Seize high growth Indian banking opportunities through ... · 1 Indian banking opportuntiies IBM...

31

IBM Business Consulting Services ibm.com/bcs An IBM Institute for Business Value executive brief Seize high growth Indian banking opportunities through focus and execution

Transcript of Seize high growth Indian banking opportunities through ... · 1 Indian banking opportuntiies IBM...

IBM Business Consulting Services

ibm.com/bcs

An IBM Institute for Business Value executive brief

Seize high growth Indian banking opportunities through focus and execution

IBM Business Consulting Services, through the IBM Institute for Business Value, develops

fact-based strategic insights for senior business executives around critical industry-specific

and cross-industry issues. This executive brief is based on an in-depth study by the Institute’s

research team. It is part of an ongoing commitment by IBM Business Consulting Services to

provide analysis and viewpoints that help companies realize business value. You may contact

the authors or send an e-mail to [email protected] for more information.

Indian banking opportuntiies IBM Business Consulting Services1

Introduction India is poised to become the world’s fourth largest economy in the span of two decades.1 Economic prosperity is providing many in this populous nation with real purchasing power; it simply is an opportunity that cannot be overlooked by global banks. Despite its appeal, India remains a developing economy. Thus, global banks seeking a presence or expansion in India must craft a business strategy that considers the country’s attendant challenges: long-established competitors; rudimentary infrastructure; dynamic political environment; restrictive regulations; and developing country operational risks.

These challenges should be weighed against the potential gains from entering the marketplace, as well as the likely cost of doing nothing. Extensive research conducted by the IBM® Institute for Business Value pinpointed four of the most promising product areas for global banks entering the Indian market: housing loans, automobile loans, small and medium enterprise (SME) banking and personal financial services. However, recognizing the growth opportunities is only the beginning. Global banks targeting India as a source of new growth will have to do much more than just "show up" – success will lie in the details of execution.

What’s hot in Indian retail bankingWith one of the most underpenetrated retail lending markets in Asia-Pacific, India offers great potential. India’s mortgage debt in 2002 totaled only 2 percent of gross domestic product (GDP), compared to 7 percent of Thailand’s GDP, 8 percent of GDP in China and much higher proportions in other parts of the region: Malaysia (28 percent), South Korea (30 percent) and Hong Kong (52 percent).2 While India remains characterized by extreme wealth and poverty, a middle class is beginning to emerge, with absolute demand for products and services on the rise.

To seize this opportunity, new market entrants must exploit specific market niches and leverage best-in-class capabilities while addressing the unique challenges of the Indian banking environment. Four banking product areas with high growth potential have been identified: • Housing loans - The appealing combination of low, stable interest rates, rising household income and

more receptive customer attitudes toward holding debt translated into a market that expanded 35 percent annually from 1999 to 2004.3

• Vehicle loans – The automotive lending market benefits from the same drivers that are shaping the mortgage opportunity; car sales volume in 2004 soared to more than a million vehicles, up from 664,127 in 2003 and beating earlier estimates of reaching 954,354 annually in 2007.4

• SME banking – The public sector banks in India have traditionally focused on serving big industry rather than small businesses; however, India’s SME market has expanded to over 3.5 million businesses which are growing, increasingly exporting and importing, and demanding more sophisticated banking products and services.5

Contents

1 Introduction

2 India’s bright economic forecast: Continuing growth

5 A view of India’s banking industry

8 Global banks in India: Gaining a foothold

11 Identifying high-potential retail entry points

13 Credit products: Housing and vehicle loans

16 Full-service offerings: Small and medium enterprise banking and personal financial services

20 Crafting an India-specific retail banking strategy

23 About the authors

23 About IBM Business Consulting Services

24 References

Indian banking opportuntiies IBM Business Consulting Services2

• Personal financial services – The growing market for wealth management offers good opportunities for banks that can establish the right combination of account management and distribution infrastructure. Banks and brokerages are doing business with less than a third of the 50,000 families in India with net worth of US$1 million and higher.6

India’s bright economic forecast: Continuing growth During the last decade, India has emerged as one of the biggest and fastest growing economies in the world. The strengthening economy in India has been fueled by the convergence of several key influences: liberalization policies of the government, growth of key economic sectors, development of an English-speaking, well-educated workforce and the emergence of a middle-class population.

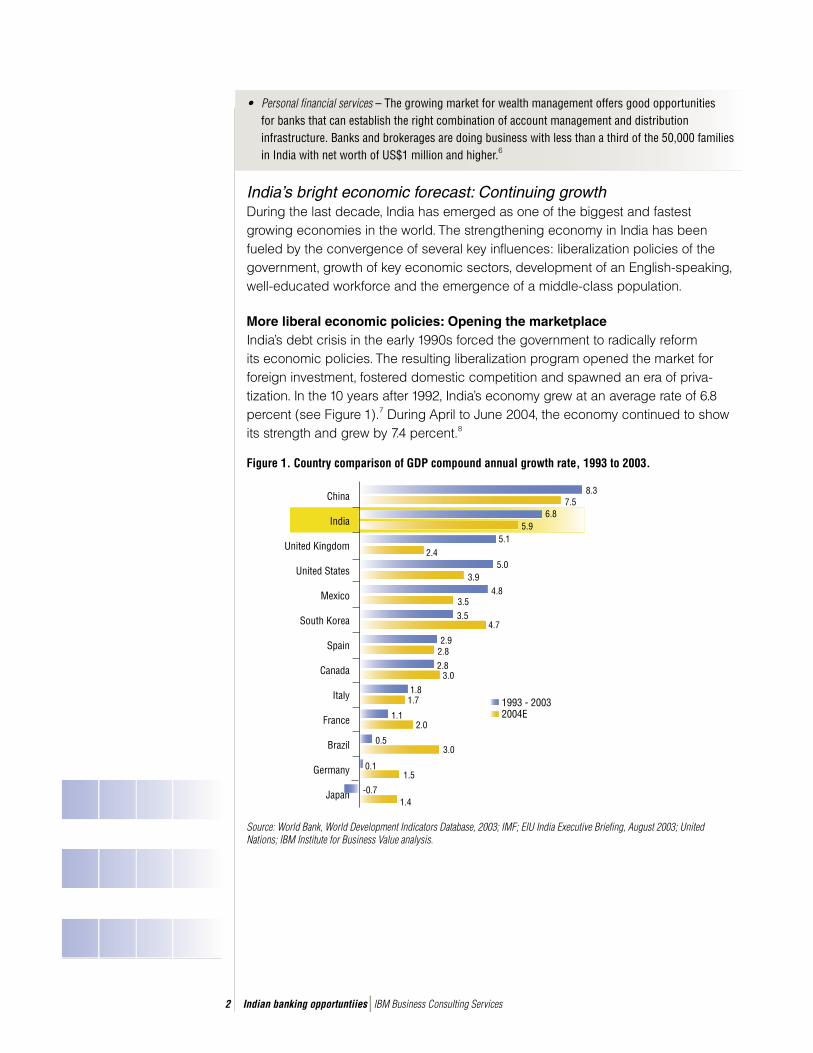

More liberal economic policies: Opening the marketplace India’s debt crisis in the early 1990s forced the government to radically reform its economic policies. The resulting liberalization program opened the market for foreign investment, fostered domestic competition and spawned an era of priva-tization. In the 10 years after 1992, India’s economy grew at an average rate of 6.8 percent (see Figure 1).7 During April to June 2004, the economy continued to show its strength and grew by 7.4 percent.8

Figure 1. Country comparison of GDP compound annual growth rate, 1993 to 2003.

Source: World Bank, World Development Indicators Database, 2003; IMF; EIU India Executive Briefing, August 2003; United Nations; IBM Institute for Business Value analysis.

