Securing Your Future Since 1919 Howard Sharfman President 500 West Madison Street, Suite 2700...

12

Securing Your Future Since 1919 www.schwartzbrothers.com Howard Sharfman President 500 West Madison Street, Suite 2700 Chicago, IL 60661 O: 312.683.7152 F: 312.759.4452 C: 312.927.6343 [email protected] April 17,2013 FOR AGENT USE ONLY

-

Upload

cameron-davidson -

Category

Documents

-

view

213 -

download

0

Transcript of Securing Your Future Since 1919 Howard Sharfman President 500 West Madison Street, Suite 2700...

Securing Your Future Since 1919www.schwartzbrothers.com

Howard SharfmanPresident500 West Madison Street, Suite 2700Chicago, IL 60661O: 312.683.7152F: 312.759.4452C: [email protected]

April 17,2013

FOR AGENT USE ONLY

Case study

• Case study one – managing a WL portfolio and IUL

• Case study two – insurance as an asset class• Case study three – insurance protecting a

concentrated position

Case Study One

Client One

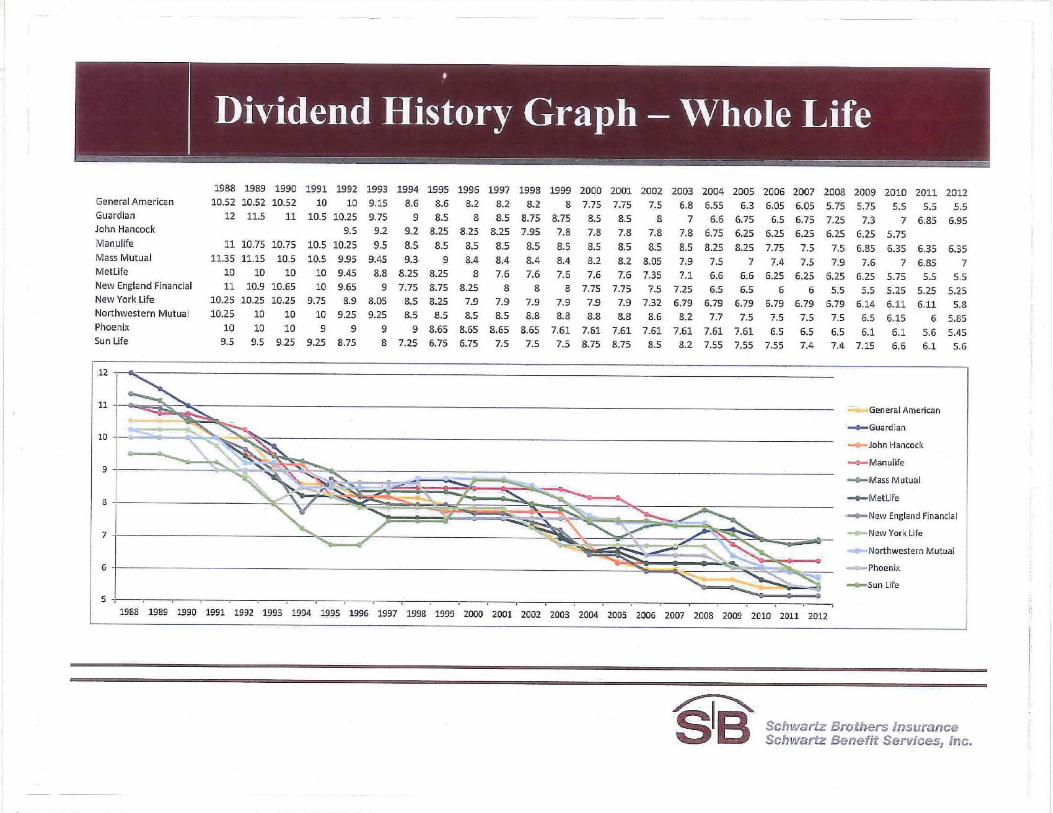

• Client 56M - UHNW – PR/NS• Capacity issues with Placement• Managing large WL portfolio for 10+ years• Concerned with Interest Dividend rate

declines• Wants to maintain high CV• Interest in and has had good experience with

