Sections 351(e) & 368(a)(2)(F) - American Bar Association · Sections 351(e) & 368(a)(2)(F)...

43

Sections 351(e) & 368(a)(2)(F) American Bar Association Section of Taxation Boca Raton, Florida January 22, 2011 Erik H. Corwin William Alexander Mike Kaibni Ropes & Gray LLP Internal Revenue Service Ernst & Young LLP Washington, DC Washington, DC Washington, DC Rachel Kleinberg Don Leatherman Davis Polk & Wardwell LLP University of Tennessee Menlo Park, CA Knoxville, TN

-

Upload

nguyentruc -

Category

Documents

-

view

215 -

download

0

Transcript of Sections 351(e) & 368(a)(2)(F) - American Bar Association · Sections 351(e) & 368(a)(2)(F)...

Sections 351(e) & 368(a)(2)(F)

American Bar AssociationSection of TaxationBoca Raton, FloridaJanuary 22, 2011

Erik H. Corwin William Alexander Mike KaibniRopes & Gray LLP Internal Revenue Service Ernst & Young LLPWashington, DC Washington, DC Washington, DC

Rachel Kleinberg Don LeathermanDavis Polk & Wardwell LLP University of TennesseeMenlo Park, CA Knoxville, TN

Topics

� Section 351(e)

� A Brief History

� Overview of Rules

� Determination of an Investment Company

� Diversification

� One Bad Apple

� Affirmative Use of Section 351(e)

� Section 368(a)(2)(F)

� A Brief History

� Overview of Rules

� Base Cases

� Problem Cases

2

3

Section 351(e)

4

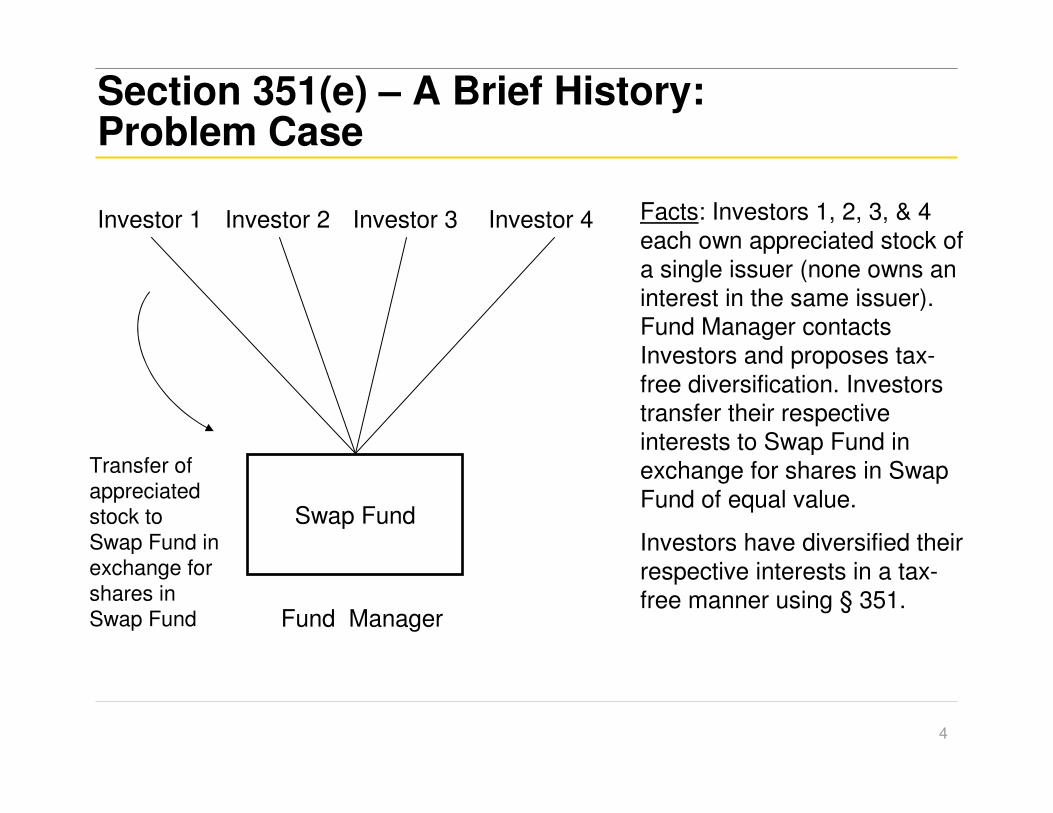

Section 351(e) – A Brief History: Problem Case

Investor 1 Investor 2 Investor 3 Investor 4

Fund Manager

Swap Fund

Facts: Investors 1, 2, 3, & 4 each own appreciated stock of a single issuer (none owns an interest in the same issuer). Fund Manager contacts Investors and proposes tax-free diversification. Investors transfer their respective interests to Swap Fund in exchange for shares in Swap Fund of equal value.

Investors have diversified their respective interests in a tax-free manner using § 351.

Transfer of appreciated stock to Swap Fund in exchange for shares in Swap Fund

5

� IRS had historically issued § 351 rulings to the effect that no tax resulted from the exchange of appreciated stock for shares in aninvestment fund (See S. Rep. No. 1707, 89th Cong., 2d Sess. (1966) (providing background to enactment of § 351(e)).

� Rev. Proc. 62-32,1962-2 C.B. 527, provided that the IRS would not rule as to “[w]hether the transfer of appreciated stocks or securities to a newly organized investment company in exchange for shares of the stock of such investment company, as a result of solicitation by promoters, brokers or investment houses, will constitute nontaxable exchanges within the meaning of this section [351].”

� Swap funds continued to be organized relying on the advice of tax counsel

� § 351(e) (then § 351(d)) was enacted in 1966 to provide an additional requirement for qualifying under § 351

Section 351(e) – A Brief History (cont.)

Section 351(e) – Overview of Rules

� § 351(e)(1): A transfer of property to an investment company will not qualify for tax-free treatment under § 351

� The Code does not define an “investment company”

� Unlike § 721(b) (the parallel provision for partnerships), the provisiondoes not deny a loss for a transfer to an investment company

� Reg. § 1.351-1(c)(1): § 351(e) will apply if:

� The transfer results, directly or indirectly, in diversification of the transferors’ interests, AND

� The transferee is a (i) RIC, (ii) REIT, or (iii) corporation more than 80 percent the value of whose assets are specified assets that are held for investment (an “80% Corporation”)

� A transfer ordinarily results in diversification if two or more persons transfer nonidentical assets to a corporation in the exchange (unless each person is transferring a diversified portfolio of securities)

6

Section 351(e) – Overview of Rules (cont.)

� Under the regulations, the specified assets for purposes of determining an 80% Corporation were only readily marketable stocks or securities or interests in a RIC or REIT. Cash and non-convertible debt were excluded from the calculation.

� § 351(e) was amended in 1997 to expand the list of assets that canlead to investment company status

� Stocks and securities no longer need to be “readily marketable”

� Other assets, including cash, debt instruments, foreign currency, and certain precious metals, are now included

� Note that Reg. § 1.351-1(c) still contains the outdated list of assets

7

Determination of an Investment Company: Treatment of Cash

� Under § 351(e)’s expanded notion of an 80% Corporation, cash now counts if it is “held for investment”

� Reg. § 1.351-1(c)(3) only defines “held for investment” by reference to stock and securities: stock and securities will be considered held for investment unless they are (i) held primarily for sale to customers in the ordinary course of business or (ii) used in a banking, insurance, brokerage, or similar trade or business

� Presumably, this regulation should not be read to suggest that cash used for working capital needs of a non-financial business will be “held for investment”

8

Determination of an Investment Company: Treatment of Cash (cont.)

� What should updated regulations provide? What if cash is temporarily invested in anticipation of use in a business?

� Reg. § 1.351-1(c)(2) provides: “The determination of whether a corporation is an investment company shall ordinarily be made byreference to the circumstances in existence immediately after the transfer in question. However, where circumstances change thereafter pursuant to a plan in existence at the time of the transfer, this determination shall be made by reference to the latter circumstances.”

� The Senate Report reiterates that if cash is contributed and non-investment assets are purchased pursuant to a plan, the investment company determination will be made after such events. See S. Rep. No. 105-33, 105th Cong., 1st Sess. 131 (1997) (the “1997 Senate Report”).

� What if the plan is a very long term plan?

9

Determination of an Investment Company: Treatment of Cash – Example

10

StartupCo

$85cashIP

worth $15

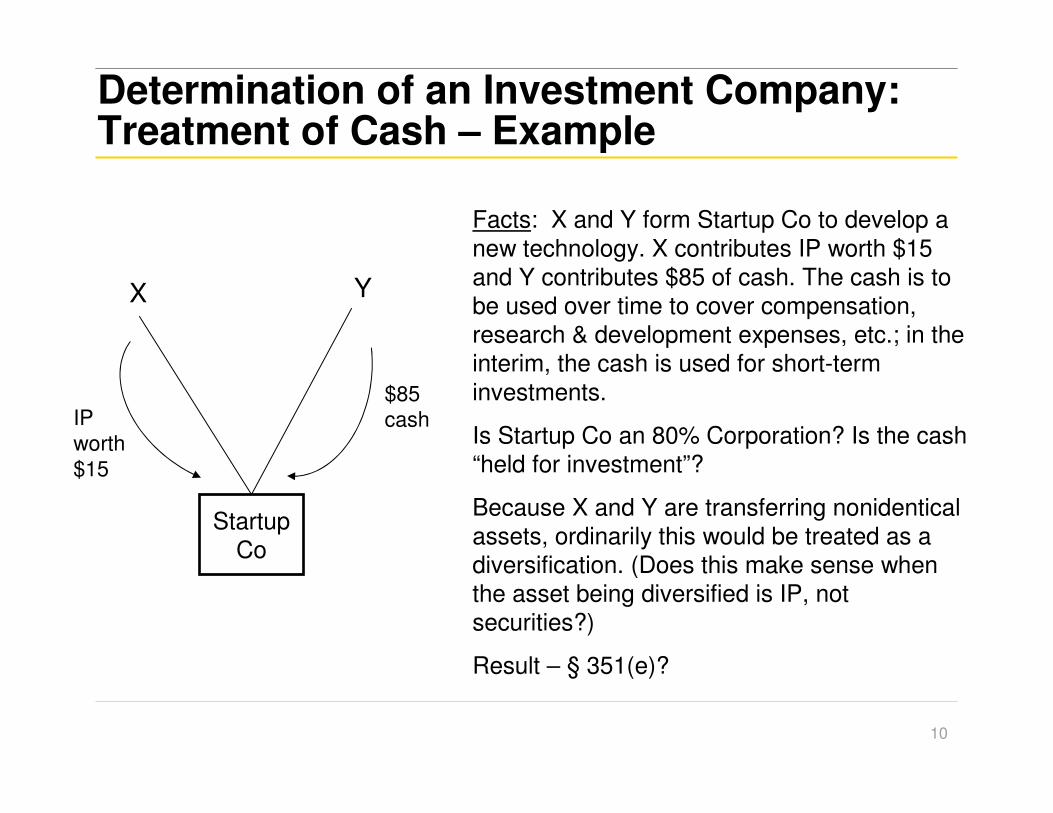

Facts: X and Y form Startup Co to develop a new technology. X contributes IP worth $15 and Y contributes $85 of cash. The cash is to be used over time to cover compensation, research & development expenses, etc.; in the interim, the cash is used for short-term investments.

Is Startup Co an 80% Corporation? Is the cash “held for investment”?

Because X and Y are transferring nonidentical assets, ordinarily this would be treated as a diversification. (Does this make sense when the asset being diversified is IP, not securities?)

Result – § 351(e)?

X Y

Determination of an Investment Company: Subsidiary Look-Through Rule

� Reg. § 1.351-1(c)(4): stock and securities in subsidiary corporations are disregarded and the parent corporation is deemed to own its ratable share of its subsidiaries’ assets. A corporation shall be considered a subsidiary if the parent owns 50% or more of (i) the combined voting power of all classes of stock entitled to vote or (ii) the total value of shares of all classes of stock outstanding.

� The 50% look-through rule does not include any attribution rules.

� Absent the look-through rule, stock of a subsidiary generally would be a tainted asset because stock will be treated as “held for investment” unless it is held for sale to customers in the ordinary course or used as part of a finance-related business.

