scaling complex rules…. - Pulp Fusionimages.pulpfusion.com/cpadallas/fcpemay2014/05... ·...

55

Accounting for Income Taxes: Recent Trends & Developments DALLAS CPA Society Katherine Morris, CPA May 8, 2014 scaling complex rules….

Transcript of scaling complex rules…. - Pulp Fusionimages.pulpfusion.com/cpadallas/fcpemay2014/05... ·...

Accounting for Income Taxes: Recent Trends & Developments

DALLAS CPA SocietyKatherine Morris, CPA

May 8, 2014

scaling complex rules….

a tangled web of complex matters…

Accounting for Income TaxesCourse Learning Objectives: This presentation will provide participants with one hour of A&A credit and the knowledge of recent trends & developments impacting the reporting of income taxes in the financial statements under ASC 740.

April 21, 2014

Agenda of Tax Provision Recent Trends

• Recent Trends• Focus on Issues

1. Valuation allowance (VA) considerations

2. Effective tax rate (ETR) reconciliation / Interim Reporting

3. Indefinite reinvestment of foreign earnings

4. Uncertain tax positions (UTP)

Best Practices will be shared during each topic discussion.

3 April 21, 2014

Recent Trends

April 21, 20144

Accounting for Income Taxes is most relevant to C-Corporations and has been one of the key areas of restatements, material weaknesses and significant deficiencies for public filers over the past 12 years. (Audit Analytics - Analysis of past 12 years, report released April 2013)

Observation: Similar to the impact of Sarbanes-Oxley on auditing, the SEC’s focus on income taxes has trickled down from the audit of public companies and are now addressed by both those performing audits and those conducting peer reviews of auditors of private companies.

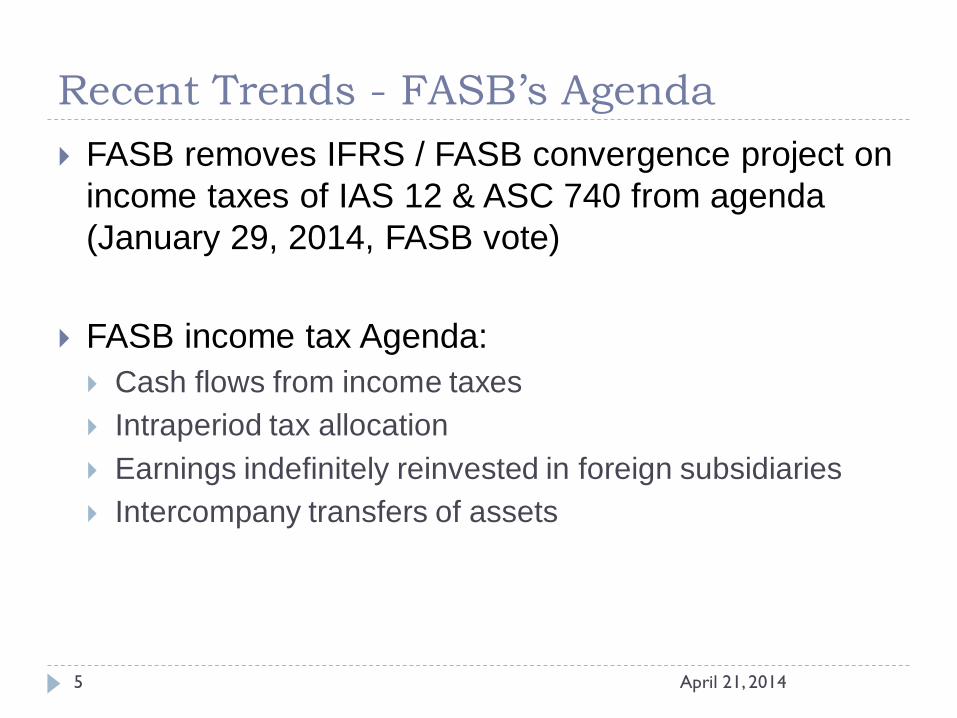

Recent Trends - FASB’s Agenda FASB removes IFRS / FASB convergence project on

income taxes of IAS 12 & ASC 740 from agenda (January 29, 2014, FASB vote)

FASB income tax Agenda: Cash flows from income taxes Intraperiod tax allocation Earnings indefinitely reinvested in foreign subsidiaries Intercompany transfers of assets

