SECURITIES AND EXCHANGE BOARD OF INDIA Memorandum to …

139

Page 1 of 9 SECURITIES AND EXCHANGE BOARD OF INDIA Memorandum to the Board No. 58 / 2014 Report of the Depository System Review Committee 1. SEBI Board in its meeting held on July 28, 2011 suggested that demat system may be reviewed on the basis of CPSS-IOSCO principles by an external expert appointed by SEBI. 2. To give effect to the decision of the SEBI Board, an expert committee was constituted as the 'Depository System Review Committee (DSRC)' by SEBI in June 2012 under the Chairmanship of Shri M. Balachandran (Chairman, NPCI and former CMD, Bank of India) and included the following external members: i. Prof. H. Krishnamurthy (Principal Research Scientist, IISc Bangalore) ii. Shri R. S. Loona (Managing Partner, Alliance Corporate Lawyers and former Executive Director, SEBI) iii. Prof. Vikram Kuriyan (Clinical Prof. of Finance, Indian School of Business) 3. The mandate of the committee was guided by the following Terms of Reference: i. Assessment of Existing Policy Framework of Depositories and identify areas for review. ii. Assessment of Depository System with CPSS-IOSCO principles, recommendations of CESR-ECB pertaining to CSDs so as to benchmark with Global Best Practices. iii. Identifying areas for continuous improvement of systems, procedures and practices and make recommendations thereof. iv. Identify systemically important market infrastructure providers/institutions/ depository participants and their inter-linkages

Transcript of SECURITIES AND EXCHANGE BOARD OF INDIA Memorandum to …

Page 1 of 9

SECURITIES AND EXCHANGE BOARD OF INDIA

Memorandum to the Board

No. 58 / 2014

Report of the Depository System Review Committee

1. SEBI Board in its meeting held on July 28, 2011 suggested that demat system

may be reviewed on the basis of CPSS-IOSCO principles by an external

expert appointed by SEBI.

2. To give effect to the decision of the SEBI Board, an expert committee was

constituted as the 'Depository System Review Committee (DSRC)' by SEBI in

June 2012 under the Chairmanship of Shri M. Balachandran (Chairman, NPCI

and former CMD, Bank of India) and included the following external members:

i. Prof. H. Krishnamurthy (Principal Research Scientist, IISc Bangalore)

ii. Shri R. S. Loona (Managing Partner, Alliance Corporate Lawyers and

former Executive Director, SEBI)

iii. Prof. Vikram Kuriyan (Clinical Prof. of Finance, Indian School of

Business)

3. The mandate of the committee was guided by the following Terms of

Reference:

i. Assessment of Existing Policy Framework of Depositories and identify

areas for review.

ii. Assessment of Depository System with CPSS-IOSCO principles,

recommendations of CESR-ECB pertaining to CSDs so as to

benchmark with Global Best Practices.

iii. Identifying areas for continuous improvement of systems, procedures

and practices and make recommendations thereof.

iv. Identify systemically important market infrastructure

providers/institutions/ depository participants and their inter-linkages

Page 2 of 9

and identify areas and suggest safeguards to prevent single point

failures and denial of depository service.

v. Review existing system of inspection by depositories and suggest

changes to strengthen the monitoring/oversight of depository

participants.

4. In the area of inspection and oversight function of depositories including for IT

Governance, the committee decided to carry out a detailed analysis and

formed a sub-committee for this purpose comprising Prof. Krishnamurthy,

representatives of NSDL, CDSL and officials of SEBI. The recommendations

of the sub-committee were presented to SEBI as part of an interim report. The

committee submitted its interim report in May 2013. A copy of the Interim

Report of the committee is annexed to the Board Memorandum (Annexure A).

5. The interim recommendations of the committee are as follows:

A. IT Governance Depositories should implement the following for their IT governance structure:

a) There should be an IT strategy committee at the board level of

depositories.

b) There should be an approved and comparable IT strategy/plan document

which needs to be reviewed annually by the depositories and their DPs.

c) There should be an IT Steering committee to assist the IT Strategy

Committee in implementation of IT strategy. The IT steering committee

should comprise of representatives from IT, HR, Legal and various

business functions as appropriate.

d) Information Security policy should be approved by the board and reviewed

annually.

e) There should be an office of information security and a senior official

should be designated as Chief Information Security Officer (CISO) whose

work would be to assess risk and identify the threat / vulnerabilities.

Page 3 of 9

B. Oversight and Inspection Framework

The committee carried out an extensive review of the oversight and inspection

framework for Depository Participants. The key recommendations of the

committee are as follows:

i. Inspection of Depository Participant by Depositories:

a) Inspections should be risk based rather than compliance based to

provide economic benefits such as fewer inspections for less risky

participants and frequent inspections for more risky ones. The

inspection reports should not only identify risk areas but should also

proactively suggest risk mitigation.

b) The sample size selection should be dynamic and should depend on

the past compliance of a DP in that area.

c) The inspection process of DPs and their service centers should be

automated through usage of appropriate technology. If such close

inspection / oversight modality is not possible directly by Depositories

through their own personnel, the possibility of outsourcing service

centre inspections may be explored, and a suitable outsourcing policy

may be framed.

ii. Delivery Instruction Slips (DIS) Issuance and Processing:

a) Appropriate infrastructure and other requirements, to facilitate scanning

and uploading of the DIS image, should be implemented at the DP’s

end and the depositories should put in place a suitable mechanism to

maintain a database of the scanned DIS.

b) DIS should be standardized across DPs to facilitate easy identification

and tracking of DIS issuance and processing.

c) The depositories should put in place systems such that all significant

DIS related information is available to them for off site inspections.

6. These recommendations were accepted and implemented vide SEBI circulars

dated February 07, 2014, January 21, 2014 and January 07, 2014.

Page 4 of 9

7. After submitting the interim report, the committee took up the issues relating to

assessment of existing policy framework of depositories, assessment of

depository system on the basis of CPSS-IOSCO Principles for Financial

Market Infrastructures, identification of areas for continuous improvement of

systems, procedures and practices and identification of systemically important

Market Infrastructure Institutions and their Inter-Linkages.

8. The committee held extensive discussions and deliberations with depositories

and other market participants related to the depository system. The committee

submitted its final report to SEBI on August 27, 2014. A summary of the

recommendations made by the committee in addition to the interim

recommendations given above is as follows:

A. Assessment of Existing Policy Framework of Depositories

Based on its review of the policy framework for depositories, the committee

recommended the following:

i. SEBI should ensure that the system and technology related requirements

which are verified prior to granting certificate for commencement of

business, are also maintained on an ongoing basis through regular

inspections and system audits.

ii. SEBI may put in place a mechanism so that depositories maintain

complete reconciled record of total issued and listed capital, including both

physical and dematerialized shares.

iii. Depositories are uniquely placed to scale up and utilize their infrastructure

to dematerialize not just securities but also other financial assets subject to

adequate regulatory framework and checks and balances being put in

place. The committee felt that this will promote the integration of the Indian

Page 5 of 9

Financial markets and allow the consumers greater access to and control

of a wide portfolio of financial assets.

iv. With greater integration of depositories with other financial service

providers, there is possibility of interconnectivity of depositories with

financial institutions/ FMIs/ international CSDs in future. Interconnectivity

may require standardization of messaging formats used by depositories.

The committee recommended that it may be desirable to standardize

messaging formats in the long term.

v. With regard to KYC, the committee noted that the e-KYC service launched

by Unique Identification Authority of India (UIDAI) has been accepted by

SEBI as valid process of KYC verification. The committee also informed

that NPCI has entered in to an MoU with UIDAI in order to aid financial

inclusion through Aadhaar enabled bank accounts and financial

transactions. The Committee recommended that use of e-KYC through

NPCI should be popularised among DPs.

B. Assessment of Depository System on the basis of relevant globally

accepted Principles for Financial Market Infrastructures so as to

benchmark with Global Best Practices.

The committee observed that while the Depositories are broadly compliant

with the CPSS-IOSCO principles for FMIs, certain areas needed to be

strengthened. In view of this, the committee recommended the following:

i. Risk Management Framework for depositories: FMI principles lay emphasis

on the need to have robust risk management framework to identify, monitor

and manage various risks emanating from multiple sources to its

operations.

