Section TABLE OF CONTENTS 10.26.01 BUDGET MANUAL …pnoc.com.ph/images/Budget Manual.pdf · 2...

50

PNOC BUDGET Section TABLE OF CONTENTS Section No. Effective 10.26.01 MANUAL Subject Subject No. Page SECTION SUBJECT 1 INTRODUCTION Foreword 1 The Philippine Budget Process 2 General Provision 3 Distribution and Custodianship 4 Manual Copyholders 5 2 POLICY STATEMENTS AND GUIDELINES Personal Services 1 Maintenance and Other Operating Services 2 Capital Outlay 3 Cash and Revenue Budget 4 3 PROCEDURES Preparation and Approval 1 Budget Legislation 2 Budget Execution and Implementation 3 Capital Expenditure Request/Implementation Procedure 4 Realignment 5 4 FLOWCHART (BUDGET PROCESS) 5 GLOSSARY OF TERMS 6 BUDGET CALENDAR 7 PERTINENT LAWS 8 REFERENCES 9 FORMS

Transcript of Section TABLE OF CONTENTS 10.26.01 BUDGET MANUAL …pnoc.com.ph/images/Budget Manual.pdf · 2...

PNOC BUDGET

Section TABLE OF CONTENTS

Section No.

Effective 10.26.01

MANUAL

Subject

Subject No.

Page

SECTION SUBJECT 1 INTRODUCTION Foreword 1 The Philippine Budget Process 2 General Provision 3 Distribution and Custodianship 4 Manual Copyholders 5 2 POLICY STATEMENTS AND GUIDELINES Personal Services 1 Maintenance and Other Operating Services 2 Capital Outlay 3 Cash and Revenue Budget 4 3 PROCEDURES Preparation and Approval 1 Budget Legislation 2 Budget Execution and Implementation 3 Capital Expenditure Request/Implementation Procedure 4 Realignment 5 4 FLOWCHART (BUDGET PROCESS) 5 GLOSSARY OF TERMS 6 BUDGET CALENDAR 7 PERTINENT LAWS 8 REFERENCES 9 FORMS

PNOC BUDGET

Section INTRODUCTION

Section No.

Effective 10.26.01

MANUAL

Subject FOREWORD

Subject No.

Page 1 of 1

A budget is basically an entire program of revenue, cost planning, and control activities. It summarizes all expenditures, from personnel services to materials up to machine requirements. Budget may also address the adoption of new methodologies that may require a large sum of cash outlay. It also serves as a push to all managers to take time to formulate strategies, targets, and goals geared towards its effective use. This Corporate Budget Manual lays down the policy statements, guidelines, and procedures employed by the Philippine National Oil Company–Own with regard to budget allocation. It shall serve as a guide to proper allocation of funds. Any revision to procedures stipulated in this Manual should be approved by the Corporate Planning Department in coordination with affected units. Amendments concerning policies, rules, and regulations shall be subject to the approval of the Board of Directors. With regard to amendments concerning systems and procedures, the President & CEO, thru the SVP-MS, is the approving authority. The Internal Control Office shall have custody over this Manual and shall be responsible for effecting and attesting to the changes that the President and CEO may wish to make from time to time.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject THE PHILIPPINE BUDGET PROCESS

Subject No. 2

Page 1 of 3

The Philippine Budget Process is divided into four phases, namely: Budget Preparation, Budget Legislation or Authorization, Budget Execution and Implementation, and Budget Accountability and Review. Budget Preparation Budget preparation begins with the determination of budgetary priorities and activities based on the national development plan, taking into consideration the ceilings imposed due to available revenues and borrowing limits. The overall expenditure levels, revenue projections, deficit levels, and financing plans are determined by the Development Budget Coordination Committee (DBCC), an inter-agency committee composed of representatives from the National Economic and Development Authority (NEDA), Department of Finance (DOF), and the Department of Budget and Management (DBM). Budget preparation is guided by the macroeconomic assumptions determined by NEDA. These assumptions include the projected Gross National Product (GNP), population growth rate, per capita income, price indices, inflation rates, Treasury bill rates, and foreign exchange rates. Once the levels and ceilings are determined, the DBM issues a Budget Call wherein all government agencies including government-owned and controlled corporations are called upon for a uniform approach to the preparation of their respective annual budgets. The DBM also holds budget consultations with these agencies to check if the agency budget is within the approved indicative expenditure ceilings and to allow them greater flexibility in prioritizing their funding requirements. The DBM undertakes a series of evaluations to determine areas from which a reduction can be made. The final consolidated budget then becomes the proposed national budget which the President shall submit to Congress within thirty (30) days from the opening of every regular session, as the basis of the general appropriations bill, a budget of expenditures and sources of financing, including receipts from existing and proposed revenue measures as provided for in Article VII, Section 22 of the Constitution of the Philippines. Budget Legislation or Authorization The proposed budget is presented to the House of Representatives, since all appropriation, revenue, or tariff bills shall originate exclusively from the House of Representatives, but the Senate may propose or concur with amendments as provided for in Article 6, Section 24 of the Constitution of the Philippines. Appropriations bill is prepared and filed by a House Member. On the First Reading, the bill is referred to the Committee on Appropriations, which has general jurisdiction on all matters relating to funds for the expenditures of the National Government and the payment of public indebtedness, and the classification of positions and determination of compensation of

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject THE PHILIPPINE BUDGET PROCESS

Subject No. 2

Page 2 of 3

government personnel. The Committee on Appropriations finding it necessary to conduct public hearings, schedules the public/budget hearings, issues notices and invites the Head of the Agency together with their Senior Officials to explain and justify budget submissions. Based on the results of the hearings conducted, the committee prepares the corresponding committee report and which is then referred to the Committee on Rules. On Second Reading, the Period of Debate (consisting of the Sponsorship Speech, Interpellation and the Turno en Contra), Period of Amendments (Committee Amendments, Individual Amendments) and the Approval on Second Reading (which may be by viva voce, raising of hands, division of the house or nominal or roll call) takes place. The amendments, if any, during the Period of Debate is Engrossed and is included in the Calendar of Bills for Third Reading. During this period, a roll call vote is called and a Member, if he desires, is given three (3) minutes to explain his vote. No amendment of the bill is allowed at this stage. The bill is approved by an affirmative vote of the Members present. The Approved Bill is then transmitted to the Senate for its concurrence. The Senate considers the bill in the same manner as in the House of Representatives, only that Finance Committee, the counterpart committee in the Senate conducts the public/budget hearings. After both houses approved their own versions of the General Appropriations Bill, a Conference Committee is constituted, composed of Members from both houses to settle, reconcile or thresh out differences or disagreements on any provision of the bill. The conferees are not limited to reconciling the differences in the bill but may introduce new provisions germane to the subject matter or may report out an entirely new bill on the subject. The Conference Committee Report is then submitted to both houses of Congress for consideration and approval. No amendment is allowed at this point. The General Appropriations Bill is then signed by the President of the Senate and Speaker of the House of Representatives. It is certified by both the Secretary of the Senate and the Secretary-General of the House of Representatives. It is then transmitted to the President of the Republic of the Philippines. If the General Appropriations Bill is approved by the President, the same is assigned a Republic Act Number and is transmitted to the House of Representatives where it originated. The approved bill, now a Republic Act, is sent to the official Gazette Office for publication and distributed to the implementing agencies.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject THE PHILIPPINE BUDGET PROCESS

