SECTOR Tech, Semis, Components and UPDATE Distributors …

20

SECTOR UPDATE January 13, 2016 Tech, Semis, Components and Distributors William Stein, CFA 212-319-3808 [email protected] Joseph Meares, CFA 212-303-4135 [email protected] Elliott Smith, CFA 212-303-4150 [email protected] The Industrialization of Semis Favor growth over safety • Formalizing our Industrialization of Semis thesis. After writing on this topic for the last 3 years, we formalize our industrialization thesis today, showing detailed regression analyses: Our analysis shows that semi investors have historically paid up for safety characteristics; however, growth characteristics have been better at generating alpha. As semis have become a more mature, slower-growing industry (more like industrials), investors, companies, and boards of directors should shift their favor away from safety to growth. As long as debt capital markets cooperate, expect M&A to be a major part of growth (as is the case in industrials). Key ways to invest in this thesis are to buy NXPI, AVGO, MSCC, and ADI. • Semi investors have historically "paid up" for safety. Semiconductor investors have historically "paid up" (with high P/E and EV/EBITDA multiples) for high gross margins, and low net leverage, characteristics we call "safety". Industrials investors have not consistently paid up for these metrics. • But, safety characteristics have not generated alpha. Our analysis shows that across the three time periods we studied, investing in semi companies with safety characteristics has not generated alpha. • Semi investors should instead "pay up" for growth. Across the three time periods we studied, the characteristics of semi companies that were most strongly correlated with total shareholder return were (1) earnings growth, (2) revenue growth, and (3) free cash flow growth. The same characteristics are the three most strongly correlated with shareholder return in industrials. This appears extremely supportive of continued M&A in semis (as long as debt capital markets cooperate), reflecting the same approach industrial companies have taken. • Semi Boards of Directors should shift to compensate growth metrics. We reviewed dozens of 10- K filings to investigate how compensation metrics align with our "growth over safety" view. Semi BoDs compensate for high margins in 85% of cases, but compensate for EPS and cash flow in only 35% and 13% of cases, respectively. We advocate semi BoDs should more prominently target EPS and cash flow growth, like their industrial counterparts which use these metrics in 48% and 30% of cases. • We believe the best ways to invest in the industrialization of semis is through companies that have embraced M&A to grow sales & EPS. The most prominent of these are NXPI, AVGO, MSCC, and ADI. Companies Impacted in This Note Ticker Price Rating Target ADI $51.65 Buy $71.00 APH $47.43 Neutral $55.00 ARW $48.32 Buy $65.00 ATML $7.68 Neutral $8.83 AVT $39.08 Buy $50.00 BDC $41.78 Buy $80.00 LLTC $39.51 Neutral $45.00 MCHP $41.85 Neutral $50.00 MXIM $33.15 Neutral $39.00 NXPI $77.78 Buy $103.00 PLAB $12.20 Buy $15.00 ST $39.64 Neutral $50.00 TEL $58.46 Buy $74.00 TXN $51.53 Neutral $57.00 XLNX $43.36 Neutral $45.00 AVGO $129.92 Buy $180.00 MSCC $31.33 Buy $49.00 INTC $32.68 Neutral $35.00 CY $8.39 Neutral $9.00 SEE PAGE 18 FOR REQUIRED DISCLOSURE INFORMATION Page 1 Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.actionTech, Semis, Components and Distributors Equity Research

Transcript of SECTOR Tech, Semis, Components and UPDATE Distributors …

SECTORUPDATEJanuary 13, 2016

Tech, Semis, Components andDistributors

William Stein, [email protected]

Joseph Meares, [email protected]

Elliott Smith, [email protected]

The Industrialization of SemisFavor growth over safety

• Formalizing our Industrialization of Semis thesis. After writing on this topic for the last 3 years, weformalize our industrialization thesis today, showing detailed regression analyses: Our analysis showsthat semi investors have historically paid up for safety characteristics; however, growth characteristicshave been better at generating alpha. As semis have become a more mature, slower-growing industry(more like industrials), investors, companies, and boards of directors should shift their favor away fromsafety to growth. As long as debt capital markets cooperate, expect M&A to be a major part of growth (asis the case in industrials). Key ways to invest in this thesis are to buy NXPI, AVGO, MSCC, and ADI.

• Semi investors have historically "paid up" for safety. Semiconductor investors have historically "paidup" (with high P/E and EV/EBITDA multiples) for high gross margins, and low net leverage, characteristicswe call "safety". Industrials investors have not consistently paid up for these metrics.

• But, safety characteristics have not generated alpha. Our analysis shows that across the three timeperiods we studied, investing in semi companies with safety characteristics has not generated alpha.