The committee recommended that there should be a Board approved

policy providing for a well documented comprehensive risk management

Page 6 of 9

framework at both depositories. The risk management group/

committee formed by the depositories should be active and meet

periodically to continuously identify, evaluate and assess applicable risks in

depository system through various sources vis-à-vis investors complaints,

inspections, system audit etc. and suggest measures to mitigate risk

wherever applicable. A Chief Risk officer should be made responsible,

accountable, accessible & answerable to the board on overall risk

management issues.

ii. Orderly winding down of depositories: The Committee observed that there

is no laid down system or procedure for orderly winding up of depositories

in the event of potential scenarios such as voluntary winding up by

depositories, depositories going bust due to general business risk, fraud at

the end of depositories, or depositories wound up due to regulatory action

or court order. In Indian depository micro structure, there are two

depositories. In the event of failure, disruption or winding up of one

depository, all the demat accounts and securities held with stressed

depository can be potentially moved to another depository without affecting

the interest of investors. The committee recommended that there is a need

to have a well documented framework for orderly winding down of the

depository operations including making necessary legal provisions in the

regulations, rules and Depositories Act.

C. Identification of Areas for Continuous Improvement of Systems,

Procedures and Practices

The committee identified a few areas which needed further focus from the

perspective of maintaining a robust depository system. Based on its review

of these areas, the committee recommended the following:

i. In order to achieve wider financial inclusion and encourage participation of

investors from Tier II and Tier III towns in the securities market, the DPs

Page 7 of 9

need to widen their reach in these areas. For this purpose, there is a need

to devise an incentive structure for depository participants so that they

encourage investors to open demat accounts with them. In this regard, the

revenue source of depositories may be augmented and DPs may be

incentivized by having a revenue sharing mechanism between the

depositories and DPs which may encourage the DPs to expand their reach

in tier II & III towns. Bank DPs with their large branch network and wider

reach in the tier II & III towns can play a crucial role in furthering the

objectives of financial inclusion. DPs may be compensated for the cost

incurred in account opening, especially Basic Service Demat Accounts

(BSDA) as it will act as a motivator for DPs to open more accounts.

ii. The committee recommended that SEBI may review the quantum of funds

required to be transferred to IPF by depositories and arrive upon a sizable

limit for corpus of IPF. Only profits from depository operations may be

transferred to IPF. SEBI may also formulate an Investment Policy for the

IPF. The funds of the IPF may be utilized for conducting Investor

Awareness and Education Programmes and supporting the depositories'/

DP's initiatives for financial inclusion in a variety of ways.

iii. The committee noted that certain DPs allow the promoters of companies to

use tripartite agreements usually referred to as Non-Disposal Agreement/

Non-Disposal Undertaking (NDU) to extend facilities to its clients for

lending / borrowing of shares instead of following the pledging facility

available in the depository system. The committee recommended that DPs

should not be party to such arrangements as there is no regulatory

mechanism whereby depositories and DPs can treat shares covered by

NDU as pledged / encumbered, leading to potential for fraud and multiple

pledging.

iv. In the area of outsourcing by Depositories, there is a need for further focus

and strengthening of guidelines on the lines given below:

Page 8 of 9

a) Care should be exercised while outsourcing and wherever possible

depositories should put in place various controls to ensure that there is

check on the activities of outsourced entity especially to monitor that

outsourced activities are not further outsourced downstream.

b) Core and critical activities of depositories should not be outsourced.

c) Core IT support infrastructure / activities for running the core activities

of depositories to the possible extent should not be outsourced.

d) Wherever outsourcing is allowed, depositories should ensure that risk

impact analysis is undertaken, only reputed entity having proven high

delivery standards are selected, appropriate back up / restoration

system are put in place, monitor and have checks and over all controls

over the outsourced entity on real time basis.

e) Audit of implementation of risk assessment and mitigation measures

listed in the outsourcing policy document and outsourcing agreement/

service level agreements pertaining to IT systems should form part of

System Audit of Depositories.

D. Identification of Systemically Important Market Infrastructure

Institutions and their Inter-Linkages

In view of transformation of securities market infrastructure brought about

by advances in information technology (IT) and dependence of Financial

Market Infrastructure Institutions on technology, the committee examined

the technology infrastructure of the Depositories and reviewed the usage of

technology in the Depository system. The committee recommended the

following:

i. The IT infrastructure deployed should have high availability and no single

point of failure. In the event of failure of any sub-system or component

or software the resultant solution has to work, may be with

acceptable levels of degraded performance, and the corrective mechanism

put in place to ensure that the rectification takes place within 4 hours. The

Page 9 of 9

DPs have to put in place appropriate mechanisms in order to ensure no

compromise to data integrity and transaction integrity.

ii. Depositories should take steps to ensure that the IT Infrastructure of DPs

has high availability and fault tolerance, uptime guarantee of 99.5%

measured on a monthly basis with mean time to restore (MTTR) of not

more than 4 hrs, data integrity and transaction integrity and appropriate

security access and control framework.

9. The committee has categorised its recommendations as short term, medium,

term and long term goals. A copy of the final report is annexed to the Board

memorandum for perusal (Annexure B).

10. The Report of the Depository System Review Committee is placed before the

Board for its consideration. The Board is requested to take note of the interim

recommendations of the committee which have been implemented by SEBI as

stated at para 6 and to authorise Chairman to take necessary action on the

basis of the final report as deemed appropriate.

Interim Report of the Depository System Review Committee

Page 1 of 61

Annexure A

Interim Report of the Depository System Review Committee

Interim Report of the Depository System Review Committee

Page 2 of 61

Contents

Executive Summary .............................................................................................................................................. 3

Preamble and Introduction ............................................................................................................................... 9

Oversight and Inspection Framework ........................................................................................................ 16

Risk Modeling and DP rating .......................................................................................................................... 25

DIS issuance & processing ............................................................................................................................... 46

IT Governance ...................................................................................................................................................... 50

Technology Enabled Future Road Map ....................................................................................................... 58

Interim Report of the Depository System Review Committee

Page 3 of 61

Executive Summary

The introduction of Depository System has been instrumental in eliminating various drawbacks in

handling of physical share securities in terms of problems related to transfer of shares, bad deliveries,

loss of share certificates etc. and it enabled fast and efficient settlement (T+2 settlement cycle).

Technology has been a major driver in ushering this electronic revolution in securities markets, thereby,

making securities markets more in sync with the fast changing technological environment. This, in

tandem with the dynamic nature of securities markets, presents challenges before Regulators in

maintaining orderly development of securities markets and also to protect the interest of investors.

Over the years, SEBI as a regulatory body has responded by tightening of the regulatory framework of

Depositories consisting of Regulations, circulars issued by SEBI, byelaws and circulars of the

Depositories, etc. However, there had emerged inadequacies in the systems which were misused by

certain market participants for their benefit, which led to an examination and order by a two member

committee of SEBI in 2009, which inter-alia recommended review of the depository system through an

independent body of experts.

Therefore, a Depository System Review Committee (DSRC) was constituted on June 25, 2012 under the

Chairmanship of Mr. M. Balachandran (former CMD of Bank of India) along with Prof H.Krishnamurthy

(IISc Bangalore), Mr.R.S.Loona (Ex ED SEBI), Prof Vikram Kuriyan (ISB) as members to undertake a

comprehensive review of the Indian Depository System and to benchmark against global best practices.

The committee while reviewing the system as a first measure examined

I. Inspection and Oversight

a. The oversight over the depository’s functioning including the inspection of DPs by them.

b. Inspection of depositories by SEBI

II. Risk Model and rating of DPs

III. DIS issuance & processing

IV. IT Governance

The DSRC while examining the inspection system & processes observed that the matter would need to

be looked at from two angles, viz:

A. inspection of DPs by Depositories and

B. oversight by SEBI on the functioning of Depositories and their operational control of DPs

Therefore, a sub-committee was formed comprising Prof. Krishnamurthy (DSRC Member),

representatives of NSDL and CDSL, and officials of SEBI Market Regulation Department - Division of

Market Supervision to look into aforementioned issues, review the current inspection process of the

Depositories and to frame comprehensive inspection guidelines.

The Committee noted a major change in many countries in the move from rule based supervision to

principle based supervision. Developed countries like the U.K. (A.R.R.O.W.), Singapore (C.R.A.F.T.) and

Interim Report of the Depository System Review Committee

Page 4 of 61

emerging markets like Malaysia, Thailand, China, South Africa, and Taiwan follow a risk based inspection

methodology. Thereby, enhancing the need to move from compliance based oversight & inspection

towards risk based oversight & inspection. This report discusses the need for inspections to be efficient

and effective by being more focused on risk assessment. In order to be more effective, the inspection

focus needs to be dynamic, keeping in view the changing risk profile, technological advancements and

innovations in products and market structure.

A) The committee observed that the inspection of DPs by Depositories is done as a routine annual

exercise which mainly focuses on compliance. Light monetary penalties are imposed in cases where non-

compliance / deviations are observed. Therefore, it was felt by the committee that inspection

techniques and methods should be reviewed based on thorough understanding of potential failure

modes and inspection should be made risk based. Further, DPs should be classified into risk buckets with

appropriate risk weights for the purpose of rating of DPs and an integrated risk model be developed.

