Sberbank in UAE Strategic Plans & Strategic Partners file3Q 2013 Financial Highlights 4 Sberbank is...

18

Sberbank in UAE Strategic Plans & Strategic Partners December 2013

Transcript of Sberbank in UAE Strategic Plans & Strategic Partners file3Q 2013 Financial Highlights 4 Sberbank is...

Sberbank in UAE

Strategic Plans &

Strategic Partners

December 2013

Sberbank‘s Highlights

2

Sberbank Offers

a Compelling

Combination of

Strengths Among

Global Banks

Growth

Positive Russian macroeconomic performance

Leader in the fast growing Russian

banking market

Superior customer franchise and brand

Profitability

Highest ROAA among large global banks

(by market capitalization)

High quality income mix

Healthy core margin trends

Strong development of fee income sources

Resilience

Russia in good position during global volatility

Strong balance sheet, liquidity and capital position with

focus on risk management

Ability to operate in and even take advantage

of difficult market environments

Ongoing transformation and modernization

Building leading technology and infrastructure

Process improvements through Lean Sigma

Success driven by talent

Innovation

Russia’s Most Extensive Distribution Platform

and Customer Franchise

3

18 625

1 583 1 257

24 260

Sberbank Russian Agricultural Bank VTB² All Other Banks

12x

Brand Finance, 2013

# 1 in Russia

#13 across banks globally

Top 100 among all brands

globally

Value of the brand estimated

at $14.16bn

~106 m Retail clients, out of a total

population of ~143 m

>81,500

ATMs and self-service terminals -

one of the largest single bank-

owned networks globally

83% Retail transactions executed via

remote channels3

>1.0 m Corporate lent to clients out of 4.3m

businesses in Russia

~2 bn Transactions processed for

individual clients annually

~4 m Visitors to Sberbank’s outlets daily

>12 m Active mobile banking users

>7 m “Sberbank Online” active users

Source: Rosstat, Sberbank’s operating statistics and calculations on the basis of statistics from CBR as of 30-Jun-2013. Sberbank operating statistics for the respective periods. Notes: (1) Including branches and other outlets (2) Includes VTB24, Transcreditbank and Bank of Moscow (3) Counting only retail transactions that can be executed in person at a branch or remotely (4) Sberbank’s calculation on the basis of CBR data under RAS as of 1-Jul-2013, central banks data, latest available company data. Market share of debit & credit cards as of 1-Jan-2013.

