SEMINAR ON MODEL GST LAW BY BCAS · Voluntary registration is also provided in section 19(3). ......

33

SEMINAR ON MODEL GST LAW BY BCAS Registration, Returns, Assessment & Refunds BY CA Janak Vaghani.

Transcript of SEMINAR ON MODEL GST LAW BY BCAS · Voluntary registration is also provided in section 19(3). ......

SEMINAR ON MODEL GST LAW

BY BCASRegistration, Returns, Assessment &

Refunds

BY CA Janak Vaghani.

REGISTRATION

• Schedule III provides Liability of following Persons for Registration;-

• Supplier whose aggregate turnover exceeds prescribed limit of 10 lakhs ( Four lakhs for NE States including Sikkim),

• Transitional- All existing registered dealer under earlier act like Vat, service tax, excise etc. (As per proviso to section 19(1) no need to apply but to follow prescribed procedure),

• Successor of business or transferee of business without thresh hold limit,

• Following Persons irrespective of thresh hold limit;-

• Persons making inter-State supply,

• Casual Taxable Person,

• Persons required to pay RCM,

• Non Resident Taxable Persons,

• Persons required to deduct Tax u/s.37,

Made By CA Janak Vaghani

REGISTRATION

• Agent of Supplier,

• Input Service Distributor-S.17

• Persons who supplies goods and/or services

• Through electronic Commerce operator,

• Every Electronic Commerce Operator,

• An Aggregator who supplies services under his brand or trade name

• Such other Persons as may be notified.

• Voluntary registration is also provided in section 19(3).

Made By CA Janak Vaghani

REGISTRATION

• To apply in the State from where he makes a taxable supply-Schedule III.

• No need to get registration if aggregate turnover does not cross thresh hold limit ( Not applicable to specified persons mentioned in Schedule III).

• Aggregate Turnover shall include all supplies whether made by him or made on behalf of all his principals ( Explanation 1 of Schedule III),

• Supply of goods after completion of Job work shall be treated as supply of goods by principal and it shall be excluded in the Aggregate Turnover of registered job worker (Explanation 2 to Schedule III).

Made By CA Janak Vaghani

REGISTRATION

• Single PAN based Registration qua State, but non taxable person may be granted registration on the basis of other prescribed documents- Section 19(4A).

• Persons having multiple activities can apply separately for each business vertical as may be prescribed- S. 19(2).

• If Persons required to take registrations the proper officer may register him by following prescribed procedure-Section 19(5).

Made By CA Janak Vaghani

REGISTRATION

• Grant of Unique Identity Number

• Section 19(6) provides for UIN to following persons;-

• Specialised agencies of UNO MFI,

• Foreign Consulate, Embassy,

• Any other persons or class of persons as may be notified by the board or Commissioner,

For the purpose of grant of refund.

Made By CA Janak Vaghani

REGISTRATION

• Section 19(9) provides for deemed grant of registration /UIN if no deficiency is communicated within prescribed time.

• Rejection of registration under CGST/SGST shall be deemed rejection under SGST/CGST.

• Likewise grant of registration/UIN under CGST/SGST shall be deemed registration/UNI under SGST/CGST.

• On recommendation of GST Council State or Central may specify the categories of persons who may be exempted from registration.

Made By CA Janak Vaghani

REGISTRATION

Special Provisions for Casual Taxable Persons or Non Resident- Section 19A

• Registration valid for period of 90 days may be extended for further period of 90 days,

• To make an advance deposit of tax at the time of application,

• Amount will be equivalent to estimated tax liability during the period for which registration is sought or for extended period.

• It will be credited to the electronic cash ledger.

Made By CA Janak Vaghani

REGISTRATION

• Section 20 provides for amendment to registration for any change in prescribed information.

• The proper officer may reject it after grant of opportunity of hearing.