Subject No. 2

Page 3 of 3

Budget Execution and Implementation The third phase in the budget process covers the various operational aspects of budgeting. It is concerned not only with the release of funds in the form of Notice of Cash Allocation (NCA) for regular government agencies and/or GOCC’s receiving subsidy from the National Government, but also the continuing review of the government’s fiscal position (revenues realized, borrowings and prevailing economic conditions), regulation of fund releases and implementation of cash payment schedule. Under this phase, the continuing review of organizational developments is conducted and the function of ensuring that funds are available in support of activities, given the limitations of an appropriations and available cash. Budget Accountability and Review The proper allocation of funds would call not only for a review of priorities but also for a study of the performance and cost effectiveness of agencies concerned. Even with maximum funding, no significant results can be achieved if agency efficiency is low and funds are wastefully spent. This phase therefore is concerned with the agency performance review and management accounting and control. Performance review is done through the identification of work measurement units and other quantitative and qualitative indicators of agency performance. In the case of PNOC, performance review is done not only to determine the performance of the company and all its subsidiaries but also of all the employees concerned. Regular monitoring of departmental and individual performance is made on a monthly basis. The analysis of agency operating systems and procedures is an inherent part of the budget process. The budget division is therefore expected to implement systems and procedures designed to strictly monitor the implementation and use of funds. To do this, the Accounting Department prepares the Monthly Utilization Report detailing the departmental uses of their respective budget allocations. Each department is likewise furnished copies of their respective allocations. The Budget Division monitors budget utilization and prepares the same in its report to other government bodies such as Congress and DBM.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject GENERAL PROVISION

Subject No. 3

Page 1 of 2

How to establish an effective budgeting process should always be taken as a key to a successful business venture. An existence of a sound and fully coordinated budgeting system could determine where the company is headed financially. At the end of each accounting period, budget helps determine areas of strengths and weaknesses in the financial management system of the company. Budget has always been used as a cure-all word for the financial problems of an enterprise. However, it should be clear that budget is simply a plan and specific management action plans are needed to make everything turn into reality. This Manual aims to give its readers, particularly the various PNOC cost centers, an overview of budgeting, its importance, approaches and manner of preparing one. It is expected that this will give light, much more a push to all, to consider the power of budgeting in the whole operational activities of an enterprise.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject GENERAL PROVISION

Subject No. 3

Page 2 of 2

Mission Statement The Corporate Planning Department, more particularly the Budget Division, shall be responsible for the coordination, review, consolidation, and preparation of the PNOC-Own Operating and Capital budget, including the preparation of a consolidated budget of PNOC and the subsidiaries.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject DISTRIBUTION AND CUSTODIANSHIP

Subject No. 4

Page 1 of 1

This Manual belongs to PNOC and is issued to an authorized copyholder who will be responsible for its updating and safekeeping. Entitlement to hold copy of the Manual lies on the position and should remain there whoever the occupant maybe. The copyholder should make this Manual available to his staff who may need it in the performance of his assigned tasks. Each copy of the Manual is registered by number as assigned by PNOC Internal Control Office. In case the occupant is transferred to another position or leaves PNOC, he must advise PNOC Internal Control Office so that his accountability over this Manual can be cleared.

PNOC BUDGET

Section INTRODUCTION

Section No. 1

Effective 10.26.01

MANUAL

Subject MANUAL COPYHOLDERS

Subject No. 5

Page 1 of 1

POSITION MANUAL COPYHOLDER NO. President 1 Executive Vice President 2 SVP - Legal and Administration 3 SVP - Management Services 4 Internal Control Manager 5 (Administrative System) Project Management Manager 6 Energy Research Manager 7 Corporate Communications 8 Corporate Secretary 9 Administrative Manager 10 Legal Manager 11 Estate Management Manager 12 Treasury Manager 13 Corporate Planning Manager 14 Accounting Manager 15

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject PERSONAL SERVICES

Subject No. 1

Page 1 of 4

Personal Services Cost (Schedules 1 and 2) is the provision for the salaries and wages, allowances and other compensation of employees under the approved plantilla. These are classified as follows: A. Base Pay

1. Itemized Positions Salaries of itemized positions shall be equal to the sum of the annual salaries of all

permanent positions authorized under the approved plantilla. 2. Non-itemized Positions Basic salaries, allowances and other compensations of casual and coterminous/

contractual personnel B. Mandatory Benefits

1. Representation and Transportation Allowance (RATA) The following officers and those of equivalent rank while in the performance of their

functions are granted monthly commutable representation and transportation allowances. The rates are subject to change depending on the rates as provided for under the General Appropriations Act for the specific year:

President Executive Vice-President Senior Vice-President Department Manager Assistant Department Manager Division Chief

The transportation allowance herein authorized shall not be granted to officials who are

assigned or are using a government vehicle. 2. Personnel Economic Relief Allowance (PERA) FIVE HUNDRED PESOS (P500.00) per month PERA shall be granted to all

employees in accordance with Budget Circular No. 12 dated April 7, 1997.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject PERSONAL SERVICES

Subject No. 1

Page 2 of 4

3. Additional Compensation Allowance (ACA) FIVE HUNDRED PESOS (P500.00) per month as additional compensation allowance

in accordance with the provisions of Administrative Order No. 53 dated May 17, 1993. Computation should be on the number of itemized positions entitled thereto. Employees occupying positions allocated to Salary Grade 25 and below are entitled to receive this allowance. Said allowance shall likewise be granted to all government personnel whether regular, casual, temporary, or contractual.

4. Year-End Benefits Bonus and Cash Gift shall be computed in accordance with Republic Act No. 6686, as

amended by Republic Act No. 8441: Provided, that one-half (1/2) of the amount of said year-end bonus and cash gift may be paid not earlier than May 1 but not later than May 31 of each year subject to the implementing rules and regulations issued by the Department of Budget and Management.

A one-month basic salary and cash gift depending on the approved budget shall be allocated for this benefit.

5. Uniform and Clothing Allowance The provision for uniform and clothing allowance shall be computed based on the

number of itemized positions multiplied by FOUR THOUSAND PESOS (P4,000) per annum, or as otherwise approved in the General Appropriations Act (GAA).

C. Other Compensation

1. Allowance of the Board of Directors This account includes per diem of P2,000/meeting per month for a maximum of two

meetings plus a provision of one special meeting per quarter for the Members of the Board. (Schedule 3)

2. Productivity Incentive Benefit

The amount of TWO THOUSAND PESOS (P2,000) shall be allocated per personnel

who has rendered at least a satisfactory performance for two rating periods in accordance with the provisions of Administrative Order No. 161.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject PERSONAL SERVICES

Subject No. 1

Page 3 of 4

3. Merit and Length of Service Incentive Pay This shall be computed at the rate of 2% of the total basic salaries of itemized positions.

(Grant of this incentive is based on the Joint CSC - DBM Circular No. S-1990) 4. Monetization of Leave Credits This account is allowed to employees who have accumulated fifteen (15) days of

vacation leave credits. Employees may monetize a minimum of ten (10) days, provided that a five (5) day leave balance is maintained after monetization, and provided further that a maximum of thirty (30) days may be monetized in a given year. This is based on Civil Service Commission Memorandum Circular No. 41, s. 1998, for vacation/sick leave credits.

