Scientus Pharma · to change based on market conditions and potential timing delays. ... Active...

22

S c i e n t u s P h a r m a Corporate Presentation May 2017

-

Upload

duongquynh -

Category

Documents

-

view

216 -

download

0

Transcript of Scientus Pharma · to change based on market conditions and potential timing delays. ... Active...

Scientus PharmaCorporate PresentationMay 2017

FORWARD-LOOKING STATEMENTSThis presentation contains certain forward looking statements and forward lookinginformation (collectively referred to herein as “forward looking statements”) withinthe meaning of applicable securities laws. All statements other than statements ofpresent or historical fact are forward looking statements. Forward lookinginformation is often, but not always, identified by the use of words such as “could”,

“should”, “can”, “anticipate”, “expect”, “believe”, “will”, “may”, “projected”,

“sustain”, “continues”, “strategy”, “potential”, “projects”, “grow”, “take advantage”,

“estimate”, “well positioned” or similar words suggesting future outcomes. Inparticular, this presentation contains forward looking statements relating to theimplementation of operations, licensing, production, sales and revenue generation,future opportunities, business strategies and competitive advantages. The forwardlooking statements regarding HydRx Farms Ltd. (“Scientus Pharma”, “Scientus”,

“we”, “us”, and “our”) are based on certain key expectations and assumptions ofScientus concerning anticipated financial performance, obtaining necessarylicensing to conduct the proposed business, the ability to adequately outfit itsproduction facility, prospects, strategies, the sufficiency of budgeted capitalexpenditures in carrying out planned activities, that there will be no adverseregulatory or political developments with respect to medical marihuana production,sales or consumption, the ability to obtain financing on acceptable terms and theability to achieve a listing on a recognized stock exchange, all of which are subjectto change based on market conditions and potential timing delays. Althoughmanagement of Scientus consider these assumptions to be reasonable based oninformation currently available to them, they may prove to be incorrect.

By their very nature, forward looking statements involve inherent risks anduncertainties (both general and specific) and risks that forward looking statementswill not be achieved. Undue reliance should not be placed on forward lookingstatements, as a number of important factors could cause the actual results to differmaterially from the beliefs, plans, objectives, expectations and anticipations,estimates and intentions expressed in the forward looking statements, includingamong other things: general economic and market factors, including businesscompetition, changes in government regulations; general political and socialuncertainties; lack of insurance; inadequacy of the production facility or the ability toadequately outfit such facility, delay or failure to receive board or regulatoryapprovals including failing to obtain requisite licensing from Health Canada under theMarihuana for Medical Purposes Regulations; inability to complete an initial publicoffering and listing on a recognize stock exchange; changes in legislation; timing andavailability of external financing on acceptable terms; and lack of qualified, skilledlabour or loss of key individuals.

Readers are cautioned that the foregoing list is not exhaustive.

The forward looking statements contained herein are expressly qualified in theirentirety by this cautionary statement. The forward looking statements included in thispresentation are made as of the date of this presentation and Scientus does notundertake and is not obligated to publicly update such forward looking statements toreflect new information, subsequent events or otherwise unless so required byapplicable securities laws.

2

FORWARD-LOOKING STATEMENTS

.

3

Third Party Information

Certain information contained herein includes market and industry data that has been obtained from or is based upon estimates derived from third party sources, including industry publications, reports and websites. Third party sources generally state that the information contained therein has been obtained from sources believed to be reliable, but there is no assurance or guarantee as to the accuracy or completeness of included data. Although the data is believed to be reliable, Scientus has not independently verified the accuracy, currency or completeness of any of the information from third party sources referred to in this presentation or ascertained from the underlying economic assumptions relied upon by such sources. Scientus hereby disclaims any responsibility or liability whatsoever in respect of any third party sources of market and industry data or information.

Notice to Investors

In making an investment decision, prospective investors must rely on their own examination of Scientus and the terms of such private placement offering, including the merits and risks involved. Prospective investors should not construe the contents of this presentation as legal, tax, investment or accounting advice by Scientus or any of its directors, officers, shareholders, agents, employees or advisors. This presentation does not take into account the particular investment objectives or financial circumstances of any prospective investor. Each prospective investor who reviews this presentation must make its own independent assessment of Scientus after making such investigations and each prospective investor is strongly urged to consult with its own advisors with respect to legal, tax, regulatory, financial and accounting consequences, including the merits and the risks involved, of any investment in Scientus. In particular, any estimates or projections or opinions contained herein necessarily involve significant elements of subjective judgment, analysis and assumption and each prospective investor should satisfy itself in relation to such matters. Investment is suitable only for sophisticated investors and requires the financial ability and willingness to accept the high risks and lack of liquidity that are characteristic of an investment in a private company. Purchasers of Scientus’ securities will be required to execute a subscription agreements, which will contain representations, warranties, covenants and acknowledgments of the purchasers required by the relevant regulatory authorities and Scientus to establish the availability of such exemptions and to ensure compliance with applicable securities legislation.

SCIENTUS SNAPSHOTA VERTICALLY-INTEGRATED BIOPHARMACEUTICAL COMPANY

• Market leader in evolution of cannabinoid products from medical-grade to pharmaceutical-grade

• Differentiated from cannabis companies by our proprietary extraction process and the R&D of our products based on our unique scientific understanding of the API

• Near-term therapeutic focus on pain and CNS disorders

• Licensed Dealer under Narcotics Control Regulations of Canada and ACMPR applicant (final review stage)

• Large-scale manufacturing infrastructure in place; 45,000 sq. ft. sterile facility built to GMP standards, boasting three vaults which can store over $150M of narcotics inventory

• Meaningful barriers to entry to defend large market opportunity

• Strong, seasoned management team coupled with thought-leading scientific advisors

3

CANNABIS IN CANADAA COMPLEX LANDSCAPE

SCIENCEPHARMAINTEREST

RECREATION

LICENSEDPRODUCERS

POLITICSOPIOIDCRISIS

SPECIALIZED LICENSED DEALERS

MEDICALUSE

LOBBYGROUPS

4

CURRENT STATE OF INDUSTRYMEDICAL-GRADE PRODUCT FOCUS

Concentrated extract

DRIEDCANNABIS

ETHANOL DISTILLATION

SFE(30 – 40°C)