In the aftermath of the financial crisis, wherein Financial Stability Board (FSB) and the G20 Leaders

identified the need for more intense and effective supervision particularly to systemically important

financial institutions (SIFIs) as weak risk controls at financial institutions are still being witnessed.

Further, sharing of information regarding all activities undertaken by SIFIs regulated by various

authorities need to be encouraged for improvement in supervision to ensure that it is effective,

proactive and outcomes-focused.

One of the key risks identified is operational risk, which is more dynamic in view of technological

changes, information security, systemic risk, newer products being offered and increase in sophistication

of institutions. Therefore, in the context of depositories, risk based inspection must focus more on

operational risk especially the aspects like business continuity and information security.

Since the resources available with regulators are relatively limited, the main responsibility of risk

assessment and mitigation would rest with the depositories and their participants through internal

audit, risk management and compliance. However, risk based inspections would address this through

deploying limited resources to the riskiest institutions and areas, prioritized based on an assessment of

the risks therein. As such, inspection approaches and areas of focus need to be periodically reviewed to

confirm that, for instance, institutions and areas previously classified as “low or moderate risk” still

warrant this assessment.

Effective inspection requires finding the right balance between focusing on areas of higher risk while

also ensuring some periodic coverage of all aspects, including, for example, those that might prove risky.

Striking the right balance is an ongoing challenge; however, regulatory developments should allow

inspectors to explore and leverage off deeper information sets and analysis. This includes the

information that can be made available from depositories and other centralized sources of data, and

information from implementation of recovery and resolution plans which provide supervisors with new

insights. This, therefore, puts technology into perspective and hence the need for increased use of

technology based inspections.

Interim Report of the Depository System Review Committee

Page 5 of 61

The committee felt that in a risk based inspection framework, identification of various sources of risks in

the system will be critical and quantification of same will enable effective monitoring of participants. For

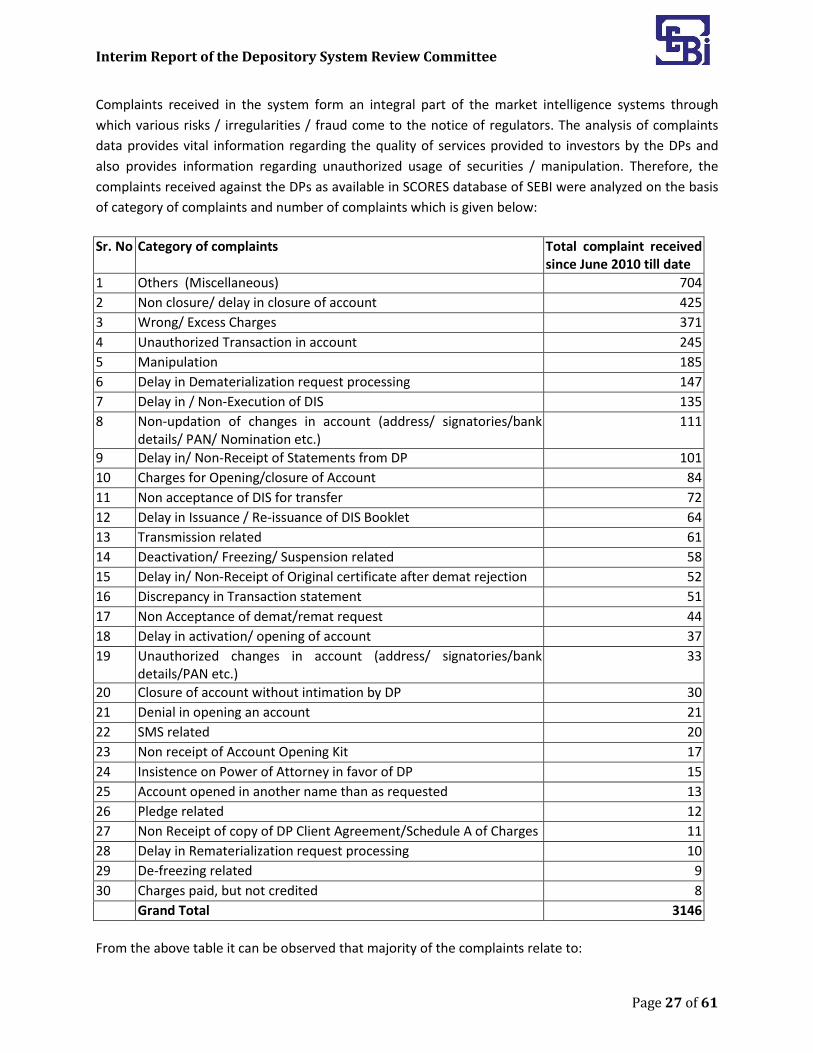

assessing the quantitative factors, one of the parameters is complaints received against DPs as this data

provides vital information regarding the quality of services provided to investors by the DPs and also

provides information regarding unauthorized usage of securities / manipulation if any. Further, non-

compliances (number of violations) observed during inspection of DPs is also another parameter which

can be quantified. However, there could also be various unquantifiable risks which can be covered

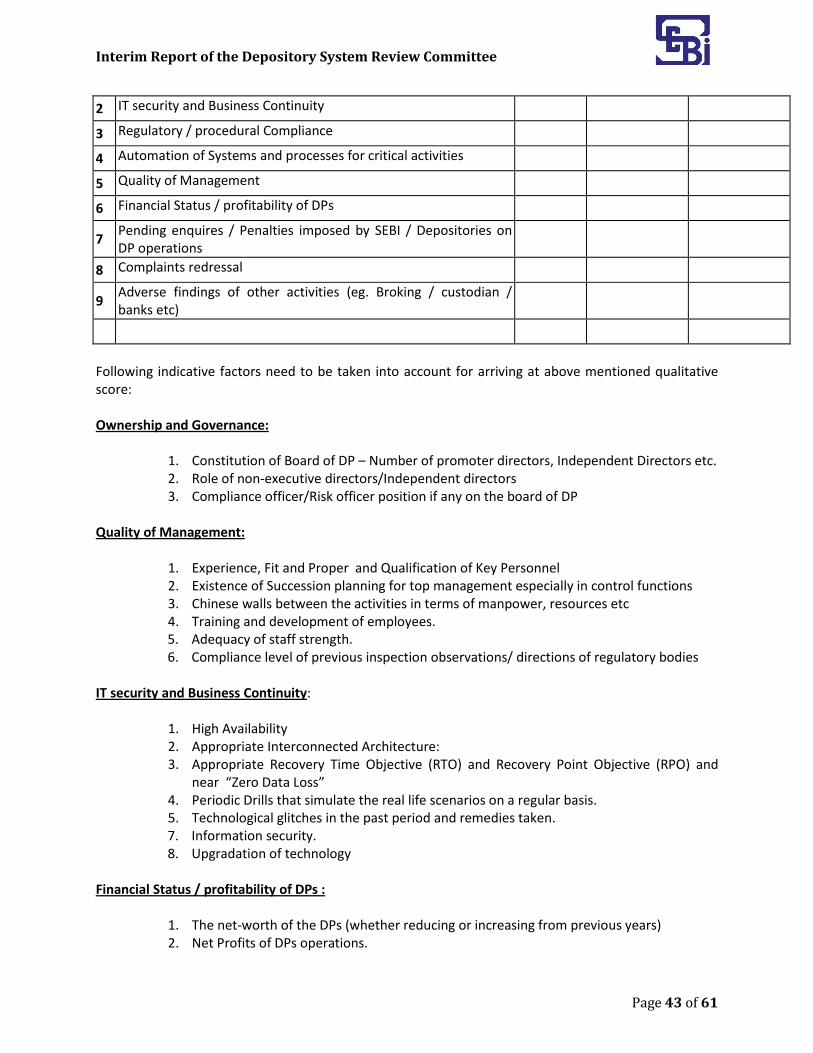

through qualitative factors. The qualitative factors includes governance in terms of corporate as well as

IT governance, management quality & capacity, reputation & goodwill, efficiency & economy of services

