Seattle Alumni Speed Training 2016 · 12/6/2016 · • Final standard was issued in June 2016...

168

Seattle Alumni Speed Training 2016 Kelly Snow Eric Coats December 6, 2016 David Cordova Brian Rose Russ Savage Kelsey Fennerty Jeff Kummer

Transcript of Seattle Alumni Speed Training 2016 · 12/6/2016 · • Final standard was issued in June 2016...

Seattle Alumni Speed Training 2016

Kelly SnowEric Coats

December 6, 2016

David CordovaBrian Rose

Russ SavageKelsey FennertyJeff Kummer

AGENDA:

• Welcome• SEC & Regulatory Update• Financial Instruments• The Global Tax Reset and BEPS• BREAK• Revenue Recognition• Discussing the FASB’s New Lease Accounting Standard• Tax Reform Developments and Election Outcomes• Closing

SEC & Regulatory Update

Copyright © 2016 Deloitte Development LLC. All rights reserved. 4SEC & Regulatory Update

• SEC overview, current landscape, and rulemaking

• Disclosure effectiveness

• SEC comment trends

• PCAOB Update

• Question and answer

Agenda

5Copyright © 2016 Deloitte Development LLC. All rights reserved.

SEC Organizational Structure

OpenChairman White(since 2013)

CommissionerPiwowar(since 2013)

Open

InvestmentManagement

Office of Chief Accountant (OCA)

Trading and Markets

CommissionerStein(since 2013)

22 other offices

Corporation Finance

Economic and Risk Analysis Enforcement

*Lisa Fairfax and Hester Peirce nominated for open seats by President Obama, subject to Senate confirmation

6Copyright © 2016 Deloitte Development LLC. All rights reserved.

Enforcement Initiatives

Financial Reporting and Audit (“FRAud”) Task Force

• Focus on financial statements, reporting and disclosures, and audit failures

• Monitor restatement activities

• Use of technology and tools for “data mining” and data analysis

Other policy-related initiatives

• Admission of wrong-doing

• Focus on the individual

FY 2015 FY 2014 FY 2013

Number of enforcement actions 807 755 676

Orders for penalties and disgorgements $4.2 billion $4.2 billion $3.4 billion

7Copyright © 2016 Deloitte Development LLC. All rights reserved.

Enforcement Initiatives Whistleblower program

7

• Largest payment announced to date - $30 million

• Retaliation and “Pre-taliation” concerns

Original information

Penalty more than$1 million

10% - 30%award

Disclosures & F/S 17.5%

Offering Fraud 15.6%

Manipulation 12.3%

SEC & Regulatory Update

FY 2015 FY 2014 FY 2013

Whistleblower tips received 3,923 3,620 3,238

8Copyright © 2016 Deloitte Development LLC. All rights reserved.

SEC Rulemaking and Interpretations

Dodd-Frank Act

• Continued effort on required rulemakings

• Recent rulemaking

—Final rule - CEO pay ratio disclosure

—Proposed rules

—Pay versus performance

—Executive compensation clawback

JOBS Act

• Regulation Crowdfunding

• FAST Act

Non-GAAP Measures - Updated Compliance & Disclosure Interpretations (C&DIs)

Disclosure effectiveness

9Copyright © 2016 Deloitte Development LLC. All rights reserved.

Misleading measures (C&DI 100.01- 100.04)

Financial measures using unrelated GAAP principles (C&DI 100.4)

• Adjusted Revenue

• A registrants' own set of principles to determine and present GAAP is not permitted

Presenting liquidity measures on a per share basis (C&DI 102.05)

• Designated performance measures that are really liquidity measures

Non-GAAP tax expense – (C&DI 102.11)

• Impact adjustments are expected to have on a registrants tax rate

• Presenting adjustments net of tax is not permitted

Non-GAAP MeasuresNon-GAAP Areas of SEC Concern

10Copyright © 2016 Deloitte Development LLC. All rights reserved.

More prominent presentation of Non-GAAP Measures (C&DI 102.10)

Examples of prominence issues:

• Full non-GAAP Income Statement

• Omitting comparable GAAP measures from press release headlines

• Bolder larger font

•

•

Non-GAAP measure that precedes a comparable GAAP measure

Equally prominent description for a GAAP measure (e.g. “record performance”)

• Tabular disclosures

• Disclosures related to forward looking non-GAAP measures

• Same discussion and prominence for GAAP measures

Non-GAAP MeasuresNon-GAAP Areas of SEC Concern (Continued)

“This quarter will be a great opportunity for companies to self correct”

– Mark Kronforst, Chief Accountant, SEC’s Division of Corporation Finance

11Copyright © 2016 Deloitte Development LLC. All rights reserved.

Non-GAAP MeasuresTop 10 Non-GAAP questions to consider based on recent SECfocus

1. Is the measure misleading or prohibited?

2. Is the measure presented with the most directly comparable GAAP measure and with no greater prominence than the GAAP measure?

3. Is the measure appropriately defined and described, and clearly labeled as non-GAAP?

4. Does the reconciliation between the GAAP and non-GAAP measure clearly label and describe the nature of each adjustment, and is each adjustment appropriate?

6. Is there transparent and company-specific disclosure of the substantive reason(s) why management believes that the measure is useful for investors and the purpose for which management uses the measure? Is the measure consistently prepared from period to period in accordance with a defined policy, and is it comparable to that of the company’s peers?

7. Is the measure balanced (i.e., it adjusts not only for nonrecurring expenses but also for nonrecurring gains)?

8. Does the measure appropriately focus on material adjustments and not include immaterial adjustments that would not seem to be a focus of management?

9. Do the disclosure controls and procedures address non-GAAP measures?

10. Is the audit committee involved in the oversight of the preparation and use of non-GAAP measures?

SEC Chair Mary Jo White

“When disclosure gets to be too much or strays from its core purpose, it could lead to… information overload…”

SEC Commissioner Kara Stein

“…It baffles me that such a huge portion of public disclosures are presented in a format that isn’t structured and easily accessible for analytics…”

Former SEC Commissioner Daniel Gallagher

“Today’s…disclosure documents are no longer efficient mechanisms for clearly conveying material information to investors…”

Disclosure Effectiveness

12Copyright © 2016 Deloitte Development LLC. All rights reserved.

13Copyright © 2016 Deloitte Development LLC. All rights reserved.

What is it?

• Providing better information to investors – more understandable, more useful and eliminating excessive disclosure

• Could result in additional disclosures

What has the SEC staff done lately?

• Request for comment on financial disclosures about entities other than the registrant

• S-K concept release – comments closed July 21, 2016

• Disclosure Update and Simplification proposed rule –issued July 13, 2016

–September 2015

1

2

3

Focus on material and relevant matters

Reduce or eliminate redundant disclosures

Tailor disclosures to company’s facts and circumstances

Disclosure Effectiveness (Continued)

14Copyright © 2016 Deloitte Development LLC. All rights reserved.

Disclosure Effectiveness (cont.)Regulation S-K Concept Release

Background on Regulation S-K and the Release What’s in?

• The overall disclosure framework

• Disclosures for investment and voting decisions –

Specific business and financial disclosure requirements in Regulation S-K

• Core company business information • Public policy and sustainability matters

• Company performance, financial information, and future prospects • Exhibits

• Risk and risk management • Scaled requirements

• Securities of the registrant • Frequency of interim reporting

• Industry guides • Presentation and delivery

15Copyright © 2016 Deloitte Development LLC. All rights reserved.

What’s out?

Public-company disclosure issues that are not a focus of the release

SEC is encouraging comments on any disclosure topic

Disclosure Effectiveness (cont.)Regulation S-K Concept Release

• Proxy Info – Compensation and governance information

• Modernization of the EDGAR system

• Non-GAAP measures • Disclosures required for foreign private issuers

• Inline XBRL • Business development companies

These topics may be considered in future stages of the SEC’s disclosure effectiveness project

16Copyright © 2016 Deloitte Development LLC. All rights reserved.

