SEB Investor Lunch Presentation Nov 2008

15

Lunch presentation November 27 2008 Annika Falkengren CEO

-

Upload

sebgroup -

Category

Economy & Finance

-

view

5.030 -

download

4

Transcript of SEB Investor Lunch Presentation Nov 2008

Lunch presentation

November 272008

Annika FalkengrenCEO

2

Highlights Q3 2008Resilient underlying business; collective provisions in the BalticsNegative financial effects due to financial crisisAccelerated cost management due to economic downturn

Financial crisis impacts profit…

* Excluding sales of Baltic properties in Q4 2007 of SEK 785mand reclassification of portfolios

0

1,000

2,000

3,000

4,000

5,000

Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

Lehman Brothers-related lossesPortfolio lossesReported operating profit*

…but underlying income generation is stable

** Net financial income, Net insurance income and Other income

0

2,000

4,000

6,000

8,000

10,000

Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

Other income**Net fee and commission incomeNet interest income

*

3

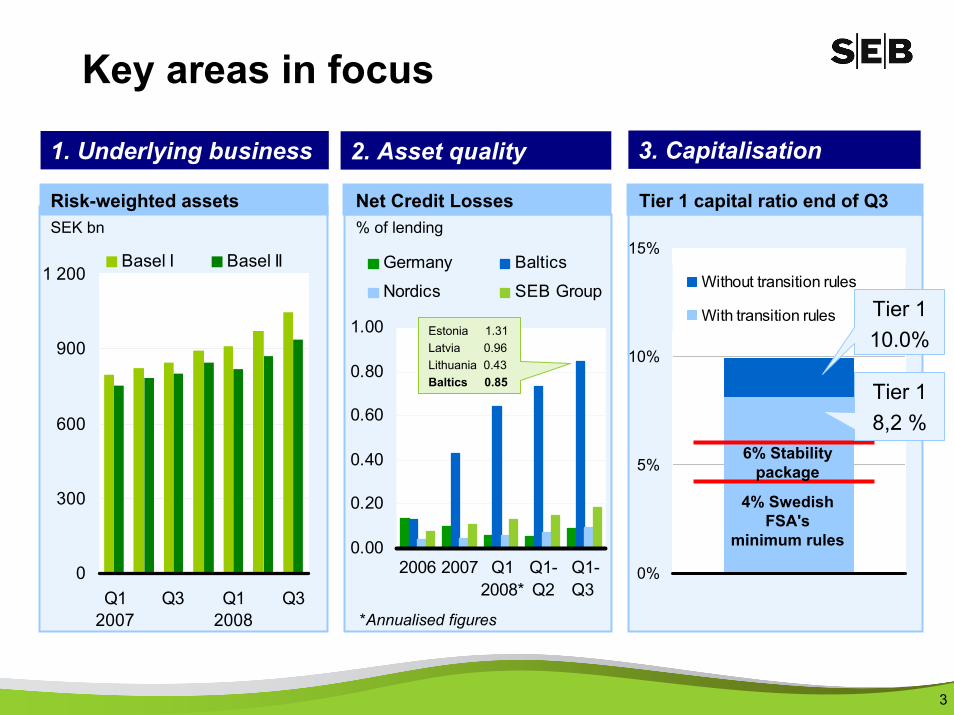

Key areas in focus

0.00

0.20

0.40

0.60

0.80

1.00

2006 2007 Q12008*

Q1-Q2

Q1-Q3

Germany Baltics

Nordics SEB Group

Net Credit Losses % of lending

Estonia 1.31Latvia 0.96Lithuania 0.43Baltics 0.85

*Annualised figures

Tier 1 capital ratio end of Q3Risk-weighted assetsSEK bn

0

300

600

900

1 200

Q12007

Q3 Q12008

Q3

Basel I Basel II

1. Underlying business 2. Asset quality 3. Capitalisation

0%

5%

10%

15%

Without transition rules

With transition rules

4% SwedishFSA's

minimum rules

6% Stabilitypackage

Tier 1 10.0%

Tier 1 8,2 %

4

… maybe 4 - Guarantee pricing in the Swedish stability package

Unsecured <1 year: 50bpsUnsecured >1 year: 50bps+28bps (CDS) = 78bps (+25bps)Covered bonds: 25bps+ ~10bps (AAA-CDS) = ~35bps

Maximum scope: for each bank: its outstanding debt maturing until April 30th, 2009; for the system: SEK 1,500bn

Participating banks to pay a risk-based fee for the guarantee; Fee level: somewhere between today's funding costs in the market and the notional funding costs under normal market circumstances

Allowed instruments: senior term debt with maturities between 3 months and 5 years, including covered bonds!