China

India

United Kingdom

United States

Mexico

South Korea

Spain

Canada

Italy

France

Brazil

Germany

Japan

8.3

1993 - 20032004E

7.56.8

5.95.1

2.45.0

3.94.8

3.53.5

4.7

2.92.8

2.83.0

1.81.7

1.12.0

0.53.0

0.11.5

-0.71.4

Indian banking opportuntiies IBM Business Consulting Services3

Foreign direct investment (FDI) grew more than twenty-fold, from just under US$0.13 billion in 1992 to almost US$2.86 billion in 2003. Meanwhile, privatization accelerated between 2000 and 2002, when 13 state-owned companies were sold,9 while the Indian government recently raised another US$3.41 billion by selling off stakes in 6 state-owned firms.10 The surge in FDI helped to create a capital markets boom and reduced the overall cost of borrowing for Indian companies, particularly contributing to expansion of the services, agriculture and manufacturing sectors.

Political changes make pace of liberalization less predictable In the general election of May 2004, the incumbent Bharatiya Janata Party (BJP) was defeated by the “upset victory” of the Congress party, which led a coalition of groups with diverse, narrow interests. For the first time since 1996, the Congress party controls India’s government. Former finance minister Manmohan Singh became Prime Minister and other key government roles were filled by leaders such as Mr. Pranab Mukherjee and Mr. P. Chidambaram, who supported market liberalization when serving in prior Congress governments.

Since foreign investment and access to external markets remain critical to the growth of the country – and specifically, its banking system – reform-minded institutional and foreign investors are monitoring the early words and actions of the new administration, uncertain whether its predecessor’s liberalization program will continue. While concerns remain given some of the mandates of its manifesto, the Common Minimum Program, the coalition’s actions thus far appear to be a “mixed bag.”

On the positive side:• The markets are up more than 25 percent since the new government took office, and new investment

is up as investors give a favorable review to the initial responses of the new government.

• Import tariffs have been cut on oil, petrochemicals and steel, thereby reducing the drag on economic growth and inflation.

• Tax on long-term capital gains has been abolished and the levy on the short-term tax has been reduced.

• Taxes at the state level are being simplified with the gradual introduction of the value-added tax.

• Federal funding for India’s 29 states has been tied to fiscal responsibility and is expected to reign in government spending which continues to be an issue for many states.

On the negative side:• States are being asked to revise labor laws in a way that is likely to impact the competitive positioning

of Export Oriented Units (EOUs) operating out of the Special Economic zones – a concern because EOUs have been providing the growth in export earnings that the country critically needs.

• Various subsidy-generating initiatives that can hinder free market growth may be reinstated, such as employment guarantee programs with noncash-related payments for services; also, the state government in Andra Pradesh has restored free electricity for farmers.

• The left-leaning allies continue to resist privatization efforts and liberalization of the rules governing the labor markets.

Indian banking opportuntiies IBM Business Consulting Services4

Booming businesses: Services, agriculture and manufacturing Domestic industries have prospered from the development of India’s capital markets and the increased foreign trade and investment across sectors. The rapidly-expanding services sector (including telecommunications and information technology), has benefited from government spending and explosive demand for IT and IT-enabled services (ITES), such as call centers and back-office administration.11 Agriculture and core industries (such as steel, cement and automobiles) are expected to remain strong over time because of affordable consumer credit and the robust economy. Even newer industries, such as pharmaceuticals, have flourished in recent years. According to the Organization of Pharmaceutical Producers of India, India has the largest number of U.S. FDA-approved manufacturing facilities outside the U.S., and it reports 2003 pharmaceutical exports of Rs. 141 billion,12 or approximately US$3.1 billion.

Other areas of the Manufacturing sector are also thriving and attracting big global players:

• Surging domestic car sales are boosting auto production (up 30 percent)13

• Toyota Motor Co. has begun exporting 150,000 transmissions to other Toyota plants14

• Bharat Forge, an Indian company, will export more than 40 percent of its production to companies such as Daimler Chrysler and Cummins Engine Co.15

• Korea’s LG is starting a new factory for exporting televisions and refrigerators

• Finland’s Elcoteq Network will begin assembling cell phones for companies such as Nokia

• Ericsson is manufacturing radio transmitters and receivers in Bangalore.

Overall, investments in automobiles, automobile components, machine engineering, textiles and pharmaceutical sectors are up 8.2 percent this year, indicating strong investor confidence.16

Infrastructure spending is expected to be very strong – fueled by big ticket projects involving national highway systems, establishment of privatized airports, and the modernization of ports and telecommunication networks. An estimated US$440 billion is expected to be spent in public and private projects over the next five years.

Gurgaon: Trying to develop

infrastructure on pace with

skyrocketing growth

India’s rapid growth trajectory

has left many “boomtowns” with

markedly inadequate infrastructure

systems. One of these boomtowns

is the New Delhi suburb Gurgaon.

Thanks to the explosion of India’s

outsourcing industry, multinational

companies have continued to move

to Gurgaon to escape the congestion

of New Delhi. The city’s popula-

tion shot up from 37,868 in 1961

to 1.7 million in 2001. As a result,

the existing power, water and road

infrastructure is struggling to keep

up, with plans already underway to

upgrade systems in each of these

important areas.19

Indian banking opportuntiies IBM Business Consulting Services5

A growing labor force: English-speaking with IT savvyGlobal investors are attracted to India because of the growing number of well-educated, English-speaking workers who are comfortable working in information technology. India’s IT workforce will be augmented by a booming population of engineering students. The number of engineering students admitted at the university level rose in 2004 to 341,649 from 310,590 in 2003.17 Furthermore, India’s labor pool also serves as an expanding customer base for retail bank products and services.

The emerging middle class: Managing "new money" The development of India’s economy is boosting overall consumer purchasing power. The percentage of middle- to high-income Indian households is expected to continue rising. The younger, more educated population not only wields increasing purchasing power, but it is more comfortable than previous generations with acquiring personal debt.

The diversity within IndiaIndia possesses a rich diversity of wealth, culture and language across its many states and regions. The states of Punjab and Maharashtra are the country’s wealthiest, followed by Gujarat and West Bengal.18 While Delhi, Mumbai, Chennai and Kolkatta are the largest metropolitan cities, Bangalore, Hyderabad and Pune are experiencing double-digit growth rates, fueled in large part by the booming ITES sector. English is prevalent among the urban population, but Hindi is the "national language" for millions. In rural areas,

regional languages still hold sway.

The continuing growth forecasted for India makes it an attractive opportunity over the medium- to long-term horizon. Yet, this growth is arising from a relatively low base, and India is still a developing market. Global banks assessing the attractiveness of the Indian opportunity must consider that the country’s infrastructure – including the availability and reliability of telecommunications – is still in "catch-up" mode.