5 April 21, 2014

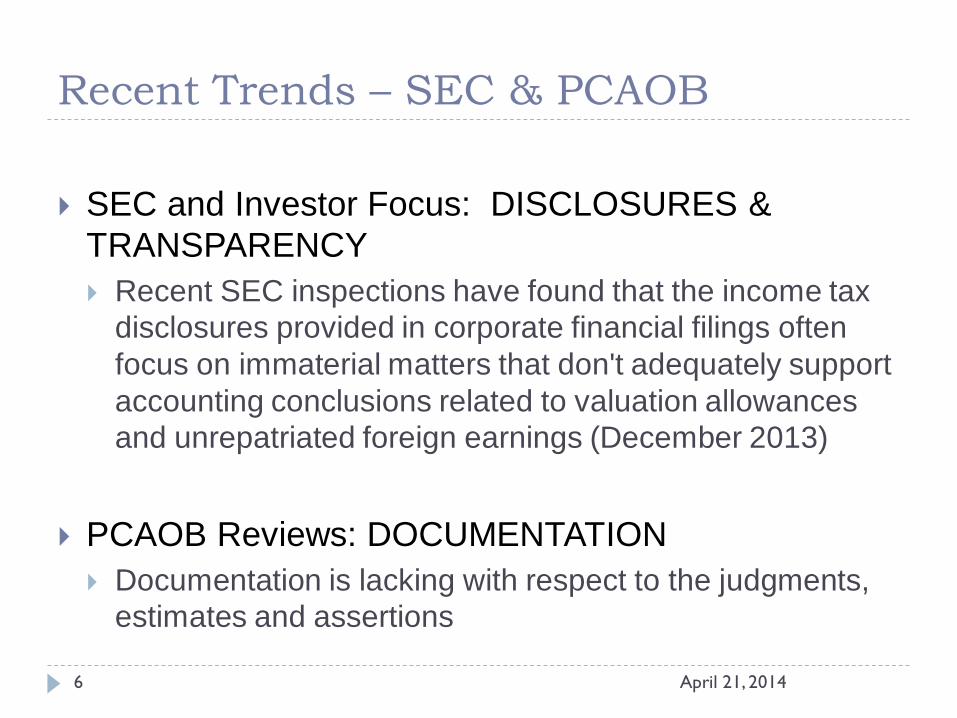

Recent Trends – SEC & PCAOB

April 21, 20146

SEC and Investor Focus: DISCLOSURES & TRANSPARENCY Recent SEC inspections have found that the income tax

disclosures provided in corporate financial filings often focus on immaterial matters that don't adequately support accounting conclusions related to valuation allowances and unrepatriated foreign earnings (December 2013)

PCAOB Reviews: DOCUMENTATION Documentation is lacking with respect to the judgments,

estimates and assertions

Recent Trends – SEC Technical Focus SEC Comments – current technical focus: Valuation allowances Rate reconciliation Repatriation of foreign earnings and liquidity ramifications Unrecognized tax benefits

Transparency: SEC continues to ask registrants to provide early-warning

disclosures about changes in the business, issues, and how they may potentially affect the financial statements.

7 April 21, 2014

value of DTAs are still an issue…

1. Valuation Allowances -Considerations

1. Valuation Allowances (VA) Considerations Overview General Rule:

Reduce a Deferred Tax Asset (DTA) by a Valuation Allowance (VA) if, based on the weight of all available evidence, it is more likely than not (i.e., >50%) that some portion or all of the DTA will not be realized (ASC 740-10-30-17)

Reduce the DTA to the amount that is more likely than not to be realized

9 April 21, 2014

Valuation Allowances – Documentation

Issues Lack of documentation and disclosure of positive and negative

evidence No contemporaneous support for need for / release of VA

Take Aways Contemporaneously Analyze & Document:

Management’s responsibility to contemporaneously examine, support and document rationale for the need for and for changes in valuation allowances

Disclose (i.e., be transparent in footnotes): Public filers - discuss in a transparent manner in the MD&A and the

footnote disclosure(s) the underlying business reasons why a valuation allowance is needed or not required

Auditors are required to retain and assess management’s support and documentation

10 April 21, 2014

Valuation Allowances –Analyze & Document the Evidence Best Practice

Qualitative & Quantitative analysis Document the need for and amount of the VA:

Negative Evidence Positive Evidence Conclusions Reached

Negative Evidence A history of operating losses or tax credit carryforwards expiring

unused (Some say a 2-year history of losses) Losses expected in early / start-up years Known circumstances that if unfavorably resolved would adversely

effect future operations and profit level

11 April 21, 2014

Valuation Allowances –Analyze & Document the Evidence

Positive Evidence: Sources of Income Future reversals of certain DTLs

Caution: consider the reversal criterion

Future taxable income exclusive of reversal of DTAs

Taxable income or credit carryback opportunities

Tax planning strategies creating income Must be considered

Must be prudent and feasible!

12 April 21, 2014

Valuation Allowances –Analyze & Document the Evidence

Other Examples of Positive Evidence Contracts or committed sales backlog that would produce more

than enough taxable income to realize all or part of the DTAs

An excess of appreciated asset value over the tax basis of the entity’s net assets in an amount sufficient to realize the deferred tax assets – if it would be feasible and prudent to sell…

Strong earnings history with evidence indicating the loss is an aberration rather than a continuing condition

Observation: Some say at least 3 years of earnings

REMINDERS:• Schedule out and quantify the impact. • Remember a valuation allowance is not an all or none amount.

