Scottish Seafood Partnership “Challenges & opportunities facing the seafood sector” Libby...

21

Scottish Seafood Partnership “Challenges & opportunities facing the seafood sector” Libby Woodhatch, CEO, Seafood Scotland 3 May 2012

-

Upload

neal-august-chandler -

Category

Documents

-

view

224 -

download

1

Transcript of Scottish Seafood Partnership “Challenges & opportunities facing the seafood sector” Libby...

Scottish Seafood Partnership

“Challenges & opportunities facing the seafood sector”

Libby Woodhatch, CEO, Seafood Scotland 3 May 2012

Agenda

Introduction Challenges & opportunities in the seafood processing

sector Exploiting opportunities

2

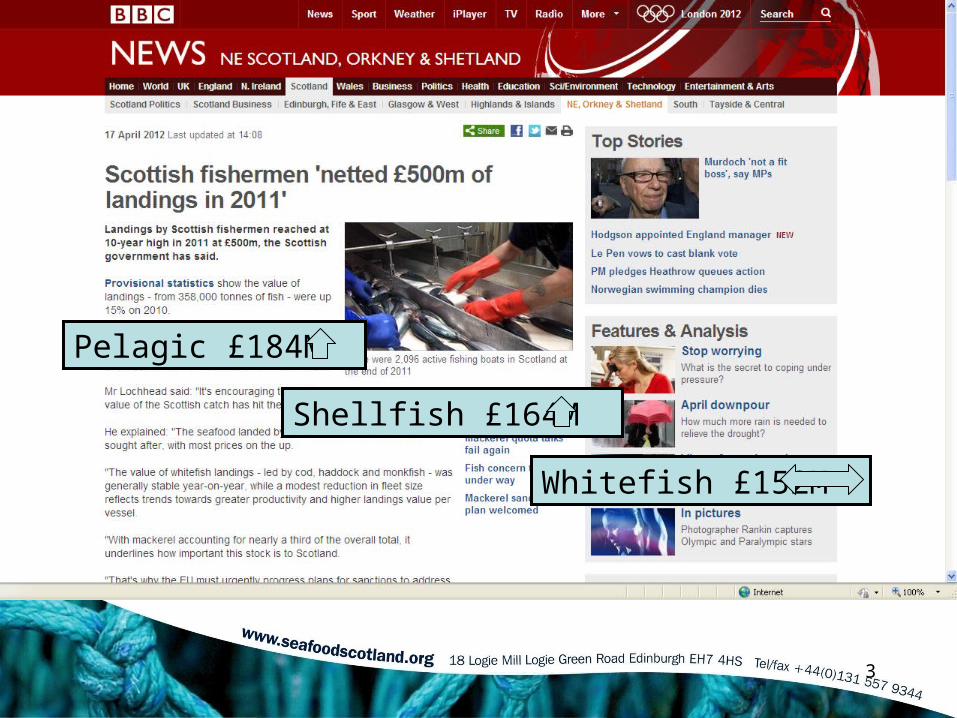

3

Pelagic £184M

Shellfish £164M

Whitefish £152M

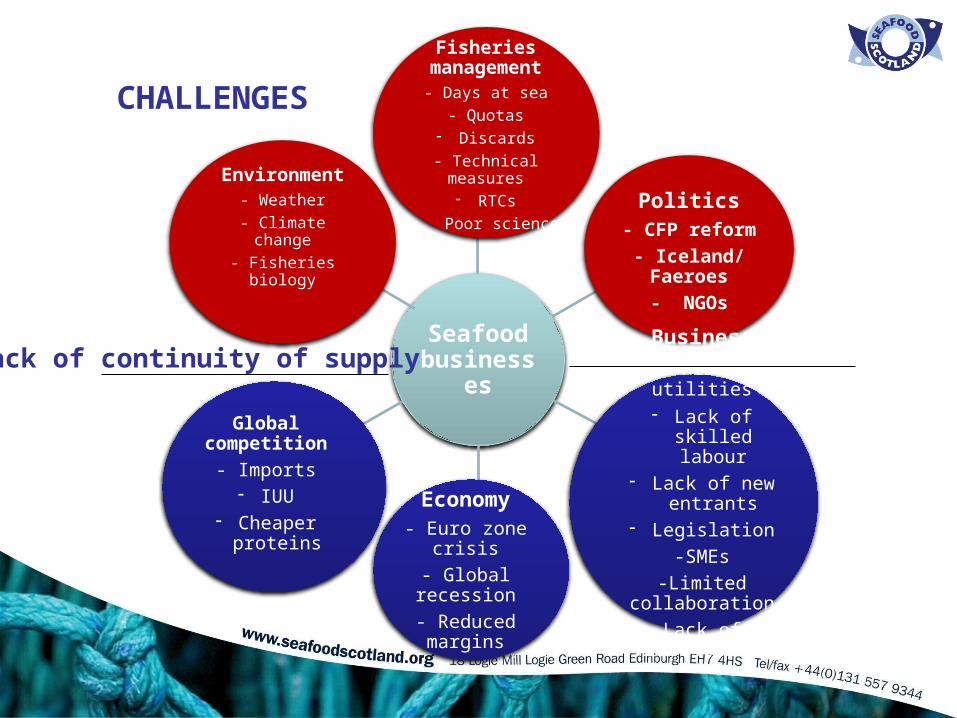

Seafood businesses

Fisheries management

- Days at sea- Quotas

- Discards- Technical measures

- RTCs- Poor science Politics

- CFP reform- Iceland/ Faeroes

- NGOs

Business- Rising utilities- Lack of skilled

labour- Lack of new

entrants- Legislation

-SMEs-Limited collaboration

Lack of investment

Economy- Euro zone crisis- Global recession

- Reduced margins

Global competition- Imports- IUU

- Cheaper proteins

Environment- Weather

- Climate change- Fisheries biology

Lack of continuity of supply

CHALLENGES

5

Mixed messages…………….

Whitefish – key issues• Fisheries management regime

– Adverse impacts from Cod recovery measures• Cost of leasing quota• Lack of foresight on landings• New control regulation on weighing• Haddock – size profile limiting• Fragmented industry

