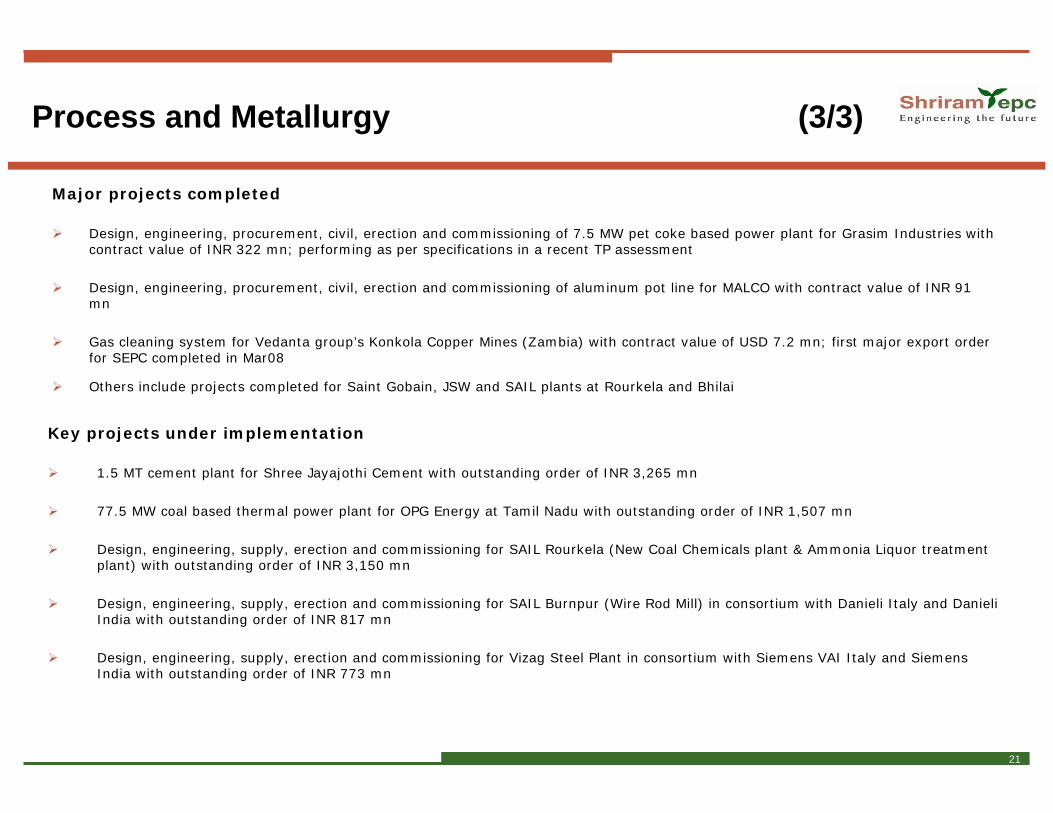

Major projects completed

Design, engineering, procurement, civil, erection and commissioning of 7.5 MW pet coke based power plant for Grasim Industries with contract value of INR 322 mn; performing as per specifications in a recent TP assessment

Design, engineering, procurement, civil, erection and commissioning of aluminum pot line for MALCO with contract value of INR 91mn

Gas cleaning system for Vedanta group’s Konkola Copper Mines (Zambia) with contract value of USD 7.2 mn; first major export order for SEPC completed in Mar08

Others include projects completed for Saint Gobain, JSW and SAIL plants at Rourkela and Bhilai

Process and Metallurgy (3/3)

Key projects under implementation

1.5 MT cement plant for Shree Jayajothi Cement with outstanding order of INR 3,265 mn

77.5 MW coal based thermal power plant for OPG Energy at Tamil Nadu with outstanding order of INR 1,507 mn

Design, engineering, supply, erection and commissioning for SAIL Rourkela (New Coal Chemicals plant & Ammonia Liquor treatment plant) with outstanding order of INR 3,150 mn

Design, engineering, supply, erection and commissioning for SAIL Burnpur (Wire Rod Mill) in consortium with Danieli Italy and Danieli India with outstanding order of INR 817 mn

Design, engineering, supply, erection and commissioning for Vizag Steel Plant in consortium with Siemens VAI Italy and Siemens India with outstanding order of INR 773 mn