13 April 21, 2014

Valuation Allowances –Analyze & Document the Evidence

Possible Sources of Income Outside Basis Differences in Foreign Sub

When expected to reverse in the foreseeable future When the foreign earnings have not been asserted as

indefinitely reinvested under APB Opinion 23 Caution: consider impact of cumulative translation adjustment

(CTA)

Equity Method Investments When there is an a expectation of reversal in the foreseeable

future

14 April 21, 2014

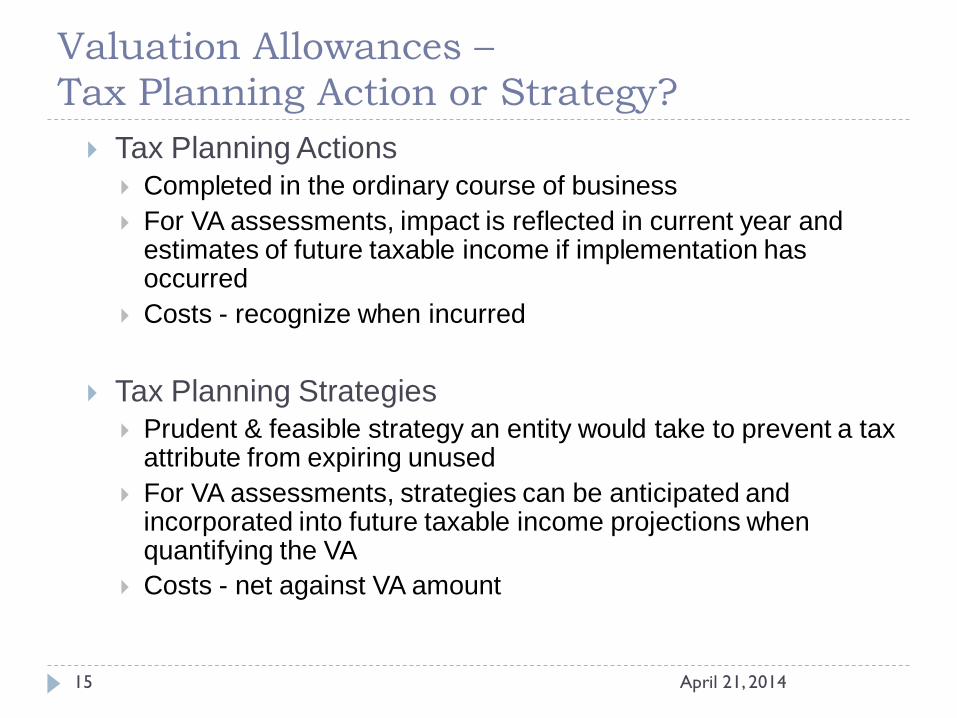

Valuation Allowances –Tax Planning Action or Strategy? Tax Planning Actions

Completed in the ordinary course of business For VA assessments, impact is reflected in current year and

estimates of future taxable income if implementation has occurred

Costs - recognize when incurred

Tax Planning Strategies Prudent & feasible strategy an entity would take to prevent a tax

attribute from expiring unused For VA assessments, strategies can be anticipated and

incorporated into future taxable income projections when quantifying the VA

Costs - net against VA amount

15 April 21, 2014

Valuation Allowances – IssuesDTL on Goodwill – Naked Credit

Guidance on sources of taxable income: Consider DTLs resulting from temporary differences that will

reverse in future periods Do not use DTLs created by the book/tax basis difference on

nonamortizable book goodwill

Common Error Companies often reduce the DTAs by all DTLs, including the

naked credit, to compute the amount of the VA

Issue By the very nature of goodwill, the DTL is not expected to reverse DTLs on indefinite lived intangibles, such as goodwill, create a

“Naked (DTL) Credit” that cannot be used as a source of income to reduce the DTA when computing the need for a VA