Monetization of fifty percent (50%) of all accumulated leave credits may be allowed for valid and justifiable reasons. This is subject to the discretion of management and the availability of funds. (Pursuant to CSC Resolution No. 98-3142, s. 1998)

This shall be charged against savings in Personal Services.

5. Terminal Leave Benefits This account is intended for employees who retire or voluntarily resign or are separated

from service through no fault of their own. Terminal leave pay benefit entitles the employees to the commutation of the unused vacation and sick leave credits based on the highest salary received.

Terminal Leave Benefits shall be computed as follows: TLB = DPi (SPi) + ... + DPn (SPn) 22 22 where: TLB = total terminal leave benefits D = number of days leave credits per personnel scheduled to retire S = highest salary received by the person Pi = first individual personnel scheduled to retire Pn = last individual personnel scheduled to retire

22 = number of working days in a month pursuant to RA 6758

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject PERSONAL SERVICES

Subject No. 1

Page 4 of 4

6. Overtime Pay 5% of the total for Personal Services shall be allotted for overtime in accordance with

the National Budget Circular No. 410. However, the total amount of overtime compensation, which maybe allowed an employee for a given calendar year, shall not exceed fifty percent (50%) of his basic salary. This shall be charged against savings in Personal Services.

D. Fixed Expenditure

1. Contribution to the GSIS Retirement and Life Insurance Premium The amount for this purpose shall be computed at 12% of the total salaries of itemized

positions. 2. Other Contributions:

a) Health Insurance Contributions (Phil. Health Insurance Corp., or PhilHealth) - the government’s counterpart contribution to the health insurance premium of itemized positions shall be computed at SEVEN HUNDRED FIFTY PESOS (P750) per employee per annum, based on PhilHealth Circular No. 75, s.1999.

b) PAG-IBIG Contributions - the government’s counterpart to the contribution of

regular member employee to the PAG-IBIG Fund shall be computed at ONE THOUSAND TWO HUNDRED PESOS (P1,200) each employee per annum.

c) Employees Compensation Insurance Premium (ECIP) - the government’s

contribution for each regular employee shall be computed at THREE HUNDRED SIXTY PESOS (P360) per annum.

All accounts under Personal Services shall be computed by the Administrative Services Department.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 1 of 9

Maintenance and Other Operating Expenses (MOOE) pertain to the regular expenses incurred in the implementation of the company's workplans and programs. These include but shall not be limited to the following: A. Traveling Expenses

1. Domestic Travel (Schedule 4) This account includes expenses incurred in the movement of officials and employees

such as transportation, subsistence, lodging, per diem, hire of guides or patrol, transportation of personnel baggage or household effects, bus, railroad, airline and steamship fares, transfers, porter’s fee, etc., of persons while traveling; charter of boats, launches, automobiles, etc., road tolls, parking fees and similar expenses incurred within the country.

All departments shall project for this expense item subject to the provisions of

Executive Order No. 248 and 248A. The Office of the President shall project for International and Energy Related Commitments to include ASCOPE based on requirements of the three (3) Business Development Committees and the Technology and Services Committee.

2. Foreign Travel (Schedule 5) These are expenses incurred by government officials and employees in connection with

attendance on scholarships, fellowships, training grants, conferences, special missions and other non-study grants held abroad. All departments/ offices shall project for this expense item, subject to Executive Orders 248 and 248-A. Corplan shall project for participation to APEC, BIMP-EAGA, and other international commitments.

The Executive Officer of the company elected to the National Chairmanship of

ASCOPE shall project for ASCOPE. The various Business Development Committees (BDC’s) and the Technology and Services Committee (TSC) shall submit ASCOPE-related requirements to the National Committee Chairman.

Only travels in relation to the job, such as project monitoring, audit, and the like, shall

be allowed. B. Communication Expenses (Schedule 6)

This account includes expenses for the use of facilities like telephones, telegraphs, pagers, facsimile, wireless and cable charges and tolls, postage charges, rent of post office boxes

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 3 of 9

which is P10,000.00 or less. 2. Items converted in the process of manufacture or construction having a life expectancy

of more than one year, but have decreased substantially in value after being put into use in only one (1) year.

The Administrative Department shall provide for the unit cost of all supplies and

materials.

Information Technology (IT) Supplies and Materials refer to all expendable IT resources for use in connection with government IT operations and with the life expectancy of less than one year.

Semi-expendable Information Technology Supplies, Accessories, Peripherals and Property refer to all semi-expendable IT resources for use in connection with government IT operations having a value of less than P10,000 but with a life expectancy of more than one year.

All departments/offices shall project for this particular expense item. All Committee

Chairmen/Chairperson shall project for the expenses of their respective committees. G. Rents (Schedule 11) This account includes the fees for the use of facilities and equipment.

All departments shall project for this expense item. H. Statement of Borrowings (Schedule 12)

1. Interests This account includes charges for the use of funds such as interest on bonds, loans,

provisional advances, treasury bills, treasury notes, certificates of indebtedness, and other interest bearing obligations.

2. Loan Repayment This account includes payment made either directly or indirectly into a sinking fund for

the retirement of public debt and other long-term obligations.

3. Commitment Fee and Other Charges

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 4 of 9

This account includes expenses for commitment fees charged by the foreign lending institutions for undrawn loans and loan related charges, such as front-end fees, management fees, bank charges, etc.

4. Loss on Foreign Exchange This account includes losses in converting foreign exchange currencies to Philippine

Peso, or vice-versa. Losses occur under the following conditions:

a. Those arising from foreign loan proceeds - a loss is incurred when the prevailing exchange rate is lower than the fixed rate of exchange as contained in the loan agreement.

b. Those arising from remittances or repayments of foreign loans by the National

Government/Company - a loss is incurred when the prevailing exchange rate is higher than the fixed rate of exchange as contained in the loan agreement.

The Treasury Department shall project for all the expense items. I. Grants, Subsidies, and Contributions (Schedule 13) This account includes all aids and contributions in the form of cash or property granted to

persons, entities, or organizations for the purpose of furthering programs or policies adjudged to be in the interest of the government.

The Office of the Chairman, President, Executive Vice President, and Senior Vice-

Presidents shall project for this expense item. J. Awards and Indemnities (Schedule 14) This account includes indemnities for destruction of property or injury to persons, awards by

courts or administrative bodies. The Estate Management Department and Legal Department shall project for this account. K. Depreciation (Schedule 15) This account includes losses of current assets due to deterioration of supplies and sales

stock, uncollectible debts and losses of government funds or property for which a relief is granted under Section 73 of PD 1445, and/or depreciation of fixed assets due to wear and

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 5 of 9

tear, in accordance with the approved schedule.

The Corporate Accounting Department shall project for all existing depreciable assets.

Corplan shall project for all assets to be acquired during the budget year. L. Water, Illumination, and Power Service (Schedule 16) This account includes the cost of water and electricity consumed in all PNOC facilities and

in connection with its operations and projects. The Administrative Department and the Estate Management Department shall project for

this expense item. M. Auditing Services (Schedule 17) This account includes the amount remitted to the Commission on Audit for auditing services

rendered to the company. The Corporate Accounting Department shall project for this expense item. N. Training and Seminar Expenses (Schedule 18) This account includes expenses incurred for the participation/attendance of personnel to

trainings and seminars/workshops held locally or abroad. All departments shall project for this expense item. The Administrative Department shall

prepare the budget for in-house training programs. O. Extraordinary and Miscellaneous Expenses

1. Employee Recreation Expenses (Schedule 19) This account includes expenses incurred in connection with the employees’ athletic and

cultural activities. In accordance with Sec. 23, General Provisions of GAA, an amount not exceeding P1,200.00 or depending on the approved budget may be used for the purchase of costumes or uniforms for each participant and other related expenses in the conduct of cultural and athletic activities.

