SCHOOL DISTRICT OF AUDUBON - New Jersey · Avenue Elementary and Audubon Junior-Senior High School....

125

SCHOOL DISTRICT OF AUDUBON Audubon Board of Education Audubon, New Jersey Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2012

Transcript of SCHOOL DISTRICT OF AUDUBON - New Jersey · Avenue Elementary and Audubon Junior-Senior High School....

SCHOOL DISTRICTOF

AUDUBON

Audubon Board of EducationAudubon, New Jersey

Comprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2012

AUDUBON SCHOOL DISTRICT

INTRODUCTORY SECTION

Letter of TransmittalOrganizational ChartRoster of OfficialsConsultants and Advisors

FINANCIAL SECTION

Independent Auditor's Report

K-I Report on Compliance and on Internal Control Over Financial Reporting Basedon an Audit of Financial Statements Performed in Accordance withGovernment Auditing Standards

Required Supplementary Information - Part IManagement's Discussion and Analysis

Basic Financial Statements

A. District-wide Financial Statements:

A-IA-2

Statement of Net AssetsStatement of Activities

Page2789

II

B. Fund Financial Statements:

Governmental Funds:B-1 Balance SheetB-2 Statement of Revenues, Expenditures, and Changes in Fund BalancesB-3 Reconciliation of the Statement of Revenues, Expenditures, and Changes in

Fund Balances of Governmental Funds to the Statement of Activities

13

16

2627

29

30

31

323334

3536

37

Proprietary Funds:B-4 Statement of Net AssetsB-5 Statement of Revenues, Expenses, and Changes in Fund Net AssetsB-6 Statement of Cash Flows

Fiduciary Funds:B-7 Statement of Fiduciary Net AssetsB-8 Statement of Changes in Fiduciary Net Assets

Notes to the Financial Statements

PageRequired Supplementary Information - Part II

C. Budgetary Comparison Schedules

C-I Budgetary Comparison Schedule - General Fund 57C-Ia Combining Schedule of Revenues, Expenditures and Changes

in Fund Balance - Budget and Actual (ifappJicable) N/AC-Ib Budgetary Comparison Schedule - Education Jobs Fund

General Fund 64C-Iba Budgetary Comparison Schedule - American Recovery & Reinvestment Act

General Fund - Government Service Funds N/AC-2 Budgetary Comparison Schedule - Special Revenue Fund 65

Notes to the Required Supplementary InformationC-3 Budget-to-GAAP Reconciliation 66

Other Supplementary Information

D. School Level Schedules: N/A

E. Special Revenue Fund:

E-I Combining Schedule of Revenues and ExpendituresSpecial Revenue Fund - Budgetary Basis 69

E-2 Demonstrably Effective Program Aid Schedule of Expenditures -Budgetary Basis N/A

E-3 Early Childhood Program Aid Schedule of Expenditures -Budgetary Basis N/A

E-4 Distance Learning Network Aid Schedule of Expenditures -Budgetary Basis N/A

E-5 Instructional Supplement Aid Schedule of Expenditures -Budgetary Basis N/A

F. Capital Projects Fund:

F-I Statement of Revenues, Expenditures, Project Balance, and Project Status -Budgetary Basis

G. Proprietary Fund:

Enterprise Fund:G-I Combining Statement of Net AssetsG-2 Combining Statement of Revenues, Expenses and Changes in

Fund Net AssetsCombining Statement of Cash FlowsG-3

Internal Service Fund: N/A

H. Fiduciary Funds:H-I Combining Statement of Fiduciary Net AssetsH-2 Combining Statement of Changes in Fiduciary Net AssetsH-3H-4

Student Activity Agency Fund Schedule of Receipts and DisbursementsPayroll Agency Fund Schedule of Receipts and Disbursements

71

75

7677

79808182

PageI. Long- Term Debt:

I-I Schedule of Serial Bonds 84

1-2 Schedule of Obligations under Capital Leases 85

1-3 Budgetary Comparison Schedule - Debt Service Fund 86

STATISTICAL SECTION (Unaudited)

J-l Net Assets by Component 88J-2 Changes in Net Assets, Last Four Fiscal Years 89

J-3 Fund Balances, Governmental Funds, Last Four Fiscal Years 91

J-4 Changes in Fund Balances, Governmental Funds, Last Ten Fiscal Years 92

J-5 General Fund - Other Local Revenue by Source, Last Ten Fiscal Years 93J-6 Assessed Value and Actual Value of Taxable Property, Last Ten Fiscal Years 94J-7 Direct and Overlapping Property Tax Rates, Last Ten Fiscal Years 95

J-8 Principal Property Tax Payers, Current Year and Nine Years Ago 96J-9 Property Tax Levies and Collections, Last Ten Fiscal Years 97J-IO Ratios of Outstanding Debt by Type, Las Ten Fiscal Years 98J-II Ratios of Net General Bonded Debt Outstanding, Last Ten Fiscal Years 99J-12 Ratios of Overlapping Governmental Activities Debt, As of December 31, 20 II 100J-13 Legal Debt Margin Information, Last Ten Fiscal Years 101J-14 Demographic and Economic Statistics 102J-15 Principal Employers, Current Year & Nine Years Ago (information not available) N/AJ-16 Full-time Equivalent District Employees by Function/Program, Last Ten Fiscal Year! 103J-17 Operating Statistics, Last Ten Fiscal Years 104J-18 School Building Information, Last Ten Fiscal Years lOSJ-19 Schedule of Required Maintenance, Last Six Fiscal Years 106J-20 Insurance Schedule 107

SINGLE AUDIT SECTION

K-2 Report on Compliance with Requirements Applicable to Each MajorProgram and on Internal Control Over Compliance in Accordance withOMB Circular A-133 and New Jersey OMB Circular Letter 04-04

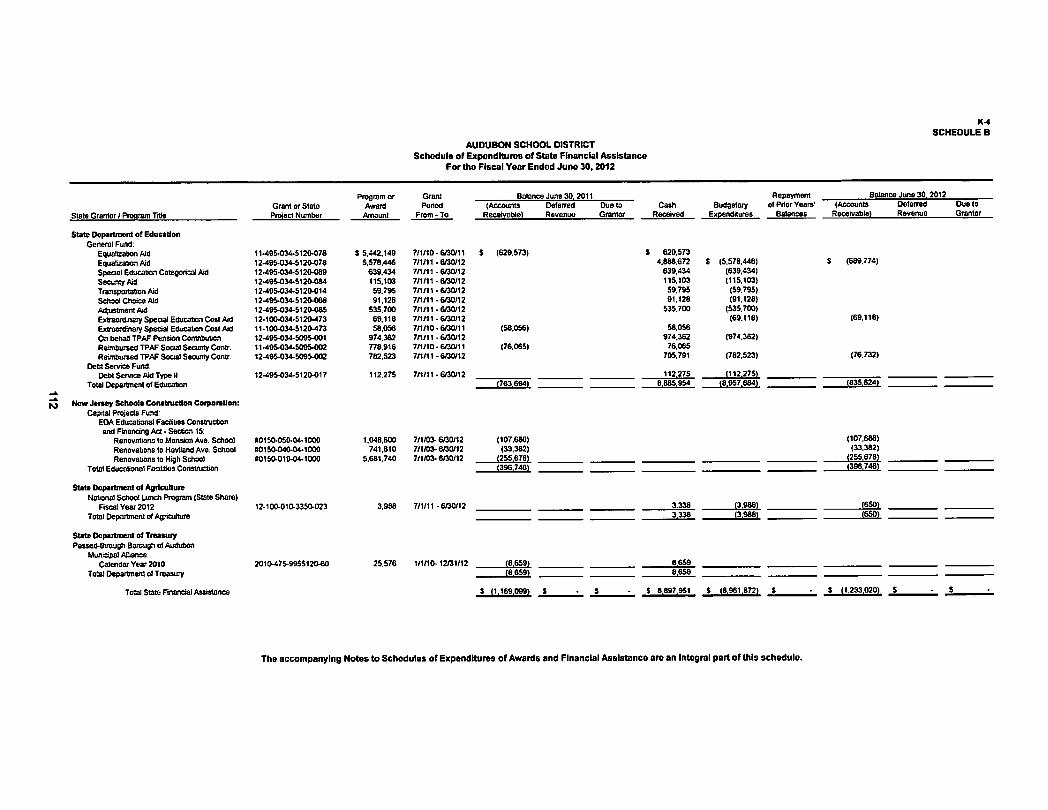

Schedule of Expenditures of Federal Awards, Schedule ASchedule of Expenditures of State Financial Assistance, Schedule BNotes to the Schedules of Awards and Financial AssistanceSchedule of Findings and Questioned Costs

109III112113us120

K-3K-4K-5K-6K-7 Summary Schedule of Prior Audit Findings

of the

Comprehensive Annual

Financial Report

Audubon Board of EducationAudubon, New Jersey

For the Fiscal Year Ended June 30, 2012

Prepared byAudubon Board of Education

Finance Department

Introductory Section

AUDUBON PUBLIC SCHOOLS350 EDGEWOOD AVENUE

AUDUBON, NEW JERSEY 08106

Donald A. BordenSuperintendent of Schools856-547-7695

October 15. 2012

Honorable President and Members ofThe Audubon Board of EducationCounty of Camden .Borough of Audubon350 Edgewood AvenueAudubon. NJ 08106

Dear Board Members:

The comprehensive annual financial report of the Audubon School District for the fiscalyear ended June 30. 2012. is hereby submitted. Responsibility for both the accuracy of thedata and completeness and fairness of the presentation. including all disclosures. restswith the management of the Board of Education. To the best of our knowledge and belief.the data presented in this report is accurate in all material respects and is reported in amanner designed to present fairly the financial position and results of operations of thevarious funds and account groups of the District. All disclosures necessary to enable thereader to gain an understanding of the District's financial activities have been included.