22

Water Treatment/ Pipe Rehab (1/3)

Source: Prospectus

Water Infrastructure

Over 70% funding for water and related environment services come from Central/ State allocations

Given the massive fund requirements and pressures on account of increasing population and urbanization, local government bodies and private sector participation is bound to increase

Government backed JNNURM 05 provides INR 500 bn grants over FY06-12 to urban local bodies of 63 cities/towns to facilitate development of water supply, sanitation and urban infrastructure (over 70% for water supply, sewerage and drainage)

Per Capita O&M expenditure on water and sewerage to rise from INR 100 and 150 respectively to INR 300 and 450

Pipe Rehabilitation

Structural problems in water/ sewer pipelines across India

• Encrustation - reduced flow capacity

• Corrosion, structural failure and leakage

• Low pressure

• Ageing pipeline

Given the ageing infrastructure, increasing population and expanding city limits, massive business opportunity for private sector players with access to the new technologies…e.g.

• For the 4 metro cities alone, ~365 km of old trunk sewers exist of which only 40 km have been rehabilitated in the last 8 years,another 85 km are under rehabilitation while balance 240 km yet to rehabilitated for the 4 metro cities alone

• More than 500 km main lateral sewers have to be rehabilitated / upsized

• Estimated INR 15,000 mn business for the next 4-5 years

23

Water Treatment/ Pipe Rehab (2/3)

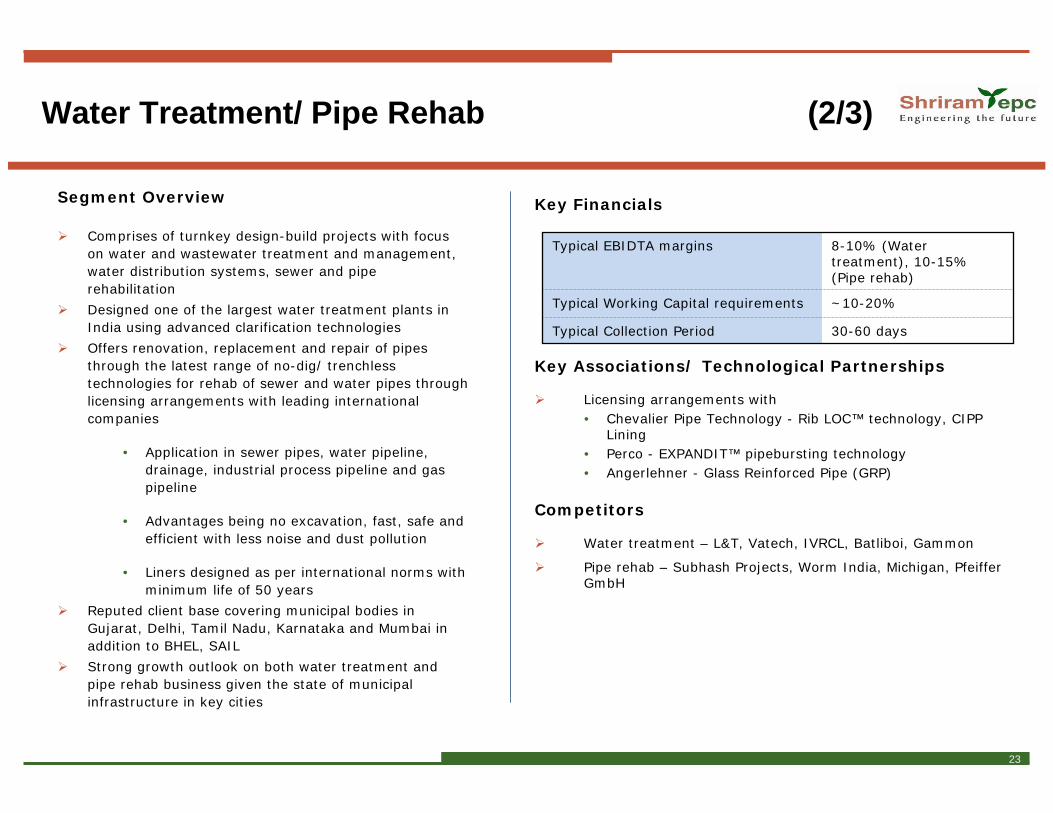

Segment Overview

Comprises of turnkey design-build projects with focus on water and wastewater treatment and management, water distribution systems, sewer and pipe rehabilitation