Disclosure Effectiveness (continued)Disclosure Update and Simplification proposed ruleType of Requirement and Goal

Redundant or duplicative requirements

Eliminate requirements that result in disclosure of substantially the same information as that required under other Commission rules,U.S. GAAP, or IFRSs. (Example Debt obligation)

Overlapping requirements Eliminate requirements that convey reasonably similar information, or information that is not materially incremental to that required underother SEC requirements, U.S. GAAP, or IFRSs and that may no longer be useful to investors. (Example segments)

Integrate certain disclosure requirements with other related Commission disclosure requirements. (Example dividend restrictions)

Modify or eliminate overlapping disclosures or refer them to the FASBfor potential incorporation into U.S. GAAP. (Example income taxes)

Outdated requirements Amend requirements that have becomeobsolete as a result of the passage of time or changes in the regulatory, business, or technological environment. (Example Market price disclosures)

Superseded requirements Amend requirements that are inconsistent with new accounting, auditing, disclosure requirements, and more recentlyupdatedCommission disclosure requirements. (Example extraordinary item)

17Copyright © 2016 Deloitte Development LLC. All rights reserved.

SEC Review Process Filing Reviews

About 9,000 registrantsFocus on 2,500 registrants that comprise 98% of market cap

All issuers reviewed at least 1 out of every 3 years

Percentage of issuers reviewed:

Staff is listening to analyst/earnings calls, reviewing press releases, Web sites, social media, and issuing comments

Comments are posted to EDGAR 20 days after completion of review

44% 48% 48% 52% 52% 51%

FY10 FY11 FY12 FY13 FY14 FY15

18Copyright © 2016 Deloitte Development LLC. All rights reserved.

Topic

12 Months- 12/31/15 12 Months- 12/31/14

Rank Frequency* Rank Frequency*

MD&A:• Results of operations• Liquidity issues• Critical accounting policies, estimates

124%11%8%

124%13%11%

Fair value measurement, estimates 2 22% 2 23%

Non-GAAP measures 3 16% 5 13%

Revenue Recognition 4 14% 3 16%

Income taxes 5 11% 7 12%

Segment reporting 6 11% 9 11%

Signatures, exhibits, agreements 7 11% 4 15%

Intangible Assets and Goodwill 8 10% 8 11%

Acquisitions, mergers, business combinations 9 9% 6 12%

Commitments, Contingencies, and Litigation 10 8% 11 10%

* Percentage of all 10-Ks and 10-Q comment letter-yielding reviews that included at least one comment on the respective topic.Source: Derived from data provided by Audit Analytics.

SEC Comment Letter Trends:Overall Summary

19Copyright © 2016 Deloitte Development LLC. All rights reserved.

SEC Comment Letter Trends Areas of Focus

Non-GAAP Measures (16%)

• Transparency & Consistency

• Misleading measures

• Usefulness of the measure

Metrics

• Clearly define metrics and explain how calculated

• Explain how used by management and why important to investors

• Describe how a metric is related to current or future results of operations

20Copyright © 2016 Deloitte Development LLC. All rights reserved.

Revenue Recognition (14%)

• Gross vs Net

• Multiple element arrangements

• Contra-revenue items

• SAB 74 Disclosures on new Revenue ASU

Income Taxes (11%)

• Valuation Allowance

• Rate reconciliation

—Appropriate breakout (and descriptions of) adjustments

• Impact of foreign operations

• Repatriation of foreign cash

SEC Comment Letter Trends Areas of Focus

21Copyright © 2016 Deloitte Development LLC. All rights reserved.

Segments (11%)

• SEC staff’s focus is evolving:

—Chief Operating Decision Maker (CODM) package- no longer determinative

—Staff will consider total mix of information

• Aggregation of operating segments still a focus - consider both quantitative and qualitative factors

• Consider whether CODM is someone other than CEO

• Both SEC and PCAOB are focusing on segments

SEC Comment Letter Trends Areas of Focus

22Copyright © 2016 Deloitte Development LLC. All rights reserved.

Business Combinations

• Purchase price allocation

• Determination of fair values and key assumptions

Goodwill and Intangibles Impairment

• Valuation Assumptions and sensitivity (FRM 9510)

• Specific events that caused the impairment – “why now”

• Early warning disclosures

SEC Comment Letter Trends Areas of Focus

23Copyright © 2016 Deloitte Development LLC. All rights reserved.

SEC Comment Letter Trends

• Ninth Edition — October 2015

• Insights into areas the SEC staff has focused on in recent comment letters including:

– Financial Statement Accountingand Disclosure Topics

– SEC Disclosure Topics

– Disclosure Topics in Initial PublicOfferings

– Industry-Specific Topics

• Consumer & Industrial Products

• Energy & Resources

• Financial Services

• Health Sciences

• Technology & Telecommunications

Financial instruments

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 25

Topics

Financial Instruments

Classification and measurement

Derivative contract novations

Contingent puts and calls in a debt host contract

CECL

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 26

Classification and measurement

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 27

Accounting Standards Update No. 2016-01Classification and measurement

Overview of the standard

• ASU 2016-01 was issued January 6, 2016

• Makes significant changes to:

− Classification and measurement of investments in equity securities

− Presentation of certain fair value changes for financial liabilities measured at fair value under the fair value option

− Disclosure of fair value of financial instruments

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 28

Accounting Standards Update No. 2016-01 (cont.)Classification and measurement (cont.)

Overview of the standard (cont’d)

• Equity investments

− Most equity securities will be carried at fair value through net income

◦ Practicability exception permitted for equity securities that do not (1) have readily determinable fair values and (2) qualify for the net asset value (NAV) practical expedient

◦ Equity method investments and investments that are consolidated are excluded from the scope of the new guidance

− Accounting for equity securities for which the practicability exception has been elected

◦ Measured at cost, less impairment

◦ Adjustments are made for (1) observable price changes and (2) impairment

◦ When considering “observable” changes they should be known or reasonably known and no undue cost is necessary in identifying such transactions

◦ Other-than-temporary impairment no longer exists for equity securities

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 29

Accounting standards update No. 2016-01 (cont.)Classification and measurement (cont.)

Overview of the standard (cont’d)

• Instrument-specific credit risk for fair value option liabilities

− Separately recognize in OCI changes in fair value attributable to instrument-specific credit risk

◦ Entire change in fair value of derivative liabilities is still presented in net income

− Instrument-specific credit may be calculated by either:

◦ Determining the excess of total change in fair value over the change in fair value that results from a change in a base market risk (e.g., risk-free interest rate, benchmark interest rate) or

◦ Using another method that the entity believes is a more faithful representation

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 30

Accounting Standards Update No. 2016-01 (cont.)Classification and measurement (cont.)

Overview of the standard (cont’d)

• Valuation allowance on a deferred tax asset (DTA) related to an AFS debt security

− Eliminates existing diversity in practice, where entities may either:

◦ Evaluate the need for a valuation allowance on a DTA related to AFS debt securities separately, or

◦ Evaluate the need for a valuation allowance on a DTA related to AFS debt securities in combination with the entity’s other DTAs

− Valuation allowance on a DTA related to an AFS debt securities now may only be assessed in combination with the entity’s other DTAs

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 31

Accounting Standards Update No. 2016-01 (cont.)Classification and measurement (cont.)

