Watch/Warnings in CAP NWS Partners Meeting Bob Bunge OCIO 1/21/10.

Boston Partners Large Cap Value Equity

Second Quarter 2018

team updated 4/25/16

Boston Partners Large Cap Value EquityTable of Contents

Boston Partners n

Section

i. Firm Overview 1

ii. Philosophy and Process 5

Appendix

i. Large Cap Value Portfolio

ii. Large Cap Value Investment Performance

iii. Concentrated Large Cap Value Equity Portfolio

iv. Supplemental Information

v. Biographical Information

vi. Investment Strategies Performance, Fee Schedules and Performance Disclosures

Boston Partners n 1

Who We AreA Focused Investment Organization

• Founded in 1995

• One philosophy and investment process that pre-dates our founding and has been in place for 30 years

• All established disciplines have outperformed their benchmark since inception2

• 152 employees: Boston, New York, California, and London

1 Data as of June 30, 2018.Assets Under Management include: Boston Partners ($94.9 B); WPG Partners ($1.7 B); and Redwood ($0.1 B).2 Boston Partners' established disciplines are defi ned as the disciplines that started the year the fi rm was founded (1995): Large Cap Value Equity; Premium Equity; Mid Cap Value Equity; and Small Cap Value Equity. Organizational information can be found in the appendix.

$96.7 Billion Assets Under Management1

Boston Partners n 2

Boston PartnersProfi le: June 30, 2018

* Key investment professionals have worked together since the founding of Boston Partners in 1995 and years before at a prior fi rm, where the investment philosophy was established.Assets Under Management include: Boston Partners ($94.9 B); WPG Partners ($1.7 B); and Redwood ($0.1 B). Organizational information can be found in the appendix.

Disciplines Assets ($ Millions)

Large Cap Value, Concentrated Large Cap Value, 130/30 Large Cap Value $34,030

Premium Equity (U.S. All-Cap Value) $13,930

Mid Cap Value $23,453

Small Cap, Small Cap II, Small-Mid Cap $5,066

U.S. Long/Short $7,880

Global, International, Concentrated International $8,801

Global Long/Short, International Long/Short $1,556

Emerging Markets Long/Short, Emerging Markets $209

Value equity expertise founded in the early 1980s*

Consistent and repeatable investment philosophy across all disciplines

Integrated bottom-up, fundamental and quantitative research

Expertise of a boutique with the depth of aglobal fi rm

Investment Profi le $96.7 Billion Assets Under Management

Boston Partners n 3

Boston PartnersRelative Performance through June 30, 2018

1 Inception dates are as follows: Large Cap Value is June 1, 1995; Premium Equity is June 1, 1995; Mid Cap Value is May 1, 1995; Small Cap Value Equity is July 1, 1995; Small Cap Value Equity II is July 1, 1998; Small/Mid Cap Value is April 1, 1999; Global Equity USA is July 1, 2008; International Equity is July 1, 2008; Long/Short Research is April 1, 2002 and Global Long/Short Equity is July 1, 2013.2 Net total return indices reinvest dividends after the deduction of withholding taxes, using (for international indices) a tax rate applicable to non-resident institutional investorswho do not benefi t from double taxation treaties.3 The Exposure-Adjusted S&P 500 Index is not an actual index. It is a supplemental benchmark created by multiplying the average monthly net exposure of the BP Long/Short Research by the actual S&P 500 Index return for the same period. Average Exposure is as follows: 1 Year at 50.33%; 3 Year at 48.75%; 5 Year at 49.03% 7 Year at 49.73%; 10 Year at 48.69%; and Since Inception at 43.96%.4 The Exposure-Adjusted MSCI World Index is not an actual index. It is a supplemental benchmark created by multiplying the average monthly net exposure of the BP Global Long/Short by the actual MSCI World Index return for the same period. Average Exposure is as follows: 1 Year at 49.73%; 3 Year at 46.02%; 5 Year at 45.61%; and Since Inception at 45.61%.Performance is supplemental to the GIPS® compliant presentation herein. Relative performance refl ects composite results versus noted benchmark and individual portfolio results will vary. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Relative Performance - Gross of Fees (%)

1Year

3Year

5Year

7Year

10Year

Since Inception1

Large Cap Value vs. Russell 1000® Value Index 3.58 0.67 0.74 1.23 2.13 1.55

Premium Equity vs. Russell 3000® Value Index 2.44 2.10 2.76 2.11 3.37 3.74

Mid Cap Value vs. Russell Midcap® Value Index 0.74 1.46 2.47 2.04 3.49 2.18

Small Cap Value Equity vs. Russell 2000® Value Index -3.42 -1.98 0.46 0.70 2.38 2.92

Small Cap Value Equity II vs. Russell 2000® Value Index -1.69 -0.86 1.19 1.63 2.87 4.13

Small/Mid Cap Value vs. Russell 2500™ Value Index -1.88 -0.14 1.03 1.19 1.85 1.26

Global Equity USA vs. MSCI World Index - Net2 -2.80 -0.80 1.17 1.74 2.09 2.09

International Equity vs. MSCI EAFE Index - Net2 -0.08 0.28 1.62 2.60 1.94 1.94

Long/Short Research vs. S&P 500 Index (Exposure Adjusted)3 -3.20 -1.09 0.81 1.60 3.31 4.47

Global Long/Short vs. MSCI World Index (Exposure Adjusted)4 -3.03 0.28 1.86 — — 1.86

Boston Partners n 4

Boston PartnersEquity Investment Team

Mark Donovan, CFALarge Cap Value Equity37 years experience

David Pyle, CFALarge Cap Value Equity23 years experience

Martin MacDonnell, CFA130/30 Large Cap Value27 years experience

Duilio Ramallo, CFAPremium Equity23 years experience

Steven Pollack, CFAMid Cap Value34 years experience

David Dabora, CFASmall/SMID Value31 years experience

George Gumpert, CFASmall/SMID Value19 years experience

Robert Jones, CFALong/Short Equity30 years experience

Christopher Hart, CFAGlobal, International, Global Long/Short27 years experience

Joshua Jones, CFAGlobal, International, Global Long/Short14 years experience

Paul Korngiebel, CFAEmerging Markets,Emerging Markets Long/Short18 years experience

Portfolio Management and Portfolio Research

Todd KnightlyDirector of Fundamental Research

Brian Boyden, CFAProperty REITs, Utilities

Scott Burgess, CFATechnology, Electronics

Lawrence Chan, CFAInternet Services, Payment Services, Recreational Products

Charles ClappGlobal Generalist

David Cohen, CFAEnergy, Engineering & Construction, Metals & Mining

Tim CollardAerospace & Defense, Transportation, Housing & Autos

Paul Donovan, CFAPaper & Packaging, Cable & Telecom, Gaming & Lodging, Chemicals

Kevin Duggan, CFABanks, Money Center

Trevor Frankel, CFAGlobal Generalist

Volkan Gulen, CFAConsumer Products, Business Services, Tobacco, Agriculture, Media & Advertising

Andrew Hatem, CFAHealthcare Therapeutics

David Hinton, CFASmall Cap Generalist

Tim HoranIndustrials & Manufacturing,Home & Offi ce Furnishings

Ross Klein, CFALong/Short Generalist

Stephanie McGirrHealth Care Services, Insurance, Restaurants, Retail

Edward Odre, CFAFinancial Services, Life Insurance

Patrick Regan, CFALong/Short Generalist

Joshua White, CFAGlobal Generalist

Bruce WimberlyLong/Short Generalist

Fundamental and Quantitative Research

Mark KuzminskasDirector of Equity Trading

Christopher BowkerSenior Equity Trader

Trading

Joseph Feeney, Jr., CFAChief Investment Offi cerLong/Short Research 33 years experience

John Forelli, CFADirector of Portfolio Research34 years experience

Carolyn Margiotti, CFAPortfolio Research24 years experience

Michael McCune, CFAPortfolio Research24 years experience

Brandon Smith, CFA, CAIAPortfolio Research12 years experience

Christopher EaganGlobal Markets Analyst33 years experience

Michael MullaneyDirector of Global Markets Research37 years experience

Eric Connerly, CFADirector of QuantitativeResearch

Jason Bartlett, CFAQuantitative Strategies

Pete CadyQuantitative Strategies

Leo FochtmanQuantitative Strategies

Rubina MoinQuantitative Strategies

Maggy Pietropaolo, CFAQuantitative Strategies

Joseph UrickQuantitative Strategies

Carissa Wong, CFAQuantitative Strategies

Thomas WalshSenior Equity Trader

Matthew EnderEquity Trader

Ian SylvetskyEquity Trader

Christopher SpazianiEquity Trading Assistant

Harry Rosenbluth, CFASenior Advisor 37 years experience

Boston Partners n 5

Boston PartnersPhilosophical Foundations: August 20, 1987

What works is what beats the market averages over reasonably long time periods: value works and "momentum" works.

Quantitative methods should be the primary tool to focus fundamental analysis effort.

Fundamental analysis works when it is fi rmly grounded in value and momentum thinking.

We all should be of one investment faith. Parties to the investment process who stray from the fl ock or commit acts of heresy should fi nd a new religion outside our church.

Fundamental Truths

This is an illustration of actual letter which illustrates the formation of Boston Partners' investment philosophy. The letter does not outline actual objectives or investment strategy and is not a guarantee of performance.