The comprehensive annual financial report is presented in four sections: introductory,financial. statistical and single audit. The introductory section includes this transmittalletter. the District's organizational chart and a list of principal officials. The financial sectionincludes the general purpose financial statements and schedules. as well as the auditor'sreport thereon. The statistical section includes selected financial and demographicinformation. generally presented on a multi-year basis. The District is required to undergoan annual single audit in conformity with the provisions of the Single Audit Act of 1984 andthe U.S. Office of Management and Budget Circular A-133. "Audits of State. LocalGovernments and Not for Profit Organizations" and the state Treasury Circular Letter 98-07OMB. "Single Audit Policy for Recipients of Federal Grants. State Grants and State AidPayments". Information related to this single audit. including the auditor's report on theinternal control structure and compliance with applicable laws and regulations and findingsand recommendation, are included in the single audit section of this report.

2

1. REPORTING ENTITY AND ITS SERVICES:

The Audubon School district is an independent reporting entity within the criteria adoptedby the GASB as established by NCGA Statement No.3. All funds and account groups ofthe district are included in this report. The Audubon Board of Education and all its schoolsconstitute the Districts reporting entity.

The school district consists of three schools - Mansion Avenue Elementary, HavilandAvenue Elementary and Audubon Junior-Senior High School. The district provides a fullrange of educational services appropriate to grade levels K-12. These include regular,vocational and special education programs. The Audubon school district also offers a pre-school program for handicap students. In 2011 the Audubon School District was approvedto participate in the State's Inter-District Public School Choice Program. This programallowed students from other districts in the surrounding area to attend Audubon HighSchool. Student admission was based on availability of space, and the district receivedstate aid for each student enrolled.

On June 30,2009 the Audubon Park Board of education was dissolved, as the State ofNew Jersey took steps to eliminate all non-operating districts in the State. The AudubonPark students are now considered resident students of the district. The district stillmaintains a send-receiving with the Mount Ephraim school district for grades nine thrutwelve.

The district completed the 2011-2012 school year, with an average daily enrollment of1,402 students. During the past few years enrollment has dipped slightly, however, weanticipate this trend to level off and leave us with a stable number of students.

Pupil Enrollments

SCHOOL YEAR AVERAGE DAILY ENROLLMENT

2002-2003 1,777

2003-2004 1,747

2004-2005 1,761

2005-2006 1.629

2006-2007 1,567

2007-2008 1524

2008-2009 1,498

2009-2010 1,482

2010-2011 1,440

2011-2012 1,402

3

2. ECONOMIC CONDITION AND OUTLOOK:

Audubon, a community of about 9,000 people, lies in the eastern portion of CamdenCounty. This community of 1.2 square miles is comprised primarily of residential units andsmall retail businesses. It is a stable community with little room for additional development.The town, however, is currently experiencing a rebirth. Several new small businesses haveopened and development of a major shopping center is now completed.

3. A SNAPSHOT OF OUR SCHOOLS

ELEMENTARY SCHOOLS

Both the Haviland Avenue School (K-2) and the Mansion Avenue School (3-6) havetaken great strides in their efforts to infuse technology into the learning process. LCDProjectors and Smartboards are being installed in classrooms. Additionally, a numberof i Pads have been purchased and will be budgeted during the next year. Thesepurchases were a significant part of the district's Strategic Plan, initiated during the2007-2008 school year. In addition, goals related to writing, transitioning students,increasing scores on standardized tests, and college preparedness continue to driveprofessional development, budgeting and curriculum development.

HIGH SCHOOL

Like the elementary schools the junior - senior high school continues to move forwardin an effort to infuse technology into all instructional areas. The need to immerse ourstudents in a technology rich learning environment is addressed as a goal in thedistrict's Strategic Plan. In addition, goals related to writing, transitioning students,increasing scores on standardized tests and college preparedness have beenestablished. This plan, in its third full year, continues to drive professionaldevelopment, budgeting and curriculum development.

BUILDINGS & GROUNDS

The Audubon Board of Education continues to place a great emphasis on propermaintenance of the facilities. The district continues to budget for Capital Projects eachyear and the Buildings & Grounds Committee meets on a regular basis with theadministration to monitor the progress of the projects.

4. INTERNAL ACCOUNTING CONTROLS:

Management of the district is responsible for establishing and maintaining an internalcontrol structure designed to ensure that the assets of the District are protected from loss,theft or misuse and to ensure that adequate accounting data are compiled to allow for thepreparation of financial statements in conformity with generally accepted accounting

4

principles (GAAP). The internal control structure is designed to provide reasonable, but notabsolute, assurance that these objectives are met. The concept of reasonable assurancerecognizes that: (1) the cost of a control should not exceed the benefits likely to be derived;and (2) the valuation of costs and benefits requires estimates and judgments bymanagement.

As a recipient of federal and state financial assistance, the District also is responsible forensuring that an adequate internal control structure is in place to ensure compliance withapplicable laws and regulations related to those programs. This internal control structure isalso subject to periodic evaluation by the District management.

As part of the District's single audit described earlier, tests are made to determine theadequacy of the internal control structure, including that portion related to federal and statefinancial assistance programs, as well as to determine that the District has complied withapplicable laws and regulations.

5. BUDGETARY CONTROLS:

In addition to internal accounting controls, the District maintains budgetary controls. Theobjective of these budgetary controls is to ensure compliance with legal provisionsembodied in the annual appropriated budget approved by the voters of the municipality.Annual appropriated budgets are adopted for the general fund, the special revenue fund,and the debt service fund. Project-length budgets are approved for the capitalimprovements accounted for in the capital projects fund. The final budget amount asamended for the fiscal year is reflected in the financial section.

6. ACCOUNTING SYSTEM AND REPORTS:

The District's accounting records reflect generally accepted accounting principles, aspromulgated by the Governmental Accounting Standards Board (GASB). The accountingsystem of the District is organized on the basis of funds and account groups. These fundsand account groups are explained in "Notes to the Financial Statements", Note 1.

10. RISK MANAGEMENT:

The Board carries various forms of insurance, including but not limited to general liability,automobile liability and comprehensive/collision, hazard and theft insurance on propertyand contents, and fidelity bonds.

11. OTHER INFORMATION:

a) Independent Audit - State statutes require an annual audit by independent certifiedpublic accountants or registered municipal accountants. The accounting firm of Inversoand Stewart, RMAlCPAs, was selected by the Board's audit committee. In addition tomeeting the requirements set forth in state statutes, the audit also was designed to meetthe requirements of the Single Audit Act of 1984 and the related OMB Circular A-128 andstate Treasury Circular Letter 98-07 OMB. The auditor's report on the general purposefinancial statements and combining and individual fund statements and schedules isincluded in the financial section of this report. The auditor's reports related specifically tothe single audit are included in the single audit section of this report.

5

the single audit are included in the single audit section of this report.

12. ACKNOWLEDGMENTS:

We would like to express our appreciation to the members of the Audubon Board ofEducation for their concern in providing fiscal accountability to the citizens and taxpayers ofthe school district and thereby contributing their full support to the development andmaintenance of our financial operation. The preparation of this report could not have beenaccomplished without the efficient and dedicated services of our financial and accountingstaff.