Overview of the standard (cont’d)

• Disclosure changes

− Non-public entities no longer required to disclose FV of financial instruments not recognized at FMV (e.g. debt)

− Public entities no longer required to disclose methods and significant assumptions used to estimate FV of financial instruments not recognized at FMV

− Public entities must use exit price notion to estimate FV of items carried at amortized cost

− Financial assets and financial liabilities must be presented separately, grouped by (1) measurement category and (2) class of financial asset

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 32

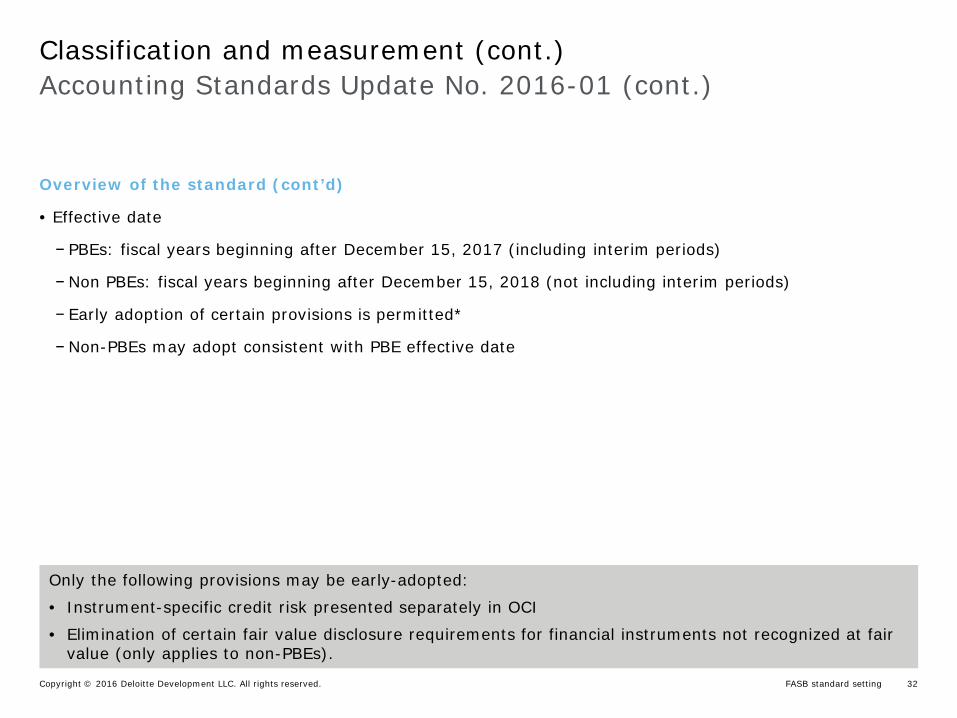

Accounting Standards Update No. 2016-01 (cont.)Classification and measurement (cont.)

Overview of the standard (cont’d)

• Effective date

− PBEs: fiscal years beginning after December 15, 2017 (including interim periods)

− Non PBEs: fiscal years beginning after December 15, 2018 (not including interim periods)

− Early adoption of certain provisions is permitted*

− Non-PBEs may adopt consistent with PBE effective date

Only the following provisions may be early-adopted:

• Instrument-specific credit risk presented separately in OCI

• Elimination of certain fair value disclosure requirements for financial instruments not recognized at fair value (only applies to non-PBEs).

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 33

Derivative contract novations

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 34

Accounting Standards Update No. 2016-05Derivative contract novations

• A change in the counterparty to a derivative instrument that has been designated as the hedging instrument in an existing hedging relationship would not, in and of itself, be considered a termination of the derivative instrument.

− Effective date (early adoption permitted):

− Public companies: fiscal years beginning after 12/15/16

− Other entities: annual periods beginning after 12/15/17 and interims after 12/15/18

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 35

Contingent puts and calls in a debt host contract

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 36

Accounting Standards Update No. 2016-06Classification and measurement

• In assessing whether a contingent put or call option is clearly and closely related to a debt host, an entity is required to only perform the four-step decision sequence in ASC 815-15-25-42.

− The event that triggers exercisability does not need to be evaluated

− Effective date (early adoption permitted):

− Public companies: fiscal years beginning after 12/15/16

− Other entities: annual periods beginning after 12/15/17 and interims after 12/15/18

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 37

Current expected credit loss model

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 38

Concept Current GAAP CECL

Loss horizon Produces an estimate of all inherent losses in the portfolio as of the balance sheet date (i.e., losses that have been incurred)

Requires institutions to estimate the contractual cash flows that are not expected to be collected over the estimated life of the loan (i.e., forward-looking)

Loss recognition

Recognizes an allowance over a defined loss emergence period after a loss event (e.g., unemployment) has occurred

Does not have a recognition threshold and produces a life-of-loan estimate

Basis for estimates

• Relevant information about past events (including historical loss experience with similar assets)

• Current conditions

• Relevant information about past events (including historical loss experience with similar assets)

• Current conditions• Reasonable and supportable

forecasts

Comparison of CECL and existing GAAPFASB impairment project (cont.)

FASB standard settingCopyright © 2016 Deloitte Development LLC. All rights reserved. 39

• Final standard was issued in June 2016 (ASU 2016-13)

FASB impairment project–where we are today

• For calendar year public SEC filers the guidance is effective January 1, 2020

• For all other calendar year entities the guidance is effective on January 1, 2021

• A one year deferral for interim periods is available for non public business entities

• Early adoption is permitted as of 1/1/19

• Modified retrospective application with cumulative-effect adjustment recognized in first period of adoption

Effective date and transition

Overview of the modelFASB impairment project

The Global Tax Reset and BEPS

David Cordova

The Global Tax ResetAn overview

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 42

Multinational companies face a new kind of tax-related challenges

Government deficits and related cut-backs, media attention and activist group interest has resulted in political interest in tax reform

The Global Tax Reset

Perception MNCs are not paying fair share of taxes

Loss of trust between tax authorities and business

Rise of source country taxation

General context

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 43

This new global tax environment has resulted in the following actions:

The Global Tax Reset

43

Change in tax authorities’ approach to

interpretation of tax law and

tax treaties

Responsible Tax agenda

Unilateral action

BEPS is part of the bigger picture

EU Commission

Fight Tax Abuse & State Aid

OECD’s BEPS project

Overview of actions

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 44

How will this play out?Tax is increasingly a theme for analysts and the media

Reporting the impactHow will this play out and how are corporates responding?

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 46

Deloitte’s Global Multinational Survey

Unilateral Legislative Changes

• Over 50% of respondents are anticipating significant unilateral legislative changes to protect the tax base that is not coordinated with what other countries are doing

Compliance Burden

• Nearly 90% of respondents are anticipating that their income tax compliance burden will substantially increase as a result of the additional reporting from the BEPS recommendations, such as country-by-country reporting and TP reporting

Legislative and Treaty Changes

• Almost 50% of respondents are anticipating significant legislative and treaty changes in their country as a result of the BEPS initiative

Results confirm the Global Tax Reset

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 47

Results confirm the Global Tax ResetDeloitte’s Global Multinational Survey

Strongly Agree AgreeNeutral DisagreeStrongly Disagree

There is increased media and political interest in tax in my country

Strongly Agree Agree

Neutral Disagree

My organization is concerned about increased media, political and activist group interest in tax

Strongly Agree AgreeNeutral DisagreeStrongly Disagree

The C-Suite and/or Board of Directors of my organization have enquired about the increased media and political activist group interest in tax

93% Agree

74% Agree

60% Agree

ResponsibleTax Agenda

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 48

Cross-border income flows increasingly disputed by the tax authorities

Lack of trust by tax authorities and the desire for a larger share of the “profit” pie is resulting in adjustments between all tax jurisdictions – not just between

high/low tax jurisdictions

High Taxed CountriesInterest

Royalties

Products

Services

Low Taxed Countries

Changes intax authorities

approach tointerpretation ofexisting tax law

and treaties

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 49

The bottom line

In an increasingly globalized digitalized world; what is the properamount of income that should be allocated between countries

for multinationals with cross border trade?

Changes intax authorities

approach tointerpretation ofexisting tax law

and treaties

Every country seems to want a bigger piece of the “profit” pie

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 50

Successfully navigating the Tax Reset

Category Practices Increased Actions Multinational Leading

External tax law/treaty modifications

• Tax law changes• Tax audit assessments• Treaty qualification standards• Government information exchanges• Anti-abuse rules• Penalties

• Avoid surprises/monitor, identify, and prioritize activities, including planning for effective dates

Multinational tax implications

• Broader income tax base• Withholding taxes• Controversy• Transfer Pricing APA’s• Transfer Pricing changes (more profit

splits)• Permanent establishments

• Planning needed for greater tax expense, uncertainty and emphasis on transfer pricing

Tax planning and reporting

• Alignment of business/tax structure• Substance/business purpose• Reporting and compliance• IT System modifications• Substantiation of intercompany

payments• Modifications to intercompany

arrangements (financing, royalty, value chain, etc.)