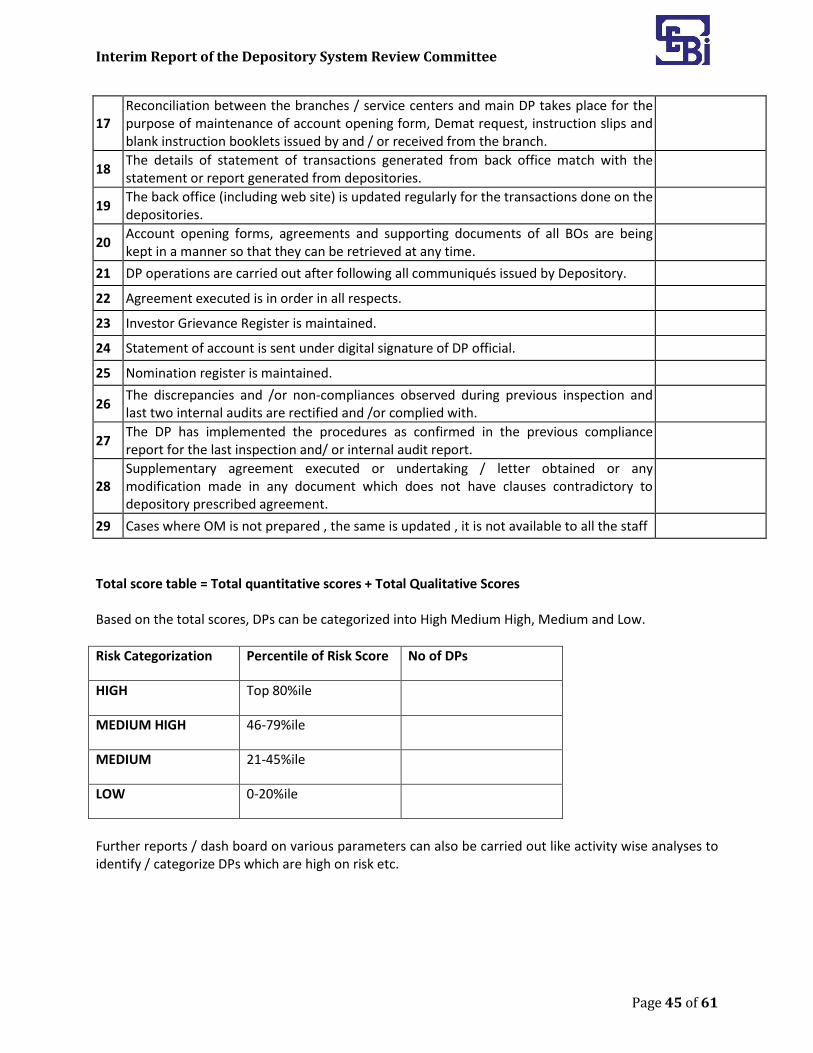

rendered, etc. Therefore committee felt the need to have weighted average risk model to include both

quantitative factors and qualitative factors to objectively assess and measure the risk profile of the DPs

and categorize them into various Risk Buckets viz. high, medium, low. This bucketing will allow the

Depositories to allocate more resources to high risk and non-compliant DPs and focus relatively less on

low risk DPs.

The interim report of the DSRC covers the current inspection process and practices by Depositories

and the recommendations of the committee on the same and IT Governance of Depositories and DPs

and best practices for DIS and future roadmap for strengthening the system.

In summary, while risks and dynamicity has increased in the system, the inspection system has remained

rooted to compliance based. Therefore, the need for risk based inspection and an integrated risk model

and moving towards oversight and inspection regimen enabled by technology based methods and tools.

To accomplish this objective, the report prescribes through the recommendations an inspection

framework based on risk assessment, which comprises of inspection guidelines, quantitative risk model

and bucketing and enhanced use of technology for effective supervision.

List of Recommendations

I. Inspection and Oversight

1. Inspection of Depositories by SEBI

The objectives of the inspection of depositories by SEBI are broadly to examine whether the

procedures and practices of the depository are in compliance with the Depositories Act,

1996, SEBI (Depositories and Participants) Regulations, 1996, SEBI circulars, the bye-laws

etc. This involves examining whether the processes, operations and systems are in

accordance with SEBI (Depository and Participants) Regulations, 1996; look into the

complaints redressal mechanism of the depository, assess whether the IT infrastructure

Including its security system are adequate with suitable business continuity arrangements,

checking the compliance level of the previous inspection findings.

Depositories should be inspected on an annual basis

Interim Report of the Depository System Review Committee

Page 6 of 61

SEBI should examine the information received through Monthly Development Reports

(MDRs) on a regular basis and capture from various angles the deficiencies in the

functioning of Depositories and DPs and convey their observations to the Depositories,

especially on the latter’s findings of the inspection of DPs.

SEBI should revamp and then examine the information received through Monthly

Development Reports (MDRs) on a regular basis and SEBI should analyze the MDRs and

convey their observations / comments to the Depositories, specifically on findings of

the inspection of DPs.

The SEBI's inspection of the Depositories should ensure that the critical observations of

SEBI’s Inspection of DPs are reflected in the critical observations of the DP inspection by

depositories.

There should be an annual interface between SEBI and Depositories to review

comprehensively and deliberate on the inspection findings on the DPs and areas of

repeat violations, non compliance, and overall status of rectification.

2. Inspection of Depository Participants by Depositories

The inspection techniques and methods should be reviewed based on thorough

understanding of potential failure modes

Consolidated / integrated risk based inspection framework for joint inspection

of DPs which are registered on both depositories and have large number of BO

accounts and custody value should be introduced.

There should be disclosures in the annual report of depositories regarding

inspections conducted and various actions taken pursuant to inspections

In order to assess the effectiveness of inspection methodology of the

depositories, the critical observations of SEBI noted during its inspection of DPs

should be communicated to depositories so as to counter check and verify

whether finding of the depository and SEBI are broadly in sync with each other.

Inspections should be risk based rather than compliance based to provide economic

benefits such as fewer inspections for less risky participants and frequent inspections for

more risky ones. The inspection reports should not only identify risk areas but should

also proactively suggest risk mitigation.

The sample size selection should be dynamic and should depend on the past compliance

of a DP in that area.

The inspection process of DPs and their service centers should be automated through

usage of appropriate technology. If such close inspection / oversight modality is not

possible directly by Depositories through their own personnel, the possibility of

outsourcing service centre inspections may be explored, and a suitable outsourcing

policy may be framed.

II. Risk Model and Rating of DPs

Interim Report of the Depository System Review Committee

Page 7 of 61

Committee recommended a weighted average risk model on quantitative and qualitative

factors to arrive at a risk score and thereafter categorize the DPs into various Risk Buckets

viz. high, medium, low. This bucketing will allow the Depositories to pay more attention and

allocate more resources to high risk and non-compliant DPs and focus relatively less on low

risk DPs. The parameters on which risk score is assigned are as follows:

Past Inspection findings, a good compliance record indicates a low risk profile and hence

will result into a low Risk Score; alternatively, a non compliant DP will be assigned a high

risk score. Repetitive violations of the same kind result into a higher risk score being

assigned to the DP.

The complaints received against the DP by various entities

The size of the DP

The Nature of the DP viz. stock broker, Bank DP will result into a different score being

assigned to the DP in conjunction with the above parameters, as different

III. DIS issuance & processing:

Standardization of DIS across Depositories will facilitate easy identification and tracking

of DIS issuance and processing. Further, it will also ensure that issue of loose slips at the

end of DP will also be monitored and regulated. The depositories should revise their

EOD reporting requirements / structure such that all significant information relevant for

their inspections available in the back office of DP should also be available with them.

The appropriate infrastructure and other requirements to facilitate scanning and

uploading of the DIS image should be implemented at the DP’s end and the Depositories

should put in place a suitable mechanism to maintain a database of the scanned DIS and

use it for easing the inspection process within a timeframe of 6 months.

Truncated image of DIS captured at branches / service centers of DPs should be

accessed and available to Depositories directly for effective monitoring of the

transactions from a market surveillance perspective.