– Limited collaboration– SMEs

• Transport surcharges• Competition from Norway

6

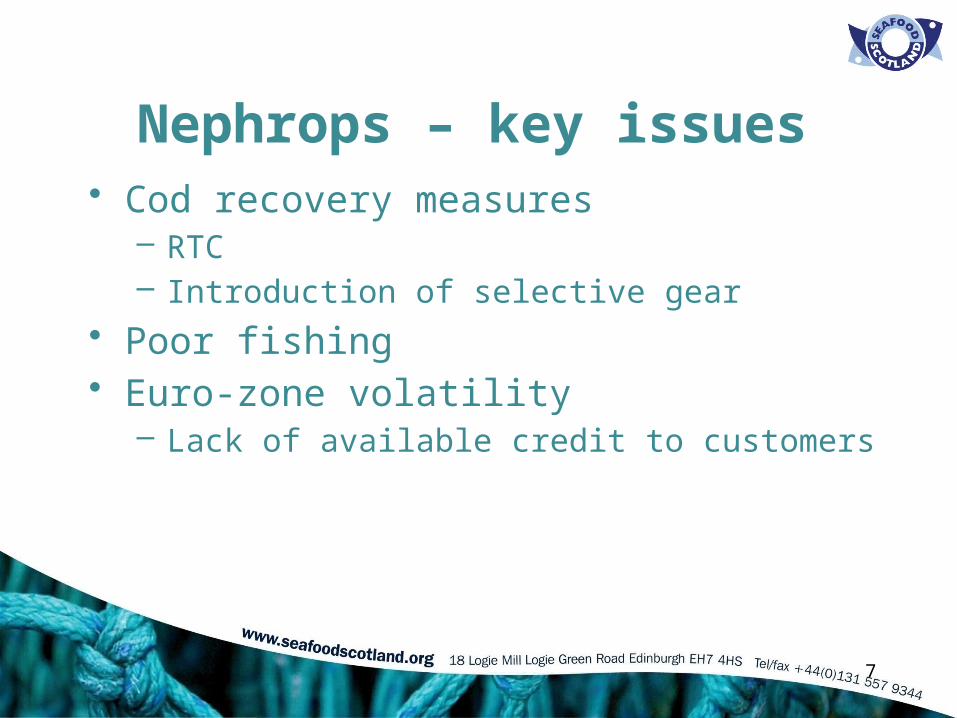

Nephrops – key issues• Cod recovery measures

– RTC– Introduction of selective gear

• Poor fishing• Euro-zone volatility

– Lack of available credit to customers

7

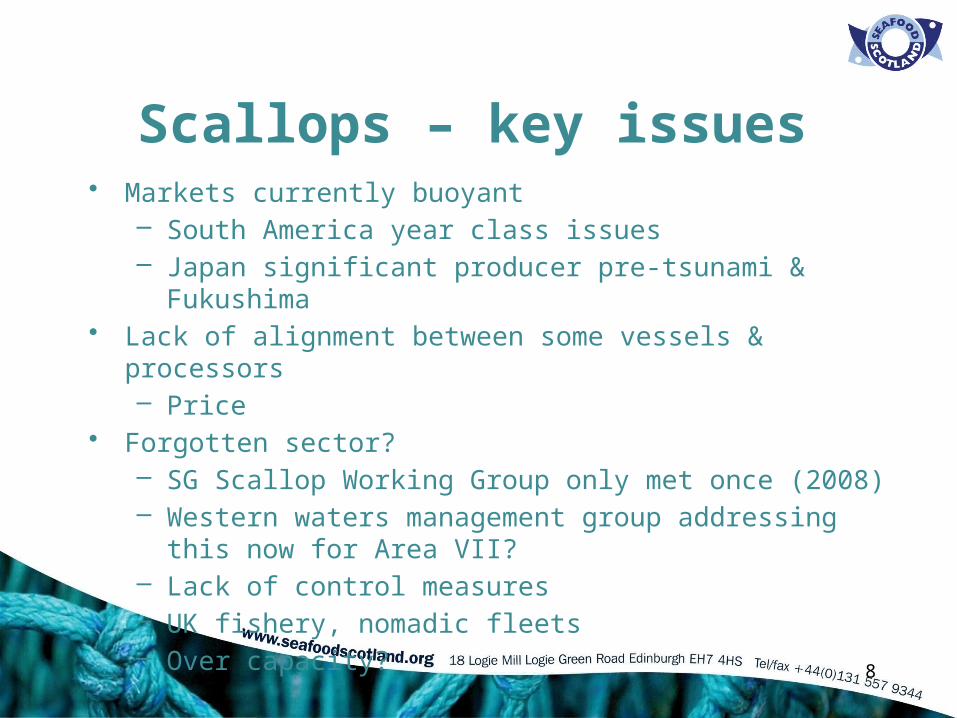

Scallops – key issues• Markets currently buoyant

– South America year class issues– Japan significant producer pre-tsunami & Fukushima

• Lack of alignment between some vessels & processors– Price

• Forgotten sector?– SG Scallop Working Group only met once (2008)– Western waters management group addressing this now for Area

VII?– Lack of control measures – UK fishery, nomadic fleets– Over capacity?