• Pressure testing existing structures, greater business tax alignment/ increased budgets and resources/reallocation of priorities, act on TP and CbC now

Stakeholder management

• Education/Communication to Top Management

• Agreement on risk profile• Risk management with Board/Audit

Committee• Public reporting • Financial accounting scrutiny • Tax department budget and

resources

• Proactive stakeholder communication/risk management and brand protection

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 51

Areas that multinationals should manage now

Intensive activity by tax authorities in many jurisdictions

• Manage audits and risk reviews• Dispute resolution (and perhaps litigation)

TP documentation • Update and strengthen documentation

Intercompany agreements • Develop or review agreements, to ensure related party transactions are appropriately documented

PE and residency • Develop or review guidelines to manage PE and residency risks

Substance

• Review- Compliance in practice with intercompany agreements, PE and residency

guidelines (is the business living the structure?)- Level of substance in holding companies, hubs, and similar entities

• Identify and correct weaknesses

Tax advantaged structures• Review and assess• Consider alternatives where appropriate

Financing• Deal with tightening of local and foreign interest deductibility rules (including

thin cap and anti-hybrid rules)• Consider options

Transparency • Deal with any new foreign disclosure requirements and media attention, where applicable

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 52

Areas that multinationals must prepare for

New TP principles for intangibles and risk

• Adapt existing structures to deal with new approaches by OECD and specific jurisdictions

Expansion of PE concept • Adapt existing structures to comply with new (anticipated) rules

Harmful tax practices and treaty abuse

• Evaluate substance in hubs and holding companies• Where necessary, restructure into more sustainable structure

- Consider operating companies as holding companies where necessary- Shut down haven or tax preferred entities with insufficient substance- Set up in locations where people functions can be established

More limits on financing• Evaluate impacts in affected countries• Restructure location of debt

Neutralisationof hybrids

• Unwind existing structures where there has been a legislative change• Develop and implement alternatives

Country-by-country reporting• Implement systems to collect and report required data

European CommissionAnti abuse program

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 54

Recent State Aid Headlines

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 55

State Aid concepts – Four criteria

State Aid

Intervention by the State or

through State resources

Giving rise to an advantage on a selective basis

Competition has been or may be

distorted

Intervention is likely to affect trade between Member States

1> <2

3> <4

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 56

Tax rulings – Selectivity

European Commission (“EC”) recently issued a white paper, which included a discussion of how Tax Rulings may be considered ‘selective’. Tax rulings confer a selective advantage if:

• The ruling misapplies national tax law and results in a lower amount of tax;

• The ruling is not available to undertakings in similar legal and factual situations; or

• The local tax administration applies a more favourable tax treatment compared with taxpayers in similar legal and factual situations

− For example, where the ruling allows a transfer pricing arrangement that is not at arm’s length

− For example, where the ruling allows for alternative, indirect methods of arriving at taxable income where more direct methods are available

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 57

State Aid – Specific challenges

European Commission (“EC”) in process of reviewing tax rulings obtained by certain MNEs to determine if rulings constitute Illegal State Aid and has

• Concluded Dutch ruling provided illegal state aid to Company A (10/21/15)*

• Concluded Luxembourg ruling provided illegal state aid to Company B (10/21/15)*

• Concluded Belgium rulings on Excess Profits provided illegal state aid to 35 companies (1/11/16)*

• Initiated investigation into whether the Irish government provided Company C with illegal state aid

• Initiated investigation into whether Luxembourg provided Company D and Company E with illegal state aid

• Indicated potential challenge to Company F (1/21/16)

In addition to cases above, EC is reported to be assessing facts of > 300 taxpayers

If EC finds member states provided rulings that constitute illegal state aid, EC has required member states to compute/charge MNEs for previously provided state aid

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 58

EU Anti-Tax Avoidance Directive

January 28, 2016Directive proposal

May 25, 2016ECOFIN meeting

June 17, 2016ECOFIN meeting

December 31, 2018 January 1, 2019 December 31, 2019 January 1, 2020

Deadline for EU Member States to transpose the Directive in their national laws for all provisions except for exit taxation

Provisions applicable (except for exit taxation)

Deadline for EU Member States to transpose the Directive in their national laws the provision for exit taxation

All provisions applicable

Set of legally binding anti-avoidance measures

Three measures linked to BEPS• Interest limitation• Hybrids• CFC rulesThree measures going beyond BEPS• General Anti-Avoidance Rule (GAAR)• Exit taxation• Switch-over clause

Failure to reach political agreement.

Disagreement on

• Scope of anti-hybrid rule (EU vs. non EU)

• Scope of CFC rules (EU vs. non EU/ substance requirement/ burden of proof)

• Switch-over clause (whether it should be included at all)

On 21 June 2016, further to the meeting of 17 June 2016, a political agreement was reached between all EU Member States after numerous discussions and changes to the original proposal

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 59

EU Anti-Tax Avoidance Directive

• Interest limitation: Interest charges exceeding interest revenues (and equivalent taxable revenues) would be deductible up to 30% of the taxpayer’s EBITA or up to EUR 3mio (whichever is higher)

• Exceptions (group-wide test/standalone entity)• Option for Member States to apply a carry-back or carry forward on exceeding interest cost.• Grandfather rule for loans concluded before 17 June 2016 if not subsequently modified

• Hybrid mismatches rules: Case whereby two EU Member States give a different characterization to the same taxpayer/instrument

• In cases of double deduction: deduction should occur only in the State of source of the payment• In case of deduction without inclusion: deduction should not be allowed

• Controlled foreign company income rules: Anti deferral tax measure whereby the tax base of a taxpayer would include the non-distributed income of an entity under conditions (basically where profits of this entity are not taxed or taxed at much lower rate than the country of the taxpayer)

• General anti-abuse rule: Case whereby non-genuine arrangements or a series thereof carried out for the essential purpose of obtaining a tax advantage that defeats the object or purpose of the otherwise applicable tax provisions shall be ignored for the purposes of calculating the corporate tax liability. Wording similar to the GAAR inserted in the Parent-Subsidiary Directive

• Exit taxation for cross-border transfer of assets, residence or business carried on by permanent establishment: Subject to four circumstances

• Tax base: Fair market value of the transferred assets, at the time of exit, less their value for tax purposes

• Deferral provision by paying in instalments over a 5 year period provided the assets/residence of a taxpayer’s head office/ permanent establishment are transferred to another European Member State or a third country that is party to the EEA Agreement

• Switch-over clause: Removed

Agreement 20 June 2016

Anti-Tax Avoidance Directive

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

ATAD in a nutshell

Anti-Tax Avoidanc

e Directive

Controlled Foreign Company Rules (inspired by BEPS Action 3)

Interest Restrictions (inspired by BEPS Action 4)

Hybrid Mismatches (inspired by BEPS Action 2)

Exit Taxation (not in OECD BEPS reports)

General Anti-Abuse Rule (not in OECD BEPS reports)

Member States should implement in national law by January 1, 2019(exit tax January 1, 2020).

61

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

“As these rules would have to fit in 28 separate corporate tax systems, they should be limited to general provisions and leave the implementation to member states as they are better placed to shape the specific elements of those rules in a way that fits best their corporate tax systems”

Source: Council of the European Union – Council Directive 2016/0011 (Anti-Tax Avoidance Directive)

A major step in BEPS implementation

Why a directive? What is a directive?