16 April 21, 2014

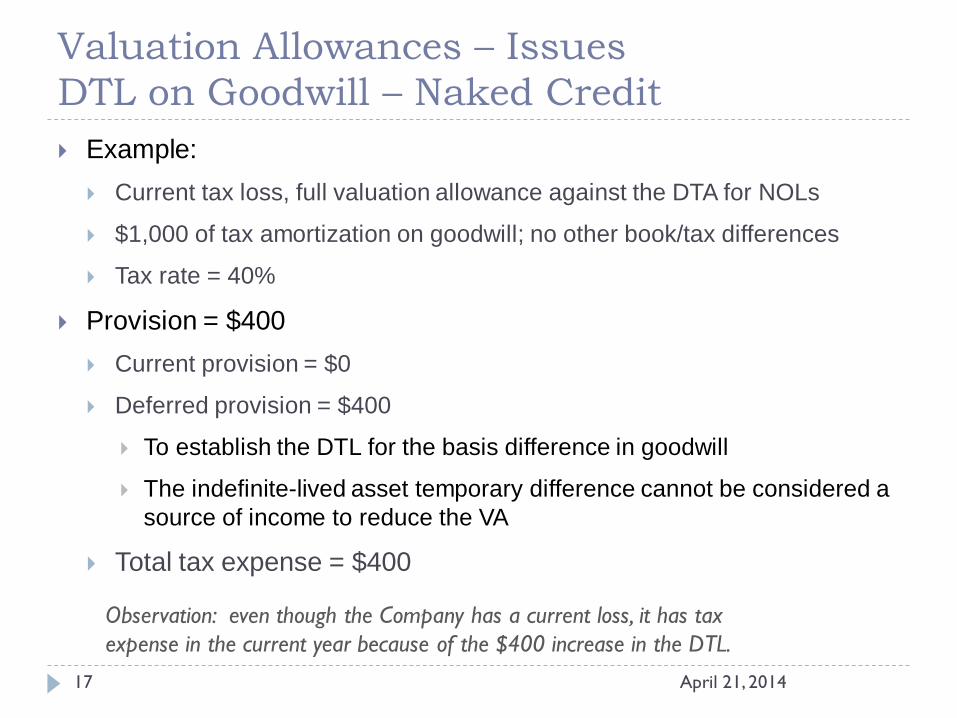

Valuation Allowances – IssuesDTL on Goodwill – Naked Credit Example:

Current tax loss, full valuation allowance against the DTA for NOLs

$1,000 of tax amortization on goodwill; no other book/tax differences

Tax rate = 40%

Provision = $400 Current provision = $0

Deferred provision = $400

To establish the DTL for the basis difference in goodwill

The indefinite-lived asset temporary difference cannot be considered a source of income to reduce the VA

Total tax expense = $400

Observation: even though the Company has a current loss, it has tax expense in the current year because of the $400 increase in the DTL.

17 April 21, 2014

Valuation Allowances –Recent Development on Goodwill

April 21, 201418

New Guidance (ASU 2014-02) Accounting Standard provides a simplified, elective approach to

accounting for book goodwill for PRIVATE companies Amortize goodwill over 10 years – or less if identifiable shorter life Test for impairment when a triggering event occurs, not annually

Effective: years beginning after 12/15/2014; early adoption permitted

Implication to VA In Review: Tax Amortization of book goodwill generally creates a (“naked

credit”) DTL on an indefinite lived asset that will not reverse in the future An election under ASC 2014-02 effectively re-characterizes goodwill as a

finite lived asset – i.e., amortizable for book The resulting reversal of the DTL could potentially support recoverability

of a DTA when looking at the need for a valuation allowance

Valuation Allowances – Issues: Analyze DTAs and DTLs for each Jurisdiction Issue

DTLs from different jurisdictions cannot be considered as a source of income to reduce the amount of VA on DTA

Example UK DTA = $100; related to UK NOLs with full VA US Parent DTL = $(100), relating to depreciation on US assets

UK DTA $100UK - Valuation Allowance (100)US DTL (100)Consolidated DTL $(100)

The US taxable temporary difference cannot be netted against UK DTA to reduce the UK valuation allowance

19 April 21, 2014

Valuation Allowances – IssueWhen Can VA Be Released? Guidance:

Report changes to the VA in the reporting period they occur Consider what triggering event(s) have occurred since the prior assessment and

whether a change in conclusion is warranted

Issue: Considerations of when the VA can be released:

When did income begin? Is it sustainable? When was a 3-year history of earnings established? Is there a carryback opportunity? Other…Has a non profitable business been disposed?

Take Aways: Document the analysis of evidence Support the triggering event(s) Judgment – i.e., quantify when and how much? Management should apply a consistent policy on what criteria should be used on

which to base VA reductions

20 April 21, 2014

Valuation Allowances – IssueWhen Can VA Be Released?

Public Filers The SEC staff has indicated registrants consider:

(1) the magnitude and duration of past losses,

(2) the magnitude and duration of current profitability, and

(3) changes in factors (1) and (2) that drove losses in the past and those currently driving profitability.

Disclosure: Include a discussion of the assessment of positive and negative factors or reasons that led to a reversal of a valuation allowance, and effectively answer the question “Why now?”

21 April 21, 2014

Valuation Allowances – IssueDTAs Not a Substitute for Analyzing UTP

Guidance DTAs should be established for all deductible temporary

differences, NOLs and Credits Record DTAs gross; then consider need for VA VA may be required if future realization is in doubt due to

insufficient future taxable income

Take Aways A VA is not an appropriate way to handle liabilities on uncertain

tax positions (UTPs) that do not meet the recognition or measurement thresholds

Companies are required to examine UTPs even when there is a “full” VA on DTAs

22 April 21, 2014

Valuation Allowances – Recent Development on Uncertain Tax Positions New Guidance (ASU 2013-11) - Presentation of an Unrecognized Tax

Benefit: When a NOL Tax Credit Carryforward Exists — reduce the DTA for an NOL

carryforward or a tax credit carryforward by the liability for the tax benefit resulting from an uncertain tax position

Exceptions: 1) When the NOL or tax credit carryforward cannot be used to settle taxes resulting

from the disallowance of the tax position, or 2) When the entity does not intend to use the NOL or tax credit carryforward DTA

for settlement If conditions 1) or 2) exist, present the liability for the uncertain tax position and do

not net the amount with a DTA.