Structured Notes• Long Term Player

Client

BEFORE AFTER moving basis to 3 IUL's at 6.25%

Cash Value Current NLV Death Benefit NLV Proposed CV NLV /New

Coverage Index @ 6.25% Proposed DB NLV/New

Coverage Index @ 6.25%

Today $ 19,416,000 $ 73,700,000 $ 18,000,000 $ 88,000,000

Year 15 $ 41,029,000 $ 74,250,000 $ 40,125,000 $ 88,000,000

Year 20 $ 49,773,000 $ 76,770,000 $ 48,500,000 $ 89,150,000

Age 81 $ 59,634,000 $ 81,300,000 $ 57,200,000 $ 92,875,000

Age 91 $ 78,154,000 $ 91,400,000 $ 76,273,000 $ 99,105,000

Reasons to change coverage

Diversify carriers and crediting strategy Similar illustrated cash value

Significant increase in Death benefit Concern over interest rate declines

Internal document - please review company provided illustrations showing guarantees and policy charges. Numbers rounded

Case Study Two

Client Two

• Large Private equity fund manager• Age 55• Has never purchased life insurance• $1B+ net Worth• Gifted $5mm to IDGT• Loaned $45mm to IDGT• Trust purchased carried interest units in fund• Trust purchased $50mm of GUL/UL – asset

allocation of $10mm of premium

WHY?

• Leverage• Non correlated asset Predictable• IRR at age 85 = 6.14% @ 90= 5.00% • Arbitrage between DB IRR and AFR• Asset allocation to tax free, estate tax free

product• Exit through liquidity of carried interest

Next Steps

Similar transaction on life of wife

Case Study Three

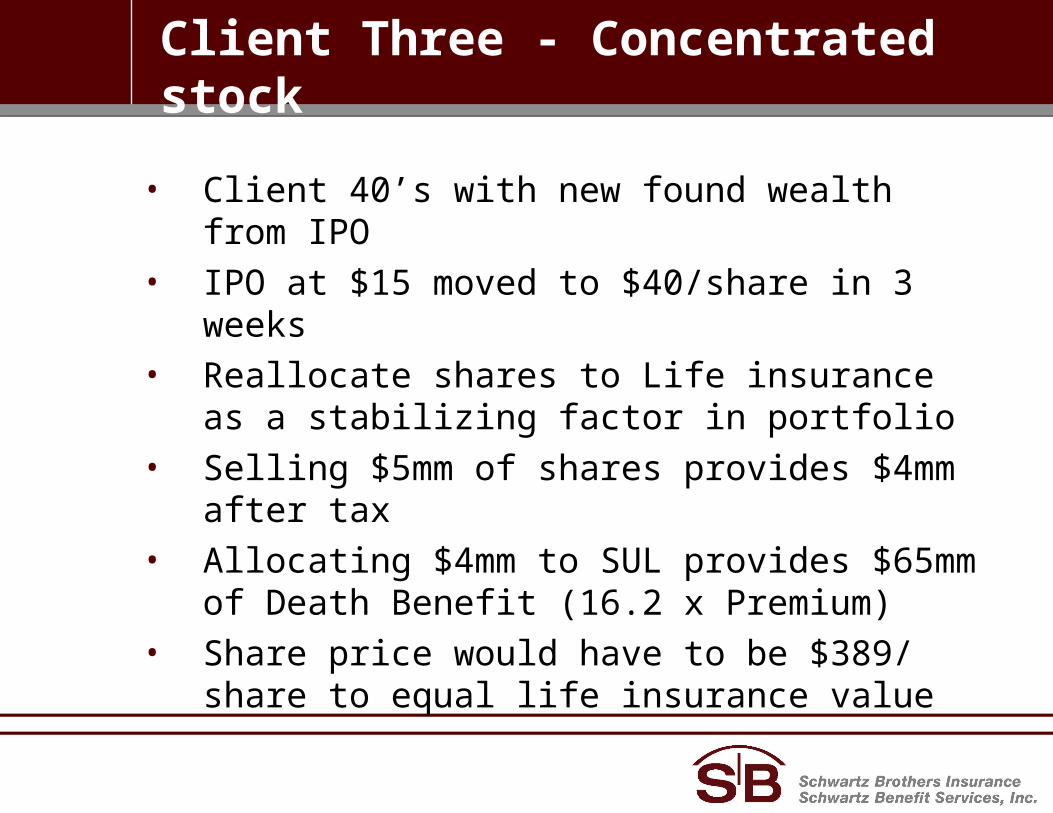

Client Three - Concentrated stock

• Client 40’s with new found wealth from IPO• IPO at $15 moved to $40/share in 3 weeks• Reallocate shares to Life insurance as a

stabilizing factor in portfolio• Selling $5mm of shares provides $4mm after

tax • Allocating $4mm to SUL provides $65mm of

Death Benefit (16.2 x Premium)• Share price would have to be $389/ share to

equal life insurance value