scai Dox: : D golu kumar

47

A PROJECT REPORT ON KASHI GOMTI SAMYUT GRAMIN SUBMITTED BY: Dinesh Singh Ghinga Roll no. 581113515 1

-

Upload

kabir-soni -

Category

Documents

-

view

228 -

download

0

Transcript of scai Dox: : D golu kumar

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 1/47

A

PROJECT REPORT

ONKASHI GOMTI SAMYUT GRAMIN

SUBMITTED BY:

Dinesh Singh Ghinga

Roll no. 581113515

1

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 2/47

ACKNOWLEGMENT

“Chain of mistakes leads towards failures, chain of failures leads to experience

and chain of experience leads to success.” That’s what a life’s path is.

Same is applicable to my project work. I do not claim that I have a complete

knowledge of the subject. I would like to thanks my friends and many persons

who directly or indirectly helped me during my project.

Dinesh Singh Ghinga

5811113515 (M.B.A. 4th sem)

2

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 3/47

PREFACE

This project report is submitted for the partial fulfillment of

Master of Business Administration degree from Sikkim

Manipal University

While developing this project, I was involved with system

analysis, design and implementation process. This is a

sample report describing in detail various aspects of the

system. I have used prototyping model for designing

3

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 4/47

STUDENT DECLARARTION

I hereby declare that the project report entitled

“ KASHI GOMTI SAMYUT GRAMIN”

Submitted in partial fulfillment of the requirement

for the degree of Master of Business Administration

to Sikkim Manipal University, India is my

original work and not submitted for the award of any

other degree, diploma, fellowship, or any other

similar title or prizes.

Place: Haldwani DineshSingh Ghinga

Roll No.581113515

4

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 5/47

CONTENT

No. Particulars

1. Current State of KASHI GOMTI SAMYUT

GRAMIN

2. Key Drivers of Financial Exclusion of

KASHI GOMTI SAMYUT GRAMIN

3. Reasons for Unprofitable KASHI GOMTI

SAMYUT GRAMIN

4. Usage Issues for Rural Customers

5. Market Opportunity of KASHI GOMTI

SAMYUT GRAMIN

6. Improving Access of KASHI GOMTI

SAMYUT GRAMIN

7. Conclusion

8. Bibliography

9. Annexure

5

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 6/47

CURRENT STATE OF KASHI GOMTI

SAMYUT GRAMIN

The Indian Economy

India is the 12th largest economy in the world in terms of

gross domestic product (GDP), and fourth in terms of

purchasing power parity (PPP)1. The growth of the economy

is equally impressive with an average of over 8.0% during

the last three years2. However, in terms of GDP per capita,

India ranks a lowly 160th among other nations. Within the

country, there is a stark divide in the incomes of urban and

rural areas with the average monthly per capita

consumption expenditure (MPCE) in urban India being

almost double that of rural India.

In addition, there are significant disparities in urban and

rural consumption expenditure between different states.

Jharkhand and Orissa, for example, have an MPCE of

6

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 7/47

approximately Rs. 900 in urban areas and Rs. 410 in rural

areas4. In other states like Punjab and Haryana, the urban

rural disparity is significantly lower. A fifth of the Indian

population is below the poverty line (BPL) today with a

MPCE below Rs 340. In some states like Jharkhand and

Orissa, the proportion of BPL is greater than 40%. Diamond

believes that the segments that are not considered BPL

should all be considered as “potentially bankable” with

genuine financial needs that could be met by formal

financial and banking systems.

Current State of Indian Banking

An important metric to determine the level of financial

outreach/inclusion is the ratio of the number of deposit

accounts to population. It gives a snapshot of thepenetration of deposit accounts and credit accounts in India

in comparison with a few select countries with similar socio-

cultural and economic conditions. Even in comparison with

other developing economies, India has a significant

opportunity for increasing penetration of both deposit and

credit accounts.

Not only is there a large disparity between India and other

countries in banking penetration but there is also a large

variation in banking penetration within urban and rural

7

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 8/47

India. While urban India seems to be over-banked with more

than 100% penetration (many urban Indians have more

than one bank account), rural India lags far behind with a

19% penetration. The variance in rural and urban deposit

and credit account penetration is not restricted only to few

states but is common across all states.

In addition, the average value of a deposit account and a

credit account is also quite low in rural areas as compared

to urban areas. Diamond believes that the reasons for lowerpenetration levels are partly economic, as explained by the

low GDP per capita in the rural areas of the country, and

partly a result of “controllable” factors that are inherent in

formal banking systems in India today. The low deposit and

credit account penetration and low average values in

deposit and credit accounts demonstrate that banking

outreach in rural India is sub-optimal. This low outreach can

be explained by two key parameters: access and usage.

Simply defined, access is the availability of financial

services, and usage is the actual use of those services.

Access is influenced by issues such as the basic economic

state of rural India, lack of physical infrastructure facilities,

regulatory constraints, and the economics of rural banking.

Usage is constrained by social issues such as illiteracy,

incomplete service offerings by banks, and high transaction

8

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 9/47

costs in the formal banking system. Access and usage are

not synonymous, as people may have access to financial

services, but decide not to use them, either for socio-

cultural reasons or because opportunity costs are too high.

List of Rural Banks in India

KASHI GOMTI SAMYUT GRAMIN started since the

establishment of banking sector in India. Rural Banks in

those days mainly focused upon the agro sector. Regional

rural banks in India penetrated every corner of the country

and extended a helping hand in the growth process of the

country.

SBI has 30 Regional Rural Banks in India known as RRBs.

The rural banks of SBI are spread in 13 states extendingfrom Kashmir to Karnataka and Himachal Pradesh to North

East. The total number of SBIs Regional Rural Banks in India

branches is 2349 (16%). Till date in KASHI GOMTI SAMYUT

GRAMIN, there are 14,475 rural banks in the country of

which 2126 (91%) are located in remote rural areas.

