Second Quarter Results - golarlngpartners.com/media/Files/G/Golar-Partners/documents/... · Unless...

15

© Golar LNG Partners LP Second Quarter 2018 Results 1

-

Upload

hoangkhanh -

Category

Documents

-

view

218 -

download

0

Transcript of Second Quarter Results - golarlngpartners.com/media/Files/G/Golar-Partners/documents/... · Unless...

© Golar LNG Partners LP

Second

Quarter

2018

Results1

© Golar LNG Partners LP

FORWARD

LOOKING

STATEMENTS

This presentation contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as amended) which

reflects management’s current expectations, estimates and projections about its operations. All statements, other than statements of historical

facts, that address activities and events that will, should, could or may occur in the future are forward-looking statements. Words such as

“may,” “could,” “should,” “would,” “expect,” “plan,” “anticipate,” “intend,” “forecast,” “believe,” “estimate,” “predict,” “propose,”

“potential,” “continue,” or the negative of these terms and similar expressions are intended to identify such forward-looking statements. These

statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond

our control and are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in

such forward-looking statements. You should not place undue reliance on these forward-looking statements, which speak only as of the date of

this presentation. Unless legally required Golar LNG Partners LP undertakes no obligation to update publicly any forward-looking statements

whether as a result of new information, future events or otherwise.

Important factors that could cause actual results to differ materially include, but are not limited to: statements about market trends in the

floating storage and regasification unit (or FSRU), liquefied natural gas (or LNG) carrier and floating liquefied natural gas vessel (or FLNG)

industries, including charter rates, factors affecting supply and demand, and opportunities for the profitable operations of FSRUs, LNG carriers

and FLNGs; Golar Partners’ ability to maintain distributions and the amount of any such distributions; statements about Golar Partners’ and

Golar LNG Limited’s ability to retrofit vessels as FSRUs or FLNGs and the timing of the delivery and acceptance of any such retrofitted

vessels by their respective charterers; Golar Partners’ ability to acquire additional common units in Golar Hilli LLC on a timely basis or at all;

Golar Partners’ ability to integrate and realize the expected benefits from acquisitions and potential acquisitions, including the FLNG Hilli

Episeyo; Golar Partners’ future share of annual contracted revenues, net of operating expenses relating to the Hilli Episeyo, which will be

accounted for under the equity method; Golar Partner’s ability to realize the expected benefits from the Atlantic project; Golar Partners’

anticipated growth strategies; the effect of a worldwide economic slowdown; turmoil in the global financial markets; fluctuations in currencies

and interest rates; general market conditions, including fluctuations in charter hire rates and vessel values; changes in commodity prices; the

liquidity and creditworthiness of Golar Partners’ charterers; changes in Golar Partners’ operating expenses, including dry-docking and

insurance costs and bunker prices; Golar Partners’ future financial condition or results of operations and future revenues and expenses; the

repayment of debt and settling of interest rate swaps; Golar Partners’ and Golar LNG Limited’s ability to make additional borrowings and to

access debt and equity markets; planned capital expenditures and availability of capital resources to fund capital expenditures; Golar Partners’

ability to maintain long-term relationships with major LNG traders; Golar Partners’ ability to leverage Golar LNG Limited’s and Golar Power

Limited’s relationships and reputation in the shipping and FSRU industries; Golar Partners’ ability to purchase vessels from Golar LNG

Limited and Golar Power Limited in the future; Golar Partners’ continued ability to enter into long-term time charters, including our ability to

re-charter the FSRUs and carriers following the termination or expiration of their time charters; Golar Partners’ ability to maximize the use of

its vessels, including the re-deployment or disposition of vessels no longer under long-term time charter; timely purchases and deliveries of

newbuilding vessels; future purchase prices of newbuildings and secondhand vessels; Golar Partners’ ability to compete successfully for future

chartering and newbuilding opportunities; acceptance of a vessel by its charterer; termination dates and extensions of charters; the expected

cost of, and Golar Partners’ ability to comply with, governmental regulations, maritime self-regulatory organization standards, as well as

standard regulations imposed by its charterers applicable to Golar Partners’ business; availability of skilled labor, vessel crews and

management; Golar Partners’ general and administrative expenses and its fees and expenses payable under the fleet management agreements

and the management and administrative services agreement; the anticipated taxation of Golar Partners and distributions to Golar Partners’

unitholders; challenges by authorities to the tax benefits of Golar Partners’ previously obtained, estimated future maintenance and replacement

capital expenditures; Golar Partners’ and Golar LNG Limited’s ability to retain key employees; customers’ increasing emphasis on

environmental and safety concerns; potential liability from any pending or future litigation; potential disruption of shipping routes due to

accidents, political events, piracy or acts by terrorists; Golar Partners’ business strategy and other plans and objectives for future operations;

and other factors listed from time to time in the reports and other documents that Golar Partners files with the U.S. Securities and Exchange