• Semi investors should instead "pay up" for growth. Across the three time periods we studied, thecharacteristics of semi companies that were most strongly correlated with total shareholder return were(1) earnings growth, (2) revenue growth, and (3) free cash flow growth. The same characteristics are thethree most strongly correlated with shareholder return in industrials. This appears extremely supportiveof continued M&A in semis (as long as debt capital markets cooperate), reflecting the same approachindustrial companies have taken.

• Semi Boards of Directors should shift to compensate growth metrics. We reviewed dozens of 10-K filings to investigate how compensation metrics align with our "growth over safety" view. Semi BoDscompensate for high margins in 85% of cases, but compensate for EPS and cash flow in only 35% and13% of cases, respectively. We advocate semi BoDs should more prominently target EPS and cash flowgrowth, like their industrial counterparts which use these metrics in 48% and 30% of cases.

• We believe the best ways to invest in the industrialization of semis is through companies thathave embraced M&A to grow sales & EPS. The most prominent of these are NXPI, AVGO, MSCC,and ADI.

Companies Impacted in This NoteTicker Price Rating Target

ADI $51.65 Buy $71.00

APH $47.43 Neutral $55.00

ARW $48.32 Buy $65.00

ATML $7.68 Neutral $8.83

AVT $39.08 Buy $50.00

BDC $41.78 Buy $80.00

LLTC $39.51 Neutral $45.00

MCHP $41.85 Neutral $50.00

MXIM $33.15 Neutral $39.00

NXPI $77.78 Buy $103.00

PLAB $12.20 Buy $15.00

ST $39.64 Neutral $50.00

TEL $58.46 Buy $74.00

TXN $51.53 Neutral $57.00

XLNX $43.36 Neutral $45.00

AVGO $129.92 Buy $180.00

MSCC $31.33 Buy $49.00

INTC $32.68 Neutral $35.00

CY $8.39 Neutral $9.00

SEE PAGE 18 FOR REQUIRED DISCLOSURE INFORMATION Page 1

Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.actionTech, Semis, Components and Distributors Equity Research

The Industrialization of Semis

Contents PM Summary: favor growth over value ........................................................................................................ 3

Introduction & A brief word on our methodology ....................................................................................... 3

Semi investors have historically “paid up” for safety ................................................................................... 3

Safety characteristics have not generated alpha .......................................................................................... 7

Semi investors should instead “pay up” for growth ................................................................................... 10

Best individual metrics ........................................................................................................................ 10

Multivariate analysis ........................................................................................................................... 13

Semi Boards of Directors should shift compensation metrics to favor growth over safety ....................... 15

Best ways to invest in the industrialization of semis theme ...................................................................... 16

NXP Semiconductors (NXPI, $77.78, Buy) ............................................................................................... 16

Avago Technologies (AVGO, $129.92, Buy) ............................................................................................ 16

Microsemi Corporation (MSCC, $31.33, Buy) ......................................................................................... 17

Analog Devices (ADI, $51.65, Buy) .......................................................................................................... 17

Tech, Semis, Components and Distributors

Page 2 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

PM Summary: favor growth over value Over the last three years we’ve written about our “industrialization of semis” thesis. Today we

formalize our thesis with regression analyses. In summary, our work suggests that as management

teams, boards of directors, and investors come to terms with a semiconductor industry that grows only

slightly faster than global GDP,

Companies will transition focus away from “safety” (high gross profit margin and low leverage)

to “growth” (sales, EPS, and cash flow per share), often by acquiring other companies, cutting

costs, and using appropriate financial leverage.

Boards of directors will likewise shift performance targets away from safety to growth metrics,

and

Ultimately we believe investors will begin to reward companies that deliver faster earnings

growth (through acquisitions & cost cuts, or otherwise) with higher valuation metrics.

Introduction & A brief word on our methodology In 2012 when we launched coverage of the semiconductor industry, feedback from investors indicated

that the key metric in evaluating semiconductors is gross profit margin, that acquisitions don’t create

value for equity because they rarely enable gross margin expansion, and that financially levered

semiconductor companies represent very risky investments. We disagreed with those views, and over

time built the regression analyses to support our opinions.

We collected 10 fundamental metrics for approximately 90 companies across the semiconductor and

industrial sectors over 3 separate time periods (the trailing 1, 3, and 5 year periods each ending

12/31/2014). We ran simple and multiple regressions of the fundamental data relative to valuation

metrics (P/E and EV/EBITDA) to determine the answers to three questions for semis and (separately) for

industrials: (1) what fundamental metrics were most highly correlated with high valuation?, (2) did

investments that favored those fundamental metrics generate alpha?, and (3) if not, what were the

characteristics most correlated with alpha generation? Separately, we studied whether performance

criteria that boards of directors established for management teams were aligned with metrics that

generate investment returns.