Effective Date: Public entities: fiscal years beginning after December 15, 2013 Nonpublic entities may wait until fiscal years, and interim periods beginning after

December 15, 2014, to adopt the amendments Early adoption is permitted

23 April 21, 2014

Valuation Allowances – IssueImpact of Tax Law Changes General Rule (ASC 740-10-30-17): Consider all currently available information about future

events when determining whether a valuation allowance is needed for a DTA.

Reminder An entity should not consider changes in tax laws or rates

when assessing the realizability of a DTA before the period in which the change is enacted.

24 April 21, 2014

Valuation Allowances –SEC Comments on Disclosures BOILERPLATE DISCLOSURES:

Cicely LaMothe, senior assistant chief accountant in the division's Office of Real Estate and Commodities, said the SEC continues to find boilerplate disclosures on deferred tax valuation allowances(Dec. 2013)

ISSUE Some registrants simply state that they considered the four sources of

taxable income required when determining the ability to realize their deferred tax assets.

SUGGESTED REMEDIES – to increase transparency Address the limitations on the entity's use of net operating losses and

foreign tax credits. Reference expiration dates. Provide a disclosure indicating the relative magnitude of each source of

taxable income that supports the realization of deferred tax assets. Disclose whether material positive or negative evidence was considered.

25 April 21, 2014

timing is everything…

2. Effective Tax Rate / Interim Reporting

2. Effective Tax Rate (ETR) Reconciliation “Effective Tax Rate” =

Income Tax Expense / Pretax Income = ETR%

Purpose of ETR Reconciliation Quantifies and explains the material differences of the

“expected” US federal statutory income tax rate of 34% or 35% to the company’s “actual” or “effective” tax rate.

27 April 21, 2014

Effective Tax Rate Reconciliation -Disclosures Reconciling Items: (shown in footnote disclosure)

Examples of Material Rate Reconciliation Items: Pretax Income * 34 or 35% State and foreign taxes (net of federal benefit) Permanent Differences Changes in the Valuation Allowance Income Tax Credits True Ups and changes in reserves or change in prior year tax Changes in Tax Rates

Show dollars ($s) or percentages (%s)

Separate-line-item disclosure is required for items when meets materiality threshold of >5%: i.e., Pretax Income on reconciling item * Statutory Tax Rate = > 5% of total Tax

Expense

Extraordinary items and Discontinued Operations are disclosed net of tax

28 April 21, 2014

Effective Tax Rate Reconciliation -SEC Staff Comments on Rate Recs Reconciling items:

Not labeled correctly / did not adequately describe the underlying nature of the amount

Inappropriately aggregated material reconciling items Inconsistent with related amounts disclosed elsewhere in a

registrant’s filing Foreign tax info not disclosed in MD&A consistent with

footnote: Each material foreign jurisdiction; each tax rate Impact of each jurisdiction on the amount in the rate rec

Corrections of errors inappropriately reflected as changes in estimates

29 April 21, 2014

Effective Tax Rate Reconciliation –Blended Rate Versus Actual Rate?

Preferred Practice:

Use actual tax rates currently in effect by jurisdiction, weighted appropriately, versus a blended rate computation

30 April 21, 2014

Effective Tax Rate Reconciliation: Changes in Tax Law Impact of new tax legislation or change in rates are

recognized in the period that includes the enactment date (ASC 740-10-25-47), regardless of the effective date

Continuing Operations: Include the impact in income from continuing operations for the

period that includes the enactment date. (ASC 740-10-45-15)

Discrete Items: Impact on DTL or DTA (ASC 740-10-35-4) Effects on taxes payable or refundable for a prior year when the

change has retroactive effects

31 April 21, 2014

Effective Tax Rate Reconciliation: Changes in Tax Law Example: Major business tax provisions “extenders” expired at the end of

2013: R&D credit Subpart F exemption for active financing income and look-through

treatment for payments between related CFCs 15-year straight-line cost recovery for qualified leasehold

improvements, qualified restaurant buildings and improvements, and qualified retail improvements

New markets tax credit Work opportunity tax credit

Action Item: The tax impact of these items cannot be considered in the 2013

financials but in the period if & when a tax law enactment occurs.

32 April 21, 2014

Effective Tax Rate Reconciliation: Changes in Tax Law New Legislation:

Fixed Assets: Capitalize vs Expense Final regulations released September 13, 2013 on applying IRC Section

263(a) of the to amounts paid to acquire, produce, or improve tangible property, as well as rules for materials and supplies (IRC Section 162)

Tangible Property Accounting Method Change

Results: Change tax accounting methods / apply rules retrospectively with

a 481(a) adjustment Changes deferred taxes / book vs tax basis on Fixed Assets

Positive 481(a) adjustment creates DTL Negative 481(a) adjustment creates DTA

Impact of timing of future reversals considered in VA on DTAs analysis

Reclasses in classified balance sheet: base on the expected reversal date of that temporary difference

33 April 21, 2014

Effective Tax RateInterim Reporting General Rule Apply estimated annual ETR to the year-to-date ordinary

income (or loss) from continuing operations

Revise estimated annual ETR at the end of each interim period based upon the best current estimate of the annual ETR

34 April 21, 2014

Interim Reporting Discrete Events

Issue Does the event impact the estimated annual effective tax

rate for the quarter/interim period computation?

