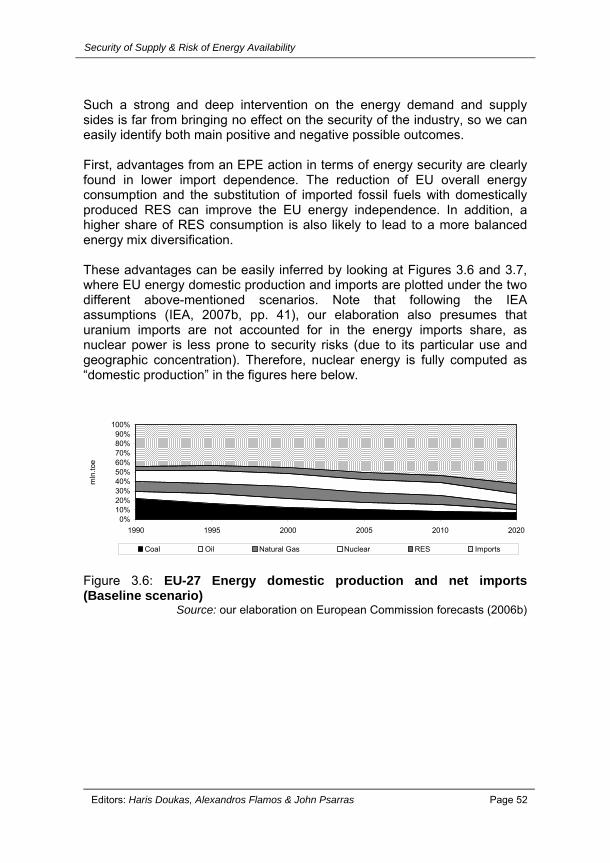

Security of Supply Risk of Energy Availability

121

Security of Supply & Risk of Energy Availability Based on the proceedings of the 1 st International Conference (1 st IC) of the FP7 project: “Risk of Energy Availability: Common Corridors for Europe Supply Security” (REACCESS)”, held in Turin, Italy on the 29 h of February 2008 Athens, June 2008

Transcript of Security of Supply Risk of Energy Availability

Security of Supply &

Risk of Energy Availability

Based on the proceedings of the

1st International Conference (1st IC) of the FP7 project:

“Risk of Energy Availability: Common Corridors for Europe Supply

Security” (REACCESS)”,

held in Turin, Italy on the 29h of February 2008

Athens, June 2008

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 2

The content of the book is based on the proceedings of the 1st International Conference (1st IC) of the FP7 project: “Risk of Energy Availability: Common Corridors for Europe Supply Security” (acronym: REACCESS) that was held in Turin, Italy on the 29h of February 2008. The REACCESS project aims to build tools suitable for EU27+ energy import scenario analyses, able to take into account at the same time the technical, economic and environmental aspects of the main energy corridors, for all energy commodities and infrastructures. The consortium partners of the FP7 project REACCESS are the following: • Politecnico di Torino, POLITO, Italy • Applied Systems Analyses, Technology and Research, Energy Models, ASATREM, Italy • Climate Change Coordination Center, CCCC, Kazakhstan • Centro de Investigaciones Energeticas, Medioambientales y Tecnologicas, CIEMAT, Spain • Deutsches Zentrum für Luft und Raumfahrt, German Aerospace Center, DLR, Germany • Kanlo Consultants, KANLO, France • Institute for the Economy in Transition, IET, Russia • Institute of Energy Technology, IFE, Norway • National Technical University of Athens, NTUA – EPU, Greece • Austrian Research Centres – Research Studios Austria, ARC, Austria • Fundacion General de la Universidad Nacional de Educaciòn a Distancia, F-UNED, Spain • Valtion Teknillinen Tutkimuskeskus , Technical Research Centre of Finland, VTT, Finland • University of Stuttgart, USTUTT, Germany • Institute of Methodologies For Environmental Analysis, CNR–IMAA, Italy

The editors would like to thank the project coordinator, Professor Evasio Lavagno and all members of the POLITO team for their excellent work in the organization and successful implementation of the 1st IC; the project officer Mr. Mathieu GRISEL for his fruitful participation and comments; The speakers for their keynote presentations and all the participants for their observations that facilitated the fruitful dialogue. Finally the editors would like to thank Mr. Kourlimpinis for designing the book cover. The editors would like to acknowledge the support from the European Commission (EC) who is financing the FP7 project REACCESS – Grant agreement no. 212011 and the project 05AKMΩΝ95 of Institute of Communication & Computer Systems (ICCS) for financing the publishing costs. 05AKMΩΝ95 is co funded by the European Union - ERDF (70%) and the Greek National Resources (30%) within the framework of Measure 4.2 of the Operation Programme "Competitiveness" of the 3rd CSF. The content of this book is the sole responsibility of its authors and editors and does not necessarily reflect the views of the EC. The authors of the chapters and the editors reserve the copyright of their work. No part of this publication or the information contained herein may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, by photocopying, recording or otherwise, without written prior permission from the authors. Published by: Bookstars-Gioggaras Elaion 34, 14564 N.Kifissia www.bookstars.gr Tel: +302108072643 ISBN: 978-960-6815-04-1

FOREWORD Demand for energy never ceases. There are no doubts that the European Union will continue to remain strongly dependent on imports and that will be more and more dependent in the future. Apart from the European strong dependence issue, another relevant issue involves the reliability of the infrastructures (for extraction, primary processing and transport to EU), as far as likely accidents and terrorist attacks are concerned. In addition to the import of primary sources, also the import of electricity will be relevant as many new interconnections are at several stages (identification, planning, development, implementation, etc.). Moreover, the concern related to the availability and the reliability of these supplies is associated with the burdens and the environmental impacts that such large and complex infrastructures have on the territories involved, outside as well as inside Europe. The Paper on “International relations and security of energy supply: risks to continuity and geopolitical risks” recently published by the Policy Department of the Directorate General External Policies of the Union states that “if Europe is to pursue a single, coordinated and efficient energy policy, a comprehensive policy framework will have to be designed as a tool for the energy sector to take up the challenges of employment generating economic growth, minimize dependence on external supplies and – at the same time – meet environmental targets, e.g. under the Kyoto Protocol”. In order to ensure, to the extent that is possible, a secure energy market, makes essential to adopt and understand that International co-operation on energy security is a win-win outcome for all countries involved. To achieve this means moving away from the traditional perception that energy is a national security issue – it is a European security issue. Energy security may, also, have a price – political and economic. But one must be sure that the cost of energy security will be small compared with the alternatives – economic instability and geopolitical tension. This book contains the proceedings of the 1st International Conference on the “Risk of Energy Availability: Common Corridors for Europe Supply Security – REACCESS” project, held in Turin, Italy on the 29th of February 2008. As a project co-ordinator of this project I do hope that this book will contribute to realizing the necessity of further investigation of all the parameters affecting the smooth and uninterrupted energy supply to Europe, as well as, to identifying the alternative practices & policies, striving towards a more sustainable energy future.

Professor Evasio Lavagno

Politechnico di Torino (POLITO), Turin, Italy 19 May 2008

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 4

EDITORIAL

On 29th February 2008, the Politecnico di Torino organized the 1st International Conference on the “Risk of Energy Availability: Common Corridors for Europe Supply Security” in Turin. The main purpose of the Conference was to stimulate a free exchange of thought among academics, practitioners and policy makers on the key issue of security of supply and risk of energy availability. In this book, seven selected articles presented during the Conference plus one article giving an exploratory analysis of energy availability risks are brought together. Each illuminates one or more of the critical issues in security of supply policy and research. The first chapter is written by Paul Isbell & Federico Steinberg from the Elcano Royal Institute for International and Strategic Studies. They analyse main strategic dilemmas in relation with energy security faced by the EU import-dependent member countries. The new dimensions of energy security are explored and they are providing some suggestions for increasing security of supply and for fostering stability in the international energy system. In their conclusion, they highlight the risks for the world economic development as a result of competition in the energy sector. The second chapter is by Maria Flouri, Charikleia Karakosta, Haris Doukas & Alexandros Flamos from the laboratory of Management & Decision Support Systems of the National Technical University of Athens. They present and exploratory analysis of risks correlated to energy supply. The emphasis is given on the supply of oil and natural gas. Following the presentation of main energy disruptions, the most important risks identified are categorised according to their probability and expected impact. This analysis is a first step toward the assessment of risks affecting the smooth energy import to the EU. The third chapter is by Stefano Verde of RIE Ricerche Industriali ed Energetiche – Bologna. Taking into account the main objectives and targets of the EU energy policy, he focuses on the latest measures proposed by the EU institutions to promote renewable energies and energy efficiency and is trying to identify the main effects of these measures on the European energy security. A preliminary conclusion is made that the “EU 20-20-20 targets”, are able to positively contribute to the achievement of the security of supply objectives set by the EU. Nonetheless, attention has to be paid as this “positive correlation” is not straightforward and an optimal and balanced amount of new investments is required.