CONCENTRATEDEXTRACT

5

OF PHYSICIANS PRESCRIBEDMEDICAL CANNABIS

12%

WOULD NOT PRESCRIBE UNDER ANY CIRCUMSTANCES

35% ARE INTERESTED BUT HAVE NOT OR WANT MORE INFO

52% ACKNOWLEDING LIMITED DATACURRENT USE IN CLINCIAL MEDICINE

6

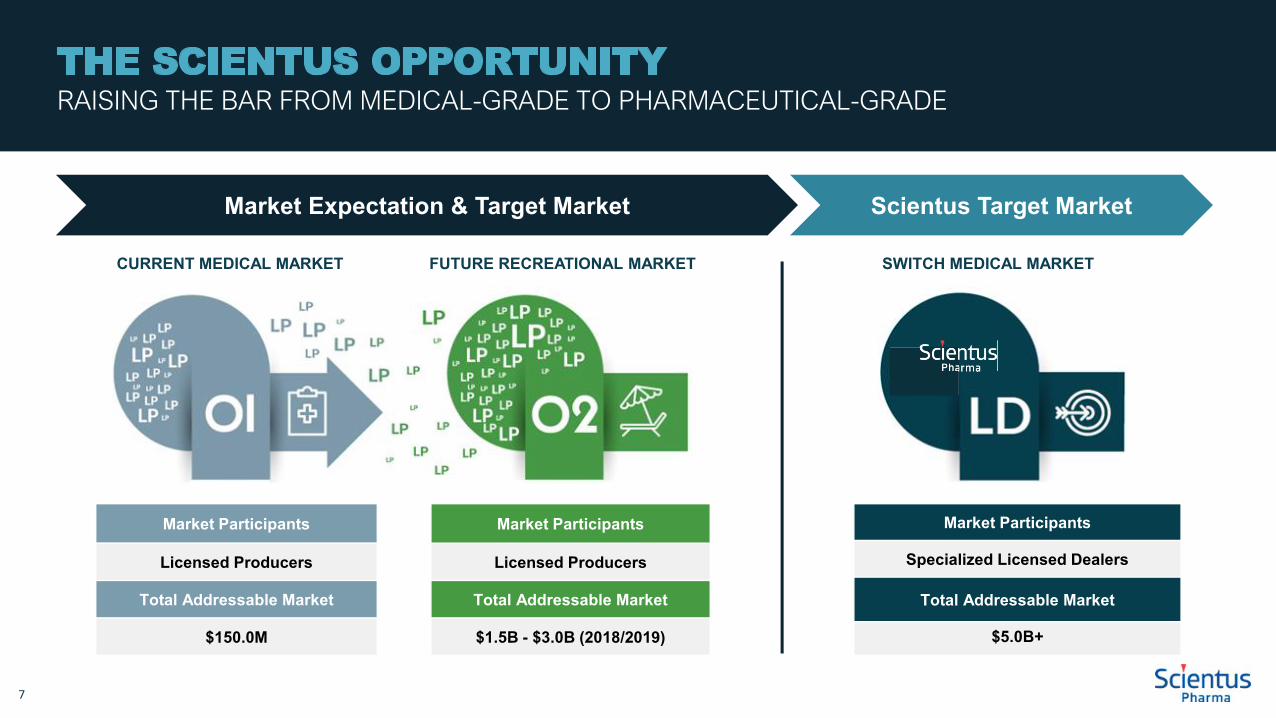

THE SCIENTUS OPPORTUNITYRAISING THE BAR FROM MEDICAL-GRADE TO PHARMACEUTICAL-GRADE

CURRENT MEDICAL MARKET FUTURE RECREATIONAL MARKET

Market Expectation & Target Market

SWITCH MEDICAL MARKET

Scientus Target Market

Market Participants

Licensed Producers

Total Addressable Market

$150.0M

Market Participants

Licensed Producers

Total Addressable Market

$1.5B - $3.0B (2018/2019)

Market Participants

Specialized Licensed Dealers

Total Addressable Market

$5.0B+

7

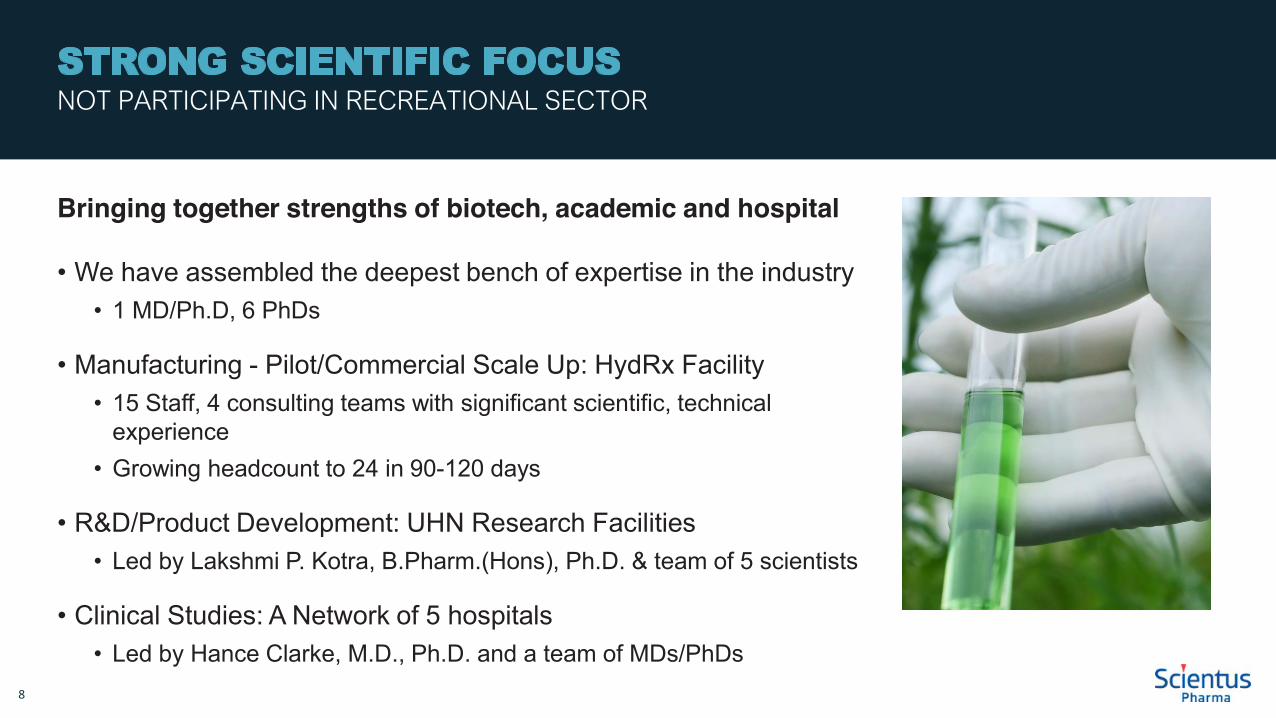

Bringing together strengths of biotech, academic and hospital

• We have assembled the deepest bench of expertise in the industry• 1 MD/Ph.D, 6 PhDs

• Manufacturing - Pilot/Commercial Scale Up: HydRx Facility• 15 Staff, 4 consulting teams with significant scientific, technical

experience• Growing headcount to 24 in 90-120 days

• R&D/Product Development: UHN Research Facilities• Led by Lakshmi P. Kotra, B.Pharm.(Hons), Ph.D. & team of 5 scientists

• Clinical Studies: A Network of 5 hospitals• Led by Hance Clarke, M.D., Ph.D. and a team of MDs/PhDs

STRONG SCIENTIFIC FOCUSNOT PARTICIPATING IN RECREATIONAL SECTOR

8

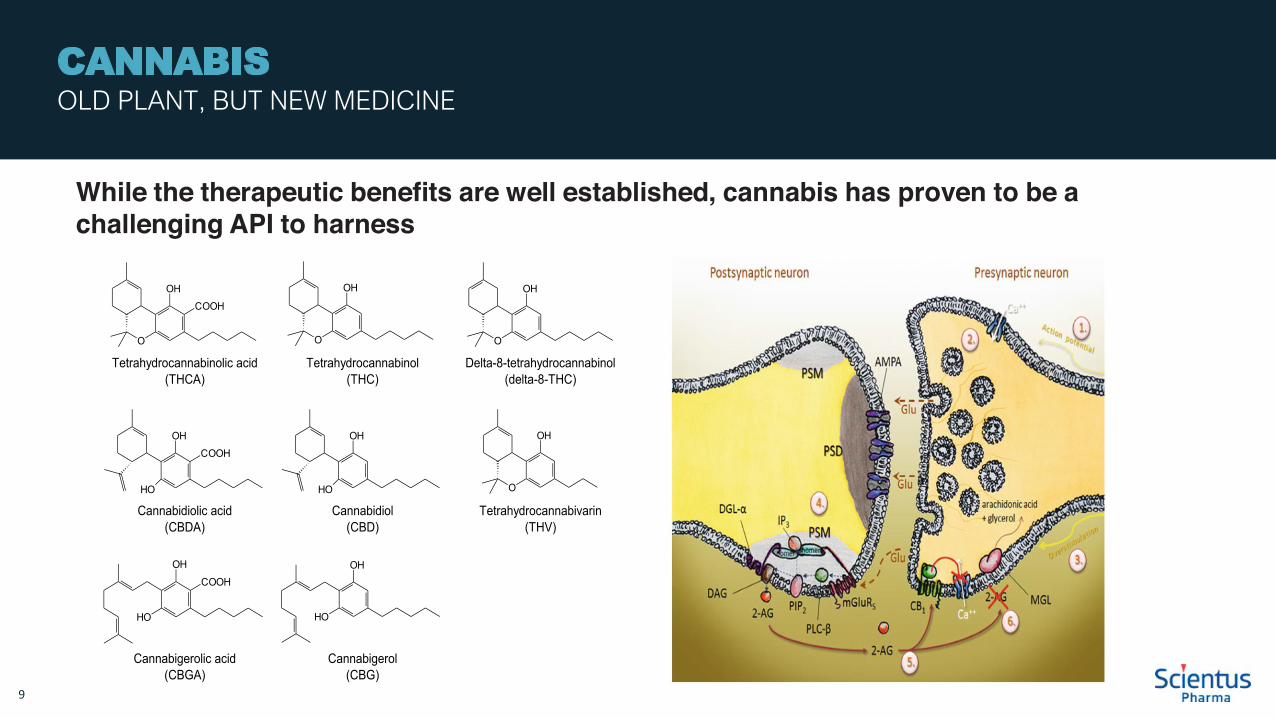

CANNABIS OLD PLANT, BUT NEW MEDICINE

Tetrahydrocannabinolic acid Tetrahydrocannabinol Delta-8-tetrahydrocannabinol(THCA) (THC) (delta-8-THC)