Designed one of the largest water treatment plants in India using advanced clarification technologies

Offers renovation, replacement and repair of pipes through the latest range of no-dig/ trenchless technologies for rehab of sewer and water pipes through licensing arrangements with leading international companies

• Application in sewer pipes, water pipeline, drainage, industrial process pipeline and gas pipeline

• Advantages being no excavation, fast, safe and efficient with less noise and dust pollution

• Liners designed as per international norms with minimum life of 50 years

Reputed client base covering municipal bodies in Gujarat, Delhi, Tamil Nadu, Karnataka and Mumbai in addition to BHEL, SAIL

Strong growth outlook on both water treatment and pipe rehab business given the state of municipal infrastructure in key cities

Competitors

Key Financials

Key Associations/ Technological Partnerships

Water treatment – L&T, Vatech, IVRCL, Batliboi, Gammon

Pipe rehab – Subhash Projects, Worm India, Michigan, Pfeiffer GmbH

Licensing arrangements with • Chevalier Pipe Technology - Rib LOC™ technology, CIPP

Lining• Perco - EXPANDIT™ pipebursting technology• Angerlehner - Glass Reinforced Pipe (GRP)

8-10% (Water treatment), 10-15% (Pipe rehab)

Typical EBIDTA margins

~10-20%Typical Working Capital requirements

30-60 days Typical Collection Period

24

Water Treatment/ Pipe Rehab (3/3)

Major projects completed

Design, supply and installation of water intake system, water treatment plants and protected water distribution systems for rural water supply for Gujarat Water Supply & Sewerage Board with contract value of INR 192 mn

Design, Engineering, Construction, O&M of 275 MLD water treatment plant for Ahmedabad Urban Development Authority with contract value of INR 198 mn

Desilting, CCTV survey, manhole repair, Pipe joint sealing for Delhi Jal Board with contract value of INR 51 mn

Pipe rehabilitation through trenchless technology in partnership with CPT for Delhi Jal Board with contract value of INR 70 mn

Key projects under implementation

Design, supply and installation of water intake system, water treatment plants and protected water distribution systems for rural water supply for GWSSB Baroda with contract value of INR 224 mn

Design, supply and installation of water supply distribution systems for KUIDFC (Kadri) with contract value of INR 177 mn

Design, supply and installation of sewer treatment plant for Ahmedabad Municipal Corporation with contract value of INR 133 mn

EPC work including surveying, desilting, laying and commissioning for Delhi Jal Board (UTS) using CIPP technology in collaboration with CPT Hong Kong with contract value of INR 316 mn

EPC work including surveying, desilting, laying and commissioning for Delhi Jal Board (NTS) using CIPP technology in collaboration with CPT Hong Kong with contract value of INR 337 mn

EPC work including surveying, desilting, laying and commissioning for Delhi Jal Board (JV with KMG) using Rib LOC technology in collaboration with CPT Hong Kong with contract value of INR 438 mn

JV with Angerlehner using GRP technology for Delhi Jal Board with contract value of INR 551 mn

25

APC systems and Cooling Towers (1/2)

Segment Overview

One of the oldest businesses, now operating through a majority JV with Hamon Group providing APC solutions and cooling towers using technology owned by Hamon Research Cottrell, Inc

Hamon Group is one of the leading international engineering and contracting company based out of Belgium with strong presence in Cooling systems, Process Heat Exchangers, APC equipment and Industrial chimneys

JV focuses on detailed engineering, project planning and management, supply/manufacture, construction, erection and commissioning on turnkey basis

Diverse client base spanning industries such as Power (Thermal and Nuclear), Refineries, Petrochemicals, Chemicals and Metals

• APC – Jindal, Tata Steel, L&T

• Cooling Towers – Adani, Reliance, BHEL, Vedanta

APC products include electrostatic precipitators, bag filters (pulse jet and reverse air), wet and dry scrubbers etc at the Umbergaon (Gujarat) manufacturing facility