Respectfully submitted,

j),~,.-~~3~Donald A. BordenSuperintendent

~~Robert DelengowskiBoard Secretary

6

AUDUBON BOARD OF EDUCATIONOrganizational Chart

(Unit Control)

Superintendent

1

M

t BuI Admln

SupBulldl

anslon Avenue GrSchool

PrincipalHavilandAvenueSchool

Principal CuMain

+DistricSpecla

Educatlo

sinessnlstrator

jervlsorngs and

ounds

stodlalltenance

HighSchoolPrincipal

11

1 1AssistantPrincipal

Guidance Athletics

!SAC.

7

AUDUBON SCHOOL DISTRICT

Members of the Board of Education:

Ralph Gilmore. PresidentPeggy Slack. Vice PresidentMarianne BrownDawn BentleyJennifer DawsonAllison CoxCheryl HauskeKathryn SullivanPatYacovelliCarl Ingram

Other Officials:

Roster of OfficialsJune 30, 2012

Donald T. Borden. SuperintendentRobert Delengowski. Business Administrator/Board SecretaryMary Lynam. TreasurerFrank Cavallo. Esq. Solicitor

8

Term Expires

201320132014201420142012201220132012

Mount Ephraim Representative

Attorney

AUDUBON SCHOOL DISTRICTConsultants and Advisors

Audit Firm

Inverso & Stewart, LLC12000 Lincoln Drive West, Suite 402

Marlton, NJ 08053

Frank Cavallo, EsquireActing for Parkerl McCay

Suite 104 Three Greentree CentreMarlton, NJ 08053

Official Depository

Susquehanna Patriot Bank, NA40 South White Horse Pike

Audubon, NJ 08106

9

Financial Section

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Lincoln Drin West, Suite 402Marlton, New Jersey 08053(856) 983-2244Fax (856) 983-6674E-Mail: [email protected]

-MemberoC-American Institute oC ePAsNew Jersey Society oCCPAs

INDEPENDENT AUDITOR'S REPORT

The Honorable President and Membersof the Board of Education

Audubon School DistrictCounty of CamdenAudubon, New Jersey

We have audited the accompanying financial statements of the governmental activities, the business-type activities, eachmajor fund and the aggregate remaining fund information of the Audubon School District, in the County of Camden. Stateof New Jersey (School District), as of and for the fiscal year ended June 30.2012. which collectively comprise the SchoolDistrict's basic financial statements as listed in the table of contents. These financial statements are the responsibility ofthe School District's management. Our responsibility is to express opinions on these financial statements based on ouraudit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America; thestandards applicable to financial audits contained in Govemment Auditing Standards, issued by the Comptroller General ofthe United States; and in compliance with audit requirements as prescribed by the Division of Finance. Department ofEducation. State of New Jersey. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includes consideration ofinternal control over financial reporting as a basis for deSigningaudit procedures that are appropriate in the circumstances.but not for the purpose of expressing an opinion on the effectiveness of the School District's internal control over financialreporting. Accordingly. we express no such opinion. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used andsignificant estimates made by management, as well as evaluating the overall financial statement presentation. We believethat our audit provides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financialposition of the govemmental activities, business-type activities. each major fund and the aggregate remaining fundinformation of the Audubon School District, in the County of Camden, State of New Jersey, as of June 3D, 2012, and therespective changes in financial position and, where applicable, cash flows thereof for the fiscal year then ended inconformity with accounting principles generally accepted in the United States of America.

In accordance with Govemment Auditing Standards, we have also issued our report dated September 27, 2012 on ourconsideration of the Audubon School District, in the County of Camden, State of New Jersey's internal control overfinancial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grantagreements and other matters. The purpose of that report is to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control overfinancial reporting or on compliance. That report is an integral part of an audit performed in accordance with GovemmentAuditing Standards and should be considered in assessing the results of our audit.

11

The accompanying management's discussion and analysis and budgetary comparison information, as listed in the table ofcontents, are not a required part of the basic financial statements but are supplementary information required byaccounting principles generally accepted in the United States of America. We have applied certain limited procedures,which consisted principally of inquiries of management regarding the methods of measurement and presentation of therequired supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise theAudubon School District's basic financial statements. The accompanying Schedule of Expenditures of Federal Awardsand State Financial Assistance are presented for purposes of additional analysis as required by U.S. Office ofManagement and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and State ofNew Jersey Circular D4-04-0MB, Single Audit Policy for Recipients of Federal Grants, State Grants and State Aid, and arenot a required part of the financial statements. In addition, the introductory section, combining statements and relatedmajor fund supporting statements and schedules, and statistical section listed in the table of contents are also presentedfor purposes of additional analysis and are not a required part of the basic financial statements. The Schedules ofExpenditures of Federal Awards and State Financial Assistance, combining statements and related major fund supportingstatements and schedules have been subjected to the auditing procedures applied in the audit of the basic financialstatements and, in our opinion, are fairly stated in all material respects in relation to the basic financial statements taken asa whole. The introductory and statistical sections have not been subjected to the auditing procedures applied in the auditof the basic financial statements, and accordingly, we express no opinion on them.

Respectfully submitted,

INVERSO & STEWART, LLCCertified Public Accountants

~~Q!c_ \Robert A. StewartCertified Public AccountantRegistered Municipal Accountant

Marlton, New JerseySeptember 27, 2012

12

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Lincoln Drive West, Suite 402Marlton, New Jersey 08053(856) 983·2244Fax (856) 983·6674E-Mail: IscPlIs.Wcootfn!ric.nel

-:\Iember or·American Institute or ePAsNew Jersey Society or ePAs

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTINGAND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

The Honorable President and Membersof the Board of Education

Audubon School DistrictCounty of CamdenAudubon. New Jersey

We have audited the financial statements of the governmental activities, the business-type activities, each major fund andthe aggregate remaining fund information of the Audubon School District (School District), in the County of Camden. Stateof New Jersey, as of and for the fiscal year ended June 30, 2012. which collectively comprise the School District's basicfinancial statements and have issued our report thereon dated September 27. 2012. We conducted our audit inaccordance with auditing standards generally accepted in the United States of America; the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; andin compliance with audit requirements as prescribed by the Division of Finance. Department of Education. State of NewJersey.

Internal Control Over Financial Reporting

Management of the Audubon School District is responsible for establishing and maintaining effective internal control overfinancial reporting. In planning and performing our audit, we considered the Audubon School District's internal control overfinancial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on thefinancial statements, but not for the purpose of expressing an opinion on the effectiveness of the School District's internalcontrol over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the School District'sinternal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees,in the normal course of performing their assigned functions, to prevent. or detect and correct misstatements on a timelybasis. A material weakness is a deficiency. or combination of deficiencies, in internal control, such that there is areasonable possibility that a material misstatement of the School District's financial statements will not be prevented, ordetected and corrected on a timely basis.

Our consideration of internal control over financial reporting was for the limited purpose described in the first paragraph ofthis section and was not designed to identify all deficiencies in internal control over financial reporting that might bedeficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control overfinancial reporting that we consider to be material weaknesses, as defined above.

13

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Audubon School District's financial statements are free ofmaterial misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts andgrant agreements, noncompliance with which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisions was not an objective of our auditand, accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance orother matters that are required to be reported under Government Auditing Standards and audit requirements as prescribedby the Division of Finance, Department of Education, State of New Jersey.

We noted certain matters that we reported to management of the Audubon School District in a separate report entitled,Auditors Management Report on Administrative Findings - Financial, Compliance and Performance dated September 27,2012.

This report is intended solely for the information and use of the management of the School District, the Division of Finance,Department of Education. State of New Jersey, and federal and state awarding agencies and pass-through entities and isnot intended to be and should not be used by anyone other than these specified parties.

Respectfully submitted,

INVERSO & STEWART, LLCCertified Public Accountants

Robert A. StewartCertified Public AccountantRegistered Municipal Accountant

Mariton, New JerseySeptember 27,2012

14

Required Supplementary Information - Part I

Management's Discussion and Analysis

Audubon School DistrictManagement's Discussion and AnalysisFor the Fiscal Year Ended June 30, 2012

As management of the Board of Education of the Borough of Audubon, New Jersey (SchoolDistrict), we offer readers of the School District's financial statements this narrative overview andanalysis of the School District for the fiscal year ended June 30, 2012. We encourage readers toconsider the information presented in conjunction with additional information that we havefurnished in our letter of transmittal, which can be found in the introductory section of this report.

Financial Highlights

• The assets of the School District exceeded its liabilities at the close of the mostrecent fiscal year by $10,348,565 (net assets).

• Governmental activities have an unrestricted net assets deficit of $1,274,859. Theaccounting treatment in the governmental funds for compensated absences payable,accrued interest payable, the June state aid payments, and state statutes thatprohibit school districts from maintaining more than 2% of its adopted budget asunrestricted fund balance are primarily responsible for this deficit balance.