8

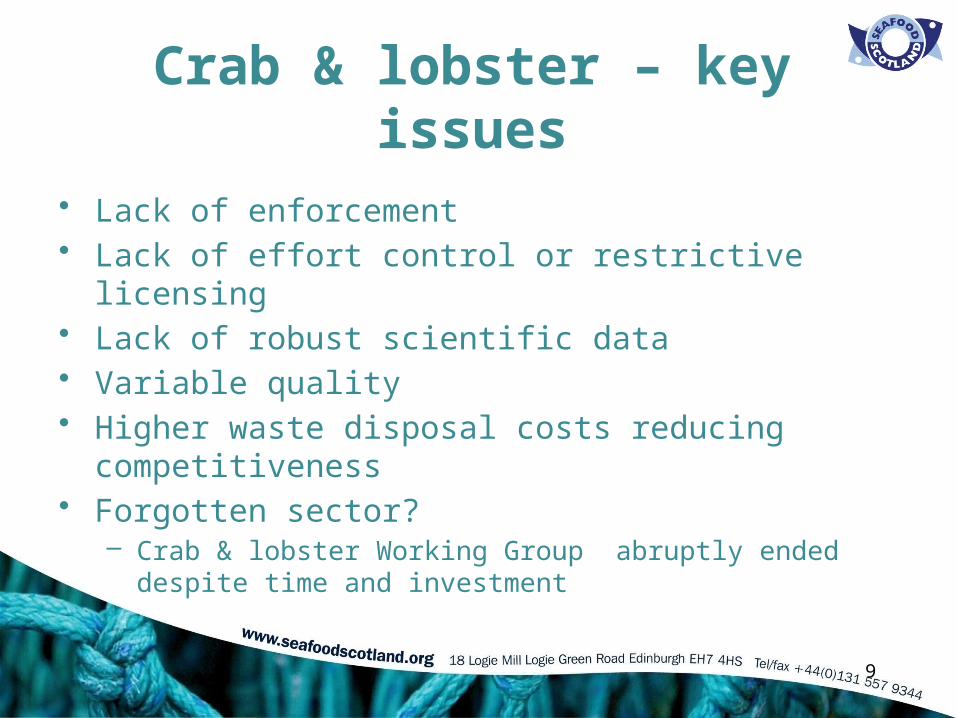

Crab & lobster – key issues

• Lack of enforcement• Lack of effort control or restrictive licensing • Lack of robust scientific data• Variable quality• Higher waste disposal costs reducing competitiveness• Forgotten sector?

– Crab & lobster Working Group abruptly ended despite time and investment

9

Pelagics – key issues• Iceland & Faroese situation

– Continuing loss of market share– Suspension of MSC accreditation– Future loss of quota?

• Limited supplies, short seasons• Norwegian competition

– Scottish vessels landing in to Norway– Market perception– IPR support for UK companies limited