Commission. Factors may cause actual results to be materially different from those contained in any forward-looking statement. Golar Partners

does not intend to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in Golar

Partners’ expectations with respect thereto or any change in events, conditions or circumstances on which any such statement is based.

2

© Golar LNG Partners LP

Recent Highlights

Net income attributable to unit holders of $28.4 million and operating income of

$36.6 million.

Generated distributable cash flow1 of $23.0 million for the quarter, with a

distribution coverage ratio of 0.562.

FLNG Hilli Episeyo accepted by charterers Perenco and SNH. Completed

acquisition of initial equity interest on July 12.

Resume discussions regarding acquisition of additional common units in Golar

Hilli LLC.

Shipping market shows solid signs of improvement. Secured 10-month charter

for Golar Maria.

Selected FSRU Golar Freeze to service 15-year Atlantic project. Vessel enters

Dubai Drydocks.

Declared unchanged distribution for 2Q of $0.5775 per unit.

1 Distributable cash flow (DCF) is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure. Also see Slide 7.2 Distribution coverage ratio is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure. Also see Slide 7.

3

© Golar LNG Partners LP

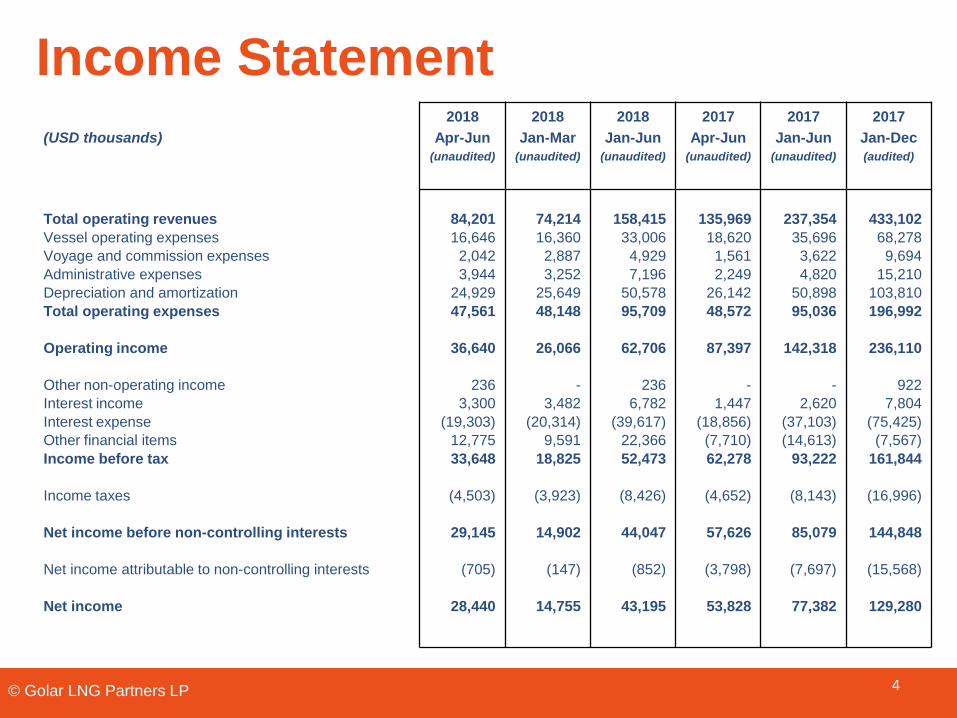

Income Statement

(USD thousands)

2018

Apr-Jun

(unaudited)

2018

Jan-Mar

(unaudited)

2018

Jan-Jun

(unaudited)

2017

Apr-Jun

(unaudited)