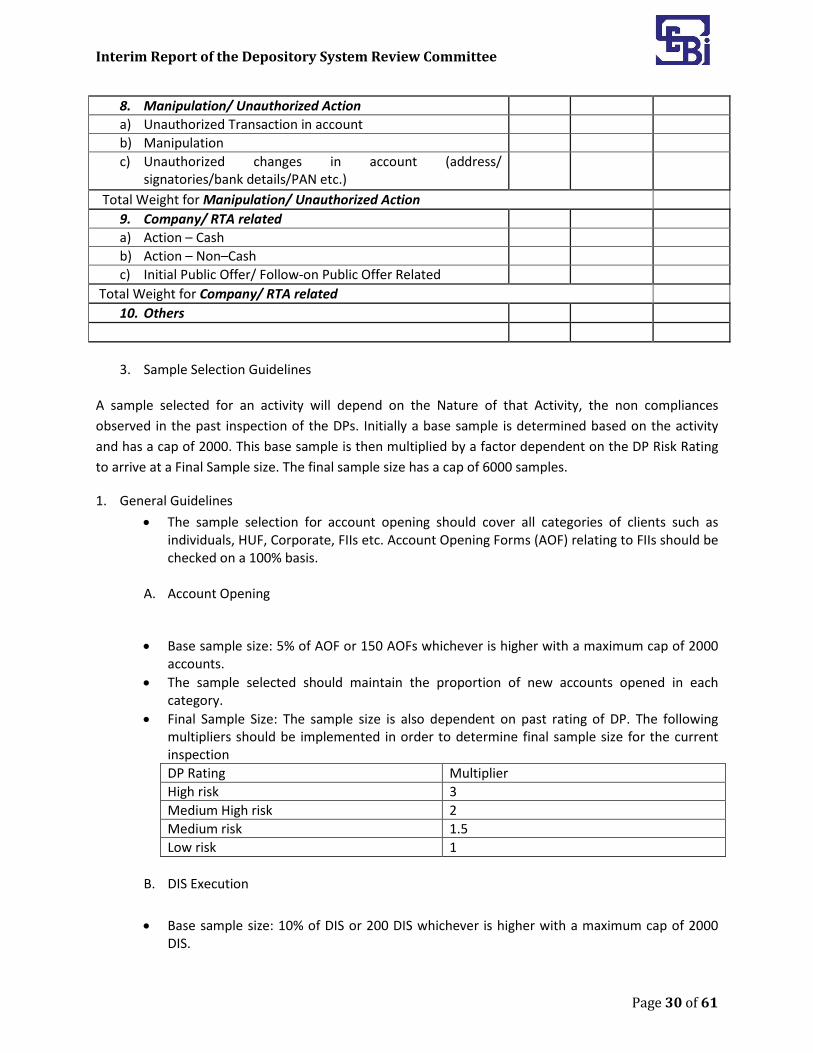

IV. Sample Selection Guidelines

The sample size for each activity will range from minimum of 2,000 samples to

maximum 6,000 samples. Sample selection shall be adaptive by taking into

consideration various risk parameters for following activities and dynamically adjusted

depending on the risk rating of DP.

Account opening

DIS execution

Investor complaints

Demat / Remat / Pledge / Unpledged

Client master Changes Samples and other miscellaneous areas

Interim Report of the Depository System Review Committee

Page 8 of 61

V. IT Governance and Internal Audit

The inspection process should ensure verification of the following:

o The depositories and their DPs should have an approved IT strategy / plan document

which needs to be reviewed annually.

o A System Audit framework should be prescribed for DPs.

o Create an IT Steering committee to assist the IT Strategy Committee in implementation

of IT strategy.

o Information Security policy should be approved by the boards and reviewed annually

o Create an office of information security and designate a senior official as Chief

Information Security Officer (CISO) whose work would be to assess risk and identify the

threat/ vulnerabilities.

o In the event of disaster, there should be no disruption in services and in case there is a

disruption, there should be near zero data loss

o Designate a senior official as Head of BCP function

o Increased use of technology so as to ensure effective off site inspections of DPs and

their branches and service centers

o The subcommittee also desired to enhance the efficacy of internal audit of DPs and

towards accomplishing the objective suggested that :

Areas for concurrent audit to include high risk areas such as account opening

and modification, issuance and execution of DIS, investor grievance redressal,

POA modifications, etc.

Review scope and format of reports of Internal Audit

Software utilities to identify data entry errors

Insurance coverage

Periodicity of Inspection of new participants

People carrying out Inspection of DPs

Capital Adequacy

Annual system audit and Comprehensive BCP/DR guidelines

Interim Report of the Depository System Review Committee

Page 9 of 61

Preamble and Introduction

The enactment of Depositories Act in August 1996 paved the way for introduction of Depository system

in India. India has adopted Dematerialization system wherein by operation of law, physical shares

certificate is replaced with shares in electronic form. In the books of company, depository is the

registered owner and depository in turn maintains electronic ledger of the securities wherein movement

of securities from one account to another are recorded and maintained to ascertain the beneficial

owners. In the year 1996, National Securities Depository Limited (NSDL) was the first depository to be

established in India followed by Central Securities Depository Limited (CDSL) in the year 1999.

Introduction of Depository system has eliminated various drawbacks in handling of physical securities in

terms of problems related to transfer of shares, bad deliveries, loss of share certificates etc. and enabled

fast and efficient settlement. The Depositories Act 1996 and SEBI (Depositories and Participants)

Regulation 1996 form the backbone of the regulatory framework for depositories and depository

participants.

In the depository system, the depositories provide various services to investors / clients through their

agents i.e. depository participants. The broad services provided by these participants are as follows:

Account opening

Demat / Remat

Other services such as PoA, pledge / un pledge, transmission, freeze / unfreeze, etc.

Inter-depository transfers

Transactions / transfers - pay in, payout, early pay in, etc.

A snapshot1 of the Indian Depository System is as under:

Sr. No.

Types of DPs

CDSL NSDL

DPs BOs Custody Value (in Rs. Cr.)

DPs BOs Custody Value (in Rs. Cr.)

1 Banks 35 5,94,900 3,23,946 53 48,74,899 42,13,576

2 Custodians 11 63,207 4,45,251 6 6,99,702 26,24,861

3 Stock Brokers 506 72,71,775 2,45,498 212 68,62,581 9,31,791

4 Clearing Corporations 17 2,17,794 11,854 8 667 630

5 Others (RTA and NBFC) 6 3,157 2,237 4 63,376 48,738

6 Total 575 81,50,833 10,28,786 283 1,25,01,225 78,19,596

From the above table, it is noted that stock broker DPs hold maximum number of BO accounts whereas Bank DPs hold maximum in terms of custody value. Going forward and with financial inclusion initiative kicking in, it is envisaged that Bank DPs will play a substantial role in expanding the DP footprint to the new areas and segments of investors.

1 For the month ending November 2012

Interim Report of the Depository System Review Committee

Page 10 of 61

The different type of instruments along with their dematerialized custody value is as under:

Number of ISINs:

Type of Instrument

No. of ISINs at the end

of the month

(30/11/2012)

Demat Custody value as

on 30/11/2012 (Figures in

Rs. Cr)

Equity shares # 15,140 58,69,602

a. Listed 10,947 56,27,720

b. Unlisted 4,193 2,41,882

Preference shares 969 50,633

Debts # 14,735 11,92,099

a. Listed 6,514 10,27,578

b. Unlisted 8,221 1,64,521

Mutual Fund Units 7,402 17,976

Others 18,148 6,89,286

Total 56,394 78,19,596

From the above table it can be inferred that other instruments apart from equity will increase the choice

for investors and the demat custody value for such instruments will see an increase in the future.

Over a period of time, there had emerged inadequacies in the system which has been taken advantage,

sometimes wrongly, by the market participants for their benefit. SEBI noticed such inadequacies when

its surveillance system observed large scale off market transfers prior to the date of listing which upon

detailed analysis indicated that thousands of fictitious / benami demat accounts were fraudulently

opened by certain operators who ultimately used these demat accounts for cornering of shares in

various IPOs. Further, in another matter SEBI had observed that one of the depositories had failed to

exercise due diligence at the time of dematerialization of DSQ shares which lead to trading of unlisted

shares on stock exchanges. In this connection, SEBI had reviewed the operations of Depositories and the

following observations were made:

1. Adequacy of Bye laws on internal monitoring, review and control process - The adequacy of Bye

laws of Depositories should be assessed through independent experts

2. Audit System – No specific comments on the adequacy of audit system or audit process.

3. Supervision – Lack of an effective supervisory mechanism or if the mechanism was adequate the

failure to operate it effectively, and the consequent failure to prevent, detect and remedy

fraudulent transactions in dematerialized accounts. The system needs to be reviewed by

independent experts to develop revamped and strengthened supervisory system to proactively

anticipate and prevent fraudulent activity and safe guard the integrity of the systems.

4. Inspection – The inspections of DPs failed to detect the large scale fraud illustrating the inherent

weakness of the systems, procedures and practices in conducting inspections. It was felt

prudent to review the inspection system using suitable independent experts to develop a

Interim Report of the Depository System Review Committee

Page 11 of 61

revamped and strengthened inspection system to proactively anticipate and prevent fraudulent

activity and safe guard the integrity of the systems.

5. Data Reliability – The system established and operated was not adequately strong in

safeguarding the reliability of the data uploaded into it.

6. Sanctions and penalties – A consistent approach has not been taken on the issue of sanctions for

various types of violations and the basis for differentiation of approach is less than clear which is

not conducive for orderly development of the market. Urgent action was required to be taken to

review existing policy and practice and develop a clear, rational and transparent policy

framework on sanctions and penalties.

7. Lack of Physical Verification of DP applicants - Given the crucial role of DPs in the depositories

system, ordinary prudence and due diligence required that depository should have at a

minimum, physically inspected DP applicants before approving their status and that mere

reliance on third party certification is neither adequate nor justifiable.

8. KYC system and implementation – The staff of the DP only should carry out in-person

verification. The DP should not outsource or assign the activity of in-person verification to an

outside agency.