10

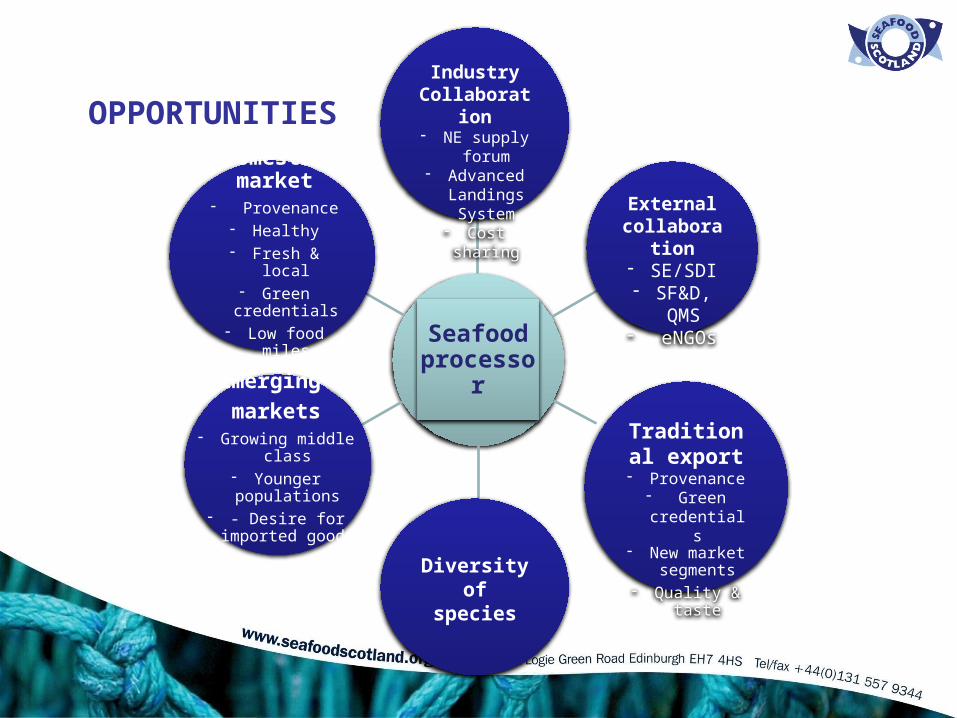

Seafood processor

Industry Collaboration- NE supply

forum- Advanced

Landings System

- Cost sharing External collaboration

- SE/SDI- SF&D,

QMS- eNGOs

Traditional export

- Provenance- Green

credentials- New market

segments- Quality & tasteDiversity of

species

Emerging markets

- Growing middle class- Younger populations- - Desire for imported

goods

Domestic market

- Provenance- Healthy

- Fresh & local- Green credentials- Low food miles

OPPORTUNITIES

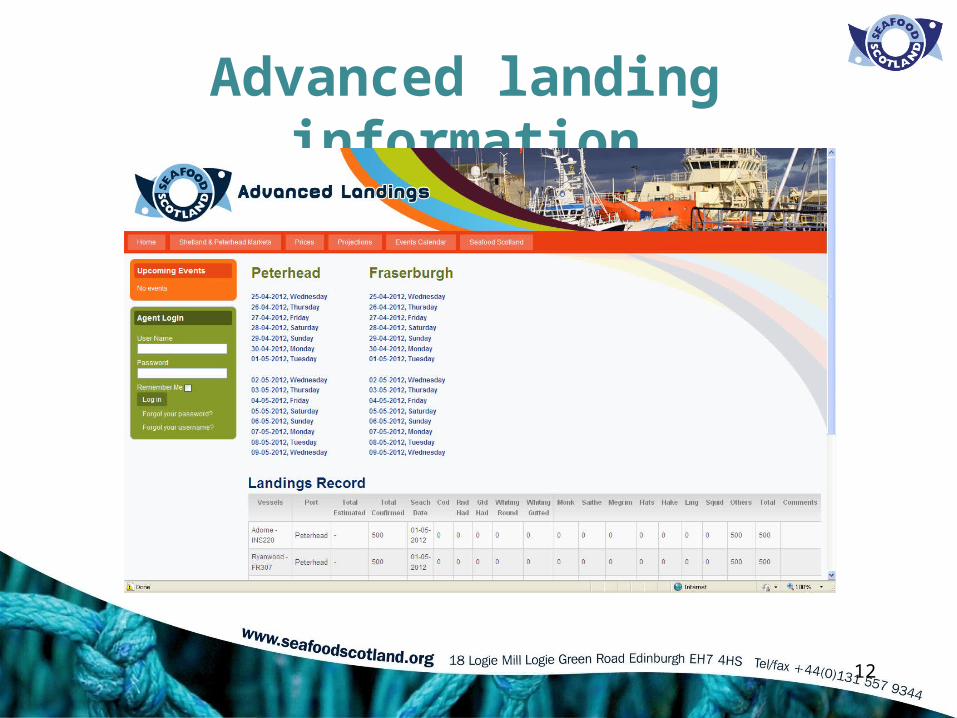

Advanced landing information

12

Advanced landing information

13

• System reliant on vessels & agents inputting data• Key foresight information missing:

– No. of vessels at sea– No. of vessels at sea but not fishing (oil jobs etc)

• Available via electronic log books – Provision of data agreed in principle with Marine Scotland– Charge of £4800 + VAT!– Would still require approval from skippers by SFS

The UK Food Service Sector• The value of the UK Foodservice sector FOOD sales is

estimated at just under £42bn, with sales to operators/outlets equating to £13bn.

• These 259,054 outlets serve 8.1 billion eating occasions a year

= Opportunities for Scottish seafood from fish & chip shops to fine dining

14

UK Food Service Project• Working collaboratively with SAOS, SF&D & industry

to maximise opportunities for Scottish seafood• The Foodservice channel is highly fragmented