2017

Jan-Jun

(unaudited)

2017

Jan-Dec

(audited)

Total operating revenues

Vessel operating expenses

Voyage and commission expenses

Administrative expenses

Depreciation and amortization

Total operating expenses

Operating income

Other non-operating income

Interest income

Interest expense

Other financial items

Income before tax

Income taxes

Net income before non-controlling interests

Net income attributable to non-controlling interests

Net income

84,201

16,646

2,042

3,944

24,929

47,561

36,640

236

3,300

(19,303)

12,775

33,648

(4,503)

29,145

(705)

28,440

74,214

16,360

2,887

3,252

25,649

48,148

26,066

-

3,482

(20,314)

9,591

18,825

(3,923)

14,902

(147)

14,755

158,415

33,006

4,929

7,196

50,578

95,709

62,706

236

6,782

(39,617)

22,366

52,473

(8,426)

44,047

(852)

43,195

135,969

18,620

1,561

2,249

26,142

48,572

87,397

-

1,447

(18,856)

(7,710)

62,278

(4,652)

57,626

(3,798)

53,828

237,354

35,696

3,622

4,820

50,898

95,036

142,318

-

2,620

(37,103)

(14,613)

93,222

(8,143)

85,079

(7,697)

77,382

433,102

68,278

9,694

15,210

103,810

196,992

236,110

922

7,804

(75,425)

(7,567)

161,844

(16,996)

144,848

(15,568)

129,280

4

© Golar LNG Partners LP

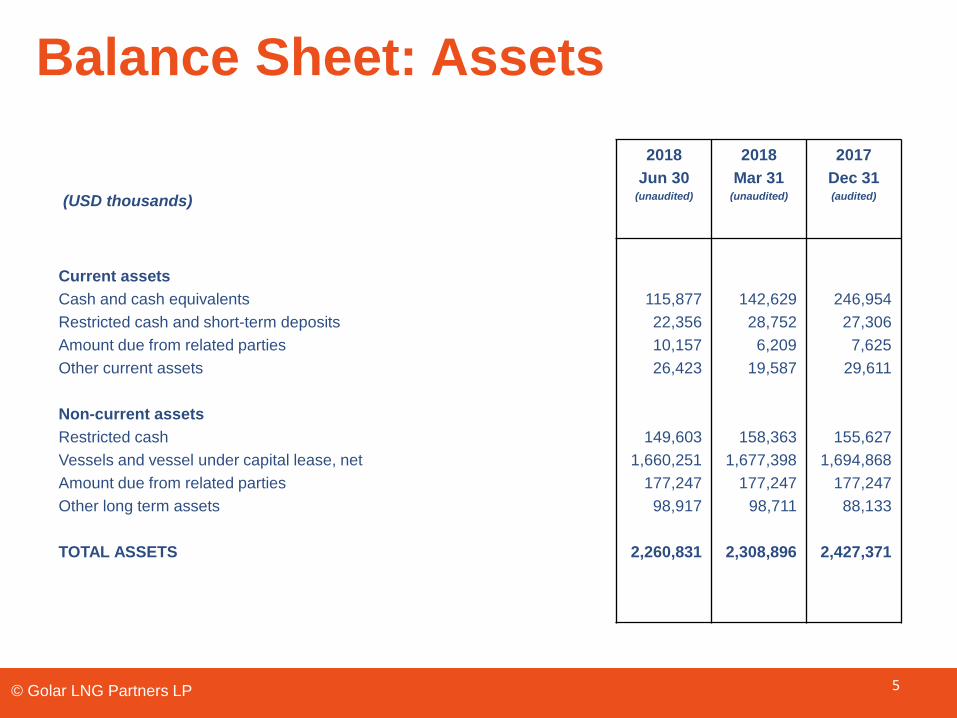

Balance Sheet: Assets

(USD thousands)

2018

Jun 30(unaudited)

2018

Mar 31(unaudited)

2017

Dec 31(audited)