11

12

Determination of an Investment Company: Subsidiary Look-Through Rule – Example

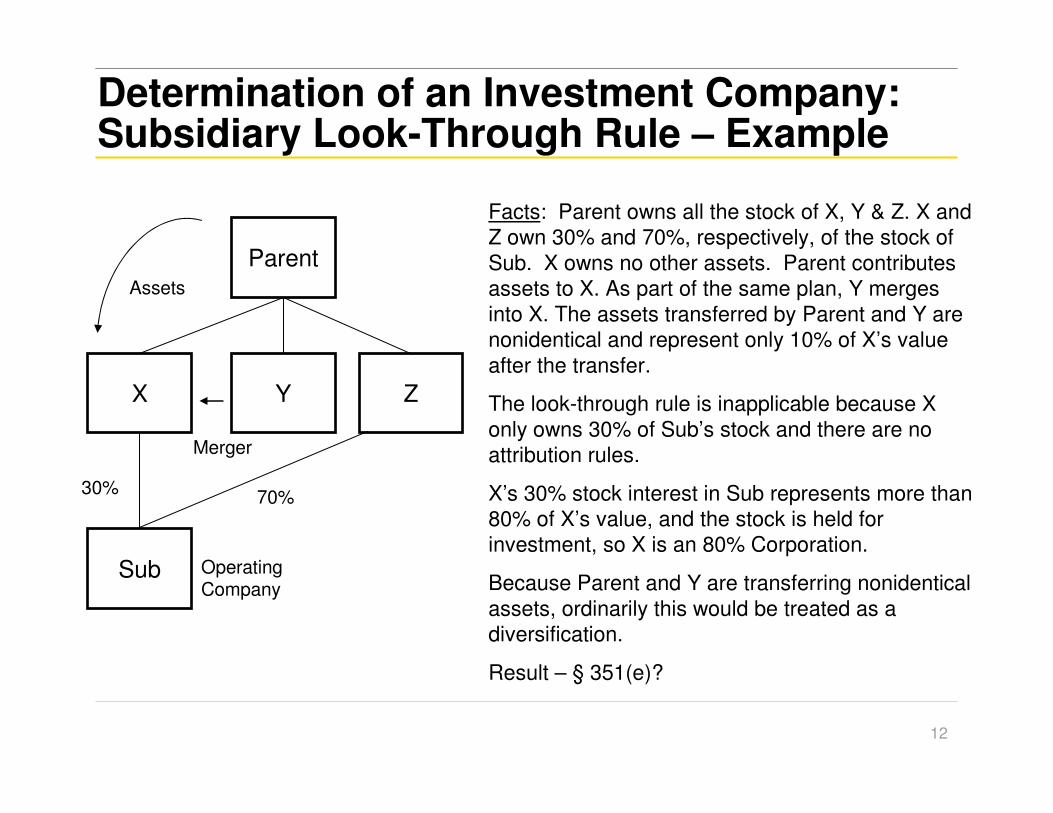

Facts: Parent owns all the stock of X, Y & Z. X and Z own 30% and 70%, respectively, of the stock of Sub. X owns no other assets. Parent contributes assets to X. As part of the same plan, Y merges into X. The assets transferred by Parent and Y are nonidentical and represent only 10% of X’s value after the transfer.

The look-through rule is inapplicable because X only owns 30% of Sub’s stock and there are no attribution rules.

X’s 30% stock interest in Sub represents more than 80% of X’s value, and the stock is held for investment, so X is an 80% Corporation.

Because Parent and Y are transferring nonidentical assets, ordinarily this would be treated as a diversification.

Result – § 351(e)?

Parent

X

Sub

Assets

Z

30%70%

Y

Merger

Operating Company

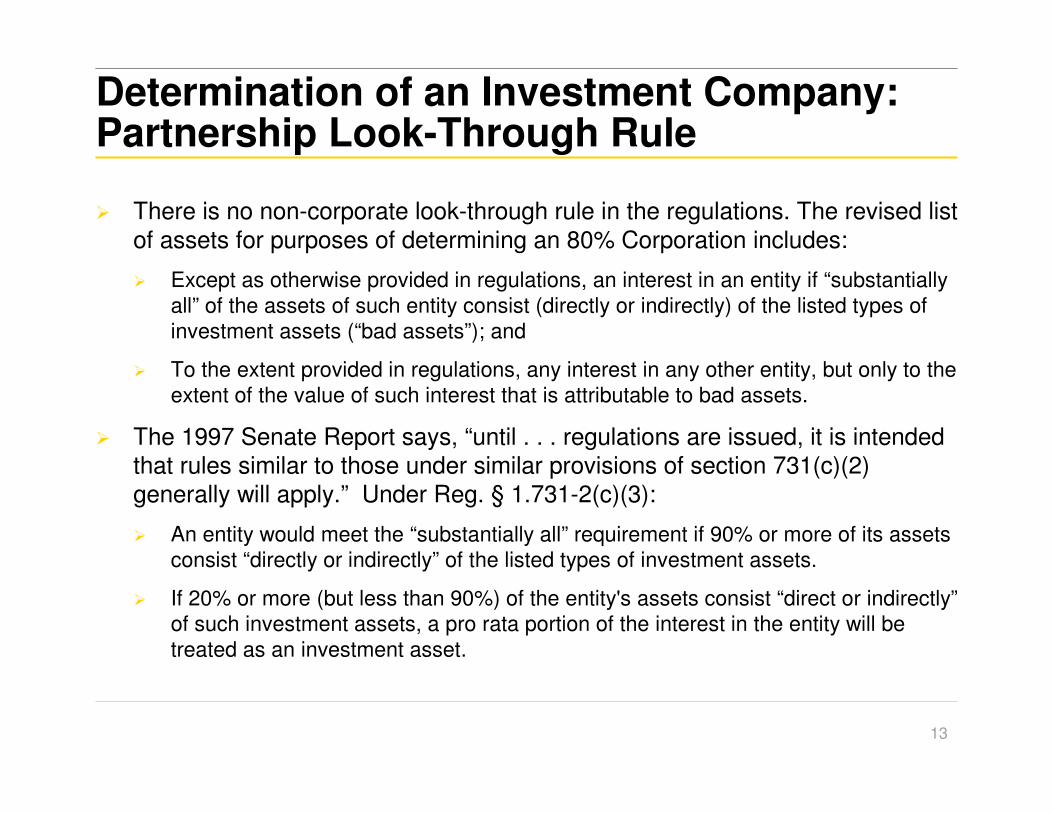

Determination of an Investment Company: Partnership Look-Through Rule

� There is no non-corporate look-through rule in the regulations. The revised list of assets for purposes of determining an 80% Corporation includes:

� Except as otherwise provided in regulations, an interest in an entity if “substantially all” of the assets of such entity consist (directly or indirectly) of the listed types of investment assets (“bad assets”); and

� To the extent provided in regulations, any interest in any other entity, but only to the extent of the value of such interest that is attributable to bad assets.

� The 1997 Senate Report says, “until . . . regulations are issued, it is intended that rules similar to those under similar provisions of section 731(c)(2) generally will apply.” Under Reg. § 1.731-2(c)(3):

� An entity would meet the “substantially all” requirement if 90% or more of its assets consist “directly or indirectly” of the listed types of investment assets.

� If 20% or more (but less than 90%) of the entity's assets consist “direct or indirectly”of such investment assets, a pro rata portion of the interest in the entity will be treated as an investment asset.

13

Determination of an Investment Company: Partnership Look-Through Rule (cont.)

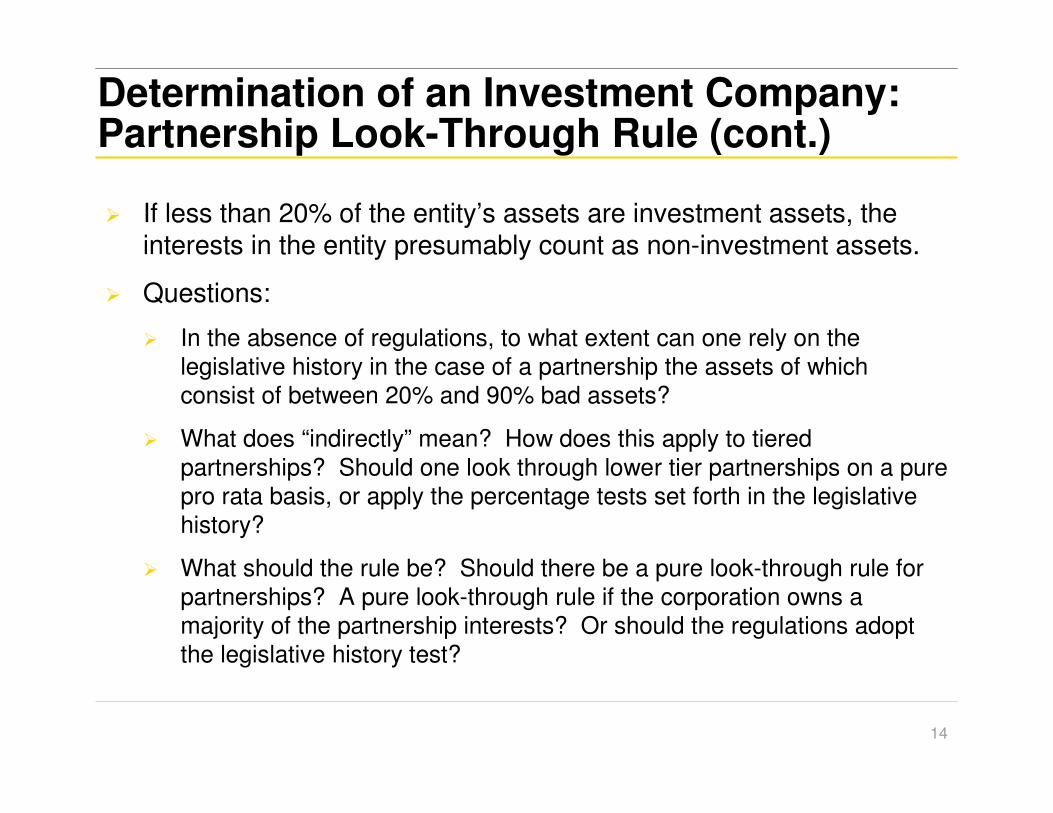

� If less than 20% of the entity’s assets are investment assets, the interests in the entity presumably count as non-investment assets.

� Questions:

� In the absence of regulations, to what extent can one rely on the legislative history in the case of a partnership the assets of which consist of between 20% and 90% bad assets?

� What does “indirectly” mean? How does this apply to tiered partnerships? Should one look through lower tier partnerships on a pure pro rata basis, or apply the percentage tests set forth in the legislative history?

� What should the rule be? Should there be a pure look-through rule for partnerships? A pure look-through rule if the corporation owns a majority of the partnership interests? Or should the regulations adopt the legislative history test?

14

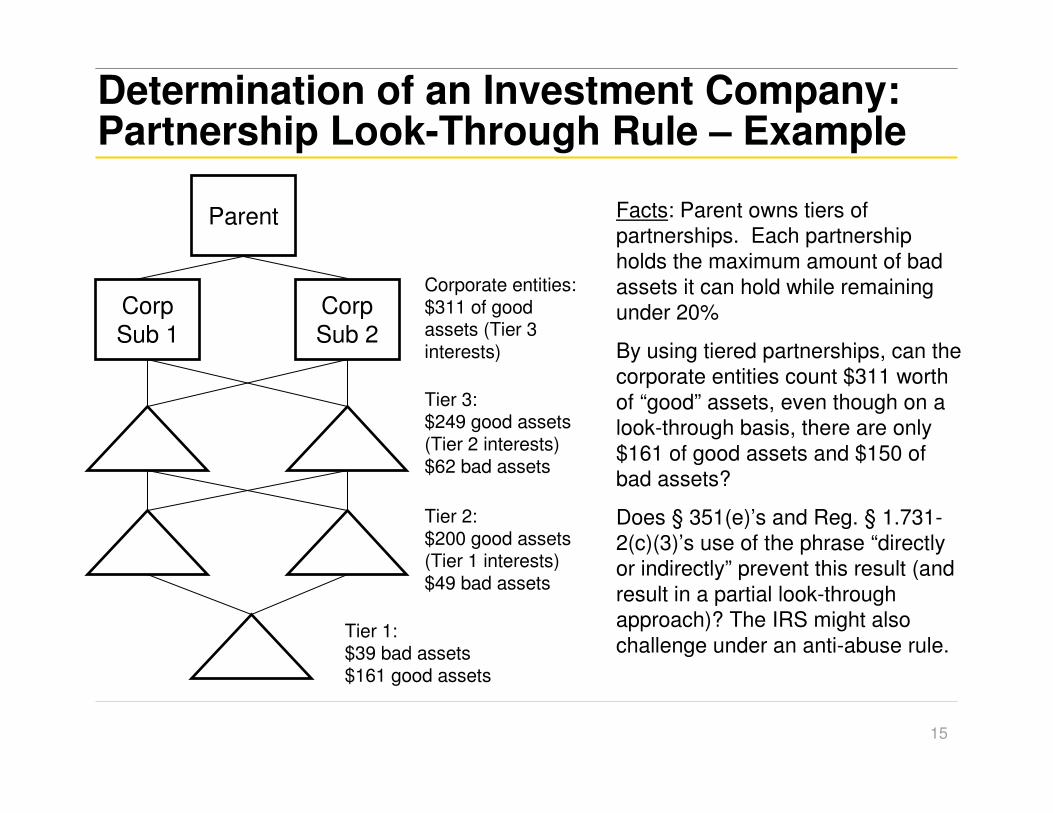

Determination of an Investment Company: Partnership Look-Through Rule – Example

Facts: Parent owns tiers of partnerships. Each partnership holds the maximum amount of bad assets it can hold while remaining under 20%

By using tiered partnerships, can the corporate entities count $311 worth of “good” assets, even though on a look-through basis, there are only $161 of good assets and $150 of bad assets?