Largest Branch Network Among Russian Banks1 Notable Facts as of June-2013

Sberbank: Russia’s Most Storied Iconic Brand

Sberbank’s Share of the Russian Banking

Sector4

45%

28% 28% 32% 32%

43%

Reta

il d

eposits

Assets

Capital

Corp

ora

te lo

ans

Reta

il lo

ans

Debit a

nd c

redit

card

s

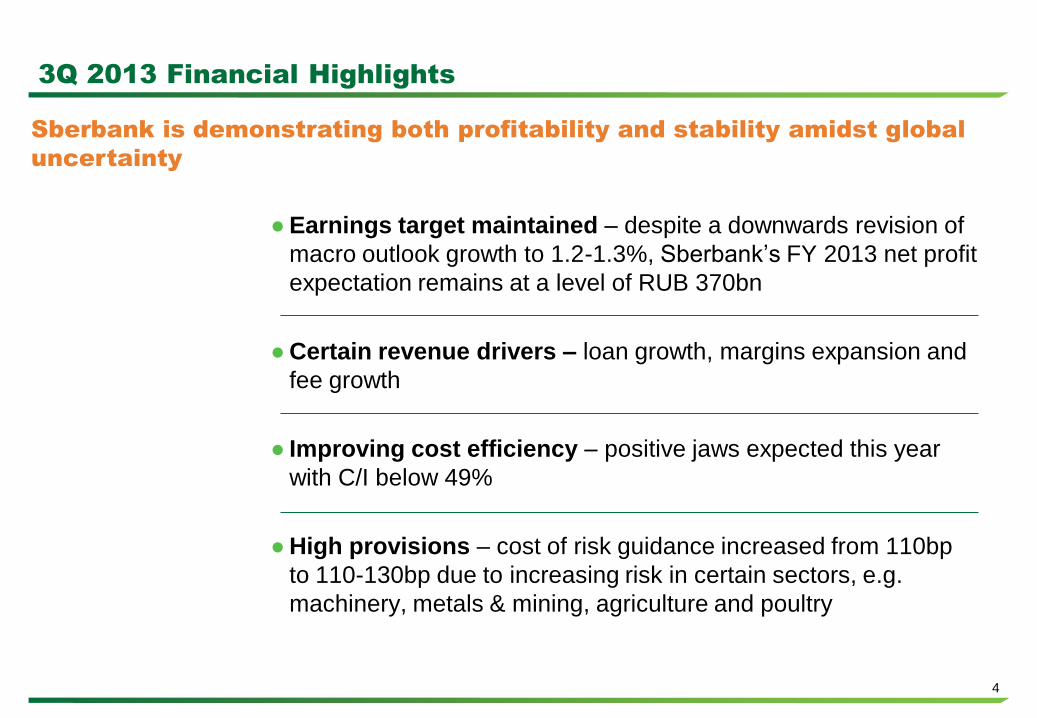

3Q 2013 Financial Highlights

4

Sberbank is demonstrating both profitability and stability amidst global

uncertainty

● Earnings target maintained – despite a downwards revision of

macro outlook growth to 1.2-1.3%, Sberbank’s FY 2013 net profit

expectation remains at a level of RUB 370bn

● Certain revenue drivers – loan growth, margins expansion and

fee growth

● Improving cost efficiency – positive jaws expected this year

with C/I below 49%

● High provisions – cost of risk guidance increased from 110bp

to 110-130bp due to increasing risk in certain sectors, e.g.

machinery, metals & mining, agriculture and poultry

5 Main Strategy Themes

5

Mature Organization: We will build organizational and

management skills and establish processes matching the

international scale of Sberbank Group and our new ambitions

Team and Culture: We strive to make our people and corporate

culture one of our key competitive advantages

With the customer for life: We will build enduring relationships

of trust with our clients and will become a useful, sometimes invisible,

but integral part of their lives. We strive to go beyond expectations of

our clients

Technological Breakthrough: We will complete technical

modernization of the Bank and will integrate cutting-edge technology

and innovation into our business

Financial Excellence: We will improve our financial performance

by effective management of costs and risk/return ratio

On 14 November we presented our 2014 – 2018 strategy for the

Group

Strategic Financial Highlights

ROE

18-20% ÷

Net profit

2x

2018E 2013E

~ 370 bln

Equity

2x +

2018E 2013E

~ 1.8-1.9 trln

2018E 2013E

2018E 2013E

~ 5.8-5.9%

> 4.5%

NIM

Assets

growth

2x +

2018E 2013E

Positive jaws

2018E 2013E

2018E 2013E

2018E 2013E

+75%

2.5x +

~ 110bp

120-140bp

NII

F&C

CoR

OpEx

We set ambitious financial

targets for 2018

6

Belarus

Broad Geographical Coverage through Acquisitions

7

Kazakhstan

SB JSC Sberbank ● 100.0% stake ● 1.1% of Group’s assets ● #5 by assets ● 6.1% market share by assets

Ukraine Sberbank of Russia JSC - to be merged with VBI Ukraine

● 100.0% stake ● 0.8% of Group’s assets ● #8 by assets ● 2.7% market share by assets

Source: Sberbank’s unaudited quarterly IFRS financial statements for 1H2013, Sberbank’s operational data as of 1-Jul-2013, Sberbank’s and subsidiaries’ ranks and market shares based on the

respective central banks’ data

Central & Eastern Europe

Sberbank Europe (Former “VBI”) ● 100.0% stake ● 2.7% of Group’s assets

● Headquartered in Austria; 280 branches

in 8 countries: Croatia, Czech Republic,

Slovakia, Bosnia-Herzegovina, Hungary,

Slovenia, Serbia and Ukraine

● Sberbank has unparalleled geographical footprint in Russia, which

remains its key focus and accounts for 88% of the Group’s assets

JSC BPS-Sberbank

● 97.9% stake

● 0.8% of Group’s assets

● #3 by assets ● 9.7% market share by assets

Turkey

Representative offices: ● Germany ● China

Trading platforms: ● London ● New York

Branch: ● India

Wholly-owned subsidiary: ● Sberbank (Switzerland) AG

DenizBank AS

● 99.85% stake ● 6.9% of Group’s assets

● Headquartered in Turkey

● ca. 623 branches; 3,357 ATMs;

126,863 POS terminals

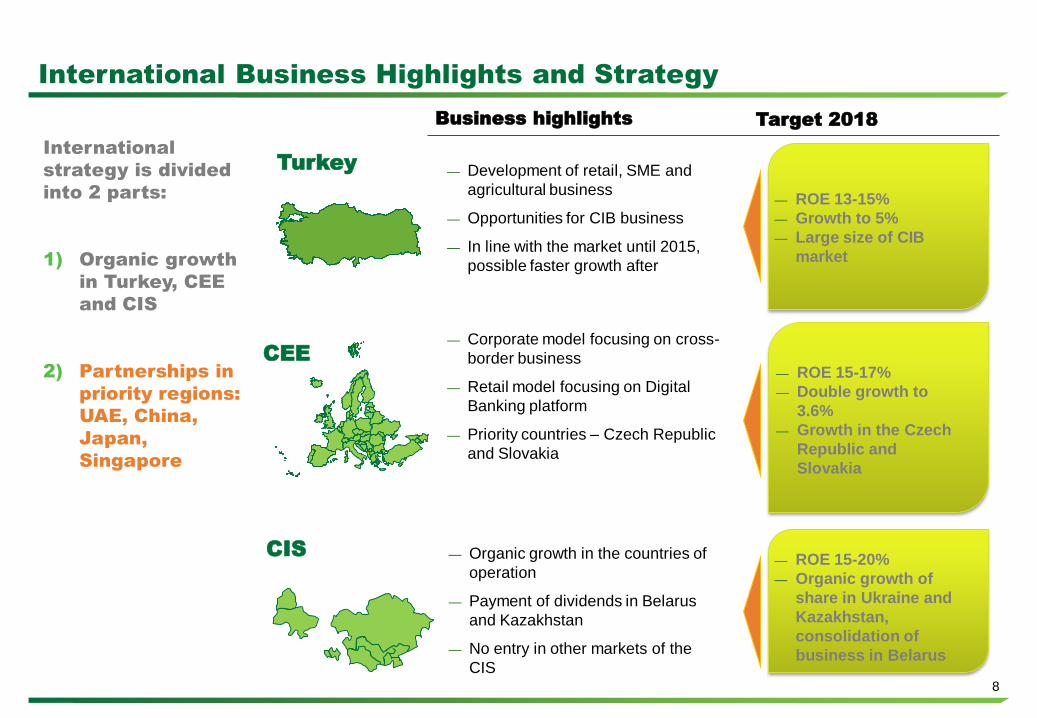

International Business Highlights and Strategy

8

— Corporate model focusing on cross-

border business

— Retail model focusing on Digital

Banking platform

— Priority countries – Czech Republic

and Slovakia

— Development of retail, SME and

agricultural business

— Opportunities for CIB business

— In line with the market until 2015,

possible faster growth after

— Organic growth in the countries of

operation

— Payment of dividends in Belarus

and Kazakhstan

— No entry in other markets of the

CIS

Business highlights Target 2018

CEE

Turkey

CIS

— ROE 13-15%

— Growth to 5%

— Large size of CIB

market

— ROE 15-17%

— Double growth to

3.6%

— Growth in the Czech

Republic and

Slovakia

— ROE 15-20%

— Organic growth of

share in Ukraine and

Kazakhstan,

consolidation of

business in Belarus

International

strategy is divided

into 2 parts:

1) Organic growth

in Turkey, CEE

and CIS

2) Partnerships in

priority regions:

UAE, China,

Japan,

Singapore

Middle East – Russia

Middle East is one of the most important financial markets in the

world

9

● Leaders of Russia UAE met and agreed on

strategic investment partnership

● Double tax treaty signed

● Leading UAE funds (ADIA, Mubadala) plan to

invest in Russian economy

Middle East is of strategic importance for Sberbank as

systemic institution in Russia and an emerging global player

I am a leader

We are a team

All for the client

Sberbank’s interests in Middle East

10

Our strategy in Middle East is based on our clients’ main interests:

● Financing of business activities in the region

● Guarantees

● Business projects consultations

… and Sberbank’s interests:

● Diversify funding base away from US and Europe:

− Instruments: syndications, Eurobobnds, ECP

● Trade Finance: passive operations to service client

trade flows and active operations in risk taking

● Global Markets: FX, Credit trading, Commodities,

Money market

● Asset management

Our aspirations should be supported by a natural choice to establish a

permanent local office

Examples of successful partnerships

11

● Signed Memoranda of Understanding:

Invest AD, Emirates NBD, NBAD

● Invest AD has long history in Russia:

− Partnering with Sberbank for Olympics project

− Currently significant IB deals pipeline in telecoms, aviation etc.

● First club transaction in Middle East (led by ENBD and NBAD) –

USD 600m club syndicated loan to support Sberbank clients’ trade

flows

● 26 meetings with MENA financial institutions during SIBOS

conference in Dubai (September 2013)

We strive to develop partnerships in Middle East to service clients’

needs

A lot is done, but more is ahead – our clients actively seek to enter the

market and we will not let them down

Invest AD Memorandum of Understanding – Moscow, Dec. 2012

12

Emirates NBD Memorandum of Understanding – St.-Petersburg

June 2013

13

NBAD Memorandum of Understanding – Moscow, June 2013

14

Sberbank, Invest AD and Sukhoi: Letter of Intention –

Dubai Airshow 2013

15

Contact Details

16

Global Head of Financial Institutions:

Alexander Dementiev

Head of International Financial

Institutions MENA and Asia:

Maxim Osintsev

Address: 4, Romanov pereulok

Moscow, 125009

Russia

Phone: +7 (495) 258-05-00

Email: [email protected]

www.sberbank.ru/en

www.sberbank.ru

Financial Institutions Contacts

17

Thank You

Q&A

Disclaimer

18

This presentation has been prepared by Sberbank of Russia (the “Bank”) and has not been independently verified. This presentation does not constitute or form part or all of, and should not be construed

as, any offer of, or any invitation to sell or issue, or any solicitation of any offer to purchase, subscribe for, underwrite or otherwise acquire, or a recommendation regarding, any shares or other securities

representing shares in, or any other securities of the Bank, or any member of the Bank’s group, nor shall it or any part of it nor the fact of its presentation or distribution form the basis of, or be relied on in

connection with, any contract or any commitment whatsoever or any investment decision. The information in this presentation is confidential and is being provided to you solely for your information and

may not be reproduced, retransmitted or further distributed to any other person or published, in whole or in part, for any purpose.

This presentation is only being distributed to and is only directed at (A) persons in member states of the European Economic Area (other than the United Kingdom) who are “qualified investors” within the

meaning of Article 2(1)(e) of Directive 2003/71/EC (as amended and together with any applicable implementing measures in that member state, the “Prospectus Directive”) (“Qualified Investors”); (B) in

the United Kingdom, Qualified Investors who are investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) and/or

high net worth companies, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order; and (C) such other persons as to whom this presentation may be

lawfully distributed and directed under applicable laws (all such persons in (A) to (C) above together being referred to as “relevant persons”). The shares, or other securities representing shares, are only

available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such securities will be engaged in only with, relevant persons. Any person who is not a relevant person

should not act or rely on this presentation or any of its contents.

The information in this presentation or in oral statements of the management of the Bank may include forward-looking statements. Forward-looking statements include all matters that are not historical

facts, statements regarding the Bank’s intentions, beliefs or current expectations concerning, among other things, the Bank’s results of operations, financial condition, liquidity, prospects, growth, targets,

strategies, and the industry in which the Bank operates. By their nature, forward-looking statements involve risks and uncertainties, because they relate to events and depend on circumstances that may

or may not occur in the future. The Bank cautions you that forward-looking statements are not guarantees of future performance and that its actual results of operations, financial condition and liquidity

and the development of the industry in which the Bank operates may differ materially from those made in or suggested by the forward looking statements contained in this presentation or in oral

statements of the management of the Bank. In addition, even if the Bank’s results of operations, financial condition and liquidity and the development of the industry in which the Bank operates are

consistent with forward-looking statements contained in this presentation or made in oral statements, those results or developments may not be indicative of results or developments in future periods.

The information and opinions contained in this presentation or in oral statements of the management of the Bank are provided as at the date of this presentation or as at the other date if indicated and are

subject to change without notice.

No reliance may be placed for any purpose whatsoever on the information contained in this presentation or oral statements of the management of the Bank or on assumptions made as to its

completeness.

No representation or warranty, express or implied, is given by the Bank, its subsidiaries or any of their respective advisers, officers, employees or agents, as to the accuracy of the information or opinions

or for any loss howsoever arising, directly or indirectly, from any use of this presentation or its contents.

This presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such

distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction.

You must return any copies of this presentation and any other hand-outs before leaving the presentation.

By attending or reviewing this presentation, you acknowledge and agree to be bound by the foregoing.