• The total net assets of the School District increased by $178,862 or a 1.75% increasefrom the prior fiscal year-end balance. The majority of the reason for the increasewas the payment of long-term liabilities.

• Fund balance of the School District's governmental funds increased by $316,288resulting in an ending fund balance of $666,014. The majority of the reason for theincrease was the receipt of additional state aid and the implementation of the schoolchoice program.

• Business-type activities have unrestricted net assets of $152,321, which may beused to meet the School District's ongoing obligations of the enterprise-relatedactivities.

• The School District's long-term obligations decreased by $705,000 which is the resultof current year payments on existing debt obligations.

Overview of the Basic Financial Statements

This discussion and analysis is intended to serve as an introduction to the School District's basicfinancial statements. Comparison to the prior year's activity is provided in this document. Thebasic financial statements are comprised of three components: 1} District-wide financialstatements, 2} Fund financial statements, and 3) Notes to the basic financial statements. Thisreport also contains other supplementary information in addition to the basic financial statementsthemselves.

District-wide Financial Statements

The district-wide financial statements are designed to provide the reader with a broad overview ofthe financial activities in a manner similar to a private-sector business. The district-wide financialstatements include the statement of net assets and the statement of activities.

16

The statement of net assets presents information about all of the School District's assets andliabilities. The difference between the assets and liabilities is reported as net assets. Over time,changes in net assets may serve as a useful indicator of whether the financial position of theSchool District is improving or deteriorating.

The statement of activities presents information showing how the net assets of the School Districtchanged during the current fiscal year. Changes in net assets are recorded in the statement ofactivities when the underlying event occurs, regardless of the timing of related cash flows. Thus,revenues and expenses are reported in this statement even though the resulting cash flows maybe recorded in a future period.

Both of the district-wide financial statements distinguish functions of the School District that aresupported from taxes and intergovernmental revenues (governmental activities) and otherfunctions that are intended to recover all or most of their costs from user fees and charges(business-type activities). Governmental activities consolidate governmental funds including theGeneral Fund, Special Revenue Fund, Capital Projects Fund, and Debt Service Fund. Business-type activities consolidate the Food Service Fund, the Community Education Program Fund andthe After School Program Fund.

Fund Financial Statements

Fund financial statements are designed to demonstrate compliance with finance-relatedrequirements. A fund is a grouping of related accounts that is used to maintain control overresources that have been segregated for specific objectives. All of the funds of the SchoolDistrict are divided into three categories: governmental funds, proprietary funds and fiduciaryfunds.

Governmental funds account for essentially the same information reported in the governmentalactivities of the district-wide financial statements. However, unlike the district-wide financialstatements, the governmental fund financial statements focus on near-term financial resourcesand fund balances. Such information may be useful in evaluating the financing requirements inthe near term.

Since the governmental funds and the governmental activities report information using the samefunctions, it is useful to compare the information presented. Because the focus of each reportdiffers, a reconciliation is provided on the fund financial statements to assist the reader incomparing the near-term requirements with the long-term needs.

The School District maintains four individual governmental funds. The major funds are theGeneral Fund, the Special Revenue Fund, the Capital Projects Fund, and the Debt Service Fund.They are presented separately in the fund financial statements.

The School District adopts an annual appropriated budget for the General Fund, Special RevenueFund and the Debt Service Fund. A budgetary comparison statement has been provided for eachof these funds to demonstrate compliance with budgetary requirements.

Proprietary funds are used to present the same functions as the business-type activitiespresented in the district-wide financial statements. The School District maintains one type ofproprietary fund - the Enterprise Fund. The fund financial statements of the enterprise fundprovides the same information as the district-wide financial statements, only in more detail.

The School District's three enterprise funds (Food Service Fund, Community Education ProgramFund and After School Program Fund) are listed individually and are considered to be majorfunds.

17

Fiduciary funds are used to account for resources held for the benefit of parties outside thegovernment. Fiduciary funds are not reflected in the district-wide financial statements becausethe resources of those funds are not available to support the School District's programs.

Notes to the Basic Financial Statements

The notes to the basic financial statements provide additional information that is essential to a fullunderstanding of the data provided in the basic financial statements.

Other Information

In addition to the basic financial statements and accompanying notes, this report also containsother supplementary information and schedules required by the New Jersey Audit Program,issued by the New Jersey Department of Education.

District-wide Financial Analysis

The assets of the School District are classified as current assets and capital assets. Cash,investments, receivables, inventories and prepaid expenses are current assets. These assetsare available to provide resources for the near-term operations of the School District. Themajority of the current assets are the results of the tax levy and state aid collection process.

Capital assets are used in the operations of the School District. These assets are land, buildings,improvements and equipment. Capital assets are discussed in greater detail in the section titled,Capital Assets and Debt Administration, elsewhere in this analysis.

Current and long-term liabilities are classified based on anticipated liquidation either in the near-term or in the future. Current liabilities include accounts payable, accrued salaries and benefits,unearned revenues, and current debt obligations. The liquidation of current liabilities isanticipated to be either from currently available resources, current assets or new resources thatbecome available during fiscal year 2012. Long-term liabilities such as long-term debt obligationsand compensated absences payable will be liquidated from resources that will become availableafierfiscalyear2012.

The assets of the primary government activities exceeded liabilities by $10,172,430 with anunrestricted deficit balance of $1,274,859. The net assets of the primary government do notinclude internal balances.

A net investment of $10,587,578 in land, improvements, buildings, equipment and vehicles whichprovide the services to the School District's public school students. Net assets of $883,525 havebeen restricted as follows:

Restricted for Future Budget Appropriations $Restricted for Future Tuition CostsRestricted for Future Capital ProjectsRestricted for Subsequent Year's Budget

302,71372,31745,790

462,705

Total $ 883,525

18

Audubon School DistrictComparative Summary of Net Assets

As of June 30, 2012 and 2011

Governmental Activities Business-Type Activities District-Wide2012 2011 2012 2011 2012 2011

ASSETSCurrent assets $ 2,331,051 $ 1,859,615 $ 154,175 $ 190,708 $ 2,485,226 $ 2,050,323Capital assets 21.2681941 2114831212 231814 231521 211292.755 21,5061733

Total assets 23,5991992 2313421827 1771989 2141229 23.7771981 23,5571056

LIABILITIESCurrent liabilities 2,474,655 2,347,885 1,854 13,922 2,476,509 2,361,807Noncurrent liabilities 10.9521907 111025.546 1019521907 11.025,546

Total liabilities 1314271562 1313731431 1854 131922 13,4291416 13.3871353

Net Assets $10.1721430 $ 91969.396 s 176,135 $ 200,307 $10,348.565 $10.169.703

Net Assets Consist of:Invested in Capital Assets $10,563,764 $10,778,212 $ 23,814 $ 23,521 $10,587,578 $10.801.733Restricted Assets 883,525 529,251 883,525 529,251Unrestricted Assets {112741859} {11338,067} 1521321 176.786 {1,122,538} {1,161,281}

Net Assets $10,172,430 $ 9,969,396 $ 1761135 $ 200,307 $10,348,565 $10,169,703

Governmental Activities

Governmental activities increased the net assets of the School District by $203,034 during thecurrent fiscal year. Key elements of the increase in net assets for governmental activities are asfollows:

• Long-term debt obligations were reduced by $705,000 accounting for the majorityof the increase in net assets.

• School choice aid increased revenues by $91,128.

• Additional state aid increased revenues by $121,650.

Business-type Activities

Business-type activities decreased the School District's net assets by $24,172. Key elements ofthe decrease in net assets for business-type activities are as follows:

• The Food Service Fund operated at a loss of $39,973 for this fiscal year beforeaccounting for a transfer from the operating fund of $11,354. The net assetsbalance at June 30, 2012 for the food service fund was $23,814.

• The Community Education Program Fund operated at a profit of $11,509 for thisfiscal year. The net assets balance at June 30, 2012 for the communityeducation program fund was $129,827.

• The After School Fund operated at a loss of $7,062 for this fiscal year. The netassets balance at June 30,2012 for the after school fund was $22,494.

