Seminar 500000 total

27

Our company has been developed to assist ordinary people achieve significant savings and financial freedom which will enable them to create real personal wealth in the shortest possible time. Total Repay is a proven system with a successful track record that operates in conjunction with leading banking and lending institutions.

-

Upload

colin-outhred -

Category

Economy & Finance

-

view

78 -

download

1

Transcript of Seminar 500000 total

Our company has been developed to assist

ordinary people achieve significant savings

and financial freedom which will enable

them to create real personal wealth in the

shortest possible time.

Total Repay is a proven system with a

successful track record that operates in

conjunction with leading banking and

lending institutions.

IS TOTAL REPAY FOR YOU?

Do You Like What We Have To Offer?

Will It Benefit Your Family and Yourselves?

Is It Affordable?

OF 100 PEOPLE AT AGE 65

1 Will be Rich

4 Will be Financially Independent

5 Will Still be Working

12 Will be Broke

29 Will be Dead

49 Will be Dependent on Welfare or Charity

In other words, 95% will either be

Dead or Dead Broke !

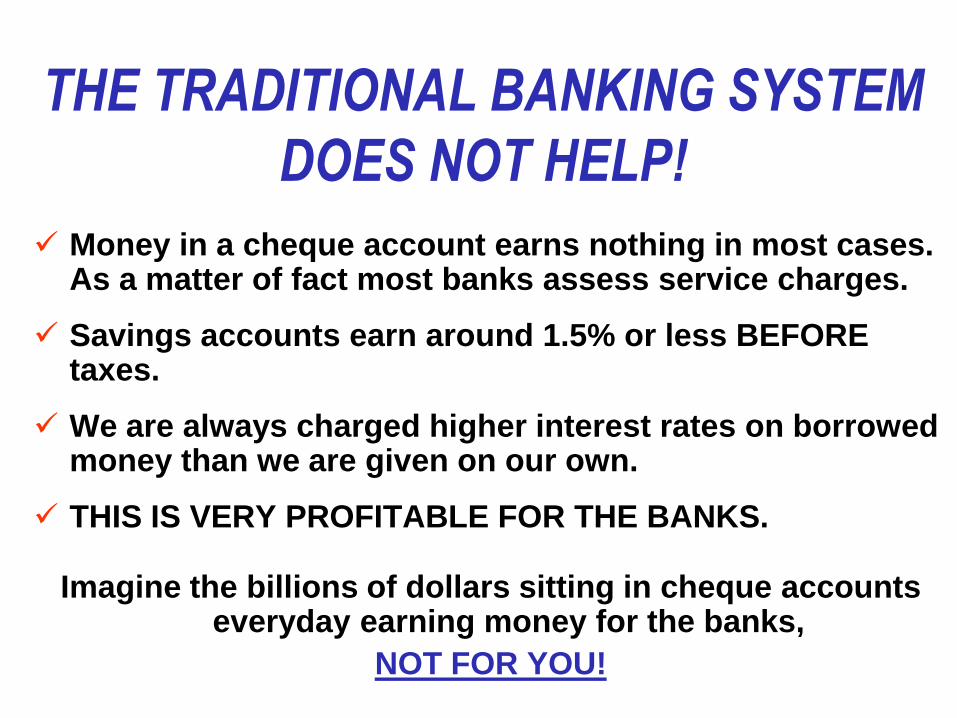

THE TRADITIONAL BANKING SYSTEM

DOES NOT HELP!

Money in a cheque account earns nothing in most cases. As a matter of fact most banks assess service charges.

Savings accounts earn around 1.5% or less BEFORE taxes.

We are always charged higher interest rates on borrowed money than we are given on our own.

THIS IS VERY PROFITABLE FOR THE BANKS.

Imagine the billions of dollars sitting in cheque accounts everyday earning money for the banks,

NOT FOR YOU!

HOW WOULD YOU LIKE TO

BEAT THE BANKS?

Remember the difference between savings

and lending rates is around 5%

ENJOYED BY THE BANKS!

By using the “Total Repay” system, not only

is the bank denied this margin, but it goes

directly to you

TAX FREE !*

*Please consult your accountant, we do not offer tax advice.

THE TRADITIONAL MORTGAGE

WE ARE PENALISED BY THE WAY THEY OPERATE.