The Administrative Department shall project for this expense item. 2. Contributions and Membership Fees (Schedule 20)

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 6 of 9

This account includes expenses/fees charged to an officer or employee in connection with membership in government associations and professional organizations.

All departments concerned shall project for this expense item. 3. Meetings and Conferences (Schedule 21) This account includes expenses related to PNOC-Wide meetings and conferences. All departments shall project for this expense item. 4. Representation and Meetings (Schedule 22) This account includes expenses incurred during meetings or official entertainment

according to prescribed standards. All departments shall project for this expense item. 5. Other Business Expense (Schedule 23) This account includes expenses in connection with the purchase of corporate giveaways

and other related expenses according to prescribed standards. The Offices of the Chairman, Board of Directors, and President shall project for this

expense account including items for International and Energy Related Commitments. P. Contingency/Emergency Expenses This account includes expenses incurred arising from the occurrence of unforeseen

events/natural calamities or financial dislocation arising thereof. This is a lump sum amount projected at 10% of the total MOOE. The Corporate Planning Department shall project for this expense item. Q. Taxes, Duties and Fees (Schedule 24) This account includes payments and provisions for all taxes, licenses, and fees except

income tax.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 7 of 9

All departments shall project for this expense item. R. Advertising and Publication Expenses (Schedule 25) This account includes the cost of advertisement and publication of notices in newspapers

and magazines of general circulation. The Administrative Department, Estate Management Department, and Corporate

Communications shall project for this expense item. S. Gasoline, Oil, and Lubricants (Schedule 26) This account includes the cost of gasoline, oil, and lubricants purchased for stock or

immediate use in connection with government operations. The Administrative Department shall project for this expense item. T. Fidelity Bonds and Insurance Premiums (Schedule 27) This account includes expenses for premiums paid for fidelity bonds of accountable officers,

premium on insurance of government properties like buildings, motor vehicles, equipment, and other government facilities.

The Estate Management Department, Treasury Department, and the Administrative

Department shall project for this expense item. U. Other Services This account includes all the other expenses not classified under any of the abovementioned

accounts. 1. Professional and Technical Services (Schedule 28) This account includes the cost/fees charged by consultants/experts and other

professionals for services rendered for the company. All departments in need of the services of consultants shall project for this account. 2. Security Services (Schedule 28) This account includes the cost charged by security agencies hired by the company.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 8 of 9

The Administrative Department and Estate Management Department shall project for the cost of this expense item.

3. Janitorial and Messengerial Services (Schedule 28) This includes cost charged by the janitorial/messengerial agencies contracted by the

company. The Administrative Department and Estate Management Department shall project for

this expense item. 4. Other Purchased Services (Schedule 28) This covers the cost of purchased services not classifiable under any of the above

characters of expense. These may include bookbinding, salary of temporary employees provided by independent employment outfits, shuttle services, etc.

All departments shall project for this expense item. 5. Printing Projects (Schedule 29) This account includes expenses in printing, reproduction, photocopying of reports,

records, annual reports, newsletters, manuals, and other documents. All departments shall project for this expense item. The Office of the President shall

project for International and Energy Related Commitments to include ASCOPE based on requirements of the three (3) Business Development Committees and the Technology and Services Committee.

6. Subscription (Schedule 30) This includes amounts paid for the subscription of magazines, newspapers, and other

reading materials. All departments shall project for this account. 7. Sundry Expenses (Schedule 31) This account includes cost of groceries and other expenses which are not listed or

classified in any of the existing account codes.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject MAINTENANCE AND OTHER OPERATING

EXPENSES

Subject No. 2

Page 9 of 9

All departments/offices shall project for this expense item subject to the prescribed standards.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject CAPITAL OUTLAY

Subject No. 3

Page 1 of 2

Capital Outlay covers appropriation for the purchase of land, equipment, and other fixed assets, the benefits of which are usually beyond one year. It also includes allocation for investment and loans extended to PNOC subsidiaries. A. Investment Outlay (Schedule 32) This account includes the cost of investment in stocks, bonds, or other securities of

government and private corporations, associations, or political subdivisions. The Office of the Chairman, President, Executive Vice-President, and Senior Vice-President

shall project for this account. The Treasury Department and the Corporate Planning Department shall project for this account based on the approved Long-Term Corporate Outlook (LTCO) submitted by the subsidiaries and the investment priorities set forth by the Executive Committee.

B. Loans Outlay (Schedule 12) This account includes loans and capital advances made to persons, government and private

corporations, revolving funds, associations, and political subdivisions. This also includes borrowings from foreign sources guaranteed by PNOC and relent to its

subsidiaries to finance their projects. The Treasury Department and the Corporate Planning Department should project for the

loan drawdowns and new loans based on the LTCO submitted by the subsidiaries. C. Land and Land Improvements Outlay (Schedule 34) This account includes the cost of rights to land ownership and the permanent improvements

to land such as filling, grading, drainage, fencing, surveying, and planting of trees. The Administrative Department and Estate Management Department shall project for this

account. D. Buildings and Structures Outlay (Schedule 35) This account includes the cost of buildings and structures, purchased or constructed, and

permanent improvements thereto. The Administrative Department and Estate Management Department shall project for this

account.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject CAPITAL OUTLAY

Subject No. 3

Page 2 of 2

E. Furniture, Fixture, Equipment, and Books Outlay (Schedule 36) This account includes furniture, fixture, equipment, and books purchased, the cost of which

shall not be lower than the minimum price prescribed by COA, whose serviceable or estimated useful life is more than one year and which add to the assets of the government. All offices/departments shall project for this account subject to the following conditions: 1. The requirement for equipment that are directly needed in the performance of line

functions should be satisfied first before items intended for administrative and support activities are considered.

2. The repair and rehabilitation of existing items should be considered as an alternative to

the purchase of new items. 3. Requests for replacement of non-serviceable equipment, considered extremely

necessary should be given priority over the purchase of additional items. Request for replacement should be supported by certification of non-serviceability duly signed by the head of agency/COA auditor.

4. The optimum utilization of existing equipment should be a precondition for the

purchase of additional ones. As much as possible, equipment like copying machines, audio-visual equipment, and similar ones which could be shared should be pooled for common use.

5. The purchase of motor vehicles shall be subject to Section 14(a), General Provisions of

the General Appropriations Act and with the applicable provisions of National Budget Circular No. 446 dated November 24, 1995.

PNOC BUDGET

Section POLICY STATEMENTS AND GUIDELINES

Section No. 2

Effective 10.26.01

MANUAL

Subject CASH AND REVENUE BUDGET

Subject No. 4

Page 1 of 1

A. Interest Income (Schedule 37) This account includes earnings from money market placements and promissory notes

granted by PNOC to its subsidiaries. The Treasury Department shall project for this account. B. Rent Income (Schedule 38) This account refers to the income/earnings arising from the ownership collected by the

company from persons/entities for the use of company properties. The Estate Management Department shall project for this account. C. Dividend Income This account refers to the earnings from Investments of the company in Petron Corporation,

Goodyear Tires, Inc., National Development Company, Philippine Resource Helicopter, Inc., Palicpican Sports Complex, etc.