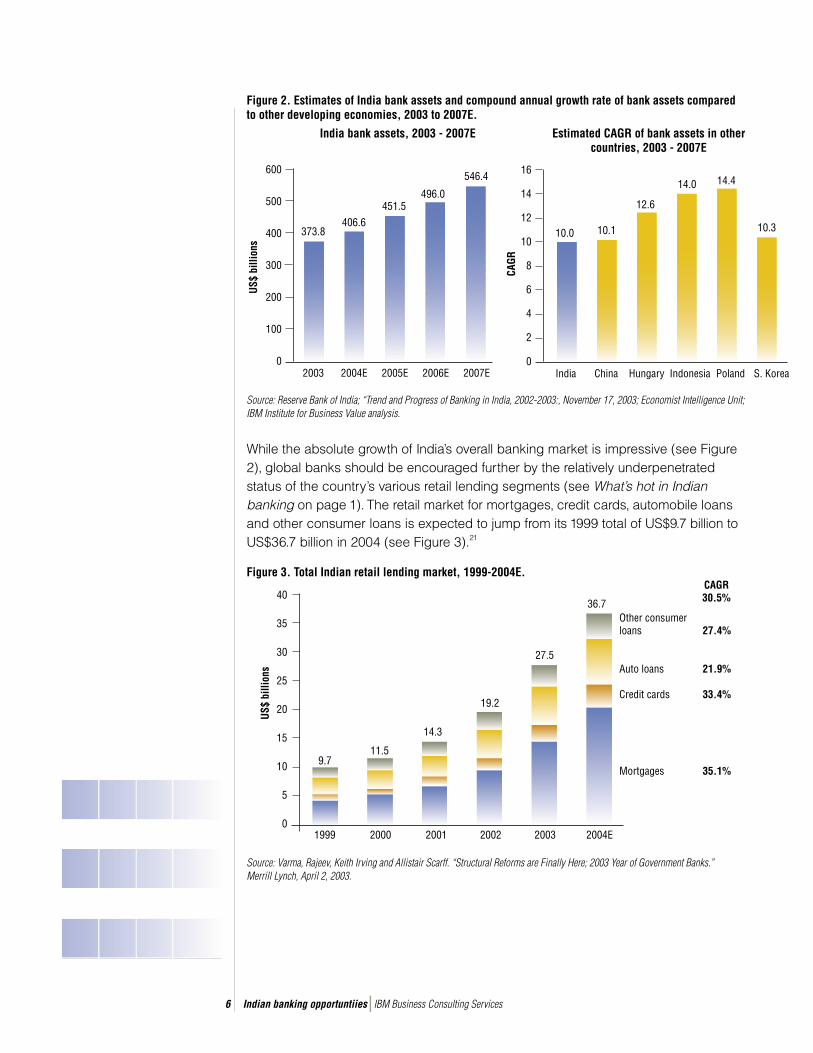

A view of India’s banking industry India’s banking industry is one of the major beneficiaries of the country’s ascendant economic power. Improving consumer purchasing power, coupled with more liberal attitudes toward personal debt, is fueling India’s explosive banking segment. Bank asset growth between 1998 and 2003 places India favorably among a sampling of the developing economies in China, Hungary, Indonesia, Poland and South Korea. For the period, total bank assets in India rose from US$187.2 billion to US$373.8 billion, a 14.8 percent CAGR.20 Even though the brisk rate of growth in the Indian banking sector is expected to level off, it should remain solid through 2007 (see Figure 2).

Indian banking opportuntiies IBM Business Consulting Services6

Figure 2. Estimates of India bank assets and compound annual growth rate of bank assets compared to other developing economies, 2003 to 2007E.

While the absolute growth of India’s overall banking market is impressive (see Figure 2), global banks should be encouraged further by the relatively underpenetrated status of the country’s various retail lending segments (see What’s hot in Indian banking on page 1). The retail market for mortgages, credit cards, automobile loans and other consumer loans is expected to jump from its 1999 total of US$9.7 billion to US$36.7 billion in 2004 (see Figure 3).21

Figure 3. Total Indian retail lending market, 1999-2004E.

600

500

400

300

200

100

02003

US$

billi

ons

Source: Reserve Bank of India; “Trend and Progress of Banking in India, 2002-2003:, November 17, 2003; Economist Intelligence Unit; IBM Institute for Business Value analysis.

373.8406.6

451.5

2004E 2005E 2006E 2007E

India bank assets, 2003 - 2007E

496.0

546.4 16

14

12

10

8

6

4

2

0India

CAGR

10.0 10.1

12.6

China Hungary Indonesia Poland

14.0 14.4

Estimated CAGR of bank assets in other countries, 2003 - 2007E

S. Korea

10.3

40

35

30

25

20

15

10

5

01999

US$

billi

ons

Source: Varma, Rajeev, Keith Irving and Allistair Scarff. “Structural Reforms are Finally Here; 2003 Year of Government Banks.” Merrill Lynch, April 2, 2003.

9.7

2000 2001 2002 2003 2004E

11.5

14.3

19.2

27.5

36.7Other consumer loans 27.4%

Auto loans 21.9%

Credit cards 33.4%

Mortgages 35.1%

CAGR30.5%

Indian banking opportuntiies IBM Business Consulting Services7

Even with this strong performance, significant opportunities for continued retail lending growth remain. Evidence suggests that India’s traditionally fiscally conservative consumers are becoming more receptive toward holding debt. The forecasted total debt of US$36.7 billion in 2004 represents just 5.8 percent of India’s expected GDP, up from 2.2 percent in 1999.22 Still, these retail lending figures lag India’s regional peers. Taking another view, India’s consumer borrowing represented just 2 percent of household income in 2002, sharply less than the totals of Singapore (176 percent), Malaysia (75 percent) and Thailand (39 percent).23

Unlike most rapidly expanding, emerging markets, India’s banking sector has exhibited financial stability and a trend toward improved governance under the management of its central bank, the Reserve Bank of India (RBI). One challenge the RBI had to contend with was the legacy of policy-directed, corporate lending by the state-owned banks that had produced high levels of nonperforming assets (NPAs). Through structural reform, remedial legislative actions, and favorable returns from the fixed income Treasury Markets, Indian banks have cut gross NPA levels from 15.7 percent in 1997 to 8.8 percent in 2003.24 Fortunately, new entrants to the market are not subjected to the same mandatory lending requirements as domestic banks and can therefore "cherry-pick" the most desirable clients, allowing them to lower their own risk of NPAs through more rigorous risk management strategies.

For its study, IBM used the RBI classification of Indian banks to examine the relative performance of each commercial banking group (see Figure 4).

Figure 4. Commercial banking groups: Two public and three private sector groups.

• India’s government took over ownership of the Imperial Bank of India in 1955 and reconstituted it as the State Bank of India (SBI) under the State Bank of India Act

• Seven state banks taken over by the SBI under The State Bank of India (Subsidiary Banks) Act in 1959

• Scheduled commercial banks that were nationalized in two phases – 1969 and 1980

• Nationalized banks are wholly-owned by the government, though some have made public issues

• The Reserve Bank of India (RBI) granted fresh bank licenses in 1993• Private banks (many community banks) that had been in existence and

spared the nationalization policies since 1969

• Nine privately-held institutions that were granted banking licenses by the RBI in 1993

• The RBI prescribed a new minimum capital requirement (Rs 100 crores)B for banks to be considered for a license

•` Foreign fi nancial institutions that have established banking operations in India

• State Bank of India• State Bank of Hyderabad• State Bank of Indore

• Bank of India• Canara Bank• Corporation Bank

• SBI Commercial and Int’l.• Karnataka Bank Ltd.• Karur Vysya Bank Ltd.

• ICICI Bank Ltd.• IDBI Bank Ltd.• UTI Bank Ltd.

• Citibank• Credit Lyonnais• Standard Chartered

State bank group

Nationalized bank group

Old private bank group

New private bank group

Foreign bank group

Note: (A) List of bank group categories above does not include cooperative banks. (B) Rs = Indian rupees, one crore = 10 million.Source: IBM Business Consulting Services; Dubey, Suman.“India’s Banking Industry Prepares for Nine New Private Institutions.” Wall Street Journal, June 1, 2003; Kumbhakar, Subal C. and Subrata Sarkar. “Deregulation, ownership and productivity growth in the banking industry: Evidence from India.” Journal of Money, Credit and Banking, March 18, 1994.

DescriptionA Examples

Publ

ic s

ecto

r ban

ksPr

ivat

e se

ctor

ban

ks

Indian banking opportuntiies IBM Business Consulting Services8

Global banks in India: Gaining a footholdThe competitive environment in India presents both challenges and opportunities to global banks seeking market entry. Entrenched domestic competitors and restrictive equity ownership ceilings imposed by the government create obstacles for banks establishing a foothold in India. Primary challenges include tough competition and government ceilings on foreign equity ownership. Opportunities exist because global banks often have technological advantages, well-honed, efficient processes and appealing products and services.

The strongest competition facing global banks in India comes primarily from the public sector (the State Bank and Nationalized Bank groups) and the New Private Bank groups. State dominance of the banking sector dates back to the inception of the RBI in 1935. When the RBI commenced operations, the state controlled 100 percent of the banking institutions. Since the 1990’s, India’s reform-driven policies have promoted the gradual deregulation and modernization of the banking sector. The formation of the Old Private Bank group and then the New Private bank group opened the marketplace to greater competition. Gradually, the grip of public sector banks has loosened, as evidenced by that group’s drop in total asset share, from 89.1 percent in 1990 to 75.7 percent in 2003.25

However, state-backed institutions remain formidable, possessing expansive channel reach and huge customer bases, controlling not only three-quarters of total assets, but also three-quarters of income.26 In 2003, the Foreign Bank group controlled less than seven percent of total industry assets and less than nine percent of total income (see Figure 5).27

Figure 5. Total assets and total income by banking groups in India, 2003.