Does § 351(e)’s and Reg. § 1.731-2(c)(3)’s use of the phrase “directly or indirectly” prevent this result (and result in a partial look-through approach)? The IRS might also challenge under an anti-abuse rule.

15

Tier 1:$39 bad assets$161 good assets

Tier 2:$200 good assets (Tier 1 interests)$49 bad assets

Tier 3:$249 good assets (Tier 2 interests)$62 bad assets

Parent

CorpSub 1

Corp Sub 2

Corporate entities:$311 of good assets (Tier 3 interests)

Diversification: “Nonidentical” Assets

� Reg. § 1.351-1(c)(5): diversification ordinarily results if two or more transferors transfer “nonidentical” assets

� No definition of “nonidentical” – is there leeway for slight variances?

� What about common stock and preferred stock of the same company?

� Bonds of the same company with different interest rates?

� Does this rule make sense outside of the context of investment assets? Why should transfers of two different pieces of equipment be treated as a diversification?

� Reg. § 1.351-1(c)(5) states that a transfer by a single transferor, or by multiple transferors of identical assets, to a newly formed company would not generally result in diversification

� How do you judge diversification for a transfer to an existing company?

16

17

Diversification: Cash as Diversifying Asset

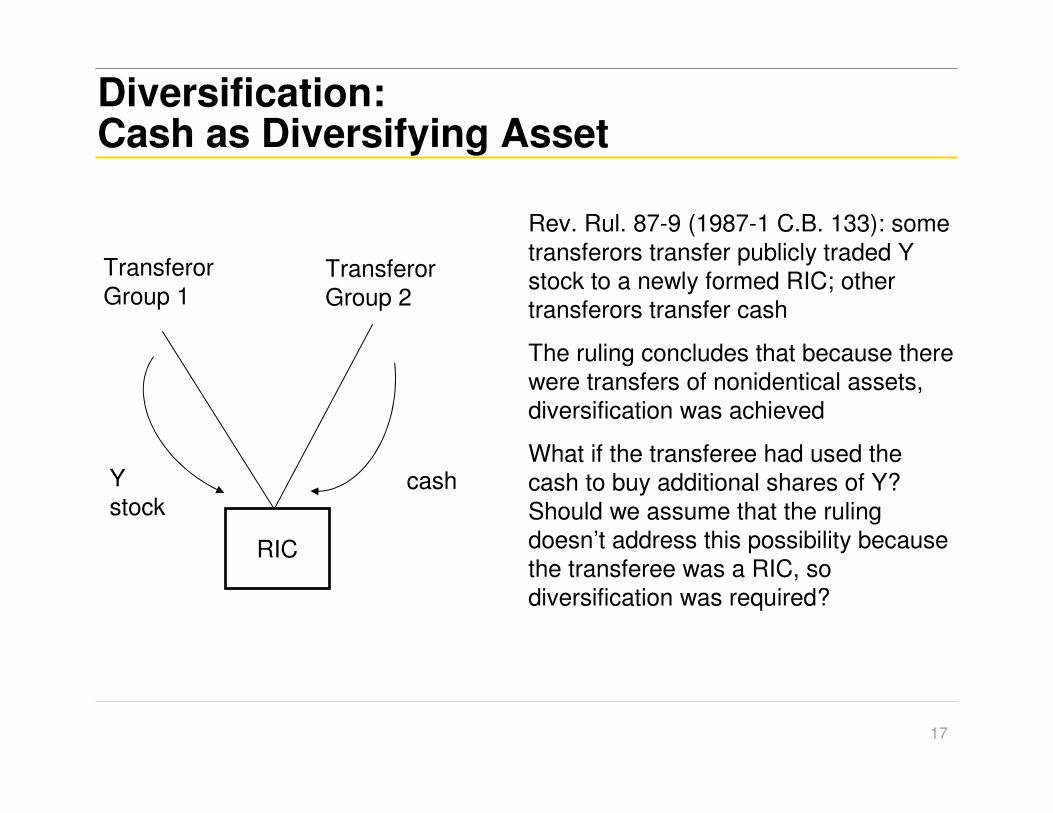

Rev. Rul. 87-9 (1987-1 C.B. 133): some transferors transfer publicly traded Y stock to a newly formed RIC; other transferors transfer cash

The ruling concludes that because there were transfers of nonidentical assets, diversification was achieved

What if the transferee had used the cash to buy additional shares of Y? Should we assume that the ruling doesn’t address this possibility because the transferee was a RIC, so diversification was required?

cashYstock

Transferor Group 1

Transferor Group 2

RIC

Diversification: Cash as Diversifying Asset (cont.)

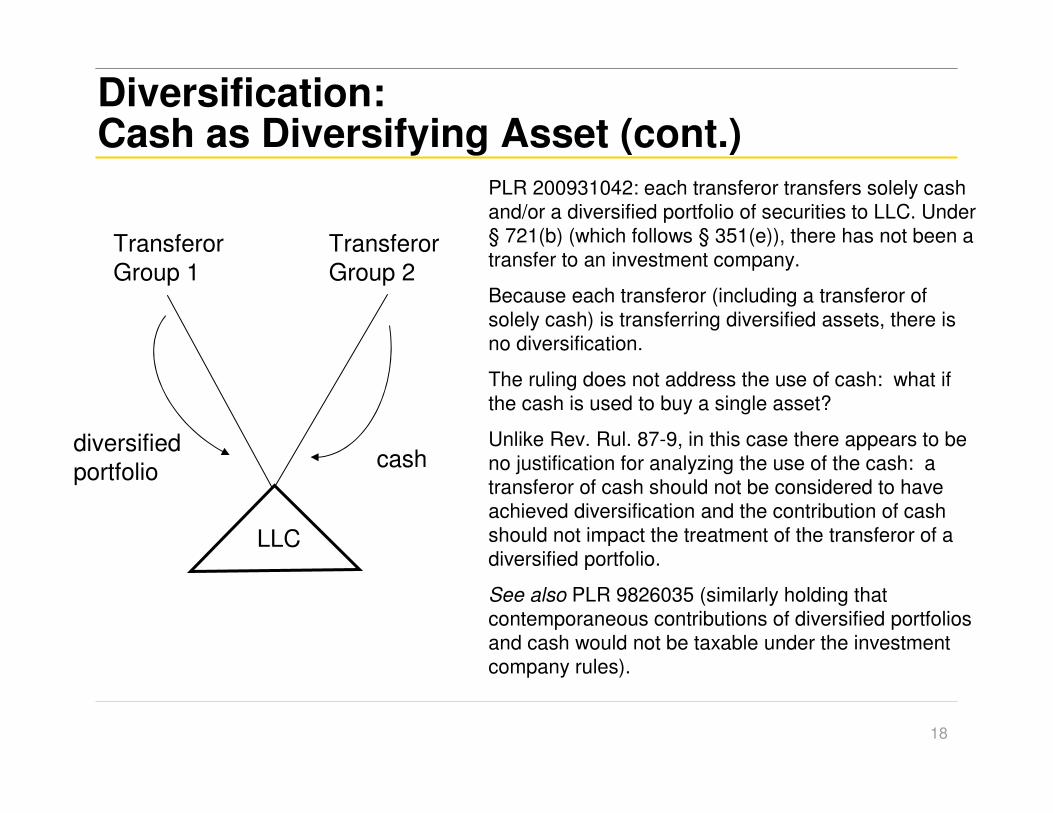

PLR 200931042: each transferor transfers solely cash and/or a diversified portfolio of securities to LLC. Under § 721(b) (which follows § 351(e)), there has not been a transfer to an investment company.

Because each transferor (including a transferor of solely cash) is transferring diversified assets, there is no diversification.

The ruling does not address the use of cash: what if the cash is used to buy a single asset?

Unlike Rev. Rul. 87-9, in this case there appears to be no justification for analyzing the use of the cash: a transferor of cash should not be considered to have achieved diversification and the contribution of cash should not impact the treatment of the transferor of a diversified portfolio.

See also PLR 9826035 (similarly holding that contemporaneous contributions of diversified portfolios and cash would not be taxable under the investment company rules).

18

cashdiversified portfolio

Transferor Group 1

Transferor Group 2

LLC

Diversification:De Minimis Rule� Reg. § 1.351-1(c)(5): If a transaction involves one or more transfers of nonidentical assets

that, in the aggregate, constitute an insignificant portion of the total value of the assets transferred, those transfers are ignored in determining if diversification has occurred

� How much is an “insignificant portion”?

� Reg. § 1.351-1(c)(7) Ex. 1 provides that nonidentical assets were an “insignificant portion”where they equaled 0.99% of the total assets transferred to a new corporation

� Reg. § 1.351-1(c)(7) Ex. 2 illustrates that transfers must be aggregated in determining significance: many small transfers of nonidentical assets aggregated to a significant number

� PLR 200006008 – in a § 721(b) ruling, transfers of nonidentical assets amounting to less than 5% of the total value of the assets transferred to an LLC were treated as insignificant for purposes of determining whether diversification exists.

� In Rev. Rul. 87-9 (discussed above), one transferor’s contribution of cash amounting to 11% of total assets was enough to cause a transfer of securities by the other transferor to be taxable.

� If one or more transferors transfer identical assets to an existing corporation that holds nonidentical assets, and the transfer is potentially treated as resulting in diversification, is a de minimis rule available?

19

Diversification: “Nonidentical” Assets & De Minimis Rule – Example

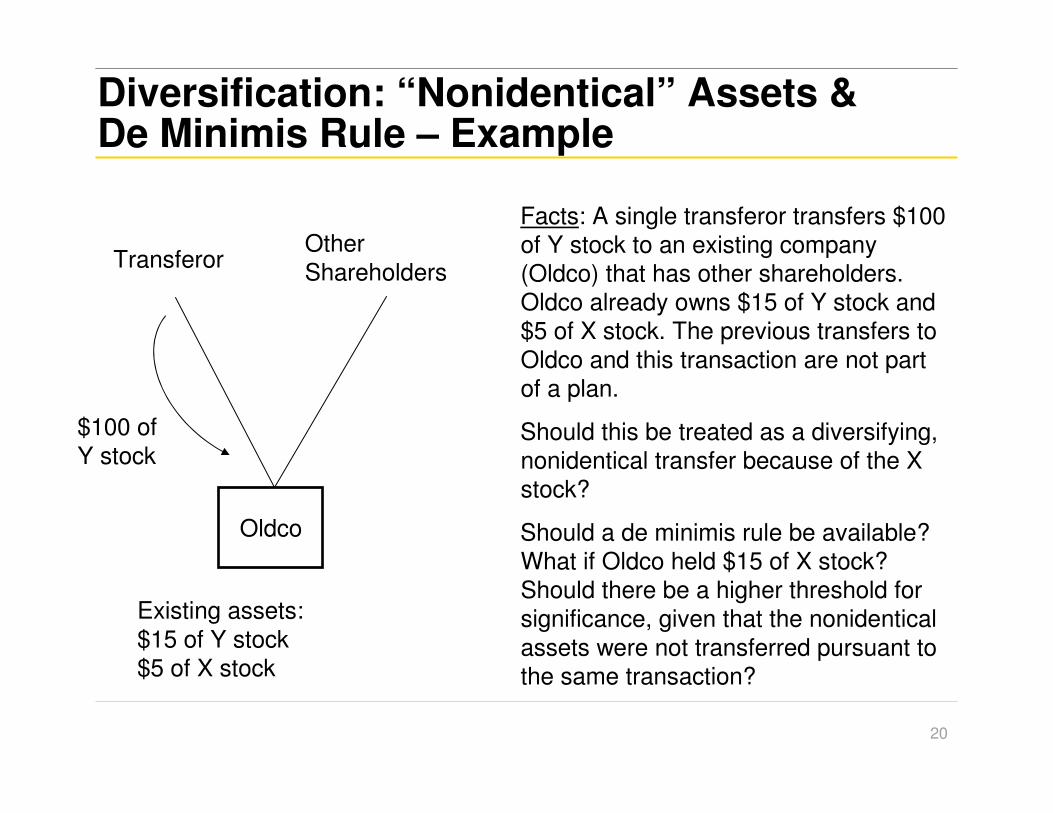

Facts: A single transferor transfers $100 of Y stock to an existing company (Oldco) that has other shareholders. Oldco already owns $15 of Y stock and $5 of X stock. The previous transfers to Oldco and this transaction are not part of a plan.