5

Resilient underlying business

0

50

100

150

200

250

300

350

400

450

500

"Nord

ic" La

rger C

lients

German

Large

r Clie

ntsBalt

ic Clie

nts

Swedish

Reta

il Clie

nts

Other

Corporate credit exposureSEK m , Q4-06, Q2-07, Q4-07, Q2-Q3-08

12.010.7 9.7

12.0 13.3 11.9 10.7

Q1-07 Q2 Q3 Q4 Q1-08 Q2 Q3

Swedish mutual funds – Net inflowsJan-Sep, SEK bn

-7.3-11.6

-1.1

-17.0

5.9

Robur SHB Nordea SEB Others

Life – Total salesSEK bn

6

Asset quality

Nordics66%

Group credit exposureTotal exposure = SEK 1,805bn

Germany24%

Baltics - Provisioning to build up reservesSEK m

Impaired Loans Volumes % of Credit Portfolio

0%

1%

2%

3%

Mar'06

Jun'06

Sep'06

Dec'06

Mar'07

Jun'07

Sep'07

Dec'07

Mar'08

Jun'08

Sep'08

SEB Group GermanyNordic Baltic

1.5%1.4%

0.6%0.2%

Lithuania5% Latvia

2%

Estonia3%

-50

50

150

250

350

Q4-07 Q1-08 Q2-08 Q3-08

Specific Collective

7

Baltic countries – Estonia Credit exposureSEK bn

Lending market shares % of lending

SEB facts

17 22 22

88 8

1419 20

Dec '06 Dec '07 Sep '08

BanksPublic AdministrationHouseholdsProperty ManagementCorporate

2006 2007 2008 YTD+38% +17% +1%

Growth rate i LCY

4150 52

SEBSwedbankSampo (no longer published)

0%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

723,000 private customers70,000 corporate customers~1,550 FTEs (present)60 branches

0

500

1,000

1,500

2005 2006 2007 9m2008

Pre-provision profit Operating profit

SEB performance, SEK m

8

Baltic countries – Latvia Credit exposureSEK bn

Lending market shares % of lending

SEB facts

18 21 224 5 610

14 14

Dec '06 Dec '07 Sep '08

BanksPublic AdministrationHouseholdsProperty ManagementCorporate

2006 2007 2008 YTD+40% +18% +4%

Growth rate i LCY

3441 44

0%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

SEBSwedbankDnB NordParex BankaSampo/DanskeNordea

929,000 private customers65,000 corporate customers~1,750 FTEs (present)65 branches

0

500

1,000

1,500

2005 2006 2007 9m2008

Pre-provision profit Operating profit

SEB performance, SEK m

9

Baltic countries – Lithuania Credit exposureSEK bn

Lending market shares % of lending

SEB facts

34 39 458

13 151322

26

Dec '06 Dec '07 Sep '08

BanksPublic AdministrationHouseholdsProperty ManagementCorporate

2006 2007 2008 YTD+47% +30% +13%

Growth rate i LCY

56

7689

0%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

SEBSwedbankDnB NordSampo/DanskeNordea

992,000 private customers61,000 corporate customers~2,200 FTEs (present)76 branches

0

500

1,000

1,500

2005 2006 2007 9m2008

Pre-provision profit Operating profit

SEB performance, SEK m

10

Notes:1 Swedbank: Including SEK 12.5bn capital rasing announced 27 October 20082 Danske: only reports tier 1 ratio under full Basel II3 DnB NOR: RWA adjusted for life insurance impact (life insurance assets risk weighted under statutory disclosure) to allow comparison

10.5 10.1 10.0 10.09.4

7.9

6.7

8.28.27.3 7.0

Swedbank Danske Bank SEB SHB DnB NOR Nordea

Tier 1 ratio - Full Basel II Tier 1 ratio - Basel II transition rules

Nordic capital ratiosTier 1 capital ratio reported Q3 2008 (%)

11

Financial effects in Q3 2008

Net financial income SEK +516m Operating profit SEK +516mNet profit SEK +372mTotal equity SEK +1,797mRWA– Basel I: SEK +5.3bn– Basel II: SEK -1.1bnCore capital ratio and Total capital ratio marginally affected

Reclassification of fixed income portfolios in Q3 2008

Q3 08

8 11

50

39

36

1

14

ABS Financialinstitutions

Coveredbonds etc.

After reclassification

Held for trading (MTM over income)

Available for sale (MTM over equity)

Loans & Receivables (No MTM, impairment tests)

12

Business update

Corporate lending growth continues – core clients, better structures and higher margins

Household mortgage lending decelerates

Stable long-term savings

SEB Equities continues to gain market shares and FX trading still strong

Transaction numbers still on very high level

Private individuals remain cautious and seek advise – creates opportunities

Investment portfolio remains healthy – reclassification limits volatility impact

13

Nordic Outlook

•Global recession - worst situation in 60 years•Sweden and the Nordic region import international recession •Baltic economies in for hard landing – but different degrees of recession •Central banks enter zero-rate territory•Global - partly synchronised, partly competing - stimuli from politicians

-6-30369

12

Sweden Nordics Estonia Latvia Lithuania

2007 2008 (f) 2009 (f) 2010 (f)

Annual GDP growthPer cent

Key themes

14

Going forward

● Holistic balance sheet management

● Robust capital and good liquidity

● Resilient customer business

● Cost management

1515