Public sector banks (state-owned)Private sector banksForeign banks

Nationalized bank group 46.9%

Foreign bank group 8.9%

Old private bank group 6.3%

New private bank group 10.5%

State bank group 27.5%

Nationalized bank group 46.6%

Foreign bank group 6.9%

Old private bank group 6.2%

New private bank group 11.3%

State bank group 29.1%

Note:*Total income - The sum of net interest income (interest income – interest expense) and non-interest income (designated “other income” by the RBI).Source: Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003.

Total assets by banking group (FY2003)Total assets: US$373.8 billion

Total income* by banking group (FY2003)Total income: US$17.3 billion

Indian banking opportuntiies IBM Business Consulting Services9

The other key competitors for global banks are the banks of the New Private Bank group – this set of institutions has proven more nimble than other domestic players. Since its formation in the 1990s, this group leveraged its strong domestic branding and above-average operational capabilities to aggressively win market share from state-backed incumbents. From 1998 to 2003, the New Private Banks had a 47.4 percent CAGR in total assets, compared to 14.7 percent CAGR for the State Bank group and 12.2 percent CAGR for Nationalized Banks.28

Asset and income market share in 2003 remained highly concentrated among top banking institutions. The top 15 banks operating in India controlled 67.7 percent of total assets – only two are not public sector banks. A slightly different top 15 group controlled 65.7 percent of total income in 2003 – of this group, 12 are public sector banks.29

Many domestic banks are ill-equipped to compete with global banks from an operational perspective. Faced with this concentrated and entrenched competitive landscape, global banks in India have achieved mixed results during the last five years. On the “plus side,” global banks have improved margins by focusing on cost, customer service and better risk management – with employee productivity and profitability metrics that outperform other banking groups.30 These banks have achieved higher margins from leveraging technology, as well as efficient, standardized processes. Global banks’ strong brand cache often allows them to justify premium pricing strategies relative to their domestic competitors, further cushioning margins. Profitability per employee for the Foreign Bank group reached US$32,375 in 2003, and the New Private Bank group held a distant second place with US$8514 for the same measure (see Figure 6).31

Figure 6. Productivity and profitability performance by banking group, 2003.

2,000,000

1,600,000

1,200,000

8,000,000

4,000,000

0Nationalized

banks

Busi

ness

per

em

ploy

ee*

(US$

)

State group banks

Old private banks

New private banks

Foreign banks

Note: *Business per employee - Advances plus deposits per bank employee.Source: Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003.

Business per employeeProfi tability per employee

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

9.8

Profitability per employee (US$)

Indian banking opportuntiies IBM Business Consulting Services10

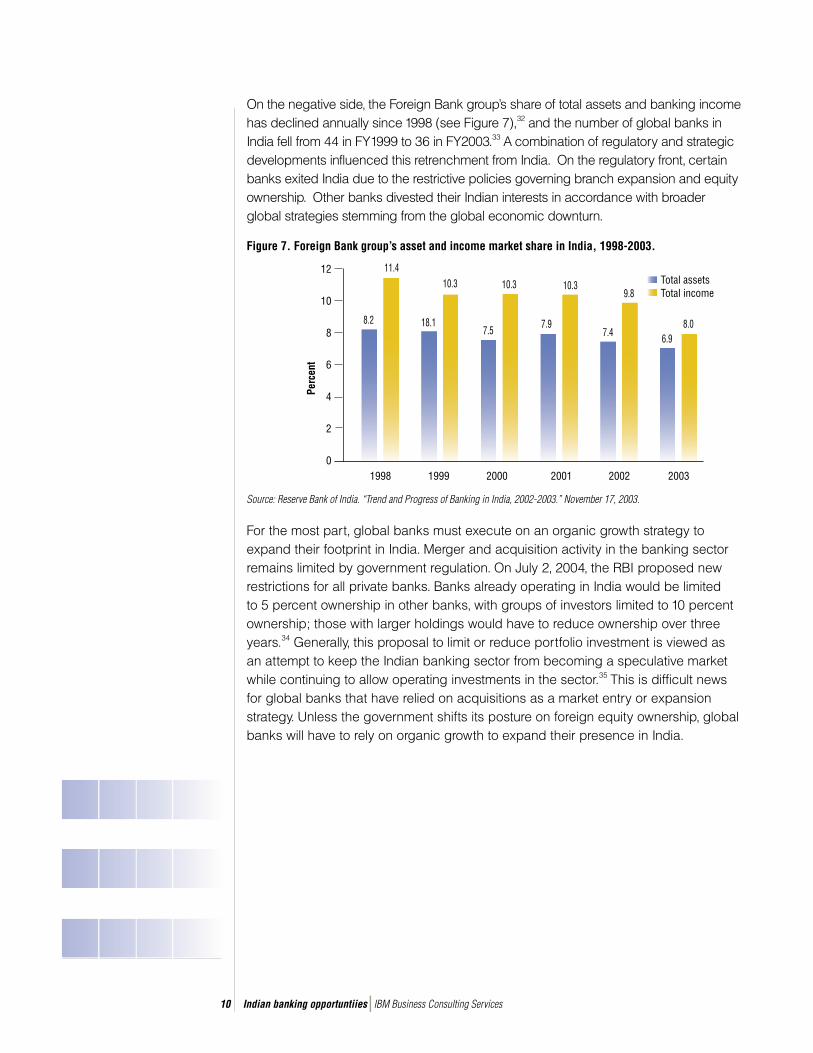

On the negative side, the Foreign Bank group’s share of total assets and banking income has declined annually since 1998 (see Figure 7),32 and the number of global banks in India fell from 44 in FY1999 to 36 in FY2003.33 A combination of regulatory and strategic developments influenced this retrenchment from India. On the regulatory front, certain banks exited India due to the restrictive policies governing branch expansion and equity ownership. Other banks divested their Indian interests in accordance with broader global strategies stemming from the global economic downturn.

Figure 7. Foreign Bank group’s asset and income market share in India, 1998-2003.

For the most part, global banks must execute on an organic growth strategy to expand their footprint in India. Merger and acquisition activity in the banking sector remains limited by government regulation. On July 2, 2004, the RBI proposed new restrictions for all private banks. Banks already operating in India would be limited to 5 percent ownership in other banks, with groups of investors limited to 10 percent ownership; those with larger holdings would have to reduce ownership over three years.34 Generally, this proposal to limit or reduce portfolio investment is viewed as an attempt to keep the Indian banking sector from becoming a speculative market while continuing to allow operating investments in the sector.35 This is difficult news for global banks that have relied on acquisitions as a market entry or expansion strategy. Unless the government shifts its posture on foreign equity ownership, global banks will have to rely on organic growth to expand their presence in India.

12

10

8

6

4

2

01998

Perc

ent

8.2

11.4

1999 2000 2001

6.98.0

7.4

9.8

7.9

10.3

7.5

10.3

18.1

10.3

2002 2003

Source: Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003.

Total assetsTotal income

Indian banking opportuntiies IBM Business Consulting Services11

ABN AMRO: Honing in on retail banking possibilities in India ABN AMRO traces its heritage in India to 1922, when it launched its operation focusing on small businesses and diamond traders. Eighty years later, the bank operates 12 branches in 9 cities with a broader strategic focus than its initial charter.36 Since acquiring Bank of America’s Indian retail operations in 2001, ABN AMRO has pursued several strategies to succeed in India’s retail banking market:• To avoid growth limitations placed on foreign banks, ABN AMRO applied in May 2004 to the RBI for

reclassification as a private sector bank – the first foreign bank to do so.37 If approved, the bank plans to convert its India branch network to a locally incorporated, wholly-owned subsidiary.

• To leverage small business contacts into full-service retail, it hopes to open more branches throughout the country

• To become a full-service bank across India, in 2000 it began to replace legacy systems with new technology enabling integrated, 24x7 multichannel banking.