Should this be treated as a diversifying, nonidentical transfer because of the X stock?

Should a de minimis rule be available? What if Oldco held $15 of X stock? Should there be a higher threshold for significance, given that the nonidentical assets were not transferred pursuant to the same transaction?

20

Oldco

TransferorOther Shareholders

Existing assets:$15 of Y stock$5 of X stock

$100 of Y stock

Diversification:Scope of the Plan

� Reg. § 1.351-1(c)(5): “If a transfer is part of a plan to achieve diversification without recognition of gain, such as a plan which contemplates a subsequent transfer, however delayed, of the corporate assets (or of the stock or securities received in the earlier exchange) to an investment company in a transaction purporting to qualify for nonrecognition treatment, the original transfer will be treated as resulting in diversification.”

� What is the significance of the phrase “however delayed”? Is there an implication that “plan” is a particularly broad concept in this context?

21

Diversification:Testing under the 25/50 Test

� Reg. §1.351-1(c)(6): A transfer of stocks and securities will not be treatedas resulting in diversification if each transferor transfers an already diversified portfolio of stocks and securities

� A portfolio is diverse if it meets the 25% and 50% tests of § 368(a)(2)(F)(ii): not more than 25% of the value of the portfolio is stock and securities of any one issuer and not more than 50% of the value of the portfolio is stock and securities of 5 or fewer issuers

� Members of a controlled group of corporations are treated as a single issuer

� A person holding stock in a RIC, REIT or investment company that meets the 25% and 50% tests is, except as provided in regulations, treated as holding a proportionate share of that company’s assets

� Note that for this purpose (but perhaps not for purposes of the definition of “nonidentical”) different securities of the same issuer are aggregated

22

Diversification:Testing under the 25/50 Test (cont.)

� Government securities are included in the portfolio for purposes of the denominator of the 25% and 50% tests (unless they “are acquired” to meet the tests), but are not treated as securities of an issuer for purposes of the numerator.

� See Preamble to Proposed Regulations (1995-2 C.B. 464) (stating that the purpose of the Reg. § 1.351-1(c) government securities rule is to permit tax-free incorporation of funds consisting “mostly” of government securities).

� Why a different rule for government securities here than when testing under § 368(a)(2)(F)(ii)? For purposes of § 368(a)(2)(F)(ii), cash and cash items and government securities are not included in total assets.

� What does the regulation mean when it states that government securities do not count if they “are acquired” to meet the 25% and 50% tests? Does this mean acquired by the transferor or acquired by the corporation as part of the plan?

� Does it work, for instance, if the transferor already owns government securities, but includes them in the portfolio to meet the test?

� Should there be an analogous diversification exception for other types of assets? If, for instance, two transferors each contribute a portfolio of real property, should diversification result?

23

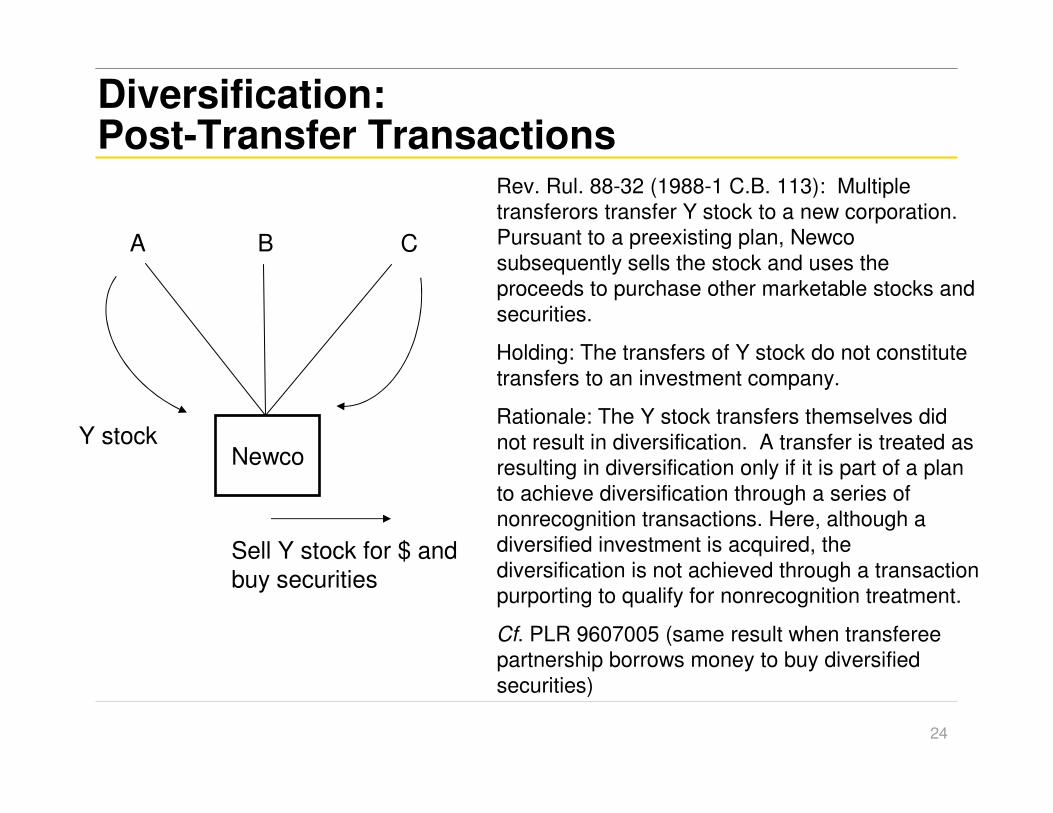

Diversification:Post-Transfer Transactions

Rev. Rul. 88-32 (1988-1 C.B. 113): Multiple transferors transfer Y stock to a new corporation. Pursuant to a preexisting plan, Newco subsequently sells the stock and uses the proceeds to purchase other marketable stocks and securities.

Holding: The transfers of Y stock do not constitute transfers to an investment company.

Rationale: The Y stock transfers themselves did not result in diversification. A transfer is treated as resulting in diversification only if it is part of a plan to achieve diversification through a series of nonrecognition transactions. Here, although a diversified investment is acquired, the diversification is not achieved through a transaction purporting to qualify for nonrecognition treatment.

Cf. PLR 9607005 (same result when transferee partnership borrows money to buy diversified securities)

24

A B C

Y stock

Sell Y stock for $ andbuy securities

Newco

One Bad Apple

� If multiple transferors transfer property to an investment company in a single transaction, and one of the transferors achieves diversification, § 351(e) denies tax-free treatment to all of the transferors

� § 351 applies, or doesn’t apply, to the transfer of property by one or more persons to a corporation. Pursuant to § 351(e) and Reg. § 1.351-1(c)(1), § 351 does not apply if property is transferred to an investment company, and the regulation provides that a transfer will be treated as a transfer to an investment company if the transfer results, directly or indirectly, in diversification of the “transferors’ interests”.

� Does this make sense, given that the reason for the provision is to prevent persons from achieving tax-free diversification? Shouldn’t only the diversifying transferor be subject to tax?

� What if transferors who collectively have § 368(c) control after the exchange do not diversify their interests, but an additional transferor does? Can one bad transferor bust a § 351 exchange if there would be a good § 351 exchange without that transferor?

25

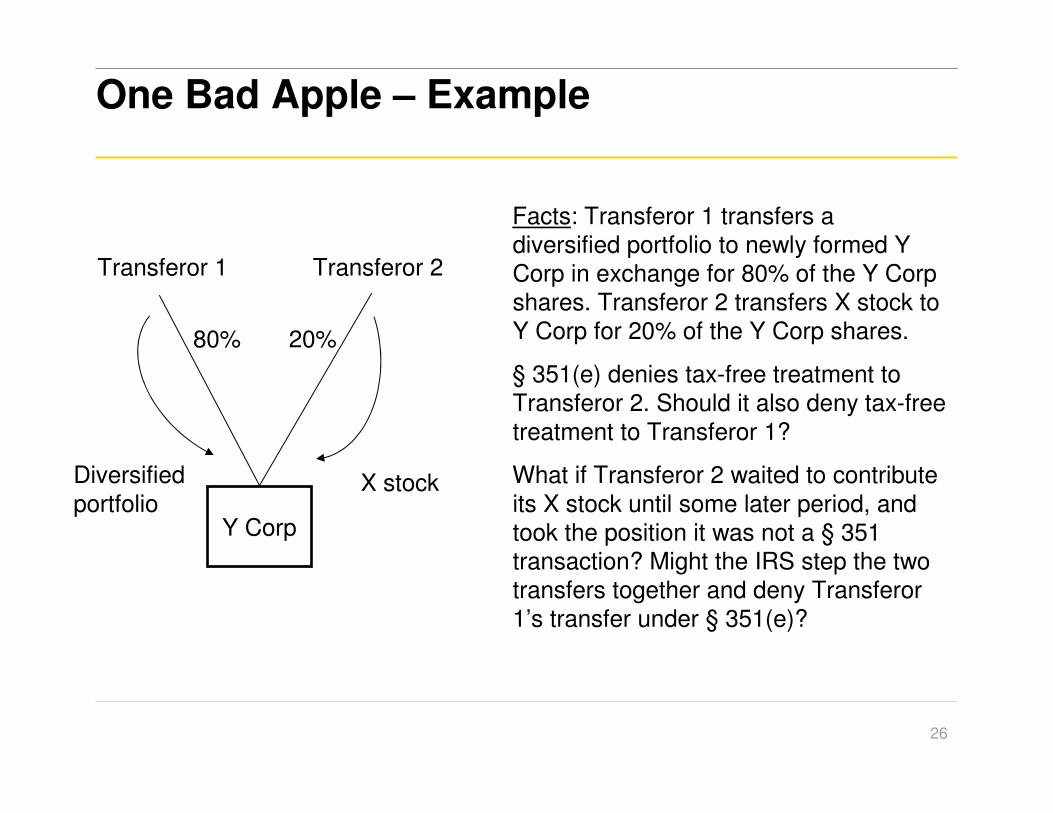

One Bad Apple – Example

Facts: Transferor 1 transfers a diversified portfolio to newly formed Y Corp in exchange for 80% of the Y Corp shares. Transferor 2 transfers X stock to Y Corp for 20% of the Y Corp shares.

§ 351(e) denies tax-free treatment to Transferor 2. Should it also deny tax-free treatment to Transferor 1?

What if Transferor 2 waited to contribute its X stock until some later period, and took the position it was not a § 351 transaction? Might the IRS step the two transfers together and deny Transferor 1’s transfer under § 351(e)?

26

Y Corp

Diversified portfolio

Transferor 1 Transferor 2

X stock

80% 20%

Affirmative Use of Section 351(e)

� As noted above, § 351(e) does not prohibit the recognition of a loss (unlike § 721(b) which only triggers gain on transfers to an investment partnership)

� Could § 351(e) therefore be used to bust a § 351 transaction?

� For instance, if transferors of a diversified portfolio want to recognize a loss, could they cause another transferor to transfer a non-diversified stock or security?