62

Presenter

Presentation Notes

Bill Dodwell Aart Nolten to make comment deviations due to different tax systems (in analogy with the VAT directive)

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

CFC rules

14 member states have CFC rules

Key characteristics:• Aimed at catching artificially diverted low-taxed (passive) income• >50% control test of companies or permanent establishments (PEs)• Rate Test: Company/PE taxed at <50% of effective tax rate in parent company member state. • Application to EU subsidiaries / PE?• EU member states must chose from two options: • Option 1 (objective test): − Passive income (interest, royalties, dividends, certain buy/sell co’s, etc)− Optional exclusion if income from defined categories is 33% or less;− Substance exemption (staff, equipment and premises)

• Option 2 (subjective test): − Nondistributed income of a CFC from nongenuine arrangements, which means that the CFC would not

own the assets or have taken the risk if it were not controlled by a company with the significant “people functions.”

63

Presenter

Presentation Notes

Bill Dodwell

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

EU HoldCo

Non-EU Company

Non-EU Company

US Parent

Non-EU CompanyLoan/license

Loan/license

20% rate

• 5% rate • No

substantial activities

• 0% rate• No substantial

activities

Non-EU Company Loan/license

Substantial activities

CFC income pickupCFC income pickup

X

X

CFC rules (cont.)

Examples of impacted structure: IP & Financing

64

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Non-EU Company

Goods

Goods

• 20% rate

• No substantial activities

• <10% rate

CFC income pickup

X

CFC rules (cont.)

Examples of impacted structure: PrincipalCo

EU HoldCo

Non-EU Company

Non-EU Company

US Parent

65

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Finance /IP

branch

Finance /IP

branch

• 20% rate

• <10% rate• No substantial

activities

• <10% rate• No

substantial activities

CFC income pickup CFC income pickup

X

X

CFC rules (cont.)

Examples of impacted structures: branches

EU HoldCo

US Parent

Non-EU Company

Non-EU Company

66

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

CFC rules: how will they impact companies

Recommendations and considerations

Recommendations:

• Review existing structure for potential CFC exposure• Monitor implementation of CFC rules by individual EU member states (local

implementation may differ) (ultimately by January 1, 2019)

Considerations:

• Add activities/functionality to CFC• Take passive activities out from under EU• Move passive activities into higher-taxed jurisdiction

67

Presenter

Presentation Notes

Bill Dodwell

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Key points:Fixed ratio• 30% of tax-based EBITDA—which must exclude tax-exempt income• Can calculate on group basis Group ratio• Income based or asset based Possible reliefs• Unlimited carryforward of capped interest• Three-year carryback of capped interest• Five year carryforward of excess capacity

Interest restrictions

EUR 3m deductible

Borrowing costs

Financing income

30% of tax-based EBITDA

deductible

68

Presenter

Presentation Notes

Bill Dodwell

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Optional exclusions• “Grandfathering” of pre-June 2016 loans• Long-term public infrastructure projects where lenders in EU• EUR 3 million de minimis level• Standalone companies, i.e. no associates• Financial sector• Conditional delay for interest rules until January 1, 2024 (or one full fiscal year after

the OECD reaches agreement as a minimum standard, whichever is earlier)

Interest restrictions (cont.)

69

Presenter

Presentation Notes

Bill Dodwell Bill to mention UK position at the end of this slide and Aart to comment on impact in The Netherlands and several other countries.

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Interest restrictions: impact

Recommendations and considerations

• Illustration of expected change

Grandfathered loan

• Under leveraged

• Over leveraged

• >30% EBIDTA

LoanLoan

US Parent

EU Company

EU Company

EU Company

• Over leveraged• >30% EBIDTA

FinCo

Consider transfer

• Review impact based on projected tax-based EBITDA capacity and projected interest cost

• Identify and “do not touch” existing loans that are potentially grandfathered• Monitor implementation of interest restrictions by individual EU member states (local

implementation may differ)• Consider rebalancing between locations with over- and undercapacity. Consider other

local interest deductibility rules when rebalancing.

70

Presenter

Presentation Notes

Bill Dodwell Bill to mention UK position at the end of this slide and Aart to comment on impact in The Netherlands and several other countries.

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

Anti-Hybrid rule restricted to EU mismatchesProposal for hybrid mismatch rules with third countries before the end of 2016?No imported mismatch & no hybrid branch clauses in hybrid mismatch rules, but EU member states may decide to implement imported mismatch rules unilaterally (e.g. UK)

Hybrid mismatches

EU Company

US Parent

Hybrid instrument

Reverse hybrid

Loan/license

EU Company

US Parent

Note: Watch imported mismatch rules

EU Hybrid Entity

EU Company

EU Parent

Loan/license

No deduction

Example EU hybrid: Examples non-EU hybrid (not in ATAD):

71

Presenter

Presentation Notes

Bill Dodwell Aart Nolten at the end of the slide to comment hybrid mismatch to 3rd countries and impact.

Tax Talent Development FOR INTERNAL USE ONLY © 2016 Deloitte Development LLC. All rights reserved.

EU HoldCo

US Parent

EU HoldCo

US Parent

Transfer tax residence to other country (where step up to FMV in assets is obtained)

Branch

Transfer IP

Illustration of expected change

Exit Taxation

Countries will be forced to tax in two circumstances (in short):• Asset or business transfer to/from head

office to a PE• A taxpayer transfers its tax residence

Calculate gain and offer five-year installments, with interest + guarantee

Triggers immediate payment if assets/business/company sold

72

Transfer PricingIntellectual Property

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 74

Intellectual Property planningBEPS Action 8

Contractual relationships between parties are a starting point for any transfer pricing analysis

Location where important functions related to intangible assetsare performed is key

Members of the group should be compensated for functions performed, assets used and risks assumed in the development, enhancement, maintenance, protection, and exploitation of intangibles

If legal owner does not control or perform functions related to development, enhancement, maintenance, protection or exploitation,it will not be entitled to ongoing benefit attributable to outsourced functions

Tax authorities already applying new guidance

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 75

Intellectual Property planningBEPS Action 8 (cont.)

Emphasis on functions performed, assets used and risk incurred

Transfer pricing outcomes in line with value creation

Identify legal owner

Identify party performing important functions

Confirm conduct of the

parties consistent with

contracts

Identify the controlled

transaction related to the

important functions

Determine the arm’s length price for the important functions

Design and control of research and

marketing programs

Management and control of budgets

Control over strategic decisions

over intangible development

Important decisions regarding

defense and protection

Ongoing quality control

Steps in determining intangible returns

Important functions

EnhancementDevelopment Maintenance Protection Exploitation

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 76

Substance requirement post-BEPS

To be entitled to IP returnMust control operational risks

• Operation means: Development, enhancement, maintenance, protection, exploitation (aka DEMPE functions)

• Thus IP return has shifted from financial capital to people functions

− Financial capital gets a projected risk-free return or a risk-adjusted return

− The OECD has not agreed on what to do with actual returns (who gets the unanticipated upsides)

Controlling operational risks requires for each operational riskIn-location people that

• Are qualified, have decision-making authority, demonstrate in-location exercise of decision-making authority as it relates to risk mitigation

• No in-location white lab coat requirement or headcount requirement

Board meetings are no longer sufficient

Setting procedures and policies no longer sufficient

Transparency

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 78

Automatic Exchange of Information

Rulings

• Developed a framework for compulsory spontaneous information exchange between governments in respect of taxpayer-specific rulings – should apply where the absence of an exchange of a ruling may give rise to BEPS concerns

• Framework details six types of ruling that will be subject to such exchange

• A ruling is defined widely as “any advice, information or undertaking” that a tax authority gives to a specific company or group on which reliance can be placed

• Companies need to be aware that rulings obtained in one country will be shared with other tax authorities

Country-by-country reporting

• Model legislation requires the ultimate parent entity of an multinational group to file the country-by-country report in its jurisdiction of residence, including backup filing requirements when that jurisdiction does not require filing

• The package also contains model agreements to facilitate the exchange of country-by-country reports among tax administrations

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 79

BEPS Action 13 recommendations

BEPS Action 13 proposes a new three tier global standard for transfer pricing documentation. The text in green represents additional information required under the new documentation model as compared to current OECD guidelines.

