Second Quarter 2016 - listed...

23

Transcript of Second Quarter 2016 - listed...

Q216 highlights

2

25.0m total subscribers 92.3% of sub base registered under DTN

THB8.7b data revenues

54.2% of service revenues ex. IC

THB6.6b EBITDA

33.4% EBITDA margin

THB4.3b CAPEX

21.7% to total revenues

THB0.42 per share dividend 71% of net profit

operational highlights

widest 4G-1800MHz bandwidth in the market

• 20MHz contiguous bandwidth on

4G-1800MHz

– service already on air in BMA

– to expand in other areas in Q3

– provide best 4G experience to all customers

with 4G-enabled devices

• 4G-1800MHz network covers all 77

provinces

• 4G-2100MHz on track to cover all

districts by Q316

• continued improvement in network

perception

19.6 20.8 23.6 24.3 25.2 26.0

2.9 3.4 3.4

6.3 10.3

15.6 22.5 24.2

27.0 30.7

35.5 41.6

Q115 Q215 Q315 Q415 Q116 Q216

4G 3G

4

no. of base stations (in thousand)

70

79

Q314 Q414 Q115 Q215 Q315 Q415 Q116

network perception

n= 2,000 2,000 2,080 2,090 2,096 2,082 2,086

Source: Independent 3rd-party Market Research.

Q115 Q215 Q315 Q415 Q116 Q216

1.0

2.9

3.5

Q115 Q215 Q315 Q415 Q116 Q216

strong development in 4G service

• 3.5 million 4G subscribers

• 23% penetration of 4G-enabled

devices – device campaigns an important factor pushing

4G adoption

• 3.4x data usage increase

– continued expansion of 4G network

– driven by video and music streaming services

5

4G subs (in million)

4G data usage (GB/sub/month)

3.4x

solid postpaid development

Q215 Q315 Q415 Q116 Q216

• network quality and perception

improvement – 4G/3G network expansion

– ongoing network perception campaign

• best offers in the market – super non-stop packages with more choices

– device campaigns

– MNP campaigns

– pre-to-post campaigns

• retail shop expansion

• digital services – VoWiFi / VoLTE

– dtac Music Infinite

6

postpaid revenues

Q215 Q315 Q415 Q116 Q216

sub base

+9.2% +13.1%

challenges in prepaid

• challenging development due to – widespread handset subsidy campaigns

– rapid decline in voice revenues

– migration to postpaid

• handset subsidy campaign to all

customers from June

• network perception campaign

• real-time personalized topping offers – dtac app, banners, SMS

– upsell, churn management

• “dtac prepaid” brand launched – targeting digital generation

– free calls when topping up data

– free YouTube and music streaming

7

Q215 Q315 Q415 Q116 Q216

prepaid revenues

Q215 Q315 Q415 Q116 Q216

sub base

-9.9% -11.0%

aspiring to become no. 1 digital brand

8

• offer attractive and relevant digital

services for customers – dtac app

– VoLTE, VoWiFi

– Capture cloud storage

– Music Infinite

– Jaew Wallet financial service

• plan to launch new services regularly

real-time personalized offers launched

contextual upsell

• contextual intelligence platform

– real-time offers for each individual

customer based on usage profile at a

specific trigger point

• launched via dtac app

– target dtac customers initially

• to expand to 3rd party channels

develop to become digital

ad/marketing platform

9

SMS & USSD &URL

dtac app, web, and

self-service machine

3rd-party channels

contextual

real-time offers

Contextual Intelligence

CMP BI

spectrum not a short-term concern

• strong spectrum portfolio

• work with authority for a clear

spectrum roadmap: 2.6GHz, 2.3GHz,

1800MHz, 850MHz, etc.

• dtac has every intent to obtain

additional spectrum in future auctions

10

Concession 1/ License 2/ Total

850MHz 1800MHz 2100MHz

2G 5MHz 5MHz

3G 10MHz 10MHz 20MHz

4G 20MHz 5MHz 25MHz

Total 10MHz 25MHz 15MHz 50MHz

1/ concession expires in 2018, excluding 20MHz of unused 1800MHz band. 2/ license expires in 2027.