Discrete Events Exclude events during the quarter that do not relate to

continuing operations or are unusual or infrequent Recognize in the period in which they occur Examples:

Settlement of a tax audit related to prior years Change in tax law which requires retroactive adjustments that

fall out of the current year (i.e., Re-enactment of R&D credit).

35 April 21, 2014

Interim Reporting Income from Continuing Operations

NOT discrete events: Company hires additional employees in Q3 and grants ISO’s

forcing an expense for the year Company releases all of its valuation allowance in the current

quarter based on current years’ earnings

36 April 21, 2014

Interim ReportingLoss YTD / Forecasts Income

Issue: The Company has a loss year-to-date but forecasts

income; no valuation allowance

Results: Show tax benefit YTD; will offset future income Show tax expense in future periods that reflect

income

37 April 21, 2014

global operations…

3. Indefinite Reinvestment of Foreign Earnings

3. Indefinite Reinvestment of Foreign Earnings General Rule Compute deferred taxes for all differences in book versus

tax basis

Exception to the General Rule for CFCs: A DTL is not recognized for differences in the amount of

the investment in the shares of the CFC subsidiary owned by the parent unless it becomes apparent that temporary differences will reverse in the foreseeable future (e.g., when foreign earnings are repatriated to the U.S.)

39 April 21, 2014

Indefinite Reinvestment of Foreign Earnings Exception – NOT an election Exception applies if the specific facts and circumstances

warrant Based on a company’s ability and intent to control the reversal

of a taxable temporary differences (i.e., the outside basis difference in the stock of CFC due to unrepatriated earnings)

Management’s Position Does Management intend to permanently reinvest the foreign

earnings overseas? Caution: review the underlying facts – do they support

Management’s Representation? Document the facts supporting management’s positions

40 April 21, 2014

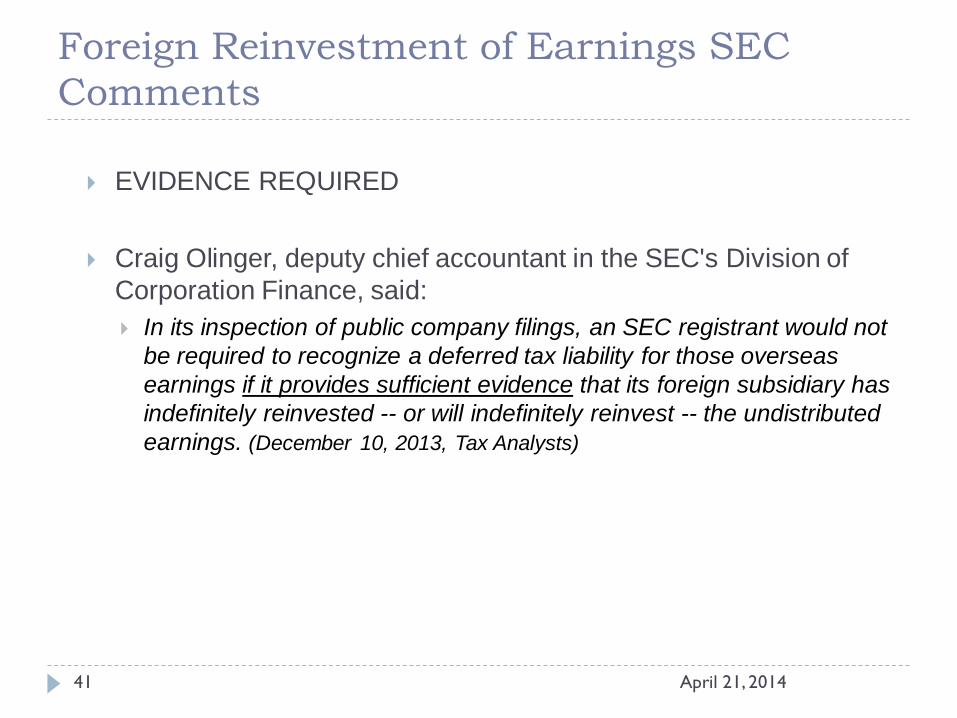

Foreign Reinvestment of Earnings SEC Comments

EVIDENCE REQUIRED

Craig Olinger, deputy chief accountant in the SEC's Division of Corporation Finance, said: In its inspection of public company filings, an SEC registrant would not

be required to recognize a deferred tax liability for those overseas earnings if it provides sufficient evidence that its foreign subsidiary has indefinitely reinvested -- or will indefinitely reinvest -- the undistributed earnings. (December 10, 2013, Tax Analysts)