9. Introduction of a correspondence address field – No adverse comments.

10. Allowing use of Agents to open accounts – No adverse comments.

In light of the above observations, to ensure that the operations were conducted in better compliance

the system was revamped. The Depositories and DPs subject themselves to independent audit

conducted on the following operations to assess whether they are adequate to ensure the integrity of

the overall depository system and the securities market:

1. Selection of DPs

2. Opening and operation of Depository accounts including the KYC system

3. Audit

4. Supervision

5. Inspection

6. Penalties and Sanctions.

Pursuant to the various inadequacies observed in the depository system, the depositories in

consultation with SEBI, to remedy the shortcomings, took various steps which are as under:

1. Strengthening of KYC Norms:

a. Verification of the identity and address of the beneficial owners.

b. PAN made mandatory for opening of dematerialized accounts.

c. In-person verification of the applicants by staff of the DP at the time of account opening.

d. Mandatory 100% verification of the account opening documents by the Concurrent

Auditor.

e. KYC non complaint accounts frozen till compliance are ensured.

Interim Report of the Depository System Review Committee

Page 12 of 61

2. Audit procedures and System Audit:

a. DPs have to conduct internal and concurrent audit programs as part of their risk

mitigation measures.

b. The Depositories were mandated to subject themselves to comprehensive system audit

on annual basis and place the report along with compliance status before the Governing

Board of depositories before forwarding the same to SEBI.

c. The depositories were advised to review the scope and format of reports of Internal

Audit on half yearly basis.

d. The depositories were advised to submit the report as well as certificate of the internal

auditor to SEBI certifying effective implementation of adequate internal control

procedures and operational control

3. Improving disclosures and Surveillance:

a. Information regarding details of dematerialization, re-materialization, and off-market

transaction were mandated to be disseminated on websites of Depositories.

b. Examination of off-market transfer of IPO shares where many (five or more)

dematerialized account holders make off market transfers to a target account.

c. De-dupe Software were developed to identify and stop multiple demat accounts being

opened with the same or similar PAN, bank account and MICR code

d. ISIN of companies issuing shares (IPOs) are activated only on the day of commencement

of trading.

e. Software utilities were developed and installed to identify and prevent data entry

errors.

f. Identifying frozen demat accounts receiving IPO credits

g. The ISIN of the companies issuing shares by way of Initial Public Offer frozen for debits

and credits while crediting the shares and the ISIN reactivated on the day of

commencement of trading on the stock exchanges.

h. SMS alert facility to the investors was introduced for debits, credits and various changes

such as address change, etc., in the demat accounts.

i. Monitoring of Minor BO accounts

j. An independent surveillance cell formed to coordinate the surveillance activities with

SEBI, FIU-India and other investigating agencies

k. Concurrent audit to include high risk areas such as account opening and modification,

issuance and execution of DIS, investor grievance redressal, POA execution and

modifications, etc.

4. Strengthening of the Regulatory Framework for Depositories:

a. Review of completeness of bye-laws and procedure for monitoring given the evolving

nature of DP operations.

b. Enhanced insurance cover with facility for free reinstatement and automatic

reinstatement of sum insured

5. Penalties and Sanctions:

a. The penalty structure was made uniform at both the depositories.

Interim Report of the Depository System Review Committee

Page 13 of 61

6. Inspection of DPs

a. Both the Depositories viz NSDL & CDSL had carried out a special review of their

inspection function/ system & procedures by an external auditor and accordingly

updated / framed their manual for conducting inspection of their participants based on

the inputs of respective auditor.

b. The depositories to update their Operations cum Manual Process Flow for Inspection of

Participant every quarter

c. Both depositories to follow a common sampling plan for carrying out inspection.

d. Conduct inspection of new DP within a limited time frame (say 6 months) to provide

guidance.

Subsequently, while disposing the matter of NSDL, the SEBI Board observed in its order

(BOARD/SEBI/1/2010) dated February 02, 2010 that"...there is scope for continuous improvement of

systems, procedures and practices in conducting inspections, The systems need to be reviewed by

suitable independent experts and a comprehensive and strengthened inspection system needs to be

developed and put in place. Such a review can, inter alia, include the issue of further use of technology

for preventing or alerting to the possibility of fictitious accounts - a cardinal issue in the integrity of

financial systems."

In light of various observations made by a two member committee appointed earlier in 2008, on the

functioning of depositories, SEBI Board in its meeting held on July 28, 2011 decided that the "Depository

system " be reviewed by an independent expert group on the basis of CPSS-IOSCO principles.

Accordingly, Depository System Review Committee (DSRC) was constituted on July 15, 2012 under the

Chairmanship of Mr. M. Balachandran to undertake a comprehensive review of the Indian Depository

system.

The terms of reference of the committee are:

a) Overall assessment / adequacy of existing depository framework and identify areas for review.

b) Assessment of depository system on the basis of relevant CPSS-IOSCO principles, recommendations

of CESR-ECB pertaining to Central Securities Depositories (CSDs) so as benchmark with the global

best practices.

c) Identify areas for continuous improvement of systems, procedures and practices and make

recommendations thereof.

d) Identify systemically important market infrastructure providers / institutions / depository

participants and their inter-linkages and identify areas and suggest safeguards to prevent single

point failures and denial of depository service.

e) Review existing system of inspection by depositories and suggest changes to strengthen monitoring

/ oversight of depository participants.

The first meeting of the committee was held on August 14, 2012 and the committee has held five

meetings so far. The committee decided that the existing systems, procedures and process be studied so

as to identify deficiencies, inadequacies, cost efficiency and scope for providing better services to

Interim Report of the Depository System Review Committee

Page 14 of 61

investors. Further it was also felt a study of depository systems in international jurisdictions could be

helpful so as to understand and indentify best practices which may deserve to be introduced in Indian

context. In the mean time the committee took up an appraisal to understand the overall operations and

activities of Indian depositories, and therefore committee visited CDSL and NSDL and had detailed

discussions with the top management team of both depositories.

Based on their initial observations of the functioning and assessment of potential risks in the system, the

committee, as a first in the agenda, took up the issue of Inspection of Depositories and the DPs by

depositories for examination. DPs being the agents of Depositories act as touch points for the customers

on behalf of depositories and the various services of the depositories are rendered indirectly through

these participants. Therefore, an effective oversight of these participants is a critical obligation of

depositories. Inspection is one of the effective means of oversight and supervision and helps in

identifying inadequacies and risks in the system. Further, it can also help the depositories to ensure

compliance and adherence to the recommendations of CPSS-IOSCO. The relevant recommendations

whose adherence can be directly assessed by inspection are as under:

Operational Reliability - identification & mitigation of operational risks through proper systems,

controls and procedures that ensure reliability, security and scalability.

Protection of Customers' Securities - Accounting practices and safekeeping procedures to fully

protect customers' securities including protection against claims of a custodian's creditors

Governance - Arrangements to fulfill requirements for public interest and promote the

objectives of owners and users

Efficiency - The systems should be efficient w.r.t. safe and secure operations in a cost effective

manner

Transparency - Proper information to be provided to the customers to help them in identifying

and evaluating risks and costs associated with the services rendered

Regulation & oversight - transparent and effective regulation and oversight with clear defined

roles and responsibilities.

The depositories are mandated by SEBI to inspect their participants on an annual basis. The depositories

conduct these inspections through an in-house team with a gap of around a year between two

inspections of the same DP. Currently a spreadsheet based system is used by depositories to

individually take information / data from databases through reports and then used for determination of

samples / adaptive samples. Since sample size and sample selection are critical pre-inspection activities

which requires sifting of data and analysis, use of proper technology can be a catalytic enabler in arriving

at an appropriate sample and its size which truly represents the criticality and risks associated with a

particular activity. Further, technology can be used in the archiving and record keeping of various

inspection findings to help prepare an appropriate integrated risk model which can quantify risks leading

to risk bucketing of DPs for efficient and effective regulation and oversight.

Interim Report of the Depository System Review Committee

Page 15 of 61

Against the aforesaid background, the committee desired to provide immediate attention to the

following issues:

1. Whether Inspections should be risk based rather than compliance based to provide economic

benefits such as fewer inspections for less risky participants and frequent inspections for more

risky ones.

2. Whether the inspection techniques and methods should be reviewed based on thorough

understanding of potential failure modes

3. Whether the inspection process of DPs and their service centers should be automated through

usage of appropriate technology for the following purpose:

a. to Make it more quality oriented and less labour intensive so as to enhance the productivity of inspection process

b. To Safeguard integrity of data and reduce the risk of failure. c. to Reduce inspection and maintenance costs without compromising integrity and

reliability of samples collected d. to Offer a flexible technique to continuously improve and adapt to changing

environment 4. Whether DPs should be classified into risk buckets with appropriate risk weights for the purpose

of rating of DPs.