financial highlights

92% of sub base registered under DTN

5.0 3.5 3.0 2.6 2.3 1.9

23.5 23.5 21.9 22.6 23.1 23.0

28.4 26.9 24.9 25.3 25.5 25.0

Q115 Q215 Q315 Q415 Q116 Q216

dtac DTN

215 218 220 238 234 227

195 198 204 220 217 211

Q115 Q215 Q315 Q415 Q116 Q216

ARPU incl. IC ARPU ex. IC

216 206 208 213 194 179

174 165 165 169 153 138

Q115 Q215 Q315 Q415 Q116 Q216

MoU incl. IC MoU ex. IC

dtac vs. DTN subscribers ARPU MoU million subs THB/sub/month mins/sub/month

• porting of subs to DTN continues

gradually

• postpaid net adds remains strong

• MoU on downward trend due to

change in consumer behavior

• VoIP traffic, however, continued to

grow

QoQ YoY

w/ IC

w/o IC

-3.1%

-2.6%

+4.1%

+7.0%

QoQ YoY

w/ IC

w/o IC

-7.4%

-9.9%

-12.8%

-16.6%

12

• YoY increase due to impact from

prepaid registration

• underlying ARPU continued trending

down

data revenue growth accelerated

13

7.8 7.3 7.1 7.1 6.6 5.8

7.5 7.6 7.8 7.9 8.2 8.7

1.6 1.5 1.5 1.6 1.6 1.5

16.8 16.4 16.4 16.6 16.4 16.0

Q115 Q215 Q315 Q415 Q116 Q216

voice data others

service revenues ex. IC data revenue

85% 86% 89% 89% 90% 90%

4% 4% 3% 3% 3% 2% 11% 10% 8% 8% 7% 7%

Q115 Q215 Q315 Q415 Q116 Q216

mobile internet messaging others

data revenue breakdown THB billion % of service revenues ex. IC % of vas revenues

• growth of revenue from data

services remains strong, reaching

54% of service revenues ex. IC

• mobile Internet continues to

dominate revenue from data services

• decline of service revenue QoQ was

partly due to seasonality

• YoY decline was mainly driven by

intense competition

7.5 7.6 7.8 7.9 8.2 8.7

44.5% 46.3% 47.5% 47.5%

50.0% 54.2%

Q115 Q215 Q315 Q415 Q116 Q216

QoQ YoY

-2.4% -2.4% THB billion

*

* excluding one-time accounting adjustment on prepaid

revenues, service revenues ex. IC would have been

THB16.2b, declining 1.4% QoQ and YoY.