Cannabidiolic acid Cannabidiol Tetrahydrocannabivarin(CBDA) (CBD) (THV)

Cannabigerolic acid Cannabigerol(CBGA) (CBG)

Cannabinolic acid Cannabinol(CBNA) (CBN)

Cannabichromenic acid Cannabichromene(CBCA) (CBC)

Cannabicyclolic acid Cannabicyclol(CBLA) (CBL)

O

OH

COOH

HO

OH

COOH

OH

HO

COOH

O

OH

COOH

OH

O

COOH

OH

O

COOH

O

OH

O

OH

HO

OH

OH

HO

O

OH

OH

O

OH

O

O

OH

9

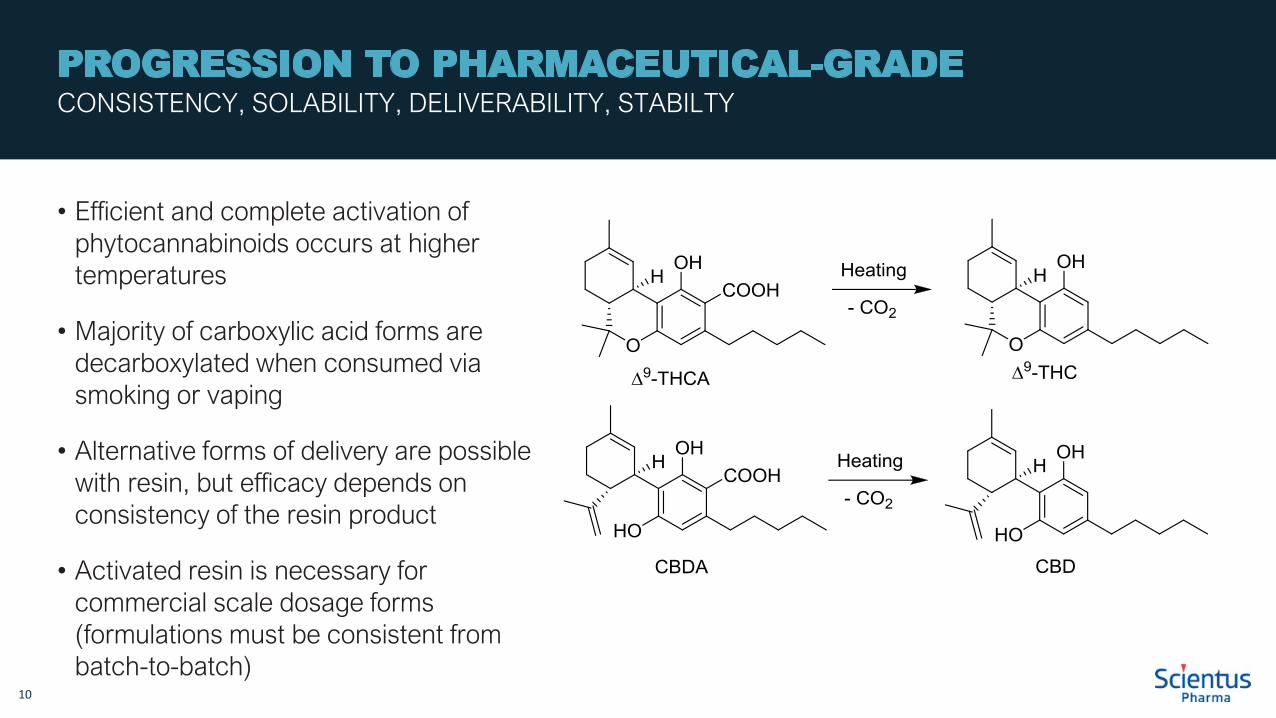

While the therapeutic benefits are well established, cannabis has proven to be a challenging API to harness

PROGRESSION TO PHARMACEUTICAL-GRADE CONSISTENCY, SOLABILITY, DELIVERABILITY, STABILTY

• Efficient and complete activation of phytocannabinoids occurs at higher temperatures

• Majority of carboxylic acid forms are decarboxylated when consumed via smoking or vaping

• Alternative forms of delivery are possible with resin, but efficacy depends on consistency of the resin product

• Activated resin is necessary for commercial scale dosage forms (formulations must be consistent from batch-to-batch)

10

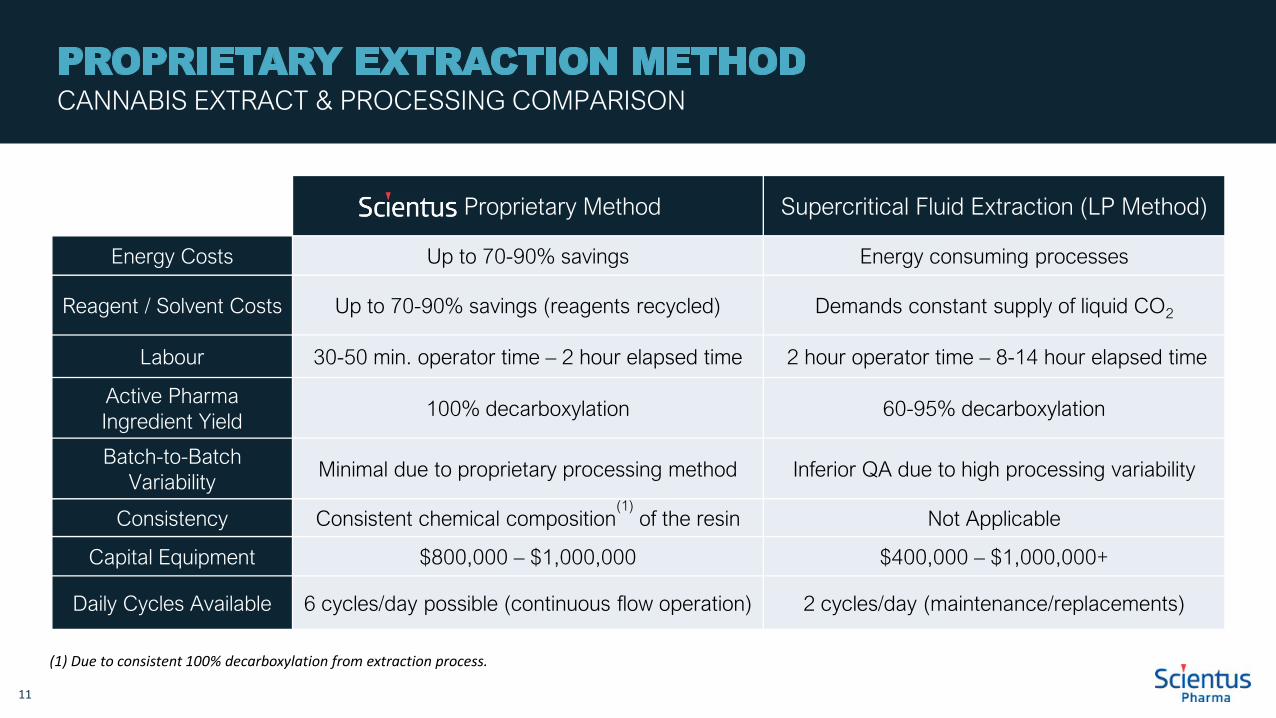

PROPRIETARY EXTRACTION METHODCANNABIS EXTRACT & PROCESSING COMPARISON

Proprietary Method Supercritical Fluid Extraction (LP Method)

Energy Costs Up to 70-90% savings Energy consuming processes

Reagent / Solvent Costs Up to 70-90% savings (reagents recycled) Demands constant supply of liquid CO2

Labour 30-50 min. operator time – 2 hour elapsed time 2 hour operator time – 8-14 hour elapsed time

Active Pharma Ingredient Yield

100% decarboxylation 60-95% decarboxylation

Batch-to-BatchVariability

Minimal due to proprietary processing method Inferior QA due to high processing variability

Consistency Consistent chemical composition(1)

of the resin Not Applicable

Capital Equipment $800,000 – $1,000,000 $400,000 – $1,000,000+

Daily Cycles Available 6 cycles/day possible (continuous flow operation) 2 cycles/day (maintenance/replacements)

(1) Due to consistent 100% decarboxylation from extraction process.