Boston Partners n 6

Boston PartnersValue Equity Investment Philosophy: Three Core Principles

Value Discipline anchored in Three "Fundamental Truths":

• Low valuation stocks outperform high valuation stocks

• Companies with strong fundamentals (high returns on invested capital) outperform companies with poor fundamentals

• Stocks with positive business momentum (improving trends/rising earnings)outperform stocks with negative momentum

"Characteristics-Based" Investment Approach:

• Valuation, fundamentals and momentum are analyzed using a bottom-upblend of qualitative and quantitative inputs

Preservation of Capital:

• Laws of compounding mathematically dictate that protecting capitalis the only risk that matters

• “Win by not losing": Keep pace in rising markets, outperform in fallingmarkets and diversify your exposure

Boston Partners n 7

Boston Partners"Three Circles" Stock Selection Criteria

We buy stocks that exhibit:

• Attractive value characteristics

and,

• Strong business fundamentals

and,

• Catalyst for change

We sell stocks based on:

• Valuation: Appreciation to price target

or

• Weakening business fundamentals

or

• Reversal of momentum

Portfolios with all three characteristics tend to outperform over time

BUSINESSFUNDAMENTALS

What are webuying?

VALUATIONHow much are

we paying?

BUSINESS MOMENTUMIs the business getting

better, staying the same,or getting worse?

Boston Partners n 8

Boston PartnersStock Selection Process

QuantitativeAnalysis Fundamental Analysis

Investment Universe

Validate Positive Characteristics

FactSet: Historical fi nancial statements, ratios, stock performance, earnings

revisions

Fundamental ResearchIdentify Catalyst

Determine Appropriate Valuation

Set Target Price

InvestmentDecision

• Statistical ranking based on composite score of three factors:

Valuation: Multiples of earnings, cash fl ow, book value

Momentum: Earnings surprise and estimate revisions

Fundamentals: Operating returns on operating assets (OROA)

• Target RichEnvironment

• Valuation: How much are we paying?

EV to Sales, Px to Earnings, EV to Cash fl ow, Px to Book, etc.

• Momentum: Is the business improvingor deteriorating?

Trend analysis: Profi t margins, asset turnover, working capital, debt structure

• Business Fundamentals:What are we buying?

Sales and earnings growth, profi tability, liquidity, capital structure, intangible assets, ROIC/OROA

• 10-Ks, 10-Qs, SEC fi lings

• Press releases, Conference call transcripts, Street events

• Management interviews

• On-site company visits

• Third-party research

• Internal models/projections

• Channel/supplier checks

• Construct portfolio

• Monitor existing holdings

• Evaluate company/industry developments

• Review/Adjust target prices

Boston Partners n 9

Boston Partners Large Cap Value EquityPortfolio Risk Controls

Portfolio risk controls can be customized to meet specific client guidelines.

Preserve Capital:

• Consistent execution of "Three Circles" investment process

- Emphasis on individual company risk

- Stocks are sold when any one of three characteristics are no longer present

- Portfolio characteristics managed using quantitative tools

• Broad diversification

• Liquidity of positions is actively monitored

Guideline Parameters:

• Account holdings in any one issuer shall not exceed the greater of the Benchmark weight plus 1 percentage point or 5% of the Account, measured at market value, in either case, determined at the time of purchase

• No individual economic sector (as defined for purposes of the Benchmark) shall represent more than the greater of the weight in such Benchmark or 35% of the Account determined at the time of purchase

- Non U.S. equity securities and ADRs will not comprise more than 15% of the market value of the portfolio, determined at the time of each purchase

• Cash will typically not represent more than 10% of the market value of the portfolio

We Do Not:

• Set tracking error limits: Tracking error is not always an accurate measure of active risk

• Remain sector neutral: If large parts of the market are unattractive, we will not invest there

Needs review: 1Q & 3Q

Boston Partners n 10

Boston PartnersDistinguishing Characteristics

Boston Partners Distinguishes Itself Through:

• An analytical advantage: in-house, bottom-up research employing an effective blend of quantitative and fundamental inputs

• A consistent and repeatable investment process guided by our fundamental truths: valuation, fundamentals, and business momentum

• The experience and familiarity of its investment team

• A risk averse approach: proven ability to protect clients’ investment principal in declining markets

Boston Partners n

i. Large Cap Value Portfolio

ii. Large Cap Value Investment Performance

iii. Concentrated Large Cap Value Equity Portfolio

iv. Supplemental Information

v. Biographical Information

vi. Investment Strategies Performance, Fee Schedules and Performance Disclosures

Boston Partners Large Cap Value EquityAppendix

"Three Circles"

An attractive valuation,strong businessfundamentals,and positive businessmomentum. Porfolios withall three characteristics tendto outperform over time.

Valuation

Business Momentum

Fundamentals

Portfolio R1000V SP500

13.2x 14.6xP/E (FY0)

P/E (FY1)

P/B

12.0x 13.5x

2.0x 2.1x

17.2x

15.6x

3.3x

Portfolio R1000V SP500

32.9% 27.6%OROA (5 Yr)

ROE (5 Yr)

LT EPS Gr. Rt.

12.7% 10.7%

15.4% 14.6%

38.5%

14.2%

15.6%

Portfolio

83%Percent of companieswith positive/neutralearnings momentum

Toyota Motor Sales USA RetirementPortfolio Characteristics: As of June 30, 2018

Please refer to the back for important disclosures.BP Large Cap Value Equity

FCF Yield* 3.1% 2.6% 2.5%

Boston Partners n 12

Boston Partners Large Cap Value EquityPortfolio Characteristics: June 30, 2018

* FCF Yield is reported as median excluding financials.Portfolio characteristics are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. Please refer to the last appendix for other important disclosures.

"Three Circles"

An attractive valuation, strong business fundamentals, and positive business momentum. Portfolios with all three characteristics tend to outperform over time.

BUSINESS

FUNDAMENTALS

BUSINESS MOMENTUM

VALUATION

Boston Partners n 13

Boston Partners Large Cap Value EquityLargest Active Positions: June 30, 2018

Source: Boston Partners Quantitative Research Group.Active weight is the absolute value of the portfolio's weight as compared to the Index's weight for a given stock. The stocks listed as not held reflect the largest holdings in the Russell 1000® Value Index not held by the portfolio. Portfolio holdings are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for advisory clients. It should not be assumed that investments in these sectors or securities were or will be profitable. This information is supplemental to the GIPS® compliant presentation herein. Please refer to the last appendix for other important disclosures.

StockLCV

% Portfolio

Russell 1000® Value Index

% BenchmarkActive Weight

Percentage

Citigroup Inc. 3.6 1.3 2.3

Bank of America Corporation 4.3 2.1 2.2

Royal Dutch Shell Plc 2.2 0.0 2.2

TE Connectivity Ltd. 1.8 0.0 1.8

Cisco Systems, Inc. 3.3 1.6 1.7

Andeavor Corporation 1.8 0.1 1.7

Johnson & Johnson 3.7 2.1 1.6

NetApp Inc. 1.5 0.0 1.5

Berkshire Hathaway Inc. 3.9 2.4 1.5

Wells Fargo & Company 3.2 1.9 1.3

Total 29.3% 11.5% 17.8%

What We Own What We Do Not Own

Russell 1000® Value Index

S&P 500 Index

Portfolio Active Share % Versus:

69% 77%

Stock

Russell 1000® Value Index

% Benchmark

Exxon Mobil Corporation 2.7

AT&T Inc. 1.8

Intel Corporation 1.8

The Procter & Gamble Company 1.5

DowDuPont Inc. 1.2

Philip Morris International Inc. 1.0

Wal-Mart Stores Inc. 0.9

General Electric Company 0.9

Medtronic, Inc. 0.9

Abbott Laboratories 0.8

Total 13.5%

Sector Weightings (% of Portfolio)Largest Holdings (%)

0.6

2.1

14.2

1.6

14.7

30.9

13.1

4.8

0.6

1.1

2.8

6.6

4.8

6.3

1.5

10.3

5.1

12.7

23.1

10.6

8.1

5.9

1.6

5.2

5.9

3.9

3.3

2.1

24.4

2.8

13.4

15.4

6.0

11.9

6.9

1.1

3.7

6.8

2.3

Utilities

Transportation

Technology

REITs

Health Care

Finance

Energy

Consumer Services

Consumer Non-Durables

Consumer Durables

Communications

Capital Goods

Basic Industries

Portfolio R1000V SP500

Bank of America Corp 4.3

Berkshire Hathaway Inc Cl B 3.9

JPMorgan Chase & Co 3.8

Johnson & Johnson 3.7

Citigroup Inc 3.6

Cisco Systems Inc 3.3

Wells Fargo & Co 3.2

Chevron Corp 2.9

Pfizer Inc 2.6

Royal Dutch Shell Plc 2.2

33.5Total

Number of Securities

SP500

82 505

Wtd. Avg. Mkt. Cap ($M) $133,449

2.0%

$198,898

Dividend Yield 2.2%

40.8%Turnover (Trailing 1 Year)

Portfolio

Portfolio Statistics

-

729

R1000V

$110,697

2.5%

-

Toyota Motor Sales USA RetirementPortfolio Characteristics: As of June 30, 2018

BP Large Cap Value EquityPlease refer to the back for important disclosures.

Sector Weightings (% of Portfolio)Largest Holdings (%)

0.6

2.1

14.2

1.6

14.7

30.9

13.1

4.8

0.6

1.1

2.8

6.6

4.8

6.3

1.5

10.3

5.1

12.7

23.1

10.6

8.1

5.9

1.6

5.2

5.9

3.9

3.3

2.1

24.4

2.8

13.4

15.4

6.0

11.9

6.9

1.1

3.7

6.8

2.3

Utilities

Transportation

Technology

REITs

Health Care

Finance

Energy

Consumer Services

Consumer Non-Durables

Consumer Durables

Communications

Capital Goods

Basic Industries

Portfolio R1000V SP500

Bank of America Corp 4.3

Berkshire Hathaway Inc Cl B 3.9

JPMorgan Chase & Co 3.8

Johnson & Johnson 3.7

Citigroup Inc 3.6

Cisco Systems Inc 3.3

Wells Fargo & Co 3.2

Chevron Corp 2.9

Pfizer Inc 2.6

Royal Dutch Shell Plc 2.2

33.5Total

Number of Securities

SP500

82 505

Wtd. Avg. Mkt. Cap ($M) $133,449

2.0%

$198,898

Dividend Yield 2.2%

40.8%Turnover (Trailing 1 Year)

Portfolio

Portfolio Statistics

-

729

R1000V

$110,697

2.5%

-

Toyota Motor Sales USA RetirementPortfolio Characteristics: As of June 30, 2018

BP Large Cap Value EquityPlease refer to the back for important disclosures.

Boston Partners n 14

Boston Partners Large Cap Value EquityPortfolio Characteristics: June 30, 2018

Portfolio characteristics and sector weightings are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for advisory clients. It should not be assumed that investments in these sectors or securities were or will be profitable. This information is supplemental to the GIPS® compliant presentation herein. Please refer to the last appendix for other important disclosures.

Weighted Average

Large Cap Value $133.4 B

Russell 1000® Value Index $110.7 B

S&P 500 Index $198.9 B

Market Capitalization

Sector Weightings (%)Largest Stock Holdings (%)

Rio Tinto Plc 0.5

⇑ FMC Corp 0.5

Barrick Gold Corp 0.4

Methanex Corp 0.8

Nutrien Ltd 0.6

Steel Dynamics Inc 1.1

WestRock Co 0.9

Celanese Corp 0.0∅

DowDuPont Inc 0.0∅

Basic Industries 4.8

Boeing Co 1.0

Dover Corp 0.5

Owens Corning 0.3

⇑ Cummins Inc 1.4

⇑ United Technologies Corp 1.8

CEMEX SAB de CV 0.5

CRH Plc 0.6

Raytheon Co 0.5

Arconic Inc 0.0∅

General Dynamics Corp 0.0∅

L3 Technologies Inc 0.0∅

Spirit AeroSystems Holdings Inc 0.0∅

Capital Goods 6.6

⇑ Comcast Corp Cl A 1.6

Verizon Communications Inc 1.2

Liberty Latin America Ltd 0.0∅

Communications 2.8

BorgWarner Inc⇓ 0.4

Fiat Chrysler Automobiles NV 0.6

Consumer Durables 1.1

Coca-Cola European Partners Plc 0.6

Consumer Non-Durables 0.6

Consumer Services 4.8

Consumer Services (cont...)

Lowe's Companies Inc 0.6

Wyndham Destinations Inc 0.5

Wyndham Hotels & Resorts Inc 0.5

Home Depot Inc⇓ 0.3

TJX Companies Inc⇓ 0.5

CVS Health Corp 1.6

eBay Inc 0.8

CBS Corp Cl B 0.0∅

Energy 13.1

Apergy Corp 0.3

Cimarex Energy Co 0.7

Marathon Oil Corp 0.8

⇑ ConocoPhillips 1.8

⇑ EQT Corp 0.8

Andeavor 1.8

Chevron Corp 2.9

Energen Corp 0.6

Marathon Petroleum Corp 1.2

Royal Dutch Shell Plc 2.2

Diamondback Energy Inc 0.0∅

Finance 30.9

⇑ Allstate Corporation 1.6

⇑ American International Group Inc 1.2

⇑ Wells Fargo & Co 3.2

XL Group Ltd⇓ 0.2

American Express Co 1.2

Bank of America Corp 4.3

Berkshire Hathaway Inc Cl B 3.9

Capital One Financial Corp 0.9

Chubb Ltd 1.1

Citigroup Inc 3.6

Discover Financial Services Inc 1.1

Everest Re Group Ltd 0.8

Finance (cont...)

Goldman Sachs Group Inc 1.3

JPMorgan Chase & Co 3.8

KeyCorp 0.7

Lloyds Banking Group Plc 0.5

Regions Financial Corp 1.2

TD Ameritrade Holding Corp 0.5

Synchrony Financial 0.0∅

Health Care 14.7

Novartis AG 0.7

⇑ McKesson Corp 0.9

Anthem Inc 1.1

Cigna Corp 1.0

Gilead Sciences Inc 1.2

Johnson & Johnson 3.7

Laboratory Corp of America Hldgs 1.1

Merck & Co Inc 1.9

Pfizer Inc 2.6

UnitedHealth Group Inc 0.6

Cardinal Health Inc 0.0∅

REITs 1.6

SL Green Realty Corp 0.9

⇑ Equity Residential 0.7

Technology 14.2

Booking Holdings Inc⇓ 0.3

ABB Ltd 0.4

Alphabet Inc 0.6

Avnet Inc 0.3

Cisco Systems Inc 3.3

DXC Technology Co 1.2

Eaton Corp Plc 0.8

HP Inc 1.2

Microsoft Corp 0.9

Technology (cont...)

NetApp Inc 1.5

Oracle Corp 1.9

TE Connectivity Ltd 1.8

Flex Ltd 0.0∅

Perspecta Inc 0.0∅

Transportation 2.1

Delta Air Lines Inc 1.2

Southwest Airlines Co 0.9

Utilities 0.6

⇑ Edison International 0.6

Account Summary: April 1, 2018 through June 30, 2018

Toyota Motor Sales USA Retirement

New HoldingKey: ⇓= |== |♦ Increased Position | Unchanged=∅⇑ LiquidatedDecreased Position |

BP Large Cap Value EquityPlease refer to the back for important disclosures.

Boston Partners n 15

Boston Partners Large Cap Value EquityPortfolio Holdings (Percent of Portfolio): April 1 through June 30, 2018

Security holdings as of June 30, 2018 are based upon a representative account in the composite and are subject to change. Values are percent of portfolio and are rounded to one decimal place. It should not be assumed that an investment in these securities was or will be profitable. This information is supplemental to the GIPS® compliant presentation herein.

Boston Partners n 16

Calendar Year Performance (%)

2009201220152016 2010201120142017 20082013

Large Cap Value - Gross of Fees 26.7521.27-4.0814.74 13.751.2911.8520.07 -32.9537.14

Large Cap Value - Net of Fees 26.3020.66-4.3714.40 13.360.8211.4919.71 -33.1736.64

Russell 1000® Value Index 19.6917.51-3.8317.34 15.510.3913.4513.66 -36.8532.53

S&P 500 Index 26.4616.001.3811.96 15.062.1113.6921.83 -37.0032.39

Annualized Performance (%)

3Year

7Year

5Year

10Year

SinceInception*

1Year

2Q2018

YTD2018

Large Cap Value - Gross of Fees 10.92-0.18 10.35 8.93 11.08 12.50 10.62-1.77

Large Cap Value - Net of Fees 10.54-0.26 10.01 8.60 10.73 12.10 10.22-1.92

Russell 1000® Value Index 9.371.18 6.77 8.26 10.34 11.27 8.49-1.69

S&P 500 Index 9.373.43 14.37 11.93 13.42 13.23 10.172.65

Boston Partners Large Cap Value EquityInvestment Performance through June 30, 2018

* Inception date is June 1, 1995.Boston Partners has prepared and presented this report in compliance with the GIPS®. Returns reflect composite results and individual portfolio results will vary. Past performance is not an indication of future results. Please refer to the appendix for other important disclosures.

Boston Partners n 17

Boston Partners Large Cap Value EquityPerformance Attribution: Second Quarter 2018

Large Cap Value 4.89 6.49 2.50 1.60 0.63 4.50 12.87 32.64 14.76 1.10 15.16 2.24 0.61 100.00%

Russell 1000® Value Index

2.98 6.14 3.35 1.51 5.78 7.20 11.19 26.39 13.28 4.90 9.71 1.39 6.18 100.00%

Relative Weight 1.91 0.36 -0.85 0.09 -5.15 -2.70 1.68 6.25 1.48 -3.79 5.45 0.85 -5.57

Large Cap Value 5.04 -10.39 0.84 -11.48 -1.67 3.02 13.15 -3.41 1.28 4.05 -0.09 -9.85 0.34 -0.10%

Russell 1000® Value Index

2.21 -2.86 -3.67 -1.38 -3.96 3.04 14.49 -3.51 2.47 8.35 -1.08 -0.50 4.94 1.18%

Sector Allocation 0.02 -0.04 0.03 0.02 0.27 -0.01 0.20 -0.29 0.00 -0.26 -0.09 -0.02 -0.19 -0.36%

Stock Selection 0.13 -0.54 0.11 -0.14 0.01 -0.05 -0.15 0.04 -0.18 -0.05 0.15 -0.22 -0.03 -0.92%

= -1.28%

Capit

al Goo

ds

Basic

Indu

stries

Commun

icatio

nsCo

nsum

er D

urab

lesCo

nsum

er N

on-D

urab

lesCo

nsum

er S

ervic

esEn

ergy

Finan

ce

Wei

ghtin

gsRe

turn

sCo

ntri

butio

n

Health

Car

eRE

ITs

Tech

nolog

y

Trans

porta

tion

Utilitie

s

Tota

l

Attribution is calculated using end of day security prices and returns shown are equity only and exclude cash. Results are from a representative account in the composite and are gross of fees. Individual portfolio results may vary. The information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners n 18

Boston Partners Large Cap Value EquityPerformance Attribution: Year to Date as of June 30, 2018

Large Cap Value 5.40 6.49 2.68 1.65 0.62 5.06 11.98 32.93 14.29 0.57 15.96 2.04 0.36 100.00%

Russell 1000® Value Index

2.95 6.26 3.33 1.53 6.00 7.44 10.76 26.70 13.33 4.72 9.50 1.38 6.10 100.00%

Relative Weight 2.45 0.23 -0.66 0.12 -5.38 -2.38 1.22 6.23 0.96 -4.15 6.46 0.66 -5.74

Large Cap Value 0.87 -12.46 -10.68 -13.02 3.66 -0.84 10.08 -4.08 -4.03 4.17 4.03 -15.11 1.06 -1.78%

Russell 1000® Value Index

-3.10 -8.26 -10.64 -10.74 -11.03 0.54 8.41 -4.68 0.47 0.38 4.75 -2.34 0.74 -1.69%

Sector Allocation -0.03 -0.05 0.05 0.00 0.53 0.00 0.19 -0.22 0.01 -0.04 0.54 0.00 -0.10 0.89%

Stock Selection 0.20 -0.35 -0.01 -0.04 0.09 -0.11 0.13 0.19 -0.62 -0.05 -0.11 -0.28 -0.03 -0.97%

= -0.09%

Capit

al Goo

ds

Basic

Indu

stries

Commun

icatio

nsCo

nsum

er D

urab

lesCo

nsum

er N

on-D

urab

lesCo

nsum

er S

ervic

esEn

ergy

Finan

ce

Wei

ghtin

gsRe

turn

sCo

ntri

butio

n

Health

Car

eRE

ITs

Tech

nolog

y

Trans

porta

tion

Utilitie

s

Tota

l

Attribution is calculated using end of day security prices and returns shown are equity only and exclude cash. Results are from a representative account in the composite and are gross of fees. Individual portfolio results may vary. The information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners n 19

Boston Partners Large Cap Value EquityPerformance Attribution: One Year as of June 30, 2018

Large Cap Value 5.80 6.23 2.18 1.39 0.67 6.12 10.49 32.05 15.42 0.28 17.11 1.88 0.38 100.00%

Russell 1000® Value Index

2.86 6.49 3.41 1.56 6.38 7.41 10.44 26.23 13.47 4.93 9.05 1.35 6.42 100.00%

Relative Weight 2.94 -0.26 -1.23 -0.17 -5.71 -1.29 0.05 5.82 1.95 -4.65 8.07 0.52 -6.04

Large Cap Value 16.62 -4.19 -8.53 5.55 2.80 3.36 35.70 10.15 1.25 4.17 21.21 -13.22 -4.88 10.60%

Russell 1000® Value Index

14.53 -8.33 -5.51 3.46 -9.69 9.02 24.15 8.49 2.68 1.92 21.30 5.16 3.81 6.77%

Sector Allocation 0.29 0.00 0.19 -0.03 0.97 -0.01 0.14 0.06 -0.15 0.33 1.16 -0.05 0.25 3.15%

Stock Selection 0.04 0.22 -0.10 0.03 0.08 -0.41 0.83 0.49 -0.02 -0.05 0.07 -0.42 -0.10 0.68%

= 3.83%

Capit

al Goo

ds

Basic

Indu

stries

Commun

icatio

nsCo

nsum

er D

urab

lesCo

nsum

er N

on-D

urab

lesCo

nsum

er S

ervic

esEn

ergy

Finan

ce

Wei

ghtin

gsRe

turn

sCo

ntri

butio

n

Health

Car

eRE

ITs

Tech

nolog

y

Trans

porta

tion

Utilitie

s

Tota

l

Attribution is calculated using end of day security prices and returns shown are equity only and exclude cash. Results are from a representative account in the composite and are gross of fees. Individual portfolio results may vary. The information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners n 20Boston Partners n 18

Boston Partners Large Cap Value EquityPerformance Attribution: Calendar Year 2017

Large Cap Value 6.54 5.41 1.63 1.54 0.70 7.06 9.66 29.24 16.38 0.00 19.33 1.95 0.56 100.00%

Russell 1000® Value Index 2.90 6.92 3.61 1.51 6.88 6.12 10.82 26.13 12.12 5.09 9.34 1.78 6.80 100.00%

Relative Weight 3.64 -1.51 -1.98 0.04 -6.18 0.95 -1.16 3.11 4.26 -5.09 9.99 0.18 -6.24

Large Cap Value 23.75 22.52 11.56 41.07 29.99 12.38 10.88 19.51 18.75 0.00 34.00 10.11 -8.08 20.50%

Russell 1000® Value Index 26.03 3.98 -2.49 21.55 11.26 15.09 -1.19 20.88 18.37 6.07 28.16 22.78 10.76 13.66%

Sector Allocation 0.37 0.08 0.47 -0.04 0.13 0.06 0.07 0.45 0.57 0.40 1.23 -0.05 0.18 3.91%

Stock Selection -0.12 0.99 0.22 0.35 0.14 -0.25 1.21 -0.32 0.09 0.00 1.14 -0.37 -0.14 2.94%

= 6.84%

Capit

al Goo

ds

Basic

Indu

stries

Commun

icatio

nsCo

nsum

er D

urab

lesCo

nsum

er N

on-D

urab

lesCo

nsum

er S

ervic

esEn

ergy

Finan

ce

Wei

ghtin

gsRe

turn

sCo

ntri

butio

n

Health

Car

eRE

ITs

Tech

nolog

y

Trans

porta

tion

Utilitie

s

Tota

l

Attribution is calculated using end of day security prices and returns shown are equity only and exclude cash. Results are from a representative account in the composite and are gross of fees. Individual portfolio results may vary. The information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners n 21

Boston Partners Large Cap Value EquityPerformance Attribution: June 1, 1995 through June 30, 2018

4.7

-7.6

-0.8

34.5

13.0

38.2

-4.0

5.9

23.5

4.9

15.9

39.2

1.4

18.9

10.5

10.6

3.6

7.9

19.4

6.4

6.1

-6.0

21.5

1.0

7.5

12.3

-20

0

20

40

60

Perc

ent

(%)

Security Selection Sector Allocation

168.

711

9.5

-150

-50

50

150

250

350

Sectors are sorted from largest (+) overweight sector to largest (—) underweight sector relative to benchmark. Overweights and underweights represent averages over entire attribution period. Attribution is calculated using end of day security prices and returns shown are equity only and exclude cash. Results are from a representative account in the composite and are gross of fees. Individual portfolio results may vary. The information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners Large Cap Value vs. Russell 1000® Value Index

Sector Allocation: 119.5% positive in 12 out of 13 sectorsSecurity Selection: 168.7% positive in 10 out of 13 sectorsTotal Value Added: 288.2% positive in 13 out of 13 sectors

Total 23.6 2.9 9.8 38.1 20.8 57.6 2.4 12.1 17.5 26.3 16.9 46.6 13.6 288.2

Boston Partners n 22

Boston Partners Large Cap Value EquityPerformance Traits throughout the Market's Cycles

61% 54%57%

Large Cap Value Equity Has Preserved Capital and Compounded Returns for Favorable 10-Year Performance

Data as of June 30, 2018 for 10-year period.Returns reflect composite results and individual portfolio results may vary. This information is supplemental to the GIPS® compliant presentation herein. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Percentage of the time that Large Cap Value Equity Composite has outperformed the Russell 1000® Value Index

• There have been 44 months in which the market has produced a negative return.

• Composite has outperformed the Index 61% of the time.

• There have been 76 months in which the market has produced a positive return.

• Composite has outperformed the Index 54% of the time.

• The entire period is 120 months.

• Composite has outperformed the Index 57% of the time.

"Down" Markets "Up" Markets Entire Period

Boston Partners n

Boston PartnersConcentrated Large Cap Value Equity

Boston Partners n 24Boston Partners n 11

Boston Partners Concentrated Large Cap Value EquityPortfolio Risk Controls

Portfolio risk controls can be customized to meet specifi c client guidelines.

Preserve Capital:

• Consistent execution of "Three Circles" investment process

- Emphasis on individual company risk

- Stocks are sold when any one of three characteristics are no longer present

- Portfolio characteristics managed using quantitative tools

• Broad diversifi cation

• Liquidity of positions is actively monitored

Guideline Parameters:

• No holding shall represent more than a 10% weight in the portfolio

• Positions will be initiated at 1% or greater

• No individual economic sector shall exceed 3x Index weight or 40% of the portfolio

• Non U.S. equity securities and ADRs will not comprise more than 20% of the total portfolio

• The portfolio will target 35-40 holdings

• Cash will not represent more than 10% of the total portfolio

We Do Not:

• Set tracking error limits: Tracking error is not always an accurate measure of active risk

• Remain sector neutral: If large parts of the market are unattractive, we will not invest there

Boston Partners n 25Boston Partners n 12

"Three Circles"

An attractive valuation,strong businessfundamentals,and positive businessmomentum. Porfolios withall three characteristics tendto outperform over time.

Valuation

Business Momentum

Fundamentals

Portfolio R1000V

13.2x 14.6xP/E (FY0)

P/E (FY1)

P/B

12.0x 13.5x

1.9x 2.1x

Portfolio R1000V

27.4% 27.6%OROA (5 Yr)

ROE (5 Yr)

LT EPS Gr. Rt.

13.5% 10.7%

16.8% 14.6%

Portfolio

84%Percent of companieswith positive/neutralearnings momentum

Boston Partners Concentrated Large Cap ValuePortfolio Characteristics: As of June 30, 2018

Please refer to the back for important disclosures.BP Concentrated Large Cap Value

FCF Yield* 2.9% 2.6%

Boston Partners Concentrated Large Cap Value EquityPortfolio Characteristics: June 30, 2018

* FCF Yield is reported as median excluding fi nancials.Portfolio characteristics are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. Please refer to the last appendix for other important disclosures.

"Three Circles"

An attractive valuation, strong business fundamentals, and positive business momentum. Portfolios with all three characteristics tend to outperform over time.

BUSINESS

FUNDAMENTALS

BUSINESS MOMENTUM

VALUATION

Boston Partners n 26Boston Partners n 13

Sector Weightings (% of Portfolio)Largest Holdings (%)

0.0

3.8

16.1

0.0

12.9

32.7

16.0

1.5

0.0

0.0

4.2

8.8

2.5

6.3

1.5

10.3

5.1

12.7

23.1

10.6

8.1

5.9

1.6

5.2

5.9

3.9

Utilities

Transportation

Technology

REITs

Health Care

Finance

Energy

Consumer Services

Consumer Non-Durables

Consumer Durables

Communications

Capital Goods

Basic Industries

Portfolio R1000V

Bank of America Corp 6.6

Berkshire Hathaway Inc Cl B 5.4

JPMorgan Chase & Co 5.4

Johnson & Johnson 4.9

Citigroup Inc 4.2

Cisco Systems Inc 4.2

Anthem Inc 3.8

Chevron Corp 3.3

Royal Dutch Shell Plc 3.2

Andeavor 3.1

44.1Total

Number of Securities

R1000V

38 729

Wtd. Avg. Mkt. Cap ($M) $154,645

2.5%

$110,697

Dividend Yield 2.0%

41.3%Turnover (Trailing 1 Year)

Portfolio

Portfolio Statistics

-

Boston Partners Concentrated Large Cap ValuePortfolio Characteristics: As of June 30, 2018

BP Concentrated Large Cap ValuePlease refer to the back for important disclosures.

Sector Weightings (% of Portfolio)Largest Holdings (%)

0.0

3.8

16.1

0.0

12.9

32.7

16.0

1.5

0.0

0.0

4.2

8.8

2.5

6.3

1.5

10.3

5.1

12.7

23.1

10.6

8.1

5.9

1.6

5.2

5.9

3.9

Utilities

Transportation

Technology

REITs

Health Care

Finance

Energy

Consumer Services

Consumer Non-Durables

Consumer Durables

Communications

Capital Goods

Basic Industries

Portfolio R1000V

Bank of America Corp 6.6

Berkshire Hathaway Inc Cl B 5.4

JPMorgan Chase & Co 5.4

Johnson & Johnson 4.9

Citigroup Inc 4.2

Cisco Systems Inc 4.2

Anthem Inc 3.8

Chevron Corp 3.3

Royal Dutch Shell Plc 3.2

Andeavor 3.1

44.1Total

Number of Securities

R1000V

38 729

Wtd. Avg. Mkt. Cap ($M) $154,645

2.5%

$110,697

Dividend Yield 2.0%

41.3%Turnover (Trailing 1 Year)

Portfolio

Portfolio Statistics

-

Boston Partners Concentrated Large Cap ValuePortfolio Characteristics: As of June 30, 2018

BP Concentrated Large Cap ValuePlease refer to the back for important disclosures.

Boston Partners Concentrated Large Cap Value EquityPortfolio Characteristics: June 30, 2018

Portfolio characteristics and sector weightings are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. The specifi c securities identifi ed and described do not represent all of the securities purchased, sold or recommended for advisory clients. It should not be assumed that investments in these sectors or securities were or will be profi table. This information is supplemental to the GIPS® compliant presentation herein. Please refer to the last appendix for other important disclosures.

Weighted Average

Concentrated Large Cap Value Equity $154.6 B

Russell 1000® Value Index $110.7 B

Market Capitalization

Sector Weightings (%)Largest Stock Holdings (%)

Boston Partners n 27Boston Partners n 14

Steel Dynamics Inc⇓ 1.2

WestRock Co 1.3

Celanese Corp 0.0∅

Basic Industries 2.5

Boeing Co 2.4

CRH Plc 1.3

Owens Corning 1.0

⇑ Cummins Inc 2.3

United Technologies Corp 2.0

Raytheon Co 0.0∅

Capital Goods 8.8

⇑ Comcast Corp Cl A 2.6

Verizon Communications Inc 1.6

Communications 4.2

eBay Inc 1.5

Consumer Services 1.5

ConocoPhillips 2.6

⇑ EQT Corp 2.1

⇑ Royal Dutch Shell Plc 3.2

Andeavor 3.1

Chevron Corp 3.3

Marathon Petroleum Corp 1.9

Diamondback Energy Inc 0.0∅

Energy 16.0

Allstate Corporation 2.7

⇑ American International Group Inc 2.7

⇑ Chubb Ltd 1.9

⇑ Discover Financial Services Inc 2.2

⇑ Goldman Sachs Group Inc 1.6

Bank of America Corp⇓ 6.6

Citigroup Inc⇓ 4.2

JPMorgan Chase & Co⇓ 5.4

Finance 32.7

Finance (cont...)

Berkshire Hathaway Inc Cl B 5.4

Health Care 12.9

⇑ Anthem Inc 3.8

Cigna Corp 2.1

Gilead Sciences Inc 2.1

Johnson & Johnson 4.9

Merck & Co Inc 0.0∅

Technology 16.1

⇑ DXC Technology Co 2.5

Alphabet Inc⇓ 1.6

Booking Holdings Inc⇓ 1.2

Microsoft Corp⇓ 2.2

Cisco Systems Inc 4.2

Eaton Corp Plc 1.7

TE Connectivity Ltd 2.6

Oracle Corp 0.0∅

Perspecta Inc 0.0∅

Transportation 3.8

Delta Air Lines Inc 2.2

Southwest Airlines Co 1.6

Account Summary: April 1, 2018 through June 30, 2018

Boston Partners Concentrated Large Cap Value

New HoldingKey: ⇓= |== |♦ Increased Position | Unchanged=∅⇑ LiquidatedDecreased Position |

BP Concentrated Large Cap ValuePlease refer to the back for important disclosures.

Boston Partners Concentrated Large Cap Value EquityPortfolio Holdings (Percent of Portfolio): April 1 through June 30, 2018

Security holdings as of June 30, 2018 are based upon a representative account in the composite and are subject to change. Values are percent of portfolio and are rounded to one decimal place. It should not be assumed that an investment in these securities was or will be profi table. This information is supplemental to the GIPS® compliant presentation herein.

Boston Partners n 28Boston Partners n 16

Boston Partners Concentrated Large Cap Value EquityInvestment Performance through June 30, 2018

* Inception date is July 1, 2017.Boston Partners has prepared and presented this report in compliance with the GIPS®. Returns refl ect composite results and individual portfolio results will vary. Past performance is not an indication of future results. Please refer to the appendix for other important disclosures.

Annualized Performance (%)

2Q2018

YTD2018

Since Inception*

Concentrated Large Cap Value - Gross of Fees -1.22 -2.23 11.17

Concentrated Large Cap Value - Net of Fees -1.39 -2.57 10.41

Russell 1000® Value Index 1.18 -1.69 6.77

Boston Partners n 29Boston Partners n 1

Boston Partners Market ObservationsAs of June 30, 2018

The U.S. Equity markets refers to the S&P 500 Index.Discussions of securities returns and trends are not intended to be a forecast of future events or returns. The specifi c securities identifi ed and described do not represent all of the securities purchased, sold or recommended for advisory clients. It should not be assumed that investments in these sectors or securities were or will be profi table. Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

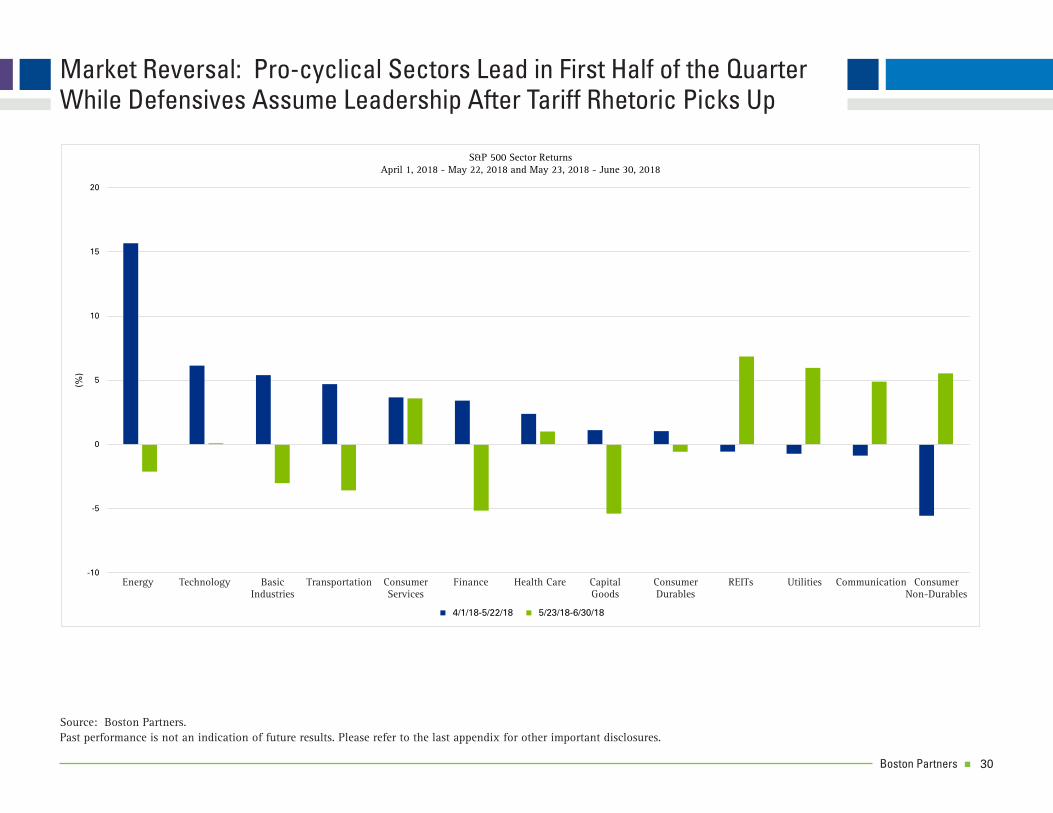

• The U.S Equity markets experienced a sharp reversal during the quarter as pro-cyclical sectors continued their leadership in the fi rst half of the quarter while defensives led in the second half

- REITs, Utilities and Communications assumed leadership from late May onwards after negative returns in the fi rst part of the quarter

- Capital Goods, Finance and Basic Industries lagged in last part of the quarter

• Investors are losing confi dence in future economic growth despite very strong current data due to:

- Trade War concerns

- Flattening yield curve and potential for the Fed tightening too much

- “Peak” economic conditions and accelerating infl ation

- Mid-term elections and European political issues

• We continue to see accelerating economic growth in the U.S. and most regions abroad

- U.S. Economic activity remains very strong

- Current wage infl ation and yield curve are far away from historical recession signals

- Benefi ts from tax reform far outweigh the potential drag from increased tariffs

- S&P 500 earnings growth expected to exceed 20% this year

• Value equity valuations have returned to “a good deal” as earnings have accelerated and value returns have stagnated year to date

- Russell 3000® Value Index trades at a reasonable 14.6x expected 2018 earnings compared to 21.4x for the Russell 3000® Growth Index

- U.S. equity market continues to be more attractive than U.S. fi xed income market

Boston Partners n 30Boston Partners n 2

Market Reversal: Pro-cyclical Sectors Lead in First Half of the Quarter While Defensives Assume Leadership After Tariff Rhetoric Picks Up

Source: Boston Partners.Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

-10

-5

0

5

10

15

20

Energy Technology Basic Industries Transportation ConsumerServices

Finance Health Care Capital Goods ConsumerDurables

REITs Utilities Communications Consumer Non-Durables

(%)

S&P 500 Sector Returns April 1, 2018 - May 22, 2018 and May 23, 2018 - June 30, 2018

4/1/18-5/22/18 5/23/18-6/30/18

Energy Technology Basic Transportation Consumer Finance Health Care Capital Consumer REITs Utilities Communication Consumer Industries Services Goods Durables Non-Durables

Boston Partners n 31Boston Partners n 9

0

-5

-4

-3

-2

-1

0

1

2

3

4

CFN

AI T

hree

Mon

th M

ovin

g A

vera

ge

Federal Reserve National Activity Index

Federal Reserve National Activity Index

Updated on 7/16/2018 from website

1967 through May 31, 2017.Source: FRB Chicago.Past performance is not an indication of future results.

The Chicago Fed National Activity Index (CFNAI) is a 3 month moving average index designed to gauge overall economic activity and infl ationary pressure. It is a weighted average of 85 indicators of economic activity, measuring production & income, employment, consumption/housing, and sales/inventories. Values above +0.70 indicate above trend growth and infl ationary pressures. Values below -0.70 indicate a recession has begun.

Boston Partners n 32Boston Partners n 4

ISM Purchasing Manager Indices Remain Firmly in Expansion TerritoryAs of June 30, 2018

Source: Institute of Supply Management.Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

ISM Purchasing Manager Indices Remain Firmly in Expansion Territory

Source: Institute of Supply Management

Boston Partners Past performance is not an indication of future results. Please refer to the appendix for other important disclosures.

Boston Partners n 33Boston Partners n 5

Current Wage Infl ation and Yield Curve are Far Away from Historical Recession Signals

Source: Strategas. Data as of June 30, 2018.Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

-300

-200

-100

0

100

200

3001

2

3

4

5

6

7

8

9

10

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Average Hourly Earnings: Production and Nonsupervisory Workers (Y/Y, SA, $/Hour)

vs. 10/2 Spread (bps, 12 Mo Lead)

Yield Curve Inverted ,

Average Hourly Earnings,

Boston Partners n 34Boston Partners n 6

U.S. Nominal Goods Trade Balance with China

Source: Bureau of Economic Analysis (U.S. Department of Commerce). Data as of December 31, 2017. Please refer to the last appendix for other important disclosures.

-$397.6

-$450.0

-$400.0

-$350.0

-$300.0

-$250.0

-$200.0

-$150.0

-$100.0

-$50.0

$0.0

3-Month Avg. Annual Rate ($USD billions)

China joins WTO

Boston Partners n 35Boston Partners n 7

Fiscal Stimulus Dwarfs Estimated Tariff Repercussions

-300

-200

-100

0

100

200

3001

2

3

4

5

6

7

8

9

10

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Average Hourly Earnings: Production and Nonsupervisory Workers (Y/Y, SA, $/Hour)

vs. 10/2 Spread (bps, 12 Mo Lead)

Yield Curve Inverted ,

Average Hourly Earnings,

Source: Strategas.Past performance is not an indication of future results. Please refer to the last appendix for other important disclosures.

Boston Partners n 36Boston Partners n 4

Percentile Distribution of S&P Trailing Twelve Month Earnings Multiples, 1957 to Present

Percentile 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

LTM P/E 9.7 12.1 14.4 16.4 17.0 17.7 18.2 20.2 22.1 29.7

$165 1,601 1,997 2,376 2,706 2,805 2,921 3,003 3,333 3,647 4,901

$161 1,562 1,948 2,318 2,640 2,737 2,850 2,930 3,252 3,558 4,782

$159 1,542 1,924 2,290 2,608 2,703 2,814 2,894 3,212 3,514 4,722

$155 1,504 1,876 2,232 2,542 2,635 2,744 2,821 3,131 3,426 4,604

$151 1,465 1,827 2,174 2,476 2,567 2,673 2,748 3,050 3,337 4,485

$147 1,426 1,779 2,117 2,411 2,499 2,602 2,675 2,969 3,249 4,366

$144 1,397 1,742 2,074 2,362 2,448 2,549 2,621 2,909 3,182 4,277

$141 1,368 1,706 2,030 2,312 2,397 2,496 2,566 2,848 3,116 4,188

$137 1,329 1,658 1,973 2,247 2,329 2,425 2,493 2,767 3,028 4,069

$133 1,290 1,609 1,915 2,181 2,261 2,354 2,421 2,687 2,939 3,950

Percentile Distribution of 10 Year U.S. Treasury Bond Yield, 1957 to Present

Percentile 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

10 Yr. Yield 9.8% 8.1% 7.3% 6.5% 5.7% 4.8% 4.2% 3.9% 2.8% 1.4%

S&P 500 Fair ValueTargets Based on Trailing Twelve Month Historical Earnings Multiples

P/E multiples are based on S&P 500 trailing 12-month operating EPS estimates from 1957 to present. Source: The Leuthold Group.Data as of June 30, 2018. S&P 500 earnings estimates according to Factset.Please refer to the appendix for other important disclosures.

S&P

500

Earn

ings

Per

Sha

re

YE 2017 A

YE 2018 E

6/30/2018 E

Boston Partners n 37Boston Partners n 9

Value has Outperformed Growth by a Wide Margin Since 1979Growth of $1.00

Source: Boston Partners. Data as of June 30, 2018.Past performance in not an indication of future results. Please refer to the last appendix for other important disclosures.

Russell 1000® Value Index 12.01%

Russell 1000® Growth Index 11.44%

Annualized Return since January 1979

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Russell 1000® Value Index

Russell 1000® Growth Index$88.48

$72.19

Boston Partners n 38Boston Partners n 4

The Case for Active ManagementBoston Partners Large Cap Value Equity

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Boston Partners LCV Net of Fees as of 6/30/2018

Russell 1000® Value Index as of 6/30/2018

S&P 500 Index as of 6/30/2018

Cumulative Growth of a $10 Million Investment June 1, 1995 to June 30, 2018 (Net of Fees)

$79.1 million

$101.1 million

$79.1 million

This is a hypothetical illustration of $10 million had it been invested in the Boston Partners Large Cap Value strategy since inception on June 1, 1995. The results of this illustration may be changed depending on investment guidelines and cash fl ow. This illustration is net of investment management fees. A GIPS® compliant presentation is contained herein. Past performance is not an indication of future results. Please refer to the appendix for other important disclosures.

Boston Partners n 39Boston Partners n 2Boston Partners n 2

Boston Partners U.S. All Cap Stock Selection ModelRolling 12-Month Top Ranking less Worst Ranking Stock Performance

-40%

-20%

0%

20%

40%

60%

80%

Jul-9

4

Feb-

95

Sep-

95

Apr-9

6

Nov-

96

Jun-

97

Jan-

98

Aug-

98

Mar

-99

Oct-9

9

May

-00

Dec-

00

Jul-0

1

Feb-

02

Sep-

02

Apr-0

3

Nov-

03

Jun-

04

Jan-

05

Aug-

05

Mar

-06

Oct-0

6

May

-07

Dec-

07

Jul-0

8

Feb-

09

Sep-

09

Apr-1

0

Nov-

10

Jun-

11

Jan-

12

Aug-

12

Mar

-13

Oct-1

3

May

-14

Dec-

14

Jul-1

5

Feb-

16

Sep-

16

Apr-1

7

Nov-

17

Jun-

18

ROLL

ING

12 M

ONTH

PERF

ORM

ANCE

Boston Partners US All-Cap Stock Selection ModelRolling 12 Month Performance of Buy-Rated less Sell-Rated Stocks

July 1993 through June 2018

Despite the positive long-term performance, there have been interim periods when the "Sell" candidates outperform the "Buy" candidates.l

Internet & Telecom Bubble

Accounting Scandals: Enron, Worldcom, HealthSouth, Tyco, Freddie Mac Low Volatility/Dividend Bubble

and Top-Line Growth at any Price

The chart above illustrates the monthly rolling 12-month performance spread which is calculated by subtracting the equal-weighted performance of the worst-ranked stocks (deciles 8-10) from the equal-weighted performance of the best-ranked stocks (deciles 1-3) as ranked by the Boston Partners Quantitative Equity Team. The investment universe – all U.S. traded stocks with a market capitalization greater than $200 million – is deciled based on quality, valuation, and business momentum factors and rebalanced monthly. While we have been utilizing a derivation of this model since the fi rm’s inception in 1995, signifi cant model revisions went into effect on December 31, 2012. Performance prior to that date is hypothetical back-test returns, while data displayed beyond this date is not back-tested, but is still generated by the model. All data shown above does not represent the results of actual trading, and in fact, actual results could differ substantially, and there is the potential for loss as well as profi t. The performance does not refl ect management fees, transaction costs, and other fees and expenses a client would have to pay, which reduce returns. Past performance is not an indication of future results.

Annualized as of June 30, 2018 2Q 2018 YTD 2018 1 year 3 year 5 year 10 year

Difference between Best- and Worst-Ranked Stocks -4.9% -3.1% 0.9% 6.4% 7.5% 9.1%

Best-Ranked Stocks and Worst-Ranked Stocks

July 1993 through June 30, 2018

Boston Partners n 40

Boston Partners Large Cap Value EquityActive Share (Annual): June 30, 2018

• Active share measures the percentage of portfolio holdings that differ from a portfolio’s benchmark index.

• Active share can range between 0% (for a passive index fund) to 100%.

• Active share helps to predict performance.

• There is compelling evidence that high active share portfolios outperform their benchmark index while portfolios with low active share underperform.

0

10

20

30

40

50

60

70

80

90

100

1995* 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD2018

Act

ive

Shar

e (%

)

We actively manage portfolio construction to take full advantage of the investment universe

* Inception is June 1, 1995.Portfolio characteristics are based upon a representative account in the composite and are subject to change. Individual portfolio characteristics may vary. Please refer to the last appendix for other important disclosures.Source: “How Active Is Your Fund Manager? A New Measure That Predicts Performance,” Cramers and Petajisto, Yale School of Management, January 2007.

Boston Partners n 41Boston Partners n

Boston PartnersDefi ned Contribution Plans - Over $6.3 Billion in AUM and More Than 68 Clients*

Vehicles available for value strategies:

• Separate Account

• Collective Trust

• Mutual Fund

Advantages of a Collective Trust Vehicle:

• Daily net asset values (NAVs) from the National Securities Clearing Corp. (NSCC)

• Daily liquidity

• Competitive fees with low operating expenses

- Inclusive of custody and other administrative costs

• Ease of administration

- Experience with a variety of record keepers

- Automated daily NAV feeds available

• Participant education and communication

- Quarterly fact sheet designed specifi cally for DC plan participants

- Customized reporting also available

* As of June 30, 2018. Includes separate account and collective trust defi ned contribution clients. Mutual fund assets are not included.Boston Partners Trust Company is a New Hampshire nondepository trust company pursuant to NH RSA 392 of the Banking Laws of NH and exempt from the defi nition of security under the Securities Act of 1933, Section 3a(2).

J:\Marketing\_Book Production\_VIP\DC Capabilities\2018\033118 DC Capabilities.indd

Boston Partners n 42

Boston PartnersBiographical Information

ExecutivesMark E. Donovan, CFAMr. Donovan is Co-Chief Executive Offi cer of Boston Partners and lead portfolio manager for BP Large Cap Value portfolios. He is responsible for strategic and tactical operating decisions affecting the fi rm. He was one of the founding partners of Boston Partners Asset Management in 1995. He joined the fi rm from The Boston Company where he was Senior Vice President and equity portfolio manager. He also spent fi ve years as a consulting associate with Kaplan, Smith & Associates, and two years as a securities analyst for Value Line Inc. Mr. Donovan holds a B.S. degree in management from Rensselaer Polytechnic Institute. He holds the Chartered Financial Analyst® designation. He has thirty-seven years of investment experience.

Joseph F. Feeney, Jr., CFAMr. Feeney is Co-Chief Executive Offi cer and Chief Investment Offi cer for Boston Partners. He is responsible for the fi rm’s strategic, fi nancial and operating decisions, and all aspects of investment management including the fi rm’s fundamental and quantitative research groups. He was one of the original partners of Boston Partners Asset Management in 1995. Prior to assuming these roles, he was director of research. Mr. Feeney joined the fi rm upon its inception in 1995 from Putnam Investments where he managed mortgage-backed securities portfolios. He began his career at the Bank of Boston where he was a loan offi cer specializing on highly leveraged loan portfolios. Mr. Feeney holds a B.S. degree in fi nance (Summa Cum Laude, Phi Beta Kappa) from the University of New Hampshire and an M.B.A. with High Honors from the University of Chicago. He holds the Chartered Financial Analyst® designation and is past President of

the Fixed Income Management Society of Boston. He has thirty-three years of investment experience.

Portfolio ManagementDavid M. Dabora, CFAMr. Dabora is a senior portfolio manager for Boston Partners Small Cap Value, Small Cap Value II, and Small/Mid Cap Value portfolios as well as the Alpha Blue Capital L.P. product. Prior to managing Boston Partners small cap value portfolios, he was an assistant portfolio manager for Boston Partners Premium Equity product. Additionally, he was a research analyst with responsibility for a wide variety of industries. He was one of the original partners of Boston Partners Asset Management in 1995. He joined the fi rm from The Boston Company Asset Management, Inc. where he was an equity analyst in their Los Angeles and Greenbrae, California offi ces. Mr. Dabora holds a B.S. degree in business administration from Pennsylvania State University and an M.B.A. degree from The Anderson School of Management at the University of California at Los Angeles. He holds the Chartered Financial Analyst® designation. He has thirty-one years of investment experience.

George Gumpert, CFAMr. Gumpert is a portfolio manager for Boston Partners Small Cap Value, Small Cap Value II, and Small/Mid Cap Value portfolios. Prior to managing Boston Partners small cap value portfolios, he was a research analyst and specialized in the small capitalization sectors of the equity market. Mr. Gumpert holds a B.A. degree in economics from Amherst College. He holds the Chartered Financial Analyst® designation. He has nineteen years of investment experience.

Christopher K. Hart, CFAMr. Hart is a senior portfolio manager for Boston Partners Global Equity and International Equity products. Prior to this, he was the portfolio manager for the Boston Partners International Small Cap Value product and before that, an assistant portfolio manager for the Boston Partners Small Cap Value products for three years. Previously, he was a research analyst and specialized in conglomerates, engineering and construction, building, machinery, aerospace & defense, and REITs sectors of the equity market. He joined the fi rm from Fidelity Investments where he was a research analyst. Mr. Hart holds a B.S. degree in fi nance, with a concentration in corporate fi nance from Clemson University. He holds the Chartered Financial Analyst® designation. He has twenty-seven years of investment experience.

Joshua Jones, CFAMr. Jones is a portfolio manager on Boston Partners Global and International products. Prior to this role, he was a research analyst specializing in the energy, metals and mining sectors of the equity market and was a global generalist. He joined the fi rm from Cambridge Associates where he was a consulting associate specializing in hedge fund clients. Mr. Jones holds a B.A. degree in economics from Bowdoin College. He holds the Chartered Financial Analyst® designation. He has fourteen years of investment experience.

Robert T. Jones, CFAMr. Jones is a senior portfolio manager for Boston Partners Long/Short Equity product. Previously, he was the Director of Research and portfolio manager for the Large Cap Value and Large Cap Value Focused products. He was a founding Partner of Boston Partners Asset Management. He joined the fi rm from The Boston Company Asset Management, Inc. where he spent seven

Boston Partners n 43

years as Vice President and equity portfolio manager. Mr. Jones holds a B.A. degree in philosophy from Denison University. He holds the Chartered Financial Analyst® designation. He has thirty years of investment experience.

Paul Korngiebel, CFAMr. Korngiebel is the lead portfolio manager on all Boston Partners Emerging Markets strategies, including Boston Partners Emerging Markets Equity and Emerging Markets Long/Short Equity. He also serves as a supporting member of the greater Global Equity team, providing input on idea generation for various international and global portfolios. Mr. Korngiebel joined the fi rm from Deccan Value Advisors, which he co-founded, and prior to that he worked at Brandes Investment Partners. Both fi rms are dedicated to global value investing. Mr. Korngiebel holds a B.A. from Bowdoin (Phi Beta Kappa), M.A. degrees from Harvard and St. Johns College, and an M.B.A. degree from Northwestern (Beta Gamma Sigma). He holds the Chartered Financial Analyst® designation and has eighteen years of investment experience.

Martin P. MacDonnell, CFAMr. MacDonnell is a portfolio manager for Boston Partners 130/30 Large Cap Value product as well as a research analyst specializing in quantitative strategies. He joined the fi rm from ITS Associates, Inc., where he managed the installation of investment software systems. Prior to that, he spent three years at The Boston Company in the investors services group, as a senior performance consultant. Mr. MacDonnell holds a B.A. degree in economics from Fairfi eld University. He holds the Chartered Financial Analyst® designation. He has twenty-seven years of investment experience.

Steven L. Pollack, CFAMr. Pollack is the equity portfolio manager for Boston Partners Mid Cap Value Equity product. He is in his fi fteenth year with the fi rm. He joined the fi rm from Hughes Investments where he spent twelve years as an equity portfolio manager, managing value equity across the market capitalization spectrum. He also oversaw the outside investment managers who manage assets for Hughes’ pension plan. He began his career at Hughes as an Investment Analyst where he spent four years covering a variety of industries and sectors. Prior to that, he was with Remington, Inc., and Arthur Anderson & Co. Mr. Pollack is a graduate from Georgia Institute of Technology and holds an M.B.A. from The Anderson School of Management at the University of California at Los Angeles. He holds the Chartered Financial Analyst® designation. He has thirty-four years of investment experience.

David J. Pyle, CFAMr. Pyle is a portfolio manager for Boston Partners Large Cap Value portfolios. Prior to assuming this role, he was a research analyst covering the utility, insurance, leisure & lodging, packaging, publishing, and computer equipment & services sectors. Mr. Pyle joined the fi rm from State Street Research where he was a research analyst and associate portfolio manager in their equity value group. Prior to that, he spent fi ve years with Price Waterhouse. Mr. Pyle holds a B.S. degree in business administration from California State University, Chico, and an M.B.A. degree from the Kenan-Flagler School of Business at the University of North Carolina. Mr. Pyle holds the Chartered Financial Analyst® designation. He has twenty-three years of investment experience.

Duilio R. Ramallo, CFAMr. Ramallo is the senior portfolio manager for Boston Partners Premium Equity product. Previously, Mr. Ramallo was the assistant portfolio manager for the Small Cap Value products. Prior to his portfolio management role, Mr. Ramallo was a research analyst for Boston Partners. He joined the fi rm from Deloitte & Touche L.L.P., where he spent three years, most recently in their Los Angeles offi ce. Mr. Ramallo holds a B.A. degree in economics/business from the University of California at Los Angeles and an M.B.A. from the Anderson Graduate School of Management at UCLA. He holds the Chartered Financial Analyst® designation. He is also a Certifi ed Public Accountant (inactive). He has twenty-three years of investment experience.

Harry J. Rosenbluth, CFAMr. Rosenbluth is a senior advisor for Boston Partners Global Equity and International Equity products. Prior to this, he was the portfolio manager for Boston Partners Premium Equity Product and co-manager for our Mid Cap Value Equity product. He was one of the founding partners of Boston Partners Asset Management in 1995. Mr. Rosenbluth joined the fi rm following fourteen years with The Boston Company Asset Management, Inc. as Senior Vice President and the portfolio manager for the Dynamic Equity Fund. Mr. Rosenbluth was also a member of the Equity Policy Group of The Boston Company Asset Management, Inc. Before that, Mr. Rosenbluth was a consultant for Arthur Andersen & Company. Mr. Rosenbluth holds a B.A. degree in Economics from George Washington University and an M.B.A. from The Amos Tuck School of Business Administration at Dartmouth College. He holds the Chartered Financial Analyst® designation. He has thirty-seven years of investment experience.

Boston PartnersBiographical Information (continued)

Boston Partners n 44

Portfolio ResearchJohn C. Forelli, CFAMr. Forelli is the Director of Portfolio Research for Boston Partners. In this position, he directs our team of investment professionals in formulating, developing, and communicating the investment narrative for Boston Partners. Prior to this role, he was a senior portfolio analyst and has extensive experience with all of the fi rm’s strategies. Mr. Forelli has 12 years of experience as a portfolio manager focused on large cap equities. He joined the fi rm from Independence Investments where he was large cap core portfolio manager, senior partner and member of the investment committee. Mr. Forelli was also a research analyst specializing in health care, chemical, capital goods and industrial companies. He began his career as an investment banker with Prudential Securities focusing on raising capital for emerging growth companies and merger and acquisition transactions. Mr. Forelli holds a B.A. degree in economics from Dartmouth College and an M.B.A. degree from the Tuck School of Business at Dartmouth College. He holds the Chartered Financial Analyst® designation and FINRA licenses 7 and 66. He has thirty-four years of industry experience.

Carolyn Margiotti, CFAMs. Margiotti is a senior portfolio analyst for Boston Partners and has extensive experience with all of the fi rm’s strategies. Ms. Margiotti also serves as a member of the relationship management team managing a number of the fi rm’s key relationships. Prior to joining the fi rm in 2005, Ms. Margiotti was the manager of investments for PG&E Corporation where she managed over $12 billion in pension, 401(k) and taxable trust assets. Her primary responsibilities included strategic asset allocation, investment strategy recommendations and investment

manager selection and oversight. Ms. Margiotti is a member of the Financial Women of San Francisco, serving as Scholarship Committee team leader for many years. She has been an adjunct professor at the University of San Francisco and an instructor for the CFA review program. Ms. Margiotti holds a B.S. degree in industrial management and fi nance from Purdue University and an M.B.A. degree from the McLaren School of Business at the University of San Francisco. She holds the Chartered Financial Analyst® designation, FINRA licenses 7 and 63, and has twenty-four years of industry experience.

Mike McCune, CFAMr. McCune is a portfolio analyst for Boston Partners and has extensive experience with all of the fi rm’s strategies. He began his career at Boston Partners in 2003 as a quantitative analyst, and later became a portfolio manager with the WPG Partners’ Quantitative Equity Group. Additionally, Mr. McCune has spent time as the U.S.-based Client Portfolio Manager for Robeco’s fundamental Emerging Markets and quantitative strategies. Prior to joining Boston Partners, Mr. McCune was a quantitative analyst at Deutsche Asset Management. Mr. McCune holds a BSc degree in fi nance from Villanova University and an M.B.A. from New York University. He holds the Chartered Financial Analyst designation. Mr. McCune has twenty-four years of industry experience.

Brandon Smith, CFA, CAIAMr. Smith is a portfolio analyst for Boston Partners and has extensive experience with all of the fi rm's strategies. Prior to this, Mr. Smith was a Vice President and senior investment analyst at Envestnet Asset Management. Before that, Mr. Smith held investment analyst roles within the fund of hedge funds groups at Gottex Fund Management and Columbia Partners

Investment Management. Mr. Smith holds a B.A. degree in government from Dartmouth College. He holds the Chartered Financial Analyst® and Chartered Alternative Investment Analyst designations. Mr. Smith has twelve years of industry experience.

Christopher EaganMr. Eagan is a global markets analyst for Boston Partners. He will be examining markets with a macro perspective. He joined the fi rm from Boenning & Scattergood Inc. where he was a managing director. Before that he was with Jessup & Lamont Securities and prior to that with Bank of America. He spent fi fteen years with Fidelity Capital Markets as a vice president, supervising an equity trading desk. Mr. Eagan began his career in New York City at Prudential Securities before moving onto Nomura Securities. He holds a B.A. degree in economics from the College of the Holy Cross and has thirty-three years of investment experience.

Michael A. MullaneyMr. Mullaney is the director of global markets research for Boston Partners. He rejoined the fi rm from Fiduciary Trust Company where he was chief investment offi cer with responsibilities that included setting the fi rms overall investment policy practices and establishing both strategic and tactical asset allocation targets for client portfolios. Prior to that, Mr. Mullaney was the director of fi xed income with Boston Partners Asset Management. Prior to joining Boston Partners, Mr. Mullaney was managing director and senior investment strategist at Putnam Investments, specializing in portfolio strategy and key account portfolio management. Before that, he was a senior consultant with Chase Econometrics/ Interactive Data Corporation, focusing on quantitative methodologies in fi xed income and equity management. Mr. Mullaney holds a B.S. degree (Cum Laude) in

Boston PartnersBiographical Information (continued)

Boston Partners n 45

biological sciences from Boston University and an M.B.A. in Finance from Babson College. He has a total of thirty-seven years of investment experience.

ResearchEric S. Connerly, CFAMr. Connerly is the director of quantitative research for Boston Partners. Prior to assuming this role, he was a research analyst covering the fi nancial, electronics, defense, transportation, and energy sectors and managed a merger arbitrage portfolio. He joined the fi rm from John Hancock Mutual Funds where he was an analyst and assisted in the management of a small cap portfolio. Prior to that, he was a senior equity analyst at SEI Investments overseeing their small cap equity portfolios. Mr. Connerly holds a BSFS degree Cum Laude in development economics from Georgetown University and an MBA degree in security analysis and investment management, Beta Gamma Sigma, from Columbia Business School. He holds the Chartered Financial Analyst® designation. He has twenty-fi ve years of experience.