compared to Retail. 5 Retailer Groups account for 90% of the Retail channel compared with 2800 Foodservice groups accounting for only 48% share of sales !

15

UK Food Service Project1. Food service sector mapping2. Development of networks with all seafood buyers3. A support programme to match Scottish suppliers

with new opportunities4. Educational programme for buyers and consumers

to raise awareness of Scottish provenance.

Awaiting formal confirmation of funding from EFF PAC

16

17

Developing emerging markets for Scottish seafood 2012 - 2014

• EFF-funded project working in collaboration with SDI, SSPO, SF&D & industry

• Targeting “high-end” food service sector in SE Asia• Raising awareness of Scotland and Scottish seafood• Will benefit Scottish companies already in the market

& help further companies access opportunities

18

Launched at ESE 2012……

19

Domestic market• Regional sourcing opportunities

– Morrisons – 1 May 2012• New processing facility in Humberside• Committed to Scottish sourcing• Requested support to increase supplies, develop marketing

messages, handbooks for fish counter staff• Keen this message is relayed to Scottish Government!

20

21

Services Available• Business development & marketing • Value added programme• Environmental advice & support• Quality & technical advice• Promotions & marketing• Signposting• Enquiry Service

Seafood ScotlandHow can we help?

Visit www.seafoodscotland.org or contact us on 01321 557 9344 for further information or specific enquiries.