Evolution of existing transfer pricing documentation requirements

• Group wide description including supply chain, value drivers, main markets, high level functional analysis, details of business changes

• High level description of IP strategies, IP location and R&D management and location

• High level description of group financing arrangements

• Consolidated group accounts

• Description of APAs or other rulings

Transactional/Entity specific

• Local management structure, detailed functional analysis, economic analysis and reconciliations of TP to accounts

• Local documentation nuances continue?

A new requirement

• Revenue

• Profit before tax

• Cash tax paid

• Current Tax accrual

• Capital and retained earnings

• NBV of tangible assets

• Number of employees

• Complete list of entities and PE’s for each country, with activity codes to be attached to template

Master file Local file Country-by-country template

ObjectivesEnsure consideration of transfer pricing requirements

Transfer pricing risk assessment Transfer pricing audit

Questions?

Please remember to complete your evaluation

The Global Tax Reset and BEPSCopyright © 2016 Deloitte Development LLC. All rights reserved. 84

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates and related entities, shall not be responsible for any loss sustained by any person who relies on this presentation.

85Copyright © 2016 Deloitte Development LLC. All rights reserved.

Revenue Recognition

86Copyright © 2016 Deloitte Development LLC. All rights reserved.

Objectives

• Recognize the scope of the new standard

• Recognize the principles for recognizing revenue and capitalizing costs, and the disclosure requirements

• Identify areas that require professional judgment when adopting the new standard

• Recognize the implementation challenges entities may encounter

87Copyright © 2016 Deloitte Development LLC. All rights reserved.

Goals of the new standard

Convergence of revenue recognition principles under U.S. GAAP and IFRS

Improve revenue recognition requirements and disclosures by…

Removing inconsistencies

Providing amore robust framework

Improvingcomparability

Providing moreuseful

information

Eliminatingindustry-specific

guidance

88Copyright © 2016 Deloitte Development LLC. All rights reserved.

Effective Date

• In August 2015, the Financial Accounting Standards Board (“FASB”) issued an ASUthat defers the effective date of Accounting Standards Codification (“ASC”) 606 byone year.

—Annual reporting periods beginning after December 15, 2017 (public)

—Annual reporting periods beginning after December 15, 2018 (nonpublic)

• Additionally, the ASU allows entities to early adopt ASC 606 as of the original effective date (annual reporting periods beginning after 12/15/16, FY2017).

• In September 2015, the International Accounting Standards Board (“IASB”) issued anamendment to International Financial Reporting Standard (“IFRS”) 15 in order to defer the effective date by one year.

—Annual reporting periods beginning on or after January 1, 2018

• The IASB continues to allow entities to early adopt IFRS 15.

89Copyright © 2016 Deloitte Development LLC. All rights reserved.

New revenue guidance Standard setting activity

Issue Status

2014-09 Revenue from Contracts with Customers Final ASU issued May 28, 2014

2015-14 Effective Date Delay (deferral for one year) Final ASU issued August 12, 2015

2016-12 Narrow-Scope Improvements and Practical Expedients (collectibility, contract modification in transaction, sales tax practical expedient, transition disclosures, non-cash consideration)

Final ASU issued May 9, 2016

2016-10 Identifying Performance Obligations andLicensing (clarify guidance on identifyingperformance obligations and recognizinglicense revenue)

Final ASU issued April 14, 2016

2016-08 Principal Versus Agent (clarifying application of the guidance)

Final ASU issued March 17, 2016

2016-XX Technical Corrections (minor amendments and clarifications)

Exposure draft expected soon.

90Copyright © 2016 Deloitte Development LLC. All rights reserved.

Full retrospective approach

• Restate prior periods in compliance with ASC 250

• Optional practical expedients

Modified retrospective approach

• Apply revenue standard to contracts not completed as of effective date and record cumulative catch-up

• Required disclosures:

—Amount of each F/S line item affected in current period

—Explanation of significant changescumulative catch-up

Transition Methods

Existing contracts New ASU + cumulative catch-up

Legacy GAAP Legacy GAAP

UPDATEPractical expedient for contract modifications

(FASB & IASB)

January 1, 2018 Initial Application Year

2018Current Year

2017 2016Prior Year 1 Prior Year 2

New contracts New ASU

Completed contracts Legacy GAAP Legacy GAAP

91Copyright © 2016 Deloitte Development LLC. All rights reserved.

New Revenue GuidanceSecurities and Exchange Commission

Five-year table

At the September 2014 Financial Accounting Standards Advisory Council (FASAC) meeting, the SEC staffclarified its views on how registrants would reflect their implementation of ASC 606 in the five-year tablerequired under SEC Regulation S-K, Item 301

• The staff indicated that it would not object if a registrant reflected its adoption of the new revenue standard in the five-year table on a basis that is consistent with the adoption in its financial statements (i.e., reflected in less than each of the five years in the table)

• A registrant could present in the five-year table:

—Only the most recent three years if the registrant uses the full retrospective method to adopt the new revenue standard

—Only the most recent fiscal year if it uses the modified transition basis

Regardless of the transition method adopted, registrants would be expected to disclose the method they used to reflect the information (e.g., how the periods are affected) and that the periods are not comparable

92Copyright © 2016 Deloitte Development LLC. All rights reserved.

Scope of the New Revenue Standard

• Applies to an entity’s contracts with customers

• Does not apply to:

—Lease contracts (ASC 840, ASC 842)

—Insurance contracts (ASC 944)

—Certain financial instruments and other contractual rights or obligations

—Guarantees (other than product or service warranties)

—Nonmonetary exchanges whose purpose is to facilitate a sale to another party

• Some key aspects apply to transfer (sale) of nonfinancial assets

Glossary termsContract: An agreement between two or more parties that creates enforceable rights and obligationsCustomer: A party that has contracted with an entity to obtain goods or services that are an output of the entity’s ordinary activities in exchange for consideration

93Copyright © 2016 Deloitte Development LLC. All rights reserved.

New Revenue Standard The five-step model

Copyright © 2016 Deloitte Development LLC. All rights reserved. Revenue Recognition 90

Identify the contract with a customer

(Step 1)

Identify the performance obligations in the contract

(Step 2)

Determine the transaction

price(Step 3)

Allocate the transaction

price toperformance obligations

(Step 4)

Recognize revenue when

(or as) the entity

satisfies a performance

obligation(Step 5)

Core principle: Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration the entity expects to be entitled in exchange for those goods or services

This revenue recognition model is based on a control approach, which differs from the risks and rewards approach applied under current U.S. GAAP

94Copyright © 2016 Deloitte Development LLC. All rights reserved.

Step 1: Identifying the Contract

A legally enforceable contract (oral or implied) must meet all of the following requirements:

A contract will not be in the scope if:

The contract has commercial substance

The parties have approved the contract and are committed to perform

The entity can identify each party’s rights regarding goods or services

The entity can identify the payment terms for the goods or services to be

transferred

The contract is wholly unperformed Each party can unilaterally terminate the contract without compensation

Step1

Step2

Step3

Step4

Step5

It is probable the entity will collect the consideration to which it will be entitled in exchange for the goods or services

that will be transferred to the customer

AND

Criteria impacted by ASU 2016-12

Collectibility threshold

95Copyright © 2016 Deloitte Development LLC. All rights reserved.

Combining Contracts

Combining Requirement

In most cases, entities will apply the model to individual contracts with a customer.However, the new standard requires entities to combine contracts entered into at or near the same time with the same customer if they meet one or more of the criteriaindicated below:

a. The contracts are negotiated as a package with a single commercial objective.

b. The amount of consideration to be paid in one contract depends on the price or performance of the other contract.

c. The goods or services promised in the contracts (or some goods or servicespromised in each of the contracts) are a single performance obligation

96Copyright © 2016 Deloitte Development LLC. All rights reserved.

Portfolio Approach

Portfolio Approach

• Although in general the standard should be applied on an individual-contract basis, a“portfolio approach” is permitted if it is reasonably expected that the approach’s impact onthe financial statements will not be materially different from the impact of applying the revenue standard on an individual-contract basis.