11

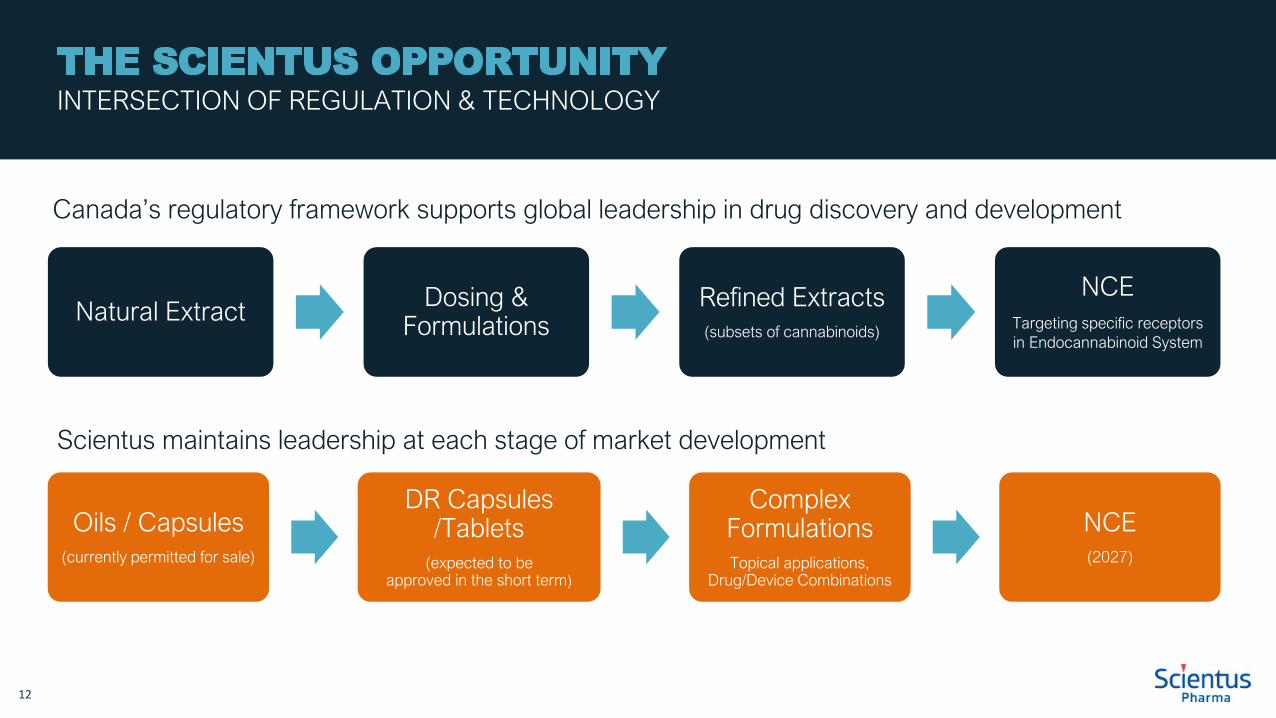

THE SCIENTUS OPPORTUNITYINTERSECTION OF REGULATION & TECHNOLOGY

Scientus maintains leadership at each stage of market development

Natural Extract Dosing & Formulations

Refined Extracts(subsets of cannabinoids)

NCETargeting specific receptors in Endocannabinoid System

Oils / Capsules(currently permitted for sale)

DR Capsules /Tablets

(expected to beapproved in the short term)

Complex FormulationsTopical applications,

Drug/Device Combinations

NCE(2027)

Canada’s regulatory framework supports global leadership in drug discovery and development

12

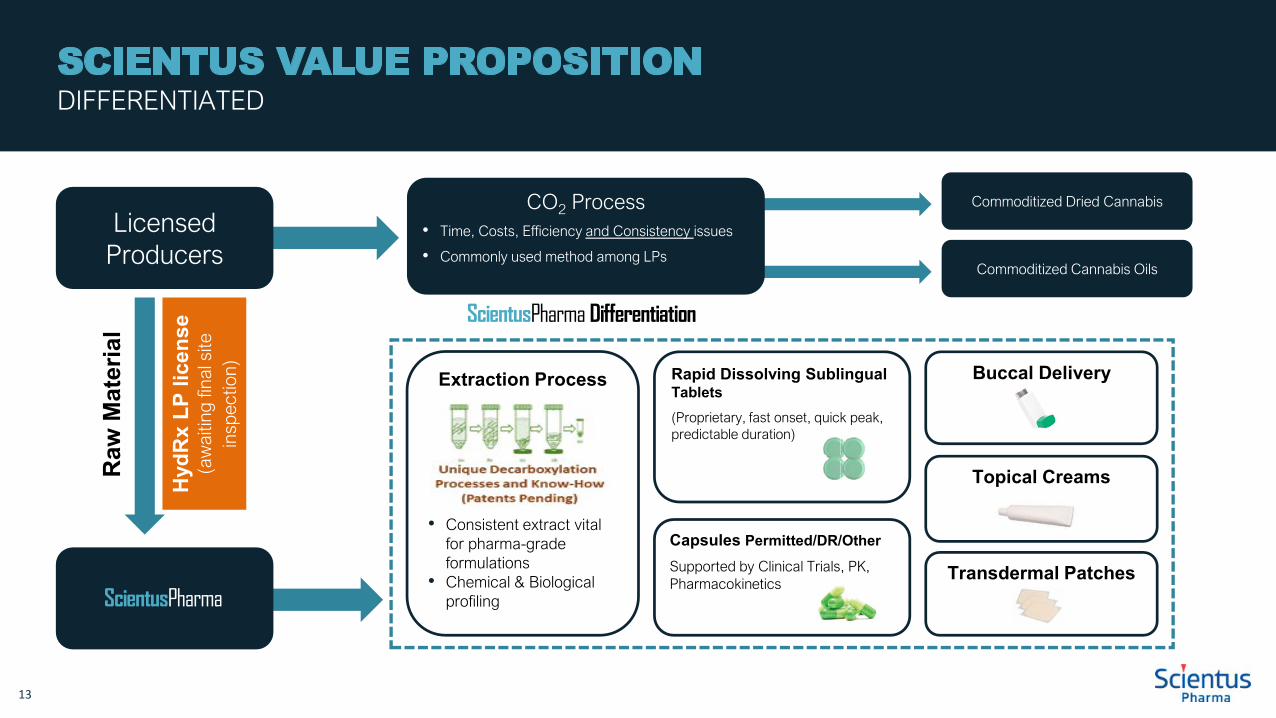

SCIENTUS VALUE PROPOSITIONDIFFERENTIATED

LicensedProducers

Commoditized Dried Cannabis

Commoditized Cannabis Oils

Extraction Process

• Consistent extract vital for pharma-grade formulations

• Chemical & Biological profiling

Rapid Dissolving Sublingual Tablets(Proprietary, fast onset, quick peak, predictable duration)