Made By CA Janak Vaghani

CANCELLATION OF REGISTRATION- S.21

In following cases registration is liable for cancellation;-

• Dis-continuation of business, death of proprietor, transfer of business, amalgamation or demerger or disposal of business ,

• Any change in constitution of business,

• Person (Except registered voluntarily) no longer liable for registration as per schedule III

Made By CA Janak Vaghani

CANCELLATION OF REGISTRATION- S.21

The proper officer may cancel registration on his own motion from such date including anterior date after giving opportunity of hearing in following cases;-

• Contravention of act or rules,

• Failure to file returns for three consecutive period for Composition dealer and for others for continuous period of six months,

• Person taken voluntary registration and has not done business within six months from the date of registration,

• Registration obtained by means of fraud, wilful misstatement etc.

Liability to continue till date of cancellation whether determined before or after the date of cancellation.

Upon cancellation to pay inputs held in stock or the output tax which ever is higher. For capital goods to pay credit taken on inputs as reduced by prescribed percentage points or the tax on transaction value of such goods whichever is higher.

Made By CA Janak Vaghani

REVOCATION OF CANCELLATION OF REGISTRATION- S.22

• Any registered taxable person mayapply for Revocation of Cancellation of registration Within 30 days from the date of service of order.

• Proper officer to revoke or reject

• Not to reject without giving proper of opportunity of hearing.

• Order of rejection of application for registration or cancellation order or rejection of revocation of cancellation of registration can be subject to appeal.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Returns to be filed by registered taxable person monthly except for composition supplier to file quarterly within 21 days of next month or quarter, as the case may be.

• First to file bill wise details of out ward supply within 10 days from the end of month to which it relates- Not applicable to input service distributor and composition supplier and person paying TDS under section 37.

• Details will include intra State as well as inter-State supplies, zero rated supplies, export debit notes credit notes etc.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Then to file details of inward supplies on the basis of outward supplies filed by his supplier and to modify, vary, delete and add any other supplies not included therein and validate and submit by 15th of next month.

• The Board/ Commissioner empowered to extend period by notification.

• Both details can be rectified up to the date of return filed for September of next year or date of filing of annual return whichever is earlier.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Return for next period can not be filed unless return for previous period is filed.

• To pay tax due as per return within the prescribed date for filing of return.

• Unless full tax is paid return will not be treated as valid return.

• To file return even in case of NIL turnover.

• To pay and file TDS return for the month in which tax is deducted within 10 days of next month.

• Input service distributor to file return for every month or part thereof within 13 days of next month.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Revised return can be filed on or before the date of return for September of next month or date of filing of annual return which ever is earlier.

• First return to be filed from the date on which he became liable to pay to the end of month in which the registration is granted. However he has to file details of inward supply from the effective date of registration till the end of the month in which registration is granted.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Provision is made for matching credit of input tax and reversal and reclaim of reduction in out put tax liability and provisional acceptance of thereof .

• In case of invalid return for want of payment of tax no credit of input tax will be available till he makes payment of tax as per return.

• ITC will be matched and any discrepancies will be intimated to both supplier and recipient.

• Any unmatched details not complied by supplier shall be added in tax liability of recipient in return for the month succeeding the month in which discrepancies is communicated.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• In case of duplicate claims the input tax credit taken earlier shall be added in output tax liability in his return for the month in which duplication is communicated.

• Likewise the recipient shall be eligible to reduce his output tax liability if the supplier declares the details of invoice etc. in his valid return within the prescribed time for filing revised returns.

• The interest shall be payable on additional amount due to unmatched or duplicate credit from the date of taking credit to the date of corresponding additions are made.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• The interest shall be payable on additional amount due to unmatched or duplicate credit from the date of taking credit to the date of corresponding additions are made.

• Likewise any reduction on output tax shall be subject to grant of interest maximum up to interest paid by supplier.

• Any reduction of out put tax in contravention of sub section (7) shall be added to out put tax of recipient in his return for the month in which contravention took place and it will be subject to interest.

• Similar provision is made for reversal and reclaim of reduction in out put tax liability for payment with interest.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Every registered taxable person is required to file annual return for every financial year on or before first day of December of next year.

• Every taxable person who is required to get his accounts audited required to file annual return along with audited copy of annual accounts along with reconciliation statement.

• Final return shall be filed within three months from the date of cancellation or date of cancellation order which ever is later.