Apart from SBI, there are many other banks which function

for the development of the rural areas in India. These banks

are listed below:

9

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 10/47

Andhra Pradesh Bihar

•

Andhra PradeshGrameena Vikas

Bank

• Andhra Pragathi

Grameena Bank

• Deccan Grameena

Bank

• Chaitanya Godavari

Grameena Bank

• Saptagiri Grameena

Bank

Chhattisgarh

•

Chhattisgarh GraminBank

• Surguja Kshetriya

Gramin Bank

• Durg-Rajnandgaon

Gramin Bank

Haryana

• Harayana Gramin

Bank

•

Madhya Bihar Gramin Bank• Bihar Kshetriya Gramin

Bank

• Uttar Bihar Kshetriya

Gramin Bank

• Kosi Kshetriya Gramin

Bank

• Samastipur Kshetriya

Gramin Bank

Gujarat

• Dena Gujarat Gramin Bank

• Baroda Gujarat Gramin

Bank

• Saurashtra Gramin Bank

Himachal Pradesh

• Himachal Gramin Bank

• Parvatiya Gramin Bank

10

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 11/47

• Gurgaon Gramin

Bank

Jammu & Kashmir

• Jammu Rural Bank

• Ellaquai Dehati Bank

• Kamraz Rural Bank

Assam

• Assam Gramin

Vikash Bank

• Langpi Dehangi

Rural Bank

Jharkhand

• Jharkhand Gramin

Bank

• Vananchal Gramin

Bank

Madhya Pradesh

• Narmada Malwa

Gramin Bank

Punjab

• Punjab Gramin Bank

• Faridkot-Bhatinda

Kshetriya Gramin Bank

• Malwa Gramin Bank

Kerala

• Narmada Malwa Gramin

Bank

• North Malabar Gramin

Bank

Tamil Nadu

• Pandyan Grama Bank

• Pallavan Grama Bank

Maharashtra• Marathwada Gramin Bank

• Aurangabad -Jalna Gramin

Bank

• Wainganga Kshetriya

Gramin Bank

• Vidharbha Kshetriya

Gramin Bank

• Solapur Gramin Bank

• Thane Gramin Bank

• Ratnagiri-Sindhudurg Gramin Bank

11

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 12/47

• Satpura Kshetriya

Gramin Bank

• Madhya Bharath

Gramin Bank

• Chambal-Gwalior

Kshetriya Gramin

Bank

• Rewa-Sidhi Gramin

Bank

• Sharda Gramin Bank• Ratlam- Mandsaur

Kshetriya Gramin

Bank

• Vidisha Bhopal

Kshetriya Gramin

Bank

• Mahakaushal

Kshetriya Gramin

Bank

• Jhabua Dhar

Kshetriya Gramin

BankKarnataka

• Karnataka Vikas

Grameena Bank

• Pragathi Gramin

Rajasthan

• Baroda Rajasthan Gramin

Bank

• Marwar Ganganagar

12

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 13/47

Bank

• Cauvery Kalpatharu

Grameena Bank

• Krishna Grameena

Bank

• Chikmagalur-Kodagu

Grameena Bank

• Visveshvaraya

Gramin Bank

Bikaner Gramin Bank

• Rajasthan Gramin Bank

• Jaipur Thar Gramin Bank

• Hodoti Kshetriya Gramin

Bank

• Mewar Anchalik Gramin Bank

Orissa

• Kalinga Gramya

Bank

• Utkal Gramya Bank

• Baitarani Gramya

Bank

• Neelachal Gramya

Bank

• Rushikulya Gramya

Bank

West Bengal

• Bangiya Gramin Vikash

Bank

• Paschim Banga Gramin

Bank

• Uttar Banga Kshetriya Gramin Bank

Meghalaya

• Ka Bank Nogkyndong

Ri Khasi- Jaintia

Arunachal Pradesh

• Arunachal Pradesh Rural

Bank

Manipur

• Manipur Rural Bank

Nagaland

• Nagaland Rural Bank

Tripura

13

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 14/47