41 April 21, 2014

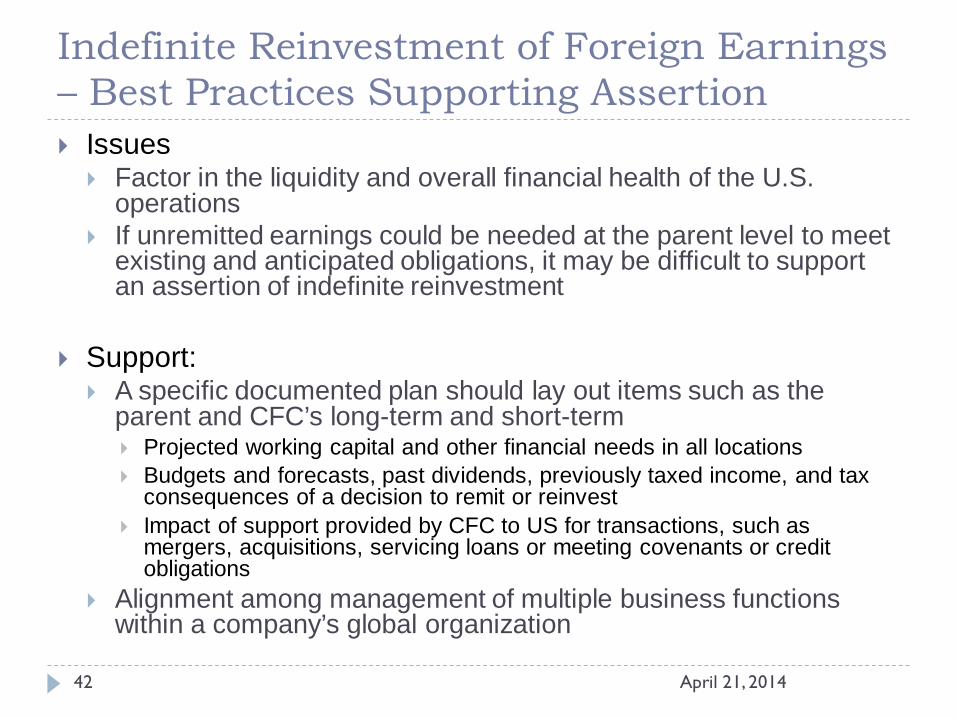

Indefinite Reinvestment of Foreign Earnings – Best Practices Supporting Assertion Issues

Factor in the liquidity and overall financial health of the U.S. operations

If unremitted earnings could be needed at the parent level to meet existing and anticipated obligations, it may be difficult to support an assertion of indefinite reinvestment

Support: A specific documented plan should lay out items such as the

parent and CFC’s long-term and short-term Projected working capital and other financial needs in all locations Budgets and forecasts, past dividends, previously taxed income, and tax

consequences of a decision to remit or reinvest Impact of support provided by CFC to US for transactions, such as

mergers, acquisitions, servicing loans or meeting covenants or credit obligations

Alignment among management of multiple business functions within a company’s global organization

42 April 21, 2014

solitary facts…

4. Uncertain Tax Positions

4. Uncertain Tax Positions General Rule: ASC 740-10, fka FIN 48, requires

all material income tax positions for all open tax years to be reviewed.

If the position is more likely than not to be sustained upon audit, an amount must be accrued.

44 April 21, 2014

Uncertain Tax Positions – IssuePosition Taken When is a tax position considered “taken”?

1. A position taken in a previously filed return or expected to be taken in a future tax return (original or amended)

2. When the taxpayer fails to file a required return

45 April 21, 2014

Uncertain Tax Positions – IssueEffectively Settled A tax position is considered to be “effectively settled”

when:

1. Exam is complete (ASC 740-10-25-10a)

2. The taxpayer does not intend to appeal or litigate any aspect of the exam’s conclusions (ASC 740-10-25-10b)

3. When it is remote that the taxing authority would examine/reexamine any aspect of a tax position (ASC 740-10-25-10c)

46 April 21, 2014

Uncertain Tax Positions – Issue Changes in Judgment Issue:

Company changes the liability for uncertain tax positions.

Guidance: Measurement of a tax position should "be based on management's best

judgment given the facts, circumstances, and information available at the reporting date"

Subsequent changes in judgment must be based on the evaluation of new information

Additional analysis of existing information would not typically constitute new information for purposes of adjusting prior estimates

Presentation: A change in judgment that results in subsequent recognition,

derecognition or a change in measurement of a position taken in a prior annual period must be recognized as a discrete item in the period in which the new information becomes available. (ASC 740-10-25-15)

Disclose change

47 April 21, 2014

Uncertain Tax Positions –SEC Comments/Expectations Observations Failure to provide required disclosures about

unrecognized tax benefits, which include a tabular reconciliation of such benefits (under ASC 740-10-50-15 and 50-15A).

Where no liability or benefit for unrecognized tax benefits exists (or for which such benefits are immaterial), consider disclosing those facts.