The fourth chapter is by GianCarlo Tosato, IEA/ETSAP – ASATREM Srl, Italy. He is presenting energy security from a system analysis point of view. Starting from the statement that “energy services security” extends the security of supply to the energy system as a whole he stresses the need that analyses should encompass all energy systems technologies and commodities. The risk aspects of the single points of the chains can be combined to form a “system risk”. Another important result is that the same system and analytical tool has to be used for analysing the effects of undesired events and remedial policies on all the three main objectives of energy policies: energy security, economic development and environment sustainability at the same time. His concluding remark is that attributing the responsibility of energy security to groups that will have to bare the main costs of less security would trigger the transition towards sustainability. The fifth chapter is by Franz Trieb from DLR – German Aerospace Center. He describes the perspective of a sustainable supply of electricity for Europe (EU), the Middle East (ME) and North Africa (NA) up to the year 2050. His study shows that a transition to competitive, secure and compatible supply is possible using renewable energy sources and efficiency gains, and fossil fuels as backup for balancing power. Of course, close cooperation between EU and MENA for market introduction of renewable energy and interconnection of electricity grids by high-voltage direct-current transmission are keys for the viability of such a plan and the necessary measures will take decades to be-come effective. Therefore, adequate policy, regulatory and economic frameworks for their realization have to be introduced immediately. The sixth chapter is by Kostis G. Perrakis from RAE – Regulatory Authority for Energy, Athens, Greece. He is providing an analysis on security of energy supply from the regulators side and highlights the priority to address the issue of security of electricity supply in a coherent and systematic way, from the regulatory perspective and taking into account all relevant impacts and dependencies. The chapter is concluding with the need to develop suitable indexes-signals for each category of actors involved (regulators, TSOs, generators, consumers, etc) for the continuous monitoring and forecasting of the energy security of supply. In following chapter, George Giannakidis from CRES – Centre for Renewable Energy Sources, Greece, is analysing the need for continuous monitoring and evaluation of the RES directives implementation in the EU27 and their impacts to the security of energy supply. In this framework, an overview of the FP7 RES2020 project is provided and its main aims are analysed. Finally, the need to define future options for policies and measures by calculating concrete targets for the RES contribution that can be achieved by the implementation of these options and the examination of all the implications of the achievement of these targets to the European Economy is highlighted.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 6

In the last chapter, Antonio Lopez de Sebastian from UNESA – Asociacion Espanola de la Industria Electrica, Spain, is providing an exploratory analysis reagrding the place of cross-border interconnections in the European Energy Strategy and in particular, its connection with the most relevant concerns on the European energy policy: the fight against the climate change and the security of energy supply. In addition, he examines the specific singularity of the interconnectors as a weak element in Transmission Networks, the important role that the reinforcement of networks and interconnectors plays in security of supply and in markets development and expansion. Finally, particular emphasis is laid in the cases of the Medring and the Iberian Market. It is hoped that this special issue aligning latest practices, innovation and case studies with academic frameworks and theories provides you with information on critical parameters of the complex issue of security of energy supply and trigger regarding the need to develop tools for EU27+ energy import scenario analysis.

The Editors, Professor John Psarras, Dr. Alexandros Flamos & Haris Doukas

Management & Decision Support Systems Laboratory

National Technical University of Athens (NTUA), Greece 22 May 2008

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 7

TABLE OF CONTENTS

INTRODUCTION ............................................................................ 10 Chapter 1 ENERGY GEOPOLITICS AND ENERGY SECURITY.................... 14 1.1. ENERGY SECURITY: AN OVERVIEW................................................................ 15

1.2. ENERGY SECURITY AND THE ENERGY SUPPLY CHAIN............................... 17

1.3. DIVERSITY IS THE KEY...................................................................................... 21

Chapter 2 RISKS ON ENERGY SECURITY OF SUPPLY: AN EXPLORATORY ANALYSIS FOR THE RESEARCHER ........................................... 25 2.1. METHODOLOGICAL NOTES .............................................................................. 29

2.2. IDENTIFIED RELATED INCIDENTS.................................................................... 30

2.3. RISKS QUALITATIVE ASSESSMENT................................................................. 40

Chapter 3

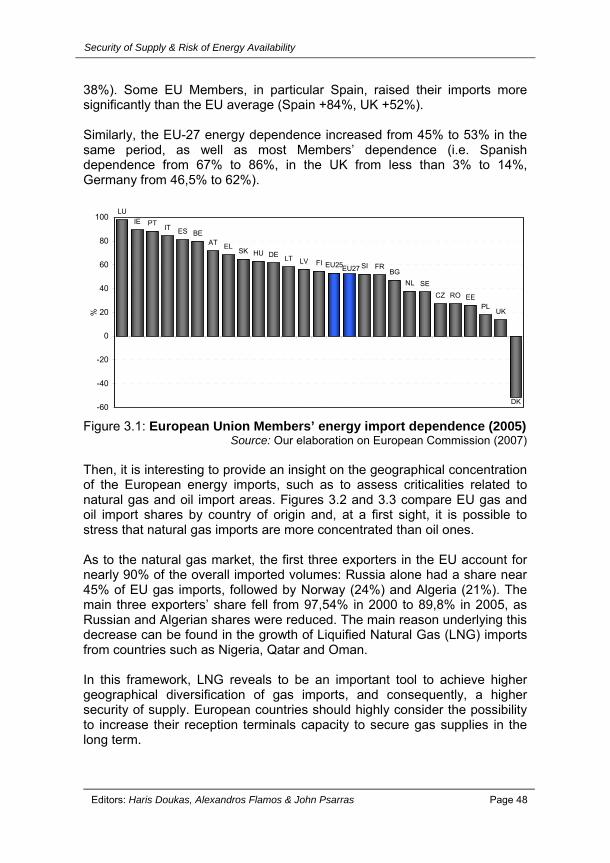

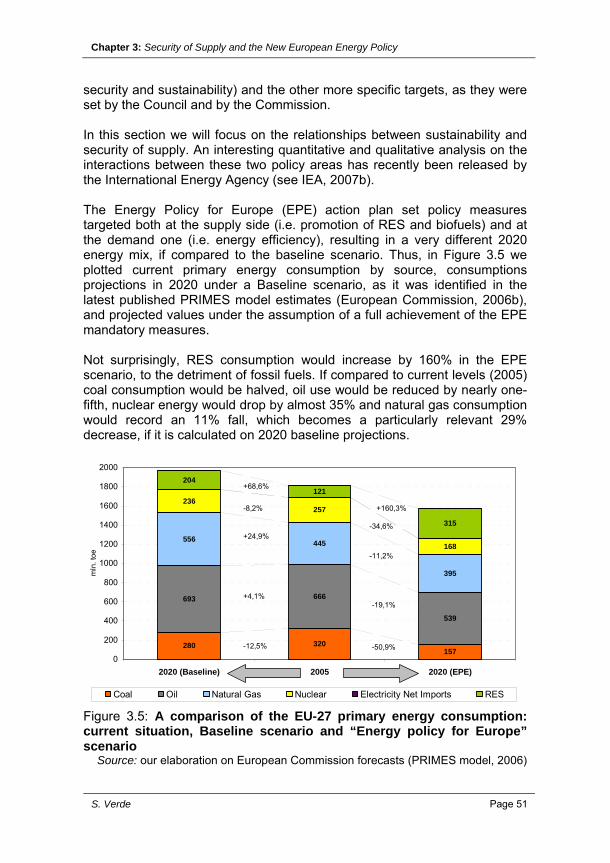

SECURITY OF SUPPLY AND THE NEW EUROPEAN ENERGY POLICY .......................................................................................... 45 3.1. DEFINING AND ASSESSING ENERGY SECURITY .......................................... 47

3.2. EFFECTS OF A NEW ENERGY POLICY ON SUPPLY SECURITY ................... 50

Chapter 4 ENERGY SECURITY FROM A SYSTEMS ANALYSIS POINT OF VIEW: INTRODUCTORY REMARKS............................................. 56 4.1. AN EXTENDED CONCEPT OF ENERGY SECURITY........................................ 57

4.2. IDENTIFICATION OF THE EVENT SPACE......................................................... 58

4.3. THE PROBLEM OF QUANTIFYING THE RISK .................................................. 59

4.4. QUANTIFICATION OF THE DAMAGES.............................................................. 59

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 8

4.5. WHAT MAKES THE DAMAGE OF UNDESIRED EVENTS SO HIGH?............... 60

4.6. TRADITIONAL OPTIONS TO REDUCE THE RISK AND THE DAMAGE ........... 61

4.7. TECHNICAL OPTIONS AND THEIR IMPACT EVALUATED THROUGH TECHNICAL ECONOMIC MODELS .................................................................... 62

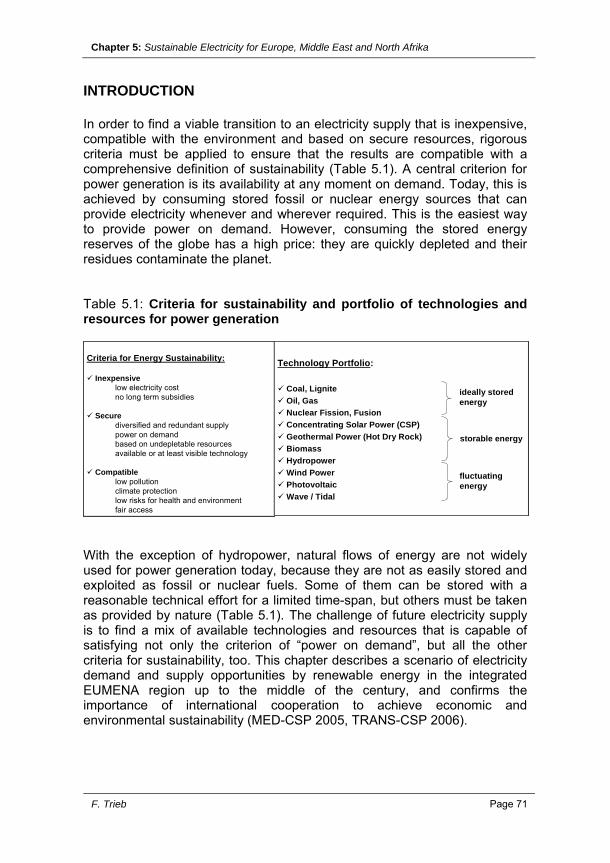

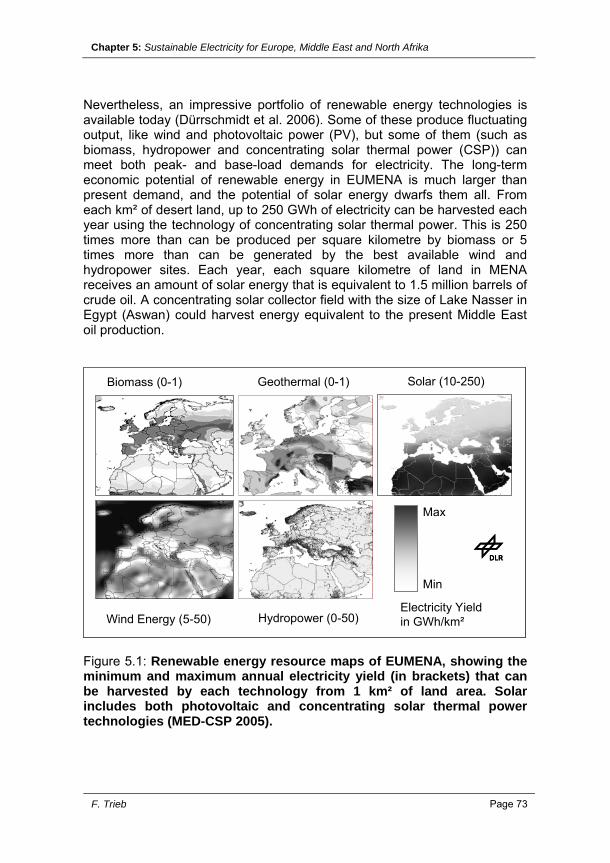

Chapter 5 SUSTAINABLE ELECTRICITY FOR EUROPE, MIDDLE EAST AND NORTH AFRICA ............................................................................ 70 5.1. INCREASING PRESSURE ON POWER SOURCES........................................72