We found that semi investors have historically favored safety (high gross margin and low financial

leverage). These characteristics are not associated with alpha generation. Outsized returns are most

correlated with growth metrics, specifically EPS, cash flow, and sales growth. We also found that BoDs

place too much emphasis on safety (specifically margins) and not enough on EPS or cash flow growth.

Semi investors have historically “paid up” for safety The valuation component of our study had the most striking differences between semi and industrial

companies, and is an important area regarding our industrialization theme. We based this study on a

simple regression of historical metrics versus valuation multiples at the beginning of the study period,

which we then verified through multivariate iterations. For semis, investors have historically "paid up"

Tech, Semis, Components and Distributors

Page 3 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

(with high P/E and EV/EBITDA multiples) for high gross margins and low net leverage. By contrast, in

industrials, investors do not place a consistent premium on any particular fundamental metric, meaning

no metric was significant across all 3 periods of the study.

While different time periods have slight differences in which metrics have the highest correlations (and

some time periods have much stronger correlations than others), the important trends were evident –

semi investors apply premium valuations to companies with historically high gross margins and low net

leverage. Other metrics were correlated during different periods, but we were more concerned with

what investors have repeatedly paid a premium for. In the following exhibit, we show an example of the

high correlation between historical gross profit margin and EV/EBITDA valuation for semiconductor

companies in the 2011-2014 study.

Exhibit 1: Semiconductor 2011-2014 simple regression study, historical GPM vs. EV/EBITDA valuation

Source: Company Data, FactSet, STRH Analysis

In the following exhibit, we outline the simple regression conclusions for each time period.

y = 14.823x + 0.1274R² = 0.5072

0

2

4

6

8

10

12

14

16

18

20

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

EV/E

BIT

DA

Historical GPM

Historical GPM vs. EV/EBITDA

Tech, Semis, Components and Distributors

Page 4 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 2: Simple regression study conclusions for what investors have “paid up” for

Source: Company Data, FactSet, STRH Analysis

Next, we show the filtered, multiple regression conclusions. These results take the simple regression

output a few steps further, removing high levels of multicollinearity and false positives to try and find

the true drivers of valuation. In the following exhibit, we show an example of our multiple regression

analysis for the same 2011-2014 semiconductor study comparing EV/EBITDA valuation with historical

gross profit margin. The multiple regression analysis verifies our simple regression above, and we show

the results below.

Regression Simple Regression Simple Regression Simple Regression

Gross Profit Margin Level Gross Profit Margin Level Net Leverage

Net Leverage Net Leverage Gross Profit Margin Level

ROIC level Gross Profit Margin Level Gross Profit Margin LevelGross Profit Margin Level Operating Profit Margin Level ROIC Level

ROIC LevelNet Leverage

No significant metrics ROIC Level Operating Profit Margin Level

Gross Leverage

Net Leverage

Gross Profit Margin Level Gross Profit Margin Level Net leverageEV/EBITDA

Valuation

What do Investors

Pay For?