—Entities with a very large number of customer contracts or a wide array of productcombination options will likely use this approach

—A portfolio approach would be appropriate only if

—It is applied to a group of contracts (or performance obligations) with “similarcharacteristics” and

—The entity “reasonably expects” that the effects on the financial statements ofapplying the standard to the portfolio “would not differ materially” from the effects ofapplying guidance to the individual contracts (or performance obligations) in thatportfolio.

97Copyright © 2016 Deloitte Development LLC. All rights reserved.

The ASU defines a performance obligation as a promise to transfer to the customer a good or service (or a bundle of goods or services) that is distinct

Identify all (explicit or implicit) promised goods and services in the contract

Step 2: Identifying Performance Obligations

Are promised goods and services distinct from other goods and services in the contract?

Capable of Being Distinct Distinct Within Context of Contract

Can the customer benefit from the good or service on its own or

together with other readily available resources?

Is the good or service separatelyidentifiable from other promises

in the contract?

AND

Account for as a performance obligation

Combine 2 or more promised goods or services and reevaluate

YES NO

Step1

Step2

Step3

Step4

Step5

Impacted byASU 2016-10

A series of goods or services with the same pattern of transfer may

be a single obligation

98Copyright © 2016 Deloitte Development LLC. All rights reserved.

Identifying Performance Obligations Why was the ASU 2016-10 issued?

The following implementation questions submitted to the TRG informed the Board about certain concerns with the guidance on identifying performance obligations:

Identifying Performance Obligations

a. Whether a promise is separately identifiable, and whether the good or service is “distinctwithin the context of the contract” (which is one of the criteria required to separatelyaccount for the good or service)

b. Whether shipping and handling activities should be consider a separate performance obligation.

c. When identifying performance obligations, whether it is necessary to identify and evaluatepromised goods or services that are immaterial

99Copyright © 2016 Deloitte Development LLC. All rights reserved.

Identifying Performance Obligations

Distinct goods or services

The ASU clarifies the meaning of a promise that is separately identifiable.

• Objective is to determine whether the nature of the entity’s overall promise is to:

—Transfer each of those goods or services (multiple performance obligations) or

—Transfer a combined item or items to which the promised goods or services are inputs (one combined performance obligation)

• Factors that indicate that two or more promises to transfer goods or services to acustomer are not separately identifiable include, but are not limited to, thefollowing:

a. Performing a significant service of integrating

b. Significantly modification or customization

c. The goods or services are highly interdependent or highly interrelated

The ASU amended and added examples to the standard’s implementation guidance to clarify these principles.

100Copyright © 2016 Deloitte Development LLC. All rights reserved.

Identifying Performance Obligations

Shipping and handling services

Implementation questions arose regarding whether shipping would need to be considereda performance obligation.

The ASU adds guidance that clarifies when shipping and handling activities occur:

• Before control transfers to the customer, they are fulfillment costs

• After control transfers, entities are allowed to elect a policy to treat shipping andhandling activities as fulfillment costs

If revenue is recognized before contractually-agreed shipping and handling activities occur,the related costs of those activities should be accrued.

101Copyright © 2016 Deloitte Development LLC. All rights reserved.

Identifying Performance Obligations

Options to acquire additional goods and services

• Represents a performance obligation (requiring the deferral of revenue) if it provides amaterial right that would not have been received without entering into that contract:

— incremental discounts on additional goods/services

— favorable renewal options on services

102Copyright © 2016 Deloitte Development LLC. All rights reserved.

Identifying Performance Obligations

Warranties

• Assurance warranties (those that assure compliance with agreed-upon specifications) use a cost accrual accounting model

• An option to purchase or those warranties that provide a service in addition to agreed-upon specification would be a potential performance obligation

Upfront fees

• An entity should assess whether the fee relates to the transfer of a promised good orservice.

• An upfront fee is often an advance payment for future goods or services and,therefore, would be recognized as revenue when those future goods or services are provided.

• Generally, recognize advance payments when future good or services are provided (maybe beyond initial contract term).

103Copyright © 2016 Deloitte Development LLC. All rights reserved.

Step 3: Determining Transaction Price

Transaction price shall include…

• Fixed consideration

• Variable consideration (estimated and potentially constrained)

• Noncash consideration (FASB updates)

• Adjustments for significant financing component (practicalexpedient available)

• Adjustments for consideration payable to customer

Transaction price does NOT include…

• Effects of customer credit risk

Principle: The transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer (which excludes estimates of variable consideration that are constrained)

Step1

Step2

Step3

Step4

Step5

104Copyright © 2016 Deloitte Development LLC. All rights reserved.

When accounting for variable consideration an entity shall…

• Estimate using following methods:

1) expected value (probability weighted)

or

2) most likely amount

Variable consideration should include revenue to the extent that it is “probable” that asignificant reversal in the amount of cumulative revenue recognized will not occur (i.e.“constraint”)

Factors to consider:

• Highly susceptible to factors outside entity’s influence

• Uncertainty not expected to be resolved for a long time

• Entity’s experience is limited

• Entity typically offers broad range of price concessions/payment terms and large numberof broad range possible outcomes

Determining Transaction Price

Need to consider whether adjustments are for

concessions or credit risk

105Copyright © 2016 Deloitte Development LLC. All rights reserved.

Determining Transaction Price

When accounting for consideration payable to the customer:

• Account for consideration payable to a customer as a reduction of the transactionprice and, therefore, of revenue unless the payment to the customer is in exchangefor a distinct good or service that the customer transfers to the entity and paymentis at fair value.

• If the consideration payable to a customer includes a variable amount, it’s aform of variable consideration that is subject to the constraint.

106Copyright © 2016 Deloitte Development LLC. All rights reserved.

Narrow-scope improvements & practical expedients Sales taxesand noncash transactions

Presentation of Sales Taxes and Other Similar Taxes

• The ASU provides entities with a policy election to exclude amounts collected fromcustomers for sales taxes from the transaction price (i.e. report sales tax on a net basis) without applying the principal/agent guidance.

• Gross reporting of sales taxes or other similar taxes is only appropriate if an entity isthe principle for such taxes under the principal/agent guidance.

Noncash transactions

• ASC 606 stated that noncash consideration should be measured at fair value but didnot provide clear guidance on when to measure consideration.

• The ASU amends ASC 606 to clarify that…

—noncash consideration should be measured at contract inception

—variable consideration guidance only applies to variability resulting from reasonsother than the form of the consideration (i.e., the constraint would not apply tovariability due to the form of the consideration)

107Copyright © 2016 Deloitte Development LLC. All rights reserved.

Step1

Step2

Step3

Step4

Step5

Allocate transaction price on a relative stand-alone selling price basis (estimatestand-alone selling price if not observable)

• The expected cost-plus margin method, adjusted market assessment method, or residual method (only if price is highly variable or uncertain) are acceptable

Allocate transaction price to all performance obligations (and subsequent changesbased on initial allocation), unless a portion of (or changes in) the transaction pricerelate entirely to one or more obligations and certain criteria are met

Do not reallocate for changes in stand-alone selling prices

If certain criteria are met, a discount or variable consideration may be allocated toone or more, but not all, of the performance obligations in a contract

Step 4: Allocating Transaction Price

108Copyright © 2016 Deloitte Development LLC. All rights reserved.

Evaluate if control of a good or service transfers over time, if not then controltransfers at a point in time. An entity satisfies a performance obligation over time if…

Measure progress toward completion using input/output methods

Step 5: Recognizing Revenue

Performance does not create an asset with an alternative use and the entity has an enforceable right to payment for performance completed to date

Performance creates or enhances a customer controlled asset (e.g., home addition)

The customer receives and consumes the benefit as the entity performs (e.g., cleaning service)

Step1

Step2

Step3

Step4

Step5

OR

OR

109Copyright © 2016 Deloitte Development LLC. All rights reserved.