Made By CA Janak Vaghani

RETURNS ss. 22 TO 33

• Upon failure to file return notice will be issued to file within such time as may be prescribed.

• Late fees will be payable 100 RS. per day subject to maximum of RS. 5000/- for late submission of return, details of outward and inward supplies. In case of annual return late fees of RS. 100 per day subject to maximum of quarter percent of his aggregate turnover.

• Approved Return Preparers eligible to file return etc. on behalf of taxable persons. However liability for correctness remains with taxable persons.

Made By CA Janak Vaghani

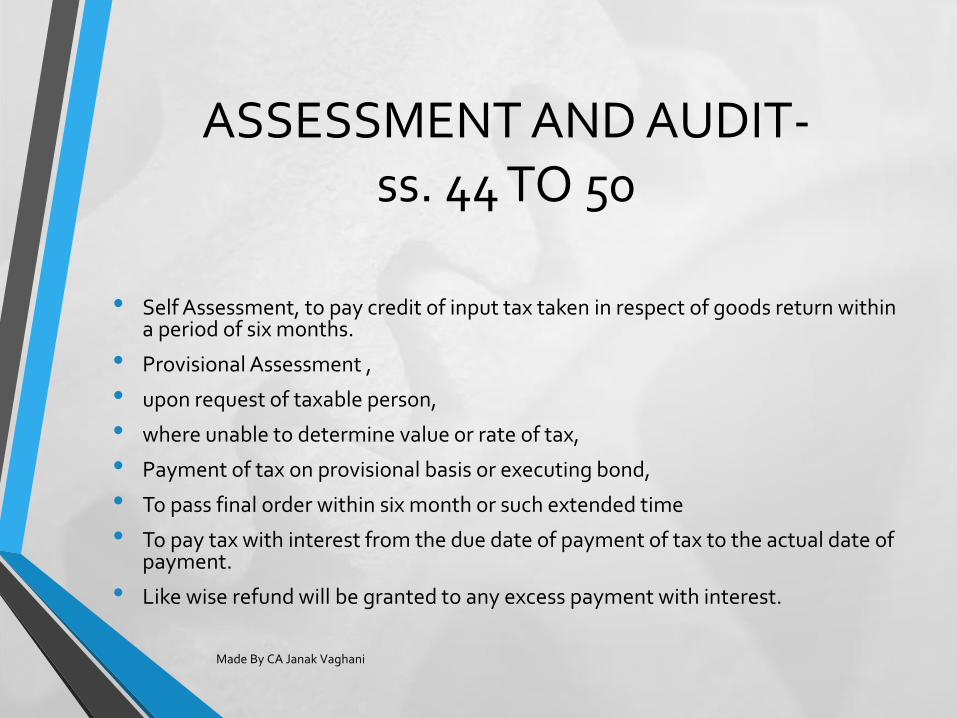

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Self Assessment, to pay credit of input tax taken in respect of goods return within a period of six months.

• Provisional Assessment ,

• upon request of taxable person,

• where unable to determine value or rate of tax,

• Payment of tax on provisional basis or executing bond,

• To pass final order within six month or such extended time

• To pay tax with interest from the due date of payment of tax to the actual date of payment.

• Like wise refund will be granted to any excess payment with interest.

Made By CA Janak Vaghani

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Scrutiny of Returns to verify correctness of returns,

• To issue notice for any discrepancies,

• To be complied within 30 days or extended period,

• Failure to pay tax with interest after acceptance or to comply notice or failure to take the corrective measure, will attract provisions of audit by department.

Made By CA Janak Vaghani

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Assessment of Unregistered Persons,

• Who fails to take registration even though liable to take so,

• Best Judgment assessment within 5 years from due date of filing annual return for the relevant year.

Made By CA Janak Vaghani

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Summary assessment in certain special cases

• When any evidence showing tax liability,

• To protect interest of revenue,

• On sufficient grounds to believe that any delay

• In passing assessment adversely affect interest of revenue,

• To issue assessment order.

• When taxable person is not ascertainable and such liability pertains to supply of the goods,

• The person in charge of such goods shall be liable to pay tax.