19

Audubon School DistrictComparative Schedule of Changes in Net Assets

As of and for the Fiscal Year Ended June 30, 2012 and 2011

Revenues:Charges for servicesOperatinggrants and

contributionsPropertytaxesState aid - unrestrictedOther revenues

Total Revenues

Expenses:GovernmentalActivities:InstructionTuitionRelated servicesAdministrativeservicesOperations andMaintenance

TransportationEmployeebenefitsInterest on debtOther

Business-TypeActivities:Food ServiceCommunity EducationAfter School Program

Total EpensesIncrease(Decrease) in NetAssets before transfers

TransfersChange in Net AssetsNetAssets, July 1NetAssets, June 30

Governmental Activities2012 2011

$ 2,861,756

2,362,86711,053,1857,290,221

322,73623,890.765

9,927.770981.328

2,194,1561,943.711

1,725.813341.603

5,234,737701.040626,219

23.676,377

214.388(11,354)203.034

9,969.396$ 10,172.430

$2,702,485

2.163,17610,774,5916.763.062

199.82722.603.141

9,595,767789.288

2,208,5811,771,932

1,849,599334.505

4.794.167466,463616,756

22,427,058

176,083(33,098)142,985

9.826,411$9.969,396

Business-Type Activities2012 2011

$ 427,289

145,719

851573,859

427,49672,997

108.892609.385

(35,526)11,354

(24,172)200,307

$ 176,135

$ 478,746

117,742

1414597,902

432,21676,943

110.980620,139

(22,237)33,09810,861

189,446$ 200,307

Financial Analysis of the Governmental Funds

District-Wide2012 2011

$ 3,289,045

2,508,58611,053,1857,290,221

323.58724,464.624

9,927,770981,328

2,194,1561,943,711

1,725,813341,603

5,234,737701,040626,219

427,49672,997

108,89224.285.762

178,862

178,86210,169.703

$ 10.348.565

As noted earlier, the School District uses fund accounting to ensure and demonstrate compliancewith finance-related legal requirements.

Governmental Funds - The focus of the School District's governmental funds is to provideinformation on near-term inflows, outflows, and balances of spend able resources. Suchinformation is useful in assessing the School District's financing requirements. In particular,unreserved fund balance may serve as a useful measure of a government's net resourcesavailable for spending at the end of the fiscal year.

As of the end of the current fiscal year, the School District's governmental funds reported acombined ending fund balance of $666,014, an increase of $316,288 in comparison with the prioryear. Additional state aid and school choice aid accounts for the majority of this increase.

20

$ 3,181,231

2,280,91810,774,5916,763,062

201.24123,201,043

9,595,767789,288

2,208,5811,771,932

1,849,599334,505

4.794,167466,463616,756

432,21676,943

110.98023,047.197

153,846

153,84610.015,857

$ 10.169,703

The unreserved fund balance for the School District at the end of the fiscal year represents theunreserved deficit fund balance for the General Fund of $217,511. The remainder of the fundbalance is reserved to indicate that it is not available for new spending because it has alreadybeen committed as follows, 1) appropriated as a revenue source in the subsequent year's budget($462,705),2) reserved for future tuition payments in accordance with state statutes ($72,317),3)reserved for capital projects expenditures ($45,790), or reserved for future appropriation inaccordance with state statutes ($302,713).

The general fund is the chief operating fund of the School District. As discussed earlier, thedeficit balance in the unreserved fund balance is due, primarily, to the accounting treatment of theJune state aid payments as discussed in the notes to the basic financial statements, and statestatutes that prohibit New Jersey school districts from maintaining more than 2% of its adoptedbudget as unrestricted fund balance.

Revenue in the special revenue fund is generally recognized at the time that the outlays areidentified; therefore no fund balances are normally generated in the special revenue fund.

General Fund Budgetary Highlights

There is no difference between the original budget and the revised budget.

At the end of the current fiscal year, unreserved fund balance (budgetary basis) of the generalfund was $472,263, while total fund balance (budgetary basis) was $1,325,111. As a measure ofthe general fund's liquidity, it may be useful to compare both unreserved fund balance (budgetarybasis) and total fund balance (budgetary basis) to total general fund expenditures. Actual(budgetary basis) expenditures of the General Fund including other financing uses amounted to$22,209,302. Unreserved fund balance (budgetary basis) represents 2.12% of expenditureswhile total fund balance (budgetary basis) represents 5.96% of that same amount.

Capital Asset and Debt Administration

The School District's investment in capital assets for its governmental and business-type activitiesas of June 30,2012, totaled $21,292,755 (net of accumulated depreciation). This investment incapital assets includes land, improvements. buildings and equipment. The total decrease in theSchool District's investment in capital assets for the current fiscal year was $213,978.

Major capital assets events during the current fiscal year included the following:

• Depreciation expense for the current fiscal year was $665,909.

Capital Asset (net of accumulated depreciation)June 30,2012 and 2011

Governmental Activities2012 2011

Business-Typel Activities2012 2011

District-Wide2012 2011

Land s 764.000 $ 764.000 $ 764.000 $ 764.000Const. in ProgressSite Improvements 719.592 759.826 719.592 759.826Building and Building

Improvements 19,162,999 19.273.676 19,162,999 19.273.676Equipment 622.350 685.710 $ 23.814 $ 23.521 646.164 709.231

Net Assets $ 21.268.941 $ 21,483.212 $ 23.814 $ 23,521 $ 21.292.755 $21,506.733

21

Additional information on the School District's capital assets can be found in the notes to thebasic financial statements (Note 5) of this report.

Long-term debt - During the fiscal year ended June 30, 2012, the School District had totalbonded debt outstanding of $10,410,000 backed by the full faith and credit of the School District.Additionally, the School District has long-term obligations for capital leases in the amount of$295,177 and compensated absences balance of $1,070,038 outstanding at the end of thecurrent fiscal year.

General Obligation Bonds for the School District decreased by $705,000, reflecting debt servicepayments made during the year.

The School District continues to maintain its AA rating from Standard & Poor's Corporation for itsgeneral obligation bond issues.

State statutes limit the amount of general obligation debt that the District may issue. At the end ofthe current fiscal year, the legal debt limit was $30,088,948 and the legal debt margin was$19,678,948.

Additional information on the School District's long-term obligations can be found in the notes tothe basic financial statements (Note 7) of this report.

Economic Factors and Next Year's Budgets and Rates

The following factors were considered and incorporated into the preparation of the SchoolDistrict's budget for the 2012-2013 fiscal year.

• The 2012-2013 budget increased by $439,769 (2.14%) over the previous year's budget.Despite big increases in out-of-district placements (25%) and health benefits (15%), thedistrict realized savings from the retirement of six staff members, and was able to reducea number of budget line items from the previous year.

• For the first time in several years the budget received an increase in State Aid. In April2012 the Audubon School District was chosen to participate in the Inter-district PublicSchool Choice Program. The district will have fifty students attend Audubon High Schoolunder this program for the 2012-2013 school year. From a financial standpoint thedistrict received $417,450 in state aid for these students

• With the additional revenue generated through the school choice program, the districtwas able to keep the tax levy under the 2% cap. The tax levy increase for the 2012-2013school year was at 1% or just over $100,000.

• The district continues to budget funds for capital improvements. For the 2012-2013school year the district has increased its capital budget by almost $400,000. This year'scapital budget includes a new boiler system for the Haviland Avenue School as well asfunds for additional technology purchases.

• The Audubon School District has committed itself to strong financial controls. TheBusiness office continually monitors spending requests in relation to the district budgetand is committed to review its business practices in order to maximize revenues andgenerate a budget surplus each year. Additionally, the district is looking to improve itsuse of technology in the coming years in an effort to meet all future educationalchallenges.

22

Requests for Information

This financial report is designed to provide a general overview of the School District's finances forall those with an interest in the School District. Questions concerning any of the informationprovided in this report or requests for additional financial information should be addressed to theAudubon School District Business Administrator, 350 Edgewood Avenue, Audubon, New Jersey,08106, telephone number (856) 547-1716.