� Other loss disallowance rules (such as § 267) would still apply

27

28

Section 368(a)(2)(F)

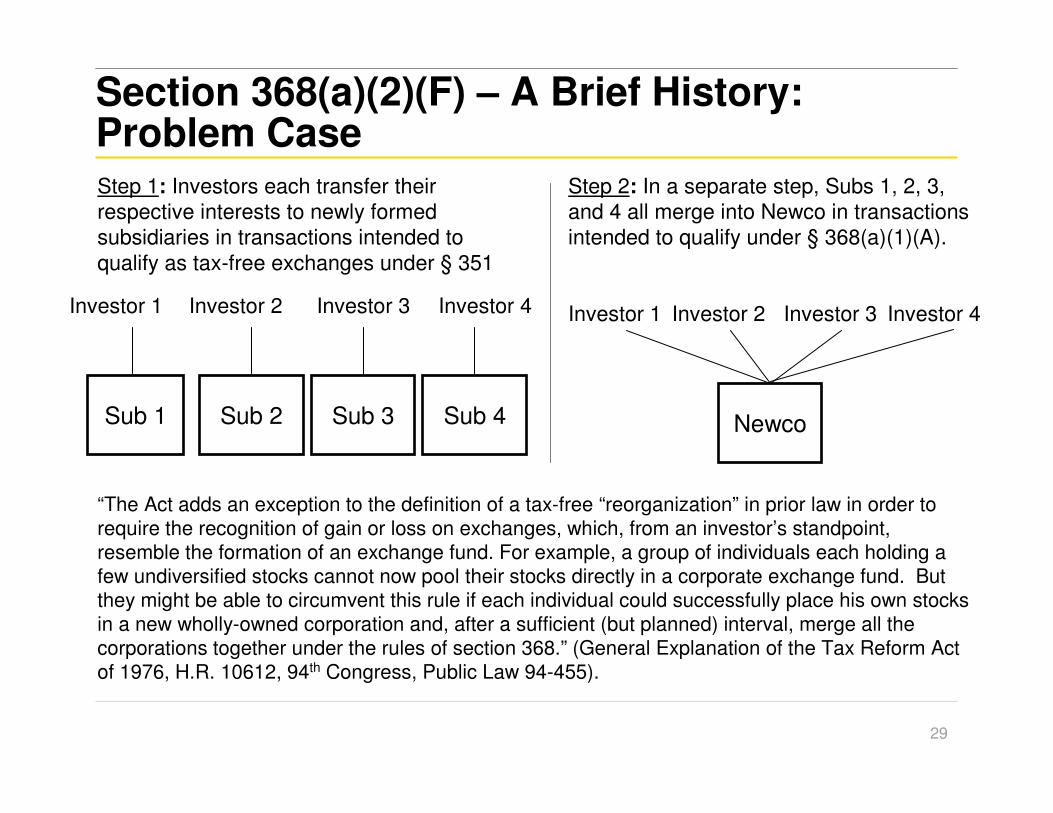

Section 368(a)(2)(F) – A Brief History:Problem Case

29

Investor 1 Investor 2

“The Act adds an exception to the definition of a tax-free “reorganization” in prior law in order to require the recognition of gain or loss on exchanges, which, from an investor’s standpoint, resemble the formation of an exchange fund. For example, a group of individuals each holding a few undiversified stocks cannot now pool their stocks directly in a corporate exchange fund. But they might be able to circumvent this rule if each individual could successfully place his own stocks in a new wholly-owned corporation and, after a sufficient (but planned) interval, merge all the corporations together under the rules of section 368.” (General Explanation of the Tax Reform Act of 1976, H.R. 10612, 94th Congress, Public Law 94-455).

Sub 1 Sub 2 Sub 3 Sub 4

Investor 3 Investor 4 Investor 2 Investor 3 Investor 4Investor 1

Newco

Step 1: Investors each transfer their respective interests to newly formed subsidiaries in transactions intended to qualify as tax-free exchanges under § 351

Step 2: In a separate step, Subs 1, 2, 3, and 4 all merge into Newco in transactions intended to qualify under § 368(a)(1)(A).

Overview of Rules

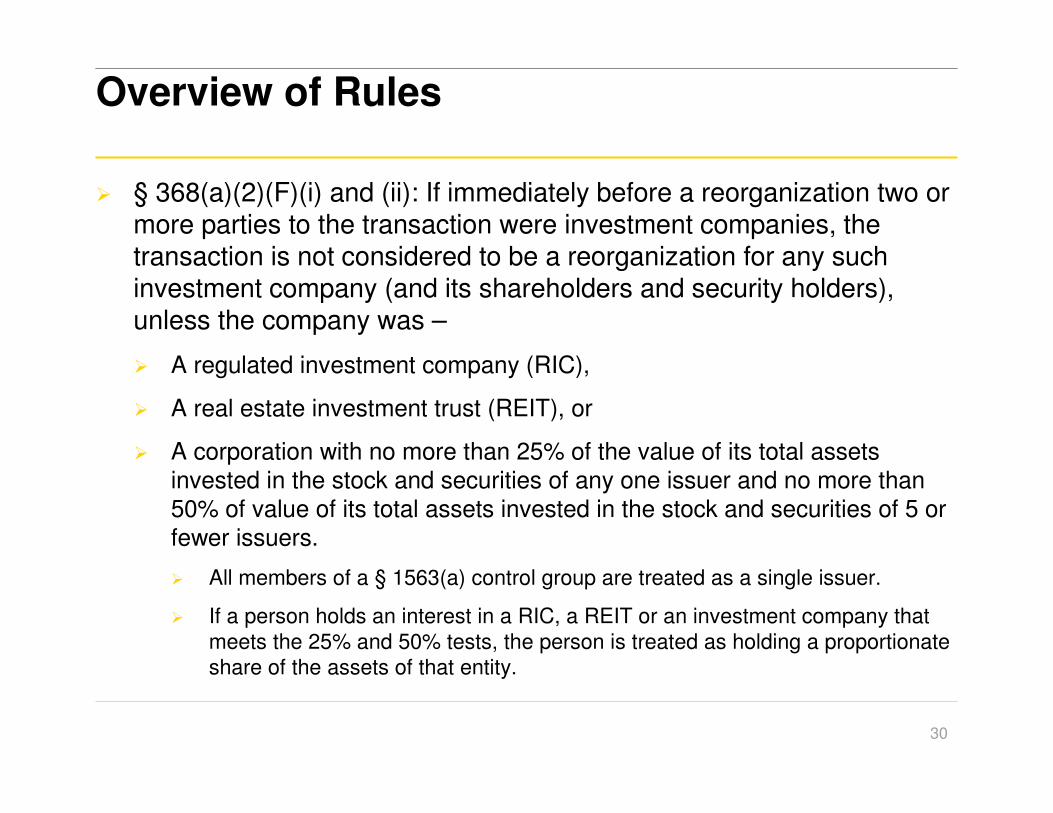

� § 368(a)(2)(F)(i) and (ii): If immediately before a reorganization two or more parties to the transaction were investment companies, the transaction is not considered to be a reorganization for any such investment company (and its shareholders and security holders), unless the company was –

� A regulated investment company (RIC),

� A real estate investment trust (REIT), or

� A corporation with no more than 25% of the value of its total assets invested in the stock and securities of any one issuer and no more than 50% of value of its total assets invested in the stock and securities of 5 or fewer issuers.

� All members of a § 1563(a) control group are treated as a single issuer.

� If a person holds an interest in a RIC, a REIT or an investment company that meets the 25% and 50% tests, the person is treated as holding a proportionate share of the assets of that entity.

30

Overview of Rules (cont.):Investment Company and Total Assets

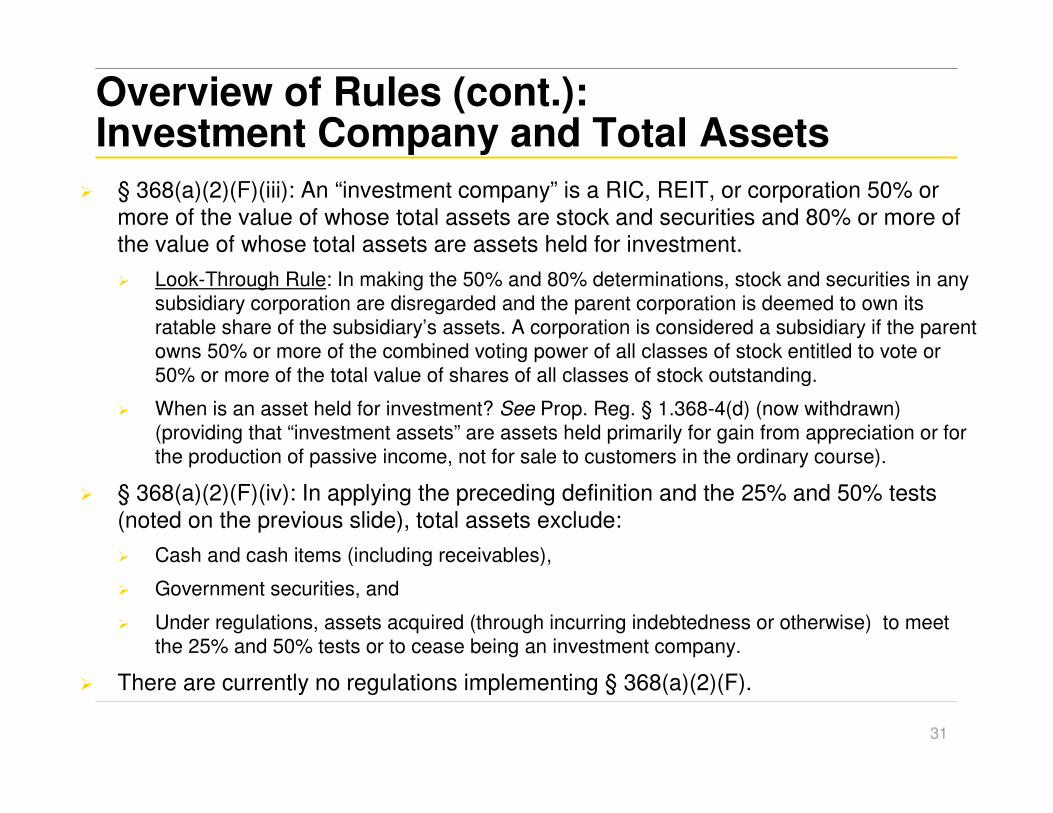

� § 368(a)(2)(F)(iii): An “investment company” is a RIC, REIT, or corporation 50% or more of the value of whose total assets are stock and securities and 80% or more of the value of whose total assets are assets held for investment.

� Look-Through Rule: In making the 50% and 80% determinations, stock and securities in any subsidiary corporation are disregarded and the parent corporation is deemed to own its ratable share of the subsidiary’s assets. A corporation is considered a subsidiary if the parentowns 50% or more of the combined voting power of all classes of stock entitled to vote or 50% or more of the total value of shares of all classes of stock outstanding.

� When is an asset held for investment? See Prop. Reg. § 1.368-4(d) (now withdrawn) (providing that “investment assets” are assets held primarily for gain from appreciation or for the production of passive income, not for sale to customers in the ordinary course).

� § 368(a)(2)(F)(iv): In applying the preceding definition and the 25% and 50% tests (noted on the previous slide), total assets exclude:

� Cash and cash items (including receivables),

� Government securities, and

� Under regulations, assets acquired (through incurring indebtedness or otherwise) to meet the 25% and 50% tests or to cease being an investment company.

� There are currently no regulations implementing § 368(a)(2)(F).

31

32

Overview of Rules (cont.):Securities

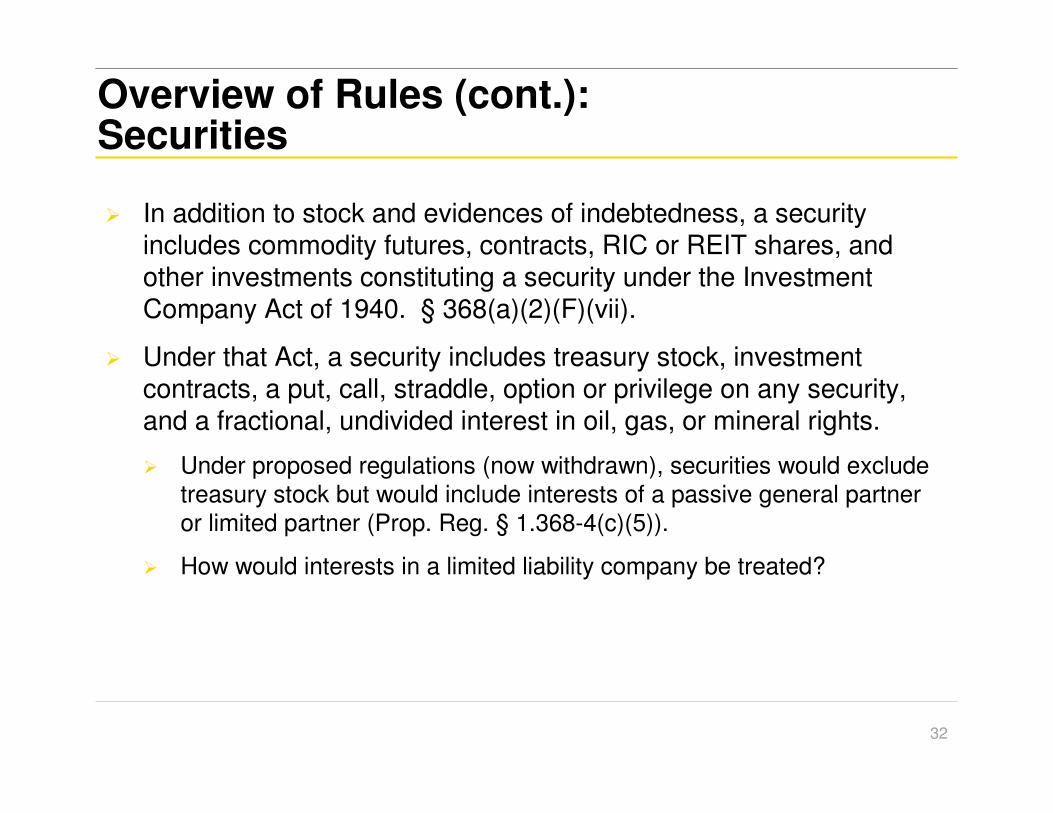

� In addition to stock and evidences of indebtedness, a security includes commodity futures, contracts, RIC or REIT shares, and other investments constituting a security under the Investment Company Act of 1940. § 368(a)(2)(F)(vii).