In the first years we pay mostly interest and very

little principal.

Most people compound their situation by refinancing or buying a new home every 5 years.

which…

BEGINS THE INTEREST PAYMENT PROCESS ALL OVER AGAIN!

The Cost Of A $500,000 Mortgage @ 6%

(When is 6% NOT 6%?

Year Total Paid Principal Interest Balance

1

2

10

20

30

35,972

71,945

359,729

719,459

1,079,192

6,140

12,658

81,570

229,980

500,000

29,832

59,287

278,159

489,479

579,192

493,860

487,341

418,429

270,019

0

More Than the Cost in

Interest Alone

Compare the Options

$500,000Total

Repay

Principal

& Interest

Fortnightly

Principal

& Interest

Monthly

YEARS TO BE

DEBT FREE

INTEREST PAID

12 YEARS

$209,731

25 YEARS

$468,776

30 YEARS

$579,192

YOU HAVE CHOICES !REGULAR CHEQUE ACCOUNT

Deposit Income

Household

Cheque

Earns

0%

Interest

• Cheques

• Bank Fees

• Money Orders

• Travellers Cheques

• Bounced Cheques

• Etc.

Mortgages

Living Expenses

Credit Cards, etc.

Miscellaneous

INTEREST ONLY 2 ND MORTGAGE (Line of Credit.)

Income

Lowers

Balance –

Saves $$

(interest)

Deposit Income/

Make Payment

Mortgages

Living Expenses

Credit Cards, etc.

Miscellaneous

We Pay

For

BENEFITS

• Simple Interest

• Tax Deductible

• Interest Only

• Pre-Approved Limit

• Purchasing Power

John & Jane Doe

What’s In A Home?

Value

1st Mortgage

Payment/Month

Principal/Month

$600,000

$500,000

$3,000

$500

Fixed 1st Mortgage

1st Year Balance

Yearly Principal

Sub Total

$500,000

$6,000

$494,000

Example: Consumer Debt Debts That Could Be Consolidated

Loans (car, etc.) Amt. Pymt.

Cards, etc. Amt. Pymt.

Total

$20,000

$30,000

$500

$785

$1,285$50,000

Example: Consumer Debt

Debts That Could Be Consolidated

Loans (car, etc.) Amt. Pymt.

Cards, etc. Amt. Pymt.