23

Basic Financial Statements

District-Wide Financial Statements

A-1AUDUBON SCHOOL DISTRICT

Statement of Net AssetsJune 30, 2012

Governmental Business-TypeActivities Activities Total

ASSETS:Cash and cash equivalents $ 432,764 $ 120.865 $ 553,629Receivables. net 1.809.122 20.763 1,829,885Inventory 12.547 12.547Restricted assets:

Cash and cash equivalents 15,113 15,113Deferred bond issuance costs - net 74,052 74.052Capital assets. net (Note 5) 21.2681941 231814 2112921755

Total Assets 2315991992 177 989 23.7771981

LIABILITIES:Accounts payable 738,675 1,854 740.529State aid anticipation note payable 681,264 681.264Deferred revenues 171,046 171.046Accrued interest payable 61,362 61.362Noncurrent liabilities (Note 7):

Due within one year 822.308 822.308Due beyond one year 1019521907 10.9521907

Total Liabilities 13,427.562 1854 13.429,416

NET ASSETS:Invested in capital assets. net of related debt 10,563.764 23,814 10.587,578Restricted for:

Capital projects 45.790 45.790Other purposes 837.735 837,735

Unrestricted {1.27418591 152.321 p.122.5381

Total Net Assets ;i 10,172,430 ~ 176,135 ~ 10,348,565

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

26

A-2

AUDUBON SCHOOL DISTRICTStatement of Activities

For the Fiscal Year Ended June 30, 2012

Net (Expense) Revenue andProgram Revenues Changes In Net Assets

Operating CapitalCharges for Grants and Grants and Governmental Business-Type

FunctionsIP!2Srams Exe!nses Services Contributions Contrtbutlons Activities Activities Total

Govemmental Activities:Instruction:

Regular $ 6,699,651 $ 2,861,756 $ (3,837,895) $ (3,837,895)Special Education 2,103,198 $ 411,980 (1,691,218) (1,691,218)Other instruction 1,124,921 (1,124,921) (1,124,921)

Support Services:Tuition 981,328 (981,328) (981,328)Student & instruction related services 2,194,158 81,727 (2,112,429) (2,112,429)General administrative services 468,260 (468,260) (468,260)School administrative services 982,722 (982,722) (982,722)Central administrative services 492,729 (492,729) (492.729)Plant operations and maintenance 1.725.813 (1.725.813) (1.725.813)Pupil transportation 341,603 (341,603) (341.603)Unallocated employee benefits 5.234.737 1.758.865 (3.477.852) (3.477.852)

N Interest on long-term debt 701.040 112.275 (588.765) (588.765)....,Unallocated depreciation and amortization 626,219 1626,219~ 1626,2191

Total Govemmental Activities 23,676,377 2,861,756 2,362,867 {18,451,754} {18,451,754}

Business-Type Activities:Food service 427.496 S 241,804 145,719 S (39.973) (39.973)Community education program 72.997 83,655 10,658 10,658Arter school program 108,892 101 830 !Z,0621 !Z,0621Total Business- Type Activities 609,385 427,289 145,719 138,3771 136,3771

Total Primary Govemment 124.285,762 $3.289.045 12,508,586 118,451,754) 136,377) 118,488,131}

General Revenues:Taxes:

Property taxes, levied for general purposes, net 10,010,169 10,010,169Taxes levied for debt service 1,043,016 1.043.016

Federal and State aid not restricted 7.290.221 7.290,221Miscellaneous Income 322.736 851 323,587

Special Items:TransferTransfer 111.3541 11.354

Total general revenues, special items, extraordinary items and transfers 18,654,788 12,205 18,666,993Change in Net Assets 203.034 (24,172) 178,862Net Assets· June 30. 2011 9,969,396 200,307 10,169,703Net Assets - June 30. 2012 ! 10,172,430 1 176,135 i 10.348,565

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

Fund Financial Statements

B-1AUDUBON SCHOOL DISTRICT

Balance SheetGovernmental Funds

June 3D, 2012

Special Capital Debt TotalGeneral Revenue Projects Service Governmental

ASSETS Fund Fund Fund Fund Funds

Assets:Cash and cash equivalents $ 982,000 $ (183,167) $ (366,069) $ 432,764

Receivables, net:District tax levy 698,856 698,856State aid 145,850 396,746 542,596Federal aid 71.055 381,495 452,550Other 115,120 115,120

Restricted assets:Cash and cash equivalents 15113 15113

Total Assets $ 2,027,994 S 198,328 S 30,677 ~ S 2,256,999

UABIUTIES AND FUND BALANCESUabilities:Accounts payable s 711,393 $ 27,282 $ 738.675Deferred revenue 171,046 171,046State aid anticipation note payable 681,264 681.264

Total Liabilities 1,392,657 198,328 1.590,985

Fund Balances:Restricted for:

Excess surplus 302,713 302,713Tuition reserve 72,317 72,317Capital reserve 15,113 30,677 45,790

Assigned to:Subsequent year's budget 462,705 462,705

Unassigned {217,511} 1217.511}

Total Fund Balances 635,337 30,677 666.014

Total Liabilities and Fund Balances ~ 2,027,994 ~ 198,328 ~ 30,677 $

Amounts reported for govemmental activities in the statement of net assets(A-1) are different because:

Capital assets used in governmental activities are not financial resourcesand therefore are not reported in the funds. The cost of the assets is$31,126,202 and the accumulated depreciation is $8,857,261. 21,268,941

Bond issuance costs are amortized over the life of the bonds on thestatement of net assets. 74,052

Long-term liabilities, including bonds payable, are not due and payablein the current period and therefore are not reported as liabilities in thefunds:

General Obligation BondsCapital Lease PayableAccrued Interest PayableCompensated Absences Payable

$ (10,410,000)(295,177)(61,362)

(1.070,038}(11,836,577)

S 10,172,430Net assets of govemmental activities

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

29

B·2AUDUBON SCHOOL DISTRICT

Statement of Revenues, Expenditures and Changes In Fund BalancesGovernmental Funds

For the Fiscal Year Ended June 30, 2012

Special Capital Debt TotalGeneral Revenue Projects Service Govemmental

Fund Fund Fund Fund FundsREVENUES:Local sources:Local tax levy s 10,010,169 s 1,043,016 s 11,053,185Tuition 2,861,756 2,861,756Miscellaneous 322,736 322.736

Total local sources 13,194,661 1,043,016 14,237,677

State sources 8,785,408 112,275 8,897,683Federal sources 261,698 $ 493,707 755.405

Total Revenues 22,241,767 493,707 1,155,291 23,890.765

EXPENDITURES:Current expense:

Regular instruction 6,629,431 6,629.431Special education instruction 1,691,218 411,980 2,103,198Other instruction 1,124,921 1,124,921Support services and undistributed costs:Tuition 981,328 981,328Student & instruction related services 2,112,429 81,727 2,194.156General administrative services 467,745 467.745School administrative services 982,722 982,722Central administrative services 492,729 492,729Plant operations and maintenance 1,706,521 1.706,521Pupil transportation 332,230 332,230Unallocated employee benefits 5,234,737 5,234,737

Capital outlay 453,291 453,291Debt service:

Principal 705,000 705,000Interest and other charges 450.291 450,291

Total Expenditures 22,209.302 493.707 1,155,291 23,858,300

Excess (deficiency) of revenues over(under) expenditures 32,465 32.465

Other Financing Sources (Uses):Capital lease 295,177 295,177Transfers out {11,354! {11,354!

Total other financing sources (uses) 283.823 283.823

Net Change in Fund Balance 316,288 316,288Fund balance - July 1, 2011 319,049 $ 30,677 349,726

Fund Balance - June 30.2012 ~ 635,337 s ~ 30,677 ~ ~ 666,014

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

30

AUDUBON SCHOOL DISTRICTReconciliation of the Statement of Revenues, Expenditures

and Changes In Fund Balances of Governmental Fundsto the Statement of Activities

For the Fiscal Year Ended June 30, 2012

Total net change in fund balances - governmental funds (from B-2)

Amounts reported for governmental activities in the statement of activities (A-2)are different because:

Governmental Funds report capital outlays as expenditures. However, in thestatement of activities, the cost of those assets is allocated over their estimateduseful lives as depreciation expense. This is the amount by which capitaloutlays exceeded depreciation in the current period.

Depreciation expenseFixed assets additions

$ (661,027)446,756

Repayment of long-term debt is an expenditure in the governmental funds,but the repayment reduces long-term liabilities in the statement of net assetsand is not reported in the statement of activities.

The issuance of long-term debt provides current financial resources tothe funds but has no effect on net assets.

Governmental funds report the effect of issuance costs, premiums, discountsand similar items when debt is first issued, whereas these amounts are deferredand amortized in the statement of activities. This amount is the net effect ofthese differences.

Interest on long-term debt in the statement of activities is accrued, regardlessof when due. In the governmental funds, interest is reported when due. Thisamount is the net effect of the difference in the treatment of interest onlong-term debt.