5.2. PORTFOLIO OF SOURCES AND TECHNOLOGIES .......................................72

5.3. CONCENTRATING SOLAR POWER AS PART OF THE ENERGY MIX ............ 75

5.4. SUSTAINABLE ELECTRICITY MIX FOR EUMENA............................................ 76

5.5. LEAST COST RENEWABLE ELECTRICITY ....................................................... 82

5.6. AN ALTERNATIVE CLIMATE CHANGE AND NUCLEAR PROLIFERATION ..... 84

Chapter 6 SECURITY OF ELECTRICITY SUPPLY: ISSUES OF REGULATORY IMPORTANCE...................................................... 89 6.1. TAXONOMY SCHEME FOR ELECTRICITY SECURITY OF SUPPLY ............... 92

6.2. ENERGY ONLY MARKETS ................................................................................. 92

6.3. MECHANISMS ON GENERATION SIDE ENSURE ADEQUATE CAPACITY..... 93

6.4. MONITORING THE ELECTRICITY SECURITY OF SUPPLY ............................. 94

Chapter 7 MONITORING AND EVALUATION OF THE RES DIRECTIVES IMPLEMENTATION IN EU27 AND POLICY RECOMMENDATIONS FOR 2020-RES2020....................................................................... 97 7.1. OBJECTIVES ....................................................................................................... 98

7.2. MODELLING OF DISTRIBUTED GENERATION ................................................ 99

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 9

7.3. MODELLING OF THE BIOENERGY SUPPLY CHAIN ...................................... 102

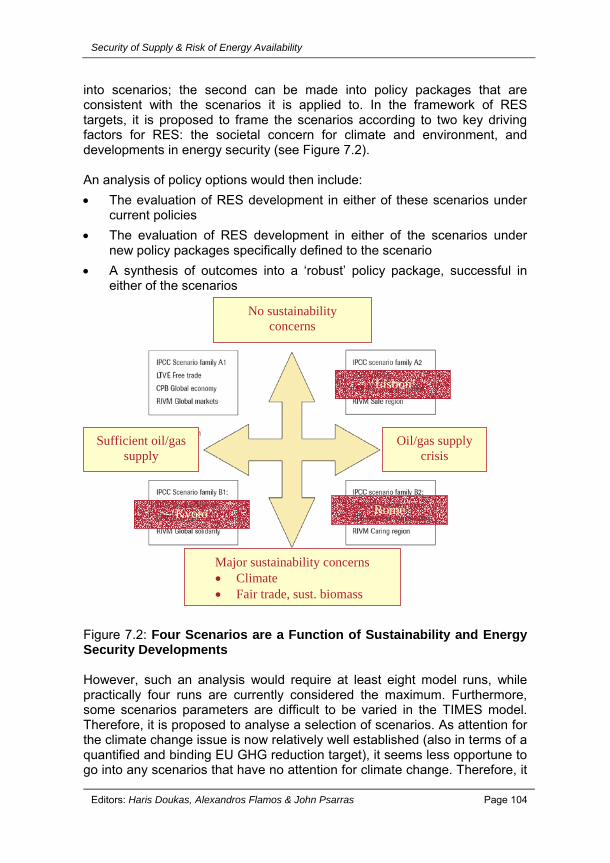

7.4. DEFINITION OF SCENARIOS........................................................................... 103

Chapter 8 CROSS BORDER INTERCONNECTIONS: A DRIVING FORCE IN SECURITY SUPPLY AND MARKETS DEVELOPMENT ............. 108 8.1. SECURITY OF SUPPLY AND MARKETS DEVELOPMENT IN THE EUROPEAN

ENERGY STRATEGY........................................................................................ 109

8.2. CROSS-BORDER INTER CONNECTORS: A WEAK POINT IN THE EUROPEAN TRANSMISSION NETWORKS .......................................................................... 110

8.3. SCARCITY MANAGEMENT AND REINFORCEMENT OF THE NETWORK.... 112

8.4. TRANSMISSION NETWORK ADEQUACY: SECURITY OF SUPPLY AND MARKET DEVELOPMENT ................................................................................ 113

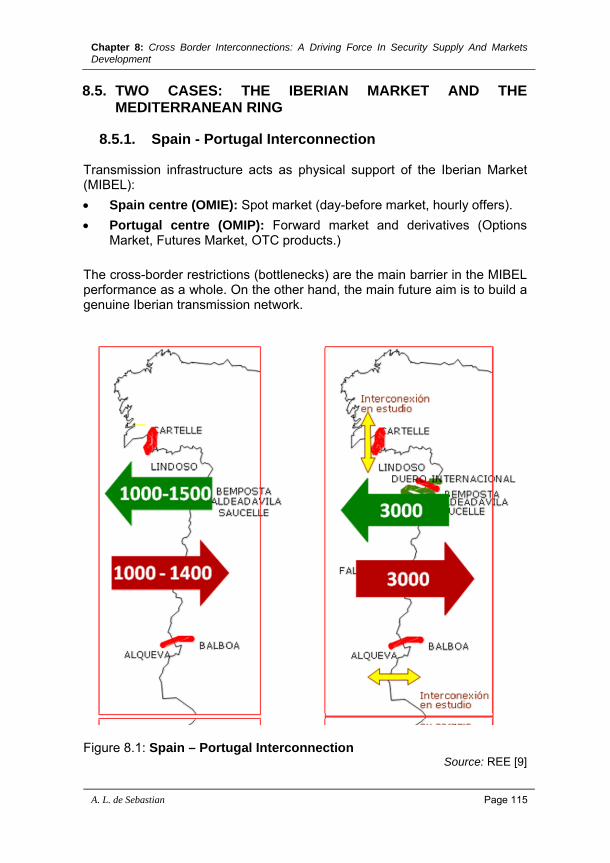

8.5. TWO CASES: THE IBERIAN MARKET AND THE MEDITERRANEAN RING .. 115

8.6. MEDRING........................................................................................................... 117

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 10

INTRODUCTION Pedro Miras, Director of Oil of the National Energy Commission, Member of the Board of Directors of the Strategic Reserves Corporation A secure energy supply is one of governments' and administrations' main concerns. This is nothing new, since it appeared at almost the same time as the first societies organised themselves around a fire and started to settle as soon as they could obtain and use fire safely. The European Union recognises this concern, and in the Commission’s communication to the Council of Europe and the European Parliament, “An Energy Policy for Europe”, a secure supply was included as one of the three attributes that the community energy policy should have. According to the document, Europe must generate sustainable, competitive and secure energy so that it results in the wellbeing of all its citizens. Supply security in energy markets is based on the following two policies. The first being long-term policies. Long-term policies are those that allow for an improvement in the supply at times when markets are operating normally and which are not valid in acute and occasional crises. Included in this group are energy saving and efficiency measures, the diversification of sources and understanding between producing and consuming areas. The second therefore being short-term measures. Short-term measures, however, respond to critical episodes lasting a short time and they are based on emergency actions and stock management. Lastly, the existence of interconnections between the energy networks in the different regions is a measure that has both a long- and short-term effect. These aspects will be discussed in this article.

Introduction

Pedro Miras Page 11

The European Union is in a highly vulnerable position when oil supply is concerned. To be precise, in 2007 over 81,7% of total consumption came from outside the Union’s borders. If we take into account the European energy matrix’s high degree of dependence on hydrocarbons, it is easy to understand the importance of assuring the supply of this energy source. This is even more critical if we consider that virtually half of the sources are geographical areas that are relatively unstable politically. Nonetheless, since their beginnings, oil markets have established short- and long-term supply assurance measures. If we take into account that the international oil trade was almost 63% of total consumption (83.1 MBbl/d) in 2006, and that this value is far higher than the ratios shown by other energies (26% for the natural gas business and only 11% for the European electricity business), it is easy to understand the importance of measures within this sector. Long-term assurance of oil supplies is based on the diversification of supply. This diversification needs to take into account the geographical imbalance between supply (producing countries) and demand (consuming countries). Therefore, if estimated reserves1 are borne in mind, 62% of the 1,208 thousand million barrels counted come from the Middle East area, which, on the other hand, only accounts for 7% of worldwide consumption. On the contrary, the countries in the OECD, responsible for 58% of consumption, only account for 7% of the oil reserves. The only long-term solution for this imbalance is to foster international dialogue. This dialogue would be aimed at making access possible for the majority of the reserves by means of fair and balanced trade that benefits both consuming and producing countries. However, the occurrences of occasional crises that can lead to restrictions in the supply (due to natural disasters, such as hurricane Katrina in August 2005) must be tackled with fast response measures. The most appropriate example is the International Energy Agency’s action protocols, which oblige its member countries to hold strategic reserves for a minimum of ninety days with counting and availability standards in the event of a crisis that, are known and accepted by all its members. These mechanisms need to be improved to perfect oil supply assurance systems, as well as the possibility of extending them to other types of energy. The natural gas market is also affected by similar aspects to oil’s, although its particular characteristics require additional approximations. Specifically, and besides the oil market’s characteristics, the supply of natural gas must respond to aspects such as those derived from technical faults,