Total

$20,000

$30,000

$500

$785

$1,285

Line of Credit $50,000

$50,000

6%

Interest

Only

Line of Credit $50,000

Payment $250

Pay Off

-$250

$1,035

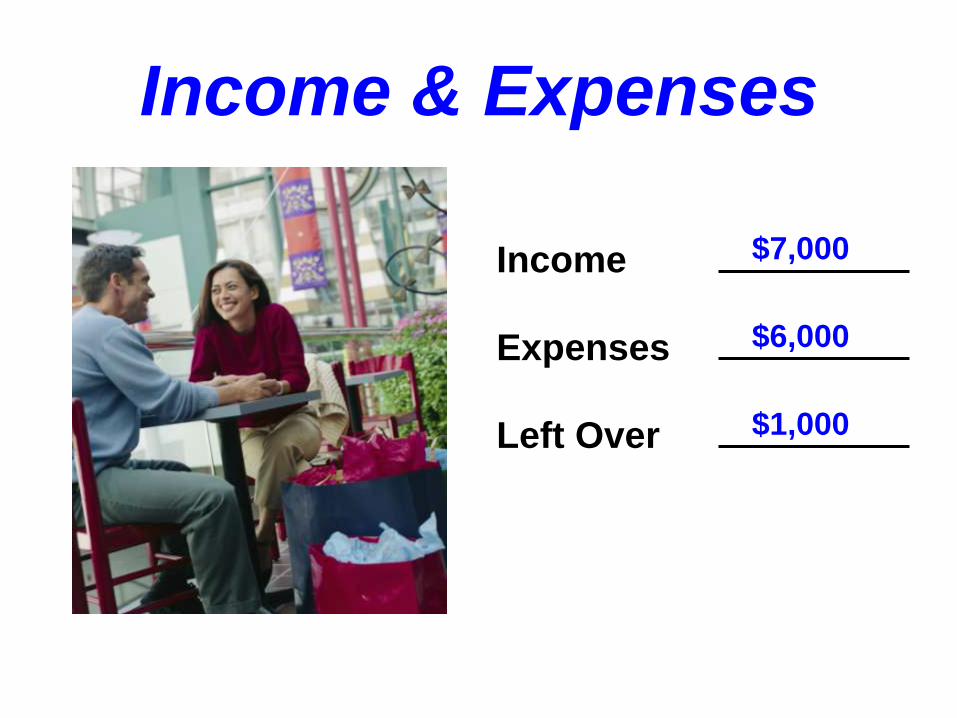

Income & Expenses

Income

Expenses

Left Over

$7,000

$6,000

$1,000

2nd MORTGAGE AS THE

EVERYDAY ACCOUNTStart Balance

Payment / Income

Balance

Expenses

Balance Month One

Payment / Income

Balance

Expenses

Balance Month Two

$50,000

-7,000

43,000

+6,000

49,000Surplus 1st mo. $1,000

-7,000

42,000

Surplus 2nd mo. $1,000

+6,000

48,00012 Month $12,000

2nd Balance $38,000

Reducing the 1st Mortgage

1st Year Bal.

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 1

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 2

$500,000

$6,000

$494,000

From 2ND Mortgage

$482,000

$12,000$12,000

Amortisation Schedule

Amortisation Schedule For: John & Jane

Property Address: 13 Owe D’ Bank Way

Loan Programme:

Loan Amount $500,000

Interest Rate 6%

Term 30 Years

1 1 2.997.75 2,500.00 497.75 499,502.25

1 2 2.997.75 2,497.51 500.24 499,002.01

1 3 2.997.75 2,495.01 502.74 498,499.27

1 4 2.997.75 2,492.50 505.25 497,994.02

1 5 2.997.75 2,489.97 507.78 497,486.24

1 6 2.997.75 2,487.43 510.32 496,975.92

1 7 2.997.75 2,484.88 512.87 496,463.05

1 8 2.997.75 2,482.32 515.43 495,947.62

1 9 2.997.75 2,479.74 518.01 495,429.61

1 10 2.997.75 2,477.15 520.60 494,909.01

1 11 2.997.75 2,474.55 523.20 494,385.81

1 12 2.997.75 2,471.93 525.82 493,859.99

35,973.00 29,832.99 6,140.01

2 1 2.997.75 2,469.30 528.45 493,331.54

2 2 2.997.75 2,466.66 531.09 492,800.45

2 3 2.997.75 2,464.00 533.75 492,266.70

2 4 2.997.75 2,461.33 536.42 491,730.28

2 5 2.997.75 2,458.65 539.10 491,191.18

2 6 2.997.75 2,455.96 541.79 490,649.39

2 7 2.997.75 2,453.26 544.50 490,104.89

2 8 2.997.75 2,450.52 547.23 489,557.66

2 9 2.997.75 2,447.79 549.96 489,007.70

2 10 2.997.75 2,445.04 552.71 488,454.99

2 11 2.997.75 2,442.27 555.48 487,899.51

2 12 2.997.75 2,439.50 558.25 487,341.26

35,973.00 29,454.27 6,518.73

Year Month Payment Interest Principal Balance

3 1 2.997.75 2,436.71 561.04 486,780.22

3 2 2.997.75 2,433.90 563.85 486,216.37

3 3 2.997.75 2,431.08 566.67 485,649.70

3 4 2.997.75 2,428.25 569.50 485,080.20

3 5 2.997.75 2,425.40 572.35 484,507.85

3 6 2.997.75 2,422.54 575.21 483,932.64

3 7 2.997.75 2,419.66 578.09 483,354.55

3 8 2.997.75 2,416.77 580.98 482,773.57

3 9 2.997.75 2,413.87 583.88 482,189.683 10 2.997.75 2,410.95 586.80 481,602.89

3 11 2.997.75 2,408.01 589.74 481,013.15

3 12 2.997.75 2,405.07 592.68 480,421.47

35,973.00 29,052.21 6,920.694 1 2.997.75 2,402.10 595.65 479,824.82

4 2 2.997.75 2,399.12 598.63 479,226.19

4 3 2.997.75 2,396.13 601.62 478,624.57

4 4 2.997.75 2,393.12 604.63 478,019.94

4 5 2.997.75 2,390.10 607.65 477,412.29

4 6 2.997.75 2,387.06 610.69 476,801.60

4 7 2.997.75 2,384.01 613.74 476,187.86

4 8 2.997.75 2,380.94 616.81 475,571.05

4 9 2.997.75 2,377.86 619.89 474,951.16

4 10 2.997.75 2,374.76 622.99 474,328.17

4 11 2.997.75 2,371.64 626.11 473,702.06

4 12 2.997.75 2,368.51 629.24 473,072.82

35,973.00 28,625.35 7,347.65

Year Month Payment Interest Principal Balance

REDUCING THE 1st MORTGAGE

1st Year Bal.