In order to address the above issues, review the current inspection process of the Depositories, and to

frame comprehensive inspection guidelines, the DSRC formed a sub-committee consisting of Prof.

Krishnamurthy (DSRC Member), representatives of NSDL and CDSL, and officials of SEBI Market

Regulation Department - Division of Market Supervision. The findings and suggestions of the

subcommittee are incorporated in this report.

Interim Report of the Depository System Review Committee

Page 16 of 61

Oversight and Inspection Framework

The enactment of SEBI Act, 1992 bestows upon SEBI, the responsibility of protecting the interests of

investors in securities and to promote the development of, and to regulate, the securities markets and

for matters connected therewith or incidental thereto. Further, the enactment of Depositories Act, 1996

provides for regulation of depositories in securities and for matters connected therewith or incidental

thereto.

The statutory provisions in the SEBI Act (Sections 11 and 11B) and the Depositories Act (Section 19)

confer powers and responsibilities on SEBI to achieve the objectives of the abovementioned laws i.e. to

protect the interests of investors and safeguard the orderly development of the securities market.

These provisions cover all “persons” who fall within Section 12 of the SEBI Act, including depositories.

Section 19(ii) of the Depositories Act empowers SEBI “to prevent the affairs of any depository or

participant (DP) being conducted in the manner detrimental to the interest of the investors and

securities market.” The responsibility for conducting its affairs in a manner not detrimental to the

interest of investors of the securities market thus lies on each depository/ DP and SEBI has the duty to

prevent or correct any failure on the part of depositories / DPs to fulfill this obligation.

The above statutory responsibility is reflected in regulatory provisions such as the following:

Section 26 of the Depositories Act, 1996 requires depositories to frame bye laws which may

inter-alia provide for…….

(i) The procedure for ensuring safeguards to protect the interest of the participants and

beneficial owners,

(ii) The internal control standards including procedure for auditing reviewing and monitoring.”

Regulation 34 of the Securities and Exchange Board of India (Depositories and Participants)

Regulations, 1996 (hereinafter referred to as “Depositories Regulation”), provides that “every

depository shall have adequate mechanisms for the purpose of reviewing, monitoring and

evaluating the depository’s controls systems, procedures and safeguards.”

Regulation 35 of the Depositories Regulation provides that “every depository shall cause an

inspection of its controls, systems, procedures and safeguards to be carried out annually and

forward a copy of the report to the Board.”

Regulation 59 of the Depositories Regulations provides that SEBI may appoint one or more

persons as inspecting officers to undertake inspection of the books of account, records,

documents and infrastructure, systems and procedures, or to investigate the affairs of a

depository, participant, beneficial owner, an issuer or its agent for any of the purposes specified

therein.

These provisions show the extensive authority and responsibility given to depositories to carry out

inspection in an intensive manner to prevent and detect system and operational failures and fraudulent

transactions. Further, SEBI Act and Depositories Act, in the interest of investors, empowers SEBI to inter-

Interim Report of the Depository System Review Committee

Page 17 of 61

alia inspect into the affairs of a depository or a participant. Depositories are also mandated to monitor

and supervise their DPs regularly so as to ensure that apart from potential fraud / irregularities

detection, various services rendered to investors are effectively and efficiently delivered by participants

in a cost effective manner.

The criticality of effective supervision through inspection came to the fore when IPO irregularities and

inadequacies of Depository Systems in the matter of dematerialization of DSQ shares were found and

the two member committee (Dr Mohan Gopal and Shri Leeladhar) formed to look into the said issues

observed that the inspections by depositories had failed to detect the fraud illustrating the inherent

weakness of the systems, procedures and practices in conducting inspections. The committee,

therefore, recommended review of the inspection system using suitable independent expert to develop

a revamped and strengthened inspection system.

Current Inspection Framework

The current inspection framework at the end of SEBI and depositories are as mentioned below.

Inspection of Depositories by SEBI

As per the inspection policy of SEBI, depositories are inspected annually. SEBI has clearly laid down

inspection manual approved by the Whole Time Member of SEBI which is updated on a regular basis.

Besides annual comprehensive inspections, SEBI also conducts specific purpose inspections.

The objectives of the inspection of depositories are broadly to:

a) Examine whether the procedures and practices of the depository are in compliance with the

Depositories Act, 1996, SEBI (Depositories and Participants) Regulations, 1996, SEBI circulars,

the bye-laws etc.

b) Check whether the books of account are being maintained by the depository, in the manner

specified in SEBI (Depository and Participants) Regulations, 1996;

c) Look into the complaints received by depositories from participants, issuers, issuers' agents,

beneficial owners or any other person;

d) Assess whether the IT infrastructure including its security system are adequate with suitable

business continuity arrangements.

e) Check whether violations and deficiencies pointed out in the last inspection report have been

rectified and procedures and systems have been suitably modified/ enhanced so that the

violations and or deficiencies would not occur again.

Interim Report of the Depository System Review Committee

Page 18 of 61

The broad areas covered in the inspection are as under:

1. Organization Structure: Infrastructure, committees and their working, bye-laws of the

depositories, employees, compliance officer etc.

2. Administrative and Monitoring Control: Process flow and operational manual, cooperation with

other entities

3. Issuer’s/ RTAs: Admission of issuer’s security, administration of issuers of securities, RTAs,

allocation and activation of ISIN, reconciliation of issuers’ records, corporate action.

4. Depository participants : Admission, renewal, withdrawal of participants , supervision &

inspection of participants

5. Operations : General operations of the depository

6. Systems Audit: Systemic issues of the depository

7. Financial Analysis: Financial performance, net worth, insurance, contingency funds etc.

8. Connectivity with other entities such as depository participants, clearing houses/corporations,

issuers, RTAs and stock exchanges

9. Other Aspects: Maintenance of books of accounts etc

10. Chinese walls in operations and systems between the capital market de/re materialization

related functions and non core activities undertaken by the depositories.

As per the existing procedure, SEBI calls for data from depositories through pre-inspection questionnaire

and the same is analyzed manually. The data so analyzed enables SEBI to identify areas which needs

greater focus and verifications during on-site inspection. Any major observations noted during on-site

inspections are discussed with the management of depositories for their immediate information and

compliance. Further, periodically follow up with the depositories is done till all pending observations are

fully implemented. The time taken to complete the entire exercise starting from pre-inspection data,

analysis of data, on-site inspection, and preparation of report and follow up with depositories may take

up to 6 months. Since the entire process is manual and labor intensive with minimal usage of

technology, the time taken in certain cases may further increase depending on number of inspecting

officials.

The current inspection methodology of SEBI is primarily compliance based wherein focus is on

ascertaining the compliance status of various guidelines and safeguards mandated by SEBI from time to

time.

Apart from inspection of depositories, SEBI also conducts annual inspection of DPs on selective basis and

such inspection is again primarily compliance based. Further, SEBI also receives monthly development

reports (MDR) from depositories which contain various details including number of routine / specific

purpose inspections of DPs conducted by them along with the name of the DPs and various actions /

penalties imposed by them.

Interim Report of the Depository System Review Committee

Page 19 of 61

Details of SEBI inspection of CDSL are as follows:

Period of Inspection Date of commencement

Nature of Inspection

August 2002- Jan 2004 Feb 23, 2004 Comprehensive Inspection

Feb/March 2004 – March 2005 July 5, 2005 Comprehensive Inspection

April 2005-March 2007 March 26, 2007 Comprehensive Inspection

N.A. Oct 19, 2010 Special purpose inspection to ascertain systems , processes and Inspection mechanism of Depository

April 2007- August 31, 2012 Nov 23, 2012 Comprehensive Inspection

Details of SEBI inspection of NSDL are as follows:

Period of Inspection Date of commencement

Nature of Inspection

August 2002- March 2005 April 28, 2005 Comprehensive Inspection

April 2005-May 2007 July 29, 2007 Comprehensive Inspection

N.A. Oct 11, 2010 Special purpose inspection to ascertain systems , processes and Inspection mechanism of Depository

The number of DPs inspected by SEBI from 2009-10 onwards is as follows

Year 2009-10 2010-11 2011-12

Number of DPs inspected 9 11 13

The major findings of SEBI inspection of Depositories are as follows:

NSDL CDSL

NSDL’s monitors Exposure limit of SBDP on a weekly basis rather than on a daily basis as advised by SEBI.

As regards to the process of appointment of system auditor, CDSL does not have a practice of obtaining a certificate from auditors towards conflict of interest

NSDL admits issuers/ companies who are not satisfying the eligibility criteria in certain cases even though the byelaws and operating manual does not provide for the discretion to relax the conditions.