• Upon application made by taxable person within 30 days from the date of receipt of order or ,

• Own his own the Additional /Joint Commissioner who considers the order erroneous ,

• May withdraw the order as per procedure laid down in section 51.

Made By CA Janak Vaghani

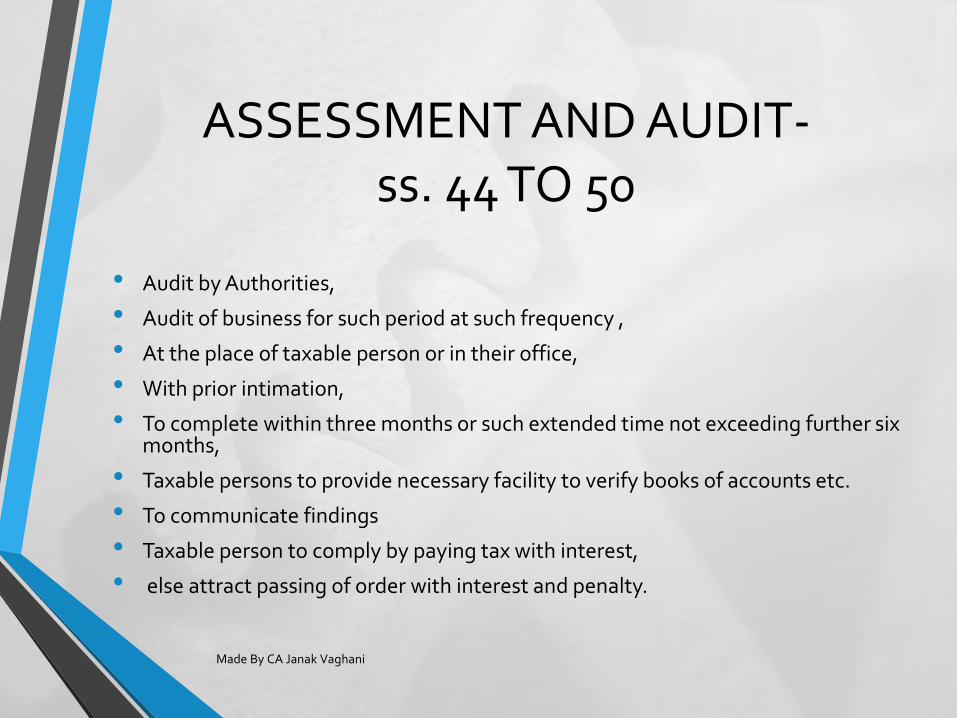

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Audit by Authorities,

• Audit of business for such period at such frequency ,

• At the place of taxable person or in their office,

• With prior intimation,

• To complete within three months or such extended time not exceeding further six months,

• Taxable persons to provide necessary facility to verify books of accounts etc.

• To communicate findings

• Taxable person to comply by paying tax with interest,

• else attract passing of order with interest and penalty.

Made By CA Janak Vaghani

ASSESSMENT AND AUDIT-ss. 44 TO 50

• Special Audit over and above audit by , Chartered Accountant or Cost Accountant etc.

• When value is not correctly declared or,

• The credit availed is not within the normal limit,

• to direct taxable person to get his accounts audited by any nominated Chartered Accountant or Cost Accountant.

• To submit report within period of 90 days or extended period of further 90 days,

• The opportunity of hearing will be granted to taxable person,

• Any tax payable found to be payable as a result of audit payable by taxable person with interest.