The Treasury Department shall project for this account. D. Collection of Receivables This account refers to the collection of past due accounts taken up in the books either as

trade receivables, claims receivables, receivables from the Philippine Government, inter-company advances, or other current receivables.

The Treasury Department shall project for this account.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject PREPARATION AND APPROVAL

Subject No. 1

Page 1 of 3

Budget Preparation is the first step of the budget process. It covers the estimation of company revenues, determination of work plans and programs in line with the government's thrust and the translation of these to expenditure levels. Estimates are prepared by the different departments and initially reviewed by the Corporate Planning Department. It is then evaluated and approved by the Budget Review Committee, members of which are the following officers: Executive Vice-President - Chairman Senior Vice-President, Management Services - Co-Vice-Chairman Senior Vice-President, Legal, Administrative - Co-Vice-Chairman Services and Estate Management Manager, Corporate Planning Department - Member The President and the Board of Directors are likewise involved in the evaluation and approval process. Once accomplished, it is submitted to the President of the Philippines through the DBM. Responsibility Action

President and CEO 1. Issues corporate thrusts, priorities, and directions of the company both on short-term and long-term basis.

Manager, Corporate Planning Department 2. Prepares planning and budget guidelines based on the approved thrusts, priorities, directions, and related schedule of deliberations.

3. Issues budget guidelines and related financial assumptions/economic indicators as basis for the preparation of the departmental budget. These guidelines and assumptions are in accordance with the Annual Budget Call issued by the Department of Budget and Management.

4. Furnishes subsidiaries with financial assumptions/economic indicators as basis for their Long Term and Short Term Corporate Outlook (LTCO and STCO).

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject PREPARATION AND APPROVAL

Subject No. 1

Page 2 of 3

Responsibility Action

Proponent Department 5. Prepares budget proposals based on their approved workplans and performance commitments.

6. Submits to Corplan for their initial review.

Corporate Planning Department 7. Evaluates work program and related budget (Operating and Capital Budget) of proponent departments and thereafter conducts departmental planning and budget consultations.

Proponent Department 8. Presents programs and budget proposals.

Chief, Budget Division & Budget Officers 9. Consolidates department budgets.

10. Submits to Department Manager.

Manager, Corporate Planning Department 11. Conducts initial review and evaluation based on work programs, utilization, and prevailing economic and financial condition of the company and recommends accounts for budget cuts/reduction.

12. Transmits the consolidated budget together with the analyses and recommendations to the EXECOM for review and evaluation.

EXECOM 13. Conducts review and evaluation.

14. Presents to the President and CEO.

President and CEO 15. Approves budgetary level and endorses the same to the Board for approval.

Corporate Secretary 16. Calendars budget submission.

Board of Directors 17. Deliberates budget submission and approves budget.

Corporate Secretary 18. Prepares Secretary’s Certificate.

Chief, Budget Division & Budget Officers 19. Coordinates with the Accounting Department for the actual results of operation for incorporation in the prescribed DBM forms.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject PREPARATION AND APPROVAL

Subject No. 1

Page 3 of 3

Responsibility Action

Chief, Budget Division and Budget Officers 20. Prepares the PNOC Corporate Operating Budget based on the prescribed DBM forms for both the audited, certified, and proposed years (normally covering a 4-year period).

Manager, Accounting Department 21. Signs the audited and certified years portion of the DBM forms.

22. Returns to Corplan.

Manager, Corporate Planning Department 23. Signs the proposed years portion of the DBM forms.

24. Endorses to the Executive Vice-President for her initials.

Executive Vice-President 25. Affixes initials on all DBM forms prior to signature of the President.

26. Endorses the COB to the President.

President and CEO 27. Affixes signature on all DBM forms.

28. Transmits the proposed COB to Corplan.

Manager, Corporate Planning Department 29. Transmits the proposed COB to DBM.

30. Deliberates budget submission. Approves budget.

Department of Budget and Management 31. Conducts agency consultations.

32. Prepares Secretary’s Certificate.

33. Returns approved budget to Corplan.

President of the Republic of the Philippines 34. Submits the proposed National Budget to the House of Representatives within thirty (30) days from the opening of every regular session.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject BUDGET LEGISLATION

Subject No. 2

Page 1 of 3

Budget Legislation is the second step of the budget process. The House of Representatives and the Senate act on the budget proposal of the agency. This process includes review and enactment into law of the budget proposal. Responsibility Action

Department of Budget and Management 1. Reviews and conducts consultation meetings/budget hearings with the company's representatives (Officers and Corporate Planning Department) regarding the proposed budget. If the budget is found to be realistic and reasonable, DBM endorses this to the President of the Philippines for approval.

President of the Republic of the Philippines 2. Submits the proposed National Budget to the House of Representatives within thirty (30) days from the opening of every regular session.

House of Representatives 3. A House Member files an Appropriation Bill based on the National Budget submitted by the President of the Republic of the Philippines.

4. Within three (3) days from its filing, the Appropriation Bill is calendared for First Reading and is referred to the Committee on Appropriations.

Committee on Appropriations 5. Finding it necessary to conduct public hearings, schedules the public/budget hearings, issues notices and invites the Head of the Agency together with their Senior Officials to explain and justify budget submissions.

6. Based on the results of the hearings conducted, the committee prepares the corresponding committee report and which is then referred to the Committee on Rules, reading for plenary deliberations (2nd reading).

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject BUDGET LEGISLATION

Subject No. 2

Page 2 of 3

Responsibility Action

House of Representatives 7. On Second Reading, the Period of Debate (consisting of the Sponsorship Speech, Interpellation and the Turno en Contra), Period of Amendments (Committee Amendments, Individual Amendments) and the Approval on Second Reading (which may be by viva voce, raising of hands, division of the house or nominal or roll call) takes place.

8. During the Period of Debate, the Chairman of the Sub-Committee on Energy, sponsor of the PNOC Budget presents and defends the budget of the company from any House Member who may want to make a query on the plans, programs, budget, and many others regarding PNOC.

9. The amendments, if any, during the Period of Debate is Engrossed and is included in the Calendar of Bills for Third Reading. During this period, a roll call vote is called and a Member, if he desires, is given three (3) minutes to explain his vote. No amendment of the bill is allowed at this stage. The bill is approved by an affirmative vote of the Members present. The Approved Bill is then transmitted to the Senate for its concurrence.

Senate 10. The Senate considers the bill in the same manner as in the House of Representatives. Only the Finance Committee, the counterpart committee in the Senate, conducts the public/budget hearings.

Conference Committee 11. After both houses approved their own versions of the General Appropriations Bill, a Conference Committee is constituted, composed of Members from both houses to settle, reconcile or thresh

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject BUDGET LEGISLATION

Subject No. 2

Page 3 of 3

Responsibility Action

out differences or disagreements on any provision of the bill. The conferees are not limited to reconciling the differences in the bill but may introduce new provisions germane to the subject matter or may report out an entirely new bill on the subject.

House of Representatives/Senate 12. The Conference Committee Report is then submitted to both houses of Congress for consideration and approval. No amendment is allowed at this point.

President of the Senate/Speaker of the House of Representatives

13. The General Appropriations is then signed by the President of Senate and Speaker of the House of Representatives. It is certified by both the Secretary of the Senate and the Secretary-General of the House. It is then transmitted to the President of the Republic of the Philippines.