1 BP Statistical Review 2007.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 12

meteorological conditions that may affect them, few LNG loading and unloading ports, or the difficulties derived from an asymmetrical regulation in gas transit between different markets. Aware of this situation, the European Union has published two directives that try to address these problems in particular. Specifically, Directive 2003/55/EC and the one on security in the natural gas supply 2004/67/EC propose rules for improvement, such as the promotion of gas storage facilities, the development of common operating rules among the operators in the national systems, promotion of cross-border capacities or the study of measures on the demand-side in the event of interruptions. All these actions aim to improve supply assurance systems in line with what has been done in the past with oil. However, in a market such as natural gas, which is constantly changing, the rules need to be subject to ongoing review. As a result, declarations such as those made recently by the Ministry of Energy and Mines in Algeria2 stating that the natural gas markets have changed from being a buyer’s to a seller’s market, and suggesting that this change has not simultaneously brought about the corresponding premium in the security of the supply, should force us to be constantly reviewing the supply assurance measures of this type of energy. In view of all the above, the answer for the natural gas market is to promote interconnections. This does not only mean physical interconnections, such as pipelines and gas storage facilities, or, more recently, the construction of LNG terminals, but also what could be termed “regulatory” interconnections. Therefore, as the directives state, we need to work towards common rules that reflect shared operation standards for all the operators of regional networks as a measure to ensure supplies at all times. In turn, work needs to be done on coordinated response measures, in the style of what has already been well developed by the IEA in the oil sector. As far as the electricity sector is concerned, expected growth in consumption will also require a constant consideration of supply assurance measures. Average growth in recent years, around 4%, of the member countries of the UCTE3 and the forecasts of worldwide consumption virtually doubling by 2030 made by the OECD make this task very necessary. The diversification of sources of generation seems to be the most important measure in all cases. The potential of generating renewable energies and

2 (PIW, Vol XLVII, N 7, February 18, 2008). 3 Union for the Co-ordination of Transmission of Electricity (UCTE).

Introduction

Pedro Miras Page 13

the role that nuclear power has to play in the future is essential for the implementation of a secure energy policy. Nevertheless, for this type of energy, a key factor is the development of transmission networks. If we take into account that according to UCTE data, the electric power business among its member countries was only 13% of what was generated, and that, in some cases, such as Iberia, the figure dropped to 4%, it is easy to understand that there is a long way to go in this field. The so-called “energy islands” can clearly be detected in the European environment, and the Iberian Peninsula is an example of one, although not the only one, as there is also the British Isles (in this case geographical islands as well) and Scandinavia. Consequently, in this case, and with even more necessity than in the natural gas markets, interconnection is the answer. Yet again, as a measure to secure the supply, there is a need to foster harmonised regulation that accompanies the development of physical interconnection networks in energy corridors. All without forgetting that emergency systems that are as flexible as possible also need to be promoted. As a result of all the above, and bearing in mind the importance of energy in the development of society and the need to ensure the energy supply, we need to answer to some questions that arise in the European market. Specifically, they are: Do we have a common energy market?. Are we considering that markets are changing (gas)?. Is dialogue enough to face geopolitical risks?. Is there enough diversification to face the problem?. Are we planning physical interconnections as required?. Are we aware of the requirements for “regulatory interconnections”?. Is it possible to translate any oil So-s ST measures to grid energies?. Are Regulatory Authorities, TSO, Governments and Companies involved enough in the SoS task? The project “Risk of Energy Availability: Common Corridors for Energy Supply Security” must tackle all of them and propose suitable solutions.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 14

Chapter 1: ENERGY GEOPOLITICS AND ENERGY SECURITY Paul Isbell, Director, Energy Programme, Elcano Royal Institute for International and Strategic Studies Federico Steinberg, Energy Programme, Elcano Royal Institute for International and Strategic Studies Rising energy demand from emerging economies, higher energy prices, new energy nationalism both by consumer and producer countries, and obstacles to international economic cooperation have radically transformed the global energy scenario in recent years. Therefore import-dependent countries in the European Union face important strategic dilemmas in relation with energy security. This chapter explores the new dimensions of energy security and presents some suggestions for increasing security of supply and for fostering stability in the international energy system.

Chapter 1: Energy Geopolitics and Energy Security

P. Isbell and F. Steinberg Page 15

INTRODUCTION

If the energy issue came to the forefront of world attention with the outbreak of the Iraq crisis in the autumn of 2002 –after more than a decade of absence from the international community’s strategic concerns– over the past years it has emerged as the global strategic issue par excellence. It is not just that energy now exerts an enormous influence on the dynamism of the international economy, the stability of world geopolitics and the future of our environment on a planetary scale; it also appears that the energy issue will not recede into the strategic background again for several decades. Within this context the concept of energy security has become crucial, particularly in most European countries that depend heavily on energy imports. Moreover, the European Union (EU) faces a difficult dilemma. On the one hand, it appears as the main global actor capable of fostering a market and rules-based system that would promote stability and security in international energy markets and, at the same time, erode the ability and the will of other actors to use energy as a geopolitical weapon. However, on the other hand, the EU faces internal difficulties to consolidate a common energy policy, which would be key to act as a global leader and provide multilateral governance in global energy issues. This chapter provides a brief discussion of these issues. First, it focuses on the concept and facets of energy security. Second, it explores the geopolitical implications of the new energy scenario and provides some suggestions for enhancing energy security in the European Union and worldwide. 1.1. ENERGY SECURITY: AN OVERVIEW The standard, and overused, definition claims that energy security is a state of affairs that provides for secure – or reasonably guaranteed – flows of energy to consumers at reasonable prices. Unfortunately, this definition is as vague and incomplete as to be basically useless in any serious discussion of energy economics or geopolitics. Perhaps the only positive thing that could be said of this definition is that while it is almost always mentioned at the beginning of such discussions, it is almost always quickly abandoned – right about at this point in the analysis. The energy terrain must be profoundly dissected if anything useful is to come of a discussion of energy security. First, there is the dichotomy between energy security for consumers (“security of supply”) and energy security for producers (“security of demand”). For consumers this issue (with

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 16

only few exceptions) basically boils down to price and the perception that price will not experience increases which are economically painful. For producers, the issue boils down to income, and the perceived need for revenues to be maintained at sufficient levels to pursue serious, long-term economic development. For better or for worse, these two perspectives are linked. Excessively low prices stimulate consumption and growth in consumer economies, but they undermine the potential for revenue-driven economic development in producer economies. Furthermore, low prices also limit the incentive for investment in future output in producer countries, setting the stage for much higher prices in the future – unless low prices become the door through which international private oil companies (IOCs) gain cheap access to the vast reserves of producer countries. However, such a development has often created a perception on the part of producer countries that their economic and political sovereignty is being compromised, provoking various manifestations of energy nationalism which often augur higher prices in the future (Isbell 2007). Higher prices, on the other hand, tend to have harmful effects on both perceptions and real economic activity in consumer countries, boding dangerously for producer country revenues if demand collapses as a result. Furthermore, high prices can stimulate investment in future output, with moderating effects on prices in the middle run, but they often provide the incentive for the resurgence of energy nationalism which, more often than not, limits the rate of investment in new output over the long run. Finally, high prices can also stimulate the development of non-fossil fuels alternatives which ultimately might dislodge hydrocarbons from their central role in the world’s economy and in producer state finances. A large part of the energy security debate revolves around fossil fuels. This is as it should be, given that fossil fuels provide for about 80% of the world’s primary energy mix. Therefore, energy security is inextricably bound up with the production and consumption of fossil fuels, particularly oil and gas which are the main internationally traded energy sources and which make up over half of the world energy mix (coal tends to be consumed in the country of production). Nevertheless, the generation, transmission and distribution of electricity (which accounts for nearly half of the world’s final energy consumption and can also be generated by non-fossil fuel energy sources), along with the security and efficient functioning of electricity systems, are also key elements of any discussion of energy security. One could argue that electricity issues are even more relevant than a merely hydrocarbon-centred discussion of the issue, given that electricity is much more important to the foundation of the economy; that is to say, in homes and in government and business office buildings around the world. While transportation to work and movement of merchandise are important, if the power goes off, it does not really matter

Chapter 1: Energy Geopolitics and Energy Security

P. Isbell and F. Steinberg Page 17

whether we are able to leave the house or get to work. Furthermore, electricity is certainly the most important energy security concern of the 1.5 billion people around the world who do not even have access to it. However, there is at least one other relevant angle in the energy security story – the insecurity that may well come if the world fails to displace fossil fuels from their dominant role in the energy economy. Even if the standard energy security concerns surrounding fossil fuels and electricity can be effectively dealt with, such success would paradoxically create a situation in which the world burns more fossil fuels more quickly and reduces carbon dioxide emissions more slowly, setting the stage for higher temperatures and even more difficult instabilities in the world’s economic and political systems. 1.2. ENERGY SECURITY AND THE ENERGY SUPPLY CHAIN Any complete discussion of energy security must address all of these angles. To facilitate such an analysis, it would be useful to address the energy security terrain through the prism of the energy supply chain, including the upstream, midstream and downstream. In the upstream of both oil and gas production – at the geographic source of reserves and production -- there are a number of concerns. The first is the debate over so-called “peak oil” – or the possibility, looming or not, that world oil production will one day peak, before falling off rapidly, or merely flat lining into a long plateau before declining. The well-known radical point of view sees the peak approaching fast, with record high prices one of the tell-tale signs. Most moderate perspectives are more sanguine about a “hard” peak; that is, a situation in which prices skyrocket to choke off demand because supply is no longer capable of rising. This point of view claims that peak theories factor in only conventional oil, ignore the economic viability of unconventional or more difficult and expensive oil in offshore regions or the Arctic zones as prices rise, and simply deny the capacity of technology to increase recovery rates of oil fields which traditionally have been only 30%. Most expert opinion sees the likelihood of a “hard” peak as very low for another 30 or 40 years, at least. Nevertheless, a few maverick voices from the oil industry, like the CEOs of Italy’s ENI or France’s Total, feel the idea that the world will ever produce 115mbd (the IEA’s projected demand level for 2030) is still a pipe dream. The idea that oil might “run out” soon – which when expressed intelligently simply means that oil might reach a peak capacity in its production level – may seem, intuitively, to be an important concern. Nevertheless, the debate over peak oil, as it is typically framed, is probably irrelevant, however counterintuitive such a conclusion might sound. It is not just that some oil will inevitably be left in the ground, whatever happens, because it will never