It is observed that CDSL does not confirm from the pledgee that the securities are available for pledge as stated in the Regulations.

It was observed from the data provided by NSDL that 7270 cases of rejections were reported out of which 6345 were because of wrong DPID and 925 were for wrong client status in case of IPOs.

It was observed that there might be a case that even though the Depository provides training to two persons of inspecting firms, the inspections of RTAs/DPs might be carried out by the persons who

Interim Report of the Depository System Review Committee

Page 20 of 61

are not trained for carrying out the inspections by the Depository.

NSDL had not taken appropriate penal action against DPs for repetitive violations by DPs observed by them during inspections. NSDL’s action has never gone beyond imposition of monetary penalties.

It was observed that the inspection report does not have any comment on the status of implementation of various circulars and communiqué issued by SEBI and CDSL to DPs/RTAs.

The Depository has not set any internal standards for the depository officials for preparation of the inspection report, for issue of letter of observation/first letter and for analysis of the reply submitted by the DP/RTA i.e. for preparation of action and presenting the case to DAC etc.

The inspection reports are not analytical in nature. From the inspection report it is very difficult to draw a conclusion as it is in ‘Yes’ and ‘No’ format.

The inspection reports of the RTAs are in very standardized formats and they do not seem to be focusing on any specific areas of concern observed/identified by the different departments of the Depository. Further, it was observed that the inspection department of the Depository does not take any feedback from other departments such as operations, investor grievances etc to analyze the areas which require more attention during the inspection.

It was observed that the DAC of the Depository had reduced the penalty levied for the violations pointed out in the inspection reports by 75% which defeats the very purpose of having penalty structure.

The inspection report does not have any comment on the status of implementation of various circulars and communiqué issued by SEBI and NSDL to RTAs.

During discussion with CDSL it was found that it takes two to seven weeks to update the net-worth records in the AVPS monitoring system after receipt of the net-worth certificate.

There were some cases where inspection reports were considered to be closed even when RTAs had not sent compliance report to NSDL for the violations made in the inspection reports. There were as many as 25 such cases of RTAs observed during the period covered under inspection.

The Reconciliation of capital is done at RTA’s end and not even inspected by the inspection team. This could lead to major issues of capital mismatch not coming to notice if the RTA commits any error of commission/omission or colludes with the issuer.

In this regard, it is pertinent to mention that SEBI does not analyze the data which could be retrieved

out of MDRs or call for the inspection reports from the depositories on their findings about DPs and

therefore no cross verification of Depositories findings with SEBI's own findings seemed to have been

done.

In view of above, the committee has suggested:-

1. SEBI should revamp and then examine the information received through Monthly Development

Reports (MDRs) on a regular basis and SEBI should analyze the MDRs and convey their

observations / comments to the Depositories, specifically on findings of the inspection of DPs.

2. The critical observations of SEBI’s Inspection of DPs should be cohesive with the critical

observations of the DP inspection by depositories. In this context, the adequacy of inspection of

Interim Report of the Depository System Review Committee

Page 21 of 61

DPs by depositories needs to be checked by SEBI during its inspection of Depositories or

otherwise.

3. There should be an annual interface between SEBI and Depositories to review comprehensively

the inspection findings on the DPs and areas of repeat violations, non compliance, and overall

status of rectification.

4. Depositories should be inspected on an annual basis

Inspection of DPs by Depositories

The DPs are inspected and supervised by Depositories in accordance with Depositories Regulations and

while these inspections are intended to be more comprehensive. But it was observed that the current

process of inspection of DPs by the depositories is more a checklist based labor intensive process. The

committee was informed that inspection policy of depositories covers the following:

Annual inspection of operations and system of every DP.

Inspections are conducted by in-house audit team with a gap of 11-13 months between two

inspections of the same DP.

Inspection of new DP is conducted within 3 months of the date of commencement of its

business.

Period of inspection of a DP is generally the period from the last date of previous inspection till

the end of the month immediately preceding the actual date of inspection.

Major areas that are looked into during the inspection of DPs by Depositories are:

Account opening (KYC and In person verification), account modification, account closure

Dematerialization / rematerialization, pledge/ unpledge, freeze / unfreeze of securities

Issuance of DIS booklets & Execution of transactions

Complaint handling

The maintenance of all mandatory registers.

Back office software

The DSRC and its sub-committee deliberated on the inspection process and the depositories were asked

to make a presentation regarding the inspection of their participants. It was noted that NSDL has 283

DPs with 320 DPMs and 5,000 service centers. Similarly, CDSL has 575 DPs, 222 branches and 13,000

service centers. It may be noted that branches are those DP offices which are connected live with

Depositories where as service centers are those offices of DPs which only act as investor service points

handling collection of forms, data, account opening & related in-person verifications, and complaints.

Yet, services centers are connected with the main office through back office system of DP. The service

centre enters the data which flows electronically to main office and the corresponding physical

applications are sent to respective main office / related branch which are then verified and stored.

The salient features of inspection of DPs by depositories are:

Interim Report of the Depository System Review Committee

Page 22 of 61

Yearly inspections of all DPs and their live connected branches.

Inspection of service centers of DPs are on sample basis which constitutes less than 5% of total

service centers.

Majority of non-compliances result in imposition of monetary penalty as a deterrent measure.

The sampling policy is uniform across both the depositories and the sample selection is done

automatically on the basis of information available with the depositories on various parameters

in the following areas :

o Account Opening and KYC Documentation

o Account Modification

o Dematerialization / Rematerialisation/ Repurchase

o Issuance and Processing of DIS

o Account Closure

o Freeze/ Unfreeze

o Pledge/ Unpledge/ Hypothecation/ Invocation

o Transmission

o POD for Transaction Statements

The sampling is adaptive sampling based on the historical non-compliance data wherein sample

size varies dynamically from one DP to other DP.

The maximum sample size in any particular area is 1000 (irrespective of size of the portfolio -

cumulative or incremental) which however, is doubled in case of repetitive violations.

The penalties imposed are displayed on the website of the depositories.

One of the important areas looked into during on-site inspection is verification of process of

Delivery Instruction Slips (DIS) issuance and processing.

Audit / verification of various back office checks mandated by depositories.

From the above, following is observed:

Most of DPs are registered as participants with both the depositories, therefore they are

subjected to inspections by the depositories separately

By the very nature of their registration criteria, all DPs are carrying out other activities such

stock broking, banking, custodian, NBFC, RTA etc.

Inspections are checklist based annual exercises focusing only on compliance.

Inspections merely result in imposing monetary penalties rather than rectifying and improving

the systems, process and procedures.

The frequency of inspections is the same irrespective of size, nature and risk profile of DPs.

All service centers are not inspected by the depositories.

Depositories do not have details of the DIS booklets issued by DPs to their BOs which get

verified only at the time of on-site inspection resulting in loss of man hours and resources.

Depositories do not have all the information available in the back office of DPs with them such

as DIS numbers, mapping, KYC documents, account details, etc.

Interim Report of the Depository System Review Committee

Page 23 of 61

Having regard to the number of DPs and their service centers, volumes transacted nature and extent of

non compliance, the complaints etc the inspection process is sought to be revamped with following

suggestions:

The inspections should be risk oriented and the inspection reports should not only identify risk

areas but should also proactively suggest risk mitigation.

Consolidated / integrated risk based inspection framework for joint inspection of DPs by both

the depositories,

The pre and post inspection process of DPs and their service centers should be automated

through usage of appropriate technology so as to make it more quality oriented and less labor

intensive which will ultimately enhance the productivity of inspection process. There should be

architecture for facilitating the system generated flow of information/ data required for

regulatory oversight and / or routine review either on line or in batch mode on prescribed

frequency.

Alternatively, if such close inspection / oversight modality is not possible directly by Depositories

through their own personnel, the possibility of outsourcing service centre inspections through

accredited / duly empanelled external audit firms may be explored.

There should be disclosures in the annual report of depositories regarding inspections

conducted, major findings and various actions taken pursuant to inspections.

Classifying DPs into risk buckets with appropriate risk weights for the purpose of rating of DPs.

Further, for the categorization of risks, relative weights should be derived and more weights

should be assigned to the operational aspects with provision for triggers on slippages.

There should be an annual interface between Depositories to review comprehensively the

inspection findings on the DPs and areas of repeat violations, non compliance, and overall status

of rectification.

Both depositories should have uniform penalty structure so that DPs do not take advantage of

regulatory arbitrage.

Integrated risk based inspection framework

In the aftermath of the financial crisis, wherein Financial Stability Board (FSB) and the G20 Leaders

identified the need for more intense and effective supervision particularly to systemically important

financial institutions (SIFIs) as weak risk controls at financial institutions are still being witnessed. Some

of the entities registered as DP may be SIFIs. Therefore, keeping in view the global focus of effective