Transdermal Patches

CO2 Process• Time, Costs, Efficiency and Consistency issues

• Commonly used method among LPs

Raw

Mat

eria

l

Hyd

Rx

LP li

cens

e (a

wai

ting

final

site

in

spec

tion) Buccal Delivery

Capsules Permitted/DR/Other

Supported by Clinical Trials, PK, Pharmacokinetics

Topical Creams

Buccal Delivery

ScientusPharma Differentiation

ScientusPharma

13

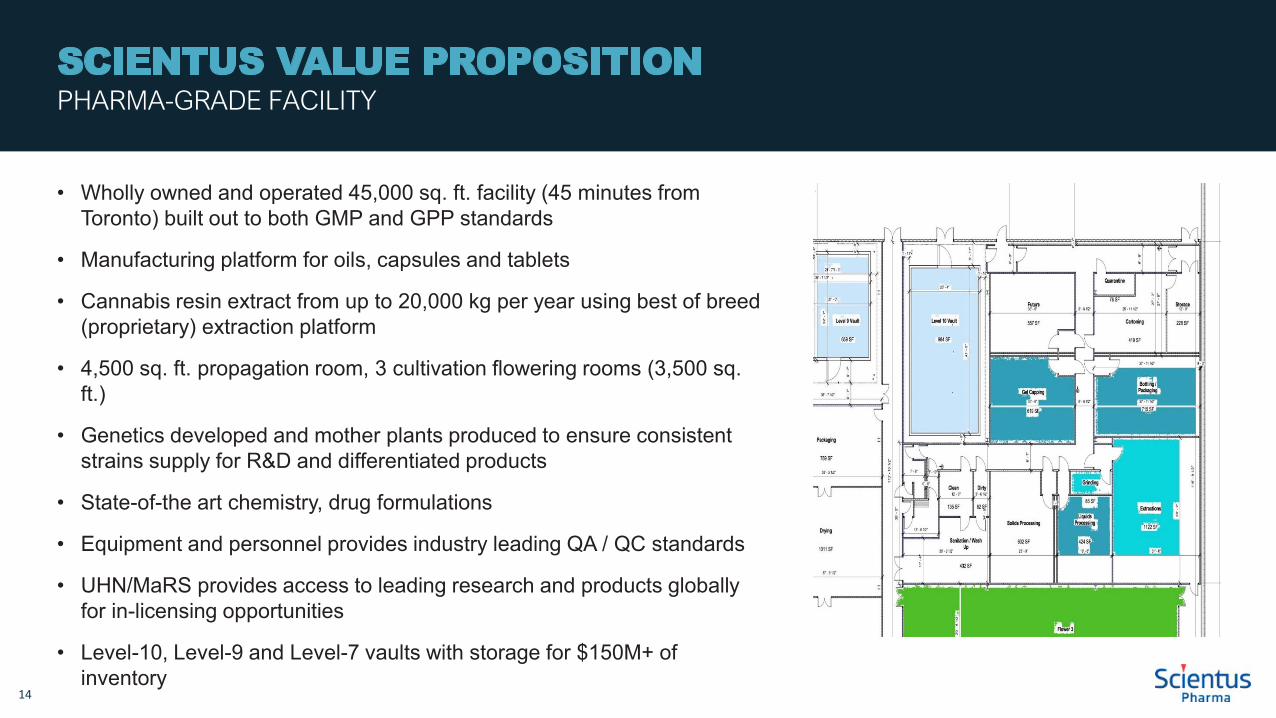

SCIENTUS VALUE PROPOSITIONPHARMA-GRADE FACILITY

14

• Wholly owned and operated 45,000 sq. ft. facility (45 minutes from Toronto) built out to both GMP and GPP standards

• Manufacturing platform for oils, capsules and tablets

• Cannabis resin extract from up to 20,000 kg per year using best of breed (proprietary) extraction platform

• 4,500 sq. ft. propagation room, 3 cultivation flowering rooms (3,500 sq. ft.)

• Genetics developed and mother plants produced to ensure consistent strains supply for R&D and differentiated products

• State-of-the art chemistry, drug formulations

• Equipment and personnel provides industry leading QA / QC standards

• UHN/MaRS provides access to leading research and products globally for in-licensing opportunities