• To herald its entry into the investment banking business in India, ABN AMRO announced four upcoming IPOs in 2004.38

• To give customers convenient access to banking functions, ABN AMRO enhanced its channels to include use of the Short Message Service (SMS) capability of cell phones, branches that are open 365 days per year and even Internet access through “bank-cafés” with free coffee

• To gain cost savings, the Dutch holding company of ABN AMRO plans to outsource some parts of its global back office and IT departments to India.

Identifying high-potential retail entry points Given the myriad challenges awaiting global banks in India, the IBM Institute for Business Value conducted research to prioritize the optimal market entry points for banks evaluating an India strategy. From the full scope of banking and financial markets products, the team used primary and secondary research to narrow the list to eight high-priority product areas: housing loans, vehicle loans, small and medium enterprise (SME) banking, personal financial services (PFS), card products, student lending, retail brokerage and mutual funds. Next, these eight product areas were assessed using a strategic framework that evaluated the various aspects of opportunity size and attractiveness, as well as any barriers to entry (see Assessment Methodology).

Indian banking opportuntiies IBM Business Consulting Services12

Assessment methodologySize and attractiveness:• Market potential – What is the present and future overall size of the opportunity? • Profitability potential – What are the present levels of profit margin and what are the future expectations

for profitability?• Customer dynamics – What is the level of demand for this product and what customer-level

developments may suggest the magnitude of this opportunity?Barriers to entry: • Competitive intensity – To what extent will the competitive environment in this space enable or

limit success?• Product sophistication – To what extent are the attributes of the product aligned with user demand? • Infrastructure requirements – To what extent will major infrastructure enhancements be required to fully

support this opportunity?

The IBM team further narrowed the field by ranking each opportunity based upon the score it generated from the framework. As a result, the four retail banking oppor-tunities deemed the most attractive are two types of credit products: housing loans and vehicle loans; and two types of full-service offerings: SME banking and PFS (see Figure 8).

Figure 8. Retail financial services opportunity assessment.

More barriers Fewer barriersBarriers to entry

Less

attr

activ

eM

ore

attra

ctiv

e

Size

and

attr

activ

enes

s

Housing loans

Retail brokerage

Student lending

Small and medium enterprise banking

Personal fi nancial services

Mutual funds

Vehicle loans

Card products

Source: IBM Institute for Business Value analysis.

Indian banking opportuntiies IBM Business Consulting Services13

Credit products: Housing and vehicle loansHousing loansWith the development of a middle class, the number of households able to afford a mortgage continues to show rapid, sustainable growth (see Figure 9). Not only do more and more people want to buy houses, but they are more willing to assume debt for that purpose. The government’s encouragement of housing construction and the RBI’s stimulation of the housing loan market further bolster this opportunity.

Figure 9. Growth in the number of households in India that can afford a mortgage, 1995-2003E.

Despite greater mortgage affordability, penetration of the mortgage loan market is relatively low, creating a natural entry point. Relatively simple housing loan products expose incumbents to new market entrants that can offer differential pricing, broader loan eligibility requirements and even more sophisticated products as the market develops. Though still a highly concentrated market, other banks (including global banks) with cheaper sources of funding are increasingly taking share from the incumbent Housing Finance Corporations (HFCs), the traditional source of mortgage funding. The market share of HFCs is expected to drop from 60 percent of percentage of outstanding loans value in 1999 to 34 percent in 2005.40

Current market projections forecast robust growth. India’s housing market is expected to grow between 30 and 45 percent by 2008 to a total value between US$45 billion and US$77 billion, with opportunity concentrated primarily in metro-politan and urban regions.41 Even though margins are under pressure – partly as

CRISIL, Ltd. stated in 2003

that “a 40 percent growth

rate in the retail (finance)

portfolio is sustainable over

the next five years without

altering the risk profile of

creditworthy households.”39

25

20

15

10

5

01995

Mill

ions

of u

rban

hou

seho

lds

2.6

1996 1997 1998

10.8

8.06.0

4.53.0

1999 2000

Note: Household = 5.2 people.Source: ICICI, August 31 2003; Statistical Outline of India by Tata Services via Merrill Lynch, April 2, 2003.

2001 2002 2003E

12.5

16.0

20.5

1995 - 2003E CAGR 29.4%

Indian banking opportuntiies IBM Business Consulting Services14

a result of the relatively small credit spread of 1 to 1.25 percent (compared to a 3 percent spread in the U.S.) – housing loans are expected to remain a profitable pick for market entry because of growth potential.

Vehicle loansThe prosperity of recent years has produced strong demand for automobiles. Though estimates of the size and growth vary, all outlooks remain positive. In fact, increasing demand for mobility is fueling sustainable growth in target markets for all classes of vehicle loans: commercial vehicles, cars and two-wheelers (see Figure 10).

Figure 10. Estimated growth in vehicle financing in India, 2001-2007E.

With rising levels of customer purchasing power, initial car sales volumes were expected to grow from 570,000 to over 950,000 between fiscal years 2001 and 2007.42 However, by October 2004, car sales volume touched the one million mark. We believe that strong double-digit growth will continue over the next 2 to 3 years, tapering to single-digit growth thereafter. Significant investments in the development of national highway systems, lowering of tariffs on petroleum-related products and a robust economy will make this possible. Year-over-year growth from 2001 to 2002 was just 0.7 percent, but rose sharply to 16.2 percent between 2002 and 2003, with an increase of more than 50 percent in 2004.43

Low, stable interest rates,

rising disposable wealth levels

and falling vehicle prices have

supported the development of

the vehicle loan market.20

18

16

14

12

10

8

6

4

2

02001

US$

billi

ons

2002 2003 2004E 2005E 2006E 2007E

Estimate 1

Estimate 2

Estimate 3

Commercial vehicles

Two wheelers

Cars

1, 2, 3 = Three independent estimates of total market size and growth, with 2 showing the split between commercial vehicles, two wheelers and cars

Source: Agarwal, Mudit and Deepak Mittal. “The Consumer Financing Business in India - Building Blocks for the Future.” Dhan. January 23, 2004.

Indian banking opportuntiies IBM Business Consulting Services15

Profit margins on loans for both cars and two-wheelers are attractive, averaging 3.1 percent profit before tax (PBT) for car loans and 4.6 percent PBT for two-wheelers in 2003.44 Though increased competition may compress margins, rapid market growth is expected to mitigate this risk and prevent unrestrained price wars.

The vehicle loan market is more fragmented than the housing loan market. More banks offer automobile loans, and demand for two-wheelers at the low end of the auto market has attracted considerable competition. Competition in the auto loan space ranges from the captive financing units of auto manufacturers to public and private sector banks. As competition intensifies, auto manufacturers, dealers and financing companies are forging alliances to offer more attractive financing terms. More innovative products are beginning to appear on the market, such as longer loan terms and new payment, leasing and refinancing options. Furthermore, more efficient processing cycles are also improving the automotive loan product on the back end: steadily reducing the requirements and the time necessary for loan application processing.

Challenges associated with offering credit productsOverall, banks entering the housing and vehicle loan markets should expect to operate in an improving, but still risky, environment. The key challenges to consider include:

• Limited credit default data. Similar to other developing countries, some Indian banks informally share consumer credit data. The country lacks a centralized repository of consumer credit information found in most developed markets. Banks that have other retail operations in India may be able to leverage those databases to support retail loan businesses; having access to comprehensive credit data repositories would be a distinct advantage.

• Rudimentary risk management systems and processes. Banks in India lack the basic risk management infrastructure that is standard in many developed banking markets. Global banks entering India can wield comparative advantage by lever-aging their existing risk management systems and best practices processes.

• Nascent state of market. Housing and vehicle loans are only beginning to reach the urban mass market’s reach, necessitating a bank-led education campaign to help market these credit products. The majority of Indian consumers are not accustomed to purchasing on credit. Enterprising competitors will gain an advantage by educating consumers on the risks and rewards of loan products, simultaneously enhancing their brand identity.