� Under that Act, a security includes treasury stock, investment contracts, a put, call, straddle, option or privilege on any security, and a fractional, undivided interest in oil, gas, or mineral rights.

� Under proposed regulations (now withdrawn), securities would exclude treasury stock but would include interests of a passive general partner or limited partner (Prop. Reg. § 1.368-4(c)(5)).

� How would interests in a limited liability company be treated?

33

Overview of Rules (cont.):Partnerships

� Under proposed regulations (now withdrawn) –

� If a partner’s interest in a partnership is not a security, the partner is deemed to own a ratable share of each asset held by the partnership. Prop. Reg. § 1.368-4(f).

� A corporate partner is deemed to own a ratable share of partnership assets if it has a direct or indirect 50% interest in the partnership’s income or capital. Prop. Reg. § 1.368-4(g)(5) and (6).

� In either case, the ratable share is determined based on all facts and circumstances.

34

Overview of Rules (cont.): Other Rules

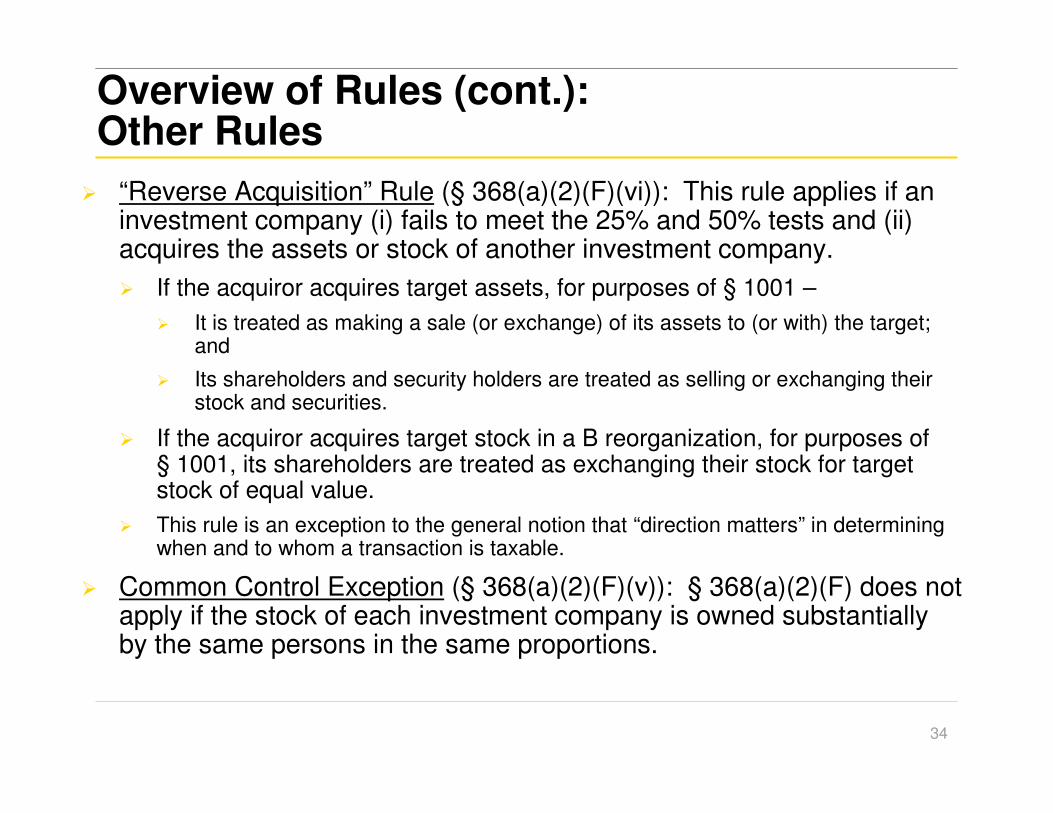

� “Reverse Acquisition” Rule (§ 368(a)(2)(F)(vi)): This rule applies if an investment company (i) fails to meet the 25% and 50% tests and (ii) acquires the assets or stock of another investment company.

� If the acquiror acquires target assets, for purposes of § 1001 –

� It is treated as making a sale (or exchange) of its assets to (or with) the target; and

� Its shareholders and security holders are treated as selling or exchanging their stock and securities.

� If the acquiror acquires target stock in a B reorganization, for purposes of § 1001, its shareholders are treated as exchanging their stock for target stock of equal value.

� This rule is an exception to the general notion that “direction matters” in determining when and to whom a transaction is taxable.

� Common Control Exception (§ 368(a)(2)(F)(v)): § 368(a)(2)(F) does not apply if the stock of each investment company is owned substantially by the same persons in the same proportions.

35

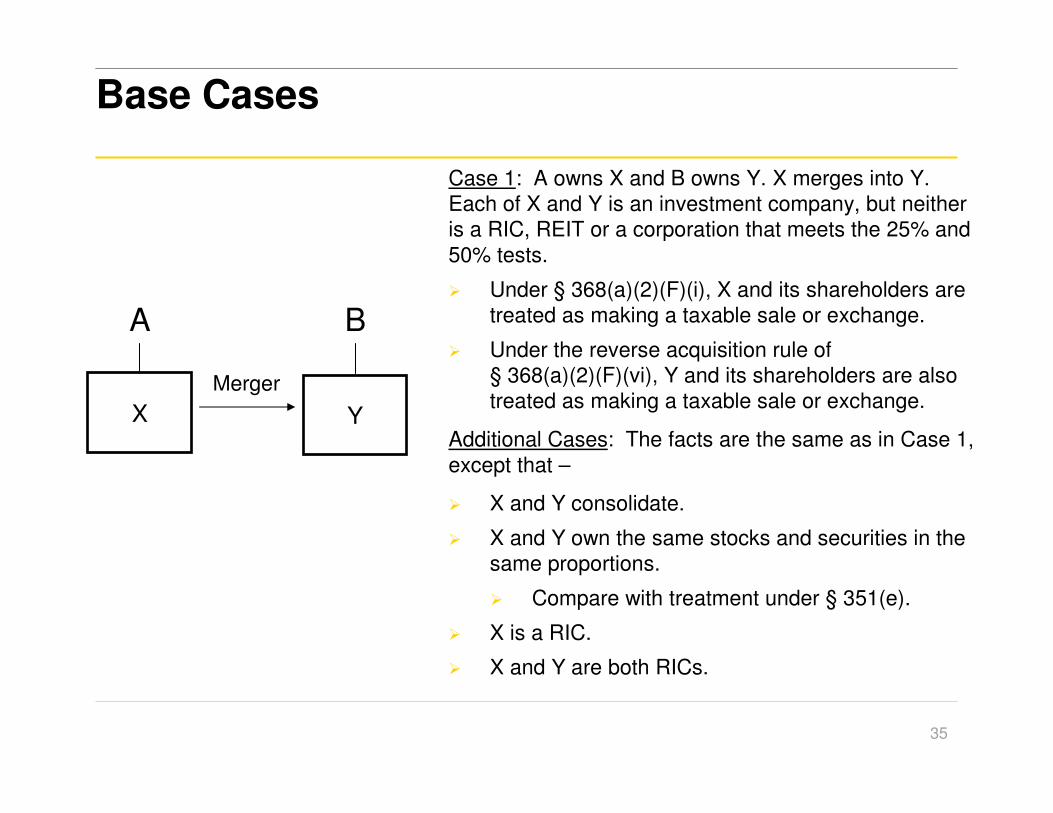

Base Cases

Case 1: A owns X and B owns Y. X merges into Y. Each of X and Y is an investment company, but neither is a RIC, REIT or a corporation that meets the 25% and 50% tests.

� Under § 368(a)(2)(F)(i), X and its shareholders are treated as making a taxable sale or exchange.

� Under the reverse acquisition rule of § 368(a)(2)(F)(vi), Y and its shareholders are also treated as making a taxable sale or exchange.

Additional Cases: The facts are the same as in Case 1, except that –

� X and Y consolidate.

� X and Y own the same stocks and securities in the same proportions.

� Compare with treatment under § 351(e).

� X is a RIC.

� X and Y are both RICs.

YX

Merger

A B

36

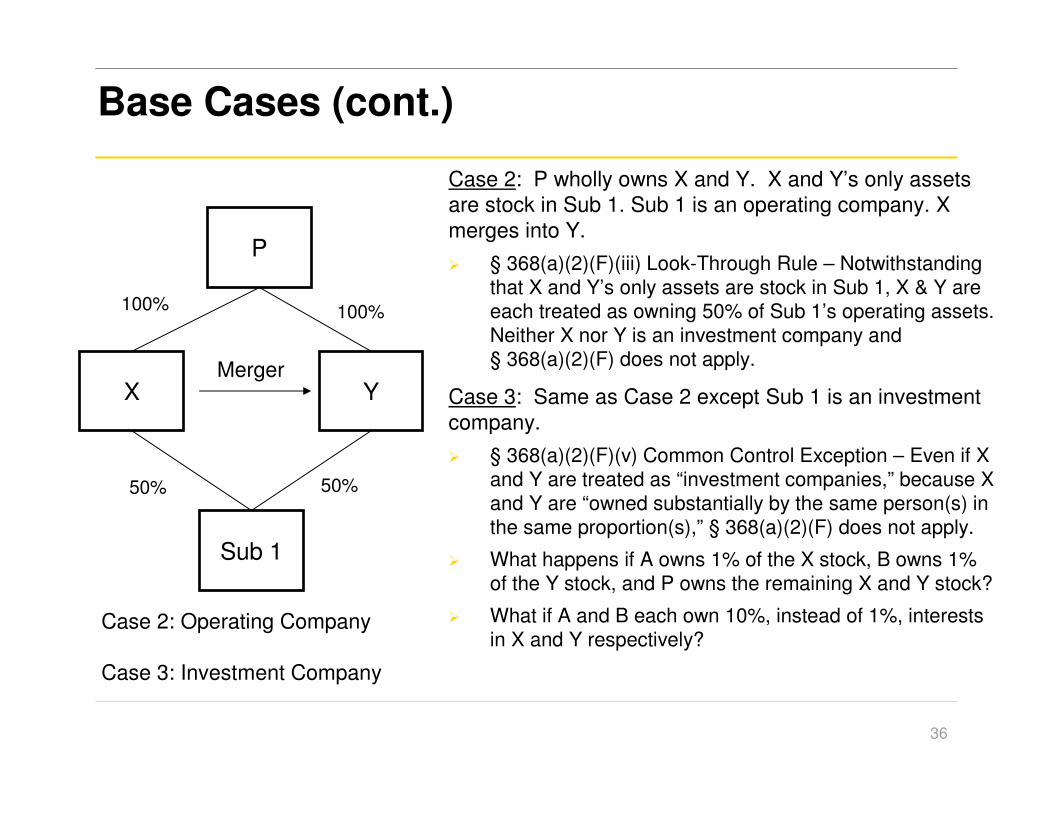

Case 2: P wholly owns X and Y. X and Y’s only assets are stock in Sub 1. Sub 1 is an operating company. X merges into Y.

� § 368(a)(2)(F)(iii) Look-Through Rule – Notwithstanding that X and Y’s only assets are stock in Sub 1, X & Y are each treated as owning 50% of Sub 1’s operating assets. Neither X nor Y is an investment company and § 368(a)(2)(F) does not apply.

Case 3: Same as Case 2 except Sub 1 is an investment company.

� § 368(a)(2)(F)(v) Common Control Exception – Even if X and Y are treated as “investment companies,” because X and Y are “owned substantially by the same person(s) in the same proportion(s),” § 368(a)(2)(F) does not apply.

� What happens if A owns 1% of the X stock, B owns 1% of the Y stock, and P owns the remaining X and Y stock?

� What if A and B each own 10%, instead of 1%, interests in X and Y respectively?

P

YX

Sub 1

50% 50%

Merger

Case 2: Operating Company

Case 3: Investment Company

100% 100%

Base Cases (cont.)

