Sbi facter affecting on sales promotional

82

SAAB MARFIN MBA Study of factors affecting sales of SBI mutual fund and promotion and competition analysis of its popular schemes MBA MARKETING PROJECT REPORT Page | 1

-

Upload

mba-corner-by-babasab-patil-karrisatte -

Category

Business

-

view

221 -

download

0

Transcript of Sbi facter affecting on sales promotional

SAAB MARFIN MBA

Study of factors affecting sales of SBI mutual fund and promotion and competition analysis of its popular

schemes

MBA MARKETING PROJECT REPORT Page | 1

SAAB MARFIN MBA

ContentsExecutive Summary...............................................................................................................................7

Introduction...........................................................................................................................................9

ORGANISATION OF A MUTUAL FUND..............................................................................................11

Sponsor:.......................................................................................................................................12

Trustees:......................................................................................................................................12

Asset Management Company(AMC):...........................................................................................12

Types of AMCs in Indian Context:................................................................................................13

Custodian:....................................................................................................................................13

Registrars & Transfer Agent(R & T Agent):..................................................................................14

SEBI – Securities and Exchange Board of India:...........................................................................14

ADVANTAGES OF MUTUAL FUND........................................................................................................16

Disadvantage of Investing Through Mutual Funds..............................................................................17

TYPES OF MUTUAL FUND SCHEMES:...................................................................................................17

VARIOUS CRITERIA TO EVALUATE THE MUTUAL FUNDS.....................................................................23

P/E Ratio..........................................................................................................................................23

Turnover Ratio.................................................................................................................................24

Expense Ratio..................................................................................................................................24

SHARPE RATIO.................................................................................................................................24

TREYNOR RATIO..............................................................................................................................25

Standard Deviation..........................................................................................................................26

BETA................................................................................................................................................26

NAV..................................................................................................................................................27

Company profile:.................................................................................................................................28

SBI- MUTUAL FUND PRODUCTS:..........................................................................................................30

EQUITY SCHEMES:...........................................................................................................................30

DEBT SCHEMES:...............................................................................................................................31

BALANCED SCHEMES:......................................................................................................................32

CHANNELS OF SELLING MUTUAL FUNDS.............................................................................................34

Mutual Fund Office:.........................................................................................................................34

Intermediaries:................................................................................................................................35

National Distributors.......................................................................................................................35

Banks...............................................................................................................................................36

Individual Financial Advisors............................................................................................................37

MBA MARKETING PROJECT REPORT Page | 2

SAAB MARFIN MBA

The Internet.....................................................................................................................................37

Learning’s from the internship –.........................................................................................................39

Competition Analysis of Various schemes...........................................................................................44

SBI Magnum MIP v/s Reliance MIP......................................................................................................46

Questionnaire......................................................................................................................................51

Factor Analysis through SPSS...............................................................................................................52

Analysis............................................................................................................................................57

Recommendations...............................................................................................................................59

LIMITATIONS........................................................................................................................................60

CONCLUSION.......................................................................................................................................61

BIBLIOGRAPHY.....................................................................................................................................62

MBA MARKETING PROJECT REPORT Page | 3

SAAB MARFIN MBA

Executive SummaryObjective –

1. To study and work in all the distribution channels of SBI mutual fund.

2. To identify various factors that influences the decision of investors while investing in

mutual fund.

3. To compare the popular schemes of SBI mutual Fund with the most popular schemes

in the same segment.

Scope of the project

The project can prove to be very useful to the company as it can help to identify the most

important factors that influence the decision of investor while investing in mutual fund and

working on these factors to improve sales and also communicating these factors to the sales

force so that they can focus on them while convincing the customers. This project will also

help the company to get information about the performance of schemes of its competitors in

the same segment.

Methodology

1. Study all about mutual fund and various schemes.

2. Sell mutual fund through various channels.

3. Identify various factors that influence the investors’ decision while investing in

mutual fund.

4. Listing down of all the factors identified.

5. Develop a questionnaire using these factors on Likert Scale.

6. Take a survey through various distribution channels and also among internal

customers of the company.

MBA MARKETING PROJECT REPORT Page | 4

SAAB MARFIN MBA

7. Analyze primary data collected through SPSS (factor analysis)

8. Study the distribution channel thoroughly and take feedback from various

intermediaries about various schemes of SBI MF and that of its competitors.

9. Based on feedback and ranking given by various organizations identify best schemes

of SBI and its competitors and do a comparative analysis.

10. Make recommendations based on findings.

Sampling

Sample size – 60

Since the questionnaire is long and not easy for anybody to understand so the respondents

were mostly who knoe about mutual i.e. investors and internal customers etc.

IntroductionMutual funds:

MBA MARKETING PROJECT REPORT Page | 5

SAAB MARFIN MBA

Mutual funds, as the name indicates is the fund where in numerous investors come together to

invest in various schemes of mutual fund. Mutual funds are dynamic institution, which plays

a crucial role in an economy by mobilizing savings and investing them in the capital market,

thus establishing a link between savings and the capital market.

A mutual fund is an institution that invests the pooled funds of public to create a diversified

portfolio of securities. Pooling is the key to mutual fund investing. Each mutual fund has a

specific investment objective and tries to meet that objective through active portfolio

management.

Mutual fund as an investment company combines or collects money of its shareholders and

invests those funds in variety of stocks, bonds, and money market instruments. The latter

include securities, commercial papers, certificates of deposits, etc. Mutual funds provide the

investor with professional management of funds and diversification of investment.

Investors who invest in mutual funds are provided with units to participate in stock markets.

These units are investment vehicle that provide a means of participation in the stock market

for people who have neither the time, nor the money, nor perhaps the expertise to undertake

the direct investment in equities. On the other hand they also provide a route into specialist

markets where direct investment often demands both more time and more knowledge than an

investor may possess.

The price of units in any mutual fund is governed by the value of underlying securities. The

value of an investor’s holding in a unit can therefore, like an investment in share, can go

down as well as up. Hence it is said that mutual funds are subjected to market risk. Mutual

fund cannot guarantee a fixed rate of return. It depends on the market condition. If a

particular scheme is performing well then more return can be expected.

It also depends on the fund manager expertise knowledge. It is also seen that people invest in

particular funds depending on who the fund manager is.

MBA MARKETING PROJECT REPORT Page | 6

SAAB MARFIN MBA

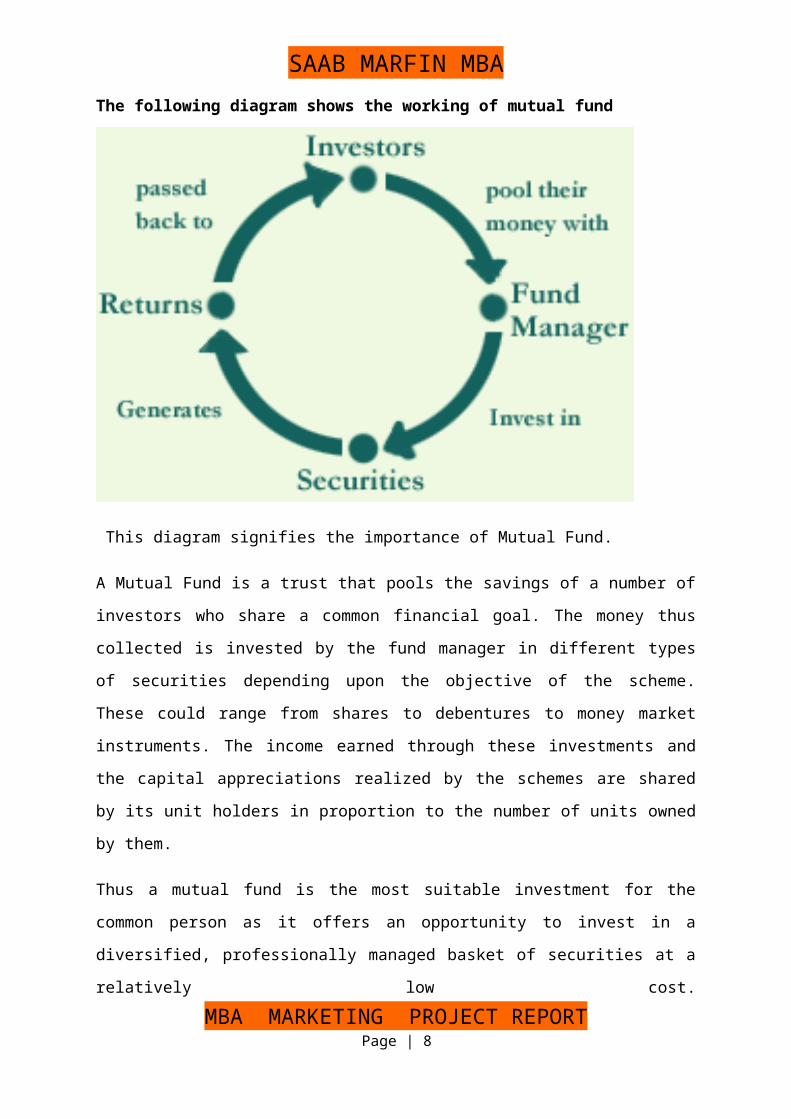

The following diagram shows the working of mutual fund

This diagram signifies the importance of Mutual Fund.

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is invested by the fund manager in different types of

securities depending upon the objective of the scheme. These could range from shares to

debentures to money market instruments. The income earned through these investments and

the capital appreciations realized by the schemes are shared by its unit holders in proportion

to the number of units owned by them.

Thus a mutual fund is the most suitable investment for the common person as it offers an

opportunity to invest in a diversified, professionally managed basket of securities at a

relatively low cost.

Since small investors generally do not have adequate time, knowledge, experience &

resources for directly accessing the capital market, they have to rely on an intermediary,

which undertakes informed investment decisions & provides consequential benefits of

professional expertise.

The advantage of Mutual Funds to the investors is professionally managed, low transaction

cost, liquidity, transparency, well regulated, diversified portfolios & tax benefits. By pooling

their assets through mutual funds, investors achieve economies of scale.

MBA MARKETING PROJECT REPORT Page | 7

SAAB MARFIN MBA

A collected corpus can be used to procure a diversified portfolio indicating greater returns has

also create economies of scale through cost reduction. This principle has been effective

worldwide as more & more investors are going the mutual fund way. This portfolio

diversification ensures risk minimization. The criticality of such a measure comes in when

you factor in the fluctuations that characterize stock markets. The interest of the investors is

protected by the SEBI, which acts as a watchdog. Mutual funds are governed by SEBI

(Mutual Funds) regulations, 1996.

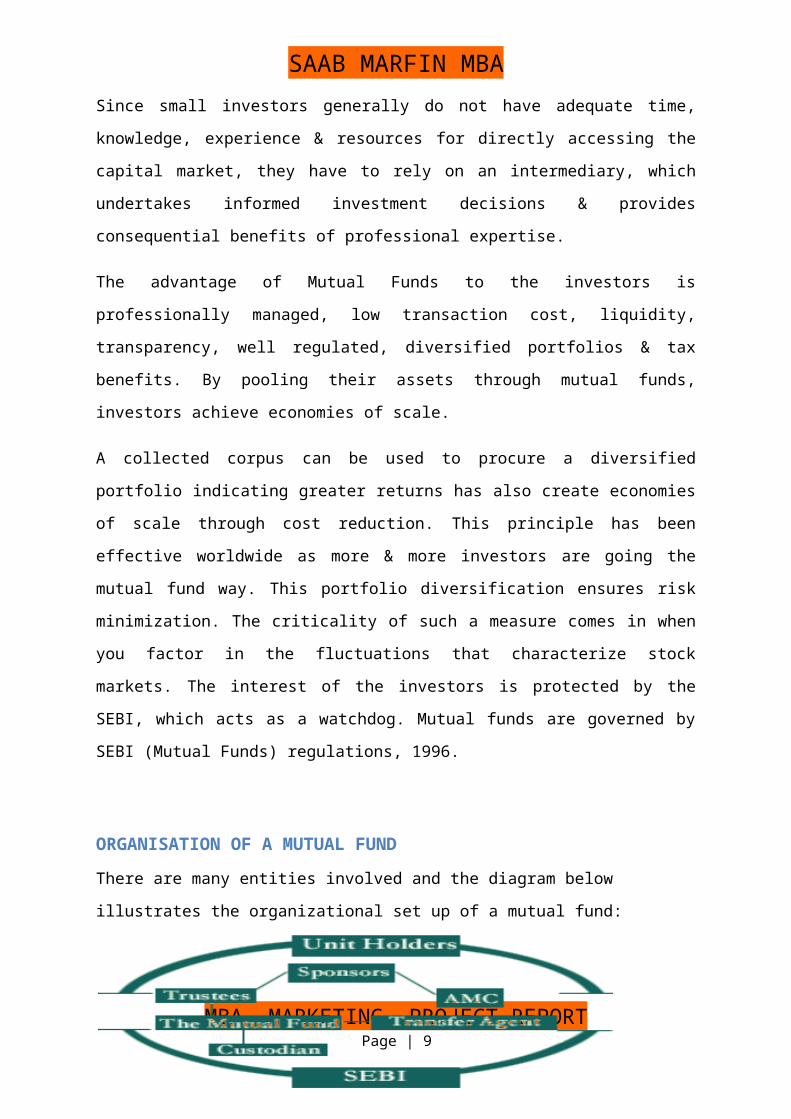

ORGANISATION OF A MUTUAL FUND

There are many entities involved and the diagram below illustrates the organizational set up

of a mutual fund:

Mutual funds have a unique structure not shared with other entities such as companies or

firms. It is important for employees & agents to be aware of the special nature of this

structure, because it determines the rights & responsibilities of the fund’s constituents viz.,

sponsors, trustees, custodians, transfer agents & of course, the fund & the Asset Management

Company(AMC) the legal structure also drives the inter-relationships between these

constituents.

The structure of the mutual fund India is governed by the SEBI (Mutual Funds) regulations,

1996. These regulations make it mandatory for mutual funds to have a structure of sponsor,

trustee, AMC, custodian. The sponsor is the promoter of the mutual fund,& appoints the

trustees. The trustees are responsible to the investors in the mutual fund, & appoint the AMC

for managing the investment portfolio. The AMC is the business face of the mutual fund, as it

manages all affairs of the mutual fund. The mutual fund & the AMC have to be registered

MBA MARKETING PROJECT REPORT Page | 8

SAAB MARFIN MBA

with SEBI. Custodian, who is also registered with SEBI, holds the securities of various

schemes of the fund in its custody.

Sponsor:

The sponsor is the promoter of the mutual fund. The sponsor establishes the Mutual fund &

registers the same with SEBI. He appoints the trustees, Custodians & the AMC with prior

approval of SEBI, & in accordance with SEBI regulations. He must have at least five year

track record of business interest in the financial markets. Sponsor must have been profit

making in at least three of the above five years. He must contribute at least 40% of the capital

of the AMC.

Trustees:

The Mutual Fund may be managed by a Board of trustees of individuals, or a trust company –

a corporate body. Most of the funds in India are managed by board of trustees. While the

board of trustees is governed by the provisions of the Indian trust act, where the trustee is the

corporate body, it would also be required to comply with the provisions of the companies act,

1956. the board of trustee company, as an independent body, act as protector of the unit-

holders interest. The trustees don’t directly manage the portfolio of securities. For this

specialist function, they appoint an AMC. They ensure that the fund is managed by AMC as

per the defined objectives & in accordance with the trust deed & SEBI regulations.

The trust is created through a document called the trust deed i.e., executed by the fund

sponsor in favor of the trustees. The trust deed is required to be stamped as registered under

the provision of the Indian registration act & registered with SEBI. The trustees begin the

primary guardians of the unit-holders funds & assets, a trustee has to be a person of high

repute & integrity.

Asset Management Company(AMC):

The role of an Asset management companies is to act as the investment manager of the trust.

They are the ones who manage money of investors. An AMC takes decisions, compensates

investors through dividends, maintains proper accounting & information for pricing of units,

calculates the NAV, & provides information on listed schemes. It also exercises due diligence

on investments & submits quarterly reports to the trustees. AMCs have been set up in various

countries internationally as an answer to the global problem of bad loans.

MBA MARKETING PROJECT REPORT Page | 9

SAAB MARFIN MBA

Bad loans are essentially of two types: bad loans generated out of the usual banking

operations or bad lending, and bad loans which emanate out of a systematic banking crisis.

It is in the latter case that banking regulators or governments try to bail out the banking

system of a systematic accumulation of bad loans which acts as a drag on their liquidity,

balance sheets and generally the health of banking. So, the idea of AMCs or ARCs is not to

bail out banks, but to bail out the banking system itself.

Types of AMCs in Indian Context:

The following are the various types of AMCs we have in India:

AMCs owned by banks.

AMCs owned by financial institutions.

AMCs owned by Indian private sector companies.

AMCs owned by foreign institutional investors.

AMCs owned by Indian & foreign sponsors.

Custodian:

Often an independent organization, it takes custody all securities & other assets of mutual

fund. Its responsibilities include receipt & delivery of securities collecting income-

distributing dividends, safekeeping of the unit & segregating assets & settlements between

schemes.

Mutual fund is managed either trust company board of trustees. Board of trustees & trust are

governed by provisions of Indian trust act. If trustee is a company, it is also subject Indian

Company Act. Trustees appoint AMC in consultation with the sponsors & according to SEBI

regulation. All mutual fund schemes floated by AMC have to be approved by trustees.

Trustees review & ensure that net worth of the company is according to stipulated norms,

every quarter.

Though the trust is the mutual fund, the AMC is its operational face. The AMC is the first

functionary to be appointed, & is involved in appointment of all other functionaries. The

AMC structures the mutual fund products, markets them & mobilizes fund, manages the

funds & services to the investors.

MBA MARKETING PROJECT REPORT Page | 10

SAAB MARFIN MBA

A draft offer document is to be prepared at the time of launching the fund. Typically, it pre-

specifies investment objectives of the fund, the risk associated, the cost involved in the

process & the broad rules to enter & to exit from the fund & other areas of operation. In India

as in most countries, these sponsors need approval from a regulator, SEBI in our case. SEBI

looks at track records of the sponsor & its financial strength granting approval to the fund for

commencing operations.

A sponsor then hires an asset management company to invest the funds according to the

investment objective. It also hires another entity to be the custodian of the assets of the fund

& perhaps the third one to handle registry work for the unit holder of the fund.

Registrars & Transfer Agent(R & T Agent):

The Registrars & Transfer Agents(R & T Agents) are responsible for the investor servicing

function, as they maintain the records of investors in mutual funds. They process investor

applications; record details provide by the investors on application forms; send out to

investors details regarding their investment in the mutual fund; send out periodical

information on the performance of the mutual fund; process dividend payout to investor;

incorporate changes in information as communicated by investors; & keep the investor record

up-to-date, by recording new investors & removing investors who have withdrawn their

funds.

SEBI – Securities and Exchange Board of India:

Securities and Exchange Board of India (SEBI) is a board (autonomous body) created by

the Government of India in 1988 and given statutory form in 1992 with the SEBI Act 1992

with its head office at Mumbai.

The Securities and Exchange Board of India is perhaps the most important regulatory body.

Similar to the Securities Exchange Commission in the US, it is the authority that has to

always be on its toes. More so, when the markets are doing well and there are a spate of IPOs

(initial public offerings) or FPO’s (follow-on public offerings) like now.

Its main mandate is to protect the interest of investors in the securities markets and to

promote the development of and to regulate the securities markets so as to establish a

dynamic and efficient securities market.

MBA MARKETING PROJECT REPORT Page | 11

SAAB MARFIN MBA

When investors have complaints against listed companies or registered intermediaries, and if

they are not solved directly between the parties concerned, or if the investor is not happy with

the response then SEBI acts as the nodal agency for addressing these complaints.

SEBI has listed certain categories of grievances for which investors can file complaints with

it. These include:

Non-receipt of refund order or allotment advice in case of investment in IPO's, FPO's

and rights issues

Non-receipt of dividend from listed companies

Non-receipt of share certificates after transfer from listed companies

Non-receipt of debentures after transfer or non-receipt of interest or principal on

redemption and non-receipt of interest on delayed repayment

Non-receipt of rights offer letter

MBA MARKETING PROJECT REPORT Page | 12

SAAB MARFIN MBA

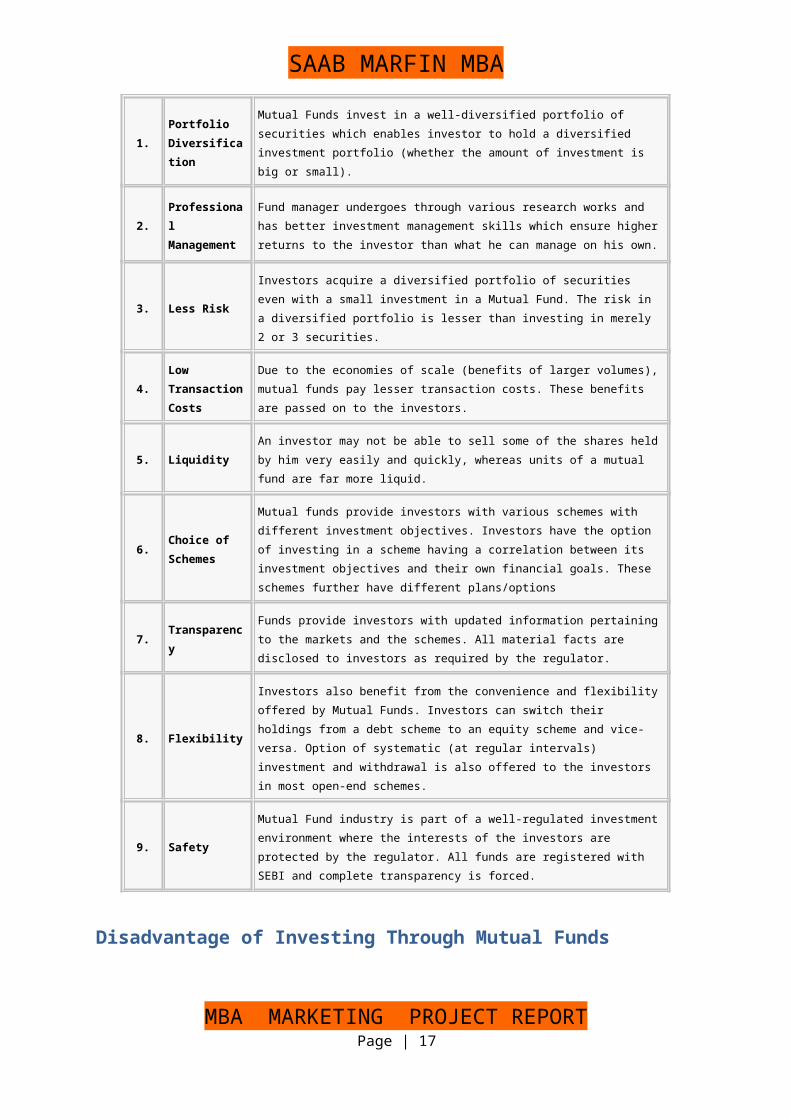

ADVANTAGES OF MUTUAL FUND

S.

No.Advantage Particulars

1.

Portfolio

Diversificati

on

Mutual Funds invest in a well-diversified portfolio of securities which

enables investor to hold a diversified investment portfolio (whether the

amount of investment is big or small).

2.

Professional

Managemen

t

Fund manager undergoes through various research works and has

better investment management skills which ensure higher returns to

the investor than what he can manage on his own.

3. Less Risk

Investors acquire a diversified portfolio of securities even with a small

investment in a Mutual Fund. The risk in a diversified portfolio is lesser

than investing in merely 2 or 3 securities.

4.

Low

Transaction

Costs

Due to the economies of scale (benefits of larger volumes), mutual

funds pay lesser transaction costs. These benefits are passed on to the

investors.

5. Liquidity

An investor may not be able to sell some of the shares held by him

very easily and quickly, whereas units of a mutual fund are far more

liquid.

6.Choice of

Schemes

Mutual funds provide investors with various schemes with different

investment objectives. Investors have the option of investing in a

scheme having a correlation between its investment objectives and

their own financial goals. These schemes further have different

plans/options

7.Transparenc

y

Funds provide investors with updated information pertaining to the

markets and the schemes. All material facts are disclosed to investors

as required by the regulator.

8. Flexibility

Investors also benefit from the convenience and flexibility offered by

Mutual Funds. Investors can switch their holdings from a debt scheme

to an equity scheme and vice-versa. Option of systematic (at regular

intervals) investment and withdrawal is also offered to the investors in

most open-end schemes.

9. Safety

Mutual Fund industry is part of a well-regulated investment

environment where the interests of the investors are protected by the

regulator. All funds are registered with SEBI and complete

transparency is forced.

MBA MARKETING PROJECT REPORT Page | 13

SAAB MARFIN MBA

Disadvantage of Investing Through Mutual Funds

S.

No.

Disadvantag

eParticulars

1.

Costs

Control Not

in the

Hands of an

Investor

Investor has to pay investment management fees and fund

distribution costs as a percentage of the value of his investments (as

long as he holds the units), irrespective of the performance of the

fund.

2.

No

Customized

Portfolios

The portfolio of securities in which a fund invests is a decision taken

by the fund manager. Investors have no right to interfere in the

decision making process of a fund manager, which some investors

find as a constraint in achieving their financial objectives.

3.

Difficulty in

Selecting a

Suitable

Fund

Scheme

Many investors find it difficult to select one option from the plethora

of funds/schemes/plans available. For this, they may have to take

advice from financial planners in order to invest in the right fund to

achieve their objectives.

TYPES OF MUTUAL FUND SCHEMES:

By Structure

o Open-ended schemes

o Close-ended schemes

o Interval schemes

By Investment Objective

o Growth schemes

o Income schemes

o Balance schemes

o Money Market schemes

MBA MARKETING PROJECT REPORT Page | 14

SAAB MARFIN MBA

Other types of schemes

o Tax Saving schemes

o Special schemes

o Index schemes

o Sector specific schemes

Schemes according to maturity period:

A mutual fund scheme can be classified into open-ended scheme or close-ended scheme

depending on its maturity period.

Open-ended Fund / Scheme

An open-ended fund or scheme is one that is available for subscription and repurchase on a

continuous basis. These schemes do not have a fixed maturity period. Investors can

conveniently buy and sell units at Net Asset Value (NAV) related prices which are declared

on a daily basis. The key feature of open-end schemes is liquidity.

Close-ended Fund / Scheme

A close-ended fund or scheme has a stipulated maturity period e.g. 5-7 years. The fund is

open for subscription only during a specified period at the time of launch of the scheme.

Investors can invest in the scheme at the time of the initial public issue and thereafter they

can buy or sell the units of the scheme on the stock exchanges where the units are listed. In

order to provide an exit route to the investors, some close-ended funds give an option of

selling back the units to the mutual fund through periodic repurchase at NAV related prices.

SEBI Regulations stipulate that at least one of the two exit routes is provided to the investor

i.e. either repurchase facility or through listing on stock exchanges. These mutual funds

schemes disclose NAV generally on weekly basis.

Interval scheme

Interval funds combine the features of open-ended & closed ended schemes. They are open

for sale or redemption during pre-determined intervals at NAV related prices.

MBA MARKETING PROJECT REPORT Page | 15

SAAB MARFIN MBA

Schemes according to Investment Objective:

A scheme can also be classified as growth scheme, income scheme, or balanced scheme

considering its investment objective. Such schemes may be open-ended or close-ended

schemes as described earlier. Such schemes may be classified mainly as follows:

Growth / Equity Oriented Schemes

The aim of growth funds is to provide capital appreciation over the medium to long- term.

Such schemes normally invest a major part of their corpus in equities. Such funds have

comparatively high risks.

These schemes provide different options to the investors like dividend option, capital

appreciation, etc. and the investors may choose an option depending on their preferences. The

investors must indicate the option in the application form. The mutual funds also allow the

investors to change the options at a later date. Growth schemes are good for investors having

a long-term outlook seeking appreciation over a period of time.

Income / Debt Oriented Scheme

The aim of income funds is to provide regular and steady income to investors. Such schemes

generally invest in fixed income securities such as bonds, corporate debentures, Government

securities and money market instruments. Such funds are less risky compared to equity

schemes. These funds are not affected because of fluctuations in equity markets. However,

opportunities of capital appreciation are also limited in such funds. The NAVs of such funds

are affected because of change in interest rates in the country. If the interest rates fall, NAVs

of such funds are likely to increase in the short run and vice versa. However, long term

investors may not bother about these fluctuations.

Balanced Fund

The aim of balanced funds is to provide both growth and regular income as such schemes

invest both in equities and fixed income securities in the proportion indicated in their offer

documents. These are appropriate for investors looking for moderate growth. They generally

invest 40-60% in equity and debt instruments. These funds are also affected because of

fluctuations in share prices in the stock markets. However, NAVs of such funds are likely to

be less volatile compared to pure equity funds.

MBA MARKETING PROJECT REPORT Page | 16

SAAB MARFIN MBA

Money Market or Liquid Fund

These funds are also income funds and their aim is to provide easy liquidity, preservation of

capital and moderate income.

These schemes invest exclusively in safer short-term instruments such as treasury bills,

certificates of deposit, commercial paper and inter-bank call money, government securities,

etc. Returns on these schemes fluctuate much less compared to other funds. These funds are

appropriate for corporate and individual investors as a means to park their surplus funds for

short periods.

Other Schemes

Tax Saving Schemes

These schemes offer tax rebates to the investors under specific provisions of the Income Tax

Act, 1961 as the Government offers tax incentives for investment in specified avenues. e.g.

Equity Linked Savings Schemes (ELSS). Pension schemes launched by the mutual funds also

offer tax benefits. These schemes are growth oriented and invest pre-dominantly in equities.

Their growth opportunities and risks associated are like any equity-oriented scheme.

Gilt Fund

These funds invest exclusively in government securities. Government securities have no

default risk. NAVs of these schemes also fluctuate due to change in interest rates and other

economic factors as is the case with income or debt oriented schemes.

Index Funds

Index Funds replicate the portfolio of a particular index such as the BSE Sensitive index,

S&P NSE 50 index (Nifty), etc these schemes invest in the securities in the same weight age

comprising of an index. NAVs of such schemes would rise or fall in accordance with the rise

or fall in the index, though not exactly by the same percentage due to some factors known as

"tracking error" in technical terms. Necessary disclosures in this regard are made in the offer

document of the mutual fund scheme.

MBA MARKETING PROJECT REPORT Page | 17

SAAB MARFIN MBA

There are also exchange traded index funds launched by the mutual funds which are traded

on the stock exchanges.

Sector specific funds / schemes

These are the funds/schemes which invest in the securities of only those sectors or industries

as specified in the offer documents. e.g. Pharmaceuticals, Software, Fast Moving Consumer

Goods (FMCG), Petroleum stocks, etc. The returns in these funds are dependent on the

performance of the respective sectors/industries. While these funds may give higher returns,

they are more risky compared to diversified funds. Investors need to keep a watch on the

performance of those sectors/industries and must exit at an appropriate time. They may also

seek advice of an expert.

MBA MARKETING PROJECT REPORT Page | 18

SAAB MARFIN MBA

MBA MARKETING PROJECT REPORT Page | 19

SAAB MARFIN MBA

VARIOUS CRITERIA TO EVALUATE THE MUTUAL FUNDS

The most important and widely used measures of performance are:-

Basic criterions to evaluate the mutual fund schemes

P/E ratio

Turnover ratio

Expense ratio

Standard deviation

P/E Ratio

A valuation ratio of a company's current share price compared to its per-share earnings.

(EPS).

Calculated as:

EPS is the profit that a company makes on a per share basis. So, if EPS is one, the PE ratio

will reflect the price that an investor will pay for this one rupee of the company's profits.

Higher PE ratio signifies that investor expectation from these shares is higher. This is because

the growth in share price is expected to follow earnings growth.

In general, a high P/E suggests that investors are expecting higher earnings growth in the

future compared to companies with a lower P/E. However, the P/E ratio doesn't tell us the

whole story by itself. It's usually more useful to compare the P/E ratios of one company to

other companies in the same industry, to the market in general or against the company's own

historical P/E.

MBA MARKETING PROJECT REPORT Page | 20

SAAB MARFIN MBA

Turnover Ratio

The turnover ratio is the lower of the total sales or total purchases over the period divided by

the average of the net assets. Higher the turnover ratio, greater is the volume of trading

carried out by the fund.

The turnover ratio is more important for equity and balanced funds where the trading cost of

equities is substantial. So, each time a fund manager buys and sells, he has to keep in mind

that the cost of buying and selling will eat into the fund's returns. Dynamic equity funds,

which can move rapidly between sectors, will obviously have a higher turnover ratio. Here

risk will not be just of the fund manager making a wrong call on a sector but also that of

turnover risk. In comparison a passively managed fund, such as an index fund, will have a

lower turnover rate compared to an active fund as it has to just mirror the index. The only

trading here will be due to investments, redemptions and changes in the index. Also, it is not

meaningful to use turnover ratio for new schemes, which are not fully invested. As the

scheme is deploying its assets there will be more transactions, at least buy orders, as

compared to a fund` which is fully invested. Turnover ratio is less relevant for income funds

as brokerage costs are much lower, and hence they will have a lower potential to eat into

returns. So, even though gilt funds may have equally high turnover as compared to equity

funds, the impact of this turnover is much less.

In Short, Turnover ratio is a measure of how a fund's portfolio changes in a year. This ratio

indicates how much a fund is trading. Understanding turnover ratio helps in gaining insights

into a fund's performance.

Expense Ratio

Expense ratio is the percentage of total assets that are spent to run a mutual fund. As returns

from bond funds tend to be similar, expenses become an important factor while comparing

bond funds.

SHARPE RATIOSt= Rp --Rf

S.D

WHERE

MBA MARKETING PROJECT REPORT Page | 21

SAAB MARFIN MBA

Rp – Avereage return to portfolio

Rf—Risk free rate of interest

S.D- Standard Deviation

Sharpe’s performce index gives a single value to be used for the performance ranking of

various funds or portfolios. Sharpe index measures the risk premium of the portfolio relative

to the total amount of risk in the portfolio. The risk premium is the difference between the

portfolio’s average rate of return and the risk less rate of return. The standard deviation of the

portfolio indicates the risk.

Higher the value of sharpe ratio better the fund has performed. Sharpe ratio can be used to

rank the desirability of funds or portfolios. The fund that has performed well comapred to

other will be ranked first then the others.

TREYNOR RATIO

Ty= Rp—Rf

B

WHERE

Rp- Average return to portfolio

Rf- Risk less rate of interest.

B- Beta coeffecient

Treynor ratio is based on the concept of characteristic line. Characteristic line gives the

relation between a given market return and fund’s return. The fund’s performance is

measured in relation to market performance. The ideal fund’s return rises at a faster rate than

the market performance when the market is moving upwards and its rate of return declines

slowly than the market return, in the decline.

Treynor’s risk premium of the portfolio is the difference between the aveage return and the

risk less rate of return. The risk premium depends on the systematic risk assumed in a

portfoilo.

MBA MARKETING PROJECT REPORT Page | 22

SAAB MARFIN MBA

Standard Deviation

Standard Deviation is the most common statistical measure of judging a fund's volatility and

risk. It gives you a 'quality rating' of an average.

A measure of the total volatility of a fund is based on the trailing three-year monthly returns.

For debt and gilt funds it is based on average weekly return over the past one and a half years.

The Standard Deviation of an average is the amount by which the numbers that go into an

average deviate from that average. It tells us how closely an average represents the

underlying numbers. A high Standard Deviation may be a measure of volatility, but it does

not necessarily mean that such a fund is worse than one with a low Standard Deviation. If the

first fund is a much higher performer than the second one, the deviation will not matter much.

BETA

Beta describes the relationship between the stock’s return and index returns. There can be

direct or indirect relation between stock’s return and index return. Indirect relations are very

rare.

1) Beta =+1.0

It indicates that one percent change in market index return causes exactly one percent change

in the stock return. It indicates that stock moves along with the market.

2) Beta= + 0.5

One percent changes in the market index return causes 0.5 percent change in the stock return.

It indicates that it is less volatile compared to market.

3) Beta=2.0

One percent change in the market index return causes 2 percent change in the stock return.

The stock return is more volatile. The stocks with more than 1 beta value are considered to be

very risky.

4) Negative beta value indicates that the stocks return move in opposite direction to the

market return.

Beta= N*∑XY- (∑X) (∑Y/ N(X*X) * (∑x)

Where

MBA MARKETING PROJECT REPORT Page | 23

SAAB MARFIN MBA

N- No of observation

X- Total of market index value

Y- Total of return to Nav

NAV

Net Asset Value or NAV of a mutual fund is the value of one unit of investment in the fund,

in net asset terms.

NAV = Net Assets of the scheme / Number of Units Outstanding

Where Net Assets are calculated as:-

(Market value of investments + current assets and other assets + Accrued income – current

liabilities and other liabilities – less accrued expenses) / No. of Units Outstanding as at the

NAV date

MBA MARKETING PROJECT REPORT Page | 24

SAAB MARFIN MBA

Company profile:

STATE BANK OF INDIA - MUTUAL FUND - A partner for life

SBI Mutual Fund (SBI MF) is one of the largest mutual funds in the country with an investor

base of over 4.6 million. With over 20 years of rich experience in fund management, SBI MF

brings forward its expertise in consistently delivering value to its investors

Proven Skills in wealth generation:

SBI Mutual Fund is India’s largest bank sponsored mutual fund and has an enviable track

record in judicious investments and consistent wealth creation.

The fund traces its lineage to SBI - India’s largest banking enterprise. The institution has

grown immensely since its inception and today it is India's largest bank, patronized by over

80% of the top corporate houses of the country.

SBI Mutual Fund is a joint venture between the State Bank of India and Société General

Asset Management, one of the world’s leading fund management companies that manages

over US$ 500 Billion worldwide.

Exploiting expertise, compounding growth:

In twenty years of operation, the fund has launched 38 schemes and successfully redeemed

fifteen of them. In the process it has rewarded it’s investors handsomely with consistently

high returns.

A total of over 60 lakh investors have reposed their faith in the wealth generation expertise

of the Mutual Fund.

Schemes of the Mutual fund have consistently outperformed benchmark indices and have

emerged as the preferred investment for millions of investors and HNI’s.

Today, the fund manages over Rs. 51,461 crores of assets and has a diverse profile of

investors actively parking their investments across 37 active schemes.

The fund serves this vast family of investors by reaching out to them through network of over

130 points of acceptance, 29 investor service centers, 55 investor service desks and 45 district

organizers.

MBA MARKETING PROJECT REPORT Page | 25

SAAB MARFIN MBA

SBI Mutual is the first bank-sponsored fund to launch an offshore fund – Resurgent India

Opportunities Fund.

Growth through innovation and stable investment policies is the SBI MF credo.

Fund house expertise:

The investment environment is becoming increasingly complex. Innumerable parameters

need to be factored in to generate a clear understanding of market movement and

performance in the near and long term future.

At SBIMF, we devote considerable resources to gain, maintain and sustain our profitable

insights into market movements. We consistently push the envelope to ensure our investors

get the maximum benefits year after year.

Research - the backbone of our Performance

Our expert team of experienced and market savvy researchers prepare comprehensive

analytical and informative reports on diverse sectors and identify stocks that promise high

performance in the future.

This team works in tandem with a compliance and risk-monitoring department, which

ensures minimization of operational risks while protecting the interests of the investors.

Quite naturally many of our equity funds have delivered consistent returns to investors and

have repeatedly out performed benchmark indices by wide margins.

Risk Management Team:

The Risk Management unit is a separate division within the organization headed by the Chief

Risk Officer (CRO). A Risk Management Committee, comprising the MD, Deputy CEO,

CRO, COO, CIO and the CMO meets on a regular basis to manage risk within the

organization.

The CRO is responsible for risk management over all the functions within the organization

including Investments, Marketing, Operations, etc. Currently, the CRO is an experienced

investment professional and is assisted by a two-member team, one being an investment

Professional with an MBA in Finance and the other being an investment professional deputed

from SGAM.

MBA MARKETING PROJECT REPORT Page | 26

SAAB MARFIN MBA

SBI- MUTUAL FUND PRODUCTS:

EQUITY SCHEMES:

The investments of these schemes will predominantly be in the stock markets and endeavor

will be to provide investors the opportunity to benefit from the higher returns which stock

markets can provide. However they are also exposed to the volatility and attendant risks of

stock markets and hence should be chosen only by such investors who have high risk taking

capacities and are willing to think long term. Equity Funds include diversified Equity Funds,

Sectoral Funds and Index Funds. Diversified Equity Funds invest in various stocks across

different sectors while Sectoral funds which are specialized Equity Funds restrict their

investments only to shares of a particular sector and hence, are riskier than Diversified Equity

Funds. Index Funds invest passively only in the stocks of a particular index and the

performance of such funds move with the movements of the index.

Magnum COMMA Fund

Magnum Equity Fund

Magnum Global Fund

Magnum Index Fund

Magnum MidCap Fund

Magnum Multicap Fund

Magnum Multiplier Plus 1993

Magnum Sector Funds Umbrella

MSFU - FMCG Fund

MSFU - Emerging Businesses Fund

MSFU - IT Fund

MSFU - Pharma Fund

MSFU - Contra Fund

MBA MARKETING PROJECT REPORT Page | 27

SAAB MARFIN MBA

SBI Arbitrage Opportunities Fund

SBI Blue chip Fund

SBI Infrastructure Fund - Series I

SBI Magnum Taxgain Scheme 1993

SBI ONE India Fund

SBI TAX ADVANTAGE FUND - SERIES I

DEBT SCHEMES:

Debt Funds invest only in debt instruments such as Corporate Bonds, Government Securities

and Money Market instruments either completely avoiding any investments in the stock

markets as in Income Funds or Gilt Funds or having a small exposure to equities as in

Monthly Income Plans or Children's Plan. Hence they are safer than equity funds. At the

same time the expected returns from debt funds would be lower. Such investments are

advisable for the risk-averse investor and as a part of the investment portfolio for other

investors.

Magnum Children’s Benefit Plan

Magnum Gilt Fund

Magnum Gilt Fund (Long Term)

Magnum Gilt Fund (Short Term)

Magnum Income Fund

Magnum Income Plus Fund

Magnum Income plus Fund (Saving Plan)

Magnum Income plus Fund (Investment Plan)

Magnum Insta Cash Fund

Magnum InstaCash Fund -Liquid Floater Plan

Magnum Institutional Income Fund

MBA MARKETING PROJECT REPORT Page | 28

SAAB MARFIN MBA

Magnum Monthly Income Plan

Magnum Monthly Income Plan Floater

Magnum NRI Investment Fund

SBI Capital Protection Oriented Fund - Series I

SBI Debt Fund Series

SDFS 15 Months Fund

SDFS 90 Days Fund

SDFS 13 Months Fund

SDFS 18 Months Fund

SDFS 24 Months Fund

SDFS 30 DAYS

SDFS 30 DAYS

SDFS 60 Days Fund

SDFS 180 Days Fund

SDFS 30 DAYS

SBI Premier Liquid Fund

SBI Short Horizon Fund

SBI Short Horizon Fund - Liquid Plus Fund

SBI Short Horizon Fund - Short Term Fund

BALANCED SCHEMES:

Magnum Balanced Fund invests in a mix of equity and debt investments. Hence they are less

risky than equity funds, but at the same time provide commensurately lower returns. They

provide a good investment opportunity to investors who do not wish to be completely

MBA MARKETING PROJECT REPORT Page | 29

SAAB MARFIN MBA

exposed to equity markets, but is looking for higher returns than those provided by debt

funds.

Magnum Balanced Fund

Magnum NRI Investment Fund - Flexi Asset Plan

MBA MARKETING PROJECT REPORT Page | 30

SAAB MARFIN MBA

CHANNELS OF SELLING MUTUAL FUNDS

Mutual funds are emerging as an important financial intermediary for the investing public in

India. Conceptually and operationally they are different. The investors need to understand the

working of a mutual fund and the increasingly diverse and complex investment options

brought to them by a large number of mutual funds. The key channel in bringing the mutual

funds to a large number of investors all over the country is the network of

INTERMEDIARIES/DISTRIBUTORS. In this industry we have five different channels

through which mutual fund are sold:

• Mutual Fund Company

• National Distributors (NDs) & Intermediaries

• Banks

• Individual Financial Advisors (IFAs)

• Internet

Each one has its own customer base. Their way of dealing with them is totally different from

other. Every one attracts in their own way. How they attract we will study. There are many

industries here. The urgency to keep increasing in size has led mutual funds to use marketing

hooks to draw investors. As we rely only on channel partners, our relation with them really is

going to play a vital role. How different companies lure the partners, we’ll study that. As to

start with we will first study about the intermediaries in brief by describing who they are and

how they help a direct investor.

Mutual Fund Office:

Anyone can walk into a mutual fund’s office, and buy/sell units of its schemes. It’s a simple

process, and there are employees of the fund house on hand to guide you through. If you are

buying units, you will have to fill up an application form and hand over a cheque equivalent

to your investment. The fund house will give you an acknowledgement of your investment in

its scheme(s) and subject to your cheque being cleared, send you an account statement within

three to seven days. Since a fund house market only its schemes and not those of its

competitors, buying directly means knowing which fund house we want to invest in. If we are

selling units, the relevant document is the redemption form, which sometimes forms part of

MBA MARKETING PROJECT REPORT Page | 31

SAAB MARFIN MBA

your account statement and can be torn off it, or can be had from the fund house’s office. The

fund house mails the cheque within three days. The problem with transacting through fund

house is that they have a very thin presence. Most fund houses have just an office or two in

the big cities; moreover, since such offices are located in the central business district, for

most investors, this means travelling a fair distance. It’s worse in smaller centres-only a few

fund houses have a scattered presence. But as the industry grows and gains greater investor

acceptance. Mutual funds are bound to expand beyond cities.

Intermediaries:

Distributors such as agents, banks and stockbrokers are present in much greater numbers,

which makes them the preferred option among investors. While dealing with the

intermediaries, make sure they have the AMFI (Association of Mutual Fund in India)

certification-a SEBI precondition; since September 2003, for selling mutual funds, intended t

ensure that only qualified distributors dispense mutual fund advice. AMFI issues photo

identity cards to registered intermediaries, which is proof of their having acquired the

certification.

National Distributors

The big agents are one-stop sellers of financial products. Agents score over mutual funds on

convenience, choice and quality of service. They operate from multiple locations-for

example, national distributors like Bajaj Capital has more outlets than most mutual funds-and

are supported by an army of registered agents, some of whom are willing to come to our

doorstop and sell schemes to you. Further, while a mutual fund offer its schemes, a big agent

has the biggest stock among all mutual fund sellers, selling virtually all schemes of virtually

every fund house, as well as other investment products. For us, this means more choice. If we

know the scheme we want to invest in, go to an agent, fill up the scheme’s form and give in a

cheque. Even if we don’t know which scheme we want to invest in, a good agent will

understand our need and help you pick a scheme. The agent should understand our reasons

for investing in a mutual fund and based on that offer us appropriate options, and let us make

a choice. An agent is supposed to be impartial and not show a preference towards a particular

fund house. The very nature of the relationship between an intermediary and fund houses

opens up the possibility of bias. Fund houses pay intermediaries a commission linked to the

business they bring in. If fund house X pays a higher commission than fund house Y, an

intermediary might push scheme X, as it stands to earn more. How do we know that we are

MBA MARKETING PROJECT REPORT Page | 32

SAAB MARFIN MBA

being misguided or not? The entry load charged by a scheme can offer us some clues. The

entry load represents the upfront costs an investor pays to invest in a scheme, and the agent’s

commission tends to flow out of it. The higher the entry load, chances are, the higher the

agent’s commission. If the agent is pushing the higher load scheme, perhaps he is more

interested in maximizing his commission than our returns. Hence always know the entry load

being charged by a scheme. Till mid 2002, intermediaries passed on a part of their

commission to investors, as an incentive to invest. The amount of cash paid depended largely

on much they got from a fund house. Obviously the more they got form the fund house, the

more they passed on to investors. This often created an unhealthy situation, where cash

incentives, and not investment-worthiness, determined which scheme, an agent

recommended. In June 2002, to stop such abuse, SEBI made it illegal for intermediaries to

give money and gifts to investors. Although intermediaries can’t lure you with money now

(legally speaking that is), their commission-based earnings structure means a distributor

could still be a partial to a fund house. Which is why, listen to what an intermediary to say

but also do the homework, and use your judgement to make an informed decision.

Banks

A number of banks, especially the private and foreign ones, are into marketing the mutual

fund schemes. Many of them market not only their own schemes, but also those of their rivals

as a point of purchase; banks are a good option because of their fantastic reach-banks can be

founded in every neighborhood. This wide reach has enabled banks to emerge as a major

distributor. In 1999, barely 10 percent of fresh mutual fund sales were made through banks;

during 2003, various estimates put the share of banks in mutual fund sales at between 30

percent and 50 percent. In terms of scope of service, banks are a notch below agents.

Whatever your profile or investment amount might be, an agent will offer you personalized

service-he will listen to your investment needs, offer you information on various schemes as

asked by you, and suggest investment options. However, typically a bank will not give you

this option or attention, unless you are a big money client and subscribe to its wealth

management services. What banks will do, unconditionally, is help you through the

investment formalities like filling up a form and offering basic information. But things are

changing and banks are also giving personalized service to its retail investors also.

MBA MARKETING PROJECT REPORT Page | 33

SAAB MARFIN MBA

Individual Financial Advisors

Big brokers combine the attributes of agents (one-stop shop, personalized service) and banks

(a team of analyst who crack the mutual fund industry). This service, though usually comes at

a cost, and is reserved for their clients. Small brokers, on the other hand, welcome retail

investors, but most of them market schemes of select fund houses only. These are

independent professionals trained to advice you on all personal finance matters. They all sell

financial products, as agents currently do. Unlike agents, though, CFPs might charge you for

their services.

The Internet

At present, around 3 percent of mutual fund transactions are done online. This figure is bound

to increase, with better Net connectivity are also expected to tie up with more banks, which

will bring more investors into the loop.The other move that will provide a fillip to online

transactions to be supplemented by physical documentation. At present, some fund houses

enable buying-and in some instances, selling on three platforms:

1. Own websites-- Most of the mutual fund houses let you buy and sell the units of their

schemes through their websites. All you need is a Net banking account with any of the banks

the fund houses have tied up with. You log on to the fund’s site, choose your scheme and

investment amount. A link on the website takes you to the website of the designated bank,

where you make your payment.

Money is transferred from your Net banking account to the mutual fund and units are allotted

to you instantaneously. The transaction is also documented in the physical form-the fund

houses send you the application form to sign, and send back. Once you have done an online

transaction with a fund house, you can open an online account with it. This will enable you to

sell your holdings, switch between the schemes and purchase additional units-at the click of a

mouse.

2. Financial Portals-- You can also buy units of several mutual funds through financial

portals as myiris.com, timesofmoney.com and indiainfoline.com among others. The process

and requirements are similar to that of for buying through the fund’s site. However, most

portals enable only purchase.

3. Online trading portals-- Share trading portals like ICICI Direct (icicidirect.com) and

Sharekhan (sharekhan.com) too offer a fair number of mutual fund schemes on their

MBA MARKETING PROJECT REPORT Page | 34

SAAB MARFIN MBA

platforms. Registered user can buy or sell their units on offer, just like a stock-at no extra

cost.

SBI Mutual Fund Gurgaon has 30 IFAs and NDs and they also sell mutual fund through all

its SBI branches in Gurgaon and some of the private banks like Axis bank. Some brokerage is

charged by NDs and IFAs, no brokerage is given for sales through SBI branches and direct

selling through head Office of SBI mutual Fund.

MBA MARKETING PROJECT REPORT Page | 35

SAAB MARFIN MBA

Learning’s from the internship –

I was put into the distribution channel of SBI mutual Fund. Most of the time was spent selling

and promoting SBI mutual fund in MR branch of SBI. Since only small investors visit that

bank so I was asked to focus mainly on two schemes of equity diversified segment of SBI

mutual fund – SBI MSFU Contra Fund, SBI MSFU Emerging Business Fund and SBI

Magnum Taxgain fund (for tax saving). Emerging Business Fund has also been rated five

stars by moneycontrol.com. Contra Fund and Taxgain fund are most famous funds of SBI

mutual fund. Most of the investors I came across had already heard about Contra and Taxgain

fund. I gained a good knowledge of Mutual fund and also a nice experience of selling mutual

funds through this internship. After spending some weeks in SBI banks I visited other

channels of Distribution. I was sent to various IFAs, National Distributors and Private Banks.

Promotion of new brokerage plan for SIP and MIP was also done while visiting IFA’s and

national Distributors. Through interaction with them I found out that SBI had a tough

competition with Reliance, Birla SL, HDFC, DSP BR, UTI, IDFC, Fidelity and ICICI

prudential. Investors especially big investors who have already invested in mutual funds

preferred these companies over SBI. Services offered by private companies were better than

that of SBI. I have shortlisted some schemes in the same segment i.e. equity diversified

scheme to compare with MSFU contra fund and MSFU emerging business fund. Based on

rankings on www.moneycontrol.com and feedback from various investors and NDs and also

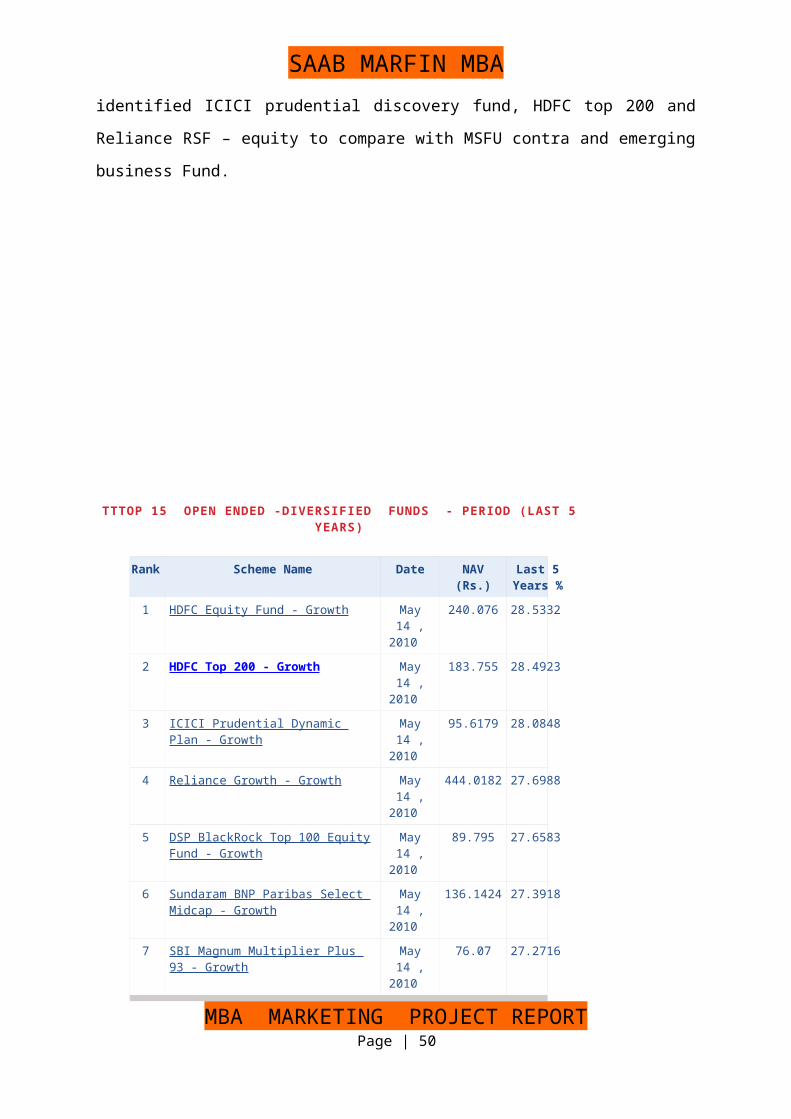

survey in banks like ICICI, Indusind etc. I identified ICICI prudential discovery fund, HDFC

top 200 and Reliance RSF – equity to compare with MSFU contra and emerging business

Fund.

TTTOP 15 OPEN ENDED -DIVERSIFIED FUNDS - PERIOD (LAST 5 YEARS)

MBA MARKETING PROJECT REPORT Page | 36

SAAB MARFIN MBA

Rank Scheme Name Date NAV (Rs.) Last 5

Years %

1 HDFC Equity Fund - Growth May 14 , 2010

240.076 28.5332

2 HDFC Top 200 - Growth May 14 , 2010

183.755 28.4923

3 ICICI Prudential Dynamic Plan - Growth

May 14 , 2010

95.6179 28.0848

4 Reliance Growth - Growth May 14 , 2010

444.0182 27.6988

5 DSP BlackRock Top 100 Equity Fund - Growth

May 14 , 2010

89.795 27.6583

6 Sundaram BNP Paribas Select Midcap - Growth

May 14 , 2010

136.1424 27.3918

7 SBI Magnum Multiplier Plus 93 - Growth

May 14 , 2010

76.07 27.2716

8 Birla Sun Life Frontline Equity Fund - Plan A - Growth

May 14 , 2010

79.89 26.9049

9 SBI Magnum Sector Umbrella - Contra Fund - Growth

May 14 , 2010

54.36 26.6358

10 Reliance Equity Opportunities Fund - Growth

May 14 , 2010

31.66 25.991

11 Reliance NRI Equity Fund - Growth May 14 , 2010

35.8151 25.8727

12 SBI Magnum Equity Fund - Growth May 14 , 2010

39.38 25.756

13 Birla Sun Life Mid Cap Fund - Plan A - Growth

May 14 , 2010

105.88 25.5568

14 DSP BlackRock India Tiger Fund - Growth

May 14 , 2010

44.928 25.5228

15 Sundaram BNP Paribas Select Focus - Growth

May 14 , 2010

83.6513 25.3097

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

Source – www.mutualfundsindia.com

From the above table it is clear that magnum contra fund and HDFC Top 200 have been

ranked in top 10 for the period of last 5 years with an average return of 26.6%.

MBA MARKETING PROJECT REPORT Page | 37

SAAB MARFIN MBA

TOP 15 OPEN ENDED -DIVERSIFIED FUNDS - PERIOD (LAST 3 YEARS)

Rank Scheme Name Date NAV (Rs.) Last 3

Years %

1 IDFC Premier Equity Fund - Plan A - Growth May 14 , 2010

28.5311 23.4317

2 Reliance Regular Savings Fund - Equity - Growth

May 14 , 2010

28.2826 21.5581

3 ING Dividend Yield Fund - Growth May 14 , 2010

21.23 21.3639

4 Sundaram BNP Paribas SMILE Fund - Growth

May 14 , 2010

31.7935 20.4443

5 ICICI Prudential Discovery Fund - IP- Growth May 14 , 2010

19.59 19.8633

6 Birla Sun Life Dividend Yield Plus - Growth May 14 , 2010

75.73 19.7577

7 UTI Dividend Yield Fund - Growth May 14 , 2010

28.64 18.9938

8 UTI Opportunities Fund - Growth May 14 , 2010

23.86 18.9221

9 ICICI Prudential Discovery Fund - Growth May 14 , 2010

44.26 18.3609

10 HDFC Top 200 - Growth May 14 , 2010

183.755 17.4927

11 Canara Robeco Equity Diversified - Growth May 14 , 2010

50.52 17.1731

12 Tata Dividend Yield Fund - Growth May 14 , 2010

29.3495 17.1138

13 Reliance Growth - Growth May 14 , 2010

444.0182 16.4405

14 Tata Equity P/E Fund - Growth May 14 , 2010

44.2171 16.4259

15 HDFC Equity Fund - Growth May 14 , 2010

240.076 16.4196

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

From the above table it is seen that none of the SBI schemes have been in top 15 if take last 3

years data, though HDFC top 200 is still there on 10 th rank. Other schemes from different

company have come up like – ICICI prudential discovery fund – Growth and Reliance

regular savings fund growth.

MBA MARKETING PROJECT REPORT Page | 38

SAAB MARFIN MBA

TOP 15 OPEN ENDED -DIVERSIFIED FUNDS - PERIOD (LAST 6 MONTHS)

Rank Scheme Name Date NAV (Rs.) Last 6

Months %

1 ICICI Prudential Discovery Fund - IP- Growth May 14 , 2010

19.59 21.7526

2 ING Dividend Yield Fund - Growth May 14 , 2010

21.23 21.4531

3 ICICI Prudential Discovery Fund - Growth May 14 , 2010

44.26 21.0613

4 ICICI Prudential Emerging STAR Fund - IP - Growth

May 14 , 2010

13.37 20.4505

5 Canara Robeco Emerging Equities - Growth May 14 , 2010

20.02 20.3848

6 DSP BlackRock Small and Midcap Fund - Growth

May 14 , 2010

16.087 19.8198

7 ICICI Prudential Emerging STAR Fund - Growth

May 14 , 2010

32.96 19.637

8 Reliance Equity Opportunities Fund - Growth May 14 , 2010

31.66 18.9689

9 SBI Magnum Sector Umbrella - Emerging Businesses Fund - Growth

May 14 , 2010

35.53 18.5519

10 Taurus Ethical Fund - Growth May 14 , 2010

21.34 18.031

11 IDFC Small & Midcap Equity Fund - Growth May 14 , 2010

16.8373 17.2538

12 Fortis Future Leaders Fund - Growth May 14 , 2010

8.785 17.2115

13 UTI Master Value Fund - Growth May 14 , 2010

46.72 17.1808

14 Escorts Growth Plan - Growth May 14 , 2010

74.9237 17.1356

15 Religare Mid Cap Fund - Growth May 14 , 2010

12.87 16.7877

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

From the above table it is seen that neither HDFC top 200 nor Magnum contra fund and nor

Reliance RSF growth are in top 15 but ICICI prudential Discovery fund growth is on 3 rd rank

and SBI MSFU emerging business fund has come up on 9th rank which was nowhere earlier.

MBA MARKETING PROJECT REPORT Page | 39

SAAB MARFIN MBA

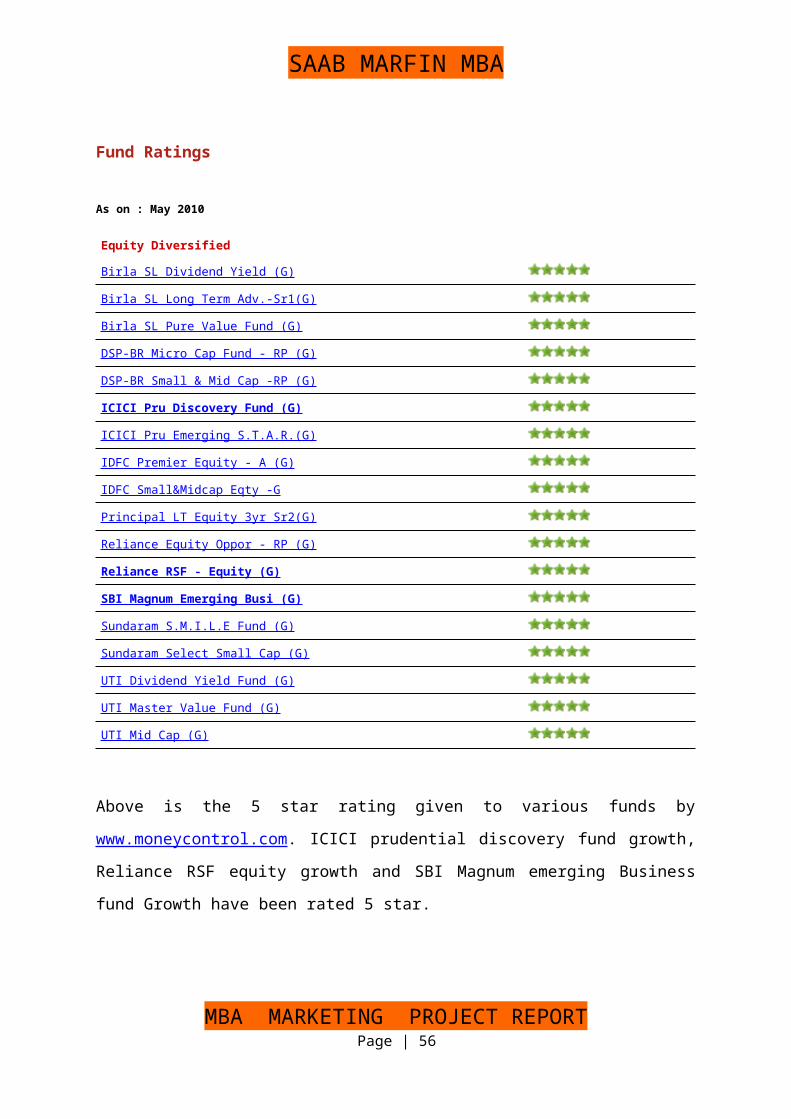

Fund Ratings

As on : May 2010

Equity Diversified

Birla SL Dividend Yield (G)

Birla SL Long Term Adv.-Sr1(G)

Birla SL Pure Value Fund (G)

DSP-BR Micro Cap Fund - RP (G)

DSP-BR Small & Mid Cap -RP (G)

ICICI Pru Discovery Fund (G)

ICICI Pru Emerging S.T.A.R.(G)

IDFC Premier Equity - A (G)

IDFC Small&Midcap Eqty -G

Principal LT Equity 3yr Sr2(G)

Reliance Equity Oppor - RP (G)

Reliance RSF - Equity (G)

SBI Magnum Emerging Busi (G)

Sundaram S.M.I.L.E Fund (G)

Sundaram Select Small Cap (G)

UTI Dividend Yield Fund (G)

UTI Master Value Fund (G)

UTI Mid Cap (G)

Above is the 5 star rating given to various funds by www.moneycontrol.com. ICICI

prudential discovery fund growth, Reliance RSF equity growth and SBI Magnum emerging

Business fund Growth have been rated 5 star.

Though HDFC top 200 has been rated 4 star and SBI magnum Contra fund has been rated 1

star. But at the same time valueresearch has rated Magnum contra fund with 4 stars.

MBA MARKETING PROJECT REPORT Page | 40

http://www.moneycontrol.com/mutual-funds/nav/sundaram-bnp-paribas-s-m-i-l-e-fund-regular-plan/MSN066

SAAB MARFIN MBA

Competition Analysis of Various schemes

From the above analysis it is observed that ICICI prudential discovery is giving highest

returns since inception followed by emerging business fund and HDFC top 200, and contra is

MBA MARKETING PROJECT REPORT Page | 41

ICICI Prudential Discovery fund (G)

SBI MSFU

Contra

fund (G)

Reliance

RSF

equity (G)

SBI MSFUemerging business fund (G)

HDFC top

200 (G)FACTS Inception Date 14/8/2004 5/7/1999 9/6/2005 17/9/2004 11/9/1996

Face Value 10 10 10 10 10Fund Size(in Cr.) 971.34 3632.34 2669.98 222.8 7219.5Increase in fund sizesince 31st mar 2010(in Cr.)

95.58 77.65 169.29 17.58 360.66

Expense ratio 2.08 1.91 1.9 2.38 1.8portfolio turnoverratio

223 111 40 198 50.95

NAV latest 44.26 54.36 28.28 35.53 183.7652-week high 45.16 57.28 29.46 37.86 187.8952-week low 23.3 41.23 18.87 21.02 131.99

returns 1 month -0.09 -4.09 -3.58 -3.19 -1.123 months 9.88 3.94 4.72 8.62 7.876 months 21.06 3.54 7.71 18.55 3.931 year 110.16 52.44 74.48 92.68 62.573 years 18.36 11.21 21.56 6.5 17.495 years 25.27 26.64 NA 16.94 28.49Since inception 29.52 19.04 23.41 25.12 23.96

Risk Sharpe -0.11 -0.11 -0.13 -0.2 -0.07Beta 0.82 0.87 0.88 0.99 0.88treynor -0.71 -0.63 -0.75 -1.25 -0.39

Portfolio Market cap (in Cr.) 35,452.31 81,798.56 52,144.25 18,543.08 79,610.86

Large 31.06 63.72 49.92 8.16 80.42Mid 48.61 28.9 31.99 49.86 14.57Small 10.44 1.11 2.08 33.62 2.41No. of stocks 56 80 45 35 66P/e ratio 21.91 26.24 20.2 35.74 24.44

Asset allocation

equity 90.96 93.73 93.37 94.77 97.41

Debt 0 0.97 0 0 0Cash and equivalent 9.04 5.3 6.63 5.23 2.59

SAAB MARFIN MBA

giving lowest returns amongst the following. If we look at Sharpe and Treynor ratio they are

highest for HDFC top 200 followed by contra fund giving the proof of better management

and better performance.

Comparing Beta values indicate that emerging business funds moves exactly with the market

compared to other funds amongst the following. Even in portfolio turnover ratio emerging

business fund is second highest. As it is seen that though SBI schemes are performing very

well but still investors go for schemes offered by other companies because of

1) Less brokerage given to IFAs and NDs,

2) Other companies provide better services comparatively.

3) Bad performance of schemes in the past. Eg. – One India Fund.

4) Even the returns from Magnum Taxgain scheme which has the highest AUM and is one of

the best schemes by SBI was less compared to tax saver schemes of HDFC and Reliance.

5) Complaints like dividend not received or statement not received were frequent.

MBA MARKETING PROJECT REPORT Page | 42

SAAB MARFIN MBA

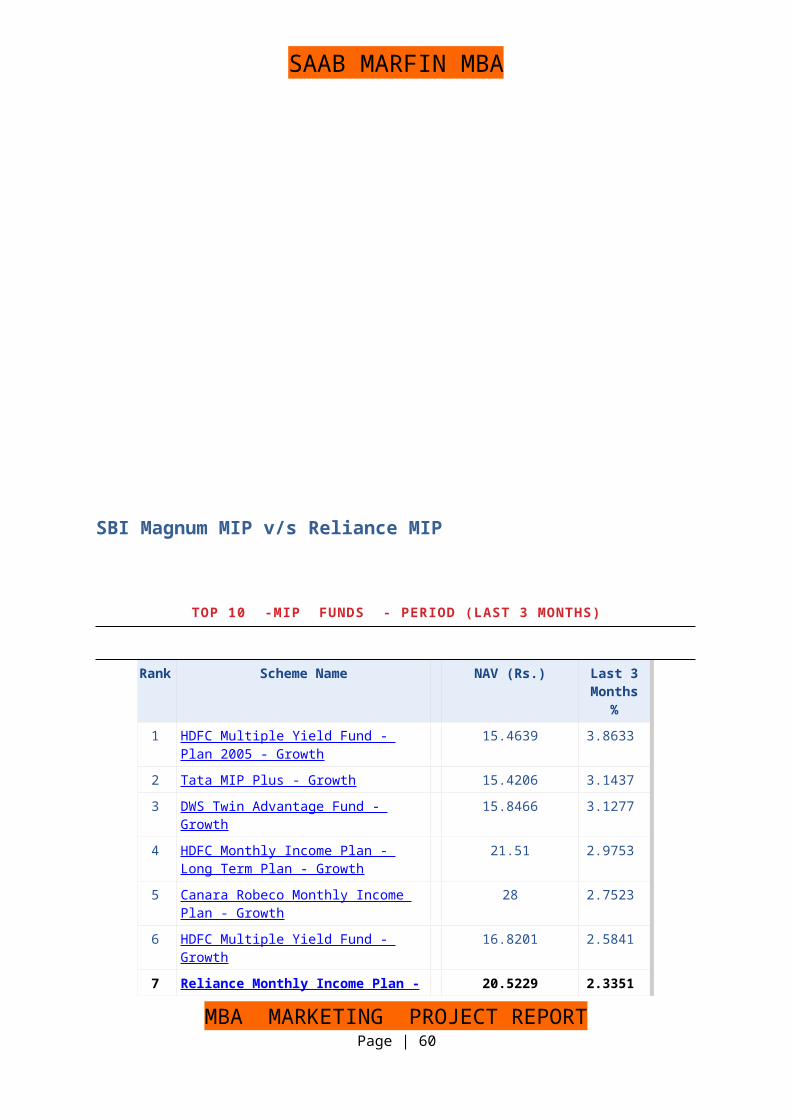

SBI Magnum MIP v/s Reliance MIP

TOP 10 -MIP FUNDS - PERIOD (LAST 3 MONTHS)

Rank Scheme Name NAV (Rs.) Last 3 Months %

1 HDFC Multiple Yield Fund - Plan 2005 - Growth

15.4639 3.8633

2 Tata MIP Plus - Growth 15.4206 3.1437

3 DWS Twin Advantage Fund - Growth 15.8466 3.1277

4 HDFC Monthly Income Plan - Long Term Plan - Growth

21.51 2.9753

5 Canara Robeco Monthly Income Plan - Growth

28 2.7523

6 HDFC Multiple Yield Fund - Growth 16.8201 2.5841

7 Reliance Monthly Income Plan - Growth

20.5229 2.3351

8 LIC MF Floater - Monthly Income Plan - Growth

17.3964 2.244

9 SBI Magnum Monthly Income Plan - Growth

19.3489 2.1821

10 ICICI Prudential Income Multiplier Fund - Cumulative

18.4546 2.1397

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

Source – www.mutualfundsindia.com

From the above ranking it is concluded that SBI magnum MIP has gained good popularity

and performed really well in the last three months.

TOP 15 MIP FUNDS – Period last 6 months

Rank Scheme Name NAV (Rs.) Last 6 Months %

1 HDFC Multiple Yield Fund - Plan 2005 - Growth

15.4639 6.0544

2 HDFC Multiple Yield Fund - Growth 16.8201 5.3007

MBA MARKETING PROJECT REPORT Page | 43

SAAB MARFIN MBA

3 Canara Robeco Monthly Income Plan - Growth

28 4.5947

4 HDFC Monthly Income Plan - Long Term Plan - Growth

21.51 4.1929

5 Tata MIP Plus - Growth 15.4206 4.1229

6 DWS Twin Advantage Fund - Growth 15.8466 3.755

7 LIC MF Floater - Monthly Income Plan - Growth

17.3964 3.4699

8 UTI Monthly Income Scheme - Growth 18.8858 3.4578

9 Reliance Monthly Income Plan - Growth

20.5229 3.4024

10 Baroda Pioneer Monthly Income Fund - Growth

12.5978 3.3208

11 HDFC Monthly Income Plan - Short Term Plan - Growth

16.4407 3.1263

12 ICICI Prudential Income Multiplier Fund - Cumulative

18.4546 3.0839

13 Birla Sun Life Monthly Income - Growth 34.5834 3.0498

14 SBI Magnum Monthly Income Plan - Floater - Growth

12.3998 2.9584

15 SBI Magnum Monthly Income Plan - Growth

19.3489 2.8059

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

Even in last six months SBI Magnum MIP is in top 15

Source – www.mutualfundsindia.com

TOP 10 MIP FUNDS LAST – 12 months

Rank Scheme Name NAV (Rs.) Last 12 Months %

1 HDFC Multiple Yield Fund - Plan 2005 - Growth

15.4639 17.382

MBA MARKETING PROJECT REPORT Page | 44

SAAB MARFIN MBA

2 HDFC Monthly Income Plan - Long Term Plan - Growth

21.51 14.75

3 HDFC Multiple Yield Fund - Growth 16.8201 14.1468

4 Reliance Monthly Income Plan - Growth

20.5229 13.8807

5 HSBC MIP - Savings Plan - Growth 18.4544 10.8725

6 UTI Monthly Income Scheme - Growth 18.8858 10.2988

7 HDFC Monthly Income Plan - Short Term Plan - Growth

16.4407 9.7701

8 Birla Sun Life MIP - Wealth 25 - Growth 16.9589 9.6535

9 Birla Sun Life Monthly Income - Growth 34.5834 9.2534

10 DSP BlackRock Savings Manager Fund - Aggressive - Growth

18.4164 9.0205

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

Top 5 MIP funds in Last 3 years

Rank Scheme Name NAV (Rs.) Last 3 Years %

1 Reliance Monthly Income Plan - Growth

20.5229 14.7699

2 L&T Monthly Income Plan - Growth 18.8877 12.2357

3 HDFC Monthly Income Plan - Long Term Plan - Growth

21.51 12.1536

4 Canara Robeco Monthly Income Plan - Growth

28 12.0961

5 Birla Sun Life MIP - Savings 5 - Growth

16.681 12.0375

*Note:- Returns calculated for less than 1 year are Absolute returns and returns calculated for more than 1 year are compounded annualized.

MBA MARKETING PROJECT REPORT Page | 45

SAAB MARFIN MBA

Source – www.mutualfundsindia.com

From the above data it is clear that Reliance MIP (G) has been performing consistently well

from last three years.

SBI Magnum MIP has been rated 3 star and Reliance MIP has been rated 5 star by

moneycontrol.com.

Comparison of the above two schemes

SBI Magnum MIP (G)

Reliance MIP (G)

FACTS Inception Date 9/4/2001 13/1/2004 Face Value 10 10 Fund Size(in Cr.) 235.06 4771.44

Increase in fund size since 30th april 2010 (in Cr.) 21.19 333.32

Expense ratio 1.73 1.57

portfolio turnover ratio NA 357NAV Latest 19.35 20.52 52-week high 19.39 20.55 52-week low 17.73 17.69returns 1 month -0.01 0.23 3 months 2.18 2.34 6 months 2.81 3.4 1 year 8.39 13.88 3 years 4.72 14.77 5 years 5.9 13.36 Since inception 7.43 11.83Risk Sharpe -0.13 0.21 Beta 0.78 1.15 Treynor -0.19 0.28Portfolio Market cap (in Cr.) 14,800.17 54,140.31 Large 2.56 13.69 Mid 6.36 4.33 Small 4.65 0.16 No. of stocks 25 70 P/e ratio 33.14 22.98Asset allocation Equity 13.56 18.82 Debt 10.88 46.45

Cash and equivalent 75.56 34.74

MBA MARKETING PROJECT REPORT Page | 46

SAAB MARFIN MBA

Sharpe and Treynor ratio of Reliance MIP is greater than that of SBI MIP giving a proof of

better management and better performance. Though last three months returns have been

almost similar but if we look at long run returns from Reliance MIP are far greater than SBI

MIP. Since sales of SBI MIP is low so the fund size is very small comparatively and it is also

increasing at a very low rate. No. of stocks invested in is also very low.

After continuous interaction with investors, IFA’s and ND’s I identified following factors

which might affect customer’s decision while investing in mutual funds. I used these factors

in form of a questionnaire on likert scale to identify the major factors.

MBA MARKETING PROJECT REPORT Page | 47

SAAB MARFIN MBA

MBA MARKETING PROJECT REPORT Page | 48

SAAB MARFIN MBA

QuestionnaireFactors Affecting Customers’ Decision while investing in mutual Fund

Factor Analysis through SPSS

Total Variance Explained

MBA MARKETING PROJECT REPORT Page | 49

S. No.

Question Strongly disagree

Disagree Neutral Agree Strongly Agree

1 Risk 2 Return3 Income of the investor4 Age of the investor5 Brand Name6 Popularity of the scheme7 Plans available for the scheme (eg. SIP, STP, MIP)8 Date of inception of the scheme9 No. of times Dividend declared for a particular scheme

10 Options available in the scheme (eg.- growth, Dividend, Lock in period)