President of the Republic of the Philippines 14. The General Appropriations Bill is approved by the President, the same is assigned a Republic Act Number and is transmitted to the house of Representatives where it originated.

House of Representatives 15. The approved bill, now a Republic Act, is sent to the Official Gazette Office for publication. It is distributed to the implementing agencies.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject BUDGET EXECUTION AND

IMPLEMENTATION

Subject No. 3

Page 1 of 2

The third step of the budget process involves the Budget Execution and Implementation. This step is mainly concerned with the appropriation of funds. Responsibility Action

Manager, Corporate Planning Department 1. Prepares the cash budget of each PNOC department/office as soon as the annual GAA is approved by the President of the Republic of the Philippines. The Cash Budget is based on the thrusts, directions, and directives of the Office of the President of the Republic of the Philippines as well as the availability of cash.

2. Endorses the Cash Budget to the EXECOM for review and approval.

EXECOM 3. Endorses the Cash Budget to the President and CEO of PNOC.

President and CEO, PNOC 4. Approves the Annual Cash Budget.

Manager, Corporate Planning Department 5. Advises the departments/offices of their respective budget allocation as basis of their expenditure level.

6. Furnishes the Accounting Department the cash budget of all departments/offices.

Accounting Department 7. Prepares the Budget Utilization Report (BUR) of all departments/offices and provides copies to the same on or before the 15th day of the succeeding month.

8. Provides Corplan a copy of the overall PNOC BUR as well as BUR of each department/office.

If at any given time, a particular budget item is exhausted or found insufficient, the Department Manager may resort to the following: 1. Request the Budget Review Committee (BRC) for realignment of expense items within the

department;

2. Request the Budget Review Committee (BRC) for an augmentation for any budget item.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject BUDGET EXECUTION AND

IMPLEMENTATION

Subject No. 3

Page 2 of 2

Upon approval of the department’s request, Corplan makes the necessary adjustments in the budget. It is then presented to the Board of Directors for approval invoking the Special Provision applicable to PNOC as provided for in the General Appropriations Act. The copy of the approved adjusted budget is submitted to the House Committee on Appropriations, the Senate Finance Committee, and the Department of Budget and Management within 30 days after such adjustments are made. Note, however, that augmentation funds shall not be used for the acquisition of motor vehicles, payment of traveling, and representation and discretionary expenses.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject CAPITAL EXPENDITURE REQUEST/

IMPLEMENTATION PROCEDURE

Subject No. 4

Page 1 of 4

The following are the activities involving capital expenditure requests: I. BUDGET PREPARATION/REQUEST STAGE Responsibility Action

Proponent 1. The proponent prepares the capital budget requirements for the budget year by accomplishing the specified forms incorporated in the budget guidelines. Furniture, Fixture, Equipment and Books Outlay shall be justified based on the need/urgency of the request.

CAPEX requirements are subject to review and approval by the proponents' respective approving authorities (President, EVP, and SVP).

Budget Review Committee 2. During the Budget Review/Deliberation Workshop, BRC will evaluate all requests based on its impact on plans and programs of the company. If found necessary, capital expenditures are included in the Corporate Operating Budget for approval by the Board of Directors.

Board of Directors 3. The consolidated capital budget as approved by the BRC forms part of the Corporate Operating Budget to be presented to the Board of Directors for approval.

Congress (The Senate & House of Representatives)

4. The Board's approved capital expenditure budget request which forms part of the Corporate Operating Budget (COB) is submitted for approval by the President of the Philippines thru Congress and the Department of Budget and Management.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject CAPITAL EXPENDITURE REQUEST/

IMPLEMENTATION PROCEDURE

Subject No. 4

Page 2 of 4

II. APPROPRIATION REQUEST/IMPLEMENTATION STAGE Responsibility Action

PNOC 5. After approval of the COB, the company submits to DBM an Annual Procurement Program based on the approved level for capital expenditure and informs the concerned units their respective capital expenditure levels.

Proponent 6. Before the proponents can make any purchases, they must accomplish the Capital Budget Request/Appropriation (CBRA) duly signed by their respective approving authorities to be forwarded to the Corplan and Accounting Departments for appropriate action.

Purchases of the following shall be subject to clearance and/or authority from appropriate agencies:

a) Motor vehicles shall be subject to the final approval of the President;

b) Communication equipment shall be subject to clearance from the National Telecommunications Commission;

c) Information Technology equipment shall be subject to the guidelines and requirements of the National Computer Center; and

d) Building construction and land acquisition shall be subject to the approval of the Office of the President.

Corporate Accounting 7. Prepares a report at the end of the month on actual utilization of the capital expenditure budget. Provides the Corplan a copy for monitoring purposes.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject CAPITAL EXPENDITURE REQUEST/

IMPLEMENTATION PROCEDURE

Subject No. 4

Page 3 of 4

The following are the activities involving furnitures, fixtures, and equipment: Responsibility Action

Corporate Planning Department 1. Prepares the list of furnitures, fixtures, and equipment (FFE) for the approval of the Department of Budget and Management as soon as the annual GAA is approved by the President of the Republic of the Philippines.

2. Informs all departments/offices the FFE they have requested to be purchased as embodied in the annual budget proposal.

Proponent Department 3. Concurs or replaces FFE based on requirements of the department/office.

Corporate Planning Department 4. Consolidates all requests and submits to the Department of Budget and Management.

Department of Budget and Management 5. Reviews, evaluates, and approves requested FFE.

Corporate Planning Department 6. Provides all departments their approved FFE.

7. Provides the Accounting Department PNOC’s approved FFE.

Proponent Department 8. Accomplish CBRA for the purpose. Purchase of the following shall be subject to clearance and/or authority from appropriate agencies:

a) Motor vehicles shall be subject to the approval of the Office of the President;

b) Information Technology equipment shall be subject to the guidelines and requirements of the National Computer Center;

c) Infrastructure Projects above P50 million pesos shall be subject to the

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject CAPITAL EXPENDITURE REQUEST/

IMPLEMENTATION PROCEDURE

Subject No. 4

Page 4 of 4

Responsibility Action

approval of the Office of the President.

Accounting Department 9. Holds a copy of PNOC’s approved FFE.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject REALIGNMENT

Subject No. 5

Page 1 of 4

Realignment of budgetary items in PNOC is provided for in the annual General Appropriations Act – Special Provision Applicable to PNOC. The Special Provision provides that,

“the Philippine National Oil Company (PNOC), through its Board of Directors, is authorized to realign programs and projects and reallocate the corresponding budgetary requirements herein approved, as well as augment the requirements which may arise from factors beyond the Company’s control. These may include, but shall not be limited to, increase in costs associated with the privatization of subsidiaries, changes in foreign exchange rates, taxes, inflation, change in interest rates, payments of obligations as a result of the final judgment of the court, and changes in programs/projects: PROVIDED, That augmentation funds shall not be used for the acquisition of motor vehicles and payment of traveling, representation and discretionary expenses: PROVIDED, FURTHER, That the Personal Services shall not be augmented by savings from Maintenance and Other Operating Expenses (MOOE), as well as, Capital Outlay, or by new funding sources. A report on the aforesaid budgetary adjustments shall be submitted to the House Committee on Appropriations and the Senate Committee on Finance, including the Department of Budget and Management, within thirty (30) days after such adjustments are made.