• Tripura Gramin Bank

Mizoram

Uttar Pradesh

•

Purvanchal GraminBank

• Kashi Gomti Samyut

Gramin Bank

• Uttar Pradesh

Gramin Bank

• Shreyas Gramin

Bank

• Lucknow Kshetriya

Gramin Bank

• Ballia Kshetriya

Gramin Bank

• Triveni KshetriyaGramin Bank

Uttaranchal

•

Uttaranchal Gramin Bank

• Nainital Almora Kshetriya

Gramin Bank

KEY DRIVERS OF FINANCIAL EXCLUSION

OF RURAL BANKING

According to Diamond estimates, approximately 245 million

adults in rural India do not have a bank account today. As

depicted in Following Table, this reflects 24% of the total

population. While 60 million out of 245 million may not need

14

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 15/47

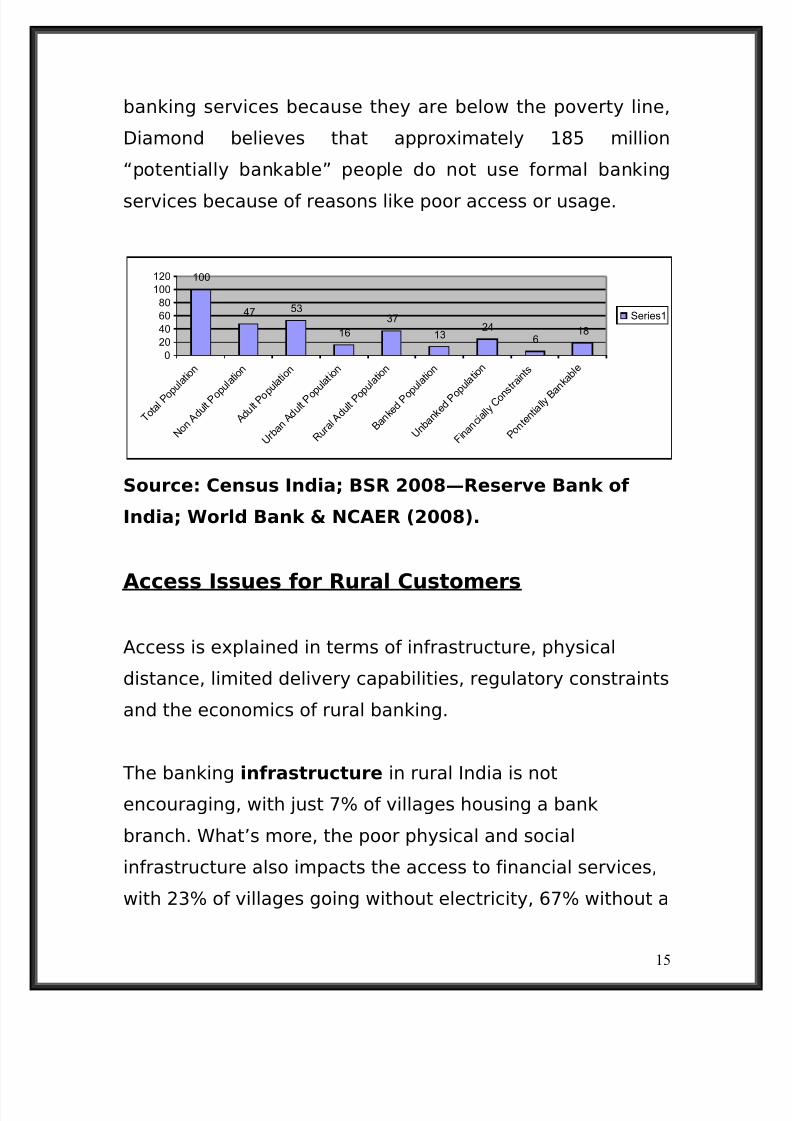

banking services because they are below the poverty line,

Diamond believes that approximately 185 million

“potentially bankable” people do not use formal banking

services because of reasons like poor access or usage.

100

47 53

16

37

1324

618

0

20

40

60

80

100

120

T o t a l P o p

u l a t i o n

N o n A d

u l t P o p

u l a t i o n

A d u l t P

o p u l a t i o

n

U r b a

n A d

u l t P o p

u l a t i o n

R u r a l A

d u l t P o p

u l a t i o n

B a n k

e d P o p

u l a t i o n

U n b a

n k e d

P o p u l a t i o

n

F i n a

n c i a l l y

C o n s

t r a i n t

s

P o n t e n t i a

l l y B a n k

a b l e

Series1

Source: Census India; BSR 2008—Reserve Bank of

India; World Bank & NCAER (2008).

Access Issues for Rural Customers

Access is explained in terms of infrastructure, physical

distance, limited delivery capabilities, regulatory constraints

and the economics of rural banking.

The banking infrastructure in rural India is not

encouraging, with just 7% of villages housing a bank

branch. What’s more, the poor physical and social

infrastructure also impacts the access to financial services,

with 23% of villages going without electricity, 67% without a

15

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 16/47

Post Office, and an average rural literacy rate of 59% and

secondary school penetration of 12%. This lack of physical

and social infrastructure in rural India is a key issue

impacting access to formal financial services.

The average distance to a branch in India is approximately

3.8 Kms. While this compares favorably to the average

distance to a branch in a developed market like the U.S.

(which is 6 Kms6), there are significant additional

challenges in India in the form of unpaved roads and limitedaccess to modern transportation. Most rural customers are

likely to sacrifice an entire day’s wage to travel to a bank

branch which is open between 10:00am and 5:00pm. While

some banking transactions could be done over phone, this

is rarely an option in a country with such low rural tele-

density.

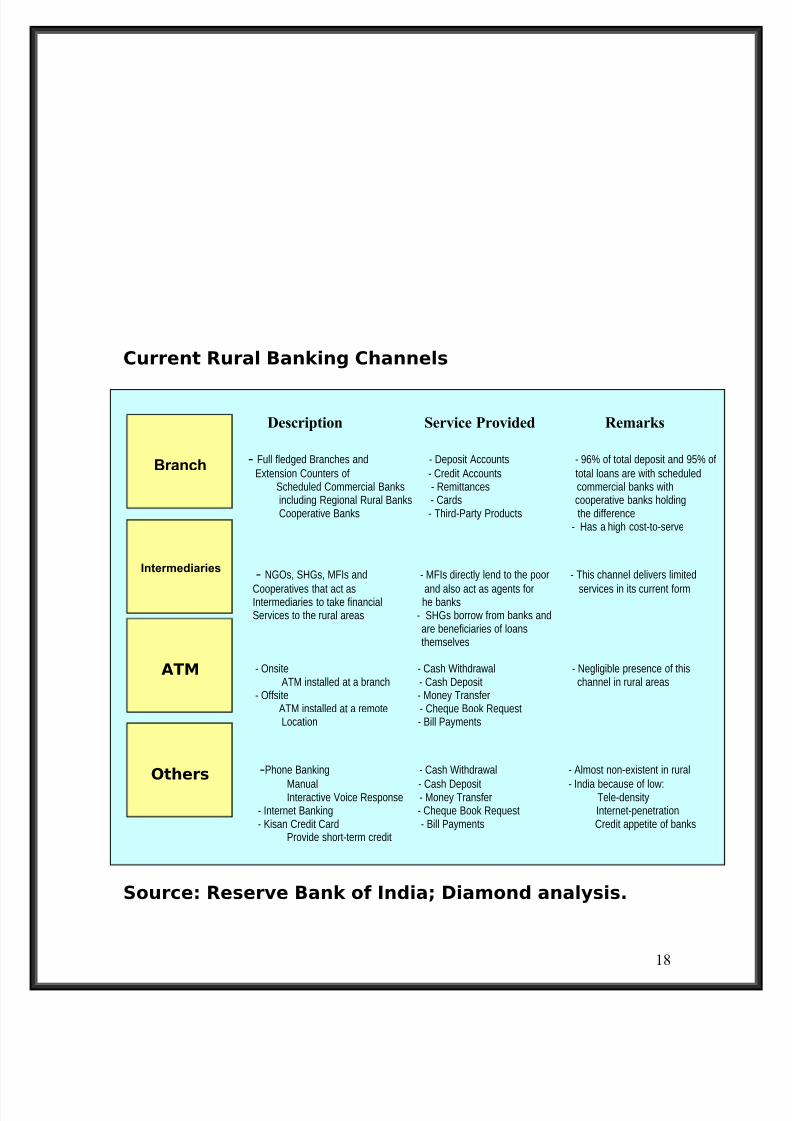

Limited delivery capability is a significant challenge.

Much of rural India is serviced through branches because

ATM penetration is low and other channels such as Phone

and Internet Banking are non-existent. Intermediaries like

Non-Governmental Organizations (NGOs), Self-Help Groups,

and Micro Finance Institutions (MFIs) are being used by

banks to improve access to credit and savings. However,

these channels, in their current form, offer limited services.

16

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 17/47

There are some regulatory constraints imposed by the

Reserve Bank of India (RBI) which may inadvertently

contribute further to the lack of formal banking services in

rural areas. For example, the RBI does not allow banks to

post any person other than a security guard at ATMs.

Hence, banks cannot deploy many ATMs in rural areas as

many rural customers require in-person support. A second

regulatory inhibitor is that new banks planning to establish

a branch in a rural area have to receive approval from the

Lead Bank and District Collector of that district. Hence,banks choose not to open new branches in certain areas

even when it is profitable to do so because there is no

certainty of getting approvals.

Many banks view the rural market as a regulatory

requirement rather than an economic opportunity. Banks

have from time to time borne the social cost of lending to

the rural economy at rates below their costs. They have

also faced capital erosion because of the write-off of loans,

particularly agriculture loans. Banks are required via

regulatory requirements to open branches in rural areas to

provide loans to agriculture and other priority sectors.

17

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 18/47

Current Rural Banking Channels

Source: Reserve Bank of India; Diamond analysis.

18

Description Service Provided Remarks

- Full fledged Branches and - Deposit Accounts - 96% of total deposit and 95% of

Extension Counters of - Credit Accounts total loans are with scheduledScheduled Commercial Banks - Remittances commercial banks withincluding Regional Rural Banks - Cards cooperative banks holdingCooperative Banks - Third-Party Products the difference

- Has a high cost-to-serve

- NGOs, SHGs, MFIs and - MFIs directly lend to the poor - This channel delivers limited

Cooperatives that act as and also act as agents for services in its current formIntermediaries to take financial he banksServices to the rural areas - SHGs borrow from banks and

are beneficiaries of loansthemselves

- Onsite - Cash Withdrawal - Negligible presence of thisATM installed at a branch - Cash Deposit channel in rural areas

- Offsite - Money TransferATM installed at a remote - Cheque Book RequestLocation - Bill Payments

-Phone Banking - Cash Withdrawal - Almost non-existent in rural

Manual - Cash Deposit - India because of low:Interactive Voice Response - Money Transfer Tele-density

- Internet Banking - Cheque Book Request Internet-penetration- Kisan Credit Card - Bill Payments Credit appetite of banks

Provide short-term credit

Branch

Intermediaries

ATM

Others

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 19/47

REASONS FOR UNPROFITABLE OF KASHI

GOMTI SAMYUT GRAMIN

High Non-performing Loans (NPL):

Banks have higher non-performing loans in rural areas

because rural households have irregular income and

expenditure patterns. The issue is compounded by the

dependence of the rural economy on monsoons, and loan

waivers driven by political agendas. NPLs from the

agriculture sector are 7.7%, compared to 3.5% across non-

agriculture sectors8. In order for banks to view rural India as

a growth opportunity, rather than a regulatory requirement,

a combination of these issues must be addressed.

Increasing financial access to rural areas is contingent upon

basic conditions such as proper infrastructure and an

enabling regulatory framework, as well as innovative

19

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 20/47

thinking on the part of commercial banks. Access issues,

however, explain only one part of the problem. Usage is an

equally important issue for rural customers.

Low Ticket Size:

The average ticket size of both a deposit transaction and a

credit transaction in rural areas is small. This means that

banks need more customers per branch or channel to break

even. Considering the small catchments area of a branch in

rural areas, generating a customer base with critical mass is

challenging.

High cost to serve:

Branches are the most used channel in rural areas. This is

because many rural people are not literate and are not

comfortable using technology-driven channels such as

ATMs, phone banking or internet banking. On the other

hand, a branch is an expensive channel for banks (Following

Table). In addition, rural people, whenever they have access

to banks, have frequent low ticket and cash-basedtransactions, which increase the overall transaction cost for

their bank.

20

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 21/47

Cost Per Transaction in Indian Banks

48

25

18

84

0

10

20

30

40

50

60

Branch Phone (Call

Centre)

ATM Phone (IVR) Internet

Series1

Source: Reserve Bank of India; CGAP, World Bank.

Higher risk of credit:

21

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 22/47

Rural households may have highly irregular and volatile

income streams. Irregular wage labor and the sale of

agricultural products are the two main sources of income

for rural households. The poor rural households (landless

and marginal farmers) are particularly dependent on

irregular wage employment. Rural households also have

irregular expenditure patterns. The typical expenditure

profile of rural households is small, with daily or irregular

expenses incurred through the month. Furthermore, a

majority of households incur at least one unscheduledexpenditure per year, with the most frequent reasons being

medical or social emergency7. In short, the rural customer

is generally considered to be a risky one.

Information Asymmetry:

Since many rural people do not have bank accounts, there

is a lack of information on customer behavior in rural India.

Absence of a Credit Information Bureau also complicates

the problem as banks have to rely on informal sources to

learn the credit history of rural customers. A lack of reliable

information can result in either missed opportunities in not

approving otherwise eligible loan candidates, or

nonperforming loans.

22

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 23/47

USAGE ISSUES FOR RURAL CUSTOMERS

Even if access to formal banking is provided to rural

customers, there is no guarantee that these services will be

used. According to a study conducted by the World Bank,

many households, even in developed countries, choose not

to have a bank account as they do not engage in manyfinancial transactions—they collect wages in cash, spend in

cash and do not wish to be burdened by a bank account9.

To compound the situation many customers in rural India,

who have access to and would otherwise choose to use

23

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 24/47

formal financial services, do not do so because the product

and service mixes do not meet their needs.

The financial service needs of rural customers are not

confined to just savings and credit, as is usually assumed.

Their financial needs are linked to their life cycle needs,

ranging from savings to credit to insurance to remittances.

In fact, even the savings and credit products currently

offered to rural customers do not entirely meet their needs.

Access to savings and investment facilities is critical for the

poor. The two critical needs for the rural poor are micro-

savings and frequent withdrawals. These needs

facilitate a customer in building capital over the long term,

as well as coping with income shocks in the near term.

However, banks do not offer adequate services to address

these needs. The lack of services, therefore, leaves the

rural poor with little option than to transact with the

informal banking market. A study conducted by Micro Save

also concludes that the poor transact with the informal

sector because it will accept small amounts, provide

doorstep service, and ensure ease of enrolment.

Rural customers need loans not only for productive

purposes but also for consumption needs (Following Table).

A part from agricultural support, rural customers need micro

24

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 25/47

credit for consumption, education and emergencies. Though

banks offer purpose free loans (personal loans and credit

cards) in urban areas quite liberally, in rural areas sanction

of such loans is significantly restricted. Therefore, the poor

raise these loans through the informal financial system (it is

worth noting that these loans taken from the informal

system are almost always repaid or renewed12). In

addition, larger households need occasional high value

micro-enterprise loans for small capital investment. Though

banks offer these loans, they require excessivedocumentation and time-consuming processes which

discourage customer applications.

Purpose of Borrowing

Rural Household Borrowing

25

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 26/47

Other business

expenditure, 14%

Household

expenditure, 48%

Agriculture

expenditure, 38%

Other business

expenditure

Household

expenditure

Agriculture

expenditure

Bank Lending to Rural Households

Personel Loans, 12%

Agriculture Loan, 36%

Other Business Loan,

52%

Personel Loans

Agriculture Loan

Other Business Loan

A significant percentage of borrowing is toward

consumption and other household expenditure, whereas

formal financial institutions in rural India provide loans

primarily for productive purposes.

Source: AIDIS—2008, National Sample Survey

Organization (NSSO);

Diamond analysis.

26

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 27/47

Insurance reduces the vulnerability of poor households by

replacing the uncertain prospect of large losses with the

certainty of payout against small, regular premium

payments. It is integral to a comprehensive risk

management strategy for poor households. This includes

life, health, accident and asset (dwelling, crop, and

livestock) insurance. Banks and insurance firms do not offer

these services in many rural areas, leading the poor to rely

on the informal financial system.

There are many rural households which depend on weekly

or monthly remittances from their family members who

have moved to urban areas. At present, they depend on

informal channels to remit the money and consequently

either risk the loss of money or pay high transaction fees.

Banks do not offer seamless remittance facilities between

urban and rural branches as many of the rural branches are

not computerized and connected to the main bank’s

computer systems. This often results in the beneficiary

receiving the amount two weeks after it has being

transferred. This represents yet another key service which

is not provided.

The transaction cost for a rural customer to receive credit

primarily constitutes four attributes: the interest rate, loan

amount received as a percentage of amount applied, bribes

27

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 28/47

paid, and the lead time to process the loan. Though the

formal banking system offers loans at interest rates lower

than informal banking systems, the time taken for a loan to

be sanctioned is high which increases uncertainty and

opportunity cost. In addition, the customer needs to pay

almost 10% of the loan amount in bribes and eventually

receives an amount that is less than what was applied for.

Therefore, while the interest rates are usurious in the

informal financing system, rural customers still resort to this

channel because the waiting time to receive the loan isnegligible and there are no indirect costs or commission.

Banks also insist on collateral security which many rural

poor cannot afford.

As far as savings are concerned, though the formal banking

system provides financial security, the cost of opening and

operating an account is high. The overall cost of transacting

with the formal financial system increases for a rural person

because of additional costs such as expenses incurred to

reach a branch and the opportunity cost of lost wages.

Since rural banks are generally not within an accessible

area and do not operate at convenient times, the rural

customer must forgo a day’s wage to reach a branch.

Informal systems, on the other hand, involve a lower

transaction cost, but they are risky and in some cases result

28

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 29/47

in the loss of one’s entire capital. In short, this leaves the

rural customer to choose between two unfavorable options.

In summary, the services being offered by the formal

banking system do not seem to meet the needs of the rural

poor. A World Bank study suggests that the poor apply a set

of criteria to judge the services being offered by any

financial service provider, including:

• Products—Are financial services available and tailored tomy needs?

• Cost—What is the total cost of the service (including

opportunity cost)?

• Convenience—How easy is it to access and use?

• Eligibility—Am I eligible for financial services and can they

be accessed repeatedly?

As explained earlier, the savings products offered in the

current format do not qualify as a flexible, convenient and

cost-efficient service. Similarly, loan products do not meet

product and eligibility criteria. In addition, insurance and

remittance services are not even available. The cost of

services, despite lower interest rates, is high because of

other indirect costs which make the banking services cost-

inefficient.

29

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 30/47

MARKET OPPORTUNITY OF RURAL

BANKING

At present, a rapidly growing urban India is the focus of the

banking sector; however, as the deposit penetration

numbers suggest (Figure 3 & 4), the market is highly

competitive and over banked. Despite this, most banks are

still not shifting their focus to the rural opportunity, as they

are apprehensive about the total market potential of the

rural market and the profitability of rural banking channels.

Contrary to the widely held notion, however, the rural

market is attractive from both a credit and deposit

perspective. The credit demand in rural areas is

approximately Rs 1,330 billion (based on an estimate by

30

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 31/47

World Bank). There are other studies by the Planning

Commission and ICICI Bank which put the figure even

higher at Rs 1,440 billion and Rs 1,500 billion respectively.

Similarly, on the deposit side, a large segment of the rural

population does not save with formal banking channels

because banks are not accessible and do not provide the

appropriate products and service, leaving a significant

opportunity to grow the deposit base.

At present, the penetration of banking in rural areas is sub-optimal with a large market remaining untapped in both the

liability (~ Rs 215 billion) and asset (~ Rs 1,204 billion)

sides of the business. These estimates clearly suggest that

there is sufficient demand in the rural market to encourage

banks to think seriously about rural areas as an alternative

growth opportunity.

As we identified earlier, access and usage are two broad

concerns which explain why the potentially bankable are

unbanked. With regard to access, the challenge for banks is

to identify profitable channels that meet the needs of rural

customers. With regard to usage, banks need to understand

the requirements of the rural customer and customize

products and services

Accordingly (Following Table).

31

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 32/47

Proposed Approach to Tap Potentially

Bankable Population

32

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 33/47

Source: Diamond analysis

IMPROVING ACCESS FOR RURAL BANKING

Convert

Potentially

Bankable

Address

Access Needs

Of Rural

Customers

Ensure

Channel

Profitability

Address

Usage Needs

Of RuralCustomers

Improve

AccessFor Rural

Customers

33

Bank

Initiatives

To Improve

Usage

Encourage

Usage of

Services

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 34/47

Today, branches are the primary delivery channel in rural

areas. Though there are 32,000 commercial bank branches

in India, they cover less than 7% of total villages. Opening

more branches is not necessarily profitable as many

pockets of rural areas do not have business enough to

justify an expensive branch channel. Therefore, to improve

access in rural areas, banks need to modify existing

channels, introduce new channels and identify innovative

ways to integrate the two.

Modify Existing Channels

Fortunately there are a variety of options available for

banks looking to modify their existing channels. To reduce

the costs imposed by branches, banks should consider the

option of sharing their branch infrastructure. Thiswould not be too dissimilar to the example of the telecom

industry sharing network infrastructure or the fast food

industry sharing food courts in urban areas. Though

infrastructure sharing may raise concerns over client

confidentiality and data leakage, in the long run banks will

only benefit from such collaboration.

ATMs are an effective channel which can deliver many of

the services frequently used by a branch customer.

However, ATMs, in their current form, are not suitable for

34

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 35/47

rural areas as the literacy level and transaction ticket

amount is too low. ATMs can, however, be designed to meet

the needs of rural customers. For example, ICICI Bank is

working with IIT Chennai to develop an ATM that has a

biometric fingerprint login, accepts soiled notes, and lower

value denominations. In addition to modifying the design of

the machines, banks should also hold discussions with the

RBI to allow an attendant to be posted at ATMs. This will

enhance the usability of ATMs.

Though phone banking and internet banking are cost-

effective channels, given very low tele-density and low

internet penetration in rural areas, the ability to use these

channels to reach the rural customer is low. However,

phone and internet banking should be considered once

infrastructure and literacy levels improve in rural India. A

business correspondent could then run an e-kiosk to assist

customers to transact over these channels. For example,

Centenary Bank in Uganda uses internet and phone banking

to provide bill payments, money transfers and loan

repayments.

Business correspondents can be provided with point-of-

sale (POS) functionality to allow customers to deposit and

withdraw cash from their accounts. Combining POS with a

smart card is one way to improve access. Brazil has

35

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 36/47

successfully used banking correspondents who use POS and

card readers to provide current accounts, loans, and

insurance, accept bill payments, and perform other

transactions.

Introduce New Channels

The RBI allows banks to appoint business

correspondents and facilitators to be used as

intermediaries in providing banking services. NGOs, MFIs,

Societies, Section 25 companies, registered NBFCs not

accepting public deposits, and Post Offices can be

appointed as Business Correspondents. Business

Correspondents can provide several services which are notcurrently offered by SHGs and MFIs, including: (i)

identification of borrowers and fitment of activities; (ii)

collection and preliminary processing of loan applications

including verification of primary information/data; (iii)

creating awareness about savings and other products and

education and advice on managing money and debt

counseling; (iv) processing and submission of applications

to banks; (v) promotion and nurturing Self Help Groups/Joint

Liability Groups; (vi) post-sanction monitoring; (vii)

monitoring and handholding of Self Help Groups/Joint

36

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 37/47

Liability Groups/Credit Groups/others; and (viii) follow-up for

recovery; (ix) disbursal of small value credit, (x) recovery of

principal/collection of interest (xi) collection of small value

deposits (xii) sale of micro-insurance/ mutual fund products/

pension products/ other third-party products and (xiii)

receipt and delivery of small value remittances/ other

payment instruments.

The introduction of Business Correspondents may face

some challenges from labor unions. However, Diamondbelieves that there may be some options to address the

concerns of the current workforce while using Business

Correspondents to capture more value from rural

customers.

Caixa Economica, a state-owned bank in Brazil, manages

the country’s lottery network and distributes government

benefits. To increase the access of its services, Caixa

extensively utilizes the Banking Correspondent channel,

with 14,000 banking correspondents covering all of Brazil’s

5,500 municipalities. In less than 2 years, Caixa opened

about 2.8 million new accounts and estimates that 40% of

its banking transactions are handled through the banking

correspondent channel.

37

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 38/47

Satellite offices are a cost-effective alternative to

branches. These offices can be established at fixed

premises in villages and are controlled and operated from a

base branch located at a block headquarters. All types of

banking transactions may be conducted at these offices.

Banks have, however, not used this channel actively,

despite the argument that this channel is relatively less

expensive, as it can draw personnel from the main branch

and can remain open for just two days a week. This

channel, therefore, is appropriate in blocks and districtswhich are densely populated. In the urban areas, most

Indian banks opt for an extension counter where the

business does not justify a full-fl edged branch. Similarly,

satellite branches can cater to rural areas which do not

justify a large branch.

Where banks do not find it economical to open full-fl edged

branches of satellite offices, mobile offices may be more

appropriate. Mobile offices extend banking facilities

through a well-protected truck or van. The mobile unit visits

villages on specified days/ hours. The mobile office would

be affiliated with a branch of the bank, and serve areas

which have a large concentration of villages. This will not be

dissimilar to the mobile ATMs implemented by some of the

Indian banks in the urban areas.

38

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 39/47

Determine the Combination of Channels

There is no one right channel or solution to improve access

in rural areas. Banks have to evaluate the trade-offs

between those channels that are most convenient to

customers and those that are the most profitable. Banks are

not comfortable opening new rural branches because many

of those that already exist are unprofitable. Therefore,

determining the right combination of channels is critical to

improving access in profitable ways. An innovative

approach to improving access will consider a combination of

these channels. For example:

• Branches and Satellite Branches— In addition to providing

regular banking operations, providing backend support to

manage and audit the operations of businesscorrespondents.

• A low-cost, custom-made ATM— Managed by a business

correspondent to bring down the operating cost and scale

the channel.

• An e-kiosk—Managed by a business correspondent with

internet banking, ATM and POS terminal in relatively large

rural areas.

• A business correspondent—Using manual ledgers or

POS/Palmtop to act as deposit collector and remitting agent

in smaller rural areas.

39

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 40/47

While this list is not exhaustive, it highlights the need for

creative solutions that apply the right channel to the right

market and transaction. In South Africa, Capitec has

combined convenient branches along transportation routes

(for example, train and bus stations, and taxi stops). In

addition, it has rolled-out debit cards and automatic teller

machines across 200 of these branches to stimulate savings

among low-income earners. Between February and August

2007, the number of customers jumped from around 30,000to more than 90,000.

CONCLUSION

40

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 41/47

There are 185 million bankable adults in rural India who are

unbanked because of access and usage issues. This

presents a significant opportunity for commercial banks.

However, to reach this market and subsequently build an

inclusive financial system, there must be a coordinated and

concerted effort by the three key stakeholders: the

Government of India, the Reserve Bank of India and the

commercial banks.

In addition, a partnership between banks and business

correspondents, and collaboration amongst banks is critical.

Furthermore, banks should tailor their product and service

mix to meet rural needs, and adapt their delivery models to

ensure commercial viability of their rural banking

operations.

BIBLIOGRAPHY

41

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 42/47

1. World Bank 2008

2. Reserve Bank of India 2008

3. www.cia.gov

4. National Sample Survey Organization (NSSO), Household

Consumer

Expenditure in India (2006)

5. Census 2006

6. Access to and Usage of Financial Services, World Bank

2008

7. RFAS, 2008, World Bank & NCAER8. Reserve Bank of India, www.rbi.org.in

9. Access to Financial Services by Stijin Claessens, World

Bank 2005

10. Rutherford Stuart, “The Poor and their Money,” January

2000

11. www.microsave-africa.com

12. RFAS 2008, World Bank

13. Bharat Nirman is a four year business plan of the

Government of India to improve rural infrastructure

14. National Sample Survey Organization (NSSO) 2007.

42

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 43/47

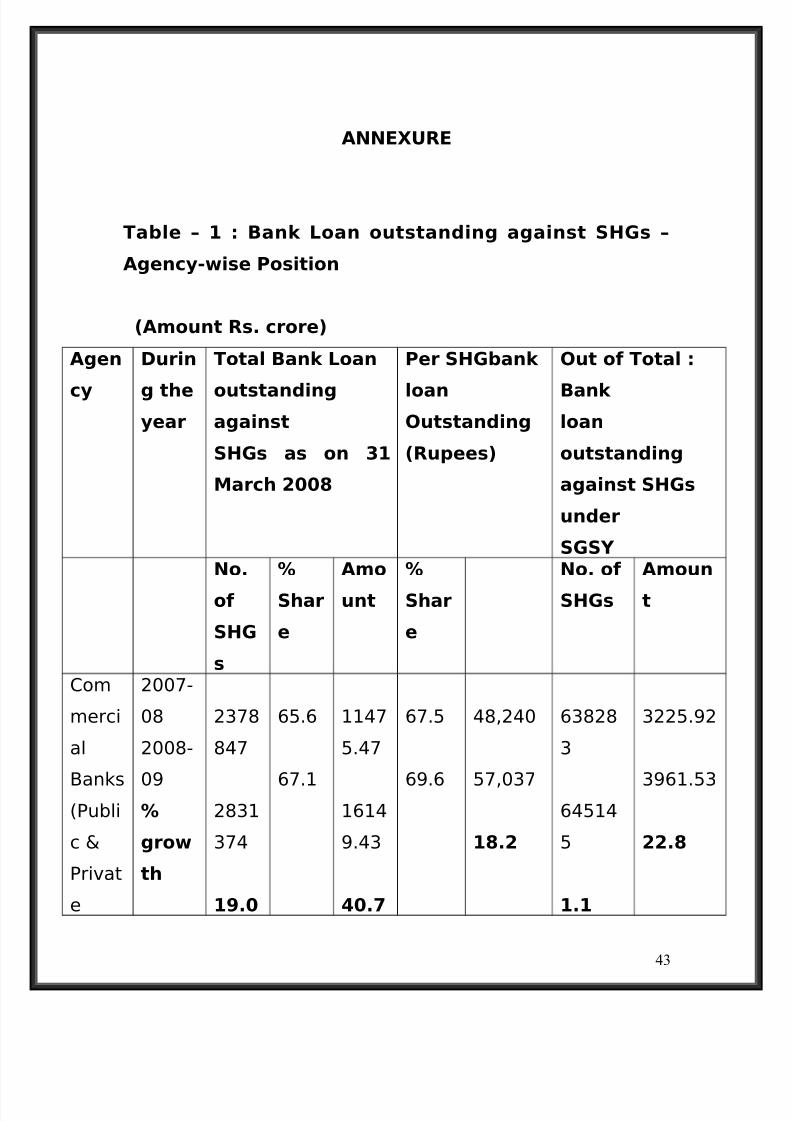

ANNEXURE

Table – 1 : Bank Loan outstanding against SHGs –

Agency-wise Position

(Amount Rs. crore)

Agen

cy

Durin

g theyear

Total Bank Loan

outstandingagainst

SHGs as on 31

March 2008

Per SHGbank

loanOutstanding

(Rupees)

Out of Total :

Bank loan

outstanding

against SHGs

under

SGSY No.

of

SHG

s

%

Shar

e

Amo

unt

%

Shar

e

No. of

SHGs

Amoun

t

Com

merci

al

Banks(Publi

c &

Privat

e

2007-

08

2008-

09%

grow

th

2378

847

2831

374

19.0

65.6

67.1

1147

5.47

1614

9.43

40.7

67.5

69.6

48,240

57,037

18.2

63828

3

64514

5

1.1

3225.92

3961.53

22.8

43

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 44/47

Secto

r)Regio

nalRural

Banks

2007-

082008-

09

%

grow

th

875716

9778

34

11.7

24.2

23.1

4421.04

5224

.42

18.2

26.0

23.0

50,485

53,428

5.8

223191

25889

0

16.0

1332.33

1508.10

13.2

Coop

erativ

e

Banks

2007-

08

2008-

09

%

grow

th

3713

78

4151

30

11.8

10.2

9.8

1103

.39

1306

.00

18.4

6.5

5.8

29,711

31,460

5.9

55504

72852

31.3

258.62

392.09

51.6

TOTA

L

2007-

08

362

594

1

100.

0

169

99.9

0

100.

0

46,884 91697

8

4816.8

7

2008-

09

%

grow

th

4224

338

16.5

100.

0

2267

9.85

33.4

100.0 53,689

14.5

97688

7

6.5

5861.72

21.7

44

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 45/47

Table – 2 : Agency-wise NPAs of Bank loans to SHGs

(

Amount Rs. crore)

Agency Total no.

of Banks

reported

data

on NPAs

NPAs as on 31 March 2009

Outstandi

ng Loans

against

SHGs**

Amount

of NPAs

% of

NPAs to

Outstandi

ng bank

loansCommerci

al Banks(Public

Sector )

26 15086.65 363.27 2.4

Commerci

al Banks

(Private

Sector)

12 1376.93 23.83 1.7

RegionalRural

Banks

(RRBs)

72 4203.46 177.79 4.2

45

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 46/47

Cooperativ

e Banks

182 894.00 60.97 6.8

TOTAL 292 21561.04 625.86 2.9

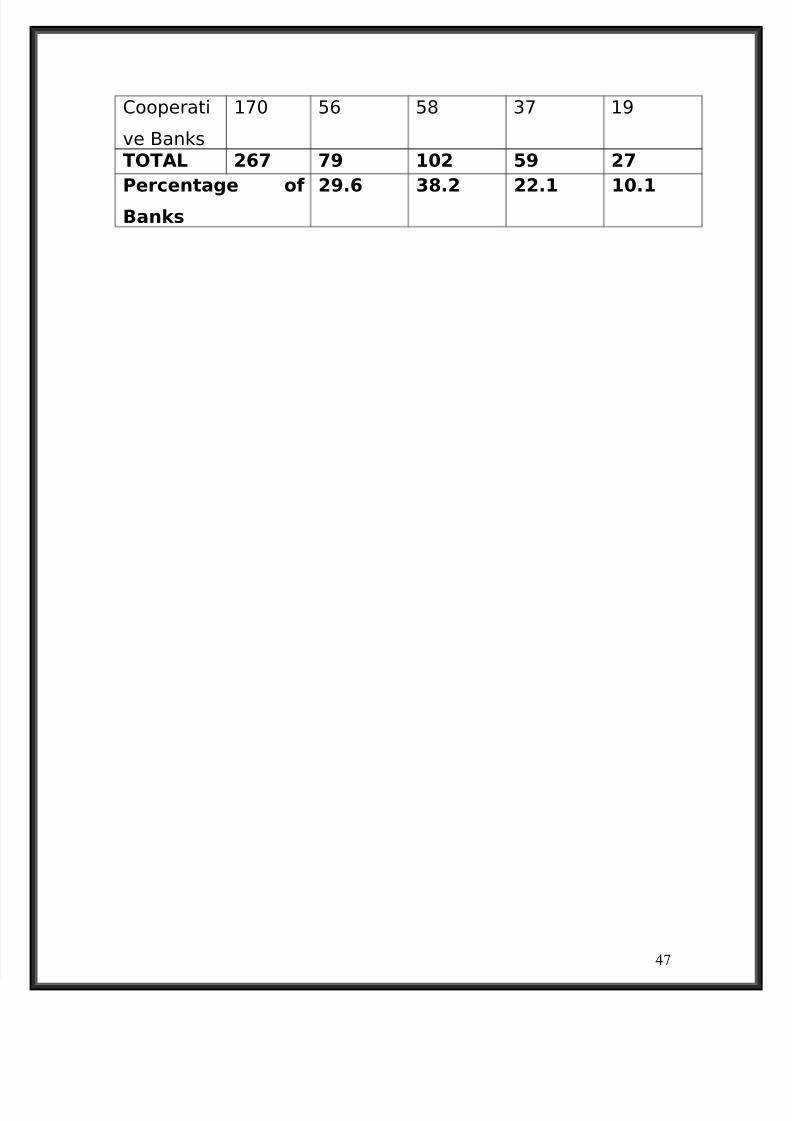

Table – 3 : Recovery Performance – Agency-wise (All

SHGs)

Agency No. of

Banks

report

ed

recove

ry

data

No. of banks based on percentage

distribution of recovery performance

of bank

loans to SHGs as on 31 March 2009=/>

95%

80-94% 50-79% < 50%

Commerci

al Banks

(Public

Sector)

25 6 12 7 0

Commerci

al Banks

(Private

Sector)

7 5 1 0 1

Regional

Rural

Banks

65 12 31 15 7

46

7/29/2019 scai Dox: : D golu kumar

http://slidepdf.com/reader/full/scai-dox-d-golu-kumar 47/47

Cooperati

ve Banks

170 56 58 37 19

TOTAL 267 79 102 59 27

Percentage of

Banks

29.6 38.2 22.1 10.1

![Supporting Information Cancer Treatment Lego” Hybrid ...Isobologram for Combo: DOX(Dose A) and PH(Dose B) (DOX+PH [1:5]). S5 Figure S6. Log(DRI) Plot for Combo: DOX and PH (DOX+PH](https://static.fdocuments.in/doc/165x107/60c3736db4ec761ebd0d1155/supporting-information-cancer-treatment-legoa-hybrid-isobologram-for-combo.jpg)