Indian banking opportuntiies IBM Business Consulting Services16

• Immature secondary market. While housing and vehicle loans are beginning to be securitized and sold off to other companies, this practice is relatively new in India. Banks entering the housing market may be able to participate in the primary and secondary markets. Further development of the mortgage-backed securities market can help diminish banks’ overall risk of holding retail debt.

Full-service offerings: Small and medium enterprise banking and personal financial services Small and medium enterprise (SME) bankingRepresenting 95 percent of India’s industrial enterprises,45 SMEs comprise a critical sector of the Indian economy on the basis of employment and GDP contribution; they represent a growing, but underserved market (see Figure 11). Based on experiences in other countries, the SME segment offers an attractive risk/return trade-off.

Figure 11 - Composition of non-food gross bank credit, FY2001–FY2003.

India’s SME market

accounts for a significant

portion of economic

activity, representing: 40

percent of value-add in the

manufacturing sector, 34

percent of national exports

and 7 percent of GDP

according to official figures,

though some estimates put

SME at a level as high as 50

percent of GDP.46

1400

1200

1000

800

600

400

200

02001

US$

mill

ions

Note: SIDBI – Small Industries Development Bank. Priority Small Scale Industries (SSI) are a category of businesses recognized by the RBI with special lending and reporting requirements.Source: The Reserve Bank of India. “Trend and Progress of Banking in India 2003.” Appendix III., Table 5: Sectoral Deployment of Gross Bank Credit.

2002 2003

Other

Trade

Medium and large industry

Priority - other

Priority - SSI

Indian banking opportuntiies IBM Business Consulting Services17

In fiscal year 2003, the Small Industries Development Bank of India (SIDBI) disbursed a total of US$23.8 million to SMEs for: refinancing (US$17.7 million), support agencies (US$2.3 million), project finance (US$2.1 million) and bills (US$1.7 million).47 Because the Indian government and the RBI now consider SMEs to be a priority sector, public banks dominate lending to this segment, with more than 80 percent of the SME market in 2003.48 In recognition of growing SME needs, the government has launched a number of measures to improve the credit flow in this direction, including:

• Encouraging banks to open specialized SME branches within each district and SME cluster

• Loosening collateral security requirements

• Offering reduced financing rates for funding technology development

• Providing capital subsidies on technology upgrades.49

Based on the situation in other countries, SMEs typically demonstrate significant revenue and profit performance, accounting for about 30 percent of total bank profitability and generating above average market returns; in the U.S., for example, returns on SME banking services range from 20 to 40 percent.50 We expect the SME segment to represent a similar opportunity over time in India.

The financial needs of small businesses in India are presently relatively unsophisti-cated but further development of the SME market in India should naturally lead to demand for a full range of financial products. According to an ICICI survey, the top four products used by India SME respondents are savings (81 percent), pay orders (72 percent), telephone funds transfer (58 percent) and term loans (49 percent).51 In comparison, SME respondents in the U.S. rely most heavily on checking (89 percent), credit cards (75 percent), insurance (70 percent) and credit line (58 percent).52

Challenges associated with entering the SME banking marketIn delivering a full-service SME offering, banks face challenges similar to those for other retail banking products:

• Limited credit default data. As with retail lending, India lacks a comprehensive, centralized credit bureau with years of default history to support lending decisions. Enterprising banks may convert this risk into an opportunity by collecting and analyzing credit data on SMEs and cross-referencing that data with information about high net worth (HNW) individuals, which often comprise a similar target segment.

Indian banking opportuntiies IBM Business Consulting Services18

• Lack of established channels to the SME segment. SMEs can be difficult and costly to serve, since many will leverage existing relationships with banks where they already possess retail accounts. To target and profitably serve the SME seg-ment within their own spheres of influence, strategies are likely to include the development of unique product bundles and availability of multichannel access.

• Need for comprehensive financial coverage. As they grow, small businesses gen-erally seek a broad range of financial products, from short-term working capital needs to longer-term lending products. Offering a complete line of financial ser-vice offerings can allow banks to act as partners to SMEs.

Personal financial services (PFS)As the economy continues to grow, the stage is set for very rapid growth in household financial assets. Though the target market of high net worth (HNW) individuals is relatively small, rising levels of household assets and customer sophis-tication are creating a more viable niche market for PFS (see Figure 12).

Figure 12. International and Indian wealth pyramids.

The IBM Institute for Business Value framed the opportunity for PFS by considering assets under management (AUM). AUM in India jumped to US$30.3 billion in 2003, up 14.3 percent from the previous year.54 Global financial institutions have made significant headway into the India PFS market, as 37 percent of AUM is controlled by foreign joint ventures and private global banks.55

There are over 50,000

families in India with net

worth of US$1 million

and higher; only 30

percent of this market

has been captured by

global and private banks

and brokerages.53

International wealth pyramid Indian wealth pyramid

US$50 million

US$5 million

US$500,000

US$1 million

US$400,000

US$200,000Affl uent

High net worth

Very high net worth

Ultra high net worth

Affl uent

High net worth

Very high net worth

Ultra high net worth

Housing Development Finance Corporation, Ltd. (HDFC) claims 2000private banking customers with an average portfolio of US$300,000

Source: IBM Business Consulting Services. “Indian Wealth Management and Private Banking Survey,” 2003-04.

Indian banking opportuntiies IBM Business Consulting Services19

PFS profitability remains good, even though the eligibility criteria for customers are less stringent than in many other countries. In fact, key credit products show greater profitability than in the corporate market.56 In a typical large, private sector bank, we estimate that PFS can generate a profit before tax of approximately 35 percent of operating income, with cost-to-income ratios of about 65 to 70 percent.57

Further deregulation is expected to allow wealth diversification and the entry of more “new money” into the sector from new Indian bank customers achieving higher wealth levels. PFS offerings are becoming more comprehensive to help these customers diversify their holdings beyond basic, traditional banking products, shifting assets into income and money market funds. This creates new opportunities for banks that can establish the right combination of account management and distri-bution infrastructure. By 2006, Indian wealth management offerings are expected to include alternative investments such as hedge funds, real estate and other offerings like pension, family office, trust administration and charity.58

Challenges associated with entering the PFS banking market From the standpoint of timing an entry into the PFS market, challenges exist beyond the new systems and infrastructures that are needed for continued revenue generation and operational effectiveness:

Risk aversion of Indian customers. The repercussions of the mutual fund scandal of the 1990s are still evident. Many Indian retail customers averse to diversifying their asset base into higher risk classes. To account for this conservative tendency, PFS offerings can be tailored to emphasize the value of a lower-risk investing approach.

“New money” mass affluent customers are not accustomed to wealth management. Most customers are used to obtaining financial services on an as-needed basis without much regard to a full view of their financial well-being. As part of the opportunity to define and develop offerings for India’s emerging HNW population, customers may need an introduction to the concept of private banking (or wealth management).

Shortage of skilled personal financial advisors. To date, the PFS opportunity has been limited to a very small segment of the population, so domestic banks have not generally developed expertise in comprehensive personal financial management. Global banks can take advantage of this gap by leveraging advisory competencies that they have cultivated in other markets, importing that expertise into the Indian market.

Indian banking opportuntiies IBM Business Consulting Services20

Crafting an India-specific retail banking strategyAs global banks have experienced in the past, successfully competing in India requires substantially more consideration than merely choosing the right market to target. It warrants a well-crafted strategy that addresses the numerous risks and challenges specific to India’s developing economy. The IBM Institute for Business Value India banking study yielded several key recommendations to help global banks customize effective market entry strategies.

Prepare a long-term India strategyIndia (along with China) is a potential jewel of banking growth in the 21st century. Global banks seeking new venues for geographic expansion have to assess the benefits and risks of entering the Indian market. However, the global banks that ultimately succeed in India will be those who accept that the short term will be fraught with operational challenges and potential setbacks. The time horizon for the India opportunity must be set for the medium-to-long term. Senior managers must design strategies that establish an initial beachhead, from which banks gradually enhance their brand positioning, regional reach and offering line breadth.