Strong growth outlook for draft towers business + export potential on account of Hamon

Competitors

Key Financials

Key Associations/ Technological Partnerships

Air Pollution Control Systems – Thermax, Alstom, BHEL

Cooling Towers – Paharpur (in-house manufacturing, Gammon (civil), GEA India

Air Pollution Control Systems – Hamon Cottrell Research

Cooling Towers – Hamon Group

10% (Air Pollution Control), 12-18% (Cooling Towers)

Typical EBIDTA margins

~10%Typical Working Capital requirements

30 days collection period (except BHEL that could be 90 days)

Typical Collection Period

26

APC systems and Cooling Towers (2/2)

Major projects completed

Design, engineering, procurement, civil, erection and commissioning of cooling tower for

• Vedanta with contract value of INR 1,241 mn

• BHEL with contract value of INR 33 mn

• Neyveli Lignite with contract value of INR 46 mn

Key projects under implementation

Cooling tower systems order from Adani Power with contract value of INR 236 mn

Cooling tower systems order from BHEL with contract value of INR 273 mn

Air Pollution Control systems order from L&T with contract value of INR 270 mn

27

22,247

16,81815,145

8,697

5,899

Germany USA Spain India C hina

Wind Energy (1/4)

4,430

6,270

8,697 9,200

10,580

12,167

13,992

16,091

2005 2006 2007 2008E 2009E 2010E 2011E 2012E

Worldwide Installed capacity of wind power (MW) ’07E

India is the 4th largest windpower generator in the world

Installed capacity in India

With a 20.2% CAGR overa 7 year period, capacityis to double

Source: GEWA and MNRE, Credit Suisse ReportState-wise data as of Jul08

Structural growth in wind installed capacity

30%

21%24% 25%

17%

41%

48%

42%

27%

27% 28%

25%

2002 2003 2004 2005 2006 2007

YoY Global installed capacity YoY installed capacity growth India

State-wise Capacity (MW)

Maharashtra20%

Karnataka12%

Others3%

Tamil Nadu45%

Gujarat14%

Rajasthan6%

28

Wind Energy (2/4)

Segment Overview

Started in 1993 with technical knowhow from Husummer Schiffswerft GmbH for manufacture of 250 kW machines

Installed more than 400 machines of 250 kW till date and achieved over 90% indigenization

In 2007, entered into JV with Netherlands-based Leitwind for expanding product range to include MW-class machines

JV would focus on both 1.5 MW and 250 kW machines• 1.5 MW machines are certified by TUV Europe

SEPC investments in JV:• Leitner Shriram ~ INR 250 mn (Manufacturing)• Shriram Leitwind ~ INR 130 mn (Marketing)

Enters into LSTK contracts for work including farm planning, site identification, manufacture of WTG, development of infrastructure, project management, installation, commissioning, O&M etc

Backward Integration for MW-class machines

In-house manufacture of nacelles, blades, control panel and generator while tower, castings/forgings and bearings would be procured outside

Current Order Book

Strong order outlook with current backlog of ~INR 1,400 mn250 kW machines order book >100% capacityMW class machines – 1st order of 20 machines for ~INR 2,000 mn at advanced stages of discussions

Advantages of Leitwind technology

Key Financials

Key Associations/ Technological Partnerships

Gearless and suitable even for low wind speed areas

Similar reliability and higher turbine yield (Power generation)

Increased efficiency due to permanent magnet technology (reduced mechanical and electrical losses)

51:49 JV with Leitwind for Marketing & 49:51 JV for Manufacturing• Capacity – 120 machines of 250 kW and 80 machines of

1.5 MW

10-15%Typical EBIDTA margins

6 months at peak Typical Working Capital requirements

45 days Typical Collection Period

INR 289 mn*9 mths Dec08 Revenues

~INR 1,400 mnCurrent Backlog (Feb09)

INR 1,487 mnFY08 Revenues

Competitors

Suzlon, Vestas, Gamesa, GE Energy, Enercon

*250 kW machines order slowdown for FY09 ~ delay in order finalization and pending transfer of technical approvals to the JV entity

29

Major projects completed

30 machines of 250 kW wind turbines for Dodanavar at Tamil Nadu/ Karnataka with contract value of INR 390 mn