Current assets

Cash and cash equivalents

Restricted cash and short-term deposits

Amount due from related parties

Other current assets

Non-current assets

Restricted cash

Vessels and vessel under capital lease, net

Amount due from related parties

Other long term assets

TOTAL ASSETS

115,877

22,356

10,157

26,423

149,603

1,660,251

177,247

98,917

2,260,831

142,629

28,752

6,209

19,587

158,363

1,677,398

177,247

98,711

2,308,896

246,954

27,306

7,625

29,611

155,627

1,694,868

177,247

88,133

2,427,371

5

© Golar LNG Partners LP

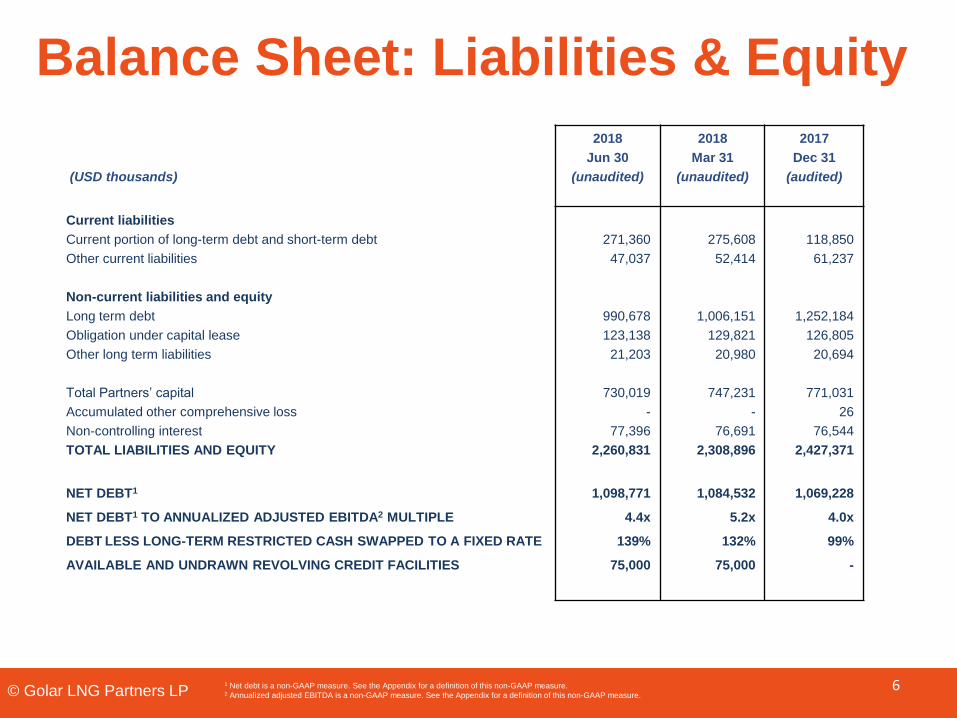

Balance Sheet: Liabilities & Equity

(USD thousands)

2018

Jun 30

(unaudited)

2018

Mar 31

(unaudited)

2017

Dec 31

(audited)

Current liabilities

Current portion of long-term debt and short-term debt

Other current liabilities

Non-current liabilities and equity

Long term debt

Obligation under capital lease

Other long term liabilities

Total Partners’ capital

Accumulated other comprehensive loss

Non-controlling interest

TOTAL LIABILITIES AND EQUITY

NET DEBT1

NET DEBT1 TO ANNUALIZED ADJUSTED EBITDA2 MULTIPLE

DEBT LESS LONG-TERM RESTRICTED CASH SWAPPED TO A FIXED RATE

AVAILABLE AND UNDRAWN REVOLVING CREDIT FACILITIES

271,360

47,037

990,678

123,138

21,203

730,019

-

77,396

2,260,831

1,098,771

4.4x

139%

75,000

275,608

52,414

1,006,151

129,821

20,980

747,231

-

76,691

2,308,896

1,084,532

5.2x

132%

75,000

118,850

61,237

1,252,184

126,805

20,694

771,031

26

76,544

2,427,371

1,069,228

4.0x

99%

-

1 Net debt is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure.2 Annualized adjusted EBITDA is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure.