Incorporate a strong educational message into marketing campaignsThe embryonic nature of the Indian retail banking market requires new entrants not only to devise marketing programs to establish and enhance brand, but also to address basic questions and concerns that may exist in the relatively unsophis-ticated banking segment, and the large “unbanked” group. Global banks entering India will confront retail consumers unaccustomed to making purchases on credit or with lingering aversions to more-risky investment products. Allaying these fears and overcoming uncertainty must be central tenets of banks’ marketing strategies.

Leverage operational efficiency advantages Global banks will face intense competition in India: from entrenched, state-owned institutions, to long-established private sector banks, to innovative, more recent arrivals. New market entrants face significant disadvantages in channel reach and brand recognition. Simply put, the odds of success are daunting. One of the areas where global banks possess a clear advantage over most domestic institutions is in terms of operational capabilities. Global banks typically maintain higher standards of productivity and profitability relative to their India peers, resulting in the need for fewer employees and branches to generate similar income levels. Consequently, entrants must leverage their best-in-class processes and systems to support back-office processing functions, as well as customer-facing activities. By focusing on operational excellence, global banks will implement a strong base to achieve future scale economies.

Indian banking opportuntiies IBM Business Consulting Services21

Transform operational expertise into insourcing playsLonger term, global banks can leverage their operational capabilities into new revenue streams by insourcing selected capabilities to other financial institutions. India’s development as a global business processing outsourcing hub has attracted major investments from global banks establishing a captive back-office presence in the country. Over time, these banks may parlay these captive businesses into revenue-generating insourcing businesses. With BPO offerings based in India moving “up market” – from call centers to data analytics; from accounts payable processing to financial reporting; and from loan origination to loan underwriting – the revenue upside of this opportunity is poised to explode.

Offer regional-level products and delivery to diverse customer base A critical part of developing a unique value proposition in India is the ability to customize products and delivery strategies by region. Far from being a homogeneous marketplace, India’s languages and cultural preferences vary widely across the nation, creating a collection of smaller, heterogeneous markets. Many global institutions have stumbled in India after failing to address its unique multi-regional requirements, such as hiring employees who are fluent in one or more regional languages. Currently, the most attractive, bankable population is located in what is known as Tier 1: the three, high-density “Golden Corridors” around New Delhi, Mumbai and Bangalore, and a cluster of smaller towns around these cities. Other metropolitan cities, such as Kolkatta and Chennai, are considered to be the next opportunity level, or Tier 2. Banks focusing on Tier 1 cities should prepare for intense competition or turn to Tier 2 cities, where growth exists, albeit at a slower pace. Through awareness of distinct customer needs, niche players – and those having monoline capabilities – can successfully roll out targeted products in underserved segments of the marketplace.

Manage operational risk by partnering with local banksThe present regulatory environment in India hampers an extensive growth-by-acquisition approach. While such restrictions may dissuade some banks from investing in India, innovative global institutions instead may circumvent these restrictions and reduce up-front investment costs. By striking alliances with established local banks, global banks can avoid significant one-time investments while positioning themselves for 2007 World Trade Organization requirements that are expected to further open the banking market. The majority of local banks are seeking both expertise and capital through alliances to improve their offering portfolios and delivery capabilities. For example, a manufacturer may enter India

Indian banking opportuntiies IBM Business Consulting Services22

by white labeling a mortgage product with an established domestic player. Other institutions with processing capabilities may assume a first mover role by allying with consortiums to create industry-standard back-office functions. A partnering strategy can provide new entrants with a deeper understanding of the nuances of the Indian banking sector, while helping to reduce operational risks ahead of Basel II. When considering partnering options, global banks should take precautions beforehand to protect both their intellectual capital and their company’s future ability to compete, should an unanticipated market exit be required.

In conclusion, the long-term banking growth opportunity in India cannot be missed by globally focused banks. The confluence of rapid economic development, elevated consumer purchasing power levels and an underserved retail banking population position India as a potential growth region for the 21st Century. However, India's banking history has also seen global banks failing to establish a profitable operation in the country. Success will truly lie in the details of execution.

To learn more about how to gain traction in the India banking market, please contact us at [email protected].

Indian banking opportuntiies IBM Business Consulting Services23

About the authorsSunny Banerjea is the Global Banking Leader in the IBM Institute for Business Value, Financial Services Sector. Sunny can be reached at [email protected].

Cormac Petit dit de la Roche is a Managing Consultant in the IBM Institute for Business Value, Financial Services Sector. Cormac can be reached at [email protected].

John Raposo is a Senior Consultant in the IBM Institute for Business Value, Financial Services Sector. John can be reached at [email protected].

ContributorsRavi Trivedy, Partner, Financial Services Sector, IBM Business Consulting Services

Daniel W. Latimore, Partner, Executive Director, Institute for Business Value

Anita Mehta-Iyer, Managing Consultant, Financial Services Sector, IBM Business Consulting Services

Ragna Bell, Associate Partner, Financial Services Sector, IBM Business Consulting Services

Dev SenGupta, Consultant, Financial Services Sector, IBM Business Consulting Services

About IBM Business Consulting ServicesWith consultants and professional staff in more than 160 countries globally, IBM Business Consulting Services provides clients with business process and industry expertise, a deep understanding of technology solutions that address specific industry issues, and the ability to design, build and run those solutions in a way that delivers bottom-line business value.

Indian banking opportuntiies IBM Business Consulting Services24

References • All Reserve Bank of India (RBI) data cited in this paper are based on the country's

fiscal year calendar, which runs from April 1 to March 31. All other data reflect calendar year-end totals.

• For this paper, conversion of Indian rupees (Rs.) to U.S. dollars was performed by using the conversion rate on December 31 for the applicable year, according to the conversion calendar at http://www.oanda.com/convert/fxhistory

1 Wilson, Dominic and Roopa Purushothaman. “Global Economics Paper No. 99: Dreaming with BRICS: The Path to 2050.” Goldman Sachs. October 1, 2003. Accessed on September 15, 2004. http://www.gs.com/insight/research/reports/report6.html

2 Rajpal, Amit, Sachin Sheth and Andrew Brown. “India Mortgages – The Next China?” Morgan Stanley. May 16, 2003; “World Development Indicators Database.” The World Bank Group. https://publications.worldbank.org/subscriptions/WDI

3 Varma, Rajeev, Keith Irving and Alistair Scarff. “Structural Reforms are Finally Here; 2003 Year of Government Banks.” Merrill Lynch. April 2, 2003.

4 Choudhury, Dipankar. “India Banking Sector: New Color of Money.” ICICI Securities Equity Research India. August 27, 2003.

5 Small Industries Development Organization (SIDO), Office of the Ministry of Small Scale Industries, Government of India. SIDO Online. Economic statistics 2002. http://www.smallindustryindia.com/ssiindia/statistics/economic.htm

6 IBM Business Consulting Services. Indian Wealth Management and Private Banking Survey, 2003-04; Merrill Lynch/Cap Gemini Ernst & Young. World Wealth Report 2003. http://www.nl.capgemini.com/resources/wwr2003-final.pdf

7 “Who Put the Shine in India?” The Economist. May 27, 2004. 8 “Economy grows by 7.4 pc in Q1.” The Hindu. September 30, 2004.9 “All Yours.” The Economist. July 17, 2003.10 Rangan, M. C. Govardhana and Shumjita Sharma. “India Privatization Gets a

Strong Foothold – Government’s Stake Sale in Six State-Owned Firms Will Raise $34.1 Billion.” Asian Wall Street Journal. March 16, 2004.