2009 - 2014 2011 - 2014

P/E Valuation

EV/EBITDA

Valuation

2013 - 2014

P/E Valuation

Semis

Industrials

Tech, Semis, Components and Distributors

Page 5 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

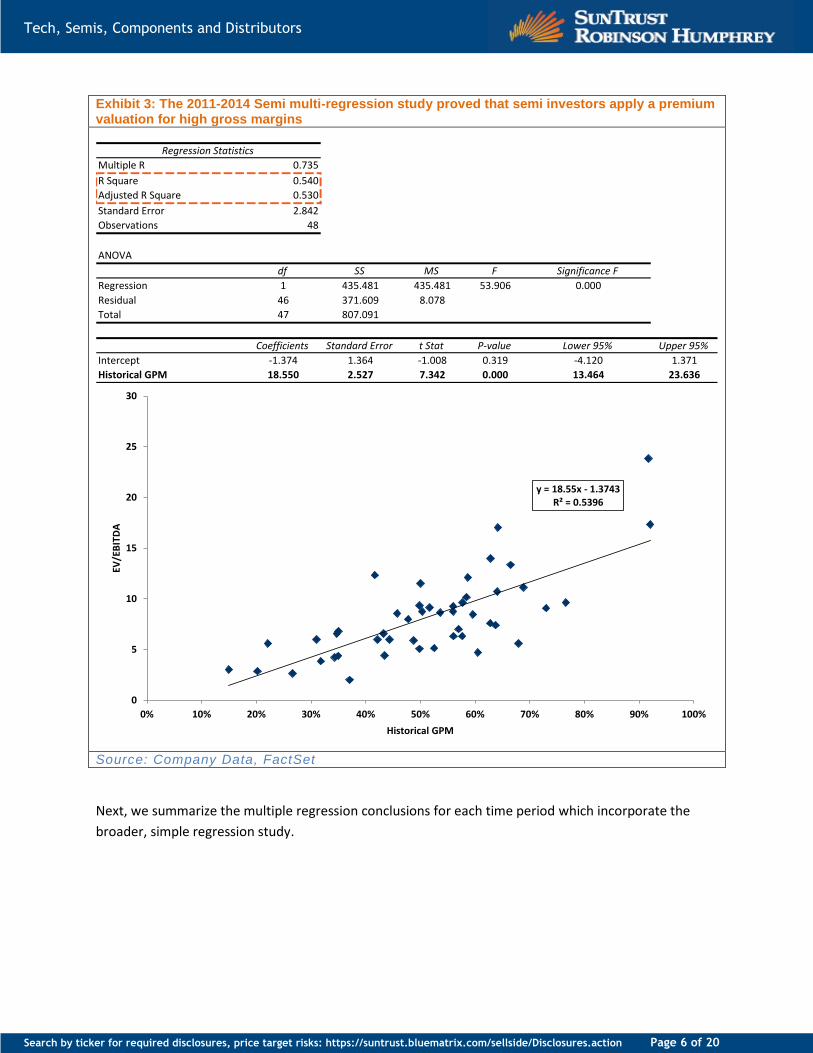

Exhibit 3: The 2011-2014 Semi multi-regression study proved that semi investors apply a premium valuation for high gross margins

Source: Company Data, FactSet

Next, we summarize the multiple regression conclusions for each time period which incorporate the

broader, simple regression study.

Regression Statistics

Multiple R 0.735

R Square 0.540

Adjusted R Square 0.530

Standard Error 2.842

Observations 48

ANOVA

df SS MS F Significance F

Regression 1 435.481 435.481 53.906 0.000

Residual 46 371.609 8.078

Total 47 807.091

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -1.374 1.364 -1.008 0.319 -4.120 1.371

Historical GPM 18.550 2.527 7.342 0.000 13.464 23.636

y = 18.55x - 1.3743R² = 0.5396

0

5

10

15

20

25

30

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

EV/E

BIT

DA

Historical GPM

Tech, Semis, Components and Distributors

Page 6 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 4: Multiple regression study conclusions for what investors have “paid up” for

Source: Company Data, FactSet, STRH Analysis

And finally, considering both regression sets across the 3 time periods, we show our conclusions. In this

final set of results, it was important to discover the most important trends across all of the time periods

as whole, not intermittent sources of significance. We found that while semi investors are willing pay a

premium for high gross profit margins and low net leverage, industrial investors are not willing to a

pay a consistent premium for any single metric.

Exhibit 5: Final study conclusions for what investors have “paid up” for

Source: Company Data, FactSet, STRH Analysis

Safety characteristics have not generated alpha Across the three time periods we studied, investing in semi companies with high margins and low net

leverage (buying "safety") has not generated alpha. In the following exhibits, we demonstrate the lack

of correlation between both historical GPM levels and net leverage with future returns over each of the

3 time periods. While some of regression lines do slope in a positive direction, the largest R-squared

among the data set is 0.08, implying a correlation of approximately 28% in the best case.

Regression Multiple Regression Multiple Regression Multiple Regression

Gross Profit Margin Level Gross Profit Margin level Net Leverage

Net Leverage Gross Profit Margin Level

ROIC level Gross Profit Margin level Gross Profit Margin LevelGross Profit Margin Level

No significant metrics No significant metrics No significant metrics

Gross Profit Margin Level Gross Profit Margin Level Net leverageEV/EBITDA

Valuation

What do Investors

Pay For?

2009 - 2014 2011 - 2014

P/E Valuation

EV/EBITDA

Valuation

2013 - 2014

P/E Valuation

Semis

Industrials

Regression

Gross Profit Margin Level

Net Leverage

Gross Profit Margin Level

No significant metrics

No significant metrics

Final Conclusion

EV/EBITDA

Valuation

What do Investors

Pay For?