30 machines of 250 kW wind turbines for Fairdeal at Tamil Nadu/ Karnataka with contract value of INR 336 mn

Key projects under implementation

100 machines of 250 kW wind turbines for Theolia project with contract value of INR 1,130 mn

60 units of 250 kW wind turbines for Berggruen Holdings in Tamil Nadu with contract value of INR 700 mn

Wind Energy (3/4)

30

Wind Energy (4/4)

Comparable uptime guarantee, higher output and lower O&M at competitive pricing

Variable Pitch

Fixed Speed

Geared

Variable Pitch

Variable Speed

Geared

Variable Pitch

Variable Speed

Gearless

Permanent Magnet

~ INR 62 mn ~ INR 70 mn ~INR 66 mn/MW

Tech

nolo

gy

Pricin

g

Reliability ~ 97%

Yield ~ 5% lower

Reliability ~ 97%

Yield – Highest for similar rated capacity

Reliability ~ 97%

Yield ~ 2-3% lower

Players Perfo

rman

ce

31

Orient Green Power (1/2)

Company Overview

OGPL Singapore was founded by SEPC in FY08 with the objective of owning and operating a portfolio of renewable energy assets

OGPL currently has ~100 MW of assets in operation • ~78 MW wind and balance biomass• Equity ~ INR 3,220 mn raised / INR 2,090 mn

deployed• Debt ~ INR 3,240 mn raised/ INR 1,650 mn

deployed

Target to reach ~300 MW by CY10• 108 MW wind and balance would be biomass/ hydel/

co-gen

IPO ready in 3 years with ~300 MW of operational assets• Listing potential at SGX/ NASDAQ/ LSE

Move towards captive or merchant power where potential for pricing is higher

Current pricing for PPA projects ~ INR 2.8-3.3/unit while for

group captive projects ~ INR 4/ unit

35Olympus Capital20Bessemer 20SEPC

Infused Equity (USD mn)Shareholder

Equity Commitments

Financial Closure

Estimated project cost for ~300 MW by 2010 ~ INR 14.5 –INR 14.7 bn or ~INR 50 mn / MW

No immediate equity raising plans; further equity requirements may be met through internal accruals

Debt tied up for ~100 MW, balance at various stages

32

Orient Green Power (2/2)

Capacity between 2 MW ~ 5 MWImplementation on Built Own Operate basis at Distilleries, Cement plants etc

Balancing the portfolio of assetsTo develop capacities in partnershipTo undertake projects without environment and R&R issues

Acquisition of second hand assets at attractive prices New wind farms in EuropePerformance guarantee provided by the SellerLocation at potential sites

Greenfield projects, co-generation as well as acquisitionGeographically diverse assetsCapacity between 5 MW ~ 10 MWLocated in Biomass rich areasBoilers support multiple fuels

BiogasSmall HydelWind PowerBiomass

Business Segments

Timeline based (MW)

2344

25

78

306

15

4017

23

Operational Mar-Sep 09 Apr-Jun 10 Sep-Oct 10

Biomass Wind Biogas Small Hydel Co-Gen

Renewable source based (MW)

23

7823

69

15

30

576

Biomass Wind C o-Gen Small Hydel Biogas

Operational Construction

License/ Land acquired MOU/ Early stage

33

Disclaimer

Some of the statements in this presentation that are not historical facts are forward looking statements. These forward-looking statements include our financial and growth projections as well as statements concerning our plans, strategies, intentions and beliefs concerning our business and the markets in which we operate.

These statements are based on information currently available to us, and we assume no obligation to update these statements as circumstances change. There are risks and uncertainties that could cause actual events to differ materially from these forward-looking statements. These risks include, but are not limited to, the level of market demand for our services, the highly-competitive market for the types of services that we offer, market conditions that could cause our customers to reduce their spending for our services, our ability to create, acquire and build new businesses and to grow our existing businesses, our ability to attract and retain qualified personnel, currency fluctuations and market conditions in India and elsewhere around the world, and other risks not specifically mentioned herein but those that are common to industry.

Further, this presentation may make references to reports and publications available in the public domain. Shriram EPC Ltd. makes no representation as to their accuracy or that the company subscribes to those views / findings.

34

Thank You