11 Country Briefing. “India Economy: Quick view – GDP growth accelerates.” Economist Intelligence Unit. January 5, 2004.

Indian banking opportuntiies IBM Business Consulting Services25

12 Indian Pharmaceutical Industry – Fact Sheet 2003. Organization of Pharmaceutical Producers of India. Accessed on August 31, 2004. http://www.indiaoppi.com/keystat.htm

13 Kripalani, Manjeet. “The Factories Are Humming”. BusinessWeek. October 18, 2004.

14 Ibid.15 Ibid.16 Ibid.17 Kumar, Shalabh. “How Sustainable is the Cost Advantage of Offshore

Outsourcing?” National Association of Software and Service Companies (NASSCOM). September 2003. Accessed on September 22, 2004. http://www.nasscom.org/download/Cost_Advantage.pdf

18 “Battle on the Home Front.” The Economist. February 19, 2004.19 Bailay, Rasul. “New Delhi Suburb Experiences Growth Pangs of Outsourcing.” The

Wall Street Journal. September 1, 2004.20 The Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.”

November 17, 2003. Accessed on September 29, 2004. http://www.rbi.org.in/index.dll/7?OpenSectionTextArea?fromdate=11/17/2003&todate=11/17/2003& s1secid=9&s2secid=0&ArchiveMode=1

21 Varma, Rajeev, Keith Irving and Alistair Scarff. “Structural Reforms are Finally Here; 2003 Year of Government Banks.” Merrill Lynch. April 2, 2003.

22 Varma, Rajeev, Keith Irving and Alistair Scarff. “Structural Reforms are Finally Here; 2003 Year of Government Banks.” Merrill Lynch. April 2, 2003; “World Development Indicators Database.” The World Bank Group. https://publications.worldbank.org/subscriptions/WDI

23 The Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003. Accessed on September 29, 2004. http://www.rbi.org.in/index.dll/7?OpenSectionTextArea?fromdate=11/17/2003&todate=11/17/2003& s1secid=9&s2secid=0&ArchiveMode=1

24 Ibid.25 Ibid.26 Ibid.27 Ibid.28 Ibid.

Indian banking opportuntiies IBM Business Consulting Services26

29 Business Standard, Banking Annual Year 2003. Accessed on September 16, 2004. http://www.business-standard.com/special/bankannual/2003/overview.htm; IBM Institute for Business Value analysis.

30 The Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003. Accessed on September 29, 2004. http://www.rbi.org.in/index.dll/7?OpenSectionTextArea?fromdate=11/17/2003&todate=11/17/2003&s1 secid=9&s2secid=0&ArchiveMode=1.; IBM Institute for Business Value analysis.

31 The Reserve Bank of India. “Trend and Progress of Banking in India, 2002-2003.” November 17, 2003. Accessed on September 29, 2004. http://www.rbi.org.in/index.dll/7?OpenSectionTextArea?fromdate=11/17/2003&todate=11/17/2003&s1 secid=9&s2secid=0&ArchiveMode=1

32 Ibid.33 Ibid.34 “Curious welcome,” The Economist. July 22, 2004. 35 “Curious welcome,” The Economist. July 22, 2004; IBM Institute for Business Value

analysis.36 About Us: ABN AMRO (India). Company Web site. Accessed on August 31, 2004.

http://www.abnamroindia.com/AboutUs/aboutus.html37 “ABN AMRO looks to RBI to convert branches into 100% arm.” The Economic

Times. Times News Network, May 22, 2004. Mumbai.38 “ABN AMRO forays into MFs.” The Economic Times. Times News Network, August

6, 2004. New Delhi.39 Ramakrishnan, G. “Retail finance: A safe bet for the next five years.” CRIS INFAC

(Research subsidiary of CRISIL Ltd.), 2003. Accessed on September 23, 2004. http://www.crisil.com/publications/insights/10RetailFinance.pdf

40 Varma, Rajeev, Keith Irving and Alistair Scarff. “Structural Reforms are Finally Here; 2003 Year of Government Banks.” Merrill Lynch. April 2, 2003.

41 IBM Institute for Business Value analysis; Ragpal, Amit, Sachin Sheth, Andrew Brown and Anil Agarwal. “India Mortgages – The Next China?” Morgan Stanley Equity Research. Asia/Pacific Industry: India Financial Services, Industry Overview. May 16th, 2003; Bhatt, Mayank. “Housing Finance From Primary Mortgage To Securitization In India.” Industry Canada Strategis. February 2003. Accessed summary on September 16, 2004. http://strategis.ic.gc.ca/epic/internet/inimr-ri.nsf/en/gr113421e.html

Indian banking opportuntiies IBM Business Consulting Services27

42 Choudhury, Dipankar. “India Banking Sector: New Color of Money.” ICICI Securities Equity Research India. August 27, 2003.

43 IBM Institute for Business Value analysis.44 Agarwal, Mudit and Deepak Mittal. “The Consumer Financing Business in India

– Building Blocks for the Future.” Dhan. Finance and Investments Club, Indian Institute of Management, Calcutta. January 23, 2004. Accessed on September 16, 2004. http://www.iimcal.ac.in/community/FinClub/dhan/dhan8/confin.pdf

45 Office of the Ministry of Small Scale Industries, Government of India. Annual Report 2003-2003.

46 Office of the Ministry of Small Scale Industries, Government of India, Annual Report 2002-2003; SIDO Online. Accessed on September 16, 2004. http://www.smallindustryindia.com/ssiindia/performance.htm; United Nations Conference on Trade and Development “Improving the Competitiveness of SMEs Through Enhancing Productive Capacity.” United Nations Commission on Enterprise, Business Facilitation and Development. Geneva, January 31, 2003. Accessed on September 16, 2004. http://www.unctad.org/en/docs//c3d51a1_en.pdf

47 Reserve Bank of India. Annual report: “Overview and Trends 2003.”48 Ibid.49 Office of the Ministry of Small Scale Industries, Government of India. Annual report

2003-2003.50 International Finance Corporation, Small and Medium Enterprise Department.

"What Works in SME Finance." 2002 SME Knowledge Base, The World Bank Group. Accessed on September 29, 2004. http://www2.ifc.org/sme/smeknowledge/html/body_strategy_development.html

51 “Overview of SME in India.” ICICI presentation to IFC Symposium on SME Finance in India, February 11, 2002. http://www.ficci.com/ficci/media-room/speeches-presentations/2002/Feb/13

52 Wendel, Charles. “Market Segmentation and Products Selection: A Practical Approach”, Financial Institutions Consulting. Presentation to IFC Symposium on SME Finance in India, February 11, 2002. http://www.ficci.com/ficci/media-room/speeches-presentations/2002/Feb/feb-sme-cwendel-market.ppt

Indian banking opportuntiies IBM Business Consulting Services28

53 IBM Business Consulting Services. Indian Wealth Management and Private Banking Survey, 2003-04; Merrill Lynch/Cap Gemini Ernst & Young. World Wealth Report 2003.

54 AMFI Update, quarterly newsletter of the Association of Mutual Funds in India, October-December 2003 Vol. III, Issue III. Accessed on September 16, 2004. http://www.amfiindia.com/OCT-DEC03.PDF

55 Ibid.56 IBM Institute for Business Value analysis; Agarwal, Mudit and Deepak Mittal. “The

Consumer Financing Business in India – Building Blocks for the Future.” Dhan. Finance and Investments Club, Indian Institute of Management, Calcutta. January 23, 2004. Accessed on September 16, 2004. http://www.iimcal.ac.in/community/FinClub/dhan/dhan8/confin.pdf; Choudhury, Dipankar. “India Banking Sector: New Color of Money.” ICICI Securities Equity Research India. August 27, 2003.

57 Choudhury, Dipankar. “India Banking Sector: New Color of Money.” ICICI Securities Equity Research India. August 27, 2003; HSBC Annual Report 2003. Accessed on September 29, 2004. http://www.hsbc.com/hsbc/investor_centre/financial-results/historic-results; IBM Institute for Business Value analysis.

58 IBM Business Consulting Services. Indian Wealth Management and Private Banking Survey, 2003-04.

© Copyright IBM Corporation 2004

IBM Global ServicesRoute 100Somers, NY 10589U.S.A.

Produced in the United States of America12-04All Rights Reserved

IBM and the IBM logo are registered trademarks of International Business Machines Corporation in the United States, other countries, or both.

Other company, product and service names may be trademarks or service marks of others.

References in this publication to IBM products and services do not imply that IBM intends to make them available in all countries in which IBM operates.

G510-3985-00