P/E Valuation

EV/EBITDA

Valuation

P/E Valuation

Semis

Industrials

Tech, Semis, Components and Distributors

Page 7 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 6: 2009-2014 semi regression comparing historical GPM and net leverage to the company’s future total return

Source: Company Data, FactSet

y = 1.1349x - 0.1912R² = 0.0816

-150.0%

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

200.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Tota

l Re

turn

Historical GPM

Historical GPM vs Future Return

y = -0.0055x + 0.3928R² = 0.0058

-150.0%

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

200.0%

-35.00 -30.00 -25.00 -20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00 15.00 20.00

Tota

l Re

turn

Historical Net Leverage

Historical Net Leverage vs Future Return

Tech, Semis, Components and Distributors

Page 8 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 7: 2011-2014 semi regression comparing historical GPM and net leverage to the company’s future total return

Source: Company Data, FactSet

y = -0.267x + 0.4822R² = 0.0095

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0%Tota

l Re

turn

Historical GPM

Historical GPM vs Future Return

y = 0.0177x + 0.4821R² = 0.0301

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

-20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00

Tota

l Re

turn

Historical Net Leverage

Historical Net Leverage vs Future Return

Tech, Semis, Components and Distributors

Page 9 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 8: 2013 – 2014 semi regression comparing historical GPM and net leverage to the company’s future total return

Source: Company Data, FactSet

Semi investors should instead “pay up” for growth Now that we know applying premium valuations for “safe” plays does not typically work, the next logical

question becomes: “What should I pay for?” Across the three time periods we studied, the coincident

metrics most strongly correlated with total shareholder return were (1) earnings growth, (2) revenue growth,

and (3) free cash flow growth. Investors should note: the same characteristics are also the three most

strongly correlated with shareholder return among industrials.

Best individual metrics

We used the same format to evaluate this section – a diverse set of simple regressions, coordinated with

a final multiple regression study. In the following exhibits as an example, we show the simple regression

analysis of EPS growth and total return for semiconductor companies in the 2011 - 2014 study, followed

by a multiple regression analysis that verifies the result.

y = -0.121x + 0.2279R² = 0.0028

-100.0%

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Tota

l Re

turn

Historical GPM

Historical GPM vs Future Return

y = 0.0208x + 0.2574R² = 0.0725

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

-20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00

Tota

l Re

turn

Historical Net Leverage

Historical Net Leverage vs Future Return

Tech, Semis, Components and Distributors

Page 10 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 9: Semiconductor 2011-2014 simple regression study, EPS growth vs. total return

Source: Company Data, FactSet

y = 0.7199x + 0.3735R² = 0.5338

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

-150% -100% -50% 0% 50% 100% 150% 200% 250%

Tota

l Re

turn

EPS Growth

EPS Growth vs. Total Return

Tech, Semis, Components and Distributors

Page 11 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 10: The 2011-2014 Semi multi-regression study proved that EPS growth was the best coincident indicator of Total Return

Source: Company Data, FactSet

In the following exhibit, we show the most significant individual metrics to explain total shareholder

return for both Semi and Industrial investors across each of the three time periods. These are the final

Regression Statistics

Multiple R 0.921

R Square 0.848

Adjusted R Square 0.843

Standard Error 0.273

Observations 32

ANOVA

df SS MS F Significance F

Regression 1 12.50 12.50 167.57 0.000

Residual 30 2.24 0.07

Total 31 14.74

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.323 0.053 6.087 0.000 0.215 0.432

EPS Growth 1.083 0.084 12.945 0.000 0.912 1.254

Correlation EPS Growth Rev Growth FCF Growth

EPS Growth 1.00

Rev Growth 0.76 1.00

FCF Growth 0.63 0.39 1.00

y = 1.0831x + 0.3234R² = 0.8482

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

-100% -50% 0% 50% 100% 150% 200% 250%

Tota

l Re

turn

EPS Growth

EPS Growth vs. Total Return

Tech, Semis, Components and Distributors

Page 12 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

results for the best coincident indicator, based on both regression sets. When looking for the single

most important metric, EPS growth is hands down the largest driver of incremental shareholder value.

Exhibit 11: Summary table showing the single best coincident indicator for total shareholder return over each period

Source: Company Data, FactSet, and STRH Analysis

Multivariate analysis

Aside from uncovering the best individual metrics, we also contemplated a traditional multivariate

analysis that attempted to uncover the best combination of variables to describe total return. While

most models ended up best described by only a single, independent variable (shown in the above

section), two portions of the study were better explained through a combination of variables. The 2011-

2014 industrial model was best described by a combination of revenue growth and free cash flow

growth, and with correlation between the two independent variables at only 39%. The 2011-2014 semi

model was also best described by a combination of revenue growth and free cash flow growth. The

multicollinearity was slightly more prevalent here with a correlation of 46%. The multiple regression

analysis results are shown in the 2 exhibits below.