In the statement of activities, certain operating expenses, (e.g. compensatedabsences) are measured by the amounts earned during the year. In thegovernmental funds, however, expenditures for these items are reported in theamount of financial resources used (paid). When the earned amount exceedsthe paid amount, the difference is a reduction in the reconciliation (-); whenthe paid amount exceeds the earned amount the difference is an addition tothe reconciliation (+)

Change in net assets of governmental activities

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

31

B-3

$ 316,288

(214,271)

705,000

(705,177)

(13,565)

159,251

(44,492)

$ 203,034

B-4AUDUBON SCHOOL DISTRICT

Statement of Net AssetsProprietary Funds

June 30, 2012

Business- Type ActivitiesEnterprise Funds

Food Community AfterService Education School

Fund Program Program TotalASSETS:

Current Assets:Cash and cash equivalents $ (31,456) $ 129,827 $ 22,494 $ 120,865Intergovernmental receivables

State 650 650Federal 20,113 20,113

Inventories 12,547 12,547

Total current assets 1854 129,827 22,494 154,175

Noncurrent assets:Machinery and equipment (net ofaccumulated depreciation) 23,814 23814

Total noncurrent assets 23,814 23,814

Total Assets 25,668 129,827 22,494 177,989

LIABILITIES:Current liabilities:

Accounts payable 1854 1,854

Total Current Liabilities 1854 1854

NET ASSETS:Invested in capital assets 23,814 23,814Unrestricted 129,827 22,494 152.321

Total Net Assets $ 23,814 i 129,827 i 22,494 i 176,135

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

32

B-5AUDUBON SCHOOL DISTRICT

Statement of Revenues, Expenses and Changes in Fund Net AssetsProprietary Funds

For the Fiscal Year Ended June 30, 2012

Business-Type ActivitiesEnter~rise Funds

Food Community AfterService Education School

Fund Pro9ram Pro9ram TotalsOperating Revenues:

Charges for services:Daily sales:

Reimbursable programs $ 119,719 $ 119,719Non-reimbursable programs 122,085 122,085

Program fees $ 83,655 $ 101,830 185,485

Total Operating Revenue 241,804 83,655 101,830 427,289

Operating Expenses:Salaries and fringe benefits 221,502 29,063 108,003 358,568Management fee 21,781 21,781Supplies and materials 15,351 889 16,240Other costs 5,820 5,820Depreciation 4,882 4,882Cost of sales 158,160 43,934 202,094

Total Operating Expenses 427,496 72,997 108:892 609:385

Operating Income (loss) (185,692} 10,658 {7:062} (182:096}

Non-Operating Revenues:State sources:

State school lunch program 3,988 3,988Federal sources:

National school lunch program 119,583 119,583Food distribution program 22,148 22,148

local sources:Interest earned 851 851

Total Non-Operating Revenues 145,719 851 146,570

Income (loss) before Contributions and Transfers (39,973) 11,509 (7,062) (35,526)

Operating Transfers In 11:354 11,354

Change in Net Assets (28,619) 11,509 (7,062) (24,172)Net Assets - July 1, 2011 52,433 118:318 29,556 200,307

Net Assets - June 30, 2012 $ 23,814 ~ 129,827 ~ 22,494 ~ 176,135

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

33

B-6AUDUBON SCHOOL DISTRICT

Statement of Cash FlowsProprietary Funds

For the Fiscal Year Ended June 30, 2012

Business-Type ActivitiesEnte!Erise Funds

Food Community AfterService Education School

Fund Proaram Program TotalCash Flows from Operating Activities:

Cash receipts from customers S 279.220 S 83.655 S 101.830 S 464.705Cash payments 10 employees for services (221.502) (29.063) (108.003) (358.568)Cash payments to suppliers for goods

and services (214.260) (43.934~ !889~ !259.083)

Net cash used by operating activities (156.542) 10.658 17.062) !152.946)

Cash Flows from Noncapltal Financing Activities:Cash received from state sources 3.338 3.338Cash received from federal sources 121.618 121.618Operating transfer in 11.354 11.354

Net cash provided by noncapitalfinancing activities 136.310 136.310

Cash Flows Used by Capital andRelated Financing Activities:

Purchase of equipmenl (5.175) ~5.175!

Cash Flow Provided by Investing Activities:Interest on cash equivalents 851 851

Net increase (decrease) in cashand cash equivalents (25,407) 11,509 (7,062) (20.960)

Cash and cash equivalents - July 1, 2011 (6.049) 118.318 29.556 141.825

Cash and cash equivalents - June 30, 2012 S (31.456) S 129.827 $ 22.494 S 120.865

Reconciliation of operating Income (loss)to net cash provided by (used for)

operating activities:Operating Income (loss) S (185.692) S 10.658 S (7,062) S (182.096)Adjustments to reconcile operating income

(loss) to cash provided by (used for)operating activities:

Depreciation 4,882 4.882Change In assets and liabilities:

(Increase) decrease in accounts receivable 37,416 37,416(Increase) decrease in inventory (1.080) (1.080)Increase (decrease) in accounts payable (12,068) (12.068)

Net cash provided by (used for)operating activities S (156.542) $ 10.658 $ (7.062) S (152,946)

Noncash Noncapltal Financing Activities:During the year the District received $22,148 of food commodities from theU.S. Department of Agriculture.

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

34

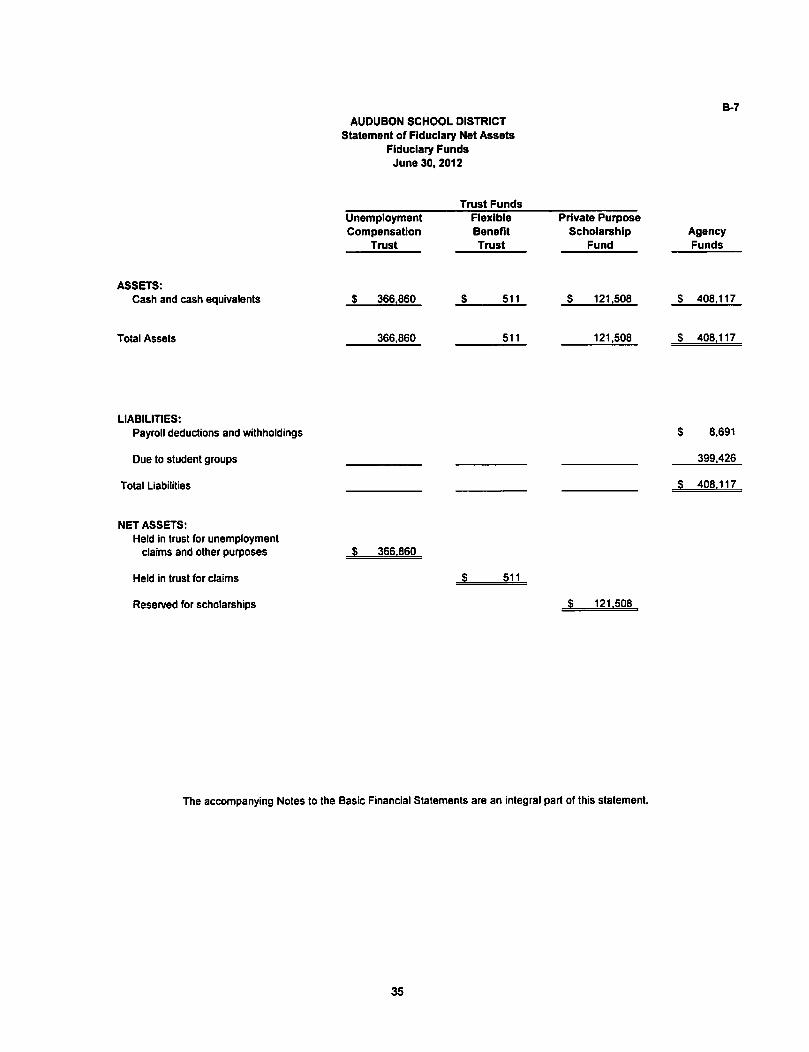

ASSETS:Cash and cash equivalents

Total Assets

LIABILITIES:Payroll deductions and withholdings

Due to student groups

Total Liabilities

NET ASSETS:Held in trust for unemployment

daims and other purposes

Held in trust for daims

Reserved for scholarships

AUDUBON SCHOOL DISTRICTStatement of Fiduciary Net Assets

Fiduciary FundsJune 30, 2012

Trust FundsUnemploymentCompensation

Trust

$ 366.860

366,860

S 366.860

FlexibleBenefitTrust

s 511

Private PurposeScholarship

Fund

$ 121,508

121,508

$ 121,508

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

35

511

$ 511

B-7

AgencyFunds

S 408.117

$ 408,117

s 8.691

399.426

S 408,117

B-8AUDUBON SCHOOL DISTRICT

Statement of Changes in Fiduciary Net AssetsFiduciary Funds

For the Fiscal Year Ended June 30, 2012

Unemployment Flexible Private PurposeCompensation Benefit Scholarship

Trust Trust FundADDmONS:

Contributions:Employee $ 12,257 $ 1,400Donations $ 8.000

Total Contributions 12,257 1,400 8.000

Interest eamed on investments 2151 834

Total Additions 14408 1401 8834

DEDUCTIONS:Claims paid 22.875 890Scholarships awarded 13.700

Total Deductions 22,875 890 13,700

Change in Net Assets (8,467) 511 (4,866)

Net Assets - July 1, 2011 375.327 126.374

Net Assets - June 30, 2012 $ 366,860 ~ 511 $ 121,508

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

36

Audubon School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity - The Borough of Audubon School District ("School District") is a Type II district located in the County ofCamden, State of New Jersey. As a Type II district, the School District functions independently through a Board ofEducation. The Board of Education is comprised of nine members elected to three-year terms. These terms are staggeredso that three member's terms expire each year. The purpose of the School District is to provide educational services forresident students in grades K through 12. In addition, the School District provides educational services for students ingrades 9 through 12 received from the Mount Ephraim School District, on a tuition basis. The Audubon School District hasan approximate enrollment at June 3D, 2012 of 1,439 students.