37

Problem Cases: Look-Through Rule

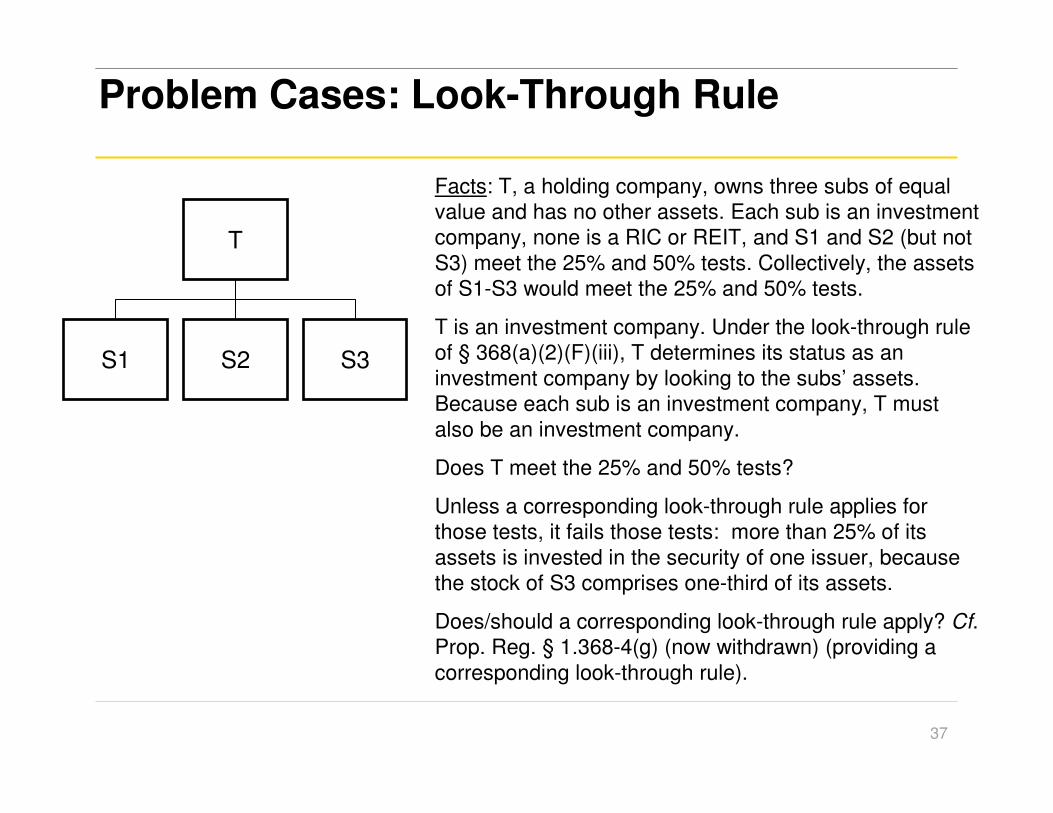

Facts: T, a holding company, owns three subs of equal value and has no other assets. Each sub is an investment company, none is a RIC or REIT, and S1 and S2 (but not S3) meet the 25% and 50% tests. Collectively, the assets of S1-S3 would meet the 25% and 50% tests.

T is an investment company. Under the look-through rule of § 368(a)(2)(F)(iii), T determines its status as an investment company by looking to the subs’ assets. Because each sub is an investment company, T must also be an investment company.

Does T meet the 25% and 50% tests?

Unless a corresponding look-through rule applies for those tests, it fails those tests: more than 25% of its assets is invested in the security of one issuer, because the stock of S3 comprises one-third of its assets.

Does/should a corresponding look-through rule apply? Cf. Prop. Reg. § 1.368-4(g) (now withdrawn) (providing a corresponding look-through rule).

T

S1 S2 S3

38

Problem Cases: Look-Through Rule and Common Control Exception

P

YX

X Sub 1

30%

Merger

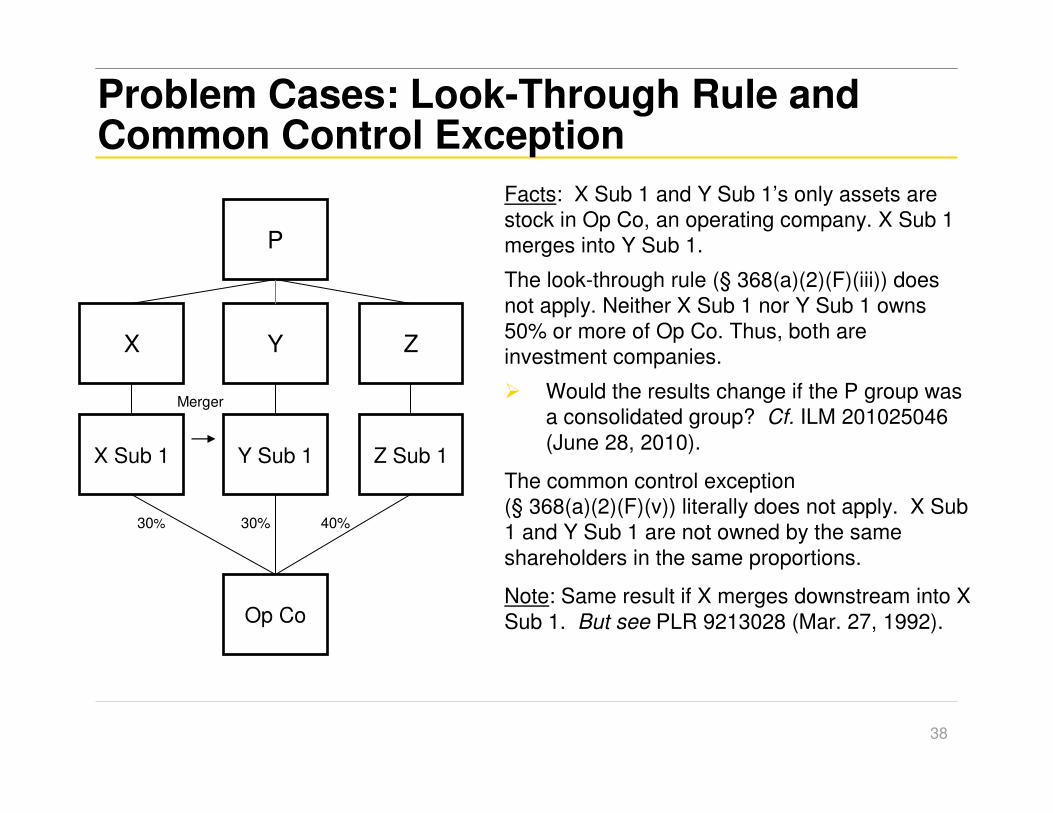

Facts: X Sub 1 and Y Sub 1’s only assets are stock in Op Co, an operating company. X Sub 1 merges into Y Sub 1.

The look-through rule (§ 368(a)(2)(F)(iii)) does not apply. Neither X Sub 1 nor Y Sub 1 owns 50% or more of Op Co. Thus, both are investment companies.

� Would the results change if the P group was a consolidated group? Cf. ILM 201025046 (June 28, 2010).

The common control exception (§ 368(a)(2)(F)(v)) literally does not apply. X Sub 1 and Y Sub 1 are not owned by the same shareholders in the same proportions.

Note: Same result if X merges downstream into X Sub 1. But see PLR 9213028 (Mar. 27, 1992).

Y Sub 1

Op Co

Z

Z Sub 1

30% 40%

39

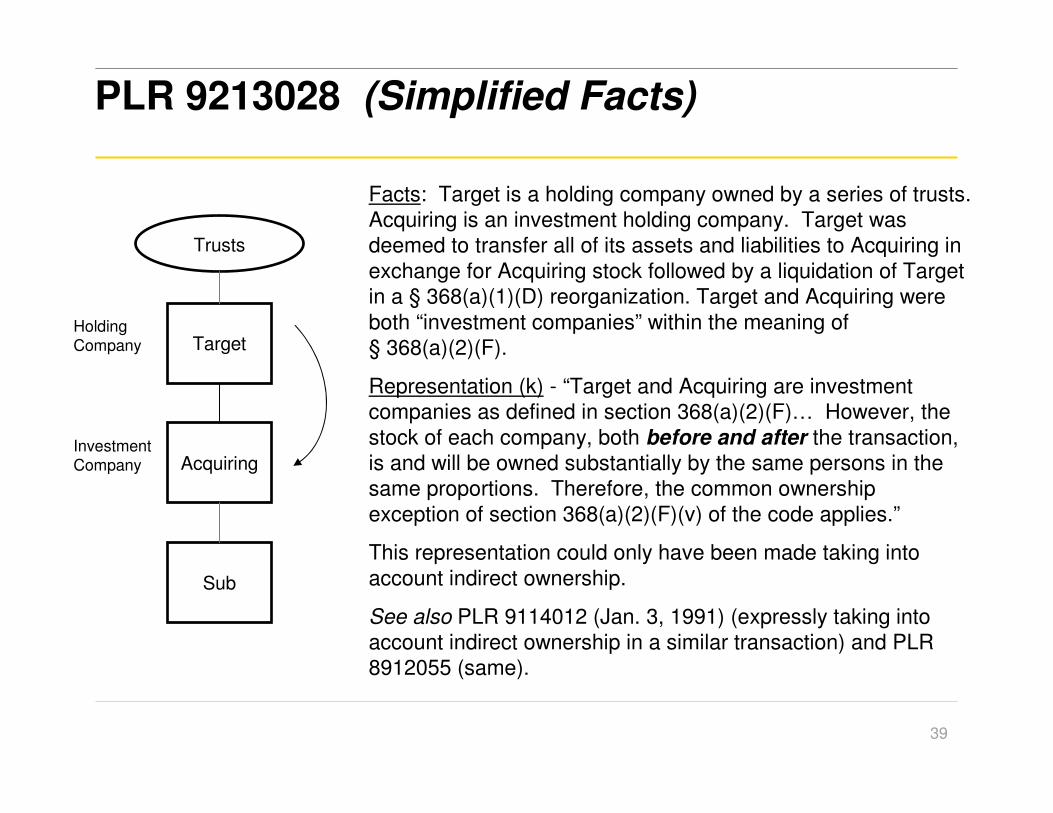

PLR 9213028 (Simplified Facts)

Target

Acquiring

Sub

Trusts

Holding Company

InvestmentCompany

Facts: Target is a holding company owned by a series of trusts. Acquiring is an investment holding company. Target was deemed to transfer all of its assets and liabilities to Acquiring in exchange for Acquiring stock followed by a liquidation of Targetin a § 368(a)(1)(D) reorganization. Target and Acquiring were both “investment companies” within the meaning of § 368(a)(2)(F).

Representation (k) - “Target and Acquiring are investment companies as defined in section 368(a)(2)(F)… However, the stock of each company, both before and after the transaction, is and will be owned substantially by the same persons in the same proportions. Therefore, the common ownership exception of section 368(a)(2)(F)(v) of the code applies.”

This representation could only have been made taking into account indirect ownership.

See also PLR 9114012 (Jan. 3, 1991) (expressly taking into account indirect ownership in a similar transaction) and PLR 8912055 (same).

40

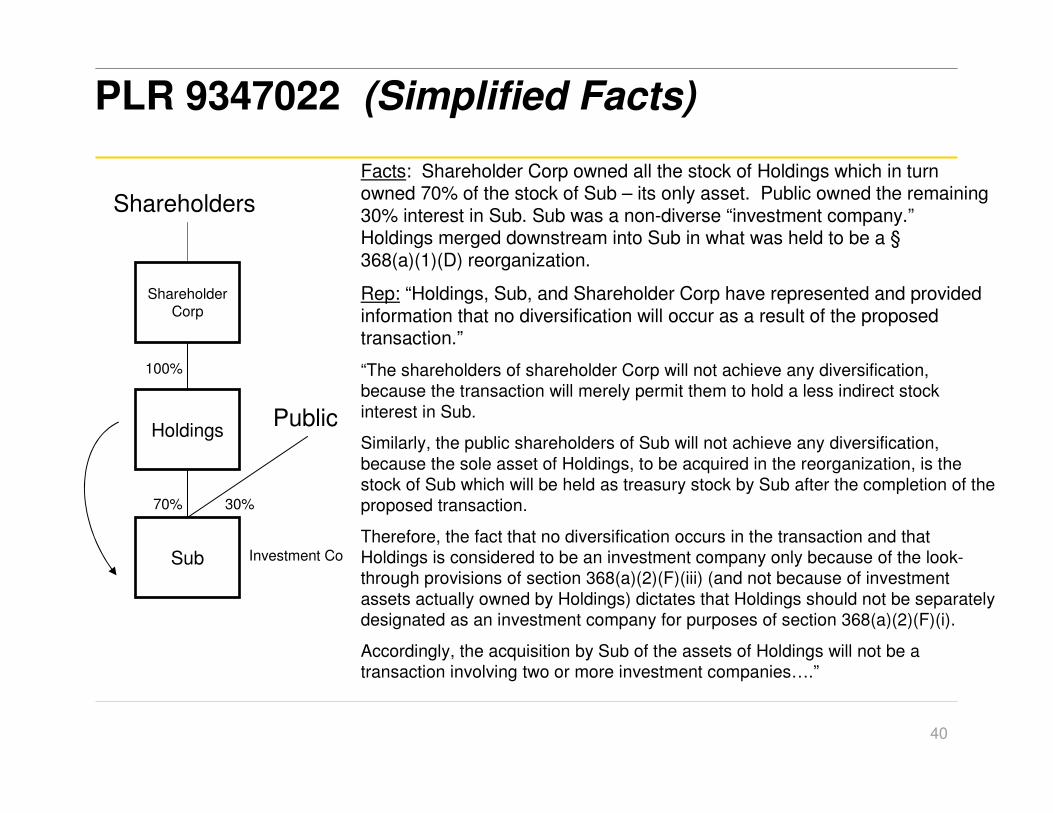

PLR 9347022 (Simplified Facts)

ShareholderCorp

Holdings

Sub

Facts: Shareholder Corp owned all the stock of Holdings which in turn owned 70% of the stock of Sub – its only asset. Public owned the remaining 30% interest in Sub. Sub was a non-diverse “investment company.”Holdings merged downstream into Sub in what was held to be a §368(a)(1)(D) reorganization.