2009 - 2014 2010 - 2014 2011 - 2014 Final Conclusion

EPS Growth EPS Growth EPS Growth EPS Growth

2009 - 2014 2010 - 2014 2011 - 2014 Final Conclusion

EPS Growth EPS Growth FCF Growth EPS Growth

Semis

Industrials

Tech, Semis, Components and Distributors

Page 13 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 12: The 2011-2014 industrial multi-regression study proved that Rev growth and FCF growth together were the best coincident indicators of Total Return

Source: Company Data, FactSet, STRH Analysis

Regression Statistics

Multiple R 0.813

R Square 0.661

Adjusted R Square 0.637

Standard Error 0.415

Observations 32

ANOVA

df SS MS F Significance F

Regression 2 9.74 4.87 28.24 1.558E-07

Residual 29 5.00 0.17

Total 31 14.74

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.298 0.085 3.505 0.002 0.124 0.472

Rev Growth 0.824 0.207 3.977 0.000 0.400 1.248

FCF Growth 0.244 0.057 4.299 0.000 0.128 0.360

Correlation EPS Growth Rev Growth FCF Growth

EPS Growth 1.00

Rev Growth 0.76 1.00

FCF Growth 0.63 0.39 1.00

Tech, Semis, Components and Distributors

Page 14 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 13: The 2013 - 2014 semi multi-regression study proved that Rev growth and FCF growth together were the best coincident indicators of Total Return

Source: Company Data, FactSet, STRH Analysis

Semi Boards of Directors should shift compensation metrics to favor

growth over safety Armed with a view that, for both semis and industrials, growth in cash flow, earnings, and sales are

more correlated with alpha generation than safety characteristics like high gross margin and low

leverage, we investigated how well aligned management teams’ compensation metrics are with

characteristics that drive alpha.

We analyzed dozens of 10-K filings to first determine compensation metrics for both semi and industrial

management teams. We then compared these results with the metrics that are most highly correlated

with shareholder returns (growth in revenue, EPS, and FCF).

Our analysis, summarized in the following exhibit, suggests BoDs, especially for semiconductor

companies, could do a much better job of aligning performance metrics with alpha generating

characteristics.

Regression Statistics

Multiple R 0.725

R Square 0.526

Adjusted R Square 0.494

Standard Error 0.254

Observations 32

ANOVA

df SS MS F Significance F

Regression 2 2.08 1.04 16.10 1.978E-05

Residual 29 1.87 0.06

Total 31 3.96

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.174 0.050 3.449 0.002 0.071 0.277

Rev Growth 0.621 0.220 2.823 0.009 0.171 1.071

FCF Growth 0.144 0.049 2.949 0.006 0.044 0.244

Correlation Rev Growth EBITDA Growth EPS Growth FCF Growth

Rev Growth 1.00

EBITDA Growth 0.82 1.00

EPS Growth 0.70 0.92 1.00

FCF Growth 0.46 0.76 0.80 1.00

Tech, Semis, Components and Distributors

Page 15 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Exhibit 14: The percentage of companies that reward their management team based on each of the criteria listed

Source: Company Data, FactSet, STRH Analysis

In particular, we highlight that the most commonly used compensation metric for Semiconductor

companies is margins, despite our analysis showing that high margins isn’t an alpha-generating

characteristic. Meanwhile, the big alpha generating characteristics EPS and Cash Flow are used by

semiconductor boards in only 35% and 13% of the time, respectively.

Simply put, to better align management’s and shareholders’ interests, semiconductor boards of

directors should shift the metrics on which they measure management from safety (specifically margins)

to growth (specifically EPS and cash flow).

Best ways to invest in the industrialization of semis theme While M&A has been an ongoing phenomenon of semiconductor investing for the last three years, we

anticipate it will continue, so long as debt capital markets cooperate. Companies in our coverage that

we believe are most aligned with our industrialization thesis include:

NXP Semiconductors (NXPI, $77.78, Buy) We believe NXPI is a leader relative to our industrialization of semiconductors theme. Even before the

company acquired Freescale, it targeted outsized EPS growth through a combination of superior sales

growth (with leading positions in ID and automotive) and shareholder friendly capital allocation (share

buybacks). Freescale gives NXP a significant step-up in EPS and a $500 million per year cost savings EPS

accelerator. Ultimately we believe NXP’s earnings growth will be approximately 17% per year. Our PT is

$103 based on 14x our 2016 EPS.

Avago Technologies (AVGO, $129.92, Buy) We see AVGO as a clear innovator relative to our industrialization of semiconductors theme. The

company’s RF filtering expertise affords it a stable growth engine that it supplements with significant

acquisitions. With BRCM we believe AVGO will have long-term organic earnings growth of 13% that

bumps to 17% with future potential M&A. Our PT is $180 based on 14x our 2017 EPS.

Metric Semis Industrials Drives Returns?