The primary criteria for including activities within the School District's reporting entity, as set forth in Section 2100 of theGovernmental Accounting Standards Board (GASB) Codification of Governmental Accounting and Financial ReportingStandards is the degree of oversight responsibility maintained by the School District. Oversight responsibility includesfinancial interdependency, selection of governing authority, designation of management, ability to significantly influenceoperations and accountability for fiscal matters. The combined financial statements include all funds of the School districtover which the Board exercises operating control. There were no additional entities required to be included in the reportingentity under the criteria as described above. Furthermore, the School District is not includable in any other reporting entityon the basis of such criteria.

Basis of Presentation

The basic financial statements of the School District have been prepared in conformity with accounting principles generallyaccepted in the United States of America (GAAP) as applied to governmental units. The Governmental AccountingStandards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financialreporting principles. The School District also applies Financial Accounting Standards Board (FASB) Statements andInterpretations issued on or before November 3D, 1989 to its governmental and business-type activities and to its proprietaryfunds, provided they do not conflict with or contradict GASB pronouncements. The more significant of the School District'saccounting policies are described below.

The School District's basic financial statements consists of govemment-wide statements, including a statement of net assetsand a statement of activities, and fund financial statements, which provide a rnore detailed level of financial information.

Government-wide Statements - The statement of net assets and the statement of activities display informationabout the School District as a whole. These statements include the financial activities of the primary government,except for fiduciary funds. The statements distinguish between those activities of the School District that aregovernmental and those that are considered business-type activities. The statement of net assets presents thefinancial condition of the governmental and business-type activities of the School District at fiscal year-end. Thestatement of activities presents a cornparison between direct expenses and program revenues for each program orfunction of the School Districfs governmental activities and for the business-type activities of the School District.Direct expenses are those that are specifically associated with a service, prograrn or department and, therefore,clearly identifiable to a particular function. The policy of the School District is to not allocate indirect expenses tofunctions in the statement of activities. Program revenues include charges paid by the recipient of the goods orservices offered by the program, grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular program and interest earned on grants that is required to be used to support a particularprogram. Revenues, which are not classified as program revenues, are presented as general revenues of the SchoolDistrict, with certain limited exceptions. The comparison of direct expenses with program revenues identifies theextent to which each business segment or governmental function is self-financing or draws from the general revenuesof the School District.

Fund Financial Statements - During the fiscal year, the School District segregates transactions related to certainSchool District functions or activities in separate funds in order to aid financial management and to demonstrate legalcompliance. Fund financial statements are designed to present financial information of the School District at thismore detailed level. The focus of governmental and enterprise fund financial statements is on major funds. Eachmajor fund is presented in a single column. The fiduciary fund is reported by type. The School District uses funds tomaintain its financial records during the fiscal year. A fund is defined as a fiscal and accounting entity with a self-balancing set of accounts. There are three categories of funds: governmental, proprietary, and fiduciary.

37

Audubon School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 3D, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Governmental Funds - Governmental funds are those through which most governmental functions typically are financed.Governmental fund reporting focuses on the sources. uses and balances of current financial resources. Expendable assetsare assigned to the various governmental funds according to the purposes for which they mayor must be used. Currentliabilities are assigned to the fund from which they will be paid. The difference between governmental fund assets andliabilities is reported as fund balance. The following are the School District's major governmental funds:

General Fund - The general fund is the general operating fund of the School District and is used to account for allfinancial resources except those required to be accounted for in another fund. Included are certain expenditures forvehicles and movable instructional or non-instructional equipment classified in the capital outlay sub-fund.

As required by the New Jersey State Department of Education. the School District includes budgeted capital outlay inthis fund. Accounting prinCiples generally accepted in the United States of America as they pertain to governmentalentities state that general fund resources may be used to directly finance capital outlays for long-lived improvementsas long as the resources in such cases are derived exclusively from unrestricted revenues.

Resources for budgeted capital outlay purposes are normally derived from State of New Jersey aid. district taxes andappropriated fund balance. Expenditures are those which result in the acquisition of or additions to capital assets forland. existing buildings. improvements of grounds. construction of buildings, additions to or remodeling of buildingsand the purchase of built-in equipment.

In addition to the capital outlay sub-fund. the School District is accountable for an additional sub-fund, the EducationJobs Fund ("Ed Jobs"). resulting from federal legislation signed into law on August 10,2010. The Ed Jobs programwas created to provide funding assistance to states in order to save or create education jobs for the period from theSeptember 30, 2010 through September 30, 2012. Jobs funded under this program include those that provideeducational and related services for early childhood, elementary, and secondary education. Ed Jobs revenues andexpenditures are recorded in the general fund (fund 18) on a reimbursement basis. As such, revenue is not includedin the fiscal year surplus, and no portion of general fund balance at June 30, 2012 is considered to be attributable toEd Jobs. Ed Jobs expenditures are included as a component of overall general fund expenditures, and are alsoincluded in general fund expenditures for purposes of the excess surplus calculation.

Special Revenue Fund - The special revenue fund is used to account for and report the proceeds of specificrevenues sources that are restricted or committed to expenditure for specified purposes other than debt service orcapital projects.

Capital Projects Fund - The capital projects fund is used to account and report financial resources that are restricted,committed, or assigned to expenditure for capital outlays, including the acquisition or construction of capital facilitiesand other capital assets. other than those financed by proprietary funds. The financial resources are derived fromNew Jersey Economic Development Authority grants, temporary notes or serial bonds which are speCificallyauthorized by the voters as a separate question on the ballot either during the annual election or at a special election.

Debt Service Fund - The debt service fund is used to account for and report financial resources that are restricted,committed, or assigned to expenditure for principal and interest.

Proprietary Funds - Proprietary funds are used to account for the School District's ongoing activities, which are similar tothose in the private sector.

Enterprise Funds - The enterprise funds are used to account for operations that are financed and operated in amanner similar to private business enterprises, where the intent of the School District is that all costs (expenses,including depreciation) of providing goods or services to the students on a continuing basis be financed or recoveredprimarily through user charges: or, where the School District has decided that periodic determination of revenuesearned, expenses incurred, and/or net income is appropriate for capital maintenance, public policy, managementcontrol, accountability, or other purposes.

38

Audubon School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Proprietary Funds (Continued) - The School District's enterprise funds are:

Food Service Fund - This fund accounts for the financial transactions related to the food service operations of theSchool District.

After School Program Fund - This fund accounts for the financial resources of the School District's extended dayprogram. This program provides before and after school care to students.

Community Education Fund - This fund accounts for the financial activity related to providing adult schoolactivities within the School District.

All proprietary funds are accounted for on a cost of services or "capital maintenance" measurement focus. This means thatall assets and all liabilities, whether current or noncurrent, associated with their activity are included on their balance sheets.Their reported fund equity (net assets) is segregated into investment in capital assets, net of related debt, and unrestrictednet assets, if applicable. Proprietary fund type operating statements present increases (revenues) and decreases(expenses) in net total assets.

Depreciation of all exhaustive fixed assets used by proprietary funds is charged as an expense against their operations.Accumulated depreciation is reported on proprietary fund balance sheets. Depreciation has been provided over theestimated useful lives using the straight-line method. The estimated useful lives are as follows:

EquipmentLight Trucks and VehiclesHeavy Trucks and Vehicles

12 Years4 Years6 Years

Fiduciary Funds - Fiduciary fund reporting focuses on net assets and changes in net assets. The fiduciary fund category issplit into two classifications: trust funds and agency funds. Agency funds are used to account for assets held by the SchoolDistrict in a trustee capacity or as an agent for individuals, private organizations, other governments, andlor other funds (i.e.payroll and student activities). They are custodial in nature (assets equal liabilities) and do not involve measurement ofresults of operations. The School District has five fiduciary funds; an unemployment compensation trust fund, a flexiblespending trust, a private purpose scholarship fund, a student activity fund, and a payroll fund.

Measurement Focus

Government-wide Financial Statements - The government-wide financial statements are prepared using the economicresources measurement focus. All assets and all liabilities associated with the operation of the School District are includedon the statement of net assets.