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 18

likely be economically or technically feasible to extract. More to the point: demand for oil itself is likely to peak long before any hard geological limitations impose a technical peak on production. Such a “soft” peak in oil production, brought on by moderating demand, is in fact what we seem to be hoping for, if not expecting, in our efforts to curb the rise in carbon emissions and stave off the worse aspects of global warming. If the threat of fossil-fuel induced climate change is real, then a geologically provoked “hard” peak is either irrelevant to us (if it is indeed only a possibility many decades in the future) or a kind of counterintuitive solution, as economically painful and disruptive as it might be (and the more useful the quicker it would come) given that the attendant supply shortages and prohibitive prices would act as an emergency break on carbon emissions, while the international crisis such a “hard” peak would produce might jolt the world into creating a carbon-free economy much faster than we might otherwise would have done with plentiful supplies and more moderate prices to enjoy in the short run. Nevertheless, if the peak oil debate is irrelevant, the possibility that hydrocarbon supplies in the upstream might not keep pace with demand -- for other “above the ground” reasons -- is a very real threat to energy security and to economic and political stability. Most of the world’s hydrocarbon reserves – conventional or not – are concentrated in a small number of countries, almost all of which are underdeveloped economically, unstable politically, lack robust democratic institutions, or feel threatened or left out by globalization. Nearly 75% of all conventional hydrocarbon reserves are found in the “Great Crescent”, running from the Arabian Peninsula and the Persian Gulf through Central Asia all the way to Eastern Siberia and Russia’s Sakhalin Island. To date, this geographic arc is one of the black holes of liberal market democracy and a major stumbling block for globalization. Most of the world’s unconventional oil is also highly concentrated in geographical terms. Nearly half is trapped in the tar sands beneath the forests and topsoils of Calgary in Canada, while nearly another half is bulked in the ultra-heavy oils of Venezuela’s Orinoco Belt. While Canada may be a model of stability and democracy, development of its tar sands would emit five times more carbon dioxide that conventional oils pumped from the traditional zones of the Middle East. Venezuela, on the other hand, is a metaphorical powder keg, at least for the moment. The concentration of hydrocarbon reserves in problematic zones beyond the OECD presents a number of challenges to what is traditionally understood as energy security. As perceptions of globalization have soured in many parts of the non-Asian, non-OECD world, and as prices have skyrocketed in recent years, energy nationalism is on the rise again for the first time since

Chapter 1: Energy Geopolitics and Energy Security

P. Isbell and F. Steinberg Page 19

the 1970s and has taken root in new areas. While the epicentre of energy nationalism was once the Arab and Islamic world (where it remains rooted), the most dramatic new examples of energy nationalism today are Russia and Venezuela, and both have spawned other examples among neighbours under their influence (Kazakhstan, Bolivia and Ecuador). The most significant challenge that such phenomena pose for the energy security of major consuming economies – and indeed for the collective energy security of the world – is the potentially damaging impact that the energy policies of such producer countries could have on the rate of future investment in exploration, extraction and maintenance of oil and gas production. Perhaps this “internal” aspect of energy nationalism would not be so worrying from the standpoint of the world’s future oil and gas supplies if it were not for the fact that estimated investment requirements for future demand to be met are daunting: the IEA (Isbell 2007) estimates that some US$22 billion in energy investment will be needed globally by 2030. Furthermore, while there are some exceptions (like Saudi Aramco and Petrobras), the general rule is that producer states and their NOCs are less than efficient when it comes to channelling revenues in ways which optimize future investment and output levels. Such doubts are particularly acute concerning Russia and Venezuela, whose governments and NOCs appear to have a number of competing interests and priorities which do not coincide with the interests of consumers to see future output maximized. As a result, a scenario is taking shape on the horizon in which hydrocarbons supplies in the middle run (by 2015-2020) will be insufficient to meet world demand, with the arbitrating influence ultimately being significantly higher prices. The difference between the implications of this scenario and that of the “hard” peak would be miniscule to the naked eye, only the root cause would not be geological limits but rather the influence of politics “above the ground” on investment. Exacerbating such a scenario would be a continuation of the recent trend of rising costs for inputs of all types (raw materials, equipment and human capital) all along the hydrocarbon supply chain. Despite the fact that this is one of the most important real threats to global energy security, the media’s attention and the public’s imagination remain captivated by another “external” sideline feature of energy nationalism: the potential use of energy supply cuts conceived of consciously by producer countries as a geopolitical weapon. Recent Russian gas and oil cut-offs to the Ukraine and Belorussia, along with Venezuela threats to halt the export of petroleum to the US have rekindled the worst kind of fears that Europe and the US might experience an energy crisis more catastrophic than the Arab Oil Embargo and the first oil shock. Citizens across the West are convinced that these energy producers have the will and the means to turn off their energy taps, generating a reactionary and protectionist attitude towards these countries and their business firms.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 20

Intuitively, such fears would seem reasonable, but they are probably ill-founded (Mabro 2007). First, the oil market is global. Oil export disruptions will either push up price for all consumers globally, or their diversion into other parts of the global market will provoke a readjustment of flows that will mute any effect on global oil prices. Gas cut-offs represent a greater threat to importing countries highly dependent on pipelined gas from a single hostile source, but even in such cases (Russian gas to Eastern and Northern Europe, Algerian gas to Southern Europe) the risks are overblown. On the one hand, neither Russia nor Algeria is inclined to be as hostile to Europe as many believe. On the other hand, such governments are too highly dependent on their revenues from gas exports to Europe to contemplate killing off the goose that lays their golden eggs. They are as smart and as rational and as humane as any of us in the so-called “West”. Global interdependence has gone too far to allow for such actions to yield anything more than pyrrhic victories. A Russian gas cut off of any significant impact is limited by similar considerations that checked the useful deployment of the old Soviet Union’s nuclear arsenal. The consequences would be too dire to contemplate. There are, nevertheless, a number of factors – other than producer state use of the energy weapon – which do provoke supply disruptions. Some of them -- like weather events (hurricanes in the Gulf of Mexico) and local instabilities (social unrest in the Niger Delta) -- are found in the upstream. Many others, however, occur in the midstream, at the level of oil and gas transportation. Oil and gas pipelines often lose flow or are shut down as a result of accident or sabotage (often one mascarades as the other). Examples include corrosion-induced leaks in BP’s Alaskan pipeline, explosions at Russian gas pipelines in Georgia, sabotage of Iraqi oil pipelines by insurgents, siphoning off from Shell’s pipelines by Nigerian militants, etc. The most significant transportation vulnerability, however, comes from threats to oil and liquefied natural gas that must be shipped along the world’s sea lanes and pass through a number of well-known “chokepoints”, like the Straits of Hormuz, the Straits of Malacca, the Bosporus and Dardanelles Straits and the Suez and Panama Canals. Nearly half of the world’s 86mbd of oil must flow through these potentially vulnerable chokepoints every day. It is estimated that by 2030, if current trends continue, some 30% of the world’s oil will have to pass daily through both the Straits of Hormuz and Malacca, almost all of it bound for East Asia. Accidents, sabotage, piracy, terrorist or military action are all capable of stopping or slowing the flow of petroleum through certain chokepoints, at least temporarily, unleashing potentially devastating effects on world prices. The most likely possibility for such action in the minds of many right now is the potential for Iran to affect the flow of oil through the Straits of Hormuz, possibly as a retaliatory action for a military strike on its territory.

Chapter 1: Energy Geopolitics and Energy Security

P. Isbell and F. Steinberg Page 21

The downstream scenario is dominated, on the hydrocarbon side, by refineries, petroleum product distributions systems, internal gas pipeline networks, and strategic reserves. On the electricity side of the fence, energy security means sufficient, reliable and safe generation, transmission and distribution, along with adequate international electricity and gas connections, particularly in relatively isolated countries like the UK or Spain. The energy security of the downstream in most countries boils down to regulatory regimes that optimize investment and maintenance of the refinery/generation systems, the distribution/transmission networks and storage facilities. Although as a rule there are relatively few breaches of energy security in the downstream, the nature of the regulatory regime is of extreme importance in order to avoid an undermining of sufficient investment or a weakening of maintenance which can, in given moments, produce blackouts like those in California and New York in recent years, or even like that experience in Barcelona last year. The extreme importance of downstream security is highlighted by the fact that such disruptions hit consumers most directly and most suddenly, typically in the form of supply cuts only ameliorated with great difficulty and distress, as opposed to the more gradual price increases produced by the kinds of disruptions mentioned above that can occur in the upstream and the midstream. 1.3. DIVERSITY IS THE KEY The key to increasing energy security is not the intuitive assumption that the ideal would be national energy independence and the capacity to control one’s own (or another’s) energy sources. Rather the key is to be inserted into the globally interdependent energy reality in the most diversified and, therefore least, vulnerable fashion. Diversity across the plane of the energy field is a more appropriate – and realistic – goal than energy independence. This means, where possible, diversity not only in energy types and geographic sources, but also of modes and routes of transportation. Better to have oil and gas from as many different geographic and political sources as possible, as well as a broad range of types of energy, ranging from fossil fuels to bio-fuels, from renewable energies to nuclear power, from combustion engines to electric hybrid motors and fuel cells. It also means diversity in the matrix of energy transportation from the upstream to the downstream. For example, rather than depending just on transit countries, like Ukraine, to pipeline Russian gas into Europe, or depending only on Russian pipelines which bypass the transit states and come directly into Germany, like the projected North Stream pipeline, Europe should encourage a balance between dependence on Russian gas that must pass through transit countries and dependence on Russian gas piped directly to the EU. This would produce a balancing effect on lobby pressures which either Russia or Ukraine might bring to bear on the EU. Likewise,