Margin / cost 87% 61% No

Sales/Bookings growth 78% 57% Yes

EPS-related 35% 48% Yes

Cash flow 13% 30% Yes

Returns (fundamental) 9% 48% No

Returns (stock) 13% 30% Yes

Tech, Semis, Components and Distributors

Page 16 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Microsemi Corporation (MSCC, $31.33, Buy) Microsemi’s intermittent acquisitions fuel a mostly inorganic growth profile. In the near-term we

anticipate approximately 40% of company sales are poised to accelerate in 2016-2017. Following its

pending acquisition of PMC-Sierra (PMCS, $11.63, NR) we believe MSCC will have long-term organic

earnings growth of 14% that bumps to 19% with future potential M&A. Our PT is $49 based on 12x our

2017 EPS.

Analog Devices (ADI, $51.65, Buy) ADI is a more recent fit into our industrialization of semis theme. We believe management is slowly

transitioning the company’s under-levered balance sheet to one that uses leverage to fuel growth. This

is most recently evidenced by the company’s raise of $875m net incremental debt that it will use to fund

either an acquisition or stock repurchase. Our PT is $71 based on 20x our C16 EPS.

Tech, Semis, Components and Distributors

Page 17 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Companies Mentioned in This NoteAnalog Devices, Inc. (ADI, $51.65, Buy)Amphenol Corp (APH, $47.43, Neutral)Arrow Electronics, Inc. (ARW, $48.32, Buy)Atmel Corp. (ATML, $7.68, Neutral)Avnet, Inc. (AVT, $39.08, Buy)Belden Inc. (BDC, $41.78, Buy)Linear Technology Corp. (LLTC, $39.51, Neutral)Microchip Technology Inc (MCHP, $41.85, Neutral)Maxim Integrated (MXIM, $33.15, Neutral)NXP Semiconductors N.V. (NXPI, $77.78, Buy)Photronics, Inc. (PLAB, $12.20, Buy)Sensata Technologies Holding NV (ST, $39.64, Neutral)TE Connectivity, Ltd. (TEL, $58.46, Buy)Texas Instruments Inc. (TXN, $51.53, Neutral)Xilinx, Inc. (XLNX, $43.36, Neutral)Avago (AVGO, $129.92, Buy)Microsemi (MSCC, $31.33, Buy)Cypress (CY, $8.39, Neutral)Intel (INTC, $32.68, Neutral)PMC-Sierra (PMCS, $11.63, NR)

Analyst CertificationI, William Stein , hereby certify that the views expressed in this research report accurately reflect my personal views about the subjectcompany(ies) and its (their) securities. I also certify that I have not been, am not, and will not be receiving direct or indirect compensation inexchange for expressing the specific recommendation(s) in this report.

Required DisclosuresAnalyst compensation is based upon stock price performance, quality of analysis, communication skills, and the overall revenue and profitability ofthe firm, including investment banking revenue.

As a matter of policy and practice, the firm prohibits the offering of favorable research, a specific research rating or a specific target price asconsideration or inducement for the receipt of business or compensation. In addition, associated persons preparing research reports are prohibitedfrom owning securities in the subject companies.

Charts indicating changes in ratings can be found in recent notes and/or reports at our website or by contacting SunTrust Robinson Humphrey.Please see our disclosures page for more complete information at https://suntrust.bluematrix.com/sellside/Disclosures.action.