Lack of transparent disclosures about possible future changes in unrecognized tax benefits about

(1) The tax rate reconciliation impact,(2) The impact on valuation allowances, and (3) Registrants’ assertions that foreign earnings are

indefinitely reinvested.

48 April 21, 2014

Appendix…

Documentation of UTPs – Best Practices

Uncertain Tax Positions –Documentation Procedures Technical merit of tax

positions Measurement By jurisdiction Federal State International Interest & penalties

Material items Current period activity Changes in judgment Assumptions

April 21, 2014

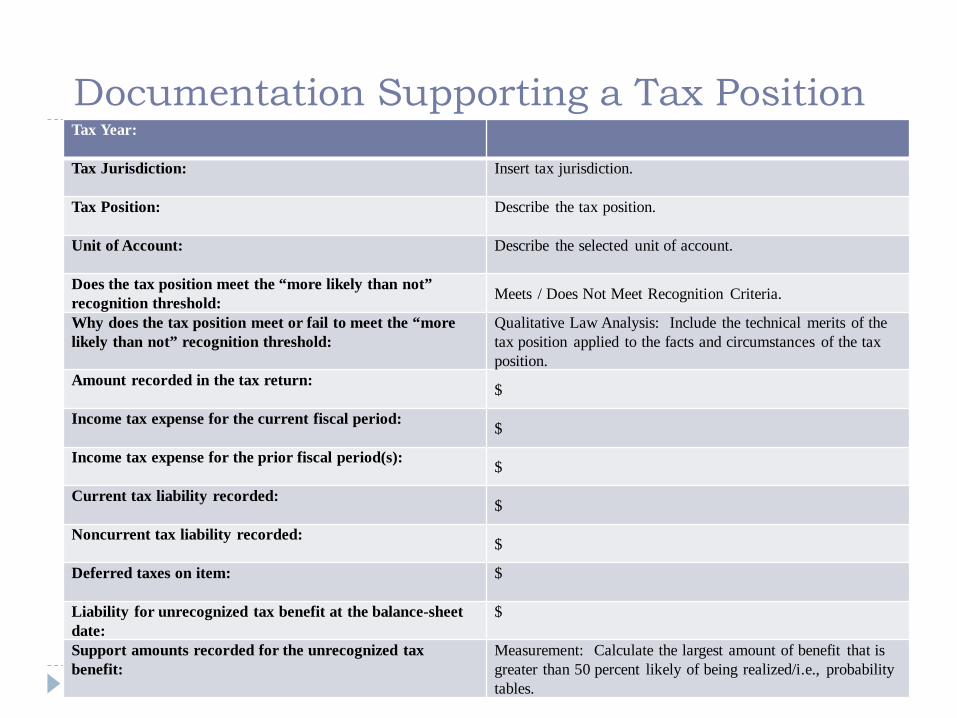

Documentation Supporting a Tax PositionTax Year:

Tax Jurisdiction: Insert tax jurisdiction.

Tax Position: Describe the tax position.

Unit of Account: Describe the selected unit of account.

Does the tax position meet the “more likely than not” recognition threshold: Meets / Does Not Meet Recognition Criteria.

Why does the tax position meet or fail to meet the “more likely than not” recognition threshold:

Qualitative Law Analysis: Include the technical merits of the tax position applied to the facts and circumstances of the tax position.

Amount recorded in the tax return: $

Income tax expense for the current fiscal period: $

Income tax expense for the prior fiscal period(s): $

Current tax liability recorded: $

Noncurrent tax liability recorded: $

Deferred taxes on item: $

Liability for unrecognized tax benefit at the balance-sheet date:

$

Support amounts recorded for the unrecognized tax benefit:

Measurement: Calculate the largest amount of benefit that is greater than 50 percent likely of being realized/i.e., probability tables.

Measurement – Assess the Probability of Outcomes

Possible Estimated Outcome

Individual Probability of Occurring

Cumulative Probability

of Occurring

$ 100 10% 10%

$ 80 20% 30%

$ 60 25% 55%

$ 50 20% 75%

$ 40 10% 85%

$ 20 10% 95%

$ 0 5% 100%

•NOTES: •$60 is the largest amount of benefit > than 50% likely of being realized upon settlement•$40 would be recorded on the balance sheet as an “unrecognized tax benefit” ($100 - $60)

Process: Document measurement process using a probability table or some other source of measurement.

April 21, 2014

Recognition & Measurement

JURISDICTION: Federal

Description of Identified Uncertain Tax Positions in Current Period

Tax (Benefit) or Accrual –

Recognition Criteria Met?

Amount to be Reported

“Measurement”

1

2

Total

Process: Document decision process on recognition criteria – MLTN or not? –and document results from the measurement step – i.e., the amount to be reported.

April 21, 2014

Thank you

Material discussed in this presentation is meant to provide general information and should not be acted on without professional advice tailored to your firm’s or company’s individual needs.

To ensure compliance with Treasury Department regulations, any tax advice that may be contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Service Code or applicable state or local tax law provisions or (ii) promoting, marketing, or recommending to another party any tax-related matters addressed herein.

April 21, 2014