6

© Golar LNG Partners LP

Distributable Cash Flow(USD thousands) Three months ended

Jun 30, 2018

Three months ended

Mar 31, 2018

Three months ended

Dec 31, 2017

Adjusted EBITDA1 61,805 51,715 67,053

Interest Income3,300 3,482 3,079

Interest expense (excluding amortization of deferred charges) (17,596) (17,734) (17,055)

Other cash financial items (224) (839) (1,625)

Current income tax charge (4,124) (3,483) (3,434)

Deferred (expenses)/income (234) (231) 332

Estimated maintenance & replacement capital expenditures (including drydocking reserve) (15,600) (15,796) (15,672)

Non-controlling interest’s share of DCF before maintenance and replacement capital expenditure (1,358) (800) (4,636)

Distributions relating to preferred units (3,019) (2,985) (2,080)

Distributable cash flow 22,950 13,329 25,962

Depreciation and amortization (24,929) (25,649) (26,556)

Unrealized net gain from interest rate derivatives7,829 10,693 9,222

Unrealized gain on IDR reset4,500 - 1,559

Unrealized foreign exchange gain / (loss)670 (262) (76)

Amortization of deferred charges(1,707) (2,580) (1,391)

Deferred expenses/(income)234 230 (332)

Movement in deferred tax liability(379) (440) (540)

Release of deferred tax asset- - (501)

Distributions relating to preferred units3,019 2,985 2,080

Estimated maintenance and replacement capital expenditures (including dry-docking reserve)15,600 15,796 15,672

Non-controlling interest’s share of DCF before maintenance and replacement capital expenditure1,358 800 4,636

Net income before non-controlling interests29,145 14,902 29,735

Distributions declared 41,169 41,224 41,478

Distribution coverage ratio2 0.56 0.32 0.63

1 Adjusted EBITDA is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure.2 Distributable cash flow is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure.

7

© Golar LNG Partners LP

$2.5bn of Effective Revenue Backlog(1)

Recent dropdown

2018 2019 2020 2021 2022 2023 2024 2025

Golar MariaSpot market

Golar Mazo (60% owned)Warm layup/spot market

Golar Eskimo10-year contract

Golar FreezeBalance of DUSUP + 15-year Atlantic charter

Golar SpiritCold layup

Methane Princess20-year contract

Nusantara Regas Satu11-year contract

Golar Winter10-year contract extended to 15 years

Golar Grand2-year contract

Hilli Episeyo (50% of common units)8-year contract

Golar Igloo5-year contract

Shell

Energy and

logistics

Company –

Atlantic basin

(1) See the Appendix for a definition of this non-GAAP measure.

Dusup = Dubai Supply Authority. Nusantara Regas = Joint venture between Pertamina and PGN (National Gas distribution company of Indonesia). KNPC = Kuwait

National Petroleum Company.

FS

RU

s

LN

G C

arr

iers

FL

NG

Base contract duration Options

Government of the

Hashemite

Kingdom of Jordan

International

Oil Major

Expected short-term trading

Spot & short-

term market

Spot market

8

Warm layupPeriod of duplicate hire Cold layup

© Golar LNG Partners LP

FLNG Hilli Episeyo

Vessel accepted on June 2 with effect May 31, 2018.

Achieved 100% commercial availability to date.

On schedule to export 6th cargo.

$960m sale & leaseback facility fully drawn on June 20, 2018.

Acquisition of initial 50% of common units in Golar Hilli LLC closed

on July 12, 2018.

Investment of available funds in additional common units currently

being discussed.

Post July 11, 2018 rights to future distributions* in

Golar Hilli LLC

Golar

Partners

Golar LNG

Limited

Keppel and

Black &

Veatch

Common units 50% 44.6% 5.4%

Expansion Capacity (currently uncontracted) 2.5% 86.9% 10.6%

Brent crude oil linked upside 0% 89.1% 10.9%

9

* Right to future distributions does not directly correlate with ownership interest as common unit holders

have 5% entitlement on a pro-rata basis to expansion capacity.