Tech, Semis, Components and Distributors

Page 18 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

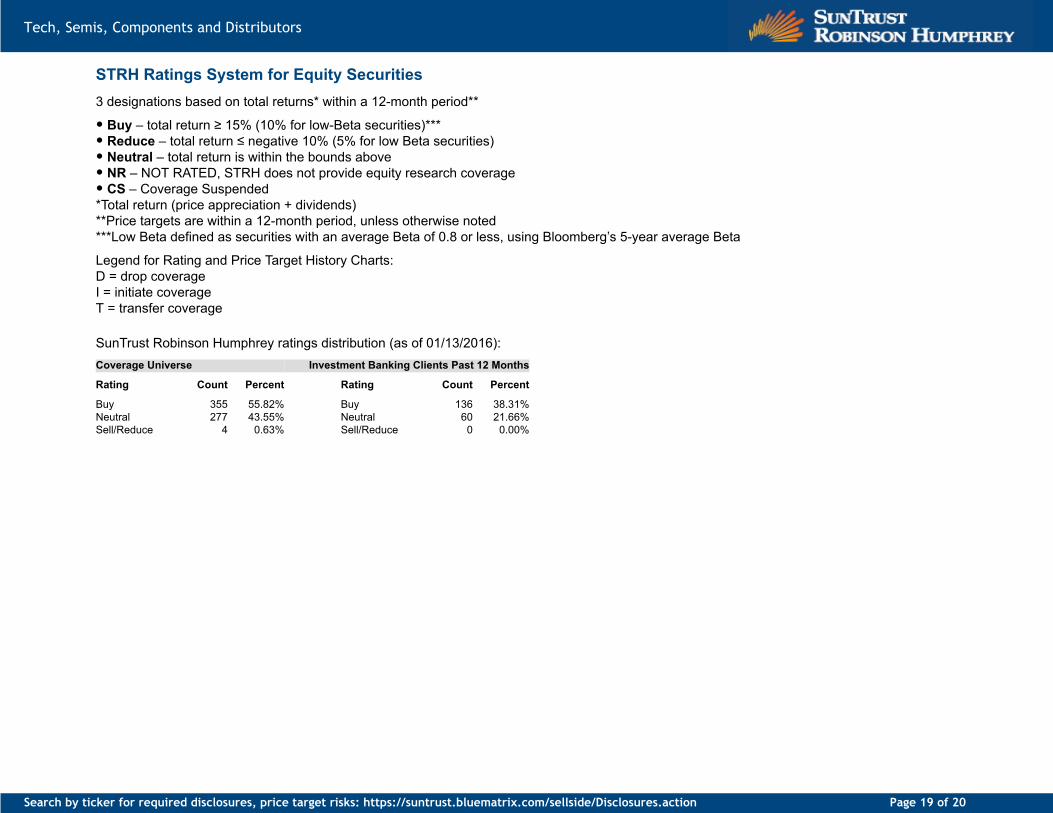

STRH Ratings System for Equity Securities3 designations based on total returns* within a 12-month period**

• Buy – total return ≥ 15% (10% for low-Beta securities)***• Reduce – total return ≤ negative 10% (5% for low Beta securities)• Neutral – total return is within the bounds above• NR – NOT RATED, STRH does not provide equity research coverage• CS – Coverage Suspended*Total return (price appreciation + dividends)**Price targets are within a 12-month period, unless otherwise noted***Low Beta defined as securities with an average Beta of 0.8 or less, using Bloomberg’s 5-year average Beta

Legend for Rating and Price Target History Charts:D = drop coverageI = initiate coverageT = transfer coverage

SunTrust Robinson Humphrey ratings distribution (as of 01/13/2016):Coverage Universe Investment Banking Clients Past 12 Months

Rating Count Percent Rating Count Percent

Buy 355 55.82% Buy 136 38.31%Neutral 277 43.55% Neutral 60 21.66%Sell/Reduce 4 0.63% Sell/Reduce 0 0.00%

Tech, Semis, Components and Distributors

Page 19 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action

Other DisclosuresInformation contained herein has been derived from sources believed to be reliable but is not guaranteed as to accuracy and does not purportto be a complete analysis of the security, company or industry involved. This report is not to be construed as an offer to sell or a solicitation ofan offer to buy any security. SunTrust Robinson Humphrey, Inc. and/or its officers or employees may have positions in any securities, options,rights or warrants. The firm and/or associated persons may sell to or buy from customers on a principal basis. Investors may be prohibited incertain states from purchasing some over-the-counter securities mentioned herein. Opinions expressed are subject to change without notice. Theinformation herein is for persons residing in the United States only and is not intended for any person in any other jurisdiction.

SunTrust Robinson Humphrey, Inc.’s research is provided to and intended for use by Institutional Accounts as defined in FINRA Rule 4512(c).The term “Institutional Account" shall mean the account of: (1) a bank, savings and loan association, insurance company or registered investmentcompany; (2) an investment adviser registered either with the SEC under Section 203 of the Investment Advisers Act or with a state securitiescommission (or any agency or office performing like functions); or (3) any other person (whether a natural person, corporation, partnership, trust orotherwise) with total assets of at least $50 million.

SunTrust Robinson Humphrey, Inc. is a registered broker-dealer and a member of FINRA and SIPC. It is a service mark of SunTrust Banks, Inc.SunTrust Robinson Humphrey, Inc. is owned by SunTrust Banks, Inc. ("SunTrust") and affiliated with SunTrust Investment Services, Inc. Despitethis affiliation, securities recommended, offered, sold by, or held at SunTrust Robinson Humphrey, Inc. and at SunTrust Investment Services, Inc.(i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution(including SunTrust Bank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested. SunTrust Bankmay have a lending relationship with companies mentioned herein.

© SunTrust Robinson Humphrey, Inc. 2016 . All rights reserved. Reproduction or quotation in whole or part without permission is forbidden.

ADDITIONAL INFORMATION IS AVAILABLE at our website, www.suntrustrh.com, or by writing to:SunTrust Robinson Humphrey, Research Department, 3333 Peachtree Road N.E., Atlanta, GA 30326-1070

Tech, Semis, Components and Distributors

Page 20 of 20Search by ticker for required disclosures, price target risks: https://suntrust.bluematrix.com/sellside/Disclosures.action