Made By CA Janak Vaghani

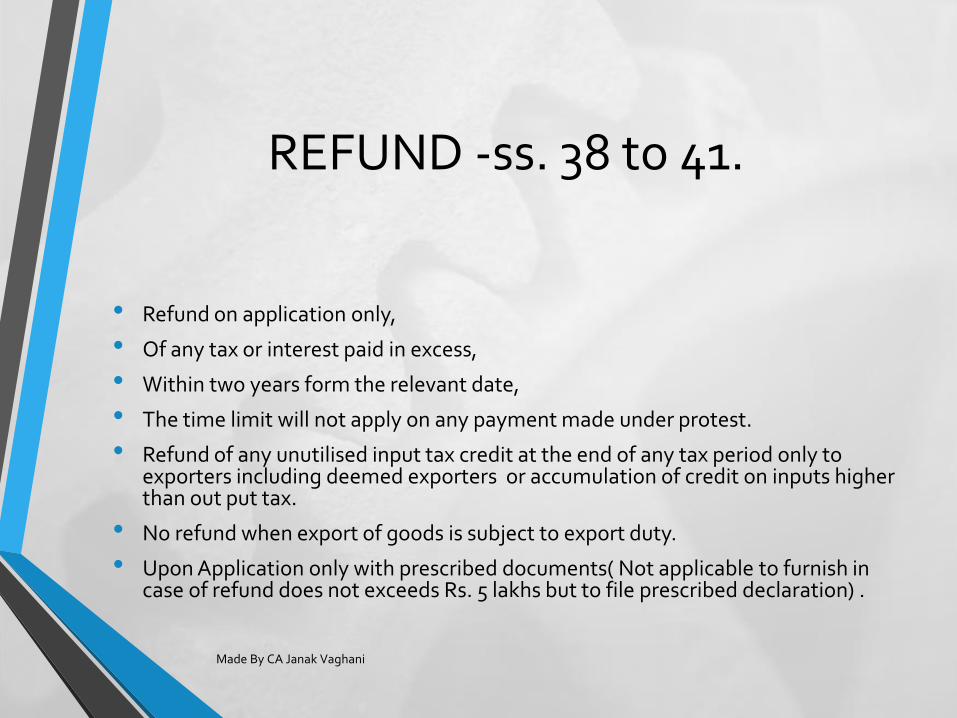

REFUND -ss. 38 to 41.

• Refund on application only,

• Of any tax or interest paid in excess,

• Within two years form the relevant date,

• The time limit will not apply on any payment made under protest.

• Refund of any unutilised input tax credit at the end of any tax period only to exporters including deemed exporters or accumulation of credit on inputs higher than out put tax.

• No refund when export of goods is subject to export duty.

• Upon Application only with prescribed documents( Not applicable to furnish in case of refund does not exceeds Rs. 5 lakhs but to file prescribed declaration) .

Made By CA Janak Vaghani

REFUND -ss. 38 to 41.• No refund if tax paid is collected or passed to another

person.

• Exporter to get 80 % of refund amount on a provisional basis.

• Remaining 20% after scrutiny of documents furnished.

• To pass order within 90 days from the receipt of application means containing prescribed information.

Made By CA Janak Vaghani

REFUND -ss. 38 to 41.

• Grant of refund subject to unpaid amount of any tax, interest or penalty by specified date,

• Specified date means last date for filing appeal if appeal is not filed; In case of appeal, thirty days after the last date of filing.

• Refund may be withhold subject to payment of interest, if the appeal is filed against the order determining refund.

• No refund if the amount is less than RS. 1000/-.

Made By CA Janak Vaghani

REFUND -ss. 38 to 41.

• Relevant date means;-

• In case of export of goods;-

-by sea or air- the date on which aircraft loaded or leaves India,

-By land – the date on which such goods pass the frontier,

- By post – the date of goods by concerned post office to a place outside India.

• In case of deemed export the date on which return relating to deemed export is filed.

• In case of refund due to goods returned for remade or remake refined recondition or any other similar process in any place of business- the date of entry in to the place of business for the said purpose.

Made By CA Janak Vaghani

REFUND -ss. 38 to 41.

• In case of export of services- the date of receipt of foreign exchange if the service is completed prior to it or the date of issue of invoice when the receipt is in advance.

• In case of refund as per any order- the date of communication of such order.

• In case of refund of unutilised credit Under sub section (2)- the end of financial year in which such claim of refund arises.

• In case of payment of tax provisionally- the date of adjustment of tax after the final assessment.

• Interest is payable on delay of grant of refund beyond period of three months from receipt of application.

Made By CA Janak Vaghani

THANK YOU

CA Janak Vaghani - +91 93246 80306