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 22

Spain should attempt to transform itself from a mere gas import terminal into a transit country funnelling much of Algeria’s gas (and regasified LNG from Trinidad and Tobago o Qatar) into France. It might also encourage Algeria to become, in addition to its key role as gas producer and exporter, a transit country for Nigerian gas passing through a future Trans-Saharan pipeline, on its eventual path to Europe via future trans-Mediterranean pipelines. The point is that diversity of supply increases energy flexibility and reduces vulnerability to any form of supply disruption, while diversity of transport modes and routes mitigates the political capacity – and the political will – of producer and transit states to be tempted into using supply cuts as a political weapon. Moreover, this strategy reinforces the long run policy objective of the EU of promoting market mechanism to manage global energy markets. Therefore, diversifying supply and making the world energy system more interdependent reduces the incentives of producers to try to use energy as a political weapon, thus reducing energy insecurity, international rivalry and energy nationalism. CONCLUSIONS Energy prices in general (and oil prices in particular) have permanently shifted to a much higher level than was usual in the past. If there is further price movement in the future, it is much more likely to be upward than downward. The perception that energy is now the central geopolitical battlefield has also grown considerably in Europe as a result of the disruptions to the supply of Russian energy, regardless of their duration or true causes. Public awareness of the role of our dependence on hydrocarbons in climate change has heightened even more the sensation of urgency that is felt in Europe to shape a European energy policy capable of overcoming this three-pronged economic, geopolitical and environmental challenge –a challenge that is being exacerbated and made more difficult by the new rise in Asian demand, on the one hand, and the US’s persistent preference for a policy that is not far from laissez faire (take this to mean: business as usual), on the other–. Europe advocates market principles and efficient economic competition as opposed to the traditional criteria of realism and geopolitical competition which are increasingly defining today’s energy field, to the detriment of global economic integration. This attitude is not without its risks, as each of the various energy policies possible only makes sense in the context of the international environment that emerges to dominate the future outlook. It will not be easy to make clinging to market principles work in the international energy sector if other significant players in the game –the major producer countries (for example Russia), the major consumer countries (China) and

Chapter 1: Energy Geopolitics and Energy Security

P. Isbell and F. Steinberg Page 23

even the major member states with their major national champions– continue to play by the rules of national rivalry and geopolitical competition. Even if energy nationalism proves incapable of truly achieving its aims –compared with the overall superiority of a well-designed and regulated market scenario– it will end up defining our world energy reality if there are enough players who espouse this idea, as there appear to be currently, posing risks to those who continue along the market path. If Europe attempts this anyway, one of its major challenges will be to carry on preserving its unity in the face of likely pressures and difficulties, seeking feasible formulas to share the burden of the inevitable adjustments. In any case, as we have argued, diversification and increased interdependence appear as the most effective long run strategies. But these dilemmas are always more acute in the case of a single small country, a typically run-of-the-mill player unable to shape the characteristics of the global energy landscape as it evolves (most EU countries would in fact fall into this category). For a major player with the potential to change the direction and profile of the international scene, acting as world leader, there is a credible possibility of success. However, in the energy issue it seems that the major actor who takes on the role of world leader is not going to be the US –it would have to be Europe–. Indeed, in the final analysis, if all remains the same, the fragmentation of the world economy that would result from national competition in the energy sector would threaten not only the future of the EU’s single market but also the possibility of progressing further with world economic integration and, as witnessed at the end of the last stage of late 19th-century and early 20th-century globalisation, it is very likely that sooner or later this trend will lead to war. What choice, then, for Europe? REFERENCES [1] British Petroleum (2007). Statistical Review of Energy 2007. [2] European Commission (2006a). Green Paper: European Strategy for a sustainable, competitive and secure energy policy. Brussels. [3] European Commission and the Secretary General/High Representative Javier Solana for the European Council (2006b). “An external Policy to serve Europe’s Energy Interests” Brussels. [4] International Energy Agency (2007). World Energy Outlook.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 24

[5] Isbell, Paul (2007). “Revisiting Energy Security” Oxford Energy Forum, Issue 70. [6] Mabro, Robert (2007). “Oil Nationalism, the Oil Industry and Energy Security Concerns” ARI 114/2007 Royal Elcano Institute. [7] Snijder, René (2008). “The Future of Gas and the Role of LNG: Economic and Geopolitical Implications” WP 14/2008, Royal Elcano Institute. [8] Youngs, Richard (2007). “Europe’s External Energy Policy: Between Geopolitics and the Market” CEPS Working Paper 278.

Chapter 2: Risks on Energy Security of Supply: An Exploratory Analysis for the Researcher

M. Flouri et al. Page 25

Chapter 2: RISKS ON ENERGY SECURITY OF SUPPLY: AN EXPLORATORY ANALYSIS FOR THE RESEARCHER Maria Flouri, Charikleia Karakosta, Haris Doukas and Alexandros Flamos NTUA-EPU, National Technical University of Athens, Greece European energy demand and import dependence continues to increase and primary energy sources are mainly used to cover European energy needs, making clear that the risks of energy security of supply and their minimization, is a critical issue. Aim of this chapter is to address the overall energy supply status, considering the energy supply corridors and procedures in the European Union, in order to underline the importance of risk analysis and risk minimization. The emphasis is given on oil and natural gas’s categorization of most important risks, as well as, in the presentation and analysis of collection of incidents that justify the categorization itself, while it demonstrates the importance of risk analysis and prediction.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 26

INTRODUCTION European energy demand increases, throughout the years, resulting in a simultaneous increase in its import dependence. European dependence on import of natural gas is the current reality for the majority of European countries. Approximately nine out of 33 European countries are more than 95% dependent on imports and only 5 are self-sufficient or net exporters [1]. According to International Energy Agency (IEA) in 2020 the European import dependency is expected to reach 90% for oil and 63% for natural gas, in comparison to 50% for oil and 36% for natural gas in 2000. In addition, 70% of the European energy needs are expected to be met by primary (and not renewable) sources by 2030. This is particularly important, taking into consideration the fact that primary energy sources are imported from areas outside Europe that are either difficult to reach or geopolitically unstable. All the above, combined with the surge in oil prices that took place in 2000, have made the issue of risks on energy security of supply and their minimization, more critical than ever. Apart from the increasing oil dependence, a gradual decrease in oil import security has been observed within the IEA network during the last 20 years. This decrease, translated into numbers, accounts for 50 days of net imports from 1986 to 2001 (110 days in 2001, while 160 days in 1986) and it constitutes an evidence of an industrial trend towards a gradual maintenance of lower levels of resources since the beginning of 1980’s, combined with the stabilization of state security resources since 1986. Nowadays, this decrease has been accelerated reflecting rationalistic trends, cost restrictions and high reliance on crude oil. The decreasing security resources restrict the possibility of an effective confrontation in case of a possible supply interruption. Thus, the market is becoming more vulnerable to possible crises, such as the occasional export interruptions in Iraq [2]. Moreover, it is more than true that oil resources are not abundant and are even less equally distributed than coal and natural gas. Furthermore, oil demand is focalized on developed countries, though its production is limited in a small number of developing countries. The Organization of the Petroleum Exporting Countries (OPEC) holds 40% of the global oil production and 80% of its known resources. Six countries of the Middle East, members of OPEC, control the 2/3 of the known oil resources worldwide [7]. OPEC’s Middle East producers are responsible for 27% of the global oil supply, a share which is expected to be doubled during the next two decades, whilst other areas’ production is reaching saturation and thus decreasing. Middle East is also responsible for 40% of crude oil’s global trade. These areas would not represent energy’s supply uncertainty factor in case they were politically and economically stable and they followed policies delimited by the market [2].

Chapter 2: Risks on Energy Security of Supply: An Exploratory Analysis for the Researcher

M. Flouri et al. Page 27

Therefore, income from oil exploitation is really crucial not only for OPEC countries’ economy but also for non-OPEC countries that export oil, such as Russia, Mexico and Norway. Periods of intense and increased competition, along with changes in the market’s share, are followed by periods of co-operation among the OPEC countries, in the framework of an effort to influence oil markets. Acts of mutual support between the oil-producing countries are expected, in order to assure a lower limit in oil price. In order for a cartel to operate properly, the existence of some rules is really important. During a crisis due to extra sufficiency in supply, which resulted in really low prices of oil, OPEC members reduced their production to levels prior to the crisis, as happened during the period 1985 -1986 and according to the agreement for reducing production of 1998 - 1999. Moving on to the natural gas market, demand is expected to increase rapidly in all sectors, due to its increased share in electricity generation in industrial countries and its use in developing countries instead of fossil fuels. The geographical allocation of natural gas resources constitutes also a serious issue, considering that 70% of the known resources are situated in the former Soviet Union and the Middle East, with Russia and Iran, obtaining half of this share. Furthermore, the natural gas import dependence from non-European countries is expected to increase from 1/3 of demand in 2000 to 2/3 in the next two decades. On an international basis this increase is justified by the fact that 9 out of the 33 European countries are 95% depended on natural gas imports, while only 5 are self-sufficient or net exporting countries. The situation is better for EU-15, with 7 countries being 95% depended and 3 countries being self sufficient or exporting. North Europe is totally depended on natural gas imports, mostly from Russia, having no alternative choices. The same situation is, also, observed in Central and South East Europe, except for the case of Romania and Croatia that are rather independent as well as Hungary and Switzerland that have more alternatives. South Europe is also highly depended on natural gas import, having only a few other alternatives. South Europe, with the only exceptions of Italy and Spain, relies mostly on Russian and Algerian natural gas and Liquefied Natural Gas (LNG). West Europe, which holds 2% of the global resources, imports from Russia and Algeria 40% of its needs. Besides the fact that North West Europe is highly import depended, with imports, not only, from countries outside the European Union (EU) but, also from England, through the Interconnector pipeline, offering additional flexibility. Greece imports 75% of its natural gas needs from Russia and 25% from Algeria. Generally, no alteration concerning the import dependence is expected during the next years and until 2020. Russia, Algeria and Norway will, gradually, increase their exports, with, a rather high, possibility to create a Baltic “corridor” for the Russian natural gas and a Mediterranean “corridor” for the Algerian