Rep: “Holdings, Sub, and Shareholder Corp have represented and provided information that no diversification will occur as a result of the proposed transaction.”

“The shareholders of shareholder Corp will not achieve any diversification, because the transaction will merely permit them to hold a less indirect stock interest in Sub.

Similarly, the public shareholders of Sub will not achieve any diversification, because the sole asset of Holdings, to be acquired in the reorganization, is the stock of Sub which will be held as treasury stock by Sub after the completion of the proposed transaction.

Therefore, the fact that no diversification occurs in the transaction and that Holdings is considered to be an investment company only because of the look-through provisions of section 368(a)(2)(F)(iii) (and not because of investment assets actually owned by Holdings) dictates that Holdings should not be separately designated as an investment company for purposes of section 368(a)(2)(F)(i).

Accordingly, the acquisition by Sub of the assets of Holdings will not be a transaction involving two or more investment companies….”

Shareholders

Public

70% 30%

Investment Co

100%

41

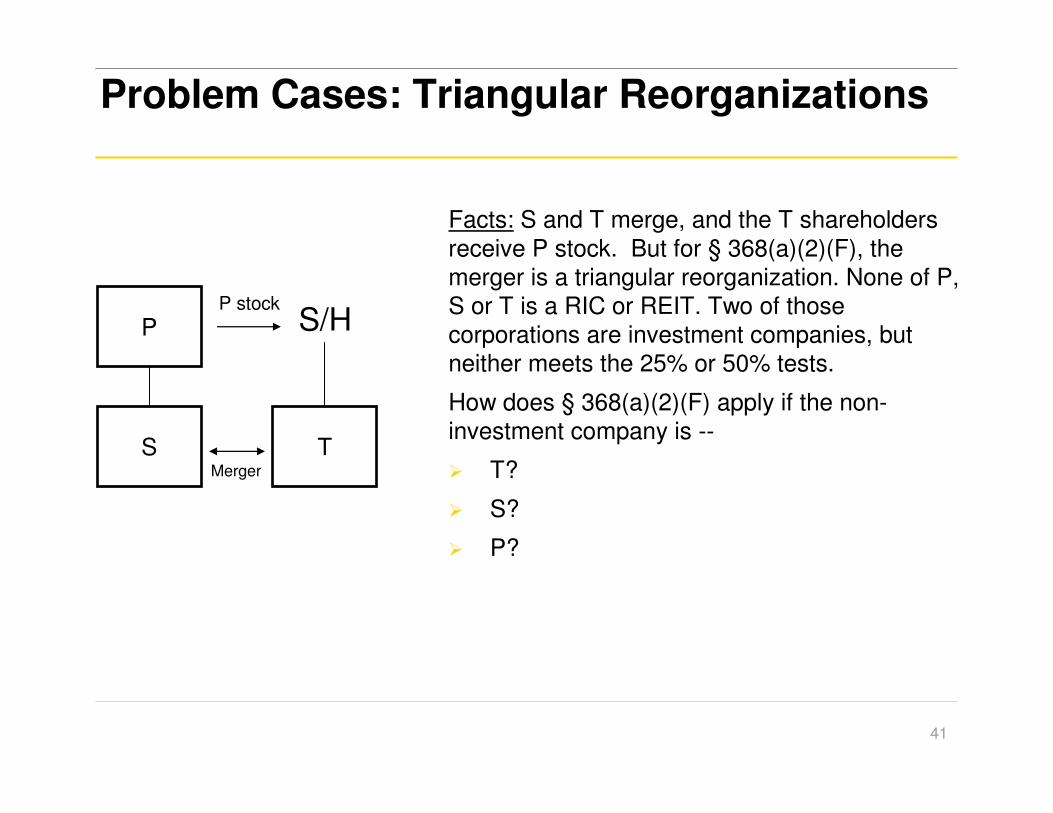

Problem Cases: Triangular Reorganizations

Facts: S and T merge, and the T shareholders receive P stock. But for § 368(a)(2)(F), the merger is a triangular reorganization. None of P, S or T is a RIC or REIT. Two of those corporations are investment companies, but neither meets the 25% or 50% tests.

How does § 368(a)(2)(F) apply if the non-investment company is --

� T?

� S?

� P?

P

TS

S/HP stock

Merger

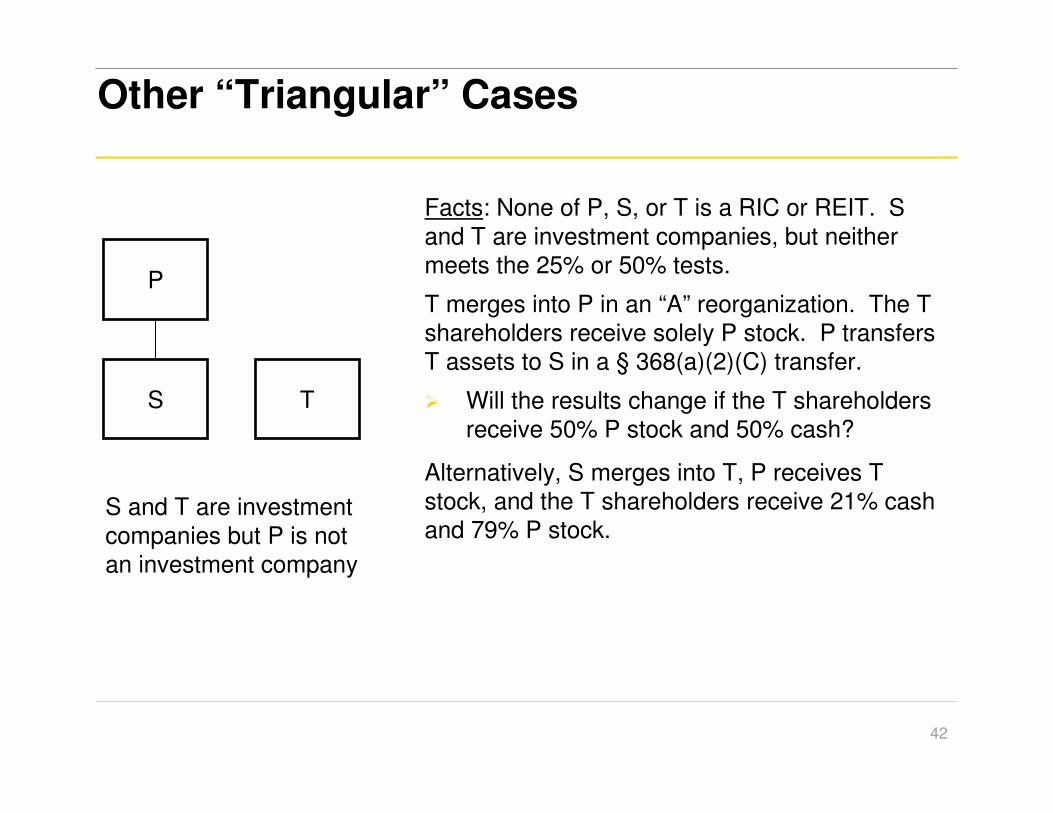

Other “Triangular” Cases

Facts: None of P, S, or T is a RIC or REIT. S and T are investment companies, but neither meets the 25% or 50% tests.

T merges into P in an “A” reorganization. The T shareholders receive solely P stock. P transfers T assets to S in a § 368(a)(2)(C) transfer.

� Will the results change if the T shareholders receive 50% P stock and 50% cash?

Alternatively, S merges into T, P receives T stock, and the T shareholders receive 21% cash and 79% P stock.

42

S and T are investment companies but P is not an investment company

P

TS

43

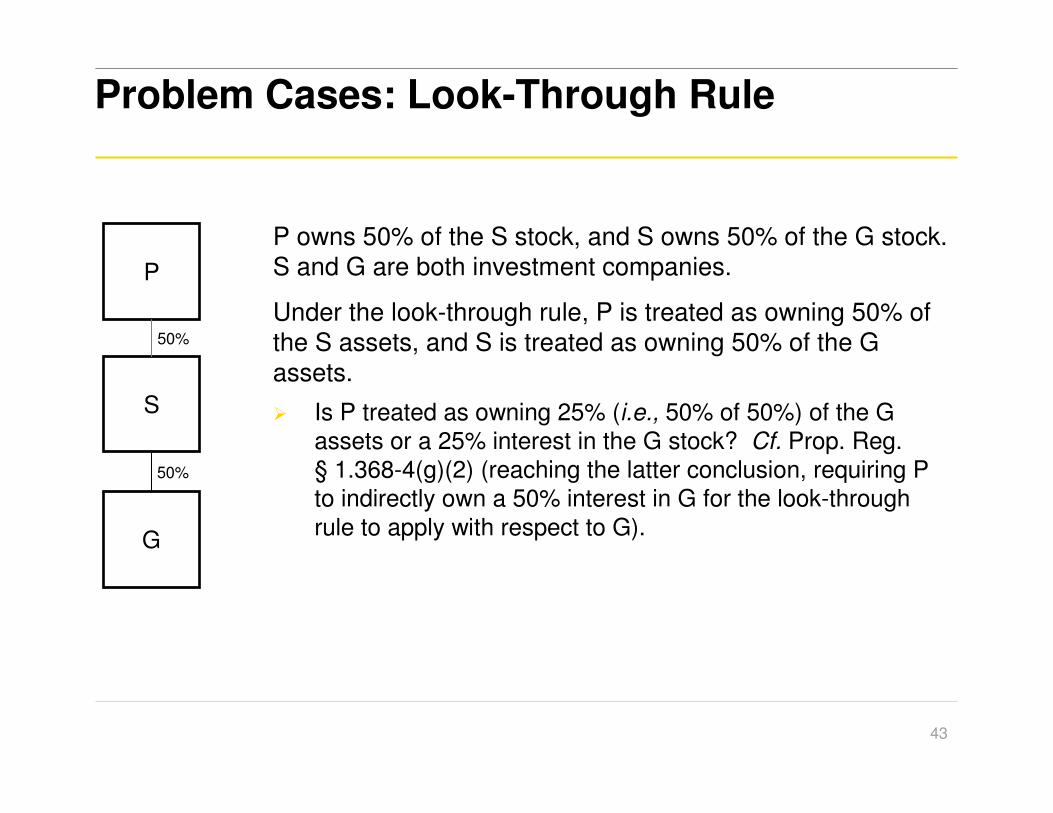

Problem Cases: Look-Through Rule

P owns 50% of the S stock, and S owns 50% of the G stock. S and G are both investment companies.

Under the look-through rule, P is treated as owning 50% of the S assets, and S is treated as owning 50% of the G assets.

� Is P treated as owning 25% (i.e., 50% of 50%) of the G assets or a 25% interest in the G stock? Cf. Prop. Reg. § 1.368-4(g)(2) (reaching the latter conclusion, requiring P to indirectly own a 50% interest in G for the look-through rule to apply with respect to G).

P

S

G

50%

50%

![(Microsoft PowerPoint - Expos\351.ppt [Mode de compatibilit\351])](https://static.fdocuments.in/doc/165x107/55503dc2b4c905b2788b46e2/microsoft-powerpoint-expos351ppt-mode-de-compatibilit351.jpg)