• Level-10, Level-9 and Level-7 vaults with storage for $150M+ of inventory

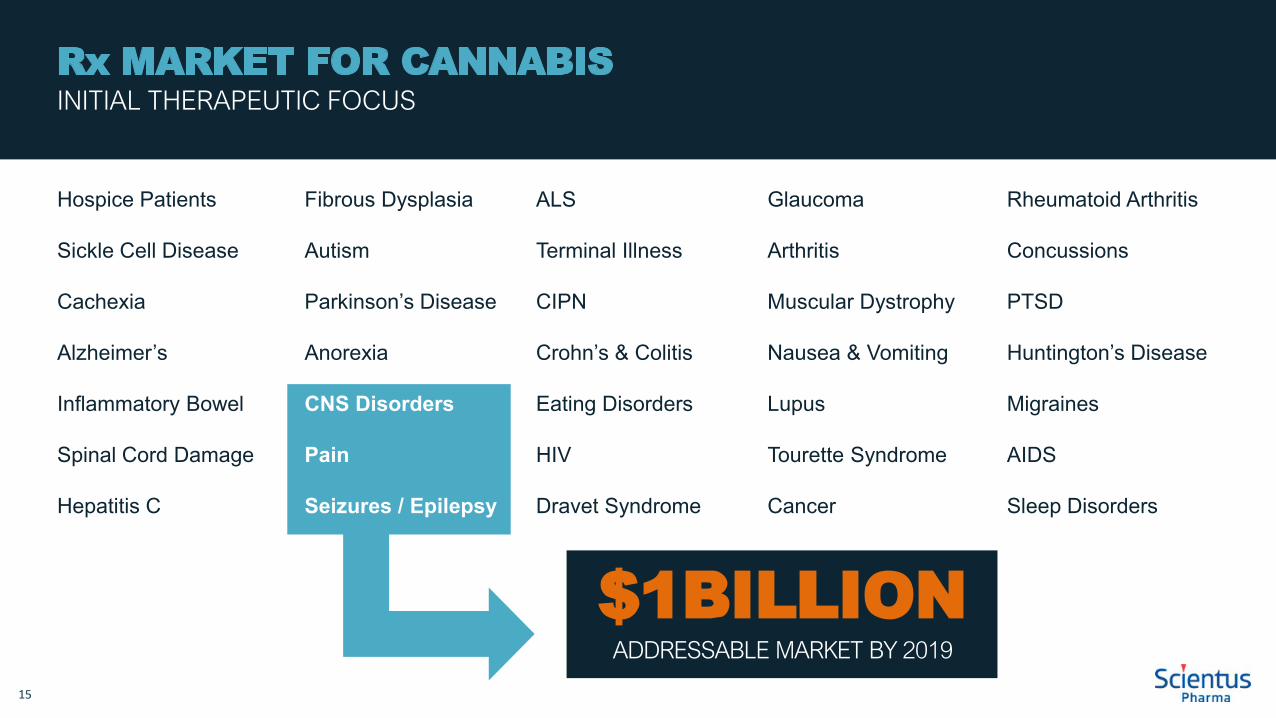

Rx MARKET FOR CANNABIS INITIAL THERAPEUTIC FOCUS

Hospice Patients

Sickle Cell Disease

Cachexia

Alzheimer’s

Inflammatory Bowel

Spinal Cord Damage

Hepatitis C

Fibrous Dysplasia

Autism

Parkinson’s Disease

Anorexia

CNS Disorders

Pain

Seizures / Epilepsy

ALS

Terminal Illness

CIPN

Crohn’s & Colitis

Eating Disorders

HIV

Dravet Syndrome

Glaucoma

Arthritis

Muscular Dystrophy

Nausea & Vomiting

Lupus

Tourette Syndrome

Cancer

Rheumatoid Arthritis

Concussions

PTSD

Huntington’s Disease

Migraines

AIDS

Sleep Disorders

$1BILLIONADDRESSABLE MARKET BY 2019

15

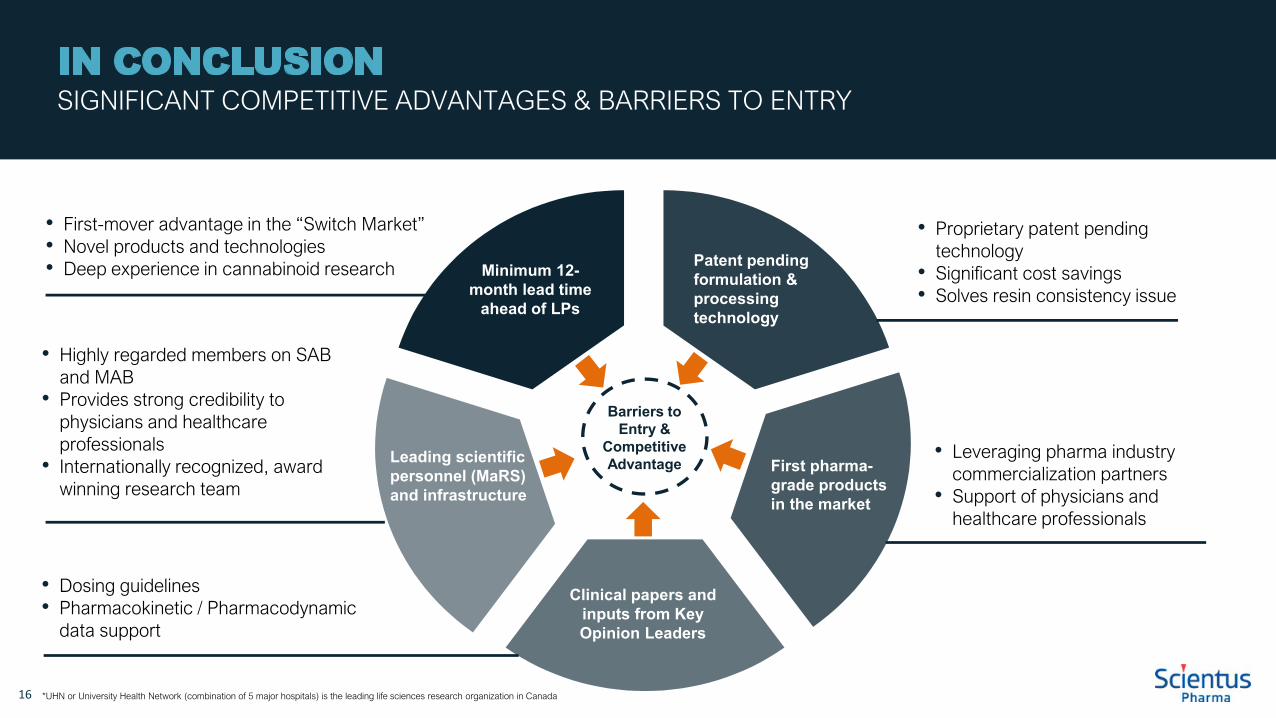

• Dosing guidelines• Pharmacokinetic / Pharmacodynamic

data support

• Leveraging pharma industry commercialization partners

• Support of physicians and healthcare professionals

• Proprietary patent pending technology

• Significant cost savings • Solves resin consistency issue

• First-mover advantage in the “Switch Market”

• Novel products and technologies• Deep experience in cannabinoid research

• Highly regarded members on SAB and MAB

• Provides strong credibility to physicians and healthcare professionals

• Internationally recognized, award winning research team

IN CONCLUSIONSIGNIFICANT COMPETITIVE ADVANTAGES & BARRIERS TO ENTRY

Barriers to Entry &

Competitive Advantage

Clinical papers and inputs from Key Opinion Leaders

Patent pending formulation & processing technology

First pharma-grade products in the market

Leading scientific personnel (MaRS) and infrastructure

Minimum 12-month lead time

ahead of LPs

*UHN or University Health Network (combination of 5 major hospitals) is the leading life sciences research organization in Canada 16

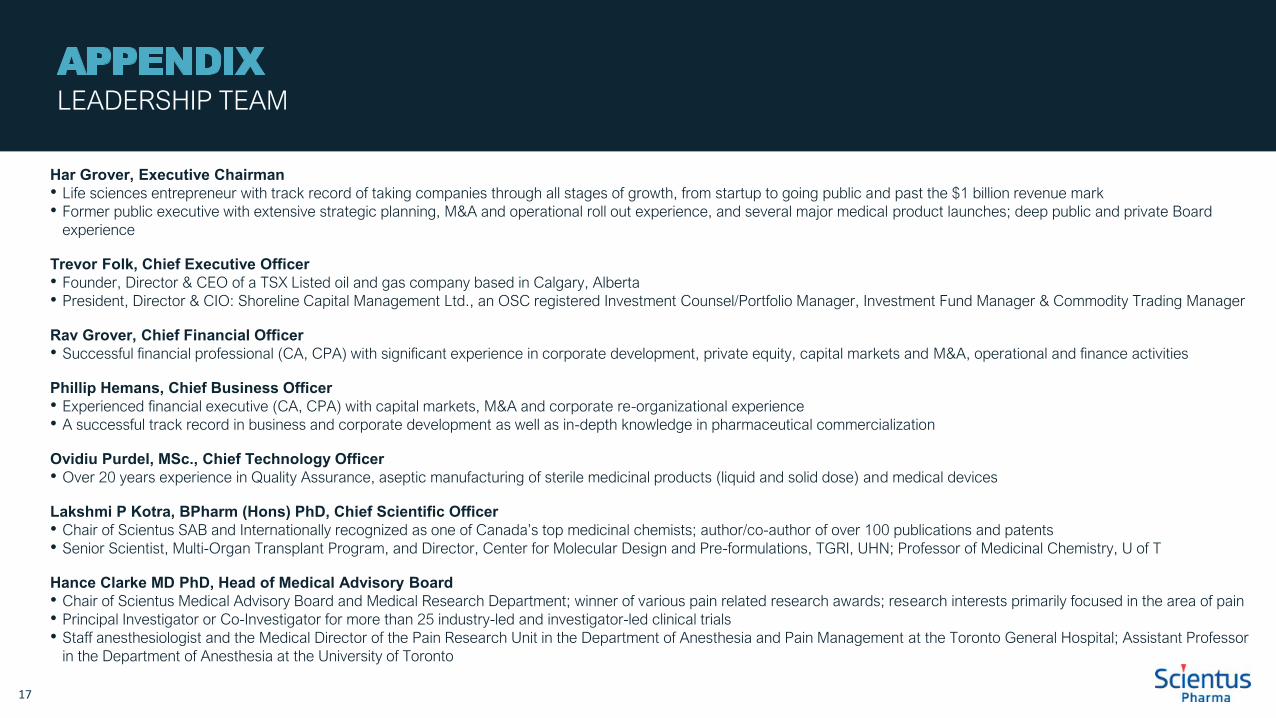

APPENDIXLEADERSHIP TEAM

Har Grover, Executive Chairman• Life sciences entrepreneur with track record of taking companies through all stages of growth, from startup to going public and past the $1 billion revenue mark• Former public executive with extensive strategic planning, M&A and operational roll out experience, and several major medical product launches; deep public and private Board

experience

Trevor Folk, Chief Executive Officer• Founder, Director & CEO of a TSX Listed oil and gas company based in Calgary, Alberta• President, Director & CIO: Shoreline Capital Management Ltd., an OSC registered Investment Counsel/Portfolio Manager, Investment Fund Manager & Commodity Trading Manager

Rav Grover, Chief Financial Officer• Successful financial professional (CA, CPA) with significant experience in corporate development, private equity, capital markets and M&A, operational and finance activities

Phillip Hemans, Chief Business Officer• Experienced financial executive (CA, CPA) with capital markets, M&A and corporate re-organizational experience• A successful track record in business and corporate development as well as in-depth knowledge in pharmaceutical commercialization

Ovidiu Purdel, MSc., Chief Technology Officer• Over 20 years experience in Quality Assurance, aseptic manufacturing of sterile medicinal products (liquid and solid dose) and medical devices

Lakshmi P Kotra, BPharm (Hons) PhD, Chief Scientific Officer• Chair of Scientus SAB and Internationally recognized as one of Canada’s top medicinal chemists; author/co-author of over 100 publications and patents• Senior Scientist, Multi-Organ Transplant Program, and Director, Center for Molecular Design and Pre-formulations, TGRI, UHN; Professor of Medicinal Chemistry, U of T