© Golar LNG Partners LP

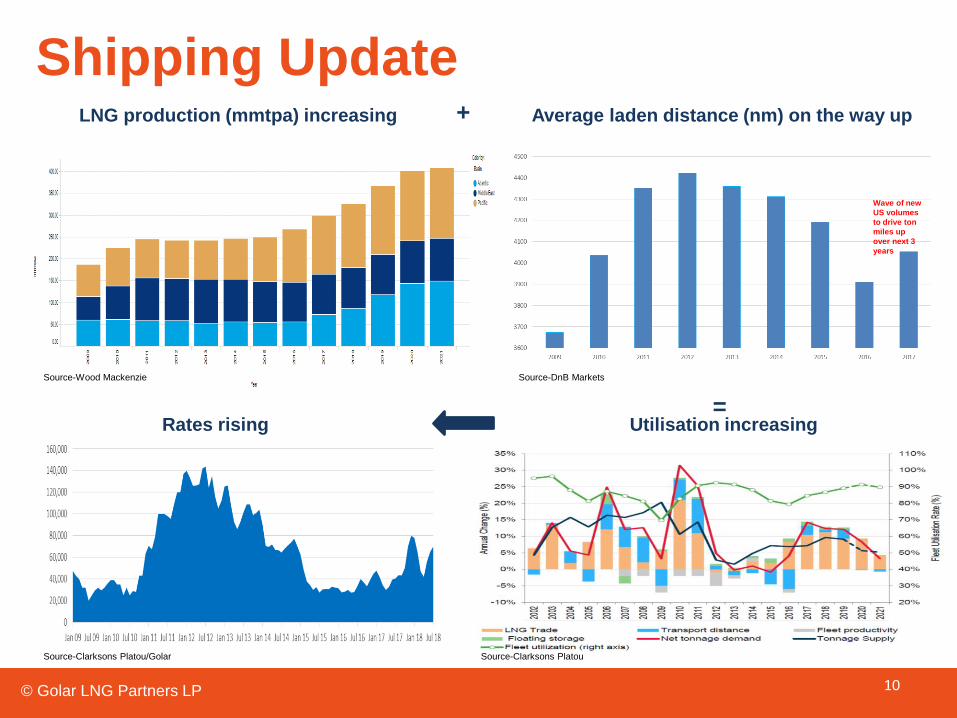

Shipping Update

10

LNG production (mmtpa) increasing Average laden distance (nm) on the way up+

Source-Clarksons Platou/Golar Source-Clarksons Platou

Source-Wood Mackenzie Source-DnB Markets

Utilisation increasing=

Rates rising

Wave of new

US volumes

to drive ton

miles up

over next 3

years

© Golar LNG Partners LP

FSRU UpdateFSRU Golar Freeze selected to service 15-year Atlantic contract:

Contract expected to commence around year-end.

Current charterer is obligated to pay charterhire until April 2019.

Vessel now in yard for dry-dock and necessary modifications. No offhire will be incurred.

Potential additional contracts: Lower capital cost of existing assets & access to low cost

conversion model allows Golar Partners to transact at rates that support other small-mid size

projects whilst still generating attractive returns:

Lebanon, Mexico, Columbia, Benin & Croatia recently issued tenders, some of which suit Golar

Partners smaller/cheaper assets. Golar Partners also in bilateral discussions for other projects.

Potential conversion contract for Maria or Mazo taking time to reach a final investment

decision.

Acquisition target: Golar Nanook represents a 2020 acquisition target:

25+1 year contract with forecast annual EBITDA1 $41 million adjusted annually for US CPI.

Attractive financing commitment received with long repayment profile.

Newbuild FSRU market highly competitive:

Golar Igloo charter likely to be re-tendered this year for commencement in 2019.

Current charterers very happy with Golar’s operations and 100% uptime – Partnership expects

to participate in tender.

If unsuccessful, Golar Igloo will trade in the increasingly attractive shipping market as a

conventional 170,000cbm TFDE carrier.

1 EBITDA is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure. 11

© Golar LNG Partners LP

Summary

Solid contract base – Effective revenue backlog1 of $2.5 billion equivalent to 7.4 revenue

backlog years2 including Atlantic FSRU contract and initial interest in FLNG Hilli Episeyo.

Excellent operating results – 100% utilization achieved for scheduled operations once again.

Fast growing LNG market – LNG share of total gas trade expected to increase from 33% to

40% by 2023.

Future acquisition and re-contracting opportunities – Additional common units in Golar Hilli

LLC and Hilli expansion; Golar Power 25-yr Sergipe project; Golar’s LNG carriers; new FLNG

and FSRU projects.

But first need to navigate transition period – 3Q distribution coverage ratio3 expected to be in

0.7 range. Improving shipping market expected to add some coverage in 4Q. Investment in

additional Golar Hilli LLC common units being considered but portion contemplated unlikely

to close gap to 1.0x.