The following are activities involving a company-wide Budget Realignment, which is usually prepared during the 1st month of the 4th quarter of the year: Responsibility Action

Accounting Department 1. Issues monthly Budget Utilization Report (BUR) – company-wide.

2. Provides copies of the BUR to the EXECOM and the Corporate Planning Department.

Corporate Planning Department 3. Reviews the BUR.

4. Determines budgetary requirements for accounts which may need realignment or augmentation.

5. Prepares Report to the Budget Review Committee/EXECOM.

Budget Review Committee and/or EXECOM 6. Reviews, evaluates, and recommends approval of the budgetary realignment and/or augmentation.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject REALIGNMENT

Subject No. 5

Page 2 of 4

Responsibility Action

President 7. Endorses the budgetary realignment and/or augmentation.

PNOC Board 8. Approves/disapproves the budgetary realignment and/or augmentation.

Corporate Planning Department 9. Incorporates the budgetary realignment and/or augmentation in the annual Corporate Operating Budget.

10. Provides the Accounting Department with the budgetary realignment and/or augmentation.

11. Secures a Secretary’s Certificate from the Office of the Corporate Secretary regarding the realignment and/or augmentation.

12. Prepares a report to the Committee on Appropriations, House of Representatives; Committee on Finance, Senate; and the Department of Budget and Management (DBM) within 30 days after the adjustments were made, as provided for in the Special Provision Applicable to PNOC.

13. Transmits the report together with the Secretary’s Certificate to the House of Representatives, Senate, and DBM.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject REALIGNMENT

Subject No. 5

Page 3 of 4

The following are activities involving a department-wide Budget Realignment: Responsibility Action

Accounting Department 1. Issues monthly Budget Utilization Report (BUR) on a per Cost Center basis.

2. Provides copies of the BUR to the Cost Center Administrators.

All Departments 3. Reviews the BUR.

Concerned Department 4. Submits to the Corporate Planning Department the Request for Realignment/Augmentation of accounts expected to run-out of budget.

Corporate Planning Department 5. Consolidates all requests.

6. Evaluates the requests based Department Work Plans.

7. Identify sources of funds or savings which can be tapped for the Cost Center’s request for realignment/augmentation.

8. Recommends approval/disapproval to the Budget Review Committee and/or EXECOM the needed realignment/augmentation.

Budget Review Committee and/or EXECOM 9. Reviews, evaluates, and recommends approval/disapproval of the recommended realignment and/or augmentation.

President 10. Approves/disapproves the budgetary realignment and/or augmentation.

Corporate Planning Department 11. Provides the Accounting Department the approved/disapproved budgetary realignment and/or augmentation.

12. Provides the concerned Cost Center Administrator the approved/disapproved budgetary realignment and/or augmentation.

PNOC BUDGET

Section PROCEDURES

Section No. 3

Effective 10.26.01

MANUAL

Subject REALIGNMENT

Subject No. 5

Page 4 of 4

Responsibility Action

13. Incorporates the approved budgetary realignment and/or augmentation in the concerned Cost Center’s Budget.

PNOC BUDGET

Section FLOWCHART (BUDGET PROCESS)

Section No. 4

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 4

START NARRATIVE DESCRIPTION OPERATION NO.

1. Government agencies determine budgetary priorities and activities based on the national development plan, with consideration of ceilings imposed by available revenues and borrowing limits 2. DBM, in coordination with NEDA and DoF, determines the overall expenditure levels, the revenue projections, the deficit levels, and the financing plans 3. DBM issues a budget call. 4. DBM holds budget consultations with agencies. 5. DBM evaluates budget to determine if reductions can be made

X

PNOC BUDGET

Section FLOWCHART (BUDGET PROCESS)

Section No. 4

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 2 of 4

X NARRATIVE DESCRIPTION OPERATION NO 6. The final consolidated budget is submitted by the President of the Philippines to Congress. 7. Proposed budget is presented first to the House of Representatives as an Appropriations bill 8. The Appropriations bill is referred to the Committee on Appropriations to handle an initial budget review. 9. The Committee summons the different agencies to explain and justify their respective proposed budget. 10. Proposed budget is presented to the House body as a bill (General Appropriations Bill).

Y

PNOC BUDGET

Section FLOWCHART (BUDGET PROCESS)

Section No. 4

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 3 of 4

NARRATIVE DESCRIPTION OPERATION Y NO.

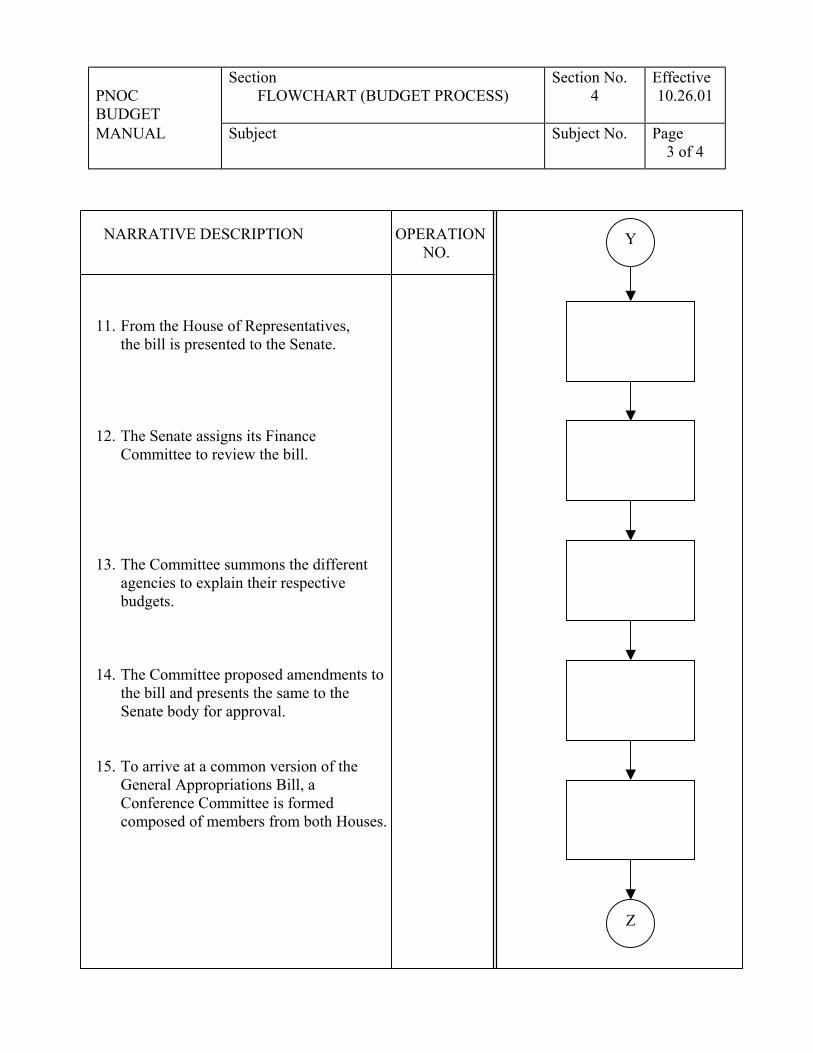

11. From the House of Representatives, the bill is presented to the Senate. 12. The Senate assigns its Finance Committee to review the bill. 13. The Committee summons the different agencies to explain their respective budgets. 14. The Committee proposed amendments to the bill and presents the same to the Senate body for approval. 15. To arrive at a common version of the General Appropriations Bill, a Conference Committee is formed composed of members from both Houses.