Hance Clarke MD PhD, Head of Medical Advisory Board• Chair of Scientus Medical Advisory Board and Medical Research Department; winner of various pain related research awards; research interests primarily focused in the area of pain• Principal Investigator or Co-Investigator for more than 25 industry-led and investigator-led clinical trials• Staff anesthesiologist and the Medical Director of the Pain Research Unit in the Department of Anesthesia and Pain Management at the Toronto General Hospital; Assistant Professor

in the Department of Anesthesia at the University of Toronto

17

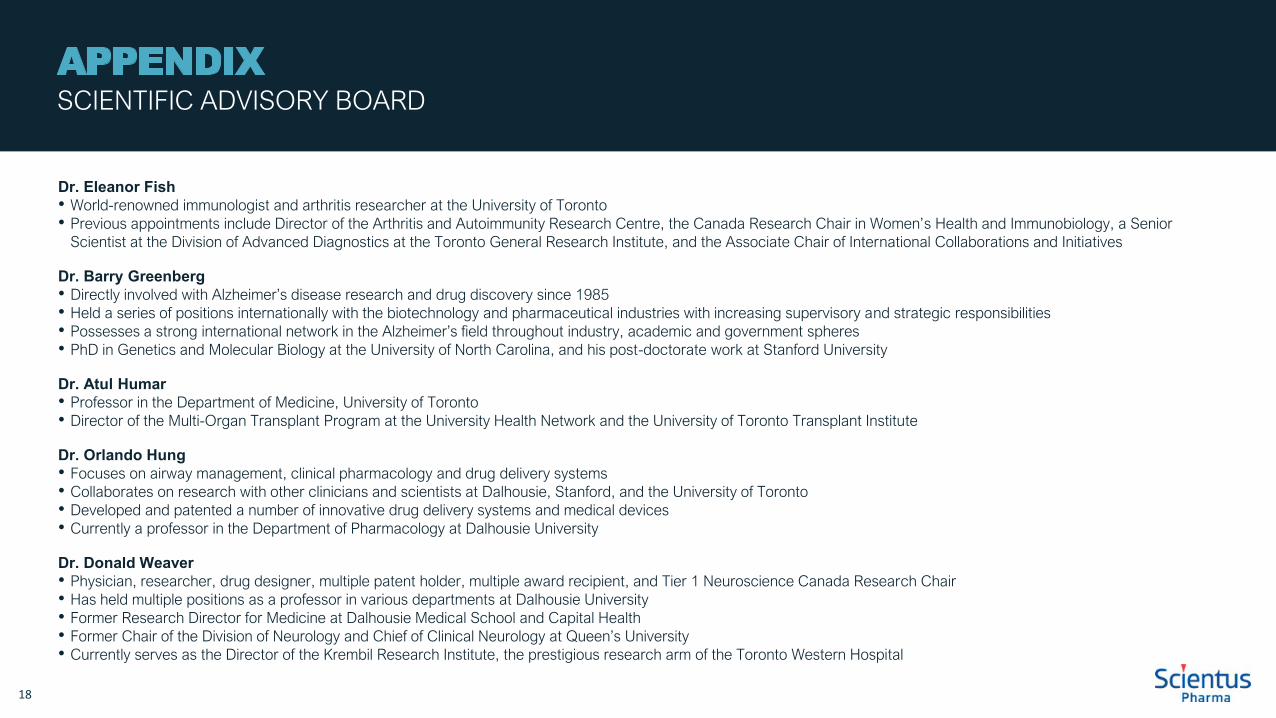

APPENDIXSCIENTIFIC ADVISORY BOARD

Dr. Eleanor Fish• World-renowned immunologist and arthritis researcher at the University of Toronto• Previous appointments include Director of the Arthritis and Autoimmunity Research Centre, the Canada Research Chair in Women’s Health and Immunobiology, a Senior

Scientist at the Division of Advanced Diagnostics at the Toronto General Research Institute, and the Associate Chair of International Collaborations and Initiatives

Dr. Barry Greenberg• Directly involved with Alzheimer’s disease research and drug discovery since 1985

• Held a series of positions internationally with the biotechnology and pharmaceutical industries with increasing supervisory and strategic responsibilities• Possesses a strong international network in the Alzheimer’s field throughout industry, academic and government spheres

• PhD in Genetics and Molecular Biology at the University of North Carolina, and his post-doctorate work at Stanford University

Dr. Atul Humar• Professor in the Department of Medicine, University of Toronto• Director of the Multi-Organ Transplant Program at the University Health Network and the University of Toronto Transplant Institute

Dr. Orlando Hung• Focuses on airway management, clinical pharmacology and drug delivery systems• Collaborates on research with other clinicians and scientists at Dalhousie, Stanford, and the University of Toronto• Developed and patented a number of innovative drug delivery systems and medical devices • Currently a professor in the Department of Pharmacology at Dalhousie University

Dr. Donald Weaver• Physician, researcher, drug designer, multiple patent holder, multiple award recipient, and Tier 1 Neuroscience Canada Research Chair• Has held multiple positions as a professor in various departments at Dalhousie University• Former Research Director for Medicine at Dalhousie Medical School and Capital Health • Former Chair of the Division of Neurology and Chief of Clinical Neurology at Queen’s University

• Currently serves as the Director of the Krembil Research Institute, the prestigious research arm of the Toronto Western Hospital

18

LEGALSTATUTORY RIGHTS OF ACTION

Securities legislation in certain of the provinces of Canada may deem this presentation to be an offering memorandum and accordingly provide purchasers with statutory rights of rescission or damages, or both, in theevent this presentation contains a misrepresentation. A “misrepresentation” is an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make anystatement not misleading or false in the light of the circumstances in which it was made. These remedies must be commenced by the purchaser within the time limits prescribed and are subject to the defences containedin the applicable securities legislation. Purchasers should refer to the applicable provisions of the securities legislation of their province for the particulars of these rights or consult with a legal adviser.

The following is a summary of the statutory rights of rescission or damages, or both, under securities legislation in certain of the provinces of Canada where that is required to be disclosed under the relevant securitieslegislation, and as such, is subject to the express provisions of the legislation and the related regulations and rules. The rights described below are in addition to, and without derogation from, any other right or remedyavailable at law to purchasers of the securities.

Ontario Purchasers

Ontario securities legislation provides that where an offering memorandum is delivered to a purchaser and contains a misrepresentation, the purchaser will be deemed to have relied upon the misrepresentation and will,except as provided below, have a statutory right of action for damages or for rescission against the issuer and a selling security holder on whose behalf the distribution is made; if the purchaser elects to exercise the rightof rescission, the purchaser will have no right of action for damages against the issuer or any selling security holder. No such action shall be commenced more than, in the case of an action for rescission, 180 days after thedate of the transaction that gave rise to the cause of action, or, in the case of any action other than an action for rescission, the earlier of: (i) 180 days after the purchaser first had knowledge of the facts giving rise to thecause of action, or (ii) three years after the date of the transaction that gave rise to the cause of action. The Ontario legislation provides a number of limitations and defences to such actions, including: (a) the issuer or anyselling security holder is not liable if it proves that the purchaser purchased the securities with knowledge of the misrepresentation; (b) in an action for damages, the issuer shall not be liable for all or any portion of thedamages that the issuer or any selling security holder proves do not represent the depreciation in value of the securities as a result of the misrepresentation relied upon; and (c) in no case shall the amount recoverableexceed the price at which the securities were offered.

These rights are not available for a purchaser that is: (a) a Canadian financial institution, meaning either: (i) an association governed by the Cooperative Credit Associations Act (Canada) or a central cooperative creditsociety for which an order has been made under section 473(1) of that Act; or (ii) a bank, loan corporation, trust company, trust corporation, insurance company, treasury branch, credit union, caisse populaire, financialservices cooperative, or league that, in each case, is authorized by an enactment of Canada or a province or territory of Canada to carry on business in Canada or a province or territory of Canada; (b) a Schedule III bank,meaning an authorized foreign bank named in Schedule III of the Bank Act (Canada); (c) the Business Development Bank of Canada incorporated under the Business Development Bank of Canada Act (Canada); or (d) asubsidiary of any person referred to in clauses (a), (b) or (c), if the person owns all of the voting securities of the subsidiary, except the voting securities required by law to be owned by directors of that subsidiary.

New Brunswick Purchasers

New Brunswick securities legislation provides that where any information relating to an offering that is provided to a purchaser of the securities contains a misrepresentation, a purchaser who purchases the securitiesshall be deemed to have relied on the misrepresentation if it was a misrepresentation at the time of purchase. Such purchaser has a right of action for damages against the issuer or may elect to exercise a right ofrescission against the issuer, in which case the purchaser shall have no right of action for damages. No such action shall be commenced more than, in the case of an action for rescission, 180 days after the date of thetransaction that gave rise to the cause of action or, in the case of any action, other than an action for rescission, the earlier of (i) one year after the plaintiff first had knowledge of the facts giving rise to the cause of action,and (ii) six years after the date of the transaction that gave rise to the cause of action. The New Brunswick legislation provides a number of limitations and defences to such actions, including: (a) the issuer is not liable if itproves that the purchaser purchased the securities with knowledge of the misrepresentation; (b) in an action for damages, the issuer shall not be liable for all or any portion of the damages that it proves do not representthe depreciation in value of the securities as a result of the misrepresentation relied upon; and (c) in no case shall the amount recoverable exceed the price at which the securities were offered.