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 28

natural gas. Moreover, there is a high possibility of new energy routes being created, with Turkey playing a leading role in this respect [1]. In addition to the above, the fact that the majority of natural gas supplies is released through a pipeline network, concentrated on a few trunk lines, which are nearly fully booked and partially not interconnected or reversible [3, 4], has as a consequence the inflexibility of the European natural gas supply logistics. In case part of the chain is blocked, the consequences within the whole system will be quite severe and they will affect both natural gas and LNG market [5]. The danger for a prolonged interruption comes from the destruction of a major production or processing facility or a deep water pipeline, whose replacement might take several months [6]. European natural gas supplies from particular sources are vulnerable to potential accidents at key transmission and import facilities, some of which are remote from the European area. The facilities of greatest importance are the Yamal – Nenets pipeline corridor, which carries nearly 90% of Russian natural gas production, the Ukrainian pipeline corridor, which carries nearly 90% of Russian natural gas exports, the Trans-Mediterranean and GME from Algeria to Italy, Spain and Portugal and, finally, the Troll field and associated pipeline infrastructure, which accounts for more than half of Norwegian production and exports. Although it is quite unlikely that any of these facilities, particularly those involving multiple pipelines or LNG trains, would suffer a major failure, such low probability events could have a substantial impact on a particular source of transit route and therefore an entire European region [1]. Moreover, regarding natural gas, market liberalization could signal the beginning of a risk domino. Particularly, investments that reach the amount of 2 billion dollars will continue to be financed by long-term contracts. However, there is a doubt whether or not investments concerning amounts higher than 2 billion dollars, and in particular higher than 5 billion dollars, could be financed. This doubt can be explained by taking under consideration the fact that these investments will take place in non European countries, with no previous structures territories, where reassuring the investments’ commercial viability and full outcome makes impossible their materialization into stages and, also, the fact that the outcome of these investments will be sold in liberated and competitive markets. This kind of investments will be, mostly, essential, in order to cover the increased demand of the period after 2010 [1]. In the above framework, this study aims to present an approach to the overall energy supply status, regarding energy supply corridors and procedures in the European Union, laying emphasis on oil and natural gas. The main scope of this chapter is to underline the importance of risk analysis for energy supply security issues. In particular, the study is an effort to

Chapter 2: Risks on Energy Security of Supply: An Exploratory Analysis for the Researcher

M. Flouri et al. Page 29

present historical data, including incidents that resulted in the interruption of energy supply, along with their assessment; evaluation. Apart from the introduction, where a brief description of the energy situation in Europe was provided, as well as a, rather indirectly, recording of potential risks, the chapter is structured along five sections. The second section is devoted to the presentation of the risk categorization that appears to be the most practical to be taken into consideration in a risk analysis of security of supply. The actual incidents per risk category are described in the third section, while their assessment and evaluation is provided in the fourth section. Finally, in the last section are the conclusions, which summarize the main points, arisen in this chapter.

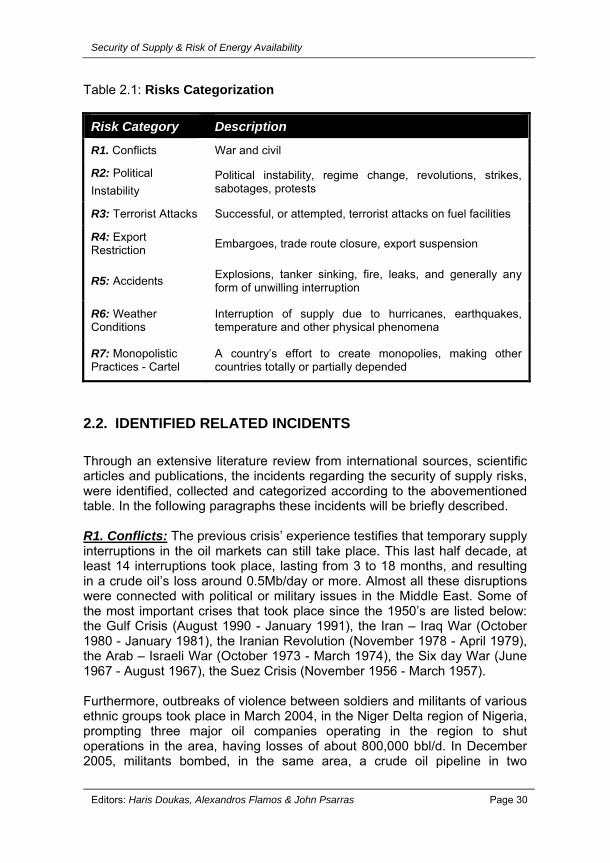

2.1. METHODOLOGICAL NOTES In the international literature, many studies exist that propose specific categorizations of risks possible to occur during energy supply. A proposed energy supply risk categorization falls into source dependence, transit dependence, facility dependence and structural risks, which contain natural disasters, political blackmail, terrorism, war, civil unrest etc [3]. Another study proposes a categorization that includes import dependence, source dependence, transit dependence, facility dependence and security incidents [1]. Moreover, risk categorization can also be found in international literature, according to the period of time; short term (12-18 months): disruptions of international supplies, medium term (3-5 years): export cartel issues, short to medium term: political issues, long term (10-15 years): resource shock, medium to long term: “real climate policy” shock [8]. Finally, another categorization includes war and civil conflicts, political instability, regime change, revolutions, successful terrorist attacks on oil facilities, export restriction, closure of trade routes and sanctions [9]. With respect to the above mentioned studies, this chapter’s categorization of oil and natural gas risks, in energy security of supplies, is defined and described in the following table.

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 30

Table 2.1: Risks Categorization

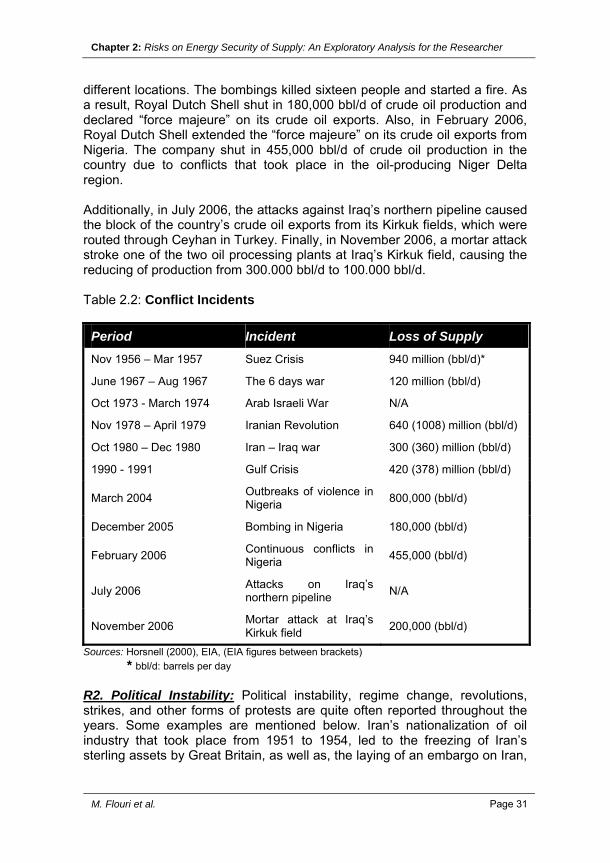

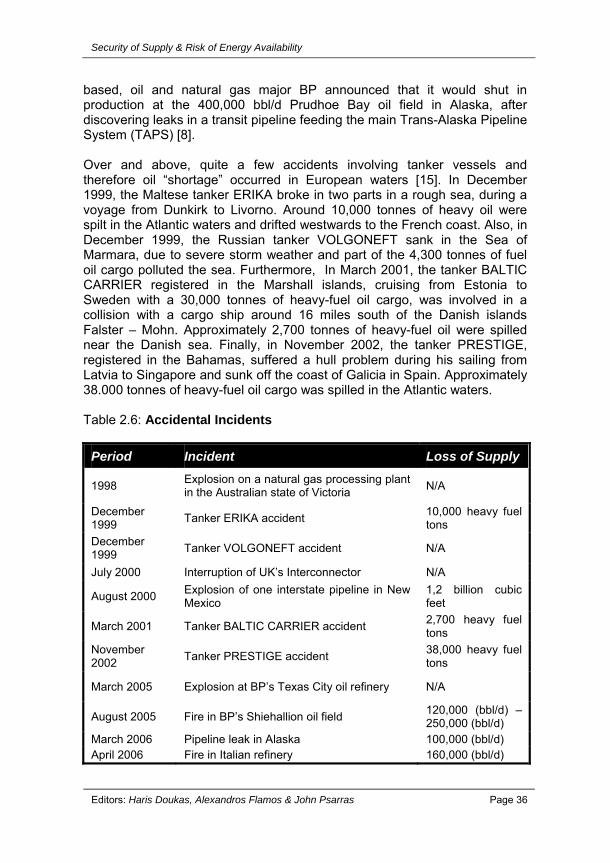

2.2. IDENTIFIED RELATED INCIDENTS Through an extensive literature review from international sources, scientific articles and publications, the incidents regarding the security of supply risks, were identified, collected and categorized according to the abovementioned table. In the following paragraphs these incidents will be briefly described. R1. Conflicts: The previous crisis’ experience testifies that temporary supply interruptions in the oil markets can still take place. This last half decade, at least 14 interruptions took place, lasting from 3 to 18 months, and resulting in a crude oil’s loss around 0.5Mb/day or more. Almost all these disruptions were connected with political or military issues in the Middle East. Some of the most important crises that took place since the 1950’s are listed below: the Gulf Crisis (August 1990 - January 1991), the Iran – Iraq War (October 1980 - January 1981), the Iranian Revolution (November 1978 - April 1979), the Arab – Israeli War (October 1973 - March 1974), the Six day War (June 1967 - August 1967), the Suez Crisis (November 1956 - March 1957). Furthermore, outbreaks of violence between soldiers and militants of various ethnic groups took place in March 2004, in the Niger Delta region of Nigeria, prompting three major oil companies operating in the region to shut operations in the area, having losses of about 800,000 bbl/d. In December 2005, militants bombed, in the same area, a crude oil pipeline in two

Risk Category Description

R1. Conflicts War and civil

R2: Political Instability

Political instability, regime change, revolutions, strikes, sabotages, protests

R3: Terrorist Attacks Successful, or attempted, terrorist attacks on fuel facilities

R4: Export Restriction Embargoes, trade route closure, export suspension

R5: Accidents Explosions, tanker sinking, fire, leaks, and generally any form of unwilling interruption

R6: Weather Conditions

Interruption of supply due to hurricanes, earthquakes, temperature and other physical phenomena

R7: Monopolistic Practices - Cartel

A country’s effort to create monopolies, making other countries totally or partially depended

Chapter 2: Risks on Energy Security of Supply: An Exploratory Analysis for the Researcher

M. Flouri et al. Page 31

different locations. The bombings killed sixteen people and started a fire. As a result, Royal Dutch Shell shut in 180,000 bbl/d of crude oil production and declared “force majeure” on its crude oil exports. Also, in February 2006, Royal Dutch Shell extended the “force majeure” on its crude oil exports from Nigeria. The company shut in 455,000 bbl/d of crude oil production in the country due to conflicts that took place in the oil-producing Niger Delta region. Additionally, in July 2006, the attacks against Iraq’s northern pipeline caused the block of the country’s crude oil exports from its Kirkuk fields, which were routed through Ceyhan in Turkey. Finally, in November 2006, a mortar attack stroke one of the two oil processing plants at Iraq’s Kirkuk field, causing the reducing of production from 300.000 bbl/d to 100.000 bbl/d. Table 2.2: Conflict Incidents

Period Incident Loss of Supply Nov 1956 – Mar 1957 Suez Crisis 940 million (bbl/d)*

June 1967 – Aug 1967 The 6 days war 120 million (bbl/d)

Oct 1973 - March 1974 Arab Israeli War N/A

Nov 1978 – April 1979 Iranian Revolution 640 (1008) million (bbl/d)

Oct 1980 – Dec 1980 Iran – Iraq war 300 (360) million (bbl/d)

1990 - 1991 Gulf Crisis 420 (378) million (bbl/d)

March 2004 Outbreaks of violence in Nigeria 800,000 (bbl/d)

December 2005 Bombing in Nigeria 180,000 (bbl/d)

February 2006 Continuous conflicts in Nigeria 455,000 (bbl/d)

July 2006 Attacks on Iraq’s northern pipeline N/A

November 2006 Mortar attack at Iraq’s Kirkuk field 200,000 (bbl/d)

Sources: Horsnell (2000), EIA, (EIA figures between brackets) * bbl/d: barrels per day R2. Political Instability: Political instability, regime change, revolutions, strikes, and other forms of protests are quite often reported throughout the years. Some examples are mentioned below. Iran’s nationalization of oil industry that took place from 1951 to 1954, led to the freezing of Iran’s sterling assets by Great Britain, as well as, the laying of an embargo on Iran,

Security of Supply & Risk of Energy Availability

Editors: Haris Doukas, Alexandros Flamos & John Psarras Page 32

challenging, this way, the legality of the oil nationalization and taking its case at the International Court of Justice in Hague. Another similar incident, concerning though the interruption of natural gas supply and energy supply in general, is the Norwegian workers’ strike that took place in UK (near the Frigg area), in April 1986, and lasted for several days, resulting in the loss of almost one fourth (1/4) of the country’s total natural gas strategic supplies. Furthermore, in April 2002, thousands of workers at the Venezuelan state oil company PdVSA protested, by closing the gates of the facilities. Some days later, a general strike begun in Venezuela, causing the shutdown of several stores and factories and almost halting oil production, refining and export. In December 2003, the business and labour groups in Venezuela, including the employees of PdVSA, begun a strike in order to obtain an early referendum on the rule of Venezuelan President Hugo Chavez. The estimated loss of production was calculated to 3 million barrels per day of strike. In June 2004, two explosions damaged the Kirkuk-Ceyhan oil pipeline, something that later was determined to be an act of sabotage. Several other Iraqi pipelines were damaged in acts of sabotage throughout the same month. In August 2004, Iraq’s crucial northern pipeline from Kirkuk to the Turkish port of Ceyhan was attacked, only two days after being brought into operation for the first time since the war, thus stopping the flow of the oil. Finally, in March 2005, Iraq closed its northern crude oil export pipeline indefinitely due to sabotage concerns. The 600,000 bbl/d - pipeline, which ran from the city of Kirkuk to the Mediterranean port of Ceyhan, was the target of over 15 attacks since January 2005. In addition, in December 2004, around 300 unarmed Nigerian villagers, including women and children, from the Kula community in Rivers State in the Southern Niger Delta, seized three oil flow stations, which were operated by the multinational oil companies of Shell and Chevron Texaco, shutting in 100,000 barrels per day (bbl/d) of production for one week. Moreover, a strike that took place in France (May 2005), caused the shut-down of five, out of six, oil refineries, operated by the international oil major Total. Another strike in July 2005, this time in Angola’s Block 0 offshore oil project, resulted in the shut down of almost all the production of the project. In September 2005, a strike at the largest oil refinery in France, Total’s Facility in Gonfreville, shut in 343,000 bbl/d of refining capacity in the country. During October 2005, in another continent, in Nigeria’s Brass River crude oil export terminal, a strike of workers caused the termination of operations at the facility for two days. At the same month workers at the Royal Dutch Shell’s Pernis refinery begun a gradual shut-down of the facility, as part of a labour dispute with the company.

Chapter 2: Risks on Energy Security of Supply: An Exploratory Analysis for the Researcher

M. Flouri et al. Page 33

In August 2005, protests in Equador’s northeast, oil-producing provinces shut in most of the country’s crude oil production. Finally, in February 2006, protesters in Equador shut down all crude oil production, that operated by state-owned Petroecuador. Table 2.3: Political Instability Incidents

Period Incident Loss of Supply March 1951 - Oct 1954 Nationalization of oil industry in Iran 940 million (bbl/d)

April 1971 - Aug 1971

Nationalization of oil industry in Algeria 90 million (bbl/d)

April 1986 Strike in UK’s – Frigg area natural gas production facilities N/A

April 2002 Strike at Venezuelan PdVSA which was generalized in all Venezuela N/A

December 2003 Strike in Venezuela 3 million (bbl/d) June 2004 - Aug 2004

Attacks at the Kirkuk – Ceyhan oil pipeline N/A

December 2004 Seizure of 3 oil flow stations in Nigeria 100,000 (bbl/d)

March 2005 Indefinite closure of Kirkuk-Ceyhan oil pipeline 600,000 (bbl/d)

May 2005 Strike in France’s oil refinery N/A July 2005 Strike in Angola’s oil project N/A

August 2005 Protests in Equador’s oil producing provinces N/A

September 2005 Strike in France, Total’s facilities 343,000 (bbl/d)

October 2005 Strike in Nigeria’s crude oil export terminal N/A

October 2005 Strike at the Royal Dutch Shell’s Pernis refinery N/A

February 2006 Protests in Equador – shutting down all crude oil production N/A

Sources: Horsnell (2000)[10], EIA [11]. R3. Terrorist Attacks: Terrorist attacks, though not so often, can cause serious damages in the energy supply procedure, either due to actual destructions or even because of the state of terror that a possible terrorism act creates. The most important terrorist attacks in the energy supply include two incidents and are mentioned and described below. In November 1997, a terrorist attack occurred when a bomb exploded in an on-shore Algerian section of the Trans-Mediterranean pipeline between Tunisia and Italy. Supplies were maintained through security storage and through additional imports by alternative suppliers, thus, limiting any further

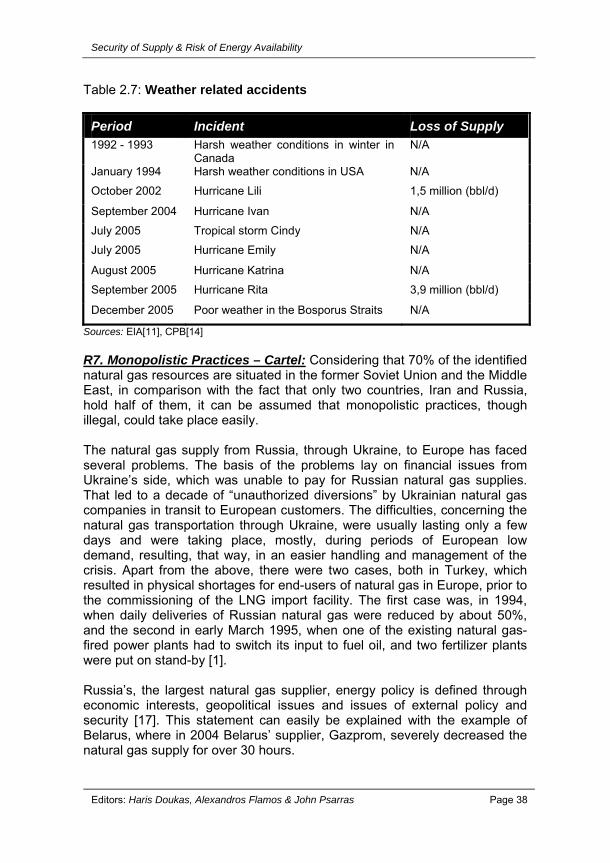

Security of Supply & Risk of Energy Availability