Point in time

For performance obligations satisfied at a point in time, indicators that control transfersinclude, but are not limited to, the following:

The entity has a present right to payment

The customer has legal title

The entity has transferred physical possession

The customer has the significant risks and rewards of ownership

The customer has accepted the asset

Step1

Step2

Step3

Step Step4 5

Recognizing Revenue

110Copyright © 2016 Deloitte Development LLC. All rights reserved.

Licensing

• Significant standalone functionality

• Recognized at a point in time

• Software, biological compounds or drugformulas, completed media content

Functional(right to use, typically)

• Does not have standalone functionality

• Entity provides both a right to intellectual property AND support and maintenance for the intellectual property

• Revenue is recognized over time.

• Examples include brands, trade names, logos,franchise rights

Symbolic (right to access)

Sales or Usage based Royalty

Notwithstanding the above, if consideration is paid in the form of a sales-based or usage-based royalty promised in exchange for a license of intellectual property,revenue should be recognized at the later of when the subsequent sale or usageoccurs or the performance obligation has been satisfied or partially satisfied.

111Copyright © 2016 Deloitte Development LLC. All rights reserved.

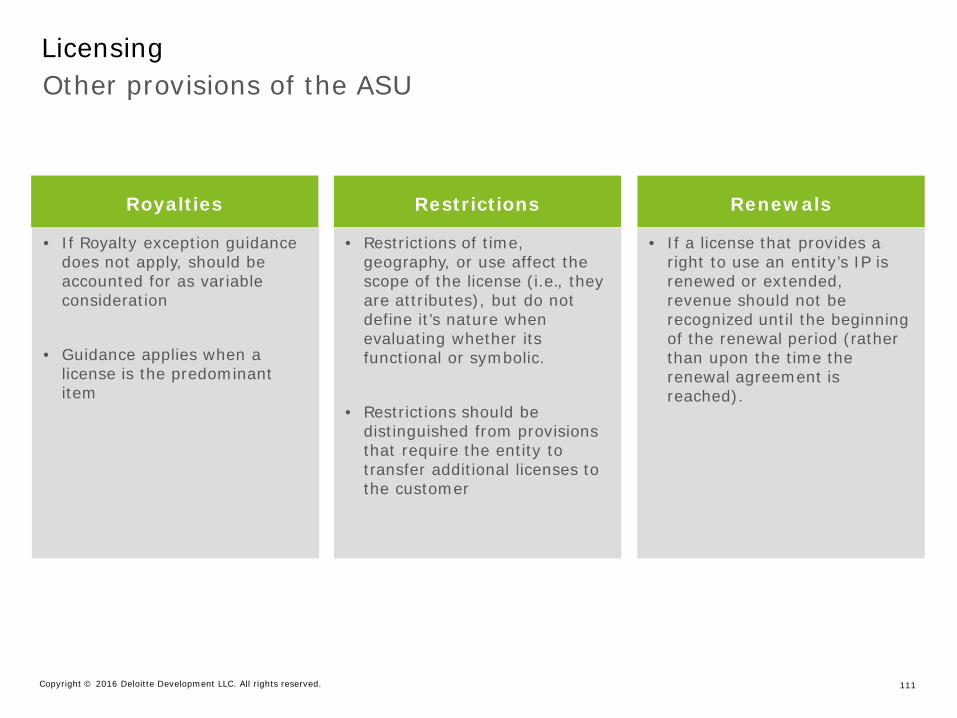

LicensingOther provisions of the ASU

• If Royalty exception guidance does not apply, should be accounted for as variable consideration

• Guidance applies when a license is the predominant item

Royalties

• Restrictions of time, geography, or use affect the scope of the license (i.e., they are attributes), but do not define it’s nature when evaluating whether its functional or symbolic.

• Restrictions should be distinguished from provisions that require the entity to transfer additional licenses to the customer

Restrictions

• If a license that provides a right to use an entity’s IP is renewed or extended, revenue should not be recognized until the beginning of the renewal period (rather than upon the time the renewal agreement is reached).

Renewals

112Copyright © 2016 Deloitte Development LLC. All rights reserved.

Contract Costs

Costs to obtain a contract

• Capitalize costs of obtaining a contract if they are incremental and expected to be recovered (e.g., sales commissions)

—One-year practical expedient

Costs to fulfill a contract

• Recognize assets in accordance with other Topics (e.g., inventory, PP&E, software), otherwise capitalize costs that:

—Relate directly to the contract (or specific anticipated contract

—Generate/enhance a resource that will be used to satisfy obligations in the future and

—Are expected to be recovered

• Costs that relate to satisfied performance obligations (or partially satisfied performance obligations) must be expensed when incurred

Amortization and impairment

• Capitalized costs are amortized on a systematic basis consistent with the transfer of the related goods or services

• Recognize impairment immediately if costs are not deemed recoverable

113Copyright © 2016 Deloitte Development LLC. All rights reserved.

Potentially Capitalized

• Direct labor• Direct materials• Costs explicitly chargeable to the

customer• Payments to subcontractors

Expensed as Incurred

• General & administrative costs• Cost of wasted materials• Costs related to satisfied or partially

satisfied performance obligations (prior performance)

Contract Costs

114Copyright © 2016 Deloitte Development LLC. All rights reserved.

Principal versus agent considerationsA practical approach to applying the ASU 2016-08

1. Identify each specified good/service to be provided to the customer

• Not the same as a performance obligation

2. Assess whether the entity controls each specified good/service before it istransferred to the customer

• Several indicators are included in the ASU to assist in the determination of control

Assessing whether the entity controls the specified good or service before it is transferred to the customer determines whether the it is a principal or an agent

115Copyright © 2016 Deloitte Development LLC. All rights reserved.

Principal versus agent considerations Application of the control principle

Control

Inventory Risk

Responsibility for providing the good or service

Latitude in establishing price

116Copyright © 2016 Deloitte Development LLC. All rights reserved.

Recap of ASU’s

• Collectibility

• Sales tax presentation (gross v. net)

• Noncash consideration

• Completed contracts

• Technical Correction – change in accounting principle

• Distinct in the context of contract

•

•Immaterial promised goods and services

Shipping and handling services

Narrow Scope Improvements

Identifying Performance Obligations

Licensing

• Licenses – functional v. symbolic

• Sales- or usage-based royalty exception to constraint guidance

• Impact of restrictions in a license

• Renewals of license

• Unit of account for assessment

• Nature of goods or services

• Applying the control principle

• Interaction of control principle with the indicators

Principal vs. Agent Considerations

117Copyright © 2016 Deloitte Development LLC. All rights reserved.

Other Guidance

Sale with a right of return

• Not a performance obligation but do not recognize revenue for goods expected to be returned

• For consideration paid that the entity does not expect to be entitled, recognize a refundliability and asset to recover products from customers

Consignment arrangements

• Control typically passes to other party (dealer or distributor) when that party sells productto customer or specified period expires

118Copyright © 2016 Deloitte Development LLC. All rights reserved.

Other Guidance

Repurchase agreements

• If entity has an obligation or right to repurchase the asset, the customer does notobtain control and is accounted for as a lease (ASC 840) or a financing arrangement

Bill-and-hold arrangements

• Evaluate if control has passed to customer (specific criteria provided, similar to current requirements)

• Must consider whether additional performance obligations exist subsequent to transfer ofcontrol to customer (for example, for custodial services) and, if so, allocate a portion of thetransaction price to those performance obligations

Customer acceptance clauses

• Entity is able to assert control has transferred if entity can objectively determine good or service meets agreed upon specifications

—If unable to do so, entity must wait for customer acceptance to conclude control hastransferred

119Copyright © 2016 Deloitte Development LLC. All rights reserved.

Disclosures Overview

Disaggregation of revenue

Information about contract

balances

Information about

performance obligations

Description of significant judgments

Transaction price, allocation

methods and assumptions

Remaining performance obligations

Annual Disclosures (ASC 606 & IFRS 15)

ASC 270,Interim

Reporting

Interim Only Disclosures

IAS 34,Interim Financial

Reporting*