Distribution therefore remains under review – Expect to provide clarity on future distribution

levels when 3Q distribution declared in October.

1 See the Appendix for a definition of this non-GAAP measure. 2 See the Appendix for a definition of this non-GAAP measure.

3 Distribution coverage ratio/coverage ratio is a non-GAAP measure. See the Appendix for a definition of this non-GAAP measure. Also see slide 7.

12

THANK

YOU

© Golar LNG Partners LP 13

© Golar LNG Partners LP

Appendix A – Non-GAAP measures

14

Adjusted EBITDA: Adjusted EBITDA is defined as earnings before interest, other financial items, taxes, depreciation and amortization and non-controlling interest.

Adjusted EBITDA is a non-GAAP financial measure. A non-GAAP financial measure is generally defined by the Securities and Exchange Commission as one that

purports to measure historical or future financial performance, financial position or cash flows, but excludes or includes amounts that would not be so adjusted in the

most comparable U.S. GAAP measure. We have presented Adjusted EBITDA as we believe it provides useful information to investors because it is a basis upon which

we measure our operations and efficiency. Adjusted EBITDA is not a measure of our financial performance under U.S. GAAP and should not be construed as an

alternative to net income (loss) or other financial measures presented in accordance with U.S. GAAP.

Distributable cash flow: Distributable cash flow is a non-GAAP measure used by investors to measure the performance of master limited partnerships. Refer to our

most recent quarterly earnings release on our investor relations section on our website (www.golarlngpartners.com) for a reconciliation to the most directly comparable

financial measure under US GAAP.

Distribution coverage ratio: Distribution coverage ratio represents the ratio of distributable cash flow to total cash distributions paid. Refer to our most recent

quarterly earnings release on our investor relations section on our website (www.golarlngpartners.com) for a reconciliation to the most directly comparable financial

measure under US GAAP.

Effective revenue backlog: Effective revenue backlog is defined as the contracted daily charter rate for each vessel multiplied by the number of scheduled hire days

for the remaining contract term, which includes GMLP's pro-rata share of Hilli Episeyo contractual billings which will be recorded as "Equity in net earnings of affiliates".

Net Debt: Net Debt is a non-GAAP financial measure and is defined as short-term debt and long-term debt, plus obligations under capital leases, less cash and cash

equivalents, less restricted cash and short-term deposits. Net Debt is used by investors to measure our performance and should not be considered as an alternative

to any other indicator of our performance calculated in accordance with U.S. GAAP. We believe that net debt assists our management and investors by increasing the

comparability of our combined indebtedness and cash position against other companies in our industry. Net Debt is not a measure of our financial performance under

U.S. GAAP and should not be construed as an alternative to other financial measures presented in accordance with U.S. GAAP.

Revenue backlog years: Revenue backlog years is defined as effective revenue backlog divided by annualized current quarter revenues. This includes the Atlantic

FSRU contracts and GMLP's pro-rata share of Hilli Episeyo contractual billings which will be recorded as "Equity in net earnings of affiliates".

© Golar LNG Partners LP

Appendix B

(USD thousands)

Three months

ended

June 30,

2018

Three months

ended

March 31,

2018

Three months

ended

June 30,

2017

Net Income 29,145 14,902 57,626

Depreciation and amortization 24,929 25,649 26,142

Interest Income (3,300) (3,482) (1,447)

Interest Expense 19,303 20,314 18,856

Other Financial Items (12,775) (9,591) 7,710

Tax 4,503 3,923 4,652

Adjusted EBITDA 61,805 51,715 113,539

Annualized Adjusted EBITDA (Adjusted EBITDA X 4) 247,220 206,860 454,156

Current portion of long-term debt and short term debt 271,360 275,608 115,758

Long-term debt 990,678 1,006,151 1,339,098

Obligation under capital lease 124,569 132,517 123,934

Total Debt 1,386,607 1,414,276 1,578,790

Cash and cash equivalents (115,877) (142,629) (301,486)

Restricted cash and short term deposits - current (22,356) (28,752) (16,845)

Restricted cash – non-current (149,603) (158,363) (121,206)

Total cash, cash equivalents and restricted cash (287,836) (329,744) (439,537)

Net Debt 1,098,771 1,084,532 1,139,253

Net Debt to Annualized Adjusted EBITDA 4.4 5.2 2.5

15