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 1

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 2

$500,000

$6,000

$494,000

From 2nd Mortgage

$482,000

$6,500

$475,500

$12,000$12,000$12,000

$463,500

Interest Savings

From Amortization$81,000

$12,000

3 1 2.997.75 2,436.71 561.04 486,780.22

3 2 2.997.75 2,433.90 563.85 486,216.37

3 3 2.997.75 2,431.08 566.67 485,649.70

3 4 2.997.75 2,428.25 569.50 485,080.20

3 5 2.997.75 2,425.40 572.35 484,507.85

3 6 2.997.75 2,422.54 575.21 483,932.64

3 7 2.997.75 2,419.66 578.09 483,354.55

3 8 2.997.75 2,416.77 580.98 482,773.57

3 9 2.997.75 2,413.87 583.88 482,189.683 10 2.997.75 2,410.95 586.80 481,602.89

3 11 2.997.75 2,408.01 589.74 481,013.15

3 12 2.997.75 2,405.07 592.68 480,421.47

35,973.00 29,052.21 6,920.694 1 2.997.75 2,402.10 595.65 479,824.82

4 2 2.997.75 2,399.12 598.63 479,226.19

4 3 2.997.75 2,396.13 601.62 478,624.57

4 4 2.997.75 2,393.12 604.63 478,019.94

4 5 2.997.75 2,390.10 607.65 477,412.29

4 6 2.997.75 2,387.06 610.69 476,801.60

4 7 2.997.75 2,384.01 613.74 476,187.86

4 8 2.997.75 2,380.94 616.81 475,571.05

4 9 2.997.75 2,377.86 619.89 474,951.16

4 10 2.997.75 2,374.76 622.99 474,328.17

4 11 2.997.75 2,371.64 626.11 473,702.06

4 12 2.997.75 2,368.51 629.24 473,072.82

35,973.00 28,625.35 7,347.65

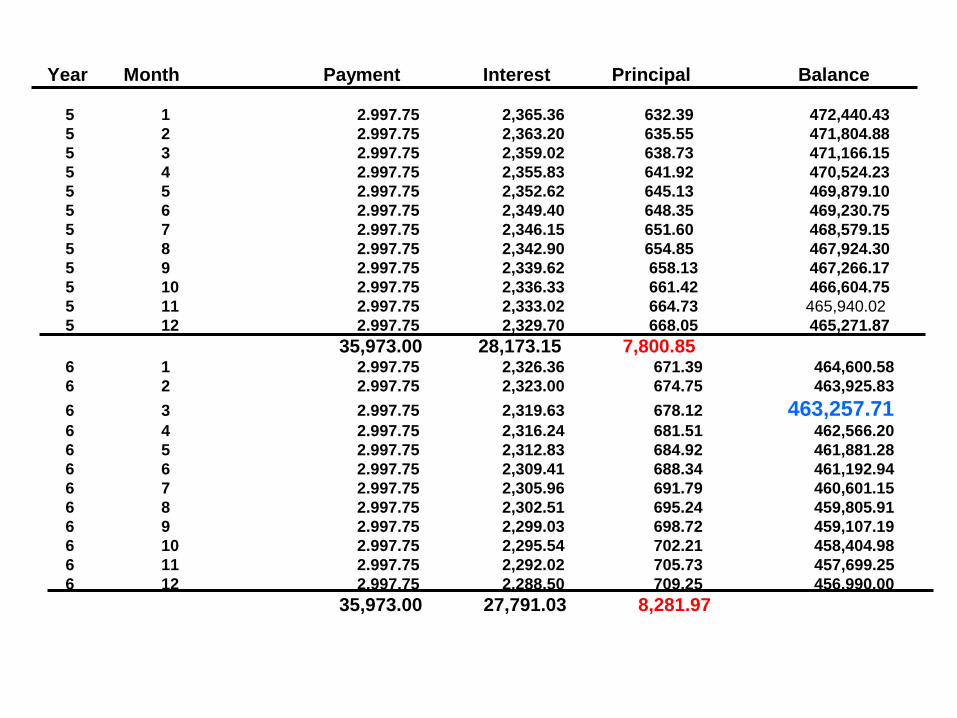

Year Month Payment Interest Principal Balance

Year Month Payment Interest Principal Balance

5 1 2.997.75 2,365.36 632.39 472,440.43

5 2 2.997.75 2,363.20 635.55 471,804.88

5 3 2.997.75 2,359.02 638.73 471,166.15

5 4 2.997.75 2,355.83 641.92 470,524.23

5 5 2.997.75 2,352.62 645.13 469,879.10

5 6 2.997.75 2,349.40 648.35 469,230.75

5 7 2.997.75 2,346.15 651.60 468,579.15

5 8 2.997.75 2,342.90 654.85 467,924.30

5 9 2.997.75 2,339.62 658.13 467,266.17

5 10 2.997.75 2,336.33 661.42 466,604.75

5 11 2.997.75 2,333.02 664.73 465,940.02

5 12 2.997.75 2,329.70 668.05 465,271.87

35,973.00 28,173.15 7,800.856 1 2.997.75 2,326.36 671.39 464,600.58

6 2 2.997.75 2,323.00 674.75 463,925.83

6 3 2.997.75 2,319.63 678.12 463,257.716 4 2.997.75 2,316.24 681.51 462,566.20

6 5 2.997.75 2,312.83 684.92 461,881.28

6 6 2.997.75 2,309.41 688.34 461,192.94

6 7 2.997.75 2,305.96 691.79 460,601.15

6 8 2.997.75 2,302.51 695.24 459,805.91

6 9 2.997.75 2,299.03 698.72 459,107.19

6 10 2.997.75 2,295.54 702.21 458,404.98

6 11 2.997.75 2,292.02 705.73 457,699.25

6 12 2.997.75 2,288.50 709.25 456,990.00

35,973.00 27,791.03 8,281.97

REDUCING THE 1st MORTGAGE

1st Year Bal.

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 1

Yearly Prin.

Sub Total

From 2nd Mort

Total Year 2

$500,000

$6,000

$494,000

From 2nd Mortgage

$482,000

$6,500

$475,500

$12,000

$463,500

Interest Savings

From Amortization$81,000

SAVINGS YEAR ONE$81,000

SAVINGS YEAR TWO$69,000

$150,000

$12,000

$12,000

THE TOTAL REPAY SOLUTION

• We evaluate your total consumer debt

• We calculate the exact split for your 1st and 2nd

Mortgages to maximise your savings.

• Use your Line of Credit like your current household

account to avoid interest and simplify your finances.

• Should your loans ever need restructuring, a certified

Total Repay broker is there to assist.

WHAT INVESTMENT IS REQUIRED ?

The $ deposit paid tonight is “Fully Refundable” if we do not save you at least $30,000 plus the cost of the programme.

Although we do get paid there are no “out of pocket” expenses involved.

The system is Fully Transferable to any property in which one of our representatives originates the mortgage.

This information offers no guarantee. All financial decisions should be done with the advice and counsel

of a qualified solicitor, financial planner or accountant. Success experienced through the “Total Repay”

system varies by client and success determined by individual participation.

![[XLS] creditors list.xlsx · Web view1 97571010 9/4/2017 2 30000000 3 20000000 4 1200000 5 3000000 6 1000000 7 5000000 8 500000 9 210000 10 500000 11 500000 12 500000 13 355000 14](https://static.fdocuments.in/doc/165x107/5aaaeb467f8b9a6c188eda50/xls-creditors-listxlsxweb-view1-97571010-942017-2-30000000-3-20000000-4-1200000.jpg)