26

LEGALSTATUTORY RIGHTS OF ACTION

Nova Scotia Purchasers

Nova Scotia securities legislation provides that in the event that an offering memorandum or a record incorporated by reference in an offering memorandum, together with any amendments thereto, or any advertising orsales literature (as defined in the Nova Scotia securities legislation) contains a misrepresentation, a purchaser who purchases the securities referred to in it is deemed to have relied upon such misrepresentation if it was amisrepresentation at the time of purchase. Such purchaser has a statutory right of action for damages against the seller (which includes the issuer) and, subject to certain additional defences, the directors of the seller.Alternatively, the purchaser while still an owner of the securities, may elect instead to exercise a statutory right of rescission against the issuer, in which case the purchaser shall have no right of action for damages againstthe seller or the directors. No such action shall be commenced to enforce the right of action for rescission or damages more than 120 days after the date payment was made for the securities (or after the date on whichinitial payment was made for the securities where payments subsequent to the initial payment are made pursuant to a contractual commitment assumed prior to, or concurrently with, the initial payment). The NovaScotia legislation provides a number of limitations and defences, including: (a) no person or company is liable if the person or company proves that the purchaser purchased the securities with knowledge of themisrepresentation; (b) in the case of an action for damages, no person or company is liable for all or any portion of the damages that it proves do not represent the depreciation in value of the securities as a result of themisrepresentation; and (c) in no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser.

A person or company, other than the issuer, is not liable with respect to any part of the offering memorandum or any amendment to the offering memorandum not purporting (a) to be made on the authority of an expertor (b) to be a copy of, or an extract from, a report, opinion or statement of an expert, unless the person or company (i) failed to conduct a reasonable investigation to provide reasonable grounds for a belief that there hadbeen no misrepresentation or (ii) believed that there had been a misrepresentation.

A person or company, other than the issuer, will not be liable if that person or company proves that: (a) the offering memorandum or any amendment to the offering memorandum was sent or delivered to the purchaserwithout the person’s or company’s knowledge or consent and that, on becoming aware of its delivery, the person or company gave reasonable general notice that it was delivered without the person’s or company’sknowledge or consent; (b) after delivery of the offering memorandum or any amendment to the offering memorandum and before the purchase of the securities by the purchaser, on becoming aware of anymisrepresentation in the offering memorandum or any amendment to the offering memorandum, the person or company withdrew the person’s or company’s consent to the offering memorandum or any amendment tothe offering memorandum, and gave reasonable general notice of the withdrawal and the reason for it; or (c) with respect to any part of the offering memorandum or any amendment to the offering memorandumpurporting (i) to be made on the authority of an expert, or (ii) to be a copy of, or an extract from, a report, an opinion or a statement of an expert, the person or company had no reasonable grounds to believe and did notbelieve that (A) there had been a misrepresentation, or (B) the relevant part of the offering memorandum or any amendment to the offering memorandum did not fairly represent the report, opinion or statement of theexpert, or was not a fair copy of, or an extract from, the report, opinion or statement of the expert.

Saskatchewan Purchasers

Saskatchewan securities legislation provides that in the event that an offering memorandum, together with any amendments thereto, or advertising and sales literature disseminated in connection with an offering ofsecurities contains a misrepresentation, a purchaser who purchases such securities has, without regard to whether the purchaser relied on the misrepresentation, a right of action for damages against: (a) the issuer andthe selling security holder on whose behalf the distribution is made; (b) every promoter and director of the issuer or the selling security holder, as the case may be, at the time the offering memorandum or anyamendment to it was sent or delivered; (c) every person or company whose consent has been filed respecting the offering, but only with respect to reports, opinions or statements that have been made by them; (d) everyperson who or company that, in addition to the persons or companies mentioned in clauses (a) to (c), signed the offering memorandum or the amendment to the offering memorandum; and (e) every person who orcompany that sells securities on behalf of the issuer and the selling security holder under the offering memorandum or amendment to the offering memorandum. If such purchaser elects to exercise a statutory right ofrescission against the issuer or selling security holder, it shall have no right of action for damages against that person or company. No such action for rescission or damages shall be commenced more than, in the case of aright of rescission, 180 days after the date of the transaction that gave rise to the cause of action or, in the case of any action, other than an action for rescission, before the earlier of (i) one year after the plaintiff first hadknowledge of the facts giving rise to the cause of action, and (ii) six years after the date of the transaction that gave rise to the cause of action.

27

LEGALSaskatchewan Purchasers (continued)

The Saskatchewan legislation provides a number of limitations and defences, including: (a) no person or company will be liable if the person or company proves that the purchaser purchased the securities with knowledge of themisrepresentation; (b) in the case of an action for damages, no person or company will be liable for all or any portion of the damages that it proves do not represent the depreciation in value of the securities as a result of themisrepresentation; and (c) in no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser.

No person or company, other than the issuer, will be liable if the person or company proves that: (a) the offering memorandum or any amendment to it was sent or delivered without the person’s or company’s knowledge orconsent and that, on becoming aware of it being sent or delivered, that person or company gave reasonable general notice that it was so sent or delivered; (b) after the filing of the offering memorandum or any amendment to it andbefore the purchase of securities by the purchaser, on becoming aware of any misrepresentation in the offering memorandum or any amendment to it, the person or company withdrew the person’s or company’s consent to it andgave reasonable general notice of the person’s or company’s withdrawal and the reason for it; (c) with respect to any part of the offering memorandum or any amendment to it purporting to be made on the authority of an expert,or purporting to be a copy of, or an extract from, a report, an opinion or a statement of an expert, that person or company had no reasonable grounds to believe and did not believe that (i) there had been a misrepresentation, or (ii)the part of the offering memorandum or any amendment to it did not fairly represent the report, opinion or statement of the expert or was not a fair copy of, or an extract from, the report, opinion or statement of the expert; (d)with respect to any part of the offering memorandum or any amendment to it purporting to be made on the person’s or company’s own authority as an expert or purporting to be a copy of or an extract from the person’s orcompany’s own report, opinion or statement as an expert that contains a misrepresentation attributable to failure to represent fairly his, her or its report, opinion or statement as an expert, (i) the person or company had, afterreasonable investigation, reasonable grounds to believe, and did believe, that the part of the offering memorandum or any amendment to it fairly represented the person’s or company’s report, opinion or statement, or (ii) onbecoming aware that the part of the offering memorandum or of any amendment to it did not fairly represent the person’s or company’s report, opinion or statement as an expert, the person or company immediately advised theSaskatchewan Securities Commission and gave reasonable general notice that such use had been made of it and that the person or company would not be responsible for that part of the offering memorandum or of the amendmentto it; or (e) with respect to a false statement purporting to be a statement made by an official person or contained in what purports to be a copy of or extract from a public official document, the statement was a correct and fairrepresentation of the statement or copy of or extract from the document and the person or company had reasonable grounds to believe, and did believe, that the statement was true.

The Saskatchewan legislation also provides that where an individual makes a verbal statement to a prospective purchaser that contains a misrepresentation relating to the security purchased and the verbal statement is made eitherbefore or contemporaneously with the purchase of the security, the purchaser is deemed to have relied on the misrepresentation, if it was a misrepresentation at the time of purchase, and has a right of action for damages againstthe individual who made the verbal statement.

The Saskatchewan legislation provides a purchaser with the right to void the purchase agreement and to recover all money and other consideration paid by the purchaser for the securities if the securities are sold in contravention ofSaskatchewan securities legislation, regulations or a decision of the Saskatchewan Financial Services Commission.

The Saskatchewan legislation also provides a right of action for rescission or damages to a purchaser of securities to whom an offering memorandum or any amendment to it was not sent or delivered prior to or at the same time asthe purchaser enters into an agreement to purchase the securities, as required by the Saskatchewan legislation.

The Saskatchewan legislation also provides that a purchaser who has received an amended offering memorandum that was amended and delivered in accordance with such legislation has a right to withdraw from the agreement topurchase the securities by delivering a notice to the person who or company that is selling the securities, indicating the purchaser’s intention not to be bound by the purchase agreement, provided such notice is delivered by thepurchaser within two business days of receiving the amended offering memorandum.

Manitoba, Newfoundland and Labrador and Prince Edward Island Purchasers

Purchasers should refer to the applicable provisions of the securities legislation of their province for the particulars of these rights or consult with a legal adviser.

PLEASE CONTACT THE COMPANY FOR FURTHER INFORMATION

28