Z

PNOC BUDGET

Section FLOWCHART (BUDGET PROCESS)

Section No. 4

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 4 of 4

NARRATIVE DESCRIPTION OPERATION Z NO.

16. The Conference Committee report is submitted to both Houses of Congress for consideration and approval 17. Once approved, the General Appropriations Bill is submitted to the President of the Philippines for signing into law. It shall be known as the General Appropriations Act. 18. DBM, as mandated by the General appropriations Act, executes and implements the expenditure program. 19. Management reviews budget execution

and seeks to report and interpret the significance of financial data as reported. 20. Management evaluates the accountability of funds and the effectiveness of programs and performance.

END

PNOC BUDGET

Section GLOSSARYOF TERMS

Section No. 5

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 1

Budget - is a financial plan composed of the estimates of income, operating expenditures and

borrowings to achieve the plans and programs of the company for the budget year. Budget year - is the entire period starting January 01 to December 31 of the year following the

current year. Budget proponent - is the department/division/office/cost center from which the budget proposal

originates. Budget Review Committee (BRC) - is an ad hoc body created for the purpose of reviewing,

analyzing and approving the budget of each department/office. The committee is composed of the following officers:

Executive Vice-President - Chairman Senior Vice-President, Management Services - Co-Vice-Chairman Senior Vice-President, Legal, Administrative - Co-Vice-Chairman Services and Estate Management Manager, Corporate Planning Department - Member Budget Deliberation Workshop - an informal gathering of officers and members involved in the

budget preparation for the purpose of discussing budget proposals and mutually arriving at an acceptable budget allocation

Realignment - is the reallocation of budget resources or savings of one expenditure item to

another expenditure item found to be insufficient to continue the implementation of programs or operation of the company. Realignment is also applicable for capital expenditure budget that remains unexpended.

Augmentation - is increasing the budget level of an expenditure item or program whose financial

resources are determined to be insufficient when implemented and subsequently evaluated.

Special Provision - is an authority requested by the company from Congress because of the

unique or peculiar conditions and/or circumstances that are applicable only to them such as its operations, changing work programs and plans and its corresponding budgetary requirements, changing financial/economic indicators and other internal and external factors which can materially affect the budget. This provision is subject to limitations or restrictions imposed by Congress which should govern the company in the use of its budget. Budget flexibility is one special provision that the company may request from Congress.

PNOC BUDGET

Section BUDGET CALENDAR

Section No. 6

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 1

ACTIVITY SCHEDULE

Issuance of Budget Call by DBM First week of January Issuance of Budget Guidelines and Second week Financial Assumptions/Economic Indicators of January by Corplan Submission of the Department's Budget and First week of subsidiaries' STCO and LTCO to Corplan February Budget Review/Deliberation Workshop Second Week of February Presentation of Budget to the BOD by the BRC First week of March Preparation of the COB First to Second Week of March Approval of COB by the President of the company Second week of March Submission of COB to DBM Second week of March Budget Hearings - DBM April to July Approval by the President of the Philippines Budget Hearings - House of Representatives July to October (General Appropriations Bill) Budget Hearings - Upper House November to (General Appropriations Act) December (Note: The above calendar is subject to change depending on the schedule set by the Department of Budget and Management and Congress of the Philippines.)

PNOC BUDGET

Section PERTINENT LAWS

Section No. 7

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 1

Presidential Decree No. 985 - a decree revising the position classification and compensation system in the National

Government, and integrating the same. Presidential Decree No. 1177 - revising the budget process in order to institutionalize the budgetary innovation of the

new society. Executive Order No. 518 - establishing a procedure for the preparation and approval of the operating budgets of

government-owned and controlled corporations. Letter of Instruction No. 457 - budgetary guidelines regarding the preparations of the General Appropriations Decree.

PNOC BUDGET

Section REFERENCES

Section No. 8

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 1

ANTHONY, ROBERT N., GLENN A. WELSCH and JAMES S. REECE. Fundamentals of

Management Accounting. Homewood, Illinois: Richard D. Irwin, Inc. 1985. CARAGUE, GUILLERMO N. Developments in Philippine Government Budgeting Under The

Aquino Administration. Manila: The Public Information Service (DBM). 1991 DEPARTMENT OF BUDGET AND MANAGEMENT. Primer on Government Budgeting FERNANDEZ, FELISA D. The Budget Process and Economic Development. Manila:

Community Publishers, Inc. 1973 LAYA, JAIME C. Philippine Government Budgeting - Policy and Practice in the New Society.

Manila: NEDA-APO Production Unit, 1979. LOUDERBACK, JOSEPH G. III and GERALDINE F. DOMINIAK. Managerial Accounting.

Boston, Massachusetts: Kent Publishing Company, 1982 MOORE, CARL L., ROBERT K. JAEDICKE and VICTOR R. CUSI. Managerial Accounting.

Cincinnati, Ohio: South-Western Publishing Co. 1981. TRAPANI, COSMO S. Management Accounting.

PNOC BUDGET

Section REFERENCES

Section No. 9

Effective 10.26.01

MANUAL

Subject

Subject No.

Page 1 of 35

The budget requirements of each department are consolidated with the use of a computerized Automated Budget System, or ABS. Each department is afforded the use of the system via the local area network connection, whereby the user inputs the figures on a screen format of the various budget categories. In turn, the Budget Division, with the aid of MIS, downloads all the data from all the users to form a consolidated budget. The following forms are printouts of the computerized schedules used to facilitate consolidation. These schedules are periodically reviewed and likewise revised, should the need arise.

Personal Services Schedules 1 & 2 Per Diem of the Board Schedule 3 Domestic Travel Schedule 4 Foreign Travel Schedule 5 Communication Expenses Schedule 6 Repair and Maintenance of Government Facilities Schedule 7 Repair and Maintenance of Government Vehicles Schedule 8 Transportation Services Schedule 9 Supplies and Materials Schedule 10 Rent Schedule 11 Statement of Borrowings Schedule 12 Grants, Subsidies, and Contributions Schedule 13 Awards and Indemnities Schedule 14 Depreciation Schedule 15 Water, Illumination, and Power Service Schedule 16 Auditing Services Schedule 17 Training and Seminar Expenses Schedule 18 Employee Recreation Schedule 19 Contribution and Membership Schedule 20 Meetings and Conferences Schedule 21 Representation and Meetings Schedule 22 Other Business Expense Schedule 23 Taxes, Duties, and Fees Schedule 24 Advertising and Publication Expenses Schedule 25 Gasoline, Oil, and Lubricants Schedule 26 Fidelity Bonds and Insurance Premiums Schedule 27 Other Services Schedule 28 Printing Projects Schedule 29 Subscription Schedule 30 Sundry Expenses Schedule 31

![dfat.gov.au · Web viewDFAT Budget Statements. DFAT Budget Statements. Portfolio overview. ASIS Budget Statements [] Budget Statements . 2019-20 PBS 31 March 1400.DOCX2019-20 PBS](https://static.fdocuments.in/doc/165x107/5ccd648688c9932b558d9fa3/dfatgovau-web-viewdfat-budget-statements-dfat-budget-statements-portfolio.jpg)