4.4 3.8

1.9

5.3

3.8

2.3

Q115 Q215 Q315 Q415 Q116 Q216

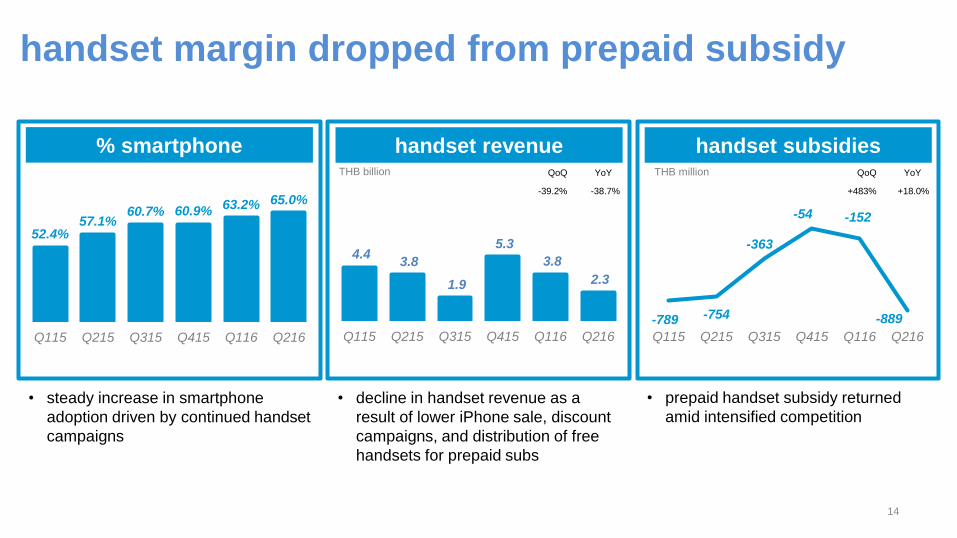

% smartphone handset revenue

52.4% 57.1%

60.7% 60.9% 63.2% 65.0%

Q115 Q215 Q315 Q415 Q116 Q216

handset subsidies

-789 -754

-363

-54 -152

-889

Q115 Q215 Q315 Q415 Q116 Q216

THB billion

• decline in handset revenue as a

result of lower iPhone sale, discount

campaigns, and distribution of free

handsets for prepaid subs

• prepaid handset subsidy returned

amid intensified competition

• steady increase in smartphone

adoption driven by continued handset

campaigns

14

handset margin dropped from prepaid subsidy

QoQ YoY

-39.2% -38.7%

THB million QoQ YoY

+483% +18.0%

3.1 3.1 3.1 2.9 2.9 2.5

1.2 1.4 1.2 1.4 1.3 1.5

1.0 1.0 1.1 1.2 1.0 0.9

5.3 5.6 5.3 5.4 5.2 4.8

Q115 Q215 Q315 Q415 Q116 Q216

regulatory network opex others

cost of services % cost of services THB billion % to service revenues ex. IC

18.3% 18.8% 18.7% 17.4% 17.7% 15.3%

7.4% 8.8% 7.3% 8.4% 7.9% 9.3%

Q115 Q215 Q315 Q415 Q116 Q216

regulatory costs network opex

• % regulatory cost dropped

from continued porting of

subs to DTN and DR rate

adjustment

• network OPEX increased

along with expansion of 4G

and 3G networks

• ongoing programs to improve

operational efficiency

* excluding depreciation and amortization, and IC

*

15

cost of services under control

QoQ YoY

-7.0% -13.6%

% SG&A expenses

• S&M expenses increased from

higher competition and launch

of new services

• general admin expenses well

under control

• continued focus on cost control

SG&A expenses THB billion

6.4%

8.0%

8.2% 8.9% 8.4% 9.7%

7.6%

7.7%

10.7% 9.8% 10.3% 10.3%

Q115 Q215 Q315 Q415 Q116 Q216

S&M gen admin

% to total revenues

* excluding depreciation and amortization

*

1.5 1.8 1.6 2.1 1.8 1.9

0.2 0.2 0.2

0.3 0.2 0.2

1.7 1.7 2.1

2.3 2.2 2.0

3.4 3.7 4.0 4.6

4.2 4.2

Q115 Q215 Q315 Q415 Q116 Q216

S&M bad debt gen admin

16

normalized SG&A stabilized QoQ

QoQ YoY

-2.0% +13.3%

solid EBITDA margin development

7.4

6.7

7.1

6.7

7.3

6.6

Q115 Q215 Q315 Q415 Q116 Q216

EBITDA (before other item) EBITDA margin THB billion

32.3% 30.7%

35.9%

29.0% 33.8% 33.4%

44.3% 41.3% 41.8%

37.8% 41.9% 42.9%

Q115 Q215 Q315 Q415 Q116 Q216

EBITDA margin EBITDA margin ex handset

• excluding handset, EBITDA

improved both YoY and QoQ,

mainly due to lower regulatory

cost

• EBITDA margin slightly

declined QoQ mainly as a

result of higher handset

subsidies, partly offset by

lower regulatory cost

• excluding one-time adjustment

on prepaid revenue, EBITDA

slightly increased YoY

17

QoQ YoY

-9.8% -1.8%

0.97

0.58 0.52 0.42

0.53

0.06 2.3 1.4 1.2 1.0 1.3 0.1

Q115 Q215 Q315 Q415 Q116 Q216

net profit THB per share (top)

THB billion (bottom)

• Decline in net profit is mainly driven

by lower EBITDA and higher D&A

charges

• In addition, THB394m one-time

restructuring cost also have

significant impact 18

THB0.42 per share dividend for H116

QoQ YoY

-88.7% -89.7%

1.9 3.6

-0.6

2.8 2.6 2.3

5.5 3.2

7.6 3.9 4.7

4.3

7.4 6.7 7.1 6.7

7.3 6.6

Q115 Q215 Q315 Q415 Q116 Q216

operating CF (ebitda-capex) capex

operating cash flow key financial ratios THB billion

2.2 2.5 2.6

4.0 3.3 3.2

0.8 1.0 0.9 1.4 1.1 1.1

Q115 Q215 Q315 Q415 Q116 Q216

net debt:equity* net debt:ebitda

* excluding other component of shareholders’ equity.

• OCF remains solid

• CAPEX level is on track to meet full

year guidance

• financial ratios improve from last

quarter

strategic direction and outlook

strategic direction – no. 1 digital brand

20

vision Empower society by connecting people to

information, content and services that

matter to them, helping to improve their

lives, and securing a better future for all

goal To be the no.1 digital brand in Thailand, by

being our customers’ favorite partner in

digital life

digital disruptor

21

slight decline from previous year

service revenues ex. IC growth

same level as previous year

capex

2016 outlook revised

EBITDA margin

31 – 33%

Certain forward looking statements may be made in the course of the presentation. These forward-looking statements

generally can be identified by use of statements that include words or phrases such as dtac or its management

“believes”, “expects”, “anticipates”, “intends”, “plans”, “foresees”, or other words or phrases of similar import. Similarly,

statements that describe dtac’s objectives, plans or goals also are forward-looking statements.

All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ

materially from those contemplated by the relevant forward-looking statement. The forward-looking statements

contained in the slides are not and should not be constructed as representations of the future performance of dtac and

that such statements are an expression of the Company’s reviews based on its current view and certain assumptions

including, but not limited to, prevailing economic and market conditions and currently available information.

disclaimer

Investor Relations

E: [email protected] T: +662 202 8882

![[XLS] · Web view11/1/2016 1/25/2016 1/22/2016 1/22/2016 1/21/2016 1/21/2016 1/21/2016 1/21/2016 1/21/2016 1/21/2016 1/21/2016 1/21/2016 1/20/2016 1/20/2016 1/19/2016 1/18/2016 1/18/2016](https://static.fdocuments.in/doc/165x107/5c8e2bb809d3f216698ba81b/xls-web-view1112016-1252016-1222016-